The US Might Change the Rules — Again

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

The Trump Trade Round-up

How do we get all the copper we need?

The Trump Trade Round-up

Are you tired of hearing us talk, non-stop, about Trump’s trade policy?

Yeahhh… we get it. We’re getting tired of it too. The White House has been a firehose of chaos over the last few months. If you, like us, care about how much your country trades with America, and are trying to watch the American president for signals, the exercise is more likely to overwhelm than to enlighten you. And with the sheer number of policy flip-flops we’re seeing, anything you do learn, more likely than not, could be reversed in just a few weeks.

And yet, we can’t not look at it either. For now, America remains our largest trade partner, and world’s biggest market, besides. And every little movement Trump makes signals the opening — or close — of a billion dollar market opportunity.

So here’s a little experiment we’re going to try. Every once in a while, we’ll drop a single, rapid-fire round-up of all the recent news on American trade policy. If this works for you, let us know in the comments!

Trade truce?

We’ve spent the last many months crying hoarse about how damaging Trump’s worldwide trade war was to the global economy.

But suddenly, it looks like that trade war is over — or at the very least, there’s now a ceasefire in place.

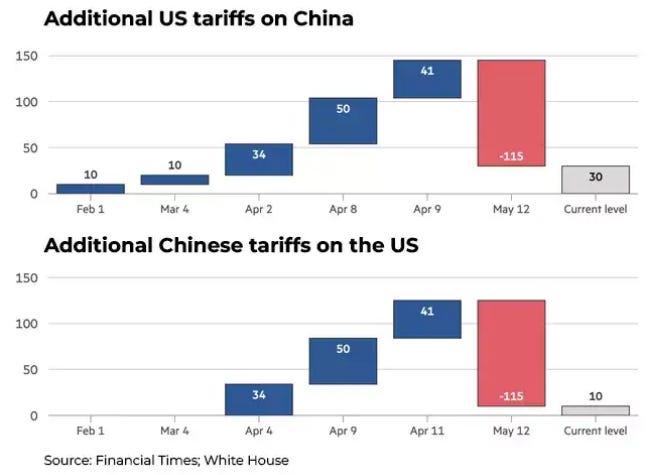

Back in April, a few days after announcing his (anything but) “reciprocal tariffs” on most countries in the world — India included — Trump paused them for 90 days, supposedly to open room for negotiation. China, though, had not been spared. In fact, the two countries went on a tit-for-tat spiral of escalating tariffs, until both had triple-digit tariffs on each other’s products.

But there now seems to be a detente in the works. On May 12, in a joint statement, both sides committed to a 90-day pause. At least for these three months, American tariffs on China have dropped to 30%, from 145% – while Chinese tariffs on America have fallen to 10%, from 120%. China’s also pulling all the other punches it landed on America — its “non-tariff countermeasures” — like its ban on key exports, and investigations on American companies. The two sides plan to use the three-month breather to thrash out some sort of longer-term arrangement.

Both countries claimed victory in their short-lived trade war. But commentators seem to think China came out with the upper hand. China absorbed the tariff shock, huddled down, and stimulated its economy — even as trade between the two countries broke down entirely. This pushed Trump to back down. In our view, though, both sides are probably relieved by the thaw.

American markets, at least, responded with a dramatic sigh of relief.

Now, we don’t want to oversell this. This isn’t an end to the uncertainty, either for China, or for anyone else. At least for now, all those tariffs are still in place — they’re just in a 90-day limbo. Nor is this a roll-back to how things were before April 2. The baseline of 10% survives, and by all indications, will be the “new normal” for American trade policy.

But this does point to an end to the madness. Calmer heads seem to have prevailed, at least at the moment.

Dash for deals

Before the 90-day clock runs out, we’re seeing a dash for deals from countries all over the world.

The United Kingdom was the first to secure a trade deal with the United States. The deal is, however, fairly narrow. The United States isn’t backing down on its 10% baseline tariff rate. However, there are a few concessions it has made — it has allowed a quota of 100,000 British cars to enter America with a 10% tariff rate, a move that has made Tata-owned JLR quite happy. In return, the United Kingdom has offered some tariff concessions of its own.

Many others — everyone from Japan to Brazil — are trying something similar before the 90-day pause ends.

India is at the front of the line. We’re pursuing some sort of tariff relaxation with considerable zeal. In exchange for an exemption from American tariffs, India seems to have offered serious tariff concessions of its own. We’re offering to cut tariffs on American products to under 4% — from the current 13%. Of these, we’ve reportedly offered to slash tariffs down to zero for 60% of all products. We’re also willing to offer “preferential access” for 90% of what we import from America, which means we’ll treat those goods better than we treat goods coming in from anywhere else — not only in terms of the tariffs we place, but the paperwork and clearances they require.

In return, we’re looking for an exemption from all tariff hikes — both, those currently in place, and any that might be coming our way in the future. We’re also hoping that the United States considers us a “trusted” location for American technology, helping us get around restrictions on everything from biotech to AI.

The consequences could be enormous. If we get terms that our competitors, like Vietnam or Bangladesh, do not, that could be a once-in-a-generation shot-in-the-arm for all our “Make In India” ambitions.

India has also signalled that it’s willing to play ‘bad cop,’ if things don’t go our way. While pursuing trade talks, we have also notified the WTO that we’re considering new tariffs on American exports, in retaliation for its steel and aluminium tariffs. We haven’t indicated the products that we’ll place these tariffs on, but it shows some willingness to punish the United States in case talks break down.

One thing that’s not on the table, from the looks of it, is the baseline 10% tariff. Treasury Secretary Scott Bessent told Japanese negotiators as much — pointing out that the additional, country-specific levy is the only thing Trump’s willing to consider. That’s what India should perhaps expect too.

Trump undoes Biden’s chip controls

We’ve spoken, before, about how Joe Biden — in one of his last moves as President — implemented an “AI diffusion framework”, which looked to us like some sort of world-wide chip License Raj. From May 15 onwards, this new framework would had carved the world into three “tiers”: and placed major restrictions on the number of AI chips that most of the world could import. Only America and 17 other countries would be given free access to America’s cutting edge chips under this regime. Everyone else — India included — would have to jump through regulatory hoops to get their hands on any.

Well, there’s some good news there. That whole framework may soon be scrapped.

Trump’s commerce department sees the framework as something “overly complex, overly bureaucratic” — and even considers it “unenforceable”. In fact, from the looks of it, those export controls were getting in the way of America’s own ability to strike deals with countries like UAE and Saudi Arabia. Those deals are hugely important to the United States; they help it secure access to critical minerals like Lithium and rare earths, in a time where China is trying to stop the United States from getting their hands on any.

There’s another reason Trump may have shifted gears on AI chip policy: by cutting the world off American chips, the United States unintentionally ceded most of the world’s chip market to China. Over the last few years, China’s Huawei appears to have nearly closed the gap with Nvidia. Its Ascend 910 series of chips, while not nearly at par with Nvidia, seem good enough for AI use. According to some rumours, for instance, China’s DeepSeek is relying exclusively on these chips to develop its next major AI model. If America forcibly cut its companies off from world markets, it would have handed Huawei the entire global market on a platter.

Officials from America’s Bureau of Industry and Security (BIS) have now been asked to stop enforcing the framework. As per a recent statement, the BIS will soon rescind the framework formally, and replace it with something simpler. The announcement instantly sent Nvidia’s stock soaring.

That said, we don’t yet know what comes in place of Biden’s diffusion framework. Does it actually make life easier for India? We aren’t sure. Reuters reports that the United States might consider negotiating bilateral chip supply arrangements, going country-by-country. That, to us, seems very much in Trump’s wheelhouse.

Meanwhile, America seems to have pivoted to attacking Huawei’s chips. The BIS, in a new guidance, claims that China — and Huawei more specifically — most probably makes chips using American software and technology, violating its chip controls. Anyone using these chips anywhere in the world, it threatens, could be hit by all kinds of criminal and administrative penalties.

How does America plan to stop people from doing so outside its borders? We aren’t sure. Here’s a clue, though: American companies have been asked to perform due diligence on their customers, and keep an eye out for anyone that might use Chinese chips.

A long-tail of trade policy randomness

This edition feels rather optimistic so far. And compared to how hard we were panicking a month ago, at least, things do seem better. But don’t confuse that for stability. There’s a long tail of random trade policy risks that is still coming out of America. Here are just a few:

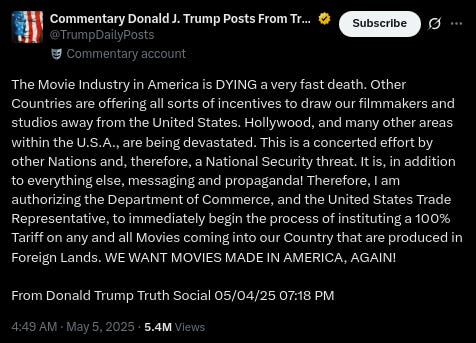

Tariffs on movies: In a recent Truth Social post, Trump announced a 100% tariff on all movies made “in foreign lands” — claiming that they were a national security risk. It isn’t quite clear how these will be imposed, or whether they will be imposed at all — after all, films aren’t imported in cargo ships, like goods are, making it much harder to tariff them when they land in America. People across the world seem confused.

Cheaper medicine for Americans: Trump introduced a new “most-favoured-nation” rule — forcing pharma companies to sell drugs in the United States at the lowest prices they charge in any OECD market. Only, it isn’t clear how this will be implemented, or whether the American president has any authority to announce such a measure at all. This could push up the competitive advantage of India’s generic drug manufacturers, given that we’re one of the world’s cheapest sources of medicine. But the US Trade Representative has also just put India on its “priority watch list” for failing to protect the patents of pharma companies, which could complicate things.

Trump doesn’t like Make in India: Out of nowhere, Trump apparently told Tim Cook that Apple shouldn’t make iPhones in India. Don’t even ask.

How do we get all the copper we need?

We've discussed this before, but it bears repeating: copper — as the best possible metal for making electrical wires (if you don’t want to go bankrupt) — is already the metal powering our modern world. And we haven’t seen anything yet.

If we’re banking on a realistic green transition, we’ll need lots and lots of copper — at a scale we’ve never seen. For example, EVs require far more copper than internal-combustion cars: a typical battery-electric vehicle contains around 80–100 kg of copper, compared to ~23 kg in a regular car. Likewise, if we’re drawing electricity from faraway renewable power projects — like solar power from desolate parts of the Thar desert, or offshore wind power from the middle of the ocean — we’ll need hundreds of kilometers of additional wire.

Where does all that copper come from?

The UN Trade and Development folks (UNCTAD) just dropped their May 2025 Global Trade Update? And this one’s all about copper.

Let’s dive in.

The Gap Between Supply and Demand

There are two sides to the copper story: demand and supply.

First, let’s look at demand.

We’re living in a time of accelerated copper demand. How much more demand, we don’t quite know. UNCTAD says copper demand will grow by over 40% by 2040. IEA predicts a 50% demand increase by 2040. Goldman Sachs analysts warn that a "net-zero" pathway requires 54% more copper by 2030.

Take your pick. We don’t know who’s right, but one thing is clear: we need more copper than we’re producing.

This is a hard problem, and one we cannot escape. Even if we never end up using EVs and green technology, we will still need copper. We’ll need it for electrical grids, and for wiring our homes and buildings, and running our devices. Unless we eventually find an alternative to electricity, the demand will always exist.

The problem is that supply just isn't keeping pace.

The world’s refined copper production added up to about 26.6 million metric tons in 2023. According to UNCTAD, if we want to avoid a copper shortage, we’ll need roughly 80 new copper mines and $250 billion of investment by 2030.

That’s harder than it looks. As we’ve mentioned before, it takes ~17 years to open a new copper mine. It seems hard to compress that timeline. If anything, the UNCTAD reports that development timelines are beginning to stretch to as much as 25 years. Think about that — a mine started today might not produce copper until 2050. These are generational investments.

Worse still, you can’t project demand two-and-a-half decades away.

This long time frame for opening new mines means that we cannot quickly adjust to sudden demand surges or supply shocks. If demand spikes, for instance, we have to fall back on old, shuttered mines, which are degrading in quality.

On top of this, mining operations often run into controversy. Opening new mines is a messy process, with huge environmental and social implications. Copper mining is water and energy-intensive, causes severe pollution, and mining projects often interfere with those whose land they’re built on. For example, over half of the world’s copper mines are in water-stressed regions and have reported water access problems.

This push and pull between demand and supply directly impacts prices — making them swing dramatically. Prices build up as demand increases — with sudden spokes around supply bottlenecks, strikes etc.. But whenever new supply comes online, prices tend to crash suddenly.

The value chain of copper

With the basics out of the way, let’s get to the juicy part of the report: on how the copper supply chain works. Understanding this helps you pick up a lot of the nuances around the business.

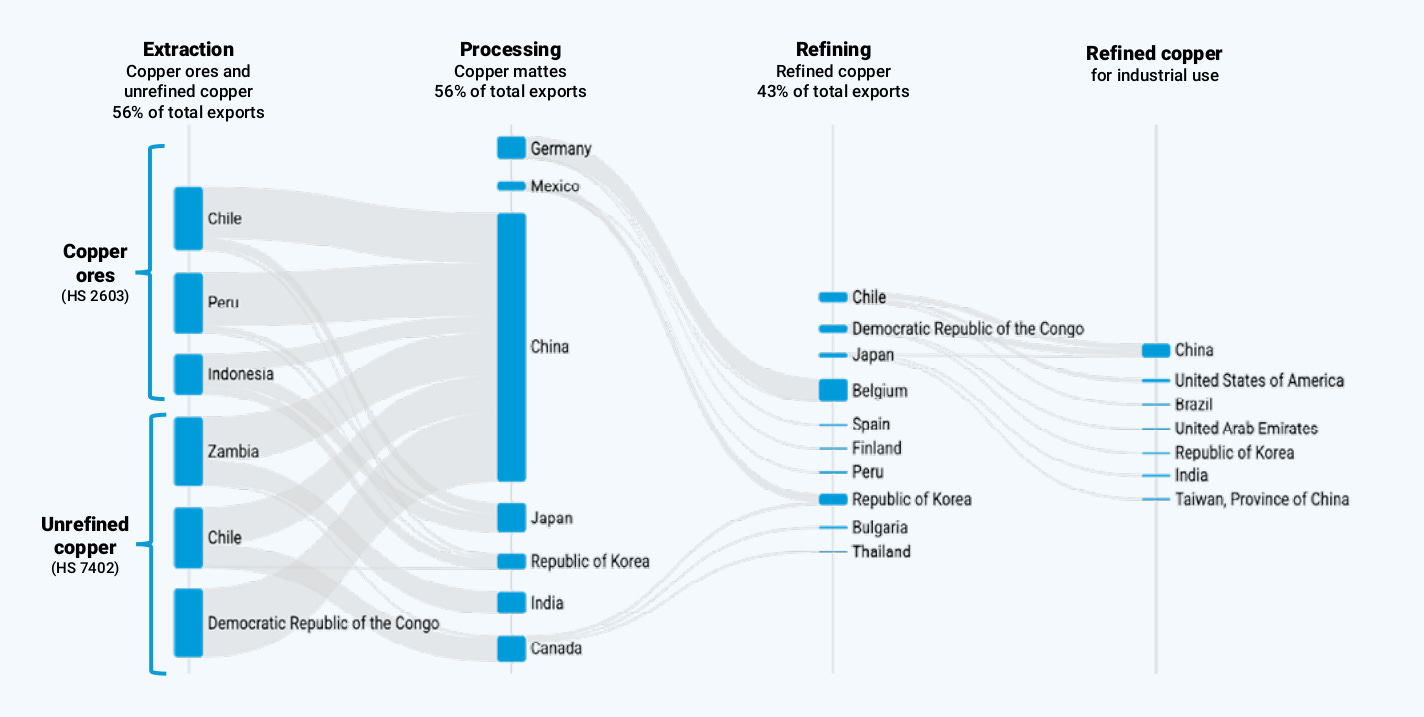

Extraction

Over half of the world’s known copper reserves are located in just five countries. One-fifth of global supply comes from Chile alone, in fact. Australia and Peru contribute 10% each, followed by the Democratic Republic of the Congo and Russia, with 8% each.

This concentration can create tricky business dynamics. It increases the risk that suppliers might try to manipulate prices, or that supplies break down during political conflicts, or that copper mining becomes subject to geopolitical concentration.

Countries like China, for instance, have already secured preferential access deals with major suppliers. Other countries, meanwhile, are left scrambling for this critical resource. This is quite like the OPEC’s hold over oil — whoever controls production controls prices.

Processing

Once mined, copper ore is ‘smelted’ into intermediate products. Surprisingly, Germany is actually the world’s top exporter of copper mattes. Zambia and the DRC are other major exporters of these intermediate products.

Refining

The market for refining copper has shifted wildly in the last few decades. In 1990, Asia produced less than one-fifth of the world's refined copper. Europe was dominant, at 32%, as were the Americas, at 39%.

But this equation was upended by the entry of the industrial juggernaut, China, who quickly turned itself into the gateway for global copper. Fast forward to 2023, and Asia now produces 60% of global refined copper. Europe has dropped to 14%; the Americas to 15%. China now imports 60% of the world’s copper ore — up from 17% just two decades ago. It produces more than 45% of the world's refined copper.

Fabrication

Refined copper is turned into ‘semi-finished’ goods: sheets, wires, tubes, and other such products. Most of it is destined to become wire, of course. Copper wire alone accounts for 63% of ‘first use’. This is where the bulk of actual economic value is created in the copper supply chain. China, Germany, Japan and the United States are the world’s main exporters in value-added copper, with Germany leading global exports of copper wire.

Recycling

That’s it for the standard copper value chain. But increasingly, we’re adding in another step.

As primary production struggles to keep up, recycling is becoming increasingly important in the copper life-cycle. For example, in 2023, secondary refined copper — or copper produced from recycled materials — made up 4.5 million tonnes. That’s nearly 20% of the world’ copper output. The United States is the world's top exporter of copper scraps and waste, followed by Germany and Japan.

Copper, in fact, is one of the most heavily recycled metals. It just makes sense. Recycling is cheaper than mining, lowers emissions significantly, and performs just as well as newly mined copper. Plus, it doesn't require opening new mines in ecologically sensitive areas.

But if recycling works so well, here’s the big question: can recycled copper help us get over our problem of growing demand? Unlikely. Recycled copper, at full scale, could satisfy about three-quarters of our projected needs, which is great.

But one-quarter still remains — which is still millions of tonnes. And that’s assuming demand doesn’t go up further.

Now, here’s something worth noticing: as you go up the value chain, none of the major raw copper producers remain. In fact, most copper ore exporters fall below the global average in economic complexity. They're stuck selling the raw material — at great political and environmental risk. That’s a high-risk, low-margin, ‘commoditised’ business.

The real value is captured by other, richer countries.

So, why don't copper-rich countries just move up the value chain, if that’s where the money is? Many reasons, perhaps — but UNCTAD identifies one major structural barrier that's keeping them down: tariffs. Surprise, surprise!

Refined copper typically faces tariffs below 2%. For finished products like wires, tubes, and pipes, though, duties rise sharply – even to around 8%. Essentially, the higher you climb up the value chain, the more exports get discouraged. And so, if you want a thriving industry for finished copper products, you probably need a large enough market to absorb a good deal of your produce.

If anything, this problem is getting worse — we’re seeing countries move further towards nationalism for critical resources.

Where does India lie?

India’s copper consumption has grown significantly in less than a decade, rising from approximately ~5 lakh tonnes in FY 2017 to ~8.5 lakh tonnes in FY 2024 — a 70% increase.

We’re trying to cut this giant copper import bill. We are the world’s second largest importer of refined copper — and that’s not great for our balance of payments. Moreover, we’ve spoken before about “weaponised interdependence” before — where countries try to use their dominance in an economic chain as leverage. Copper is ripe for something similar. Which is why the government is trying to wean us off imports. It recently imposed quality control measures to curb our imports and promote domestic production.

But can we really be self-sufficient? As of now, in every stage of the copper supply chain, India is a relatively small player.

Mining

India has minimal domestic copper mining, with Hindustan Copper Ltd as the sole producer. Annual output is just 25,200 tonnes of copper in concentrate — a tiny 0.1% of global production. Even with HCL's plans to expand ore capacity, India will remain a minor player in mining.

Why so? Does India not have more copper? We do — an estimated 1.66 billion tonnes of copper ore of resources, in fact. But less than 10% of these resources are classified as ‘reserves’ — or something economically attractive enough that companies can actually afford to dig up and sell profitably.

Also, Indian copper ore grades are low. Which is just a fancy way of saying that the rocks mined in India contain very little copper (about 1% copper content). So even though India mines millions of tons of ore, it produces very little actual copper metal from this mining.

Smelting and Refining

India has some presence in refining imported copper concentrate. Major players include Hindalco's Birla Copper, Vedanta's Silvassa refinery, and Adani's new Kutch Copper smelter. But India's share of global refined copper output, despite having grown over the last half decade, remains small — far below China's 40%.

The good news is that more capacity is coming online. Adani’s Kutch Copper is ramping up its smelting capacity. And by some estimates, once it’s completely functional, India could eliminate its copper import dependence. Keyword being could.

Fabrication

India consumes most of its refined copper domestically — in wires, cables, tubes, rods and cookware. Our abilities are skewed — we produce more simple products like rods, wires and foil domestically, but the more complex stuff is mostly imported. In 2023, India exported $891 million of copper wire. That said, we also imported $793 million of copper tubes and pipes.

Recycling

While India generates significant copper scrap, formal recycling remains underdeveloped. We have only 35 formal units. Most of our recycling happens — like for so many other products — happens in the informal sector.

Will we have enough copper?

Let’s get back to our original question: if our copper demand is ramping up, but we don’t know where the supply will come from, how do we close that gap? Are we screwed?

No, not really.

History shows that whenever we think we have too little supply of some commodity, more always comes up.

Just look at oil. In 1919, for instance, the US Geological Survey warned American oil reserves would be exhausted in "nine years and three months." But soon, new discoveries in Texas and Oklahoma quickly turned this predicted shortage into a surplus. Similarly, the 1970s oil crisis prompted dire "peak oil" forecasts. Only, technological innovations in extraction and exploration unlocked new reserves previously considered inaccessible. The 2000s saw another round of “peak oil” predictions when prices soared above $140 per barrel. But from what we can tell, we still have enough oil to get us through a few more decades.

We’ve repeated this cycle many times. The truth is, demand seems to pull in its own supply.

And this is just the supply side of things. Demand could always slow, especially if we crack an alternative.

In fact, several alternatives to copper already exist, even if they are not perfect. Aluminum, for instance, already serves as a substitute in power transmission lines and some automotive wiring due to its lighter weight and lower cost. Fiber optics have already replaced copper in telecommunications. Emerging carbon-based materials like graphene and carbon nanotubes offer promising lightweight options. They aren't commercially viable for large-scale use just yet, but they could be soon enough.

Bottom Line

Copper isn't just any other metal. Only time will tell if we can dig it out fast enough to mean anything on a global scale. In fact, UCTAD concluded the report better than we can, with a warning: "The age of copper is here, but without smart, coordinated trade and industrial strategies, many developing countries risk being left behind."

Tidbits

Edible Oil Stocks Dip to 5-Year Low as Palm Oil Imports Fall Sharply

Source: Business Standard

India’s edible oil stocks at ports and in pipelines fell to 1.35 million tonnes as of May 1, 2025 — the lowest level in five years, according to the Solvent Extractors Association of India (SEA). This decline was primarily driven by a sharp 24.29% drop in palm oil imports in April, which fell to 321,446 tonnes — the lowest in four years. While domestic supplies remain stable due to active mustard seed crushing, the falling port inventories coincide with elevated edible oil inflation, which surged to 17.4% in April as measured by the Consumer Price Index. The landed cost of crude palm oil at Mumbai ports stands at around $1,100 per tonne, higher than the sub-$1,000 levels seen last year. SEA noted that monthly imports of 60,000–70,000 tonnes from Nepal also affect port-level stock tracking. Additionally, weak demand for oil meals from the livestock sector is limiting the ability of millers to reduce retail prices, increasing pressure on edible oil margins.

Mahindra Overtakes Hyundai as India’s Auto Sales Rise 4% in April

Source: Reuters

India’s domestic car sales to dealers rose nearly 4% in April 2025, reaching 3,48,847 units compared to 3,35,629 units in the same month last year, according to the Society of Indian Automobile Manufacturers (SIAM). The growth was driven primarily by strong demand for sport utility vehicles (SUVs), a segment that continues to gain traction among Indian consumers. Mahindra & Mahindra posted a sharp 28% increase in sales, enabling it to surpass Hyundai India and secure the No.2 position in overall sales. The reshuffling of ranks among automakers signals intensifying competition in the world’s third-largest car market.

India Approves ₹37.06 Bn Semiconductor Fab by HCL-Foxconn Near Jewar Airport

Source: Reuters

India’s Union Cabinet has approved a ₹3.7 thousand crore ($435 million) semiconductor manufacturing plant by HCL Group and Taiwan’s Foxconn, to be located near Jewar airport in Uttar Pradesh. The plant will have a monthly capacity of 20,000 wafers and is expected to produce up to 36 million display driver chips annually. This marks the sixth facility approved under the India Semiconductor Mission. Commercial production is scheduled to begin in 2027. The announcement follows earlier setbacks in India’s chip ambitions, including the collapse of Foxconn’s $19.5 billion JV with Vedanta and the pause of Adani Group’s $10 billion talks with Tower Semiconductor. Other projects underway include Tata Group’s $11 billion chip facility and Micron’s $2.7 billion packaging plant.

- This edition of the newsletter was written by Pranav and Prerana.

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Good article....