Why is Vedanta investing $2 billion in Saudi Arabia?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Vedanta’s Saudi copper bet

Big reforms will change the Indian insurance industry

Vedanta’s Saudi Copper Bet

Vedanta Limited, one of India’s biggest mining and metals companies, has announced a $2 billion investment in Saudi Arabia. The plan? They’re setting up three key facilities:

First is a huge copper smelter that transforms raw copper ore into refined metal.

Second, a refinery to remove impurities and produce high-quality copper ready for industrial use. Third, a copper rod plant which is used to convert that refined copper into rods, which can then be used to make cables and other products.

Together, the smelter and refinery will produce 400 kilotonnes of copper every year, while the rod plant will have a capacity of 300 kilotonnes annually. To put this into perspective, India’s total copper demand is currently about 1,500 kilotonnes a year.

This isn’t just another expansion—it’s Vedanta making a bold move to reclaim its spot in the global copper market. But why Saudi Arabia? And why now?

To answer that, we’ll need to take a closer look at Vedanta’s rocky past, the growing demand for copper, and Saudi Arabia’s ambitious plans to transform its economy.

Vedanta is a major player in mining and metals, producing everything from zinc and aluminum to oil and gas.

Vedanta used to run a copper plant in Tuticorin, Tamil Nadu, through its unit, Sterlite Copper. At its peak, this plant produced 400 kilotonnes of copper every year, meeting around 40% of India’s refined copper needs.

But in 2018, things took a dramatic turn.

Sterlite became the center of an environmental controversy. Local communities accused the plant of polluting the air and water. Protests simmered for months and came to a head in May 2018 when police opened fire on demonstrators, killing 13 people. Following the tragedy, the Tamil Nadu government stepped in and permanently shut down the plant on environmental grounds.

This wasn’t just a setback for Vedanta—it was a blow to India’s entire copper industry. Overnight, the country went from being a net exporter of copper to a net importer, forced to depend on imports to meet its growing needs. Just last year, India had to import over 275 kilotonnes of copper to keep up with demand.

Vedanta’s challenges haven’t been limited to India. In 2004, it acquired an 80% stake in Zambia’s Konkola Copper Mines (KCM), one of the largest copper assets in the world. With promises of big investments, Vedanta seemed set for success. But things didn’t go as planned.

The Zambian government accused the company of underperforming and failing to meet environmental and social responsibilities. In 2019, the government took over KCM, sparking a long legal fight. It wasn’t until 2024 that Vedanta regained control after agreeing to invest $245 million to revive the mines.

Now, with its rich copper reserves, KCM is ready to ramp up production and play a key role in the global copper market. However, the experience highlighted the risks of operating in politically sensitive areas.

So, why is copper such a big deal anyway?

Copper is essential for building an electrified world. Its unmatched ability to conduct electricity makes it crucial for modern energy systems. Here’s why demand for copper is skyrocketing:

Electric Vehicles (EVs): EVs are major copper consumers, using about 80 kg of copper per vehicle—three times more than traditional gasoline cars. Copper is critical for EV batteries, motors, and charging stations.

Renewable Energy: Solar and wind farms rely heavily on copper. A solar farm uses about 2.4 tonnes of copper per gigawatt of capacity, while offshore wind farms need up to 13.5 tonnes per gigawatt for turbines, cables, and connectors.

Power Transmission: Unlike coal plants, renewable energy installations are often located far from cities. This requires expanded grids and high-voltage transmission lines, which are copper-intensive.

Urban Infrastructure: Copper is everywhere in modern cities—from electrical wiring in buildings to appliances and smart grids that power energy-efficient systems.

The world’s appetite for copper is only growing, and it’s clear we’ll need a lot more of it—and soon.

On the flip side, copper production is highly concentrated. Chile and Peru together account for over 40% of the world’s mined copper, while nearly 50% of refining happens in China.

Bringing new copper mines online takes about a decade, and global supply just isn’t keeping up with demand. By 2040, copper demand is expected to grow by 40%.

That’s just one side of the story. On the other side, Saudi Arabia is making a big push into copper.

Right now, over 70% of Saudi Arabia’s revenue comes from oil and gas. But depending too much on fossil fuels is risky, especially as the world shifts to cleaner energy. That’s why the Kingdom launched its Vision 2030—a bold plan to diversify its economy by focusing on industries like mining, renewable energy, and advanced manufacturing.

Copper is a key part of this plan.

For starters, Saudi Arabia aims to generate 50% of its energy from renewables by 2030. To make that happen, it needs a huge amount of copper for solar farms, wind turbines, and power lines.

But it’s not just about meeting local demand. Saudi Arabia wants to become a global mining powerhouse. The country is sitting on $1.3 trillion worth of untapped minerals, including copper, gold, and rare earth elements. By partnering with Vedanta, Saudi Arabia is building processing capacity that will reduce its reliance on imports and position itself as a major player in global supply chains.

Geopolitics adds another layer to Saudi Arabia’s copper ambitions. Right now, China dominates copper refining, handling nearly half of the world’s output. This heavy reliance on a single country makes global supply chains vulnerable to disruptions—whether from trade disputes or geopolitical tensions. Saudi Arabia’s investment in copper processing, including the Vedanta project, is part of a bigger plan to diversify away from China-controlled supply chains.

This shift is in line with global trends. It’s another example of the world’s China+1 strategy, where countries and companies are looking for alternative hubs to reduce their dependence on a single player. These decisions aren’t just about economics—they’re strategic.

Vedanta’s $2 billion investment looks like a move to reclaim its spot in the copper business. After the Sterlite controversy and the struggles in Zambia, the company needs a win to reestablish itself as a major player in copper production.

For Saudi Arabia, this partnership is a key piece of its plan to lead in the minerals critical for a low-carbon future.

For India, it could be a game-changer. These new facilities could provide India with a steady source of refined copper, reducing its dependence on imports from China. This would mean a more reliable supply chain for industries like EV manufacturing and renewable energy.

Will this partnership succeed in reshaping the global copper market? Or will it be another story of missed opportunities? One thing is clear: copper is no longer just a commodity. It’s the foundation of an electrified, decarbonized future, and everyone—from companies to nations—is racing to claim their share.

Big reforms will change the Indian insurance industry

Ever looked at insurance stocks and thought, Why are these so expensive? Valuations at 50x, 80x, even 100x earnings—it feels like they’re priced for a future that hasn’t arrived yet!

The Indian insurance industry is a bit like that late bloomer in school—everyone sees its potential, but it’s still trying to figure things out. Analysts predict the industry could grow at a staggering 12-15% CAGR in the coming years. That’s huge.

But here’s the twist: despite all the optimism, insurance penetration in India is shockingly low. That’s both an opportunity and a challenge. Opportunity, because there’s so much room to grow. Challenge, because progress has been slow.

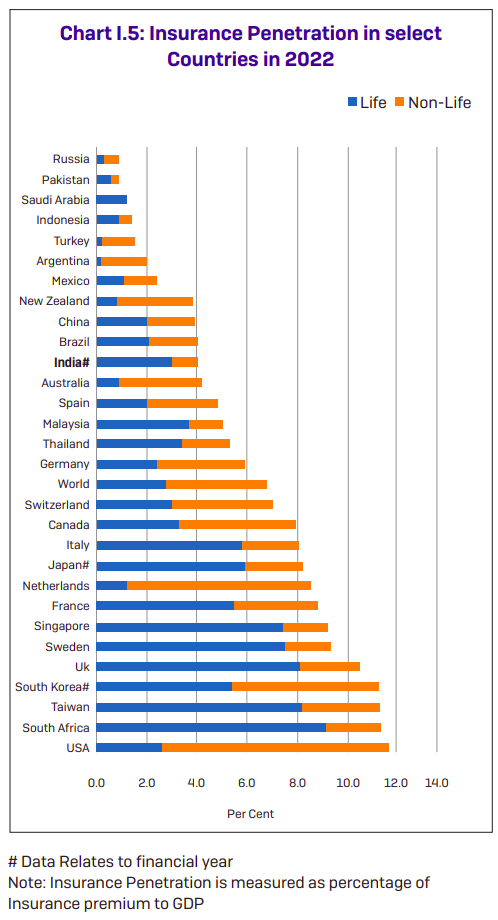

Let’s talk numbers. As of 2023, insurance penetration in India is just 4.2% of GDP. Compare that to the global average of 7.2% or emerging markets, which sit around 5-6%. Whichever way you look at it, we’re seriously underinsured. This gap highlights a massive growth opportunity for the industry.

On the flip side, we’ve been waiting for this growth in insurance for what feels like forever, but it just hasn’t shown up. India’s insurance penetration has barely budged since 2001, when the sector was opened up after decades of government control. Take a look at the numbers from the IRDAI annual report: back in 2001, penetration was around 2.7%. Today, it’s only at 4.2%. That’s two decades of painfully slow progress.

You’d think liberalization would have solved the problem—it’s worked wonders in so many other sectors. But here, it hasn’t.

This lack of progress has the government worried. In 2022, the IRDAI, India’s insurance regulator, set an ambitious goal: Insurance for All by 2047. But for that to happen, penetration needs to rise—and fast.

So, here’s the big question: what’s holding Indian insurance back?

Let’s imagine you’re trying to start an insurance business in India. The first roadblock you’ll hit is cultural. Think about it: buying insurance means spending money today for protection against something that might not even happen, sometime in the distant future. For most people, that’s just not a priority.

This mindset makes selling insurance tough. It’s a problem worldwide, but some countries, like Germany, have tackled it by making health insurance mandatory. In India, where a big chunk of earnings goes into daily expenses, many people see insurance as a luxury, not a necessity.

But let’s say you’re confident you can educate people and convince them of the importance of insurance. Well, then you’ll face a whole new set of challenges—this time, on the regulatory front.

To start an insurance business in India, the first thing you need is money—a lot of it. The law requires a minimum of ₹100 crores in capital just to get started. That’s a huge hurdle. Without that kind of money in the bank, you’re not even in the game.

One way many companies have managed this is by partnering with foreign insurers to bring in funding. Initially, foreign investment in Indian insurers was capped at 26%. Over time, the government eased these restrictions, and since 2021, foreign direct investment (FDI) of up to 74% is allowed in the insurance sector.

This has brought some big international names—like Allianz, Standard Life, and Prudential—into India through joint ventures with local companies. But thousands of global insurers are still staying out. Why? Probably because most foreign insurers don’t want to share control with Indian partners—they’d rather run the show on their own.

If you do manage to start an insurance company, your challenges don’t end there. You’re forced to choose between life and general insurance—you can’t legally offer both. So, if you’re a life insurer, you can’t cross-sell health or fire insurance, even to an existing customer. This limits what you can do, even when you already have paying clients.

Then there’s the solvency ratio. In India, insurers are required to maintain a 150% solvency ratio. To put it simply, for every ₹2 of liabilities, you need to keep ₹3 in assets. This makes sense for companies taking on a lot of high-risk policies. But here’s the catch—the rule applies equally to companies with low-risk policies. There’s no adjustment for risk, so everyone is treated the same, making it harder for some insurers to operate efficiently.

On top of that, insurance premiums in India are taxed under GST, making them more expensive for customers.

What’s the result of all this?

India has only 27 life insurers, 25 general insurers, and 7 health insurers—a total of just 59 players. For a country with 1.4 billion people, that’s shockingly low.

Compare this to the U.S., which has over 5,900 insurers serving a population of 330 million. Even when you adjust for scale, it’s clear that India’s market is seriously underdeveloped and lacks enough competition to truly thrive.

Now for the good news—change is in the air. The government and IRDAI are working on reforms that could shake things up in the insurance sector. The IRDAI has submitted a list of proposals for the upcoming Insurance Amendment Bill, set to be discussed in the winter session. Here are some key changes they’re considering:

Lowering Entry Barriers: The ₹100 crore capital requirement to start an insurance business might soon be relaxed. The IRDAI wants to allow smaller, specialized insurance businesses to start with less capital. For example, if you want to focus on agricultural insurance in Haryana, you wouldn’t need ₹100 crores. This could open the doors to niche players and help create a diverse range of insurers, similar to what we see in the U.S.

100% FDI in Insurance: The government is thinking about allowing 100% foreign direct investment (FDI) in insurance through the automatic route. This means global giants like Berkshire Hathaway or Aegon could enter the market without needing Indian partners. More players could mean more competition, more innovation, and better options for customers.

Composite Licenses: A new proposal could allow insurers to hold a composite license, meaning they could sell life, health, and general insurance under one roof. Imagine LIC agents selling health insurance alongside life policies. This would create economies of scale for insurance companies and make it simpler for customers to buy a wider range of products.

Risk-Based Capital Requirements: The solvency ratio system is set to get smarter. Instead of a one-size-fits-all rule, capital requirements will be tied to the risks insurers take on. This could reduce inefficiencies and give insurers more flexibility to expand.

There are plenty of other suggestions on the table too—ones that could make distributing insurance much more rewarding.

Here’s the thing: the Indian insurance industry has enormous potential, but it’s held back by big challenges—cultural barriers and regulatory hurdles being the most significant.

Fixing deep-rooted issues, like how we view insurance, could take decades. However, regulatory reforms can at least make steady progress and push the industry in the right direction.

That said, these changes won’t happen overnight. Turning these proposals into part of the bill and then passing them into law is still a long way off.

Tidbits

Moody's and Fitch downgraded several Adani companies to "negative," citing legal and governance risks, including bribery charges linked to Adani Green Energy. The stock market reacted quickly, with Adani Green Energy’s shares dropping 7%. Adding to the trouble, the Andhra Pradesh government may suspend a power purchase agreement with the group.

Byju’s, once valued at $22 billion, is now under a federal investigation for alleged fund misuse. After insolvency proceedings pushed the company to the brink, founder Byju Raveendran admitted the company’s valuation has dropped to zero. This has shaken investor confidence in the Indian startup ecosystem.

The EPFO plans to reinvest 50% of its ETF redemption proceeds into equities, aiming to boost returns for its 70 million members. A proposal to extend the redemption period to seven years shows a shift toward focusing on long-term growth.

India shipped 4.49 million PCs in Q3 2024, thanks to online festival sales and rising demand for premium laptops. HP maintained its position as the market leader, but desktop sales fell by 8.1%, reflecting a growing preference for portable devices over traditional setups.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.

Great Explanation