Is China Weaponising Rare Earth Minerals?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

China's Rare Earth Gambit: Weaponized Interdependence in Action

The rise of private credit

China's Rare Earth Gambit: Weaponized Interdependence in Action

Today, we're going to focus on what might just be the most significant yet underreported economic story of the week: China has just imposed major restrictions on rare earth exports. And that might just upend the world’s technology supply chains, and the geopolitical balance more generally.

But before we dive into China's move, though, let's talk about a concept that’ll help you understand what's happening: "weaponized interdependence."

Those who control chokepoints control trade

See, back in 2019, political scientists Henry Farrell and Abraham Newman showed us that global trade isn't just about mutual benefits. In a connected world, some countries can end up controlling critical chokepoints in global networks — like major shipping routes, payment systems, or rare resource supplies.

Controlling these chokepoints give a country two major powers: one, they can monitor what passes through (like spying on financial transactions), and two, they can block access entirely (like cutting countries off from banking systems). The United States has mastered this. It uses SWIFT, the global financial messaging system, for everything from tracking terrorist financing to enforcing sanctions. It's learnt to turn economic connections into a powerful source of leverage.

This idea turned conventional thinking on its head. There was a convenient justification around international trade that many people bought — countries that trade together wouldn't fight because they'd hurt themselves too. But Farrell and Newman showed that in our networked world, the pain of ceasing trade isn't equal. Whoever controls the chokepoints has the upper hand.

For decades, the United States has been the master of leveraging chokepoints. At different times, it has weaponised everything from the global financial messaging service SWIFT, to dollar clearing systems, to internet infrastructure. But now other powers, particularly China, are learning to play the same game

And rare earth minerals are one of the most potent chokepoints in its control.

China’s gambit

On April 4th, China imposed export restrictions on seven “rare earth” elements and the magnets they make.

Why does this matter? To understand that, you need to first understand what rare earths are.

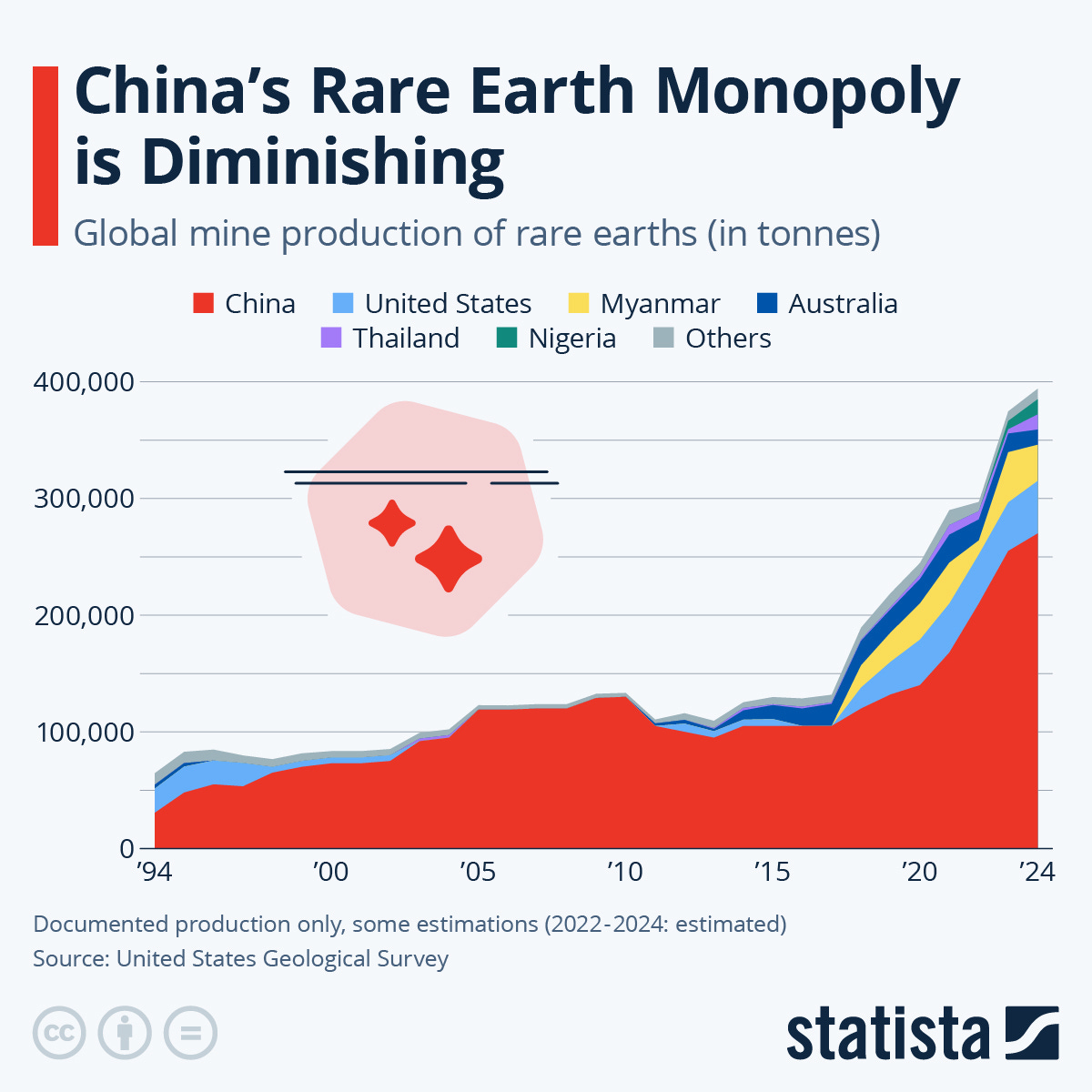

There are 17 rare earth elements. They span the periodic table, and have exotic names like neodymium, dysprosium, and terbium. Despite their name, rare earth elements aren't actually that rare in the Earth's crust. What makes them "rare", though, is that they're rarely found in concentrated, economically viable deposits. That makes mining these elements a critical chokepoint — one that China firmly has its thumb on.

What makes rare earths so valuable is their unique chemical properties. They're heat resistant, which makes them perfect for creating high-quality magnets, specialized glass, efficient batteries, and precision electronics.

As the New York Times explained yesterday, these metals can be sorted into two categories: light and heavy. Heavy rare earths have heavier atoms and are typically more scarce, which makes them prone to supply shortages. Light rare earths like neodymium and praseodymium are more abundant. But they’re still critical — and are primarily used in creating powerful magnets.

With that, let's get specific about China's latest restrictions. According to CSIS, China's Ministry of Commerce has imposed export controls on seven medium and heavy rare earth elements: samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium. Companies now need special licenses to export these elements or magnets containing them.

What makes this move particularly potent is that these specific rare earths are critical to defense and high-tech manufacturing. The F-35 fighter jet, for instance, contains over 900 pounds of rare earth elements. An Arleigh Burke-class destroyer requires approximately 5,200 pounds. A Virginia-class submarine uses around 9,200 pounds.

Beyond defense, these materials are essential for semiconductor chips powering AI systems, electric vehicle motors, wind turbines, and even the LED lights in millions of households. For example, the NYT reports that 99.9 percent of the world's dysprosium, which the chipmaker Nvidia uses to create capacitors, is mined in China.

The timing is no coincidence. According to reporting from the Center for Strategic and International Studies, this was a direct response to President Trump's tariff increases on Chinese products. They’re a calculated escalation in the ongoing trade war.

In other words, once the United States targeted Chinese exports, in return, China targeted the technological spine of modern economies itself.

How these restrictions might play out

So what's the potential impact of these restrictions? The most obvious and immediate effect of these will likely be supply disruptions and price increases for affected industries.

But more importantly, this exposes a strategic vulnerability for the United States.

Until 2023, China accounted for 99 percent of global heavy rare earth processing capacity, with only minimal output from a refinery in Vietnam. According to CSIS, even that facility has been shut down for the past year due to a tax dispute, effectively giving China a monopoly.

The United States, meanwhile, has one operational rare earth mine in Mountain Pass, California. The mine produces around 15 percent of all global rare earth materials, including lighter ones. But it lacks sufficient domestic refining capacity. As CSIS notes, almost all of this production continues to be exported for processing elsewhere.

The United States is scrambling to plug the gap. The US Department of Defense has committed over $439 million over the past four years to build domestic rare earth supply chains, aiming to develop a complete "mine-to-magnet" ecosystem by 2027. Companies like MP Materials and Lynas Rare Earths have received significant funding to establish processing facilities. MP Materials received $9.6 million in 2020 and an additional $35 million in 2022, while Lynas USA was awarded a $30.4 million grant in 2021 and another $120 million in 2022.

But that’ll all take time to come alive. The reality is that the United States is years away from true supply chain independence.

Without an adequate supply of rare earths, American manufacturing in sectors like automotive and electronics could grind to a halt. The military could face shortages of drones, missiles, and aircraft. Tech manufacturers like Nvidia, whose chips are already in short supply, would face additional constraints along with smartphone makers like Apple.

This is ultimately a trade war story

What we're seeing is only the latest move in an escalating economic chess match.

Trump began his trade war against China back in his first term. This sparked retaliatory measures from Beijing. The Biden administration continued the pressure with targeted export controls on advanced semiconductor technology, in a bid to slow China's technological advancement. China hit back with a spate of export bans and investigations. The countries have shared a frosty relationship for the better part of the last decade, to say the least.

But all of this pales against Trump’s aggressive policies ever since he returned to office. On February 1st, 2025, Trump went after China with a 10% tariff on Chinese imports — supposedly because China was flooding the United States with the drug, Fentanyl. Three days later, China responded with export controls on tungsten, tellurium, bismuth, molybdenum, and indium – all materials that could be used for both military and civil purposes.

And then, things ramped up severely this month. Trump followed with a massive 34% tariff on China, as part of his “liberation day” tariffs. In the days since, the two countries have gone after each other with round after round of tariffs. Both now have triple-digit tariffs against each other.

This is the backdrop for China’s latest restrictions. These tit-for-tat measures reflect a fundamental shift in how economic integration is viewed. Trade may once have been a matter of mutual benefit, but it’s increasingly being viewed through a national security lens.

Where do we go now?

So what move may we see next, if things continue to deteriorate?

China has already shown that it’s willing to expand restrictions to other critical minerals. For instance, in December 2023, it clamped down severely on high-quality graphite exports, which are crucial in making everything from aircraft components to EV batteries. It also banned the export of gallium and germanium late last year, both of which are crucial for semiconductors and 5G infrastructure.

If things continue in this vein, we might see similar curbs hit a variety of other critical inputs into high tech manufacturing, from transformers to specialty chemicals. China could also leverage its dominance in solar panel manufacturing, battery production, and pharmaceutical ingredients. All of this might eat into America’s ability to pursue advanced manufacturing — particularly for defence.

The United States, meanwhile, could try choking China’s access to compute, and to other critical technologies. It could further tighten semiconductor restrictions or potentially limit Chinese access to cloud computing services or key software. The Treasury Department could also restrict Chinese access to dollar funding or intensify scrutiny of Chinese investments. All of this would hasten the economic decoupling between the two countries.

As CSIS noted recently, "Both Washington and Beijing have asymmetric capabilities, and the United States has its own vulnerabilities which China can leverage."

A new battlefield

We’ve written previously about how we’re watching the collapse of the rules-based international economic order.

That collapse, we’re quickly realising, will be horribly messy. In its heyday, globalisation was a powerful force of economic development. As it unwinds, though, the very same linkages have turned into a battlefield. Economic networks that were built for efficiency have become weapons of statecraft.

We’re looking at a forced, fundamental restructuring of global economic relations. The era of weaponized interdependence is here, and from the looks of it, it’s going to hurt.

The rise of private credit

If you’re in need of a loan to run your business, who do you imagine you’ll go to? A bank? Perhaps an NBFC?

If you aren’t very plugged in to market news, though, you might not have thought of the new player that is stepping out of the shadows, quietly amassing trillions of dollars and transforming how companies get financing: private credit.

This is a relatively new phenomenon. Back in the early 2000s, private credit was hardly a thing. Now, it’s a multi-trillion dollar industry — one that’s coming under the cross-hairs of organisations like the IMF and the RBI. This is a story about innovation, risk, opportunity, and potentially, the world’s next big financial vulnerability hiding in plain sight. Let's get into it.

Let me take you back to 2008. As the dust from the global financial crisis settles, banks are pulling back from lending. They’re buried too deep under new regulations, and have been scarred by bad loans. There’s a vacuum; many people want credit that nobody is willing to supply.

Into this vacuum steps a different kind of lender – private credit funds. Fast forward to today, and that niche corner of finance has exploded into a $1 to 2.5 trillion behemoth depending on whose numbers you believe. It has seen a more than ten-fold increase from the mere $200 billion it represented in the early 2000s. For context, this relatively young asset class now rivals the size of the entire global high-yield bond market.

What exactly is private credit? Think of it as loans made outside the traditional banking system. Instead of going to JPMorgan or Bank of America, companies are increasingly turning to specialized investment funds that offer loans directly, without all the red tape and restrictions that come with bank financing.

The most common flavor of this is direct lending, where funds make loans straight to midsize businesses, usually holding onto those loans until they're paid back rather than trading them. Then there's mezzanine lending, which sits between debt and equity in the capital structure – riskier, but with higher potential returns. Asset-based lending is backed by hard assets like real estate or equipment. And distressed debt strategies involve buying troubled loans at deep discounts, betting that they'll recover more value than the market believes.

What makes these loans different from traditional bank financing? On one hand, they're usually more expensive. While a bank might charge 5% interest, a private credit fund might charge 8% or more. But on the other hand, borrowers get more flexible terms, faster execution, and often higher leverage than banks would allow. These aren't standardized products – they're bespoke financial solutions negotiated directly between lender and borrower.

The cast of characters

Let's meet the key players of the private credit saga.

First, we have lenders – the private credit funds themselves.

These are typically managed by alternative asset managers — like Blackstone, Apollo, or Ares. Many of them cut their teeth in private equity before expanding into credit. About 40% of European private credit funds and 25% of U.S. funds are affiliated with private equity firms. This creates interesting dynamics, which we'll explore later.

Unlike banks, which are primarily financed by deposits and short-term debt, private credit funds raise capital more like private equity – through closed-end funds with long-term lockups. In the U.S., they use some leverage, borrowing about 40 cents for every dollar of equity. European funds are more conservative, with only about 11 cents of borrowing per dollar of equity. This is dramatically less leverage than banks, which often operate with $10 or more of assets for every dollar of equity.

Then we have the investors – the limited partners putting money into these funds.

This is currently a sophisticated crowd: insurance companies looking for yield, pension funds seeking to match long-term liabilities, and sovereign wealth funds with decades-long investment horizons. In the U.S., insurance companies and pension funds had committed over $90 billion to private credit as of 2021.

But there's a plot twist developing. The industry is increasingly trying to tap into retail investor money, through vehicles like Business Development Companies (BDCs) in the U.S.. These already manage over $300 billion and are open to individual investors. In Europe, regulations like the European Long Term Investment Fund and Long Term Asset Funds are being designed to open these strategies to a broader audience. This potential "retailisation" of private credit is raising eyebrows among regulators.

And finally, we have the borrowers – predominantly middle-market companies that fall between the cracks of traditional financing.

They're too large or risky for standard bank loans but too small to tap public bond markets efficiently. In the U.S., these are companies with revenues typically between $100 million and $1 billion. Surprisingly, these aren’t financial basket cases – most have stable operating margins around 25-27%. They’re simply underserved.

Many of these borrowers share another very interesting characteristic – they're backed by private equity sponsors. In the U.S., private equity-sponsored deals make up about 78% of private credit activity. In Europe, it's around 42%. This creates an interesting ecosystem: private equity firms buy companies, using debt from private credit funds, which could be managed by the same parent company!

Why the explosive growth?

So what's driving this remarkable growth story? These funds arose because of a fascinating convergence of regulatory changes, economic forces, and financial innovation.

The post-2008 credit gap

The first catalyst was the post-crisis regulatory crackdown on banks. After 2008, new rules like Basel III dramatically increased capital requirements for bank lending, especially to riskier borrowers. Banks responded by retreating from certain lending activities. This created a gap.

A survey of private debt fund managers revealed that they believe about half of their portfolio companies wouldn't qualify for bank financing. Those companies were too small for bank syndication, lacked sufficient tangible assets for collateral, or had financial statements that were too messy for bank credit committees to approve. As one fund manager told researchers, "We finance companies and leverage levels that banks would not fund."

Basically, private credit funds are stepping in to supply credit to parts of the economy where banks fear to tread, offering more flexible solutions to companies that don't fit neatly into traditional bank lending criteria.

The low-interest bonanza

For over a decade after the crisis, we had an unprecedented time of low interest rates. With government bonds offering paltry yields, institutional investors like pension funds and insurance companies faced a dilemma — how could they generate the returns they needed to meet their obligations?

Private credit, with gross unlevered returns targeting 8-9%, offered a compelling alternative. Compared to five-year Treasury notes, which yielded less than 1% at the time, or BB-rated bonds, which gave returns of around 3.2%, private credit promised equity-like premiums with supposedly debt-like risk. BIS research confirms this story, finding that countries with lower policy rates tend to have larger private credit footprints.

Banks’ lost moat

The third element is a relative improvement in private credit funds' competitive position versus banks.

After the financial crisis, banks saw their cost of equity capital increase substantially. Meanwhile, private credit funds managed to reduce their own cost of capital over the same time, partly by gradually increasing their leverage. The gap in funding costs between banks and private credit narrowed by approximately 200 basis points, which made private credit funds more competitive in certain lending segments.

These storylines converged to create perfect conditions for the private credit boom. Banks were pulling back, investors were hungry for yield, and private credit funds were increasingly able to compete on price while offering more flexible terms.

Global expansion

While this story began in the United States, it's rapidly becoming a global phenomenon. The model has been exported worldwide, adapting to local conditions as it spreads.

North America is, of course, still the epicenter of the private credit boom. It accounts for 87% of the global private credit market. There, private credit represents about 7% of all lending to non-financial corporations – comparable to the shares of syndicated loans and high-yield bonds. It has, in fact, become a mainstream financing option for American businesses.

Europe is the industry’s second-largest market, albeit much smaller. Here, private credit accounts for just 1.6% of corporate lending. But that number is growing rapidly — at 17% annually. That said, these look very different from their North American cousins. European private credit funds are far less reliant on private equity sponsors. If anything, they compete more directly with banks than their American counterparts.

The newest chapter in this global expansion, however, is being written in Asia. This is still a small segment – accounting for only about 0.2% of corporate credit. But Asian private credit has been growing at an impressive 20% annually over the last five years. The market is estimated at around $93 billion. There’s already significant activity in Australia, Singapore and Hong Kong, and increasingly, it’s also spreading to emerging economies like India.

Private credit plays a slightly different role in Asia than in the West. It typically fills the many gaps left by banks in areas like acquisition financing, lending to asset-light businesses, and providing capital to distressed companies. The market remains fragmented, however — perhaps due to differences in currencies, regulatory environments, and investor protection regimes.

Of course, these markets aren’t cut-off from each other. Capital and expertise flows across borders. Many private credit fund managers based in North America are financing deals in Europe and Asia, creating global interconnections that didn't exist before.

The risks on the horizon

There’s one problem with private credit. As this market has grown, so have concerns about the risks it might pose to the broader financial system.

The first risk centers on borrower vulnerability. Unlike most bank loans with fixed rates, private credit typically comes with floating interest rates. This makes borrowers sensitive to rate increases. With central banks keeping rates high to combat inflation, many private credit borrowers have seen their interest burdens spike.

In a time like this, some firms have resorted to "payment-in-kind" interest, where they add interest to the loan principal rather than paying it in cash. This is a tricky move; while it provides temporary relief, it can lead to compounding debt if the company's performance doesn't improve. One research study found that the share of payment-in-kind interest in Business Development Companies' income has doubled since 2019 — a potential warning sign.

The second concern involves valuation opacity. Unlike publicly traded bonds or loans, private credit deals aren't regularly priced in liquid markets. Research shows that private credit valuations move much less than high-yield bonds and leveraged loans during market stress, even though the underlying companies are often riskier. That’s a problem. This opacity could mask growing problems, right until they surface, catching everyone off guard. Imagine a scenario where funds delay recognizing losses, until there’s a sudden spike in defaults and dramatic markdowns. The sheer suddenness of it could create a confidence crisis that could ripple through the system.

Third, there's growing investor concentration. Some insurance companies and pension funds have put a lot of money in private credit and other illiquid assets. Private-equity-influenced life insurers in the U.S. now manage over $1 trillion — and have median exposure to illiquid investments of around 20% of assets (compared to just 6% for other large insurers).

If these concentrated positions face losses, those can ripple through the system — particularly if investors are using derivatives or other forms of leverage. Some of the world's largest pension funds have dramatically increased both their allocation to illiquid investments and their use of derivatives, creating potentially concerning combinations of illiquidity and leverage.

Fourth, while private credit funds themselves use relatively modest leverage compared to banks, there are multiple layers of leverage throughout the private credit ecosystem. Borrowers are leveraged, funds may use moderate leverage, and even the end investors might employ leverage. This complex web of borrowing, on a bad day, could amplify losses.

Finally, there's the growing shift toward semi-liquid fund structures. Traditional private credit funds lock up capital for 5-7 years, matching the illiquidity of their assets. But newer vehicles are offering more frequent redemption windows to attract a broader investor base. This creates a potential mismatch – illiquid assets funded by increasingly liquid liabilities. This is the kind of thing that can create chaos during a severe market downturn.

The resolution – implications and future

When private credit fund managers were surveyed in 2021, they were overwhelmingly optimistic. Over 75% viewed the environment as "good" or "very good." Their main concerns were competition from other funds and finding enough good deals to deploy their capital.

That optimism has been tempered since by rising rates and economic uncertainty, even though the structural growth trend remains intact. Private credit has been surprisingly resilient through economic cycles, in fact — including the COVID-19 pandemic, where it didn't experience the same freeze-up as public markets.

Perhaps the most profound implication is the continuing evolution of our financial architecture. Credit is migrating from heavily regulated banks with deposit insurance and central bank support to less regulated private funds. This shifts risks around the system rather than eliminating them, potentially creating new vulnerabilities that aren't yet fully understood.

The future will probably bring increased regulatory scrutiny. The IMF has called for authorities to "consider a more intrusive supervisory and regulatory approach to private credit funds" and to close data gaps to better monitor risks. Just as regulators eventually caught up with shadow banking after 2008, they're now turning their attention to private credit.

In many ways, the private credit story mirrors previous chapters in financial history – innovation creating new opportunities while potentially sowing the seeds of future instability. The key question isn't whether private credit will continue to grow, but whether it can do so sustainably without becoming the next financial boogeyman.

Tidbits

Tata Sons to Use Record ₹32,722 Cr TCS Dividend for Semiconductor and Aviation Bets

Source: Business Standard

Tata Sons is set to receive a record ₹32,722 crore dividend from Tata Consultancy Services (TCS) for FY25, the highest-ever payout from its flagship IT firm. This follows a ₹24,931 crore interim dividend already paid for the first nine months of FY25. In comparison, the FY23 dividend stood at ₹30,418 crore. The group plans to use the fresh inflow to fund major investments, including ₹91,000 crore for a semiconductor fab in Dholera and ₹27,000 crore for an ATMP facility in Assam. Additionally, Tata Sons recently infused ₹1,500 crore into Tata Capital and ₹1,432 crore into Tata Projects. In FY24, it had used the TCS dividend to fully repay its bank loans, and its cash surplus rose to ₹3,042 crore as of March 31, 2024. Despite ongoing investments in sectors like digital and aviation, rating agencies have noted Tata Sons' strong financial position driven by steady dividend inflows.

OPEC Lowers Oil Demand Growth Forecast for 2025 and 2026

Source: Reuters

OPEC has reduced its global oil demand growth forecast by 150,000 barrels per day (bpd) each for 2025 and 2026, revising the projections to 1.30 million bpd and 1.28 million bpd respectively. This marks the first downward revision since December 2023. The decision follows weaker-than-expected demand data from Q1 2025 and heightened trade tensions after the U.S. imposed new tariffs. In response to these developments, OPEC has also trimmed its global GDP growth forecast to 3.0% for 2024 and 3.1% for 2025, both down by 0.1 percentage point. Despite the demand cut, Brent crude prices remained around $66 per barrel, supported by temporary U.S. tariff exemptions. The adjustments highlight how evolving trade policies and economic data are shaping the global energy outlook.

India’s Polished Diamond Exports Hit 20-Year Low Amid Global Demand Slump

Source: Reuters

India’s cut and polished diamond exports declined by 16.8% year-on-year to $13.3 billion in FY2024-25, marking the lowest level in nearly two decades, as per data from the Gems and Jewellery Export Promotion Council (GJEPC). This drop pulled down total gem and jewellery exports by 11.7% to $28.5 billion, compared to $32.28 billion in the previous fiscal year. Exports of cut and polished diamonds, which typically contribute nearly half of the sector’s total, were impacted by weak demand from major markets such as the U.S. and China. Meanwhile, imports of rough diamonds also fell 24.3% to $10.8 billion, indicating a slowdown in production. Exporters rushed to dispatch consignments in March 2025, pushing exports up 1% year-on-year to $2.56 billion ahead of the proposed U.S. tariff hike. Although a 90-day pause on the 27% tariff by the U.S. provided temporary relief, the outlook remains uncertain.

- This edition of the newsletter was written by Bhuvan and Pranav

📚Join our book club

We've recently started a book club where we meet each week in Bangalore to read and talk about books we find fascinating.

If you'd like to join us, we'd love to have you along! Join in here.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thank you guys, i wish