The new rules of paying for electricity

Draft amendments in Electricity (Rights of Consumers) Rules

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The new rules of paying for electricity

A gas the world cannot live without

The new rules of paying for electricity

Over the past few months, we’ve written about big shifts happening in India’s power sector — from the Draft National Electricity Policy 2026 to the Draft Electricity Amendment Bill aimed at fixing India’s financially broken discoms. Those were macro-level, strategy documents for how India’s grid should evolve over the next two decades. What we’re looking at today is a lot more relatable, because it directly affects us as consumers.

On March 12, the Ministry of Power released something much more immediate: a draft amendment to the Electricity (Rights of Consumers) Rules. These aren’t grand policy visions, but operational tweaks to the rules that govern your electricity connection, your bill, and your relationship with the discom.

And buried in them are three provisions that could fundamentally change how large electricity consumers — and eventually, all of us — pay for power.

The price of time

Let’s start with a simple question, should electricity cost the same at 2 PM as it does at 8 PM?

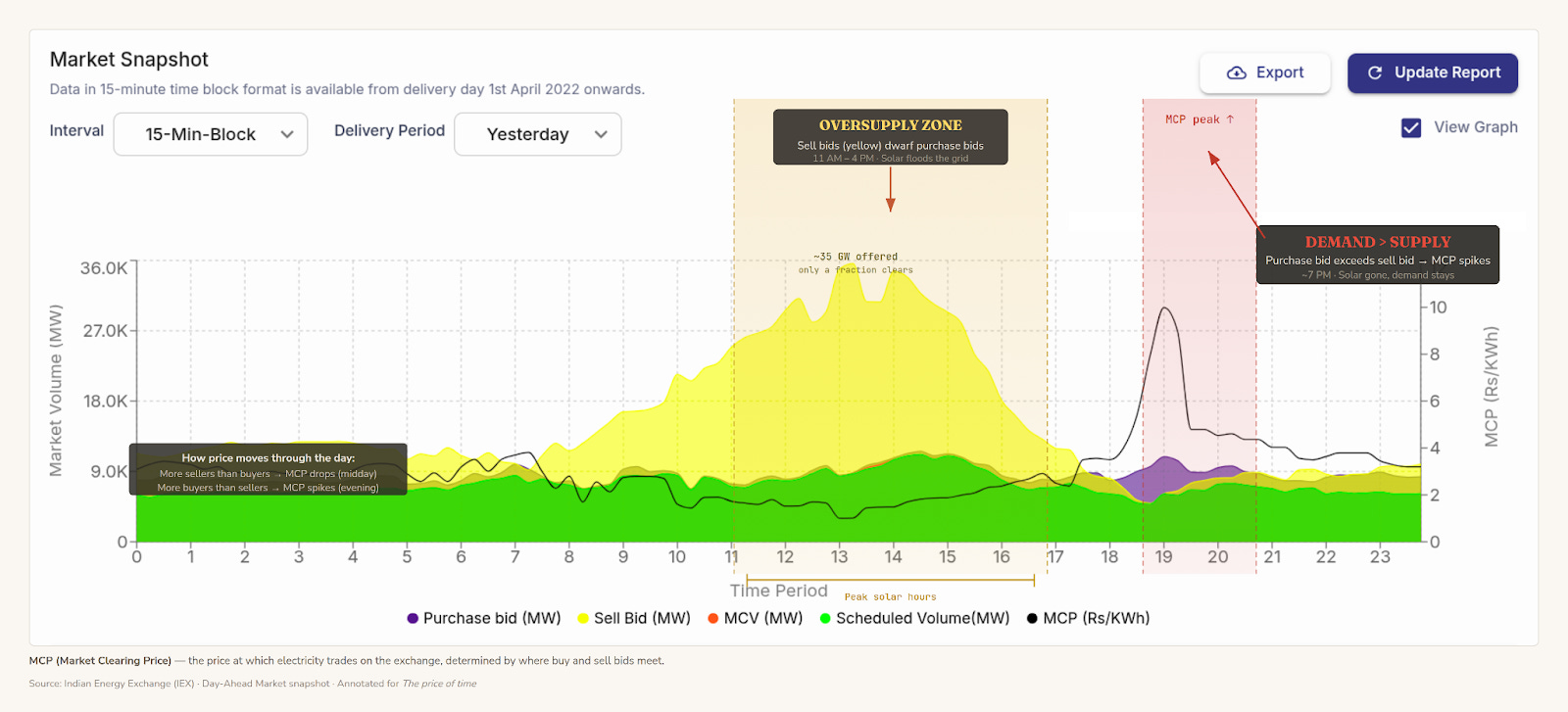

For most of India’s history, the answer has been yes. You pay a flat rate per unit, regardless of when you consume it. That made sense when most of our power came from coal plants that run around the clock at roughly the same cost. But India’s electricity mix has changed dramatically. Solar power now floods the grid during the day — and you can see this play out in real time on the Indian Energy Exchange.

On a typical day, the amount of power offered for sale between 8 AM and 3 PM dwarfs what actually gets bought. At peak, sellers offer upwards of 35 GW. Only a fraction of that is bought. That gap — that surplus electricity — is essentially stranded: panels generating power with no buyers. Come evening, that surplus vanishes. The market clearing price spikes sharply around sunset as the grid scrambles for power.

A flat tariff completely ignores this reality. If the demand of something changes during the day relative to supply, ideally, so should its price. That price would be a useful signal. Cheap prices would push consumers to use power as much as they could when it was abundant, taking some load off the hours when the grid was most stressed.

To fix that, you can have “Time of Day (ToD)” tariffs. You charge more during peak hours (peak demand and struggling supply) and less during solar hours (oversupply of solar energy), so consumers have a reason to shift their consumption patterns. This isn’t new. India’s consumer rules mandated ToD tariffs back in 2023, at least for commercial and industrial (C&I) consumers with demand above 10 kW.

Here’s what that means. Say your normal tariff is ₹10 per unit. Under ToD, the rules say your peak-hour rate must be at least 20% higher than normal, or at least ₹12. And your solar-hour rate must be at least 20% lower, or at most ₹8. That means, in a single day, the gap between the cheapest and most expensive electricity is at least ₹4 on a ₹10 base — a 40% spread. That’s the minimum spread. States can set it wider.

There’s also a safeguard built in. “Peak hours” can’t be longer than “solar hours”, which are defined as eight hours during the day. Without this cap, a DISCOM could just declare most of the day as “peak”, which would defeat the entire purpose by charging premiums through most of the day.

Those 2023 rules were supposed to kick in from April 2024 for C&I consumers, and April 2025 for everyone else (except agricultural consumers). Only, that didn’t happen. Most states dragged their feet.

The reason for this was straightforward. ToD billing requires smart meters, which can record consumption in time blocks. But India’s smart meter rollout has been painfully slow. Without the meters, the tariff is unenforceable.

The new draft acknowledges this slippage. It pushes the deadline to April 2027 for C&I consumers and April 2028 for all other non-agricultural consumers. This timeline is tied, explicitly, to the pace of smart meter installation.

For all large consumers — factories, malls, hospitals, data centres, and others — the message is: you have about a year to prepare. When ToD hits, the economics of how you run your operations will change overnight. Use heavy machinery in daylight hours, and you get a 20% discount. Use it during the evening peak, and you have to pay a 20% premium. That kind of spread is enough to justify serious investment in automated energy management or in batteries that can store daytime power for evening use.

This brings us to our next observation.

The end of the free battery

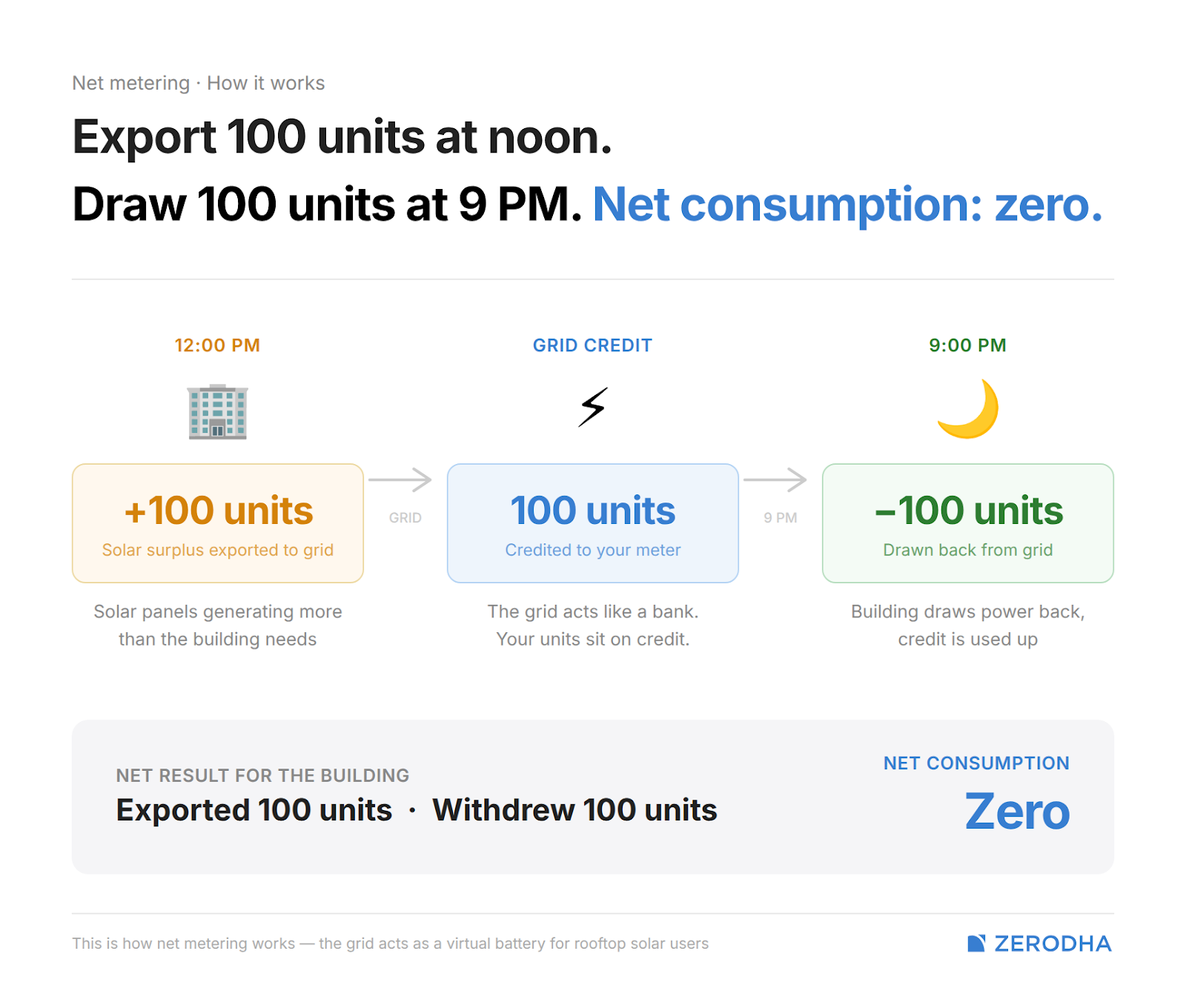

If you have rooftop solar panels on your factory or office building, you probably use something called “net metering”. During the day, if your panels generate more electricity than you need, the extra gets exported to the grid. At night, when the panels aren’t producing anything, you draw power back from the grid. At the end of the billing cycle, you pay only for the net difference — what you consumed minus what you exported.

Net metering has been the single biggest driver of rooftop solar adoption in India. But it has a hidden subsidy built into it.

Think about what happens when a large commercial building exports surplus power at noon and withdraws an equivalent amount at 9 PM. From the building owner’s perspective, they exported 100 units and drew 100 units back. Their net consumption is zero.

But the DISCOM is essentially paying for the transaction.

The DISCOM had to accept that surplus power at noon, when the grid was already flush with solar. It had to manage the transmission and distribution losses, and then balance the grid. And when evening rolled by, it had to procure expensive peak-hour power in the evening to supply that same consumer. The building owner paid nothing. The DISCOM effectively acted as a free, zero-cost battery. That’s unfair, to say the least.

There’s a second, subtler distortion. Indian electricity tariffs are typically slab-based, which means higher consumption equals a higher per-unit rate. The idea, here, is that large consumers subsidise smaller ones, which in turn cross-subsidises agricultural and low-income households. But net metering makes large consumers appear small. A factory that actually consumes 5,000 units a month might show a net consumption of just 1,000 units after solar offsets, landing it in a lower tariff slab. This breaks the design of the system. As commercial users avoid higher per-unit charges, the cost of maintaining the grid shifts further onto ordinary consumers, who can’t afford solar panels.

The draft addresses this by allowing State Electricity Regulatory Commissions (SERCs) to levy a progressive net metering charge on prosumers — consumers who both produce and consume power — with installations above 5 kW. Such a charge didn’t exist until now. Standard household rooftop systems, up to 5 kW, are fully exempt from this. But above 5 kW, the charge scales progressively, as the scale of setup increases. The charges are pegged to what a battery would cost to do the same job that the grid is currently doing for free.

So, a small commercial setup with 10 kW of solar would face a modest charge. A large industrial installation with 400 kW would face a meaningful one. The design intent is to make the grid-as-free-battery model progressively more expensive as the system’s size grows, without killing rooftop solar for households.

This is gentler than what the NEP 2026 signalled. That policy document wanted to effectively end net metering beyond 5 kW. The consumer rules take a softer route — they don’t ban net metering, they just no longer make it free. But the direction is the same.

Buy your own battery

The third provision is the most forceful. For prosumers whose renewable energy installations exceed 500 kW, state commissions now have explicit legal authority to mandate the installation of an energy storage system.

This is genuinely new. The earlier rules had no provision giving regulators the power to force a private consumer to buy a battery alongside their solar plant. They could, for sure, incentivise storage, but they couldn’t require it. The March 2026 draft creates that power through a new sub-rule.

The 500 kW threshold is carefully chosen. It captures large industrial complexes, IT parks, shopping malls, hospital campuses, and big warehouses — the segment that’s large enough to meaningfully stress the distribution network when thousands of such installations simultaneously dump surplus solar at noon. It doesn’t touch households, small shops, or mid-sized commercial setups.

This isn’t mandatory; it just gives a new lever to state commissions. They may mandate storage, not that they must. But the incentive structure makes it almost inevitable that solar-heavy states will use this power. Rajasthan, Gujarat, and Tamil Nadu — where midday grid management is already a serious operational challenge — will likely move first.

How much storage can be mandated? Well, the draft says “appropriate capacity” and leaves it to each state commission to define. It could be 2-4 hours of storage relative to peak solar output, but nothing is specified yet.

What makes this provision work, though, is how it fits with the other two. The ToD tariff creates a 40% spread between cheap daytime power and expensive evening power — which means a battery that stores solar energy during the day and discharges it at night starts to pay for itself much faster. The net metering charge removes the free alternative of using the grid as storage. And this mandate gives powers to regulators to nudge large prosumers who still don’t respond to price signals alone. Each provision reinforces the others.

What comes next

There’s one more addition worth flagging. The draft formally defines “demand response” — the idea that consumers can be paid to reduce their usage when the grid is stressed. That’s still in its early days, but it tells you where the government’s head is at.

This is an important area to think hard about. India’s solar buildout has outrun its grid. The country added about 15 GW of solar capacity in FY24, 24 GW in FY25, and a record 36.6 GW in calendar year 2025 — our cumulative capacity crossing 130 GW. But in 2025, India curtailed 2.3 TWh of solar generation. In Rajasthan, Gujarat, and Tamil Nadu, curtailment rates ran between 10% and 30%. We built the panels, but we’re still struggling to use them.

Getting the necessary infrastructure up will take time. Capital alone can’t close that gap. And so, we need better battery infrastructure, smarter demand-side optimisation for commercial and industrial clusters, and more entrepreneurs building the boring grid plumbing that makes the transition actually work.

This is something we’ve been investing in through Rainmatter. If you’re building in this space, please reach out to us.

Credit where it’s due: the government isn’t just writing grand vision documents. It set the broad direction with NEP 2026, but now, these consumer rules lay the wiring — ToD tariffs, net metering charges, storage mandates, billing safeguards, and more.

None of it is headline-grabbing. But often, the boring stuff matters most.

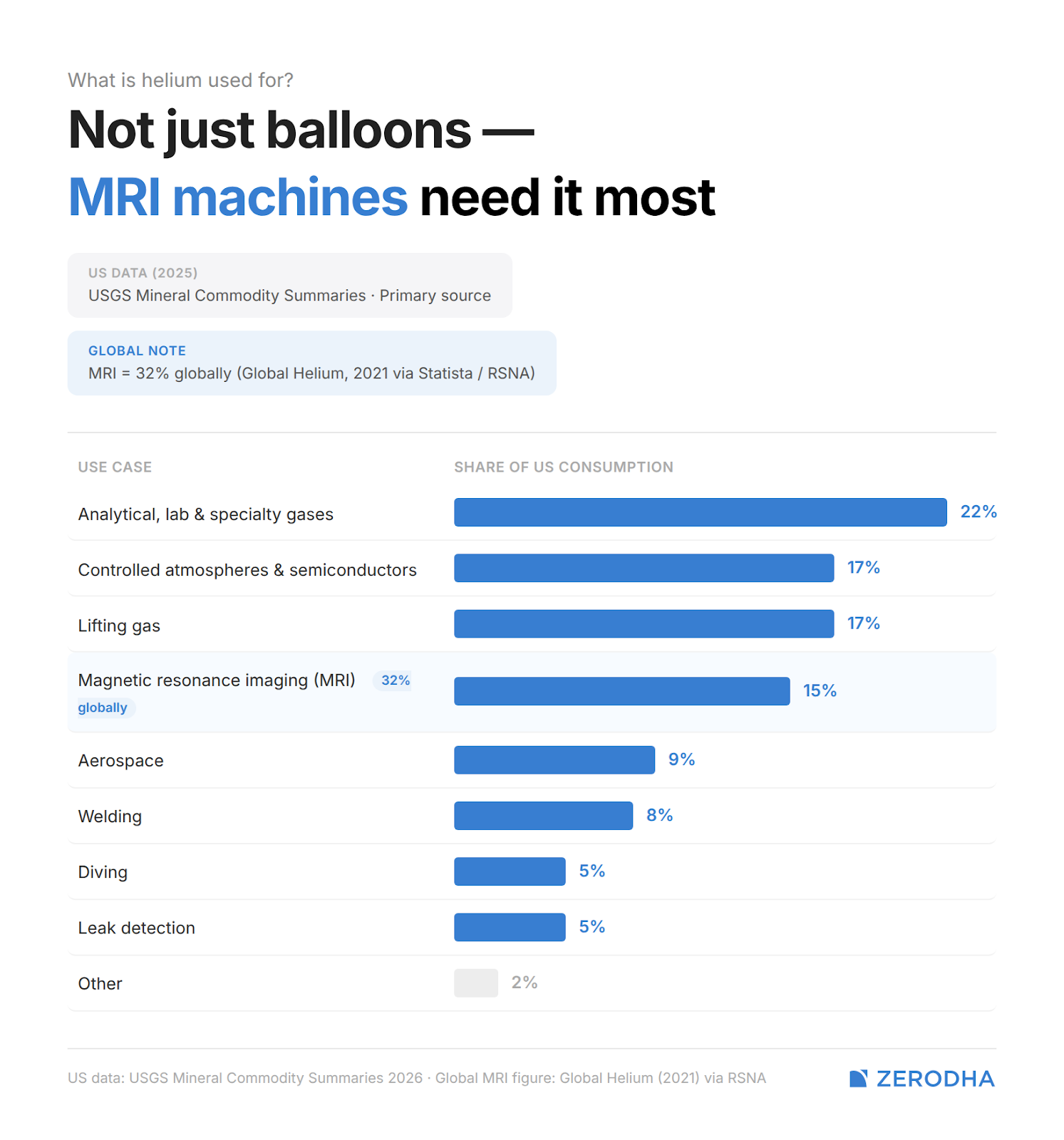

A gas the world cannot live without

We’ve written about what the closure of the Strait of Hormuz means for oil.

That was the most obvious angle we found, when we first began thinking about this war. But oil isn’t the only thing the world depends on that flows out of the Persian Gulf. There’s a gas; one most people only associate with birthday balloons, but one that is, in fact, among the most critical industrial materials on Earth. And right now, about a third of the global supply is offline.

The gas is helium. Because of this war, Qatar’s helium output has become inaccessible. And if this state of things continues for a few weeks, we might find ourselves in a crisis.

What helium actually is

Helium is the second lightest element in the universe. Out there, in space, it’s everywhere. Stars are essentially helium factories. A quarter of our own sun’s mass is helium.

Here on Earth, however, it is rare.

Helium is so light that Earth’s gravity can’t hold onto it. Unlike oxygen or nitrogen, which cycle endlessly through our atmosphere, soil, and living things, once helium escapes to the surface, it drifts up and leaks out into space. Once it’s gone from Earth, it’s gone permanently.

That is why you cannot “manufacture” helium. You cannot pull it out of the atmosphere, they way you can with oxygen or nitrogen. Helium has to be found.

The only reason we have any helium at all is that it forms underground. Some radioactive elements — primarily uranium and thorium — decay slowly inside the Earth’s crust over millions of years. As their atoms break apart, they push out helium as a by-product. This accumulates in porous rock formations deep underground, often in the same geological traps that hold natural gas.

This is why helium and natural gas are often found together. It’s also why extracting helium is not its own standalone industry; but a byproduct of natural gas processing.

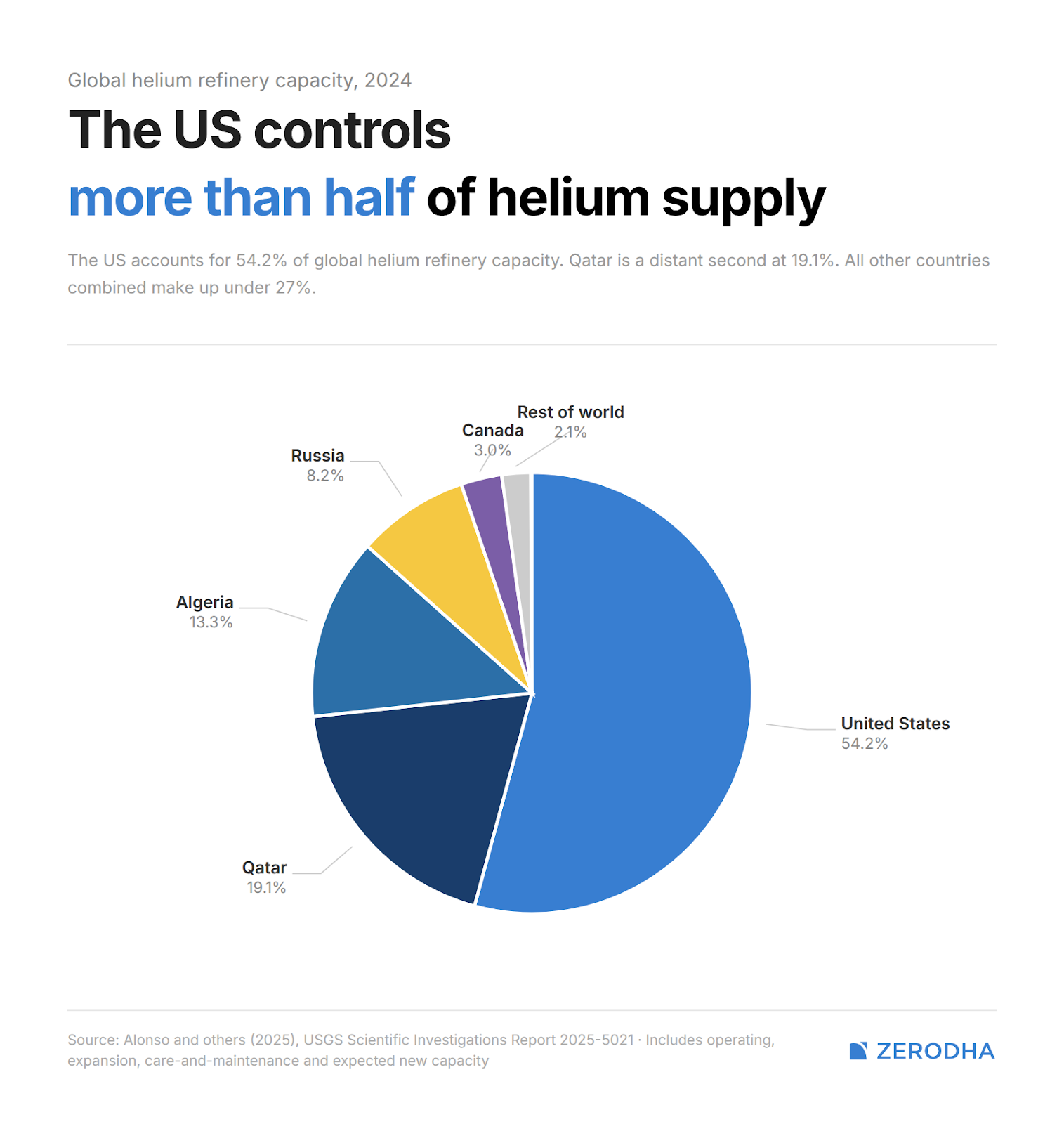

There are very few places where it accumulates in commercially useful concentrations, however. According to the US Geological Survey, the United States, Qatar, Russia, and Algeria together hold roughly 70% of known global reserves. Fewer than fifteen producers dominate global output.

Why it matters I: MRI machines

Helium has a lot of use cases. One of the biggest is MRI machines.

Before we get there, let’s start with the basics: as current flows through a wire, those electrons meet all sorts of interruptions as they move, from atoms, to impurities, to defects. That friction generates heat and wastes energy. It’s why your phone charger gets warm. This resistance is unavoidable at normal temperatures.

But at temperatures close to the coldest point physically possible — where atoms nearly stop moving completely — something strange happens to certain metals. Their resistance drops to zero. Electrons flow through them indefinitely, without losing any energy. This is called superconductivity.

An MRI machine is built around this principle. It has a coil of superconducting wire. When current passes through it, it becomes magnetic. So, you pass a current through it once, and that current keeps circulating forever, generating a powerful, perfectly stable magnetic field — which is exactly what you need to see the soft tissue inside a human body. The moment that wire warms up even slightly, superconductivity vanishes, the current stops, and the magnetic field collapses.

This is called a quench — the machine goes offline. Restarting it takes days, and a lot of money.

To prevent this, the magnet must be kept in liquid coolant at all times. This is where helium comes in. Helium is the only substance on Earth that stays liquid at the extreme temperatures superconductivity requires. Everything else freezes at that temperature. A typical MRI machine holds around 1,700 litres of liquid helium and needs periodic top-ups. There is no substitute.

To be fair, some newer MRI designs are beginning to enter the market. These don’t remove the need for helium, but they do reduce it. GE HealthCare and Siemens Healthineers have both developed systems that reduce helium requirements by up to 99%. So far, though, they’re a tiny fraction of the world’s installed MRI machines. The overwhelming majority are conventional, and they need lots of helium.

Why it matters II: semiconductors

The second critical application is less well known but increasingly important: chip manufacturing. Semiconductors currently account for roughly a quarter of the world’s helium consumption.

Making a modern chip involves etching incredibly fine circuits onto silicon wafers — features measured in nanometres, or billionths of a metre. The etching is done using plasma: a high-energy gas, charged electrically, that bombards the wafer surface to carve circuit patterns.

Only, plasma generates intense heat. And because the tolerances in chip manufacturing are so tight, even small variations in temperature across the wafer surface will distort the circuits being etched, yielding defective chips.

Enter helium.

During plasma etching, the wafer sits on a cooled metal chuck inside a vacuum chamber. But in a vacuum, two solid surfaces don’t make perfect thermal contact — there are microscopic gaps between them, and almost no heat goes from one to the other. So helium gas is pumped at low pressure behind the wafer, filling those gaps. The thermal conductivity of helium is roughly six times higher than argon, making it uniquely effective at drawing heat away uniformly from across the wafer’s surface. Without it, temperature variation across the wafer doubles — which, at modern chip dimensions, translates directly to lower yields and defective products.

Helium is also used as a carrier and purge gas during other key manufacturing steps. It’s chemical inert — it reacts to nothing — which is why it doesn’t react with any material being deposited on top of the wafer.

Qatar is home to one of only two plants globally that produces semiconductor-grade helium — the ultra-pure form required for chip fabrication. In fact, the Semiconductor Industry Association warned, as far back as 2023, that if helium supplies were disrupted, “there would likely be shocks to the global semiconductor manufacturing industry.”

The Qatar problem

Heading into 2026, the global helium market was actually in surplus. Supply had recovered from the last major shortage — a bruising period in 2022, caused by fires at a Russian processing plant and an outage at a US federal facility. New capacity had come online. The Industry forecaster Intelligas projected that supply would exceed demand in 2025 and beyond. Storage facilities in Germany and the US would have to absorb the excess.

Then, on March 2nd, Iran attacked Qatar with drones and missiles. QatarEnergy was forced to shut down its Ras Laffan Industrial City complex entirely. And Ras Laffan is where Qatar processes its natural gas for LNG export.

Along with LNG, we also draw out helium as part of that same process. The facility produces up to 17 metric tons of helium per day — roughly one-third of the entire world’s supply. Production stopped immediately. Two days later, QatarEnergy declared “force majeure” to affected buyers — a commercial and legal signal that it was incapable of meeting its contracts, for reasons outside its control. The company’s CEO has since said Ras Laffan will not restart until the conflict ends completely.

The Strait of Hormuz closure compounds the problem. Even if Qatar could resume production tomorrow, that helium would have to be shipped through the Strait. This would take specialised cryogenic ISO containers — and a significant portion of those containers are currently either stuck in Qatar but unable to leave, or en route there but unable to arrive.

Phil Kornbluth, one of the world’s leading helium consultants, said publicly that it is “hard to imagine” that helium supply will not be disrupted for a minimum of three months. And however long the production shutdown lasts, the world should expect to add at least two additional months for logistics to normalise. In his words, “the world can’t compensate for the loss of a third of its helium supply.” Industry observers are already calling this Helium Shortage 5.0 — the fifth significant global helium crisis in fifteen years.

Why it’s so hard to fix

When most industrial materials fall short, that can be partially addressed by ramping up production elsewhere, or finding substitutes. Helium offers neither option easily.

Other major suppliers — the US, Russia, Algeria — are already producing at or near capacity. There is no spare tap to turn on. And new facilities can’t come up overnight. New helium extraction infrastructure requires us to find the right geological formations, construct specialised processing facilities, and set up cryogenic supply chains. That’s a multi-year project.

Meanwhile, nothing replaces liquid helium for MRI cooling or semiconductor wafer cooling at the temperatures and conductivities required. The one partial mitigation that works is recycling — capturing and re-liquefying used helium rather than venting it. A well-designed recovery system can recapture up to 90% of helium that would otherwise be lost. But this infrastructure is expensive, and most facilities globally, particularly in lower-income countries, just Kdon’t have it.

What this means for India

India imports essentially all of its helium — there is no domestic production, and no strategic reserve. Consumption is driven primarily by healthcare, with a growing semiconductor and electronics manufacturing sector adding to demand.

India’s MRI market is valued at roughly $260–280 million. More than 90% of our machines, here, are conventional, imported systems, all of which run on liquid helium. A supply crunch means higher refill costs. Hospitals might absorb those costs, and pass at least some of it on to patients.

The more immediate risk is availability: if global helium allocation tightens, India, with no long-term supply contracts or strategic reserves, is near the back of the queue.

The semiconductor dimension of this problem, too, is growing. Most immediately, this will hit us as a shortage of chips. But we need to think hard about our vulnerabilities even beyond this episode. India is trying to develop domestic chip manufacturing capacity. As that happens, our helium requirements will increase structurally. In that sense, the current disruption is only a preview.

For now, the question is how long the conflict in the Middle East lasts. Every additional week that Ras Laffan stays offline makes the eventual supply crunch deeper and the logistics recovery longer. Hospitals that need helium to keep their MRI machines running, and chip fabs that need it to keep production lines going, are all watching the Strait closely.

Tidbits

[1] Sebi to review mutual fund distributor rules

Sebi has set up a working group to review rules for mutual fund distributors and reduce overlap with investment advisers. It also plans a common ad code and a digital platform “Sebi Setu” for easier compliance. The move comes amid concerns over falling numbers of registered advisers and rising influence of finfluencers.

Source: The Economic Times

[2] Reliance signs $3 billion green ammonia deal with Samsung

Reliance Industries has signed a $3 billion, 15-year deal to supply green ammonia to Samsung C&T starting FY29. The deal is among the largest globally and supports India’s push to become a major exporter of green fuels. It also strengthens Reliance’s clean energy ambitions.

Source: The Economic Times

[3] MakeMyTrip considers India IPO after Nasdaq listing

MakeMyTrip is exploring a potential listing in India as part of its long-term strategy, over a decade after listing on Nasdaq. The move could help raise capital locally and strengthen its presence in its core market. The plan is still subject to market conditions and approvals.

Source: Business Standard

- This edition of the newsletter was written by Kashish (Co-authored by Dinesh Pai) and Krishna.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I never thought of Helium from the conflict angle. Great read as always.

💯