Hi folks, welcome to another episode of Who Said What? I’m your host, Krishna. For those of you who are new here, let me quickly set the context for what this show is about.

The idea is that we will pick the most interesting and juiciest comments from business leaders, fund managers, and the like, and contextualize things around them. Now, some of these names might not be familiar, but trust me, they’re influential people, and what they say matters a lot because of their experience and background.

So I’ll make sure to bring a mix—some names you’ll know, some you’ll discover—and hopefully, it’ll give you a wide and useful perspective.

For all the sources mentioned in this video, don’t forget to check out our newsletter; the link is in the description.

With that out of the way, let me get started.

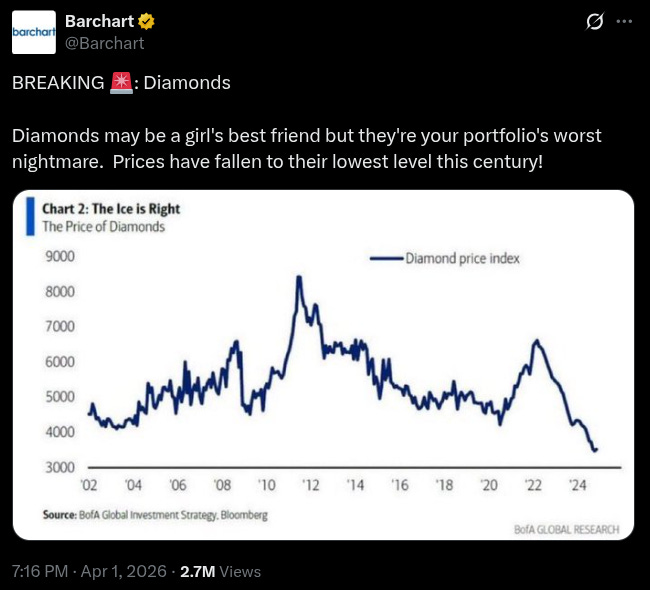

Things don’t look good in the diamond market

I came across this tweet yesterday.

It shows that diamond prices have fallen to their lowest level this century. And it reminded me that it’s been a while since we gave a proper update on what’s been happening with the diamond industry on this show, because quite a lot has happened since we last covered it. So today I want to catch everyone up and talk through a quote from Anglo American’s CEO.

But before that, let me give you some quick context.

A quick recap for those who are new

De Beers is the company that essentially invented the modern diamond industry as we know it.

In 1888, a British financier named Cecil Rhodes set it up with one specific goal — to control the global supply of diamonds so completely that prices could never collapse. The logic was elegant in a somewhat unsettling way: diamonds don’t have real intrinsic value, and when massive deposits were discovered in South Africa in the 1870s, they risked becoming worthless. So De Beers built a cartel that at its peak controlled nearly 90% of the world’s rough diamond supply, and paired that with one of the most effective marketing campaigns in history — “A Diamond Is Forever” — which convinced entire generations that a diamond ring was the only acceptable way to express lifelong love.

That cultural norm, which feels like it’s always existed, was manufactured by De Beers. We covered this in much more detail in one of our Daily Brief pieces if you want the full story.

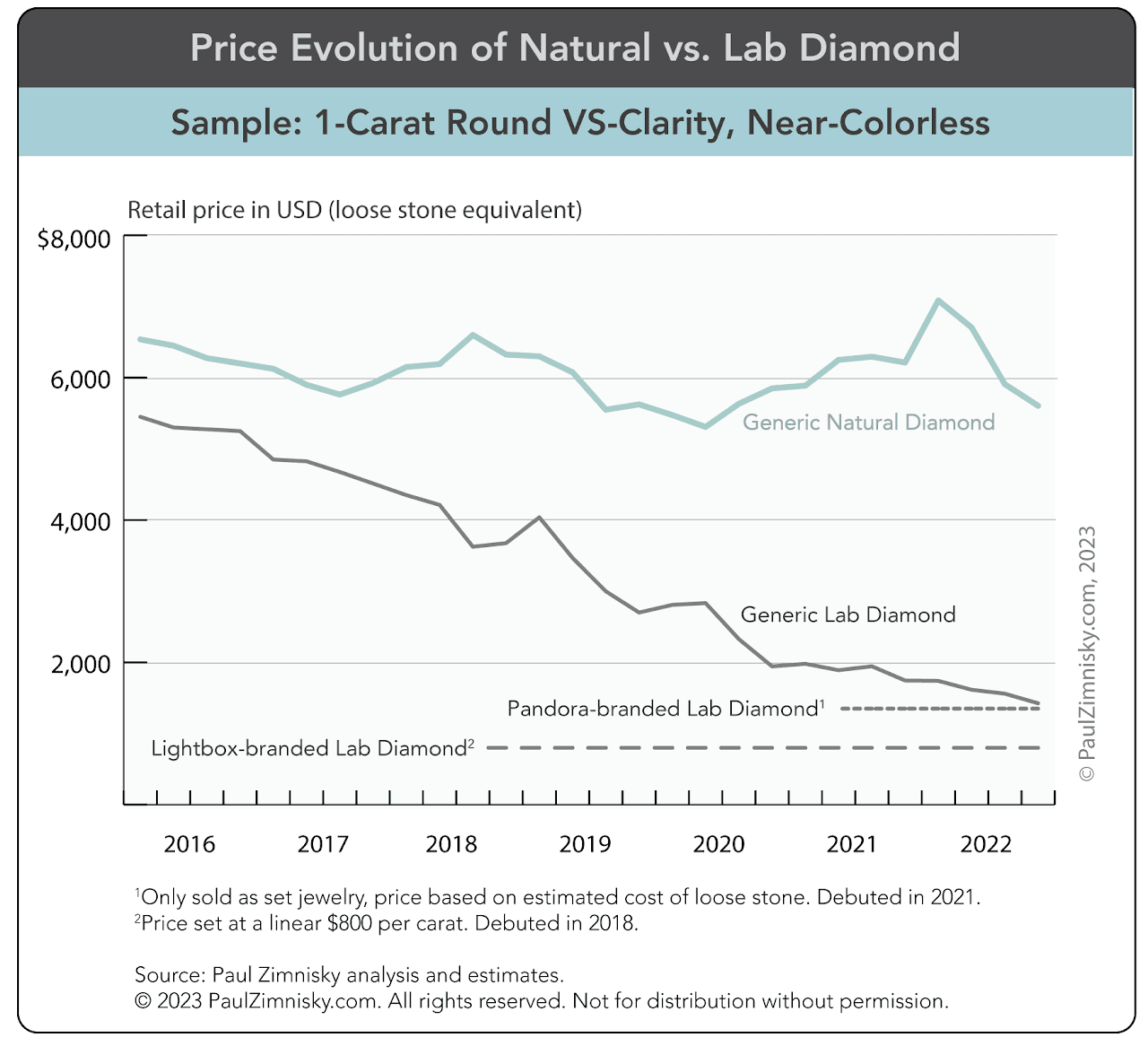

Then came lab-grown diamonds, and everything started unravelling. Scientists figured out how to grow diamonds in a laboratory — stones that are physically, chemically, and optically identical to mined ones, which a professional jeweller cannot tell apart without specialist equipment. Because they can be mass-produced, their prices collapsed. According to data tracked by diamond analyst Paul Zimnisky, a one-carat lab-grown diamond that cost around $5,000 in 2016 now costs under $1,000.

The American market shifted dramatically toward them, with more than half of all US engagement rings now carrying a lab-grown stone. China — the other great engine of global diamond demand — essentially exited the market, with Chinese diamond consumption falling from around 100 billion yuan in 2021 to just 43 billion yuan by 2024 as consumers moved toward gold instead. For a company whose entire model rested on manufactured scarcity, this was an existential problem, and the Barchart chart captures exactly what happened to prices as a result.

Anglo American and three straight years of writedowns

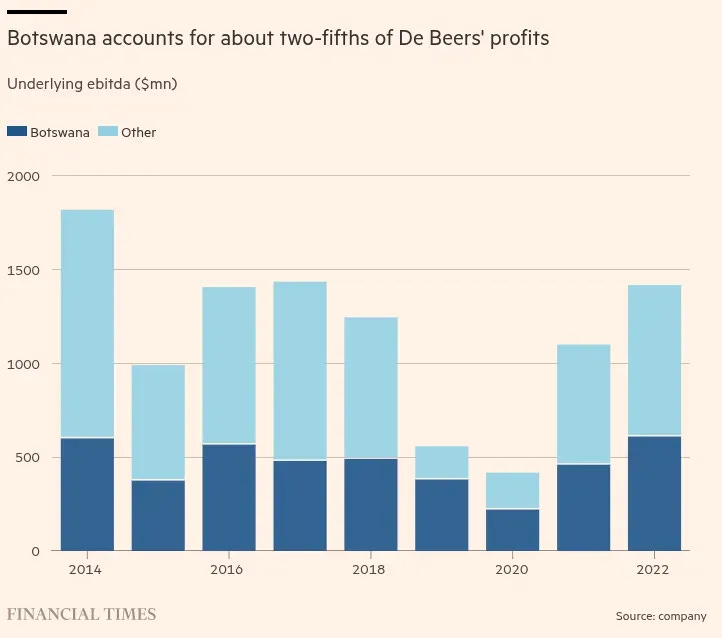

De Beers doesn’t operate independently — it’s 85% owned by a British mining giant called Anglo American, which most people haven’t heard of even though its products show up in virtually everything we use, from the copper in your phone to the iron ore in steel. The remaining 15% is held by the government of Botswana, which supplies roughly 70% of De Beers’ rough diamonds and has historically funded its schools and hospitals from diamond revenues.

As the market deteriorated, Anglo American started formally acknowledging on its books that De Beers was worth less than it had been carrying it for — what’s called a writedown. They wrote it down by $1.6 billion in 2024, by another $2.9 billion in early 2025, and by a further $2.3 billion this past February, bringing the total across three consecutive years to $6.8 billion. Anglo has also put De Beers up for sale since 2024, wanting to refocus on copper and iron ore, but the sale has been complicated because potential buyers are valuing the company at far less than even its already-slashed book value.

It was after announcing this third writedown that Anglo’s CEO got on a call with journalists and said something I found quite remarkable. When asked whether things would get better from here, he said: “I certainly hope this is a low point.“ Not I believe, not the fundamentals support a recovery. Just hope. From the CEO of one of the world’s largest mining companies, after three straight years of writing down the same asset by a combined $6.8 billion, the best he could offer was that he hoped it had stopped getting worse.

What the sightholder cuts are really saying

Alongside the writedown, something else happened last month that tells the story even more clearly. De Beers quietly informed more than 20 of its 69 so-called sightholders that their contracts would not be renewed when current agreements expire in July, reducing the list to roughly 45 names. A sightholder is essentially a member of the exclusive club De Beers built to control how rough diamonds flowed through the market. De Beers has never sold diamonds on an open exchange — instead, ten times a year, it invited approved buyers to receive a parcel of rough diamonds. You didn’t choose what was in the parcel, you didn’t negotiate the price, you took what De Beers gave you and paid what De Beers asked, and you felt fortunate to be included. Banks extended credit to sightholders. Manufacturers sought them as partners. The list itself was a signal of standing in the industry. In the 1970s, it had over 350 names on it. Then it fell to 69. And now it stands at roughly 45. From 350 to 69 to 45 — that is the contraction of the natural diamond industry in three numbers.

The surface explanation for the cuts is that De Beers is producing fewer diamonds and needs fewer buyers, having reduced its 2026 production guidance to 21–26 million carats from a previous estimate of 26–29 million. But the deeper reason it’s producing less is that it’s sitting on approximately $2 billion worth of unsold rough diamonds it cannot move — levels not seen since the 2008 financial crisis — because demand for natural stones has simply fallen away. The sightholder cuts are not a tactical adjustment while the company waits for things to bounce back. They are De Beers getting honest about the actual size of the business it now has.

Even Botswana is backing down

There’s one more thing that completes this picture.

When Anglo put De Beers up for sale, Botswana’s president Duma Boko was unambiguous about what he wanted — not a larger stake, but control. His exact words were: “It’s our people who are running this country, and we said we want De Beers, and we are going to take it.“ A few weeks ago, The Economist reported that Botswana has now quietly dropped that position, and is pursuing “at least 25%” — a minority stake. An executive at Debswana, the joint venture between the Botswana government and De Beers, told the publication: “It probably doesn’t make sense to go all out.” The fact that even the country which mines most of De Beers’ diamonds has pulled back from the idea of taking control tells you something about how people closest to this business actually feel about its trajectory.

What India means for all of this

The bull case for natural diamonds runs mostly through India. De Beers CEO Al Cook said in January that India grew 11% in natural diamond demand in 2025 — the strongest of any country in the world — and has overtaken China to become the world’s second-largest market after the US. Cook argues that Indian consumers understand the difference between natural and lab-grown, and tend to prefer the real thing for occasions that carry emotional weight. And beyond consumption, Surat is where more than 90% of the world’s diamonds are cut and polished, making India the backbone of the entire supply chain. We covered Titan’s recent entry into the lab-grown space after years of holding out, but that was targeted at the everyday fashion segment — the premium natural diamond category remains relatively insulated in India for now.

But what the sightholder cuts tell you is that De Beers is not waiting for the India story to fully play out before restructuring. It is building its business today for the smaller market that exists today. Forty-five elite buyers, $2 billion of unsold inventory, a third consecutive writedown, and a CEO who, when asked whether things will improve, says he hopes so. The ice, as the Barchart chart makes clear, is still very much melting.

That’s it for this edition. Thank you for reading. Do let us know your feedback in the comments.

Lab-grown diamonds' retail price may be $1000 per carat. My sister's business procures them at 90-100$ per carat.

It's gonna get even cheaper as production ramps up

Shared the article with my girlfriend. Thank you, Zerodha writer!