Can the pharmacy of the world test its own medicine?

India’s infrastructure for clinical trials…needs a checkup.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Can the pharmacy of the world test its own medicine?

What is plastic, actually?

Can the pharmacy of the world test its own medicine?

On April 2 — the first anniversary of his infamous “Liberation Day” — Donald Trump signed an executive order slapping 100% tariffs on most patented drugs imported into the United States. Briefly, we wondered if this was yet another barb hurled at India’s economy. But then, as the Global Trade Research Initiative clarified, India is “largely shielded.” After all, most of our pharmaceutical industry doesn’t make patented drugs at all.

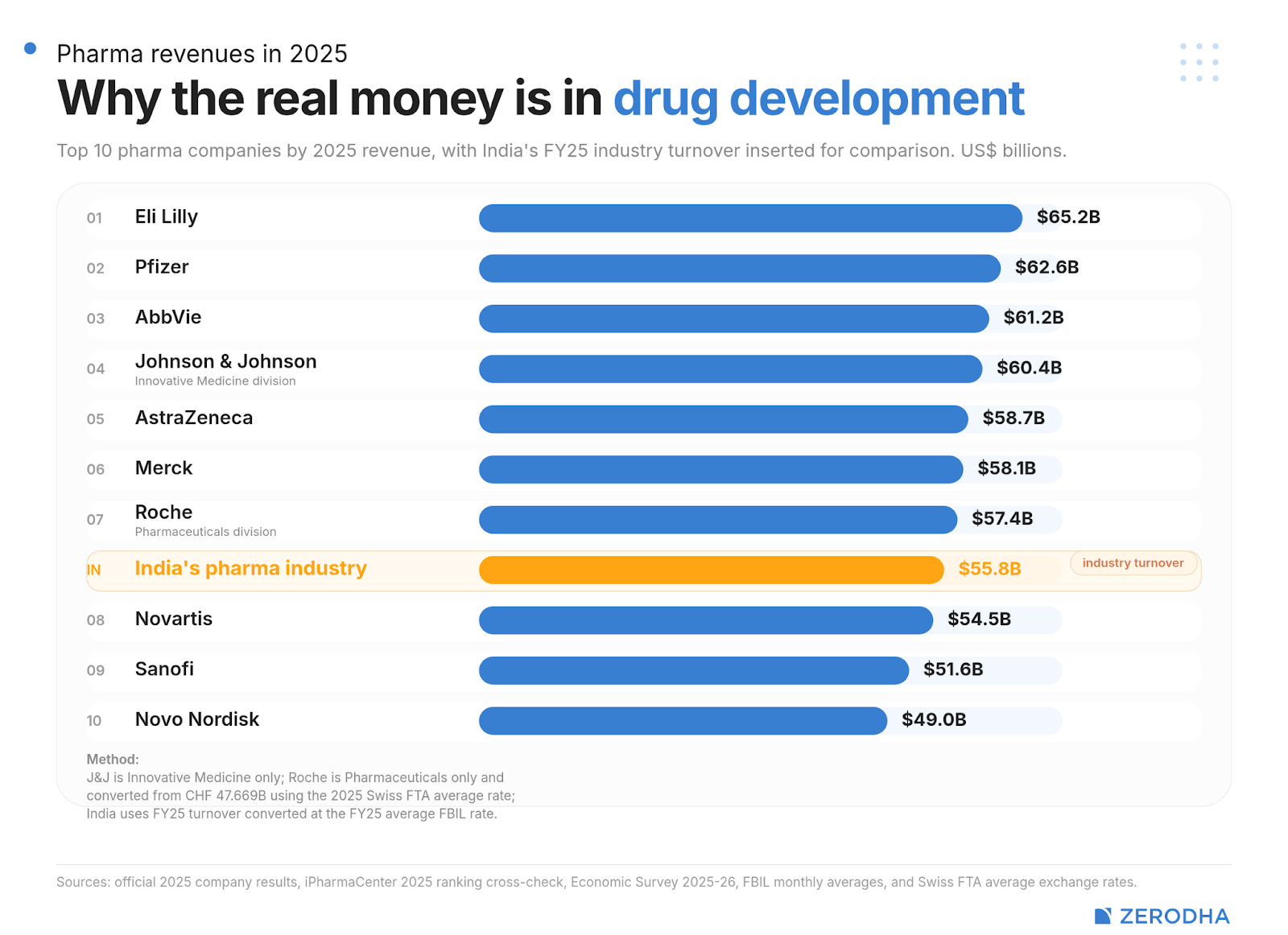

We manufacture generics. India sold over $10 billion of pharmaceuticals to the US last year, nearly all of which were copies of drugs that someone else invented.

For now, this fact might have helped us somewhat escape a geoeconomic threat. But it also points to a ceiling. The entire Indian pharmaceutical industry earned $55 billion last year. Merck, a single pharmaceutical innovator, made $58 billion in pharma sales around the same time. That’s the difference between manufacturing a drug and developing one.

One thing keeping us stuck manufacturing is a gap in clinical trials. For all its many advantages, India lacks the muscle for testing new medicines.

The birth of a medicine

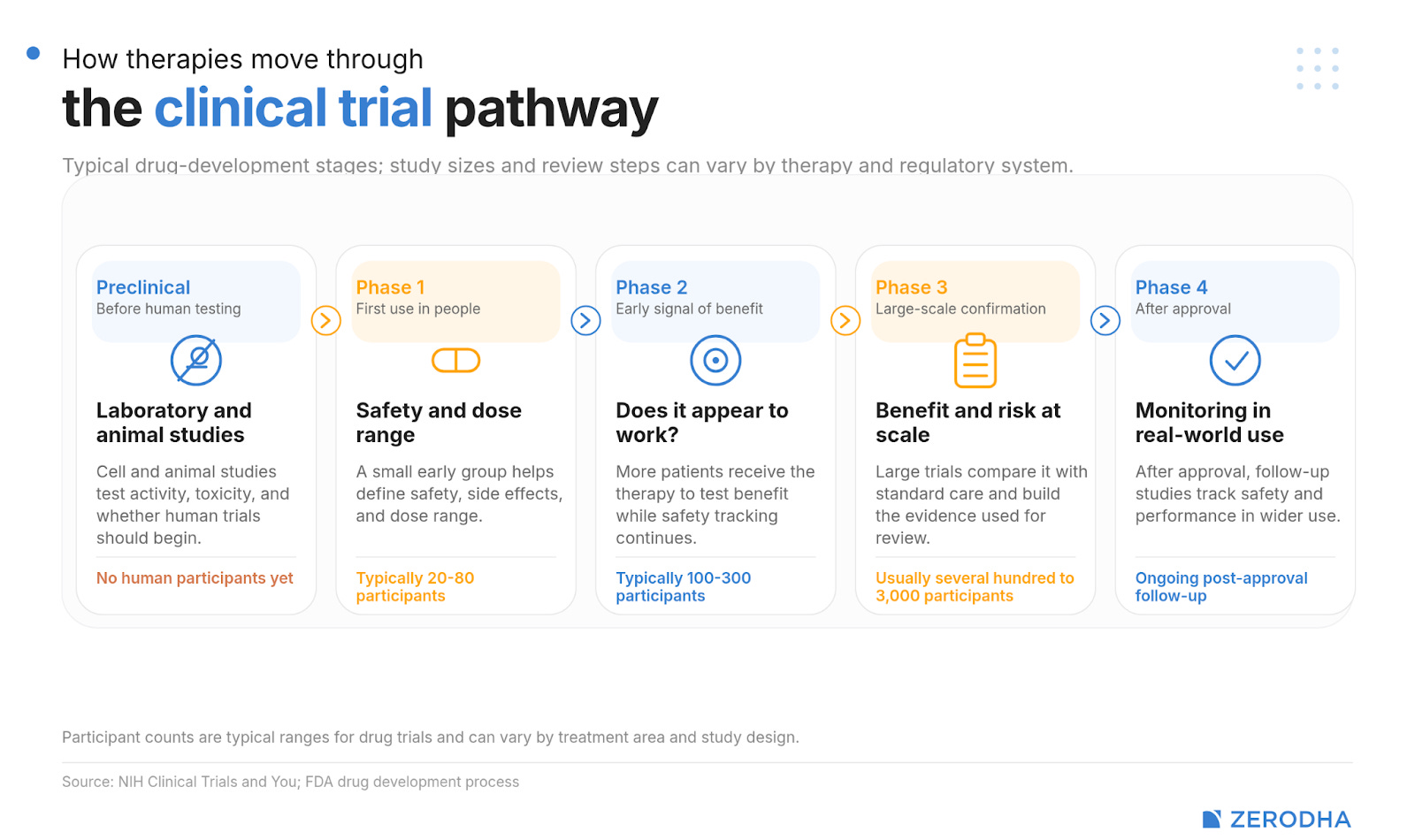

Imagine a researcher who finds a molecule that might just cure a disease we never knew we had a chance against. So far, though, they’ve only seen how it works in animals. Now comes the last and most expensive leg. They need to know: Is it safe for people to use? At what dose? Are there side effects that only show up in one in a thousand people? Does it do anything that our existing medicines can’t?

This is when they start clinical trials.

They start small. The first phase is a small safety test — they test the molecule on a few dozen people, who they watch closely. If those people seem alright, they can now move to the second phase, where they check if the drug actually works, and what the right dose might be. If the medicine works, things escalate. In the third phase, you graduate to testing the molecule in hundreds, or even thousands, of patients — comparing them to people on existing treatments.

Even in the best of cases, this is a long journey, and one prone to failure at many points. When you consider all those failures, globally, bringing a single new drug to market can cost almost $3 billion. Almost 70% of that cost is incurred in clinical testing, not chemistry.

Worse, still, is the time this costs. When things are ideal, bringing a drug to market is still a multi-year marathon. But faulty procedures can inflate that timeline considerably. And in drug development — an industry where the competition can span the world — a delay can mean irrelevance.

India and clinical trials

By registration volumes alone, India is the world’s third-largest destination for clinical trials. There are nearly 95,000 trials on our books. 18,000 of these were registered in 2024 alone.

There’s a catch, though. Most of these are late-stage trials, run by multinational companies that have already gone through several phases, and are closing into a commercially viable drug. All they need, now, are bodies. India serves these companies as a service layer. We have a vast patient pool, and per person, costs can be half of what they are in the developed world.

This doesn’t, however, make us a quality drug testing nation.

Where we lag

For all our pharmaceutical successes, we’re struggling to become the sort of country where someone can develop a molecule, test it, and bring it to market. For the thousands of trials registered in India, between 2008 and 2022, only 220 first-in-human Phase I trials were conducted in India. China, in contrast, runs over a thousand every year.

Consider the case of PopVax, a fascinating new-age Indian mRNA start-up from Hyderabad. The company designs its molecules in India, and runs its factory here. For clinical trials, however, the company had to rush to Australia.

This isn’t because of costs. The lab work, itself, is fairly cheap in India. But it simply takes too much time to get through.

What do we lose, though? Can’t we simply piggy-back on other country’s data — using drugs that have already worked in America or Japan?

Not really. For one, there’s no guarantee that Indian bodies behave the same as Western or East Asian populations. We have at least eight major genetic variations that change how we respond to medicines. A dose that works in Philadelphia may not be the right dose in Patna.

More importantly, there are many diseases that Indians are uniquely exposed to. More than a quarter of the world’s tuberculosis cases, for instance, happen in India. We also have more than a third of the world’s oral cancer cases. If we want to fight such diseases, we’re the ones that will have to develop the medicine. No other country will step up to do it for us.

The issues we face

What is holding us behind?

If you’re trying to create a new drug in India, there is, on paper, a straightforward process in front of you. You file an application with the CDSCO. According to the law, it has to respond to your application within 30 working days if your drug has been developed domestically, and 90 for those already approved abroad. In theory, if the regulator doesn’t meet these timelines, you’re deemed to have approval.

But the thing is, the clock can reset with a communication: even if the regulator neither accepts nor rejects one’s application.

The thing is, before the CDSCO actually gives its approval, it often sends applications to a Subject Expert Committee. This wasn’t always the case; things used to be more liberal before. These institutions were created after 2013, when the Supreme Court hauled up the CDSCO for lapses in clinical trials. However, this created a new problem. According to PopVax founder Soham Sankaran, there’s often a single Subject Expert Committee for any area of medicine, and that can become a bottleneck. Instead of weeks, as the law prescribes, applications are routinely stuck for half a year at this stage.

That isn’t all. Once the CDSCO gives its green light, you then need to go to an ethics committee to get your protocols approved. This is extremely important; these trials are being conducted on real people, many of them in desperate situations. Sloppiness, here, can cause severe harm. But the process also adds a few extra months. Other countries, like the United Kingdom, get around this by letting the regulatory and ethics review run in parallel. We do not.

The result? If you apply to test a promising molecule in January, it is already September by the time your first patient walks through the door.

This creates a tax on any Indian innovator that wants to test their medicines here. It also keeps India from becoming a destination where foreign pharma companies can carry out their own trials. While India wants to become a global contract research powerhouse — the way China is — as a report from the Department of Pharmaceuticals noted, our glacial timelines make us “non-starter for foreign companies exploring India as a destination for clinical trials.”

A trade-off? Or dysfunction?

It’s fair to argue, of course, that you don’t want too liberal a policy when it comes to testing new medicines. New drugs can come with terrible risks, and we don’t want to take those lightly. What is a sacrifice of a few months, if we can be more careful in ensuring that nobody is hurt?

The problem, however, is that our clinical trials themselves are still not robust.

Ideally, there are two big checks on a clinical trial. One, the trial is supposed to be monitored while it’s underway. Two, when it ends, the results are supposed to become public. Neither works well in practice.

No regulator can actually monitor how every single clinical trial is being conducted. That job goes to ethics committees. These committees, which are put together by institutions like hospitals or medical colleges, are supposed to check things like patients properly consented to a trial, the necessary protocols were followed, problems were reported, and so on.

In practice, though, these checks are loose at best. Many committees are passive, relying on reports that the investigators give them instead of checking a site for themselves. Many members, in fact, aren’t even trained to do so. Studies suggest that when they do visit, the problems can be severe.

We run into a similar problem with reporting results. Every clinical trial is supposed to be registered on the Clinical Trials Registry of India, or CTRI, where it must eventually record whatever it finds. That’s how the world finds out about how things have panned out. If a drug doesn’t work, or worse still, if it puts patients’ lives at risk, that negative result needs to be public.

In practice, though, one in every eight trials aren’t registered with the CTRI. And of those that do, more than three of every four never report what they found.

In effect, for all the blockages in our clinical trials systems, once a trial is underway, we barely have a sense of what is happening.

India’s fixes

The government understands that clinical trials have become an issue. There are recent indications that we’re moving towards reform.

This January, the government made sweeping changes to the law around clinical trials. It removed the licensing requirements for making small quantities of a drug for examination, research, or analysis. It also cut down various timelines.

A month later, Finance Minister Nirmala Sitharaman announced the “Biopharma SHAKTI” scheme as part of her budget speech. The plan, here, is to allocate ₹10,000 crores over the next five years — with three big goals: creating more than a thousand accredited clinical trial sites across India, setting up new pharmaceutical research institutes, and creating a dedicated scientific review cadre at the regulator.

Will these eventually work? The answer, to our eyes, depends on whether we’re simply suffering from inadequate capacity, or whether there’s a structural problem — where the centralized gating mechanism we’ve put together will eventually be overwhelmed, no matter how many people we staff.

One way or another, the answer will be with us soon enough.

The cusp of a revolution

This is a critical moment. With AI proliferating, we are at the cusp of a revolution. New technologies are compressing drug design from years to months. India could ride that wave — we have both the computer science talent and the biologics expertise to make the most of this moment.

Only, if all those new molecules will have to wait for over a year to be tested, they’ll probably be tested elsewhere.

Other countries understood this before us. Consider China. Under its investigator-initiated trial framework, many first-in-human trials don’t need regulatory approval, early on. If there are two equally capable labs in India and China that are working on a similar drug, the Chinese lab is likely to have Phase II data ready by the time an Indian lab can even begin testing on actual patients. As a result, the number of trials they carry out is an entire order of magnitude higher than we do. It’s partly why they’re attracting billion-dollar contract research deals from global pharma companies.

We aren’t destined to be stuck here either. During COVID-19, trials would frequently be approved within a month in India as well. We let that progress go in the post-COVID years. But if we can get it back, there’s a multi-billion dollar opportunity waiting for us as well.

What is plastic, actually?

Since the Hormuz crisis began, we’ve been tracking what’s happening to oil. Crude at $120, LPG shortages, the IEA releasing 400 million barrels from strategic reserves. But one downstream effect that hasn’t gotten enough attention is what’s happening to plastics.

Polymer prices surged over 40% in a matter of weeks. Naphtha — the key raw material for most of the world’s plastic production — nearly doubled in price. Indian PVC prices jumped 78% in a single month.

In the US, analysts at CreditSights reported that spot markets for polyethylene “barely function” because price offers by sellers expire within hours as buyers scramble to lock supply at prices unthinkable just weeks ago. Asian factories that make plastic are shutting down and American ones are running at maximum capacity to fill the gap.

And in the midst of all this, we had to admit something: we don’t actually understand what plastic is. We used terms like polymer, naphtha, PVC, and polyethylene above, without actually knowing what each of them meant.

Every time plastic comes up in conversation, the explanation starts with crude oil. It’s a neat, linear supply chain story. But it’s a bit like explaining what a cake is by starting with the wheat farm. It tells you where the ingredients come from, but nothing about what a cake actually is.

So we went back to the beginning. And the beginning, it turns out, has nothing to do with oil.

Building blocks

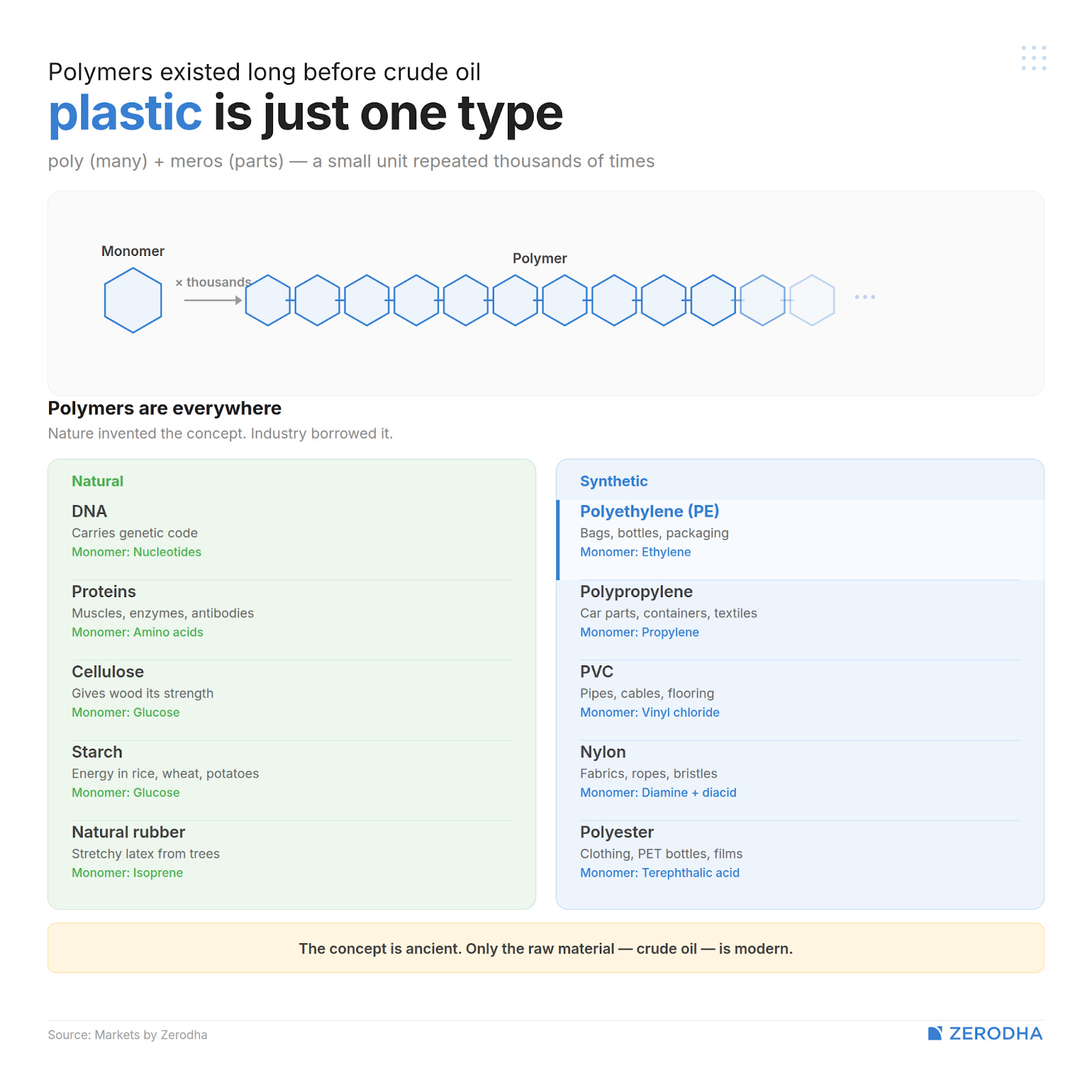

Plastic is a type of polymer. But so is DNA. So is protein. So is the cellulose that gives a tree trunk its strength. The concept of a polymer is one of the most fundamental structural ideas in the universe — and it existed long before anyone drilled for crude oil.

So what is a polymer? The word itself tells you: poly means “many” + meros means “parts”. It is a very long molecule made by repeating a small unit — called a monomer — over and over, thousands of times. This process of linking monomers into a polymer is called polymerization. If the monomer is amino acids, protein is the polymer. A long chain of nucleotide monomers is what we call DNA. And a chain of ethylene or propylene is what would make plastic.

What makes polymers extraordinary is that the arrangement of these chains determines the material’s behaviour. Straight, tightly-packed chains usually result in a rigid, hard material. If the chains branch randomly, the material becomes soft and flexible. Cross-link the chains into a web, and the material becomes heat-resistant and tough. This is why some plastics are stretchy like a carry bag, rigid like a pipe, transparent like a water bottle, or brittle like thermocol.

That’s all plastic fundamentally is: long chains of small (very specific type of) molecules, whose arrangement determines their properties. Everything else — the oil, the refinery, the cracker — is a question of where we get those small molecules from.

Yet, those small molecules manifest themselves everywhere.

The carry bag, the milk pouch from this morning — that’s polyethylene (PE), the most produced plastic on earth. The food container you just microwaved lunch in uses heat-resistant polypropylene (PP). The pipes carrying water, window frames, wiring insulation in your building comes from PVC. You’re probably familiar with PET, used commonly in water bottles. Melt that and spin it into fibre, and it becomes polyester — your “plastic” bottle and your “polyester” shirt are, at a molecular level, the same thing. The disposable cup from the chai stall, the thermocol around your new TV — that’s polystyrene.

These five, along with polyurethane, account for roughly 75-80% of all plastic produced worldwide.

How we ended up using oil — and why that choice now haunts half the world

The first plastics were actually not made from oil at all.

Celluloid, invented in the 1860s, was derived from plant cellulose. Bakelite, the first fully synthetic plastic, was created in 1907 from chemicals that had nothing to do with petroleum refining.

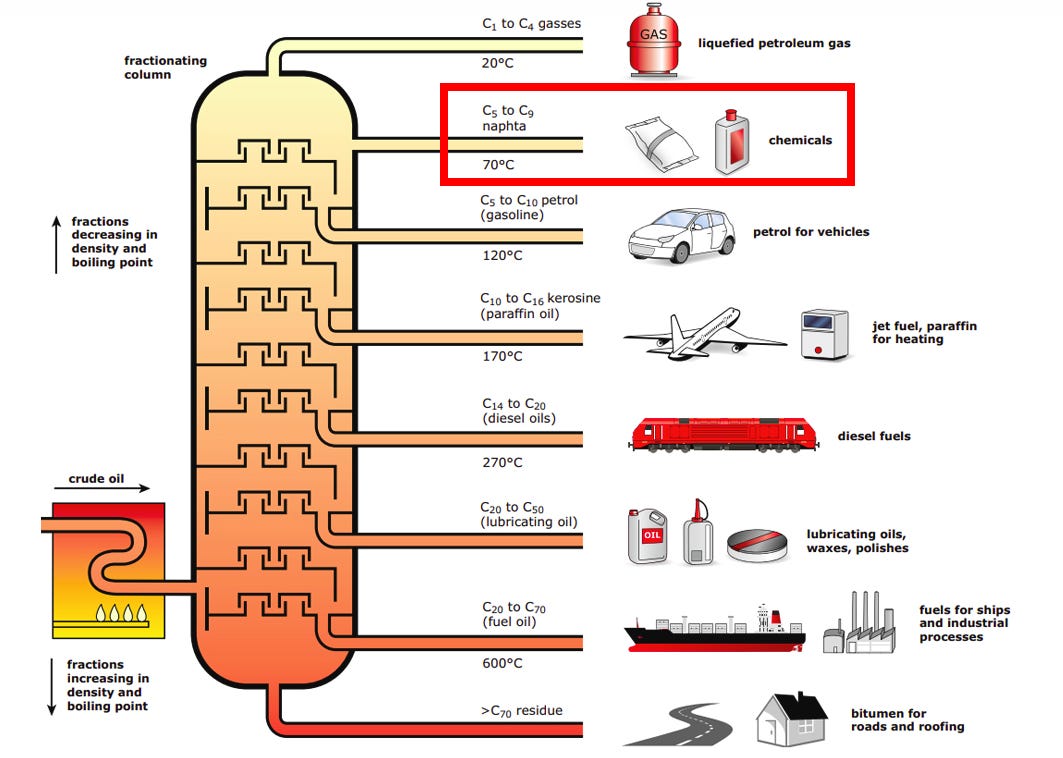

But hydrocarbons turned out to be spectacularly convenient. Oil refineries were already producing naphtha as a byproduct of making petrol and diesel. We went into the details of it in our oil primer.

In fact, naphtha, when heated to extreme temperatures, could be “cracked” into small molecules like ethylene and propylene — which happen to be ideal monomers for polymerization. They were cheap raw materials with an abundant supply and simple chemistry. The economics were irresistible, and by the mid-20th century, virtually all plastic production had shifted to petroleum-based feedstocks.

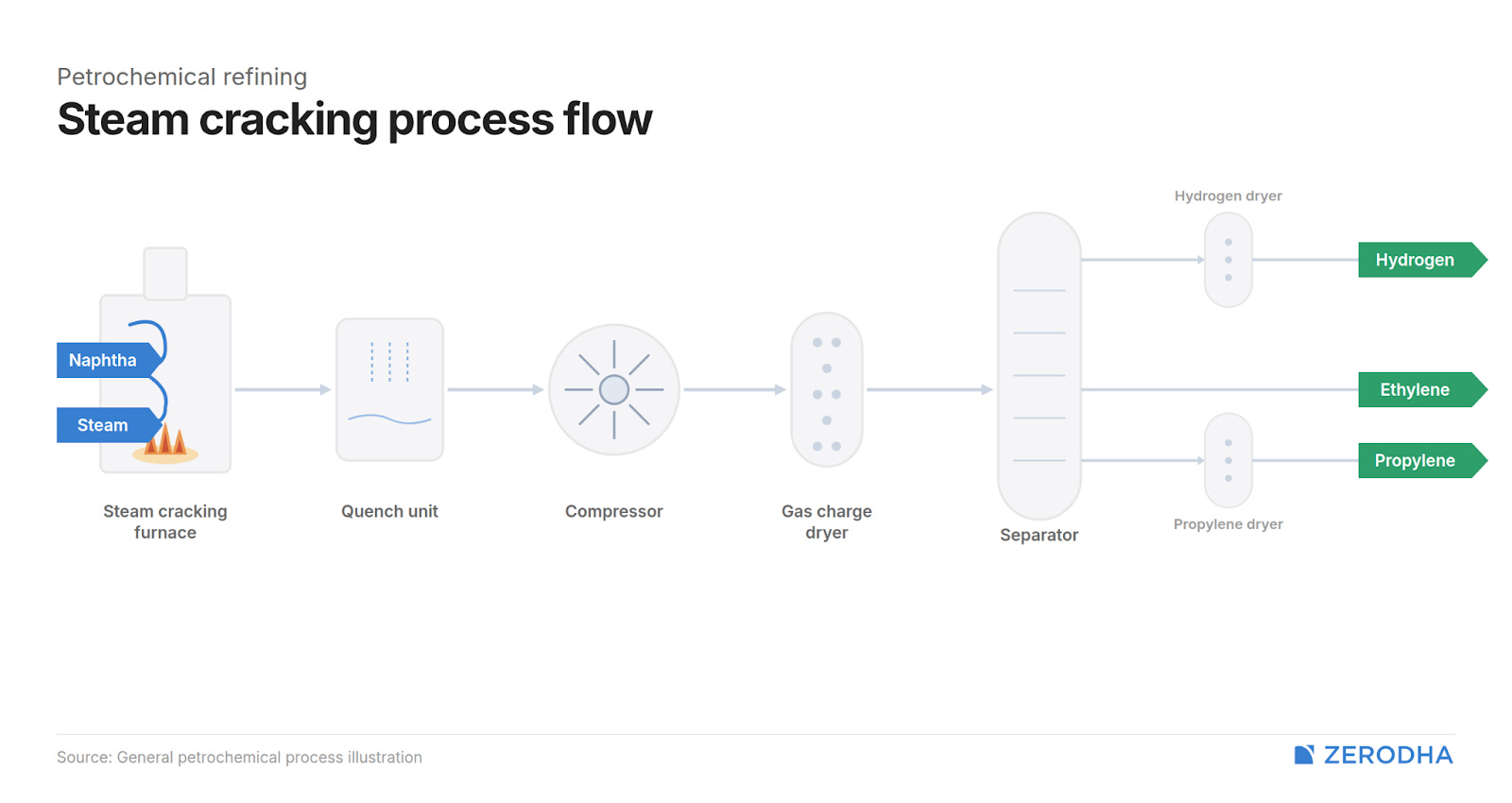

The industrial heart of this process is the steam cracker — one of the most energy-intensive machines on earth. Here, naphtha is mixed with steam and blasted through reactors at 800-870°C for mere milliseconds, then quenched instantly to freeze the output. This thermal shock breaks apart the heavier hydrocarbon chains in naphtha into ethylene, propylene, and butadiene. A single world-scale naphtha cracker needs roughly 3.3 tonnes of naphtha to produce 1 tonne of ethylene.

Naphtha isn’t the only way to get ethylene, though. You can also crack ethane, which is a byproduct of natural gas. An ethane cracker is more efficient — a ton of ethylene only needs 1.3 tonnes of ethane. Over the last 15 years, the US shale revolution flooded America with cheap domestic natural gas, and with it, cheap ethane. American petrochemical firms rebuilt their entire infrastructure around this feedstock — extracted from American soil, with no tanker, no ocean, and no external chokepoint.

Asia and Europe, meanwhile, stayed on naphtha, which comes from crude oil. That, of course, mostly comes from the Middle East, where the Strait of Hormuz is located.

When Hormuz effectively closed, naphtha prices surged 74% in two weeks. The raw material costs more than polyethylene itself — you lose money on every tonne you produce. That’s why Asian crackers started going dark.

American ethane crackers, meanwhile, are having the time of their lives. Their feedstock cost sits stable, because US natural gas prices haven’t spiked. They’re running at near-maximum capacity and shipping to Asia to fill the void left by shuttered Asian production.

Oil doesn’t have to necessarily define plastic. It’s just the most economically efficient source of the monomers plastic needs. If we found a cheaper way to get ethylene, the resulting plastic would be chemically identical.

Pellet economics

Every plastic product in the world begins as a small, translucent pellet about 2-5mm in diameter, called a nurdle. That’s the start of the plastics value chain. A PE nurdle looks nearly identical to a PP or PVC nurdle. But they’re entirely different materials, destined for entirely different products once melted and shaped.

Converters — which are the companies that turn pellets into products — buy these nurdles and process them. Before a pellet becomes a product, it’s almost always blended with additives to make it suitable for certain use cases. For example, plasticizers make rigid PVC flexible enough for medical tubing.

A handful of giant, vertically integrated companies operate the refinery-cracker-polymer complexes that produce these pellets. Reliance’s Jamnagar, for instance, is both the world’s largest refinery and one of its largest cracker sites — crude oil enters one end, plastic pellets exit the other. Add IOCL, GAIL, OPaL, and Haldia Petrochemicals, and you’ve covered the bulk of India’s upstream polymer capacity. Reliance alone controls roughly 50% of India’s capacity.

But, at the bottom end of the value chain, the conversion industry couldn’t be more different. It is massively fragmented — India alone has 30,000-50,000+ plastic processing units, and 85-90% of them are MSMEs. A plastic injection molding setup can start at ₹10-20 lakh. The barrier to entry is low, but these small converters are entirely dependent on a handful of upstream giants for their raw material. When polymer prices spike, they get squeezed.

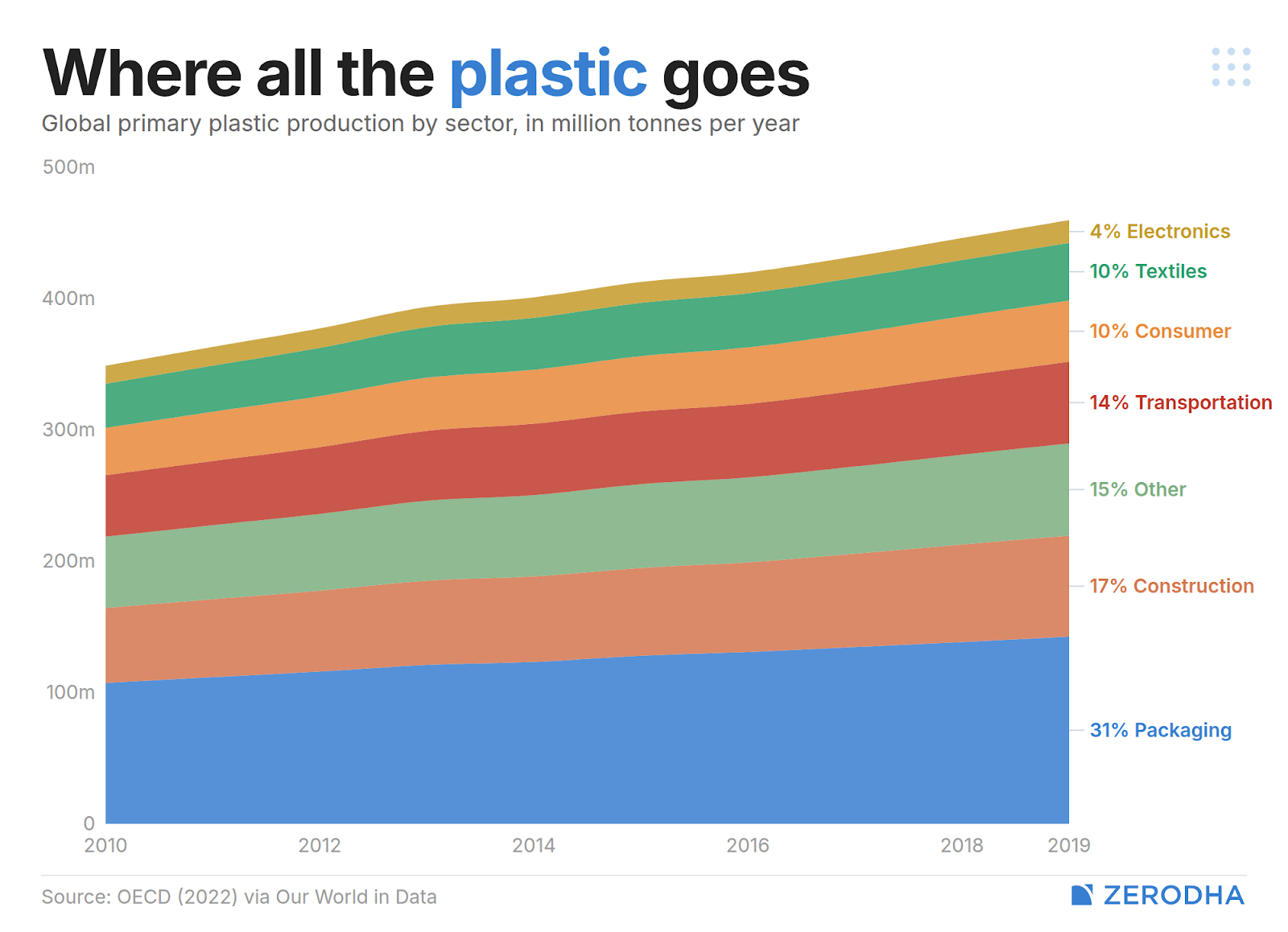

The demand side, meanwhile, is enormous and growing. Packaging consumes over 30% of all plastic produced. Construction takes roughly 20%, driven by government infrastructure pushes. Automotive accounts for about 15%.

India consumes just 11-15 kg of plastic per person per year. The US, in contrast, is at 139 kg, and the global average is 28 kg. With 1.4 billion people, even modest per capita increases mean enormous volume growth. The growth story and the plastics waste story, as it turns out, are often the same story.

The material that refuses to die

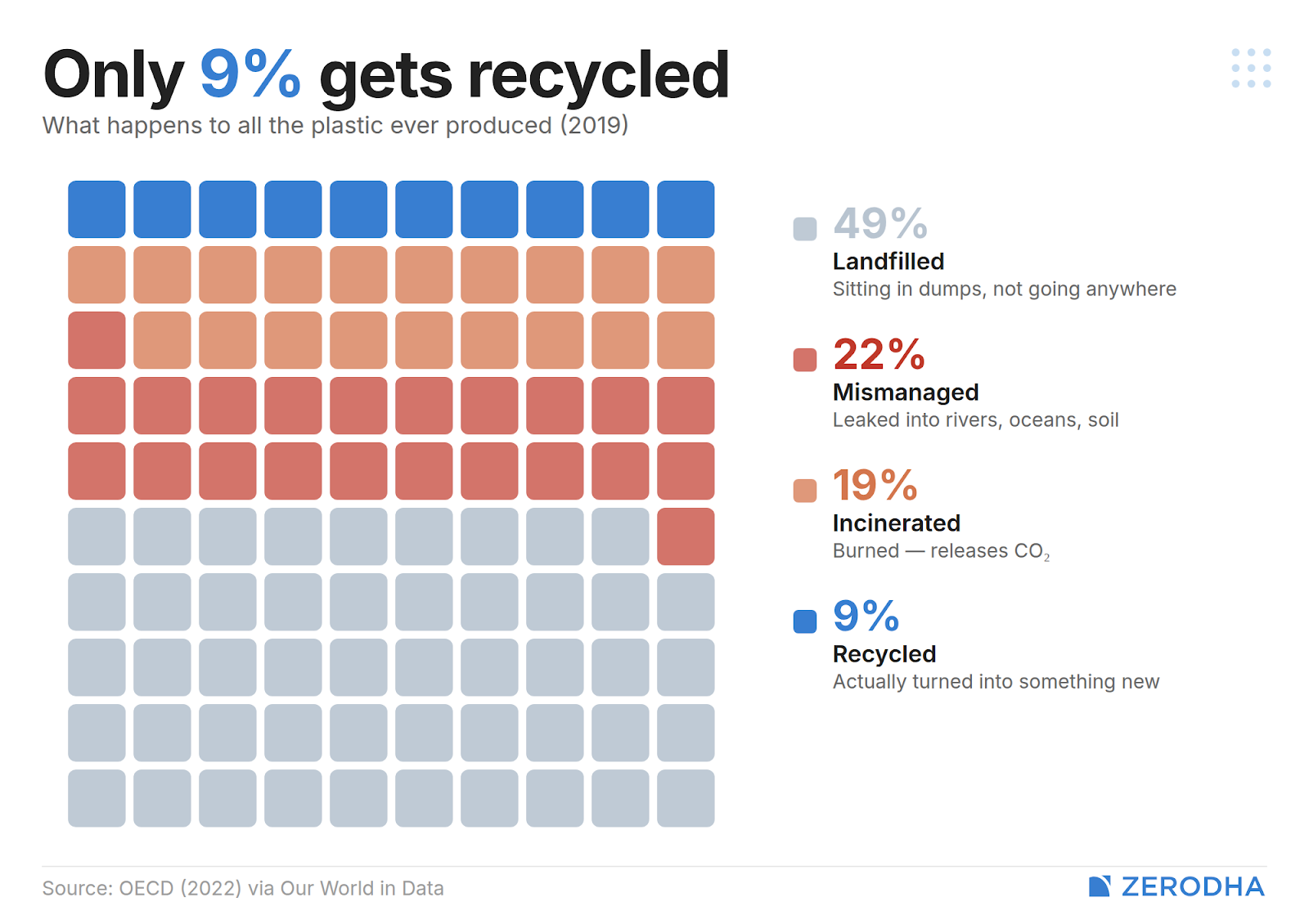

Ironically, the same molecular property that makes plastic so useful — the strong backbone that resists heat, chemicals, water, bacteria, UV radiation, and virtually every form of natural degradation — is exactly what makes it nearly indestructible as waste.

Only 9% of all plastic ever produced has been recycled, while 71% has accumulated in landfills or the natural environment. And more than half of all plastic ever made was produced in just the last two decades. We are early in this accumulation curve.

The problem isn’t technical but economic. The price of new (virgin) plastic is a function of crude oil. When oil is cheap, producing new plastic is cheaper than recycling it. In Europe, recycled PET trades at roughly €1,800 per tonne, versus €1,000 for virgin PET. Without mandates or carbon pricing, no rational manufacturer would choose recycled plastic. The entire recycling industry’s commercial viability is hostage to oil prices.

That creates a strange paradox: the Hormuz crisis, by making virgin plastic expensive, may have provided a huge silver lining for the recycling business. Something similar could be said for clean energy.

Even when recycling does happen, it’s not really a cycle — it’s a downward staircase as far as quality is concerned. See, polymer chains degrade with each pass through the melt, and its mechanical properties weaken. A PET bottle gets recycled into carpet fibre or fleece, which then cannot be recycled further. This is less recycling, more downcycling.

India’s recycling story, though, is more interesting than most. We claim a plastic recycling rate of roughly 60% — dramatically higher than the US at 5-6%.

This isn’t because of government infrastructure or civic awareness, though. Between 1.5 and 4 million people — ragpickers, kabadiwalas, small-scale aggregators and recyclers — make their livelihood from plastic waste. Ragpickers collect recyclables from streets, bins, and dumpsites, earning ₹100-500 a day. Kabadiwalas go door-to-door, buying materials by weight. Aggregators sort, clean, and bale. Small recyclers convert the material into pellets that re-enter the supply chain.

Where this leaves us

Only 4-6% of all crude oil produced globally ends up as plastic. But that small slice has created one of the most useful, most ubiquitous, and most environmentally persistent material families in human history.

The Hormuz crisis has exposed the full chain — from a barrel of crude passing through a narrow strait, to a naphtha cracker, to a polymer pellet, to a converter who moulds it into a bottle cap, to a sachet in a kirana store that no one knows how to recycle. Understanding what plastic actually is, is the first step to understanding why it’s so hard to replace.

Tidbits

Indian manufacturers are facing a 20-30% jump in raw material costs even after the ceasefire. The dollar has risen over 12% this year, electronics components priced in USD have gotten sharply more expensive, and working capital cycles are stretching. Industry executives expect 5-8% consumer price hikes across categories by Q2.

Source: Business Today

Assam, Kerala, and Puducherry voted today in single-phase assembly elections across 296 seats. Turnout was strong: Assam at 84.4%, Puducherry at 86.9%, and Kerala at 75% by 5 PM. Results for all five states (including Tamil Nadu and West Bengal, which vote later this month) will be declared in May.

Source: BBCSEBI has given a one-time breather to listed companies struggling to meet minimum public shareholding norms. The regulator won’t initiate penal action against companies with compliance deadlines between April 1 and September 30, 2026, effectively a six-month enforcement holiday driven by the market crash from the West Asia conflict.

Source: Economic Times

- This edition of the newsletter was written by Pranav and Kashish

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Why are you not on telegram; would have a channel in that app would bring in more eyeballs.

Indian is good for business because of late response of Governance. And big players masterd it.