India wants to switch from LPG to PNG

Can the WTO survive?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The shift from cylinders to pipes

Can the WTO survive the wilderness?

The shift from cylinders to pipes

If you have a piped gas connection at home but you’re holding on to an LPG cylinder as backup, the government has news for you: surrender it within 90 days, or lose your cooking fuel supply entirely.

That’s the essence of an order issued by the Ministry of Petroleum and Natural Gas, using powers under the Essential Commodities Act. Oil marketing companies — Indian Oil, BPCL, HPCL — will digitally map addresses and automatically block LPG cylinder bookings for any household where piped natural gas is available.

The trigger, of course, is the Iran War. India imports about three-fifths of its LPG, and roughly 90% of those imports transit the Strait of Hormuz — which has now been choked for the better part of a month. This caused cylinder shortages, 45-day booking gaps, and black-market prices of ₹4,000 per cylinder, forcing the government’s hand.

But India has 33 crore LPG connections and just 1.6 crore piped gas connections. That’s the gap this policy is trying to close — in months, not decades.

Two gases, two supply chains, one kitchen

LPG and PNG can seem the same. But they’re fundamentally different gases, with very different supply chains.

LPG, or liquefied petroleum gas, is a byproduct of oil refining and natural gas processing. It’s primarily propane and butane, compressed into liquid form, packed into those familiar red steel cylinders, and delivered to your doorstep. India produces only about 40% of the LPG it consumes. The rest is imported, most of which comes from the Persian Gulf.

Meanwhile, PNG, or piped natural gas, is primarily methane. It’s usually delivered in a continuous stream, through underground pipelines, at low pressure. Some of the gas comes from India’s own fields, operated by ONGC, Oil India, and the Reliance-BP joint venture in the Krishna-Godavari basin. This domestically produced gas comes under the ‘Administered Price Mechanism’, or APM — under which, the government allocates it at a capped price, to priority sectors — like households for cooking, CNG for transport, or fertilizer production. The rest is imported as ’liquefied natural gas’ (LNG), which arrives at coastal terminals and gets regasified into the grid. Overall, India produces roughly half the natural gas its PNG network consumes — marginally better than LPG.

In your kitchen, the two behave differently. LPG has roughly 2.5 times the energy density per cubic meter compared to natural gas. This creates a hot, intense flame that can be ramped up and dialled down quickly. Indian cooking is built around this: the split-second blast of heat for a tadka of spices, the sustained high flame under a kadhai of deep-frying oil, or the rapid toggle between high and low that a phulka demands.

PNG flame, on the other hand, is gentler and slower to respond. Electric induction, often suggested as a third alternative, suits us even less. It is highly energy-efficient, but hardly matches how most Indian kitchens operate. In fact, most of India’s existing cookware, too, doesn’t work on induction surfaces.

This creates friction; households are reluctant to switch away from gas cylinders. It’s expensive as well. Most Indians simply retrofit an LPG stove for PNG, by drilling out the gas jets. But this drops thermal efficiency, wasting gas and potentially producing unsafe carbon monoxide levels. A proper conversion requires an extra ₹2,000–5,000 to switching costs.

Why PNG over LPG?

But if these are two different fuels, which aren’t perfect replacements for each other, and both are imported, why is the government pushing so hard for PNG?

There are two reasons: both about how concentrated the risk is.

LPG’s import dependency is concentrated in a single chokepoint — the Strait of Hormuz. There’s almost no fallback. Unless the Strait is freed up, India can’t easily switch suppliers. The butane-heavy LPG blend most Indian households use is almost only produced in the Gulf. Other suppliers, like the US, produce a propane-heavy gas that doesn’t match India’s requirements without blending infrastructure, which we don’t have. There’s also a problem of time: even if India manages to secure US cargoes, those shipments can take 30–40 days to arrive, versus 7–8 from the Gulf.

Natural gas is different. We get half of it from India itself. For the rest, our sources are far more diverse. We have long-term LNG contracts with the US, Australia, and Qatar. That is, the closure of a single chokepoint doesn’t completely kill our ability to source gas.

In addition, India has essentially zero strategic LPG reserves. What we have, instead, is essentially just-in-time where gas flows directly from import terminals to bottling plants to consumers, with almost nothing stored in between. Our total underground LPG storage holds about 140,000 metric tonnes. We consume roughly 90,000 tonnes of LPG per day. That is, if our supply chains break down, the buffers will last less than two days. Compare that to crude oil, where India holds about 72 days of combined strategic and commercial reserves.

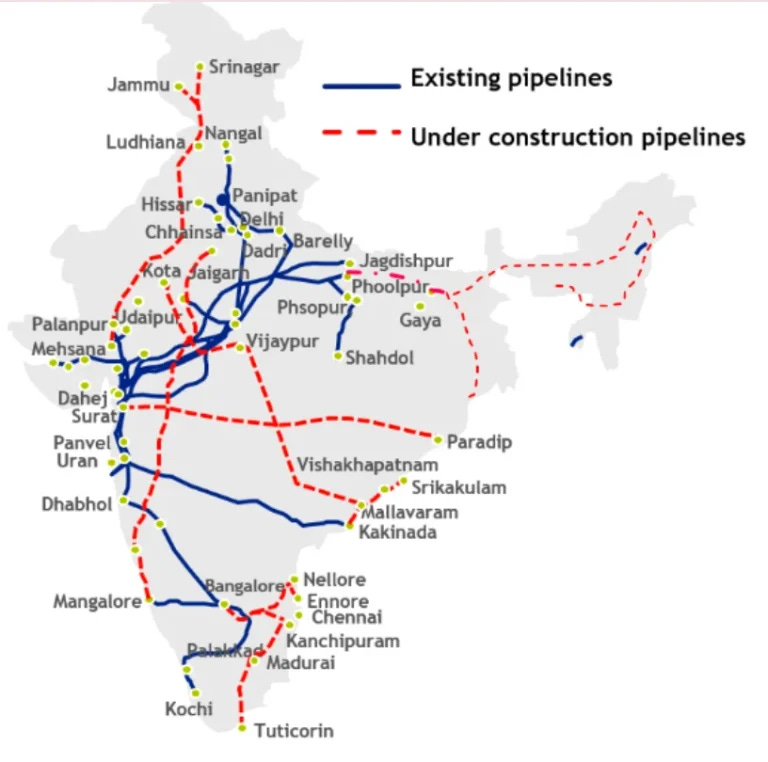

The infrastructure gap

None of this, though, means PNG is easy to scale. Building that fixed infrastructure takes years.

Modern city gas distribution in India really began in 2006, when the PNGRB (Petroleum and Natural Gas Regulatory Board) was established to regulate and auction distribution licenses. Before that, we only had metro networks — Mahanagar Gas in Mumbai, which began in 1995, and Indraprastha Gas in Delhi, which began in 1998. For the rest of the country, however, PNG has only been around for two decades.

A bureaucratic body, meanwhile, is different from physically delivering gas.

PNGRB’s network technically runs across 307 geographical areas covering 784 districts. On paper, that’s 98% of India’s population. The national gas pipeline backbone spans over 25,000 km, with another 10,000 km under construction.

That doesn’t mean, however, that most of India’s households get natural gas. Household PNG connections stand at just 1.62 crore as of December 2025 — roughly 5% of Indian households, and just 13% of PNGRB’s own target of 12.63 crore connections by 2034. Most of these are concentrated in western and northern India, which account for about 85% of all connections. The east has less than 5%. The northeast, less than 1%. Several states still have zero domestic PNG connections.

A lot of this comes from poor last-mile connectivity. To lay natural gas pipelines, you must dig through dense urban utility corridors already packed with water, sewage, electricity, and telecom lines. Piping old buildings is structurally hard. Renters need their landlord’s no-objection certificate for a connection. And even once installed, these connections underperform. Just ~63% of existing PNG connections are actually billing and live.

This is why our natural gas build-out has been excruciatingly slow. India added roughly 90 lakh PNG connections in the past five years, compared to a target of over 12 crore by 2034. To get there, we’ll have to accelerate to eight times our current speed. We might still get to the roughly 60 lakh LPG consumers who live in areas where PNG pipelines exist. Reaching anyone else, however, is a tall order.

The tariff reform behind the scenes

Before the March 2026 order, though, there was a much quieter reform from the PNGRB, that could make natural gas much more attractive.

Before 2023, the cost of transporting natural gas through India’s pipeline network was additive. That is, if gas from a coastal LNG terminal in Gujarat went through three separate pipelines owned by three different companies to reach a city in the north, the consumer paid a stacked transportation tariff for each pipeline. This created massive regional disparities: consumers near gas sources in Gujarat paid a fraction of what consumers in Bengaluru or Hyderabad paid for the same molecule. This made PNG unviable in distant markets.

The PNGRB introduced a unified tariff regime to fix this. The first phase, in April 2023, pooled pipeline revenues nationally and created three distance-based tariff zones. Then, in January 2026, the board collapsed this further into just two zones: Zone 1 — up to 300 km from gas source — and Zone 2 — beyond 300 km.

Interestingly, domestic PNG and CNG consumers across the country now pay the lower Zone 1 rate regardless of how far they actually are from the gas source. PNGRB estimates this slashes transportation costs for distant areas by nearly 50%. It could save the sector roughly ₹1,000 crore annually. Consumer prices fell by ₹0.90–1.80 per Standard Cubic Meter on implementation. There will still be small differences — state VAT on natural gas varies widely — but the reform removes the biggest structural barrier to PNG expansion into India’s hinterland.

The gas supply problem underneath it all

But all of this only works if there’s enough cheap gas to flow through the pipes.

The city gas distribution (CGD) business model hinges on access to cheap APM gas, allocated at a capped price. If there’s enough, the system works: distribution companies earn healthy margins, while consumers get gas at affordable rates.

But there’s only so much APM gas, and it’s decreasing. The gas comes from legacy fields whose production is expected to peak around now, and then decline 20% by 2030, as fields deplete. The government already stress-tested this system’s fragility in late 2024, when it slashed APM gas allocation to CGD companies by 35–40%. Companies were forced to buy gas on the spot LNG market at international rates, which were roughly double or triple the APM price. Margins collapsed; and IGL and MGL shares crashed 18–20% in a single day.

If our demand for natural gas grows, while domestic supply plateaus and declines, the sector will increasingly rely on imported LNG to fill the gap. LNG’s share of India’s total gas consumption is projected to rise from about 48% today to 75% by 2035. To a company distributing gas, input costs roughly double — which feeds directly into higher PNG rates for households.

This is the fundamental problem with the policy: it only works while we keep making cheap gas within India. The moment we fall short, PNG prices shall rise, the cost advantage narrows, and the consumer case weakens. In that sense, India isn’t eliminating a supply-chain vulnerability. We’re just diversifying from one dependency to another.

There’s another way to read this. India has been meaning to make this transition for years. But we faced inertia. People were happy with LPG, and convincing 33 crore households to voluntarily switch from something that works is, under normal circumstances, nearly impossible. The Hormuz crisis changed that. If cylinders take 45 days and cost ₹4,000 on the black market, it’s easier to make a case for switching.

This is an opportunity to complete an old project. Except, it isn’t clear if the economics makes sense anymore.

Can the WTO survive the wilderness?

Last Tuesday, some of the world’s most powerful people lined a conference room in the Palais des Congrès in Yaoundé, Cameroon. They were there for the fourteenth MInisterial Conference of the World Trade Organisation. As the morning opened, the body’s Director General, Ngozi Okonjo-Iweala, took the stage to address the delegates. The remarks she delivered were, in some senses, a lament for a dying era.

As she challenged the delegates before her, “It is now really up to you members to decide whether you want the organization to continue or you want to pull it apart.“

It is rare for the head of a multilateral institution to wonder, publicly, if her own organisation shall survive. But Okonjo-Iweala wasn’t being dramatic; the signs were clear for all to see. International trade is hurtling towards one of its worst moments of disarray since the second world war. The World Trade Organization was built to do four things: negotiate trade rules, settle trade disputes, monitor what governments did, and guarantee predictability.

At the moment, all four are in various stages of failure. And there isn’t a clear path to fixing them.

The idea underneath

The WTO rests on a particular idea of how global trade should work.

It goes roughly like this: you need to divorce trade from power. If international trade is a matter of raw leverage — where big economies dictate terms to small ones, and muscle decides outcomes — most countries end up worse off. Powerful countries invariably turn their markets into a geopolitical trump card. Meanwhile, businesses no longer have predictability, and struggle to plan their way ahead. This was just theory for decades, but we’re currently seeing it play out in real time.

The WTO was meant to be a world-wide institution that would keep that outcome at bay.

The foundations

Its foundation was the “most-favoured-nation treatment” principle, or “MFN”. By this principle, if a WTO member offered any trade terms to one member country, it would have to offer the same terms to all members. Layered, on top of this, was the idea that all tariff commitments would be bounded. Once you promised a rate, you couldn’t raise it unilaterally. The system had near-universal membership — 166 countries — making it the global floor for how trade happened. It set a minimum standard of behaviour that, at least in theory, constrained everyone equally.

If countries felt aggrieved with what others were doing, the WTO even created a dispute resolution body. This would ensure that countries wouldn’t try settling disputes through political leverage, but on the basis of rules.

Of course, there were always gaps in how it worked. In the initial negotiations around its creation, for instance, developing countries were asked to accept rules on intellectual property, services, and agriculture, which were largely designed by and for rich economies. In exchange, they would get access to better markets, and at some point in the future, were promised a development agenda that would address their concerns. Three decades on, that promise is still unfulfilled.

But the broad architecture of the body held. Until now.

Four breakdowns

The WTO didn’t break down overnight. It had four pillars, each of which have been breaking down over the decades.

Its role as a norm-setting body was, perhaps, the first to go. In fact, it never really grew into the role.

The original WTO agreement was supposed to create a framework for how trade would happen. Just as importantly, however, it was supposed to be a forum where future rules of trade could be created. But, in thirty years, the WTO has produced a sum total of two new multilateral agreements — 2017’s Trade Facilitation Agreement and last year’s Agreement on Fisheries Subsidies. In 2001, it adopted the Doha Development Agenda, aiming to improve the trading prospects of the developing world. That is dead in all but name.

The problem comes from how the WTO is designed. The body was built to operate by consensus. But getting more than a hundred companies on board for anything is an impossible ask. Any single member can block any decision, for any reason. That meant that the organisation reliably caused paralysis. In fact, it has never taken a substantive vote in its thirty-year history, even though its charter allows it.

This paralysis killed the Doha Development Agenda. Developing countries — India prominently among them — were banking on many promises made then, particularly around sensitive areas like trade in agriculture. Those simply didn’t come through. In response, developing countries began keeping new issues hostage until old promises are kept. This was politically rational. But it worsened the problem further, by ensuring that the WTO couldn’t make any moves on digital trade, investment, or industrial subsidies — the issues that actually matter in 2026 — without settling fights from 2001. This logjam meant that actual norm-setting discussions moved to regional and bilateral efforts.

Even if it was weak at setting new norms, though, for a long time, it was competent at enforcing old ones.

For many years, the WTO would decide disputes on whether a country’s trade policies worked with its charter. It entertained cases on everything from trade in aircraft to trade in shrimp. Parties to a dispute, by and large, abided by the body’s decisions. But then, that broke as well.

By design, WTO disputes are settled in two layers. Disputes first go to a panel. If a party disagrees with the panel’s verdict, however, it can appeal to an appellate body — which is tasked with reviewing the panel’s decisions.

In 2017, the United States blocked appointments to the appellate body. This defanged the whole system. If the WTO ever decided against a country, it could simply file an appeal. By 2020, the Appellate Body had zero members — it essentially no longer existed. The appeal would remain stuck indefinitely. The panel’s ruling would never be binding.

With its teeth broken, the WTO could no longer ensure predictability of any sort.

Countries became brazen in their trade policy. We all saw a demonstration of that coming out of the United States last year, with its arbitrary, country-wise tariffs. In fact, by now, countries have all but rejected the authority of WTO’s principles. The 2026 US Trade Policy Agenda, released by USTR Jamieson Greer just weeks before the recent ministerial conference, called the MFN principle “not just unsuitable for this era“ but a principle that “actively prevents countries from optimizing their trade relationships.“ The country that was once the WTO’s greatest champion no longer recognised the very rationale of its existence.

The only pillar of the WTO that survives, now, is its least glamorous function: transparency. This still works in some form. Countries still submit reports to the WTO. This creates a global repository of data; a public good that everyone benefits from. But as the body has bled away the remainder of its authority, this too is crumbling. By 2023, for instance, more than half of its members failed to submit the subsidy notifications that WTO rules require.

The fourteenth conference

It was this backdrop in which the body’s fourteenth ministerial conference was held. It is why its Director General began the session on such a dour note. If the WTO were to survive, this meeting would have to do a lot to carry it through.

The expectations

The centerpiece of this conference was the creation of a reform roadmap. Nobody expected this session to solve the WTO’s many ugly issues. But the hope was that they could reach a structured work plan, with milestones and timelines.

But around this, the WTO hoped to get a few simpler matters through, to give the body some momentum.

One of these was an extension of the “e-commerce moratorium”. This was a commitment that parties had made in 1998, that they wouldn’t impose any customs duties on cross-border data flows: like movies, games, music and the like. This commitment would frequently be rolled over, in previous conferences. This time, however, it became a high-stakes political test.

The developed world was arguing for a permanent ban — claiming that trying to tax these flows would essentially kill internet trade as we know it. A few countries, India prominently among them, claimed the opposite: that most such flows went from the developed-world — the US above all. If developing countries couldn’t tax these flows, they lost a fundamental revenue-raising opportunity. As the UNCTAD estimated, the moratorium costs developing countries up to $10 billion a year in potential tariff revenue.

The other big test, this conference, was around the Investment Facilitation for Development (or IFD) Agreement, a deal that aimed to ensure transparency and procedural efficiency in investment approvals. The deal had been co-sponsored by 129 members — with India the lone standout.

The rest of the world didn’t need India to sign this agreement, or agree to be bound by it. They were asking that it be added as a plurilateral agreement — one which only bound its signatories — but that it was added to the WTO’s Annex 4. This would bring it within the formal framework of the WTO, even if it didn’t bind everyone. But this addition, too, required consensus.

The logjam

In the end, the conference achieved practically none of its goals. A big reason, for that, was India.

It wasn’t a complete failure. For one, it came close to creating a reform roadmap, though it couldn’t get one through the line. Reportedly, drafts of such a roadmap were nearly agreed upon, though they couldn’t reach finality. Delegates expect future talks to happen in Geneva, perhaps as soon as May.

But for now, the body doesn’t have a working plan in place.

The e-commerce moratorium stalled, becoming the site of a major India-US stand-off. The United States insisted on the moratorium becoming permanent. India, on the other hand, wanted the moratorium nixed altogether. By the end, India was finally willing to concede to a two year extension — but then, Brazil put its foot down, refusing to accept a compromise. For the first time since 1998, countries are now technically free to impose customs duties on electronic flows. The WTO effectively failed to protect a three-decade old rule.

As a consolation, 66 members — covering 70% of world trade — agreed to interim arrangements that could, some day, become the basis of an e-commerce agreement. But the consensus system had failed the organisation yet again.

India also held on to its objection to the IFD agreement, ensuring that it was blocked for the ninth time. Previously, Turkey and South Africa, too, were on India’s side. This time, however, India stood alone, against 129 others.

India’s issue wasn’t really with the substance of the agreement itself — it was with precedent. India has steadily argued that old issues, like agriculture or food security, must advance before anything new can be added to the WTO’s rubric — even if plurilateral. This could, otherwise, become a route through which India’s bargaining position can be weakened.

Other issues, too, were deferred for later. Ultimately, the conference didn’t even get the dignity of adopting a comprehensive ministerial declaration.

How long can the charade last?

The WTO will perhaps survive even this. Institutions that feature most of the world don’t close overnight. But it isn’t clear how it will ever regain its former prestige as the global arbiter of trade issues. If it survives, it will probably be in some other form — perhaps as a keeper of statistics, perhaps as a forum for discussion, where willing coalitions can decide the rules they follow within their small groups.

The body’s Director General herself seems to have accepted this. In her words, “The world order and multilateral system we used to know has irrevocably changed… we will not get it back.“

The cost of this, sadly, is a world where raw economic weight decides trade outcomes. As we have learnt over the last year, that isn’t a negotiation India can always win.

Tidbits

The government approved 75 projects worth Rs 61,671 crore under its new Electronic Components and MSME (ECMS) programme to manufacture chips, magnets, PCBs, and other core electronic components domestically. IT Minister Ashwini Vaishnaw said India is now building “the heart of devices rather than just the outer shell.” Separately, India’s second Micron semiconductor plant was inaugurated on March 31, just 19 months after groundwork began. The first plant was inaugurated on February 10. Vaishnaw called the pace “a demonstration of India’s manufacturing capability.”

Source: Business TodayFrom today (April 1), RBI’s new two-factor authentication rules kick in for all digital payments, including UPI, cards, and wallets. OTP alone will no longer be enough to complete a transaction. Users will now need a second layer of verification: a PIN, password, biometric, or software token alongside the OTP. The move comes after a spike in phishing and SIM swap fraud. Small transactions may get some leniency, but for larger amounts, banks will mandatorily request additional verification. Cross-border payments get a longer runway, with similar rules applying from October 1.

Source: CNBC TV18MeitY approved 29 projects under the Electronics Component Manufacturing Scheme (ECMS) with a total investment of Rs 7,104 crore, expected to create 14,246 jobs. The standout: India’s first rare earth permanent magnet manufacturing facility using rare-earth oxides, approved at Rs 700 crore. India currently imports 85-90% of its rare earth magnets from China by quantity. These magnets go into everything from EV motors and wind turbines to defence systems and consumer electronics. Other approvals include Rs 1,683 crore for capital goods, Rs 1,350 crore for display module sub-assemblies, and Rs 500 crore for lithium-ion cells. Total ECMS approvals have now crossed Rs 61,671 crore, overshooting the scheme’s original target of Rs 59,350 crore.

Source:Moneycontrol

- This edition of the newsletter was written by Kashish and Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Cooking in PNGs are generally faster than on LPG. Further, PNG is safer to operate as methane is lighter than air and chances of build up of gases and explosion risk is low as compared to LPG. Methane also burns more cleaner than Propane and Butane, but the risk is it requires more air or ventilation to burn efficiently.

The need of the hour is to explore other models like biogas. Biogas plants can work on hub and spoke models in dense socieities, where the wet and biodegradable waste can be fed to a biogas plant in an area, which in turn generates biogas which can be used in the households thereby eliminating both waste and fuel problems.

This is a really good primer.

Kudos on the attention to detail, e.g. lpg cooking is so different from cng cooking due to the higher heat, etc.