The world’s energy transition meets a historical crisis

And the outcome is a little complicated

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Hi folks! Before we start, we want to tell you about a new project we’ve started: Subtext by Zerodha.

Our work at The Daily Brief, or elsewhere at Markets, doesn’t often involve talking to experts and scholars that we think people should know about, and even refer to in our stories. Subtext is our way of literally engaging with the rest of the world. It will house conversations and narratives with incredibly knowledgeable guests: think entrepreneurs, policymakers, academics and industry experts.

Our first episode is out, and it’s with Manoj Kewalramani, a China Studies Research Fellow at the Takshashila Institution. It’s a scintillating, mythbusting chat with someone who doesn’t just read about China extensively, but has actually lived there and speaks the language.

You can watch this episode on YouTube, or listen to it on Spotify or Apple Podcasts, or read the transcript on Substack.

In today’s edition of The Daily Brief:

The world’s energy transition meets a historical crisis

The opaque curtains of India’s gold pricing

The world’s energy transition meets a historical crisis

What happens when an unstoppable force meets an immovable object? In this case, we’re referring to the world’s energy transition clashing with the crisis at the Strait of Hormuz. We leave you to decide which is which.

Faith Birol, the head of the International Energy Agency (IEA), calls this crisis the largest supply disruption in the history of the global oil market. For many of the world’s developing and poor nations, which are almost wholly dependent on crude oil imports, energy diversification has never been more important.

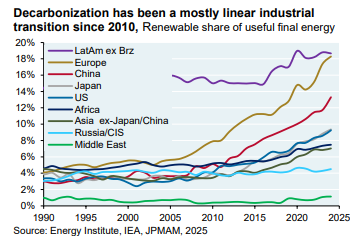

The good news is that the shift away from fossil fuels, and towards renewables and nuclear, has been undeniably consistent. And perhaps, with the price of crude oil increasing, there’s an expectation that the transition will only accelerate further.

However, progress has not been uniform across countries. And the Hormuz crisis is interacting with the world’s current energy mix in complex ways. Right now, clean energy does not have a clean story. The crisis has simultaneously accelerated the shift away from fossil fuels and caused a few setbacks for it — in different places, for different reasons, often at the same time.

That’s what our story is about.

Back to square coal

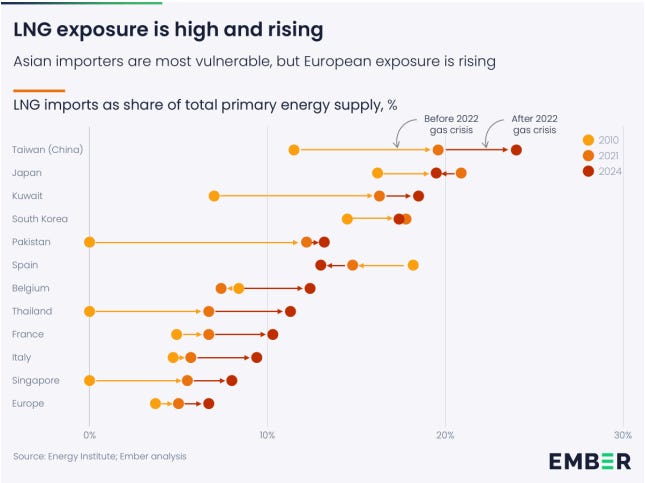

For many countries, the energy transition has depended on a crucial intermediate step: liquefied natural gas (LNG).

The theory was sensible enough. For power, coal was the primary source, and full renewable grids would take decades to build. LNG was meant to serve as a bridge in between. While a non-renewable energy source, it’s much cleaner than burning coal, and would help reduce emissions while solar and wind infrastructure were being built.

Japan, for instance, had committed to this more fully than almost anyone. After the Fukushima nuclear disaster in 2011, it shut its nuclear reactors and rebuilt its power system around imported LNG. Taiwan and South Korea followed similar paths. All three entered 2026 deeply reliant on a few LNG suppliers, especially Qatar.

However, the crisis disrupted Qatar’s supply of LNG and raised its prices. Now, this bridging strategy makes far less sense.

The immediate response across Asia was a reversion to coal. Japan lifted operating restrictions on older coal plants for up to a year, while South Korea removed its 80% cap on coal-fired generation. Meanwhile, Indonesia — the world’s largest coal exporter — is actually prioritising domestic supply, redirecting coal toward its own power plants rather than exporting it.

Europe is in a different kind of trap. In their chase of achieving a renewable-heavy grid, some European nations have fully phased out coal. They doubled down on LNG, and diversified their sources after Russia’s invasion of Ukraine in 2022, importing from Qatar and the US. However, Europe entered 2026 with abnormally low gas stockpiles.

Now, you might wonder, this is just temporary. If (and that’s a big if) this crisis ends, countries could just switch back to LNG, right?

Well, it’s not that easy. Coal plants are not designed for flexible operation — they are built for steady, continuous baseload generation, not to be switched on and off in response to a geopolitical crisis. Repeatedly ramping them up and down causes thermal stress, reduces efficiency, and drives up costs in ways that compound quietly. More problematically, new coal capacity locks in asset lifespans of 30 to 40 years. Emergency choices made now could make a long-term impact on the carbon profiles of these economies in the future.

India’s relationship with LNG was always more fraught. As we’ve covered before, imported LNG was never cheap or reliable enough to compete with domestic coal and renewables in the Indian power sector. As a result, our transition has been more of a direct jump from coal to renewables. This is partly why India is accelerating coal gasification, where domestic coal is converted into a gaseous form that is easier and cleaner to burn than real coal.

Suns and winds of change

Now that we’ve addressed the middle layer of the energy transition, what about the final phase: clean energy itself? The crisis has produced a strong price signal for clean energy alternatives. And in many markets, those alternatives are now mature enough to respond.

Electric vehicles

Let’s start with EVs.

In India, electric car registrations jumped 50% year-on-year in March. Some part of the jump in recent EV bookings is attributed to this crisis making petrol cars relatively more expensive. And industry analysts expect that this is just the beginning.

A report by Ember documented that Vietnam had already hit a 38% EV sales share, Uruguay 27%, and Indonesia 15% — all ahead of both the United States and Japan, before the crisis had even begun. China leads the pack, crossing 50% EV sales share for the first time last year.

Now, many of these countries provide consumers with tax credits and subsidies for EV adoption. But, even in countries that lack them, EV adoption has taken off in reaction to the crisis. Ironically, no country illustrates this better than one of the central actors in this crisis — the US.

See, the Trump administration ended the federal EV tax credit last year, making new EVs far more expensive for the average American. As petrol crossed $4 a gallon, consumers pivoted to the second-hand market, as used EV sales surged 12% from last year.

Solar energy

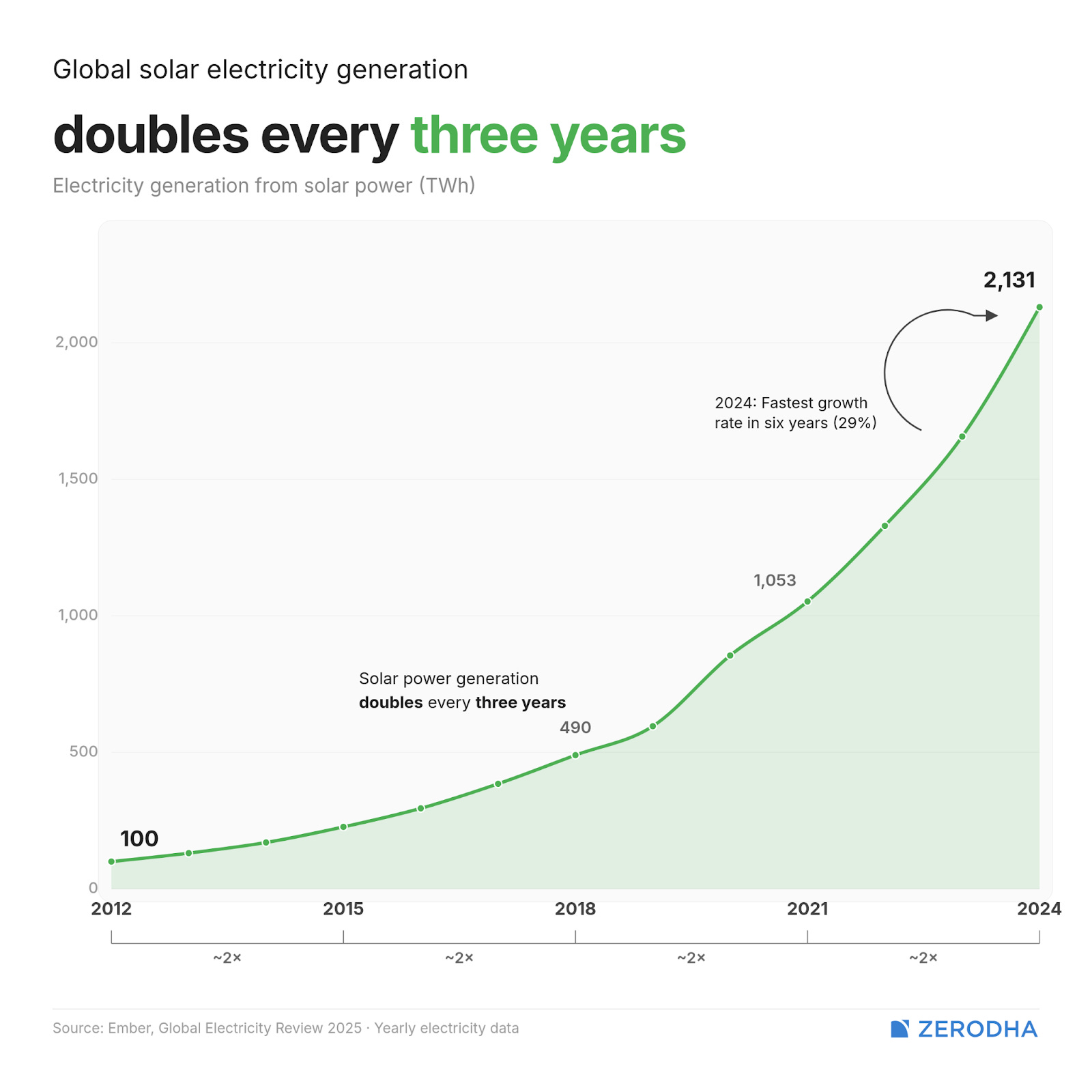

Now, let’s move on to solar, which has already been enjoying strong tailwinds. As per Ember, even prior to the crisis, solar power generation has basically been doubling every three years.

The biggest appeal of solar comes from the fact that it’s a “terminal product“. What that means is, unlike a gas-fired power station that requires you to pay for fuel every day it operates, a solar panel generates electricity for years at zero ongoing fuel cost. There’s no cost for the sun.

Across Europe, a boom in balcony and plug-in panels saved the continent ~€100 million in March alone this year, just by displacing demand for imported gas. Only recently, a developer in Vietnam recently asked the government to cancel a planned LNG terminal and build a solar and battery project in its place instead.

Perhaps, the solar story hasn’t been more powerful anywhere else than in developing nations that adopted it out of economic desperation.

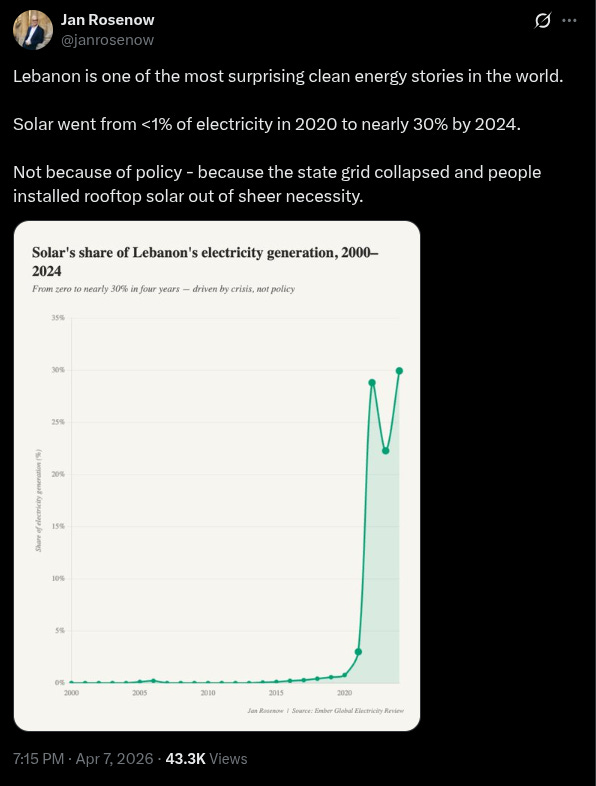

Pakistan, for instance, imported roughly 41 GW of solar panels from China since 2023 — nearly equal to its entire pre-existing power generation capacity combined. Sri Lanka, meanwhile, was just recently burnt by a foreign exchange crisis driven by fuel import costs. As a result, they’ve been rushing forward solar and battery projects to manage the current energy hardship. Lebanon, where grid power has been rationed, has seen rooftop solar spread across their country.

Solar is not fully insulated from the crisis, though. There are two big bottlenecks, one of which has directly been created by the Hormuz crisis.

See, solar panels use a lot of aluminium, which is energy-intensive to smelt. And smelters in the Gulf, where power is cheap and abundant, make up ~9% of global aluminium production. Now, they have curtailed output because of the same gas shortages hitting everyone else. Aluminium prices were already rising before this, but now, they have hit four-year highs. The crisis is briefly making solar a little more expensive to build at exactly the moment it should be most attractive to buy.

The second catch has more to do with how solar itself is being adopted. In countries like Lebanon and Pakistan (which we covered earlier), solar panels are mostly being adopted by their richer citizens. Often, it has no connection to the national grid, which has basically collapsed. The large, relatively lower-income sections of their societies, which are still reliant on the grid, are still facing the brunt of the Hormuz crisis.

Going nuclear

Meanwhile, nuclear might be having a huge dramatic political moment. The crisis has driven countries which had sworn to never take up nuclear again to announce new nuclear plants altogether.

Taiwan, for instance, promised a “nuclear-free homeland“ in 2016, decommissioning its last nuclear plant last year. But now, in a complete reversal, they might be restarting two shuttered reactors. Meanwhile, Japan is also turning back on some of its reactors.

Across Asia, nuclear is being reframed from a politically toxic legacy technology to the only firm baseload power source that doesn’t depend on imported fuel or sunny skies.

The China question

Of course, when we talk about clean energy sources like EVs and solar, it’s hard not to wonder about China’s role.

After all, China produces most of the world’s solar panels, dominates EV battery manufacturing, and also controls rare earths that feed both technologies. The supply chains of the clean energy transition run almost entirely through Chinese factories. A country scaling up solar and EVs is, in effect, trading dependence on Gulf crude for dependence on Chinese manufacturing.

With EVs, the danger is more obvious, as countries are likely to import not just EVs from China, but also batteries and the lithium that powers them. However, with solar, some argue this is not the same vulnerability. When you buy a solar panel, you buy the means of production. The leverage China has over your energy supply should end the moment the panel creates power.

However, that’s not the only geopolitical leverage China has. In this crisis, it might also be one of the most energy-secure nations in the world today.

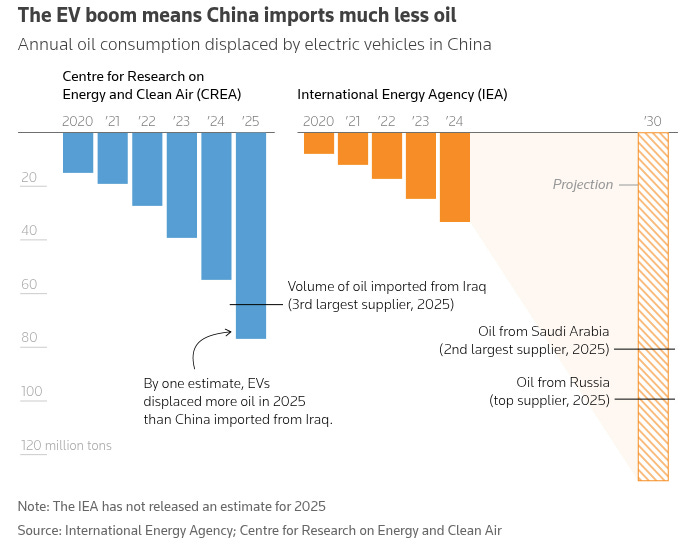

As per the IEA, the oil displaced by China’s EV fleet last year was roughly equal to what the country imported from Saudi Arabia. Its power grid is mostly powered by coal and renewables, insulating it strongly from global oil price shocks. On top of that, less than 20% of China’s oil imports are from any one source. It also has 1.2 billion barrels of crude in onshore storage as of January — roughly 108 days of import cover.

Coal, though, remains the ballast stone of China’s own energy security, accounting for over half of its electricity generation. China is simultaneously the world’s biggest clean energy manufacturer and its largest coal consumer. Those two facts coexist without contradiction, but they mean different things for different kinds of dependence.

History never ends

Prior to today, the last big oil shock was in 1974, when OPEC hiked oil prices. Up until that point, our entire mass-production economy — cars, suburbs, plastics, synthetic fertilisers — had been built on the assumption of cheap oil.

Economic historian Carlota Perez studied this crisis, and realized that when oil became expensive, the search for the next cheap input intensified. She found it in the rapidly falling cost of microelectronics, which, in turn, gave birth to the age of information technology. This was a new industrial revolution that came partly as a response to expensive energy.

History doesn’t rhyme, but does it repeat itself? Will the oil crisis of today accelerate the clean energy revolution? Will it fasten the advent of what people call “peak oil”?

There’s certainly a huge impetus. Countries are enforcing work-from-home policies, ordering AC temperatures be raised, introducing four-day workweeks, and even closing schools. Perhaps, the feeling couldn’t be more succinctly put than when Lee Jae Myung, the president of South Korea, said this:

“Right now, there is chaos worldwide due to energy issues. Frankly, the situation is so serious that I cannot sleep. South Korea must swiftly transition to renewable energy.”

The transition itself was always complicated before the Strait of Hormuz blockade. Now, that has made things even messier. Yet, it has made the call to action far louder than it has ever been, and that itself could be the biggest catalyst the new energy shift needs.

The opaque curtains of India’s gold pricing

On April 1, the Directorate General of Foreign Trade restricted all imports of gold, silver, and platinum jewellery into India, effective immediately. The next day, a second notification restricted precious metal alloys, certain forms of unwrought gold and silver, and several other categories under Chapter 71 of the tariff code. Also effective immediately.

The language was unusually aggressive — no transitional relief, no grace period, existing contracts, irrevocable letters of credit, advance payments, goods already shipped, all overridden. The government does not talk like this unless it believes something is urgently, structurally wrong.

India produces almost no gold of its own. Every year, the country imports roughly 800 tonnes. For India this fiscal year, gold was the single largest item on the import bill after crude oil. In October 2025 alone, gold imports hit a record $14.72 billion, enough to push the monthly trade deficit to an all-time high of $41.7 billion.

And between the import price and the gold you buy, there sits a small, closed group of intermediaries operating through a system so opaque that different buyers routinely pay different prices for the same gold on the same day.

This is the story of how that system works, who benefits from it, why the government keeps trying to fix it, and why it keeps failing.

A brief history

For most of independent India’s existence, importing gold was simply illegal. The Gold Control Act of 1968, introduced by Finance Minister Morarji Desai, prohibited citizens from owning gold in bar or coin form. Goldsmiths couldn’t hold more than 100 grams. Licensed dealers were capped at 2 kilograms. The reasoning was that India’s huge appetite for gold was draining foreign exchange reserves at a time when the country could barely afford to import essential goods.

Although it killed the official gold market entirely, a massive underground market replaced it. Gold was smuggled in from West Asia on dhows, landing at secluded spots along the western coast. The men who ran this trade became Bombay’s first organised crime bosses. Haji Mastan was the master of the Arabian Sea routes. Dawood Ibrahim got his start as a “landing agent,” receiving shipments on the docks.

By 1990, the broader economy was in crisis. India was on the verge of defaulting on external obligations. The government pledged 40 tonnes of gold to the Bank of England to secure emergency loans. The Gold Control Act was repealed. Liberalisation followed, and gold imports were legalised, at a specific duty of ₹300 per 10 grams, roughly 1%. Smuggling became uneconomical overnight.

But gold couldn’t be entirely decontrolled either. Unlike oil or machinery, gold doesn’t fuel production and the foreign exchange used to buy it is gone. You cannot simply place an order with an overseas supplier, even if you have an Import-Export Code. Ideally, you’ll need certain regulated entities at the centre of India’s gold trade.

And that’s what the RBI did.

Sixteen doors

In 1997, the RBI designated the first batch of seven banks as nominated agencies for gold import. They would directly buy gold from international suppliers and sell it to jewellers at a markup.

Then, in 1998, the RBI issued a circular that expanded the ways nominated banks could import gold. It added several new options, including something called “consignment“.

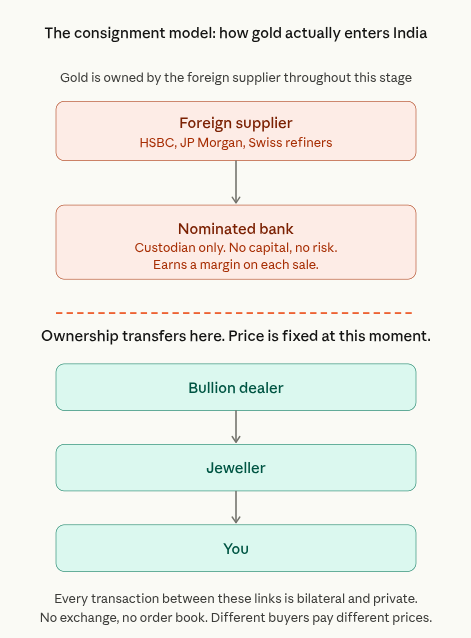

Under consignment, an overseas supplier — typically a global bullion bank like HSBC, JP Morgan, or a Swiss refinery — ships gold to India through a nominated bank. But ownership does not transfer. The gold sits in a vault in India, still belonging to the foreign supplier. The nominated bank is not a buyer as much as it’s a custodian or middleman.

The gold stays in this state, physically in India but legally owned by a foreign entity, until an actual end-buyer — like a bullion dealer or a jeweller — shows up. At that point, the nominated bank facilitates the sale. The price gets fixed only then, at the moment of sale, not when the gold was imported.

The nominated bank, in return, gets a fee on each transaction. It doesn’t need to deploy capital, or take price risk, or fund the inventory, or even bear the storage cost. Almost all gold imported into India comes through consignment because for the banks it is risk-free income.

But obviously, that means that these banks have negligible say in how gold is priced.

As per a paper from IIM Ahmedabad, the consignment model has made nominated banks “overly reliant on suppliers setting prices for them“. Most banks have “not advanced up the value chain by holding gold in their books“, even though the RBI has explicitly permitted them to do so since July 2014. The banks found a comfort zone where “a simple markup is added” to run their bullion desks, and they’ve stayed there ever since.

As of July 2025, there are exactly 16 nominated banks, including State Bank of India, HDFC Bank, ICICI Bank, and so on. On top of these banks, there are also 43 refineries certified by the Bureau of Indian Standards that can import unrefined gold for processing, and a few government agencies. But the banks are the primary channel through which gold passes into India.

The phone call market

Okay, but is there a problem here? Well, yes.

You see, when a bullion dealer wants to buy gold, they call their contact at a nominated bank. The bank checks with its overseas supplier, and a price is quoted. That price depends on the size of the order, the dealer’s relationship with the bank, the timing, how much gold the supplier currently has parked in Indian vaults, and the dealer’s negotiating power.

Every transaction in this system happens privately, bilaterally, over the counter. There is no exchange where bids and offers are visible, no centralised order book. This means there is no transparent, publicly available price at which gold changes hands in India.

A large dealer in, say, Zaveri Bazaar, who moves hundreds of kilograms every month, who has dealt with the same bank for twenty years, gets a different quote from what a regional dealer in Varanasi or Coimbatore gets through an intermediary. The nominated banks have been offering different prices to different customers.

This is why gold prices in India vary from city to city. Each city has its own bullion association that sets a daily gold rate every morning, and local jewellers price off that rate.

But these visible city-level differences are just the surface. Underneath them lies a supply chain where the spread between what the foreign supplier charges and what you eventually pay passes through multiple links. And each link adds a markup that is set in private, making the price a lot higher than what would have existed with a central exchange.

The exchange that nobody uses

Now, India has indeed built such an exchange.

The India International Bullion Exchange (IIBX) was launched by the Prime Minister in July 2022 at GIFT City. Instead of opaque consignment channels, “qualified jewellers” could import gold through exchange-traded contracts. That would mean prices that would be visible on an order book.

From launch through March 2025, IIBX traded a cumulative 101.4 tonnes. It projects 120 tonnes for FY26. India imports 800 tonnes a year, and IIBX handles roughly 15%. The other 85% still flows through consignment.

The problem is incentives. For the foreign supplier, consignment gives guaranteed market access without price competition. For the bank, it’s risk-free income. For large dealers, OTC means preferential pricing that smaller players can’t access. Transparency is not in anyone’s commercial interest, except the small jeweller at the end of the chain, who has no say.

China faced the same problem. Before 2002, its gold market was opaque. The People’s Bank of China established the Shanghai Gold Exchange and mandated that all gold flow through it. Today, the SGE is the world’s largest physical gold exchange with over two million individual investor accounts. It runs a twice-daily benchmark auction in RMB. When Chinese demand surges, the “Shanghai premium” spikes and traders worldwide respond. China has a voice in global gold pricing.

India built the exchange but didn’t mandate its use.

Finding arbitrage

Meanwhile, India’s gold imports often clashed with India’s political economy.

Between 2012 and 2013, gold imports surged so dramatically that they became a threat to macroeconomic stability. The current account deficit was ballooning, the rupee was falling. The government hiked import duty from 2% to 10%. Predictably, smuggling came roaring back — seizures in the first quarter of 2013-14 were 365% higher than the 365 days before.

Alongside the duty hike, the RBI tried the 80:20 scheme, where, for every lot of gold imported, at least 20% had to be made available exclusively for jewellery exporters. Only after proving that could the bank release the remaining 80% for domestic sale. The idea was to ensure gold imports generated some export revenue, and therefore foreign exchange.

In practice, though, it created enormous confusion, was vulnerable to round-tripping (gold exported on paper to justify more imports), and was withdrawn in November 2014, less than two years after it was introduced.

Then, in the July 2024 Union Budget, the government slashed import duty from 15% to 6%. If high duties cause smuggling, lower duties would bring imports back into official channels. It worked, in the sense that official imports surged. But it worked too well, inflating the import bill massively.

Meanwhile, traders kept finding loopholes. Some discovered they could import gold jewellery through Thailand at zero ASEAN duty. Others found they could import gold disguised as “platinum alloy” from the UAE at lower duty rates. This week’s two DGFT notifications are aimed at plugging these. They will work for a while. Until someone finds the next one.

Where this leaves us

Now, this week’s restrictions will close some of these loophole routes, but the core of the situation doesn’t lie there.

India’s gold market is worth over $69 billion a year. The RBI holds a record 880 tonnes in its reserves. Nearly 10 million Indians hold gold through ETFs. Tens of millions more buy it physically, every year, for weddings and festivals and as savings.

And all of this runs on a price set in London, imported by 16 banks that don’t actually buy the gold, sold through private calls to a few hundred dealers who each get a different quote. The fundamental problem is that India’s gold market is quite opaque, and has less reason to be less so.

Tidbits

[1] SEBI extends IPO approval validity amid market volatility

SEBI has extended the validity of IPO and rights issue approvals till September 30, 2026, giving companies more time to launch offerings. The move comes amid West Asia tensions, market volatility, and weak investor participation, with no penalties for delayed compliance during this period.

Source: ET Now

[2] RBI pegs FY27 growth at 6.9%, inflation at 4.6%

The RBI has projected FY27 GDP growth at 6.9% and inflation at 4.6%, while keeping the repo rate unchanged at 5.25%. Growth remains steady but slightly lower than last year, with risks from geopolitical tensions and energy prices. Inflation is expected to stay within the target range.

Source: Mint

[3] Adani seeks dismissal of US SEC fraud case

Gautam Adani has asked a US court to dismiss the SEC’s fraud case, arguing it falls outside US jurisdiction and shows no wrongdoing. The case relates to a 2021 bond issue by Adani Green, with the group denying allegations and saying investors suffered no losses.

Source: ThePrint

- This edition of the newsletter was written by Manie and Aakanksha

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Excellent deep dive into gold. Thank you. Could you please consider posting each deep dive with its own top level title? Easier to locate later that way.