Why did global trade come to a halt?

Marine insurance is the real chokepoint

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

In trade, the pen is mightier than the missile

India faces a monetary policy dilemma

In trade, the pen is mightier than the missile

Earlier this week, when bombs fell in the Persian Gulf, one of the first things the market was worried about was oil. After all, the Strait of Hormuz handles more than a quarter of all seaborne oil trade and roughly a fifth of the world’s LNG. We covered this a few days back.

But what actually stops oil-laden ships from moving isn’t missiles as much as it is, quite literally, a piece of paper — or more precisely, the absence of one. Perhaps, the saying “the pen is mightier than the sword” couldn’t come any closer to being real than this.

That piece of paper is marine insurance. And we found that, what is otherwise a set of financial and legal jargon, is worth its own Daily Brief story. Let’s dive in.

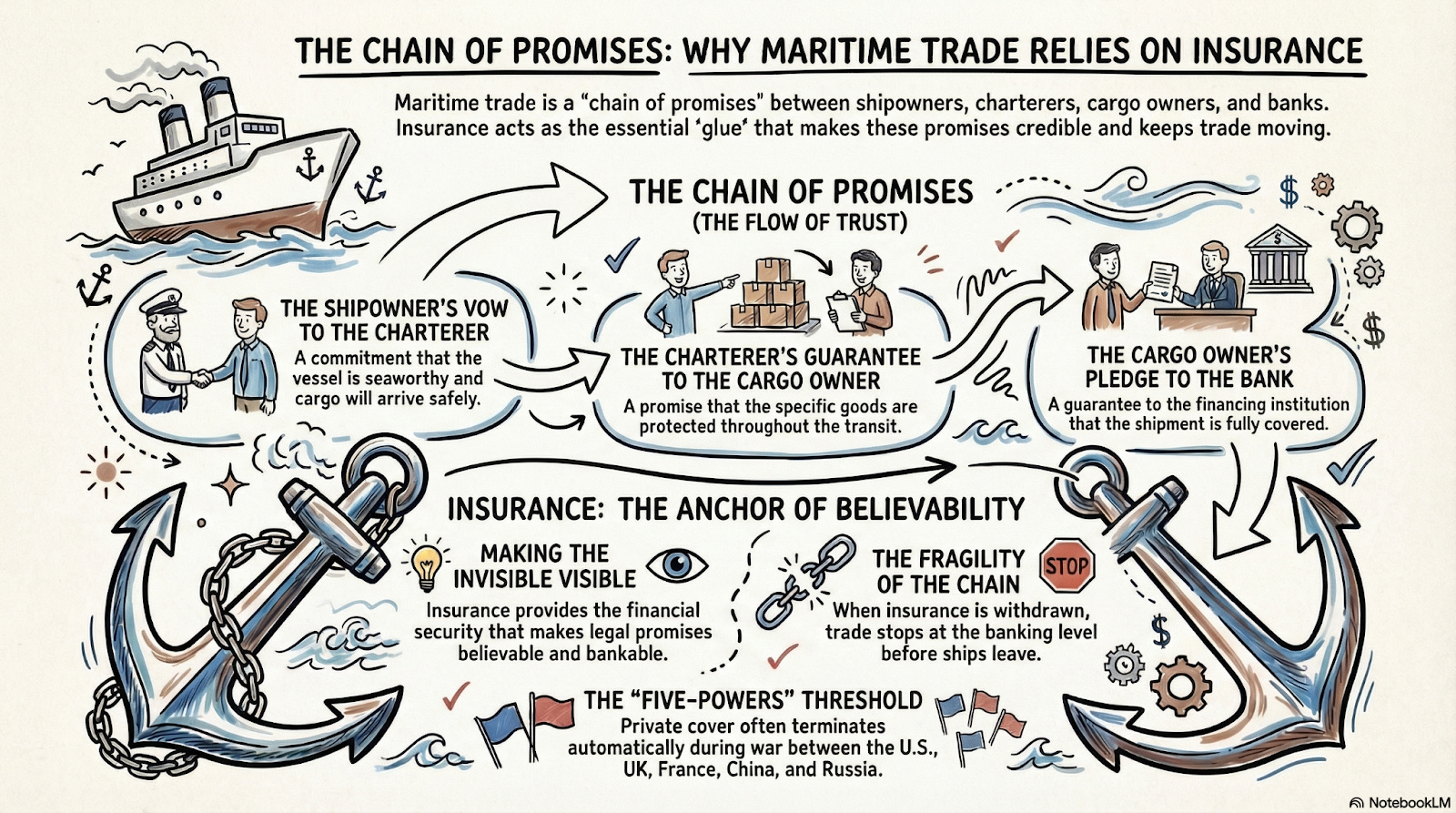

A permission slip

A ship doesn’t move just because there’s cargo to carry. It moves because an entire chain of promises holds together.

The shipowner promises the charterer the cargo will arrive safely. The charterer gives their word to the cargo owner that the goods are protected. And the cargo owner assures the bank financing the trade that the shipment is covered. Insurance is what makes all of these promises believable.

Without all of these, the chain falls apart. If the cargo isn’t insured, banks won’t issue the letters of credit needed to guarantee payment in global trade. Ports won’t let uninsured vessels dock. Even the ship’s own crew can refuse to sail. It’s not so different from how you can’t drive a car without motor insurance, except the stakes are vastly higher, and the rules much stricter.

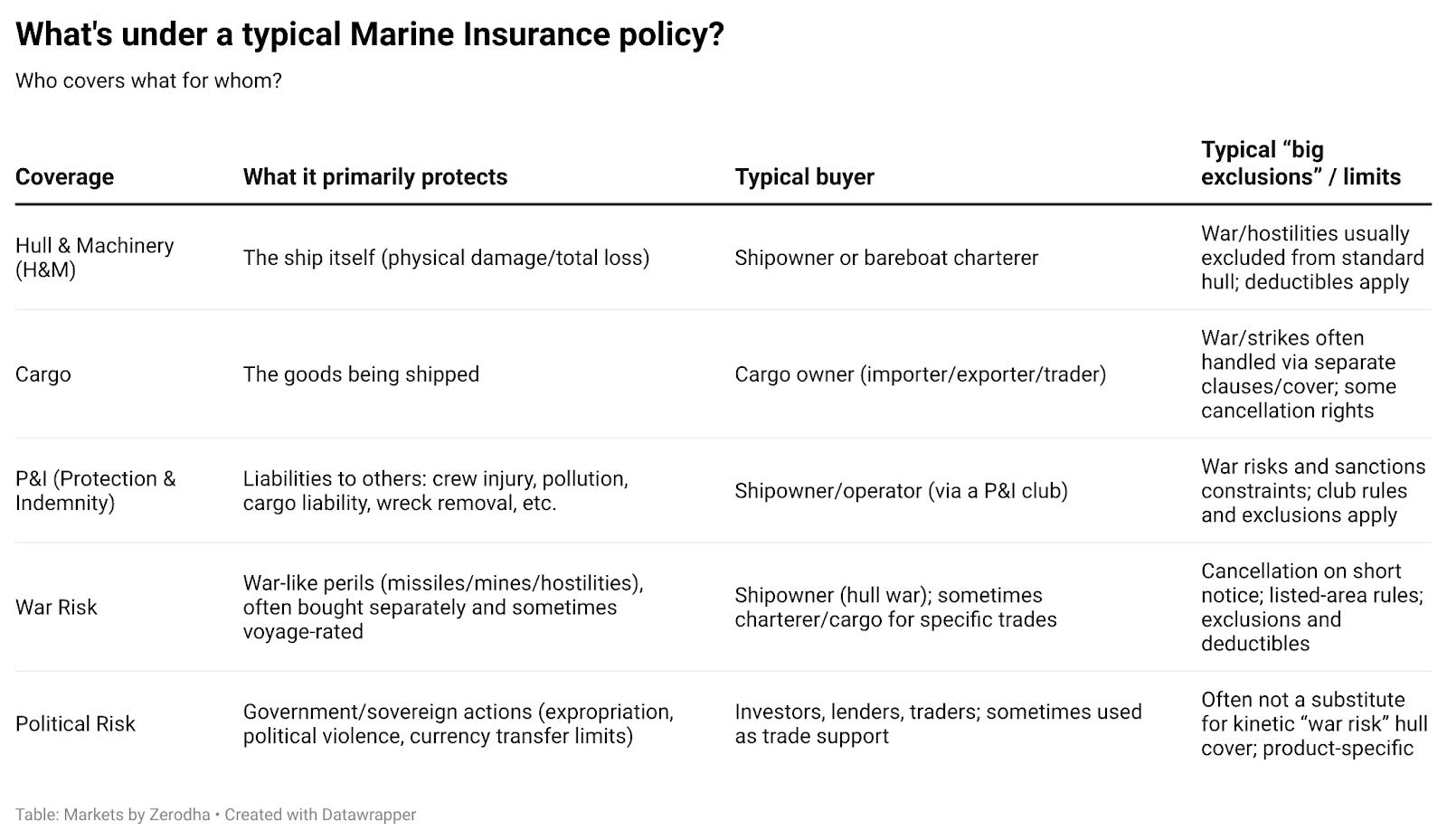

Moreover, marine insurance, unlike health or a term plan, isn’t one policy. It’s a stack that covers various things.

At the base, you have hull and machinery insurance, which covers the ship itself, think of it as the vehicle’s own insurance. Then there’s cargo insurance, which protects the goods being shipped. On top of that sits protection and indemnity (P&I). If the ship causes pollution, injures crew, or damages someone else’s property, P&I covers it.

Interestingly, P&I isn’t run by for-profit insurance firms, but by mutual clubs that are run by shipowners or ship operators themselves. Twelve major clubs, who collectively call themselves the “International Group”, cover roughly 90% of the world’s ocean-going tonnage.

And then, layered on top of everything, is what’s extremely relevant today — war risk & political risk insurance.

In normal times, war risk is part of the package. You pay a modest annual premium and your ship is covered for missile strikes, mines, and other hostilities. But there’s a catch: war risk policies come with a cancellation clause. Typically, insurers can pull the cover with just 7 days’ notice. In situations involving a major military power — like, say, the US — that window can shrink to as little as 72 hours.

This might sound unfair, but think about it from the insurer’s perspective. War is not the same as a sea storm that might leave a single ship stranded. If a conflict breaks out near a major shipping lane, dozens or hundreds of ships are exposed simultaneously. A single event could trigger billions in claims, all at once. No insurer can stomach that kind of concentrated risk for long.

So the deal is simple: during peacetime, we’ll cover you. But the moment things escalate, we reserve the right to walk away.

And that’s exactly what happened recently.

The cost of war

In late February 2026, military escalation between the US, Israel, and Iran sent shockwaves through the Gulf. The Strait of Hormuz — that narrow corridor between Iran and Oman through which a staggering volume of the world’s energy supply flows — became, in the eyes of insurers, a place where the risk calculus had changed overnight.

Most marine insurance deals are brokered in what’s called the London Market. Think of it as a specialist hub where insurers and reinsurers handle big, complicated risks. If a ship is insured, chances are the deal passed through this market.

Inside the market sits the Joint War Committee, a group of representatives who underwrite marine hull war risks. This committee maintains a list of areas considered high-risk. When missiles started flying, the designated list expanded. Waters around Bahrain, Djibouti, Kuwait, Oman, and Qatar were added to the list.

That designation matters enormously because it triggers a separate pricing regime. Instead of paying just your annual premium, any ship entering a listed area now has to pay an Additional War Risk Premium (AWRP) — typically quoted as a percentage of the vessel’s insured value. And those premiums moved fast. Insuring a $100 million vessel for a Gulf transit reportedly jumped from around $250,000 to $375,000 per voyage. That’s a 50% spike, and in some cases, quotes were even higher.

But beyond the price increases, cancellations took place left and right. Multiple major insurers — like Gard, Skuld, London P&I Club, and so on — cancelled or paused war risk cover for vessels in or near Iranian waters, effective March 5. Japan’s MS&AD suspended underwriting for war risk policies across the region entirely. One insurer mentioned a “buy-back“ option — meaning you could get your cover reinstated, but at a significantly higher price and on tighter terms.

Over 200 vessels ended up anchored in or near the Strait, waiting. And here’s the cruel irony: if a zone is dangerous and your insurance just got cancelled, wouldn’t you just leave? But you can’t. Sailing out means transiting through the very waters your insurer just declared too dangerous to cover. If something happens during that exit — a missile, a mine, even accidental damage — the shipowner is fully exposed. No one’s taking that gamble with a vessel worth tens or hundreds of millions of dollars. And even if a ship made it out safely, ports won’t accept vessels without valid insurance documentation, banks won’t honour letters of credit if the paperwork is out of order, and the act of sailing through a war zone without war risk cover could void the ship’s other insurance policies entirely.

So ships sat there, burning money on fuel and crew costs, unable to move until cover was reinstated or the situation changed. Traffic through the Hormuz strait collapsed.Freight rates surged, as VLCC (Very Large Crude Carrier) charter rates to China reportedly exceeded $424,000 per day.

The reinsurance chokepoint

Now, it’s important to note that the insurers who cancelled cover didn’t necessarily want to. Many of them were forced to, because the layer behind them — reinsurance — was pulling back.

Reinsurance is insurance for insurers. It’s the mechanism that allows an insurance company to write a $100 million policy on a ship without bearing the entire risk itself. The reinsurer takes a portion of that risk off the insurer’s books, which gives the insurer the capacity to cover more ships.

This arrangement is powerful, but also a dependency. When reinsurers get nervous — and war risk is exactly the kind of unpredictable exposure that makes reinsurers nervous — they shrink their capacity. And when reinsurance capacity shrinks, insurers have no choice but to raise prices, tighten terms, or cancel outright.

Take what GIC Re, a state-owned Indian reinsurer, did. It pulled back from its Marine Hull War Risk cover from multiple high-risk zones from March 3 effectively — including the Persian Gulf, Gulf of Oman, and parts of the Indian Ocean.

And it didn’t stop at withdrawal. GIC Re warned that any vessel transiting, calling at, or even dry-docking in the specified zones after the cutoff date would be treated as a breach of warranty. In insurance terms, a breach of warranty means your cover ceases to exist. All those marine insurance companies that were being reinsured by GIC, are now left on their own.

And the dominos fall

This starts an unstoppable chain of events where one topples over another.

Shipowners won’t risk sending a vessel worth tens or hundreds of millions of dollars into a zone where they’re uninsured. Charterers can’t fulfil contracts. Banks won’t finance shipments without valid insurance documents.

As ships pile up outside the affected zone, ports start congesting. Freight rates spike because available shipping capacity shrinks. Commodity prices rise because delivery timelines become uncertain. And then the cycle feeds on itself: higher values at risk and greater uncertainty make insurers even more cautious, which further restricts capacity, which pushes more ships to the sidelines.

It wouldn’t be wrong to say, this also trickles down to inflation in commodity prices eventually and this makes trade prohibitive.

This isn’t theoretical. We’ve seen this pattern play out before. For instance, during the Iran-Iraq Tanker War in the 1980s, commercial tankers were repeatedly targeted, and insurance markets responded with sharply higher premiums. And in late 2023, in the Red Sea, Houthi attacks pushed war risk premiums. When attacks escalated further, premiums reportedly hit 1% of ship value — meaning a million dollars per voyage for a $100 million ship. Traffic didn’t stop, but it collapsed just enough for carriers to reroute around the Cape of Good Hope, adding weeks and enormous costs to journeys.

Can Trump’s backstop fix this?

President Trump has reportedly proposed offering government-backed political risk insurance and financial guarantees to shipping companies operating in the Gulf. This echoes historical precedents — in the Iran-Iraq War, for example, the US Navy escorted and protected tankers through the Gulf.

But there’s an important distinction here that’s easy to miss. Political risk insurance covers government and sovereign actions — things like expropriation, political violence, or currency transfer restrictions. War risk insurance covers missiles, mines, and direct hostilities. They’re not the same product, and a political risk policy may not substitute wholly for war risk cover. This, perhaps, is why insurance costs surged 12 times even after the Trump guarantee.

Even if the backstop is structured correctly, there are practical questions.

Does it cover all vessels, or only US-flagged ones? Does it apply to P&I liabilities, or just hull damage? Can it be activated quickly enough to matter, given that cancellation notices are measured in hours? And critically, will reinsurers treat a government guarantee as sufficient to restore their own appetite, or will they remain cautious regardless?

A state backstop helps at the margin. But it doesn’t get the market to flip on their consensus that the new risk is too correlated and too volatile to bear.

The lines are drawn

Marine insurance is invisible when it works, but catastrophic when it doesn’t. And war is a risk like no other. The crisis in the Gulf has shown how thin private risk appetite can be. But in some ways, it is justifiably so, because how do you put a price to war?

And even when the immediate military tension subsides, the question won’t be whether the shooting has stopped. It will be whether the Joint War Committee still lists the area as high-risk, whether reinsurers are willing to restore capacity, and whether premiums come down enough for the economics of transit to work again.

Until all of those boxes are ticked, trade through the Gulf stays frozen.

India faces a monetary policy dilemma

India’s economy has always been, and still is, founded on the base of its banking system — unlike in advanced economies like the US or Singapore, where capital markets play an outsized role. When a business in India needs to raise funds, it walks into a bank branch first.

So, if there’s any decision to be made on monetary or fiscal policy, the central bank of the government largely expects our banks to cooperate. When the RBI makes rate cuts, for instance, the expectation is that banks will pass those cuts on, making credit cheaper and more plentiful.

But banks don’t always listen. Rather, they don’t always have the incentive to do so.

We’ve covered before about how, even after the RBI’s rate cuts, transmission to actual lending rates was sluggish. We’ve also explored how high inflation expectations can blunt the effect of rate cuts. But what about the banks themselves? What makes some banks more responsive to the RBI’s signals, and others less so?

A paper by researchers at the Indira Gandhi Institute of Development Research (IGIDR) — Rajeswari Sengupta, Harsh Vardhan, and Akhilesh Verma — digs into one specific factor that shapes how well monetary policy works: the capital sitting on a bank’s balance sheet. Their findings reveal an interesting dilemma in Indian banking.

Let’s dive in.

The hypothesis

The hypothesis of the paper is this: when the RBI raises short-term rates in an attempt to control bank lending, well-capitalized banks don’t respond strongly. In fact, they continue lending at strength.

But before we get to this, what does it even mean to be a well-capitalized bank?

Think of a bank’s capital as its financial cushion. It’s the money that belongs to the bank’s shareholders, as opposed to what it owes to depositors or bondholders. This also includes retained earnings or reserves that the bank has created.

The simplest way to measure this is the “bank capital ratio“ (BCR): it is the ratio of a bank’s capital and reserves to its total assets. A bank with a high capital ratio has a thicker cushion to absorb losses more easily, and is therefore less likely to fail.

That sounds like an unambiguously good thing. And for financial stability, it is. But the researchers argue that this stability comes with a contradiction.

Say the RBI is worried that banks are doling out loans a little too much, and wants to curb credit supply to prevent the economy from overheating. Then, the RBI raises rates. Higher rates mean that borrowing costs rise for banks. This usually leads them to slow down its own borrowing, and therefore, lending to others.

But a well-capitalized bank has a buffer. It can absorb the higher cost of funds without panicking. It doesn’t need to cut back lending just because rates went up. It has the financial strength to keep the credit taps open. They also have better access to alternative sources of funding.

A weakly capitalized bank, on the other hand, doesn’t have that luxury. When rates rise, it feels the squeeze immediately. Investors also perceive it as riskier. Its margins shrink, its risk appetite contracts, and it pulls back on lending — exactly as the RBI intended.

In an interesting paradox, well-capitalized banks are far less sensitive to rate increases, while banks with thinner capital cushions respond more sharply as per the RBI’s expectation. And in India, banks that are well-capitalized often tend to be among India’s biggest, most important banks.

In its role as a banking regulator, the RBI does want banks to be well-capitalized — that’s what keeps the system safe. But as a monetary policymaker, the RBI also needs the big banks to respond to rate changes. Strong banks are stable, but they’re also stubborn.

To test this, the researchers assembled data spanning between 2002-2018 from 18 Indian commercial banks — both public and private. They tracked the relationship between short-term interest rates and how much credit banks supplied. The key question: does a bank’s capital ratio change how sensitively it responds to monetary policy?

What the data says

The headline finding confirms the hypothesis.

A 100 basis point increase in short-term rates leads to roughly a 1.1 percentage point decline in credit growth across the banking system. That’s monetary policy working as intended. But banks with higher capital ratios show significantly less sensitivity to rate hikes. For every percentage point increase in a bank’s capital ratio, the negative impact of a rate hike on its credit growth is reduced by 0.03-0.05 percentage points.

That might sound small. But when you consider that private banks in the sample had average capital ratios of 11.7% while public sector banks averaged just 5.6%, the differences compound quickly. Well-capitalized banks were essentially shrugging off monetary tightening, while their less-capitalized peers were doing the heavy lifting of transmitting the RBI’s signals to the economy.

To sharpen the picture, the researchers split their sample into high-capital and low-capital banks. For well-capitalized banks, the relationship between interest rate hikes and credit growth was insignificant — rate changes barely moved the needle on their lending. For banks with low capital ratios, the relationship was strong and negative: when rates went up, these banks cut lending meaningfully.

The public vs. private divide

Perhaps, the one thing that seems clear from this is that private banks, with their higher capital ratios, are more insulated from rate hikes than public ones. The researchers found that for private banks, their capital cushions were genuinely protecting their lending from rate hikes. For public sector banks, though, the effect was statistically insignificant.

This makes intuitive sense if you look at how these two types of banks raise funds. Private banks go to the capital markets, typically raising large amounts at strategic intervals to sustain lending over 4-5 years. They tend to maintain capital ratios well above regulatory minimums.

Public sector banks (PSBs), by contrast, rely on government capital injections, which are just enough to keep them above the regulatory floor. During the 2014–2018 non-performing asset (NPA) crisis, for instance, the government poured around ₹4 trillion into PSBs to prevent them from breaching minimum requirements. This was funding purely meant for survival.

The NPA complication

The story doesn’t end here, either. The researchers also found that asset quality dramatically changes the picture.

Between 2002–2013, on a relative level, banks didn’t have a lot of NPAs, and their books were relatively clean. That’s when the capital buffer worked exactly as predicted: well-capitalized banks absorbed rate hikes and kept lending.

But between 2014-2018, banks’ balance sheets were burdened with NPAs. This was a period when the banking system was rocked by debt crises among many infrastructure players, like Bhushan Steel, Essar Group, Jaypee Group and so on. We also covered this crisis briefly with our story on DHFL. In this period, even well-capitalized banks started pulling back.

The reason is obvious: when a loan goes bad, the bank has to set aside provisions to cover potential losses, which erodes its effective capital. During the NPA crisis, many banks’ reported capital levels overstated their true financial strength. The cushion was there on paper, but it was being consumed by bad loans in practice. There was hardly any space for the capital buffer to absorb monetary policy.

The other side of the coin

Here’s the catch to all of this: so far, we’ve talked about what happens when the RBI raises rates to curb lending. But what about when the central bank cuts rates to stimulate lending?

A 2016 paper by researchers from the Bank for International Settlements (BIS), Leonardo Gambacorta and Hyun Song Shin, sheds light on this. Their findings look like they flip the first paper on its head, yet are actually consistent with that paper’s findings.

The BIS researchers found that well-capitalized banks respond much more vigorously to rate cuts. A 1 percentage point increase in the capital ratio was associated with 0.6 percentage points of additional annual lending growth. The logic behind this is that better-capitalized banks pay less for their own funding — roughly 4 basis points less for every 1 percentage point increase in their equity ratio. Depositors and bondholders see them as safer, so they demand lower returns. Lower funding costs mean more room to lend.

This was particularly relevant during the post-2008 period, when central banks around the world were desperately trying to restart credit creation. The banks best positioned to expand lending when rates would fall were the well-capitalized ones. The weakly capitalized banks, burdened by losses and fearful of further deterioration, wouldn’t lend even as money became historically cheap.

Is this a contradiction with the IGIDR paper? Well, not really. In fact, they agree on the effect of a rate increase on well-capitalized banks! The insight from Indian banks does, to some degree, apply internationally as well. Both papers agree that, either which way, a bank’s capital is an extremely useful buffer. Poorly capitalized banks, meanwhile, cut lending when rates rise (good transmission), but they also fail to expand lending when rates fall (bad transmission).

But where the two papers differ in nuance is the subject of analysis. IGIDR focuses entirely on India, a developing country with a financial system where banks dominate over capital markets. If the RBI’s decisions aren’t effectively transmitted through banks, there are few avenues to ensure those transmissions work. In contrast, in more developed countries, if banks don’t work, monetary policy can still channel its effects through capital markets.

Where does this leave us?

What does this mean for policy?

For emerging markets, this represents a difficult trade-off. As India grows economically, the private sector will take up a larger role in the system. In turn, that will mean that bank capital will become an increasingly more important factor in monetary policy.

Accordingly, the RBI’s toolkit may need to adapt. It may have to rely less on the assumption that rate changes will automatically flow through to lending, and more on complementary levers like liquidity management, macroprudential regulation, and so on. Monetary policy, as we keep rediscovering, is only as effective as the institutions that carry it out.

Tidbits

India’s services sector growth eases in February — the slowest growth pace in over a year. The HSBC India Services PMI slipped to 58.1 in February from 58.5. On the bright side, international sales rose at their fastest pace since August, and the composite PMI climbed to 58.9 — the strongest private sector expansion in three months.

Source: ReutersChina lowered its 2026 growth goal to a range of 4.5%–5%, the first formal downgrade since 2023. This is China’s lowest target since 1991, as it grapples with deflation, a property slowdown, and rising trade tensions. The budget deficit target stays at a record 4% of GDP, as the government expects to maintain its fiscal spend in order to support demand.

Source: BloombergPNGRB, India’s petroleum regulator, is preparing to propose building storage facilities near India’s eight existing LNG terminals for both commercial use and strategic reserves during emergencies. The move comes as tanker traffic through the Strait of Hormuz has ground to a near-halt following the Israel-Iran conflict.

Source: Mint

- This edition of the newsletter was written by Kashish and Manie.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉