What’s driving Oil Giants back to India?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Private Oil Giants come back home

RBI’s New Gold Loan Rulebook

Private Oil Giants come back home

India's oil refining landscape is a tale of two worlds.

On one side, you have the state-owned behemoths — Indian Oil Corporation (IOC), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL) — that have traditionally focused on serving India's massive domestic fuel appetite. We explored their businesses when we covered their results some time back.

On the other side are the private refiners, led by Reliance Industries and Nayara Energy. They built their business models in the shadow of these state-owned refineries, and so, they had to come up with completely different strategies. If state refiners had cornered our domestic market, they would look outside. They constructed world-class, complex refineries designed to process crude oil and ship the refined products — diesel, gasoline, jet fuel — to markets across Asia, Europe, Americas, and beyond.

Reliance's massive Jamnagar complex, the world's largest single-site refinery which could process 1.4 million barrels daily, was essentially built as an export machine. Similarly, Nayara's Vadinar facility, with its 20 million tonnes annual capacity, was designed to serve global markets.

How do we know that? Just look at the numbers.

In fiscal year 2022–23, Reliance exported 36.1 million tonnes of petroleum products — about 80% of India’s total fuel exports that year. One year later, when India’s exports rose to around 63 million tonnes, Reliance still accounted for an estimated 60% of what we sold.

Nayara Energy was similarly export-heavy. The company exported 4.46 million tonnes of petroleum products during the first seven months of fiscal 2022-23 — roughly 40% of everything they produced.

Why turn abroad? India's fuel market is a bit of a contradiction. While the government officially deregulated petrol and diesel prices in 2010 and 2014, it still controls what consumers pay through heavy taxation. Although Oil Marketing Companies peg themselves to international markets, setting daily prices based on global crude costs, there's the catch: taxes make up over half the price you actually pay. Although the government doesn’t directly dictate prices, it indirectly controls them by tweaking duties and taxes. And it does that often, as you’ll often see in the headlines whenever there’s volatility in oil markets.

Why deal with this? Why compete in India's price-controlled and regulated domestic market when you could sell to international buyers for better and more predictable prices?

For years, this worked brilliantly. Private refiners made the most of export markets — lodging themselves in little niches that yielded steady revenue. But lately, as Reuters reported, that is beginning to change.

The Global Oil Market

When COVID-19 hit, everything changed for the world’s oil market. The pandemic didn't just disrupt supply chains for a short while, it altered global energy consumption patterns altogether. While the immediate disruptions ended with the pandemic; those changes in broader consumption patterns turned out to be more sticky.

This wasn’t always obvious. In fact, in 2022, refiners saw one of their best years ever over what was dubbed a "refining supercycle". The world had under-invested in refining for the larger part of a decade. As the world opened up again, and in the dark days of COVID, refiners were shutting down their units. But then, suddenly, demand came roaring back. With sanctions, war, and all sorts of other market disruptions, a refiner could suddenly command incredible premia. For a short while, if you ran an oil refinery, you were almost certain to make a killing.

But this “supercycle” was based on weak foundations.

Although global oil demand saw a short spike immediately after the pandemic, structurally, the market was no better than before. If anything, it was weakening. After decades of steady growth, overall demand had more-or-less plateaued — and even declined in key markets. China, once the engine of global fuel demand growth, saw consumption peak, and then actually decline slightly in 2024 — as electric vehicles gained traction while economic growth slowed. Europe's fuel consumption remained sluggish, weighed down by high energy costs and aggressive climate policies pushing alternatives to fossil fuels.

This slowdown will probably continue. The IEA predicts that global oil demand growth will slow from 990 thousand barrels per day in 1Q25 to 650 thousand barrels per day for the rest of the year.

The flagging demand, however, didn’t discourage more supply from pouring in.

OPEC+, which historically controlled much of oil production, is finding it harder and harder to control global supply. We’ve written about this before. A steady increase in competition from the outside — production from non-OPEC+ countries, led by the United States, Brazil, Canada, and Guyana, have hurt OPEC+ power and market influence. Meanwhile, beyond production, the world was flooded with new refining capacity as well. Suddenly, there was simply too much oil chasing too little demand.

Both, together, crushed the refining supercycle. Instead, a brutal margin compression hit exporters hard. The benchmark Singapore complex refining margin — a key profitability indicator for Asian refiners — plunged to just $1.6 per barrel in September 2024, the lowest since 2020. European diesel margins crashed from a peak of $30-40 per barrel through 2022 to around $13 per barrel by August 2024.

On the other hand, India

While the rest of the world was grappling with stagnant fuel demand, India has been experiencing the opposite. Our diesel consumption hit a record 91.4 million tonnes in 2024-25, up from 85.9 million tonnes just two years earlier. Gasoline consumption soared to 40 million tonnes, compared to around 35 million tonnes in 2022-23.

The reasons for this growth are straightforward: India is still early to motorising. With only 22 cars per 1,000 people (compared to 821 per 1,000 in the US), there's enormous room for growth.

This is why, if anything, our demand for fuel is only going up. India's car industry had its best year ever in 2024, selling a record 4.3 million passenger vehicles. This broke the previous high of 4.1 million cars sold in 2023, showing that more and more Indians are buying cars. Meanwhile, two-wheeler ownership now reaches over half of Indian households.

Reliance, Nayara and Russia

As demand boomed, Reliance and Nayara kept adding capacity.

Reliance's Jamnagar complex steadily grew its output after pandemic-era lows. Its SEZ facility processed 28.3 million tonnes in 2024, up from 26.8 million tonnes in 2021. And it was also expanding operations aggressively: in August 2022, they announced a $9.4 billion plan over 5 years to expand its oil-to-chemical business.

Meanwhile, Nayara plans to invest ₹6,000 crore in a new petrochemical unit, and another ₹4,000 crore in modernizing its refinery. Meanwhile, it’s current facilities are running on overdrive. It achieved a 101.6% capacity utilization in fiscal 2024 — essentially optimising operations until it ran above its maximum capacity.

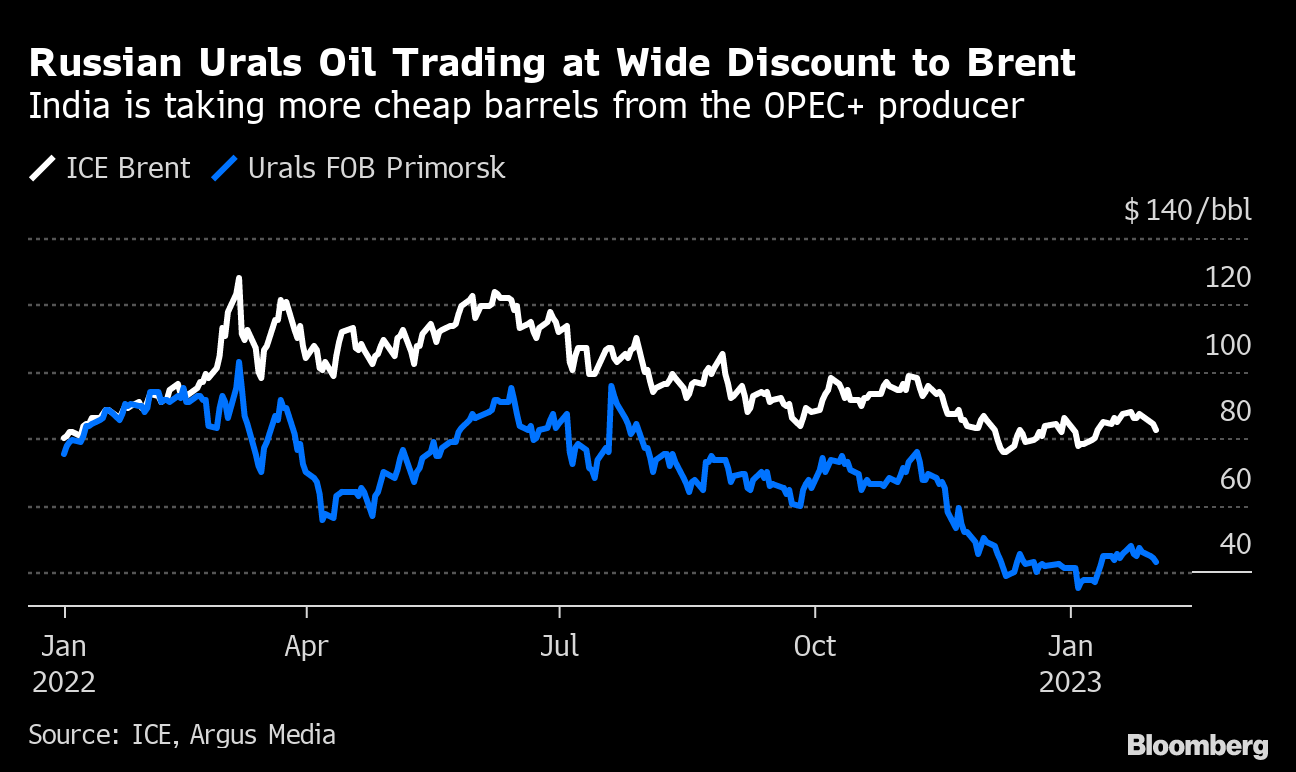

Fuelling this growth was a once-in-a-lifetime tailwind: Russian crude oil. Or more specifically, heavily discounted Russian crude oil.

Before 2022, Russia was a negligible supplier to India. It ranked 17th in our supplier list, with just 1% of our oil imports. But then, everything changed.

When the Russia-Ukraine conflict began in early 2022, Western countries — especially in Europe and North America — started cutting back on buying Russian oil. Many imposed sanctions or outright bans. Others avoided it due to reputational and legal risks. Suddenly, Russia had run out of buyers and needed to find new markets quickly.

To keep its oil flowing, Russian oil started trading at steep discounts against other sources, like Brent crude. The discounts have been substantial. In early 2023, Russian crude was selling at $25-30 per barrel below Brent prices for deliveries to India.

This was a huge opportunity. And Indian refiners, led by Reliance and the Rosneft-backed Nayara, pounced on it. By 2023, Russia became our largest crude oil supplier, accounting for more than 30% of India's total crude imports.

All this oil would, post refining, be sent back to global markets. Only, at this point, that oil was no longer tagged as “Russian oil” — and so, it became palatable for the rest of the world. India essentially came to plug a Russia-sized hole in global oil markets. The very countries sanctioned Russian oil were happy to import it from us instead.

Reliance and Nayara, sitting at the heart of this system, saw incredible returns.

Even today, Russia routinely supplies 35-40% of India's monthly crude imports, making India the biggest buyer of Russian seaborne crude. While the discounts on Russian crude have narrowed recently — to about $2.25 per barrel below Brent by mid-2025 — they still provide a significant cost advantage. Analysts estimate that Reliance's refining margin is about $2 per barrel above the Singapore benchmark, largely due to cheaper Russian crude.

The Market Share Grab

Now let’s add all this together. Global markets are plateauing, even as there’s better demand in India, and they’re seeing better margins from cheaper inputs, i.e. Russian oil, which no one else wants to touch.

And so, Reliance and Nayara are shifting their focus to the domestic market, as Reuters reports.

Both have made quick market share gains. In fiscal year 2024-2025, Reliance and Nayara together captured 11.5% of India's diesel sales and 9.2% of gasoline sales. Just two years earlier, their combined shares were only 5.2% for diesel and 6.7% for gasoline.

Just look at a recent snapshot of the two businesses. Reliance’s domestic gasoline sales jumped 24% year-on-year in the January-March quarter, outpacing overall industry growth. In the same quarter, Nayara’s results showed that they sold 70% of all petroleum products from its Vadinar oil refinery in India, translating to a whopping 48% year-on-year jump in the quarter.

How are they pulling this off?

Distribution, it seems, is key. Their growth came through an aggressive expansion of their retail networks. Reliance's Jio-BP joint venture now operates over 1,950 fuel stations, with plans to invest ₹10 billion annually to expand further. Nayara has built India’s largest private network with over 6,500 outlets and is adding 400 new stations in 2025 alone.

Now, in absolute terms, that’s not all that much — at least when you compare it to the public sector. India has around 64,600 fuel stations, with government-owned oil companies running more than 87% of them. But private players are cutting into this share, and fast.

Beyond the network, in this battle for customers, they’re also challenging the incumbents through pricing. Jio-BP is undercutting state retailer prices by ₹1 per liter on both diesel and petrol. Nayara has been even more aggressive, with discounts of ₹2-3 per liter on gasoline. These might seem like small amounts, but they add up significantly for high-volume commercial buyers like trucking companies. And in a price-sensitive country like India, each rupee matters.

So it’s clear that the companies are focusing on India much more.

But are they diverting their export business to India? Or are they just expanding their market? Is this a pivot, or plain-and-simple growth?

The April data, at least, points to diversion. In April 2025, India's diesel exports plunged to just 1.15 million tonnes — the lowest monthly volume in over a decade since 2012. Reliance, which typically accounts for the bulk of these exports, saw its diesel exports slump to around 0.8 million tonnes as it diverted more fuel to domestic buyers.

Now, don’t get us wrong. This might just be an anomaly. The May numbers, after all, show healthy exports, so the slump might be a temporary blip. We are no experts. But we don’t think so, at least from what Reliance Industries said themselves from their earnings calls. Like this bit on how they’re shifting their focus:

“China, clear reason with the increasing EV penetration also led to some extent by inventory levels were pretty high. The fact that India gasoline demand helped upgrowing 6%. So we continue to focus, as I said, on domestic placement and pushing more volumes here.”

Or this:

“So also, as I mentioned, the whole focus obviously was also on processing the right value of crudes, trying to derive advantage from the value adds coming from crude processing, domestic placements continued as a point.”

Or this estimation of domestic demand:

“Domestic demand has been good. Again, we are trying always to see how much can we maximize light fuel cracking here. And the drivers for domestic demand still remains good and we do expect that to stay.”

Or this bit, on how India compares to foreign stocks:

“Gas oil again cracks — you can see a significant fall, $14 versus 23.1. Again more led by inventories that we saw in Singapore and more exports from the Middle East demand, actually if you see it vis-a-vis other products. India demand was up only about 1.1%. Again the actions were broadly similar in terms of focusing on the domestic market and again some of the supply disruption kind of concerns can keep the cracks at least stable here.”

Bottom line

The strategic pivot by Reliance and Nayara isn’t just a random curiosity — it reflects a clear shift in the world’s oil market, and where the most attractive opportunities lie. Where export markets offer uncertain demand, brutal competition, and compressed margins, India's domestic fuel market offers some respite, with its relatively healthy pace of growth.

Our top energy companies are only reading the tea leaves.

This should always have been a no-brainer. Selling domestically helps one save on freight costs, export duties, and the various risks associated with international trade. On top of that, companies can capture better margins through their own station networks.

So far, perhaps, it didn’t look that way — perhaps because our domestic market was already saturated by the public sector. But in a world where oil demand growth is increasingly scarce, increasingly, a pivot to India is finally emerging as the clear choice.

RBI’s New Gold Loan Rulebook

The world of gold loans in India is set to get a significant makeover.

The Reserve Bank of India (RBI) recently unveiled its comprehensive "Lending Against Gold and Silver Collateral) Directions, 2025", a new rulebook that all banks, Non-Banking Financial Companies (NBFCs), and cooperative banks will need to follow by April 1, 2026, at the latest.

These rules are basically meant to create standards around how banks and Non-Banking Financial Companies (NBFCs) lend to people who bring in precious metals as collateral. It protects borrowers from all sorts of unfair practices and irregularities that RBI highlighted last September — from outsourcing important checks, to making overly large cash disbursements. We covered those too.

If you’ve been tracking this space for a while, you would’ve known that the RBI was thinking hard about what to do about these problems. Well, we finally have some answers.

Today, we’ll unpack what’s allowed (and what’s not) under these new norms, why the RBI made these changes, and how they impact everyday borrowers and gold loan companies like Muthoot Finance or Manappuram.

What’s allowed vs. what’s off-limits

Under the new directions, RBI has made crystal clear what counts as acceptable collateral.

In simple terms, you can only borrow against gold/silver that’s in the form of jewelry, ornaments, or coins. All those necklaces, bangles, or silverware sitting in your locker could be pledged for a loan. Gold or silver coins are allowed too, but only up to a point – more on that in a second.

Then what isn’t allowed?

RBI explicitly prohibits loans against “primary” gold or silver. Basically raw bullion — like gold bars or slabs — are out. If you have a gold bar, sorry, the bank won’t touch it for a loan.

Likewise, you can’t pledge gold-backed financial assets such as Gold ETFs, gold mutual funds units, or Sovereign Gold Bonds as collateral.

In essence, you need to bring gold or silver of the sort that regular people use. Neither paper gold nor pure bullion works.

But let’s say you have the right sort of gold or silver. Can you go on pledging an unlimited amount? Nope. RBI has some ceilings in place to prevent abuse.

For gold ornaments, loans to any single borrower can’t be backed by more than 1 kilogram of gold (which is quite a lot of jewelry!). For silver ornaments, the cap is set at 10 kilograms. But when it comes to coins, the limit is much tighter: all the gold coins pledged by one borrower can weigh no more than 50 grams, and for silver coins the limit is 500 grams.

Once again, there’s a strong preference for precious metals in the form that regular people use. Lenders might accept a few small coins, but not sacks of coins masquerading as collateral.

These caps, it seems, are meant to ensure that the loan-against-gold business remains targeted at household needs rather than large-scale bullion deals.

What this all means for borrowers

But what happens if you take small amounts of the right sort of gold to the bank? Is it going to be easier or harder for you and me to get a gold loan now?

The answer is a bit nuanced. Let’s look at three things.

How much money do you get?

Small borrowers actually get a boost under the new rules.

If you need a modest loan for personal use — what RBI calls a “consumption loan” — you can now borrow money worth a larger chunk of your gold’s value. The “loan-to-value” (LTV) ratio has been set at 85% for loans up to ₹2.5 lakh. That is, for every ₹100 worth of gold that you pledge, you can now get a loan worth ₹85.

This is higher than the old informal norm of ~75% LTV that many lenders followed.

In practical terms, if your gold is worth ₹1 lakh, you would be eligible for an extra ₹10,000 in loan. But that’s for small borrowers. As the value of your gold goes up, the amount you’re eligible for drops. You get 80% LTV for loans between ₹2.5–5 lakh, and 75% for loans above ₹5 lakh.

How much paperwork do you need?

The RBI is also making life simpler for small-ticket borrowers by not overburdening them with paperwork.

Loans up to ₹2.5 lakh won’t require a detailed credit assessment of your income. At that small scale, your gold itself is enough security. If you’re not doing too well, and have been thrust into a position where you’re pledging your jewellery to make ends meet, the RBI plans to make things easier. So, if a small-scale farmer’s wife pledges a necklace for a ₹50,000 emergency loan, for instance, the lender shouldn’t ask for elaborate proof and paperwork.

On the flip side, if you’re taking a larger loan (above ₹2.5 lakh), expect more questions. Lenders will do a detailed assessment of whether you can repay them, treating it more like a regular loan. This makes sense — the bigger the loan, the more risk the bank is taking. Besides, the RBI is basically pushing responsible borrowing, so people don’t end up in over their heads in debt just because they had a lot of gold to pledge.

No more roll-overs

The RBI is making yet another borrower-friendly tweak: in how interest and repayments can be structured.

Gold loans are often ‘bullet loans’. That is, the whole amount — principal and interest — comes due in one shot. RBI is still fine with that, but now, if you’re taking such a loan, it can only have a maximum 12-month term. You can still renew or roll over the loan, but only if you’ve paid off the interest that accrued for that period first.

So you can no longer have indefinite rollovers, while interest quietly keeps piling up. This might sound restrictive, but it protects borrowers from the shock of a massive interest bill later. If you want to keep the loan beyond 12 months, you need to make sure you’re constantly clearing out your interest — even if you pay the principal itself later.

Safeguards and Consumer Protections

Perhaps the brightest spot in the new regulations is the slew of consumer protection measures. Here are some key safeguards now in place:

Transparent Valuation: Lenders must have a standardized process for weighing and testing the purity of gold/silver across all their branches. No more guesstimates. If your gold bangle is 22 karat, the bank should value it at 22k rates, and publicly disclose how they calculate the value. And they can’t fib. You, as the borrower, now have the right to be present when they test your gold. If they’re making any deductions (for stones, etc.), they’ll have to give you a certificate detailing the item’s weight and purity.

Secure Storage: Your lender will have to do a lot more to keep your jewellery safe. As per these rules, your gold/silver collateral can only be handled only by the lender’s own employees. They can only keep it in branches with proper vaults and security. This is one place where regulations are catching up with industry standards — many big NBFCs already insure and secure their gold stock. But now, it’s a uniform requirement. If a branch doesn’t have a secure vault, it simply can’t lend.

Timely Return of Jewelry: Once you repay your loan in full, the lender must return your gold within 7 working days (in fact, ideally on the same day). If they delay without a good reason, they have to pay you a hefty penalty of ₹5,000 for every single day of delay.

If a borrower is scared of trusting a lender with their most precious possessions, these should give a lot more comfort and confidence. Now there’s a rule and process for nearly every stage of the transaction, from valuation to storage to auction, with the borrower’s interests explicitly safeguarded.

Implications for Gold Loan Companies

That’s that for borrowers. What do these new rules mean for the companies whose bread and butter is lending against gold? Think of the likes of Muthoot Finance and Manappuram Finance, the dominant gold-loan focused NBFCs, as well as banks like Federal Bank or Indian Bank that have sizable gold loan portfolios.

By and large, the changes bring both opportunities and responsibilities for these lenders.

First, the new rules level the playing field between banks and NBFCs. It could have gone either way; in the draft version of these rules, there was a controversial disparity: banks would have been given more leeway on loan-to-value for certain loans, which NBFCs wouldn’t get. The final rules removed this bias and made sure NBFCs aren’t put at a disadvantage.

Net-net, these new rules could expand business. With higher permissible LTVs and the ability to give “top-up” loans (additional loan on the same pledged gold) within the overall LTV limit, gold loan companies might see an increase in demand. In fact, the shares of major gold loan NBFCs, such as Muthoot Finance, shot up when the rules came out.

But it’s not all sunshine.

With all the new checks and processes the RBI is bringing, gold loan providers will need to step up their compliance and process game. While it’s allowing these companies to lend a little more, in exchange, the RBI is demanding standardized procedures, better record-keeping, and greater transparency. This doesn’t come for free. For large NBFCs like Muthoot/Manappuram, this likely means investing in staff training and IT systems upgrades to ensure every branch follows the new rulebook to the letter.

Consider this: under the new rules, valuations must be uniform across branches, and the method for valuing these loans must be published on the company’s website. That binds these NBFCs. For instance, even if you’re in a small rural branch, you can’t wing it with a handheld test if the SOP asks for a karat meter.

But that’s mostly for the good. Such standardization could increase operating costs a tad bit, at the same time, it also builds trust with customers.

If borrowers fail to repay these loans, the auction process, too, will need revamping. These companies will have to give adequate notice and even advertise auctions in newspapers now, which could delay recoveries and add cost. They also can no longer figure out side-arrangements, like quietly sell pawned gold to sister concerns or friendly jewelers. Related parties of the lender are barred from bidding in auctions to avoid conflicts of interest.

Frankly, this might not mean that much of a shift, at least for the players that dominate the space. If anything, gold-loan specialists might actually welcome many of the rules. They’ve already adopted similar practices over years of experience, and the rest of the industry will not have to catch up. Muthoot Finance, for instance, often highlights its robust safe-room infrastructure and transparency. Now all lenders, including small cooperative banks and new fintech-backed NBFCs, have to meet these standards.

For one, this raises the overall industry credibility. For the big players, it could even be a competitive moat – they can handle the compliance burden, whereas a smaller lender might find it costly to, say, install vaults in every branch or implement rigorous audits for gold purity.

Conclusion

In India, gold isn’t just an asset, as it is in so much of the world. It’s an emotional and financial lifeline for many. Given this fact, the new RBI regulations are a significant development, that’ll impact many households across the country.

The new directions try to strike a balance — between enabling people to borrow against their gold/silver for genuine needs more easily, and ensuring that lenders act responsibly and transparently. Borrowers stand to benefit from potentially higher loan amounts and stronger protections. At the same time, lenders get a clearer rulebook and the chance to innovate (within limits) on gold loan products, which could expand the market responsibly. This could create some temporary hiccups. But in the long run, for a country like ours, a better defined and more stable gold loan regime leaves everyone better off.

Tidbits

Shein-Reliance Target 1,000 Indian Suppliers as Export Plans Take Shape

Source: Reuters

Fast-fashion giant Shein and Reliance Retail plan to scale up their Indian supplier base from 150 to 1,000 within a year, with ambitions to begin exporting India-made Shein-branded apparel to the U.S. and UK in the next 6 to 12 months. The partnership, which reintroduced Shein to India under a licensing deal in February 2024, has already contracted 150 garment manufacturers and is in talks with 400 more. The Shein India app has seen 2.7 million downloads so far, with 120% average month-on-month growth. Local production currently offers around 12,000 designs, compared to 600,000 on the U.S. site. Reliance is evaluating supplier capability to replicate Shein’s global bestsellers and is working on building synthetic fabric capabilities where India lacks strength. The company is also exploring small-batch, on-demand manufacturing beginning with just 100 pieces per design.

India Set for Sugar Production Rebound After Drought-Driven Slump

Source: Reuters

India’s sugar production is projected to rise to 35 million metric tons in the 2025/26 season, marking a near 20% increase over the previous year, according to the National Federation of Cooperative Sugar Factories. This expected recovery follows two consecutive years of drought that saw net sugar output fall below domestic consumption for the first time in eight years. The turnaround is driven by unseasonally heavy May rains—1,007% above average in Maharashtra and 234% in Karnataka—which have improved soil moisture and spurred a rise in sugarcane acreage. Farmers are planting more cane, anticipating better returns. With annual consumption estimated around 27–28 million tons, industry estimates suggest India could allow over 3 million tons of sugar exports starting October 2025. India had previously exported an average of 6.8 million tons annually between 2018 and 2023 but restricted exports entirely in 2023/24 and limited them to 1 million tons in 2024/25 due to tight domestic supplies.

TP Solar Crosses 4 GW Milestone at Tamil Nadu Plant, Targets FY26 Ramp-Up

Source: Business Line

Tata Power’s solar manufacturing arm TP Solar has achieved a cumulative production of 4,049 MW of solar modules and 1,441 MW of solar cells at its Tamil Nadu facility as of May 31, 2025. The plant, built to meet Domestic Content Requirement (DCR) norms, is equipped with advanced manufacturing lines for Mono PERC and TopCon technologies. With a rated capacity of 4.3 GW, TP Solar expects full realisation in FY26 and has set a production target of 3.7 GW for solar cells and 3.725 GW for modules in the same fiscal year. The facility also supports Tata Power’s utility-scale projects, rooftop systems, and third-party installations. Additionally, the company operates a 682 MW solar module and 530 MW solar cell plant in Bengaluru.

- This edition of the newsletter was written by Prerana and Kashish.

📚Join our book club

We've started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we'd love to have you along! Join in here.

🧑🏻💻Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We've been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls "polycrisis" thinking to connect the dots.

Frames for a Fractured Reality - We're struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze's "polycrisis" concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We're facing humanity's most profound identity crisis as AI matches our cognitive abilities. Using "disruption by default" as a frame, we assume AI reshapes everything rather than living in denial about job displacement that's already happening.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉