We're measuring rooftop solar by the wrong number

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s rooftop solar problem

What happened to the world’s electricity in 2025

India’s rooftop solar problem

For years, there was one story we told ourselves about rooftop solar in India: that Indians didn’t know enough about it, or didn’t trust it. They found it too expensive, too complicated, too foreign. This pointed to one answer: if only we could get the word out, running campaigns and explaining the savings it could fetch, adoption would follow.

But that story, it turned out, was mostly wrong. The truth is more interesting, as we learnt from two new reports from the Council on Energy, Environment and Water (CEEW) — one on what drives household decisions to install rooftop solar, the other on what happens to the system once it’s up there.

Here’s the short version: India has nearly solved the demand problem. People know about rooftop solar, and a lot of them want it. What it hasn’t solved, however, are two gaps sitting on either side of that desire: one, the gap between wanting solar and actually installing it, and two, the gap between installing it and actually generating power from it. Both these gaps often seem invisible, because the only number anyone usually quotes is “installed capacity”, which tells you nothing about either. Without fixing them, however, we’re likely to find our solar ambitions stuck.

Let’s walk through both.

Wanting solar isn’t the bottleneck

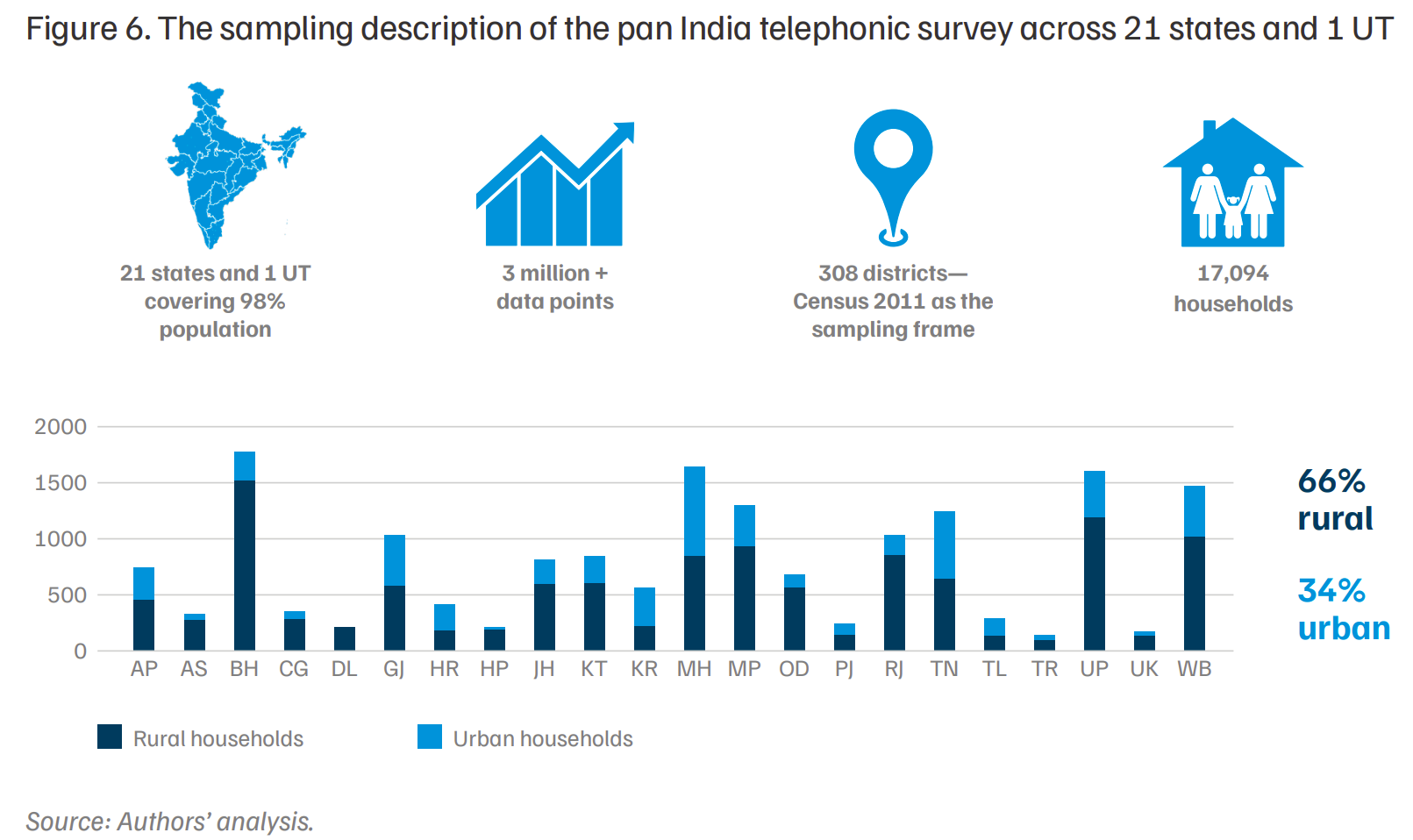

When you hear about Indians not installing enough solar panels on their roofs, one’s impulse is to assume that there isn’t enough awareness, or willingness, to make such a shift. To test this, CEEW went to 17,000 households from 308 districts across India. Their survey demolished the notion.

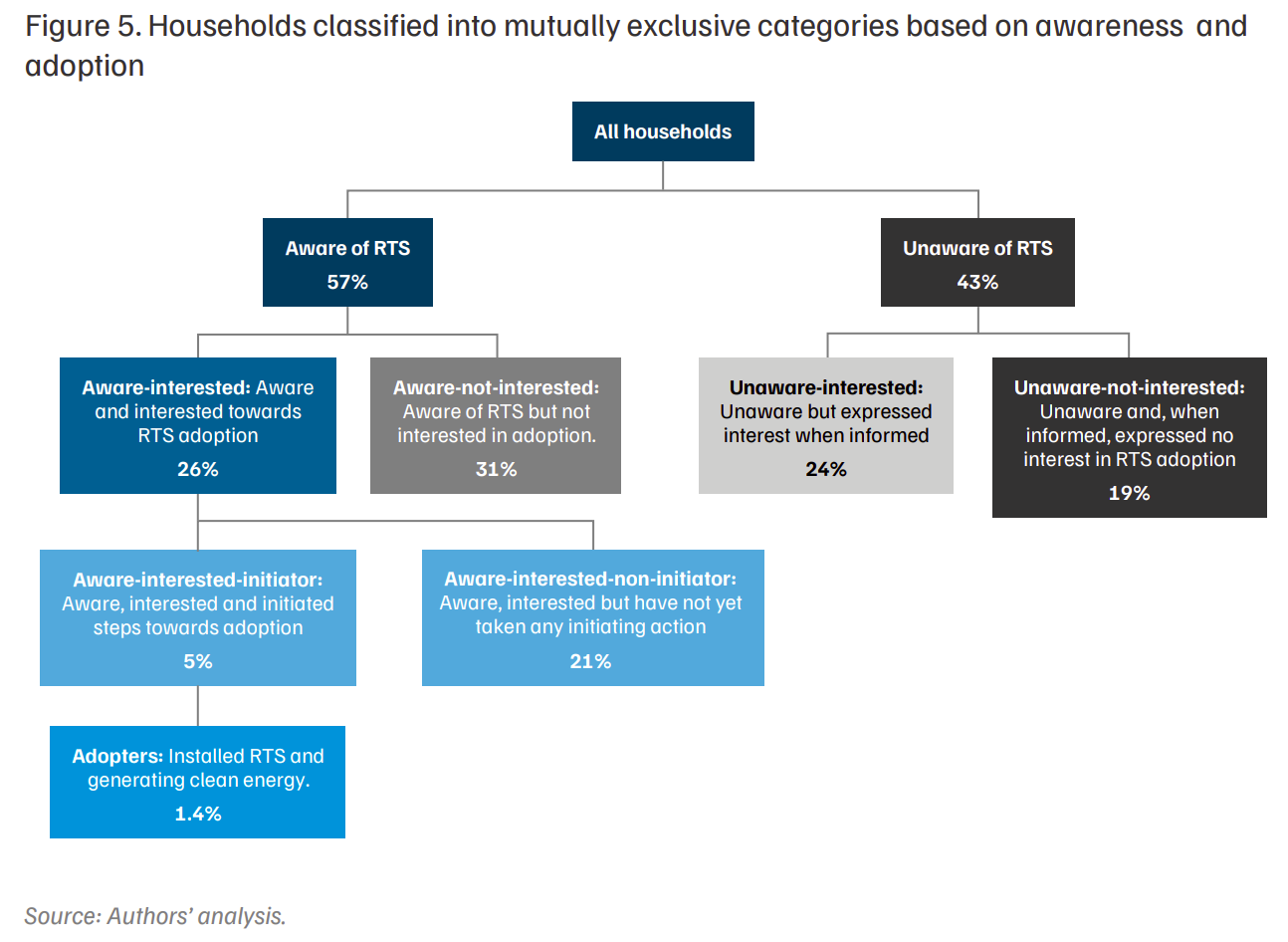

Indians clearly know about rooftop solar installations and their merits: around 57% of the households they surveyed were specifically aware that this was an option available to them. Moreover, roughly a quarter of all households they surveyed were willing to install solar panels on their rooftops. Not just that: even among the 43% of respondents that didn’t know about this option, roughly half were willing to adopt the technology once it was explained to them.

If there was so much interest, however, where did the problem come from?

Well, as the survey found, of every ten households that are willing to go solar, eight never even begin the process. That’s an 80% drop-off rate between interest and action. It is the main leak that keeps solar adoption at bay. The point where a household is supposed to turn intent into action is the one where they instead check out.

This raises the two questions we’ll try to answer through the rest of this story: one, what’s stopping willing households from installing solar panels? And two: assume they do install them. Do those installations actually work the way they’re supposed to?

The biggest barrier is the cheapest to fix

Put yourself in the shoes of a family that is ready and willing to make the leap. What would stop you? Money? Availability? Logistical challenges?

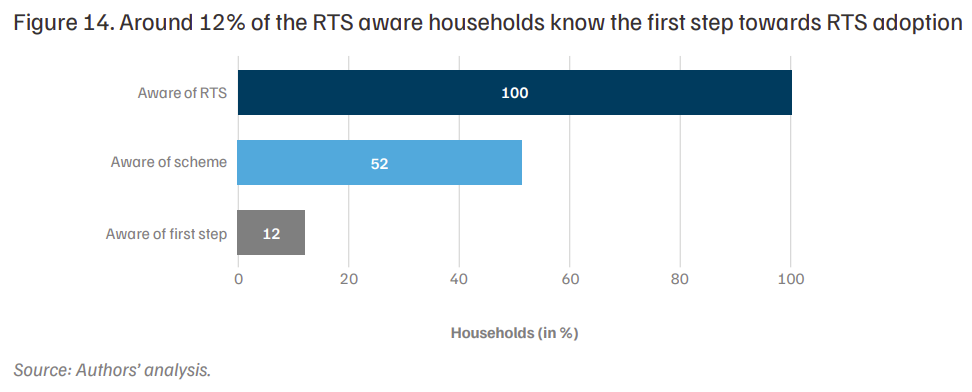

The biggest reason — one cited by roughly 68% of everyone they surveyed — was that they simply don’t know how to begin. The entire process is a fog. Simple questions — what the first step is, who you call, where you sign up — have no clear, well-publicised answers.

That changes how you would address the problem of low interest. If affordability were the problem, you would try coming up with schemes to make it more attractive. That’s what we’ve done with subsidy schemes like PM Surya Ghar: Muft Bijli Yojana. The actual problem is more basic, however. People know that rooftop solar installations are a problem, but they know little else about it. Only 12% of those who knew about rooftop solar as a concept, for instance, knew that the first step in this journey is to register on a national portal.

Without simple process knowledge being widely available, everything else falls flat.

In some ways, this is good news. Fixing an informational barrier is relatively cheap. We don’t, for instance, need to pump another few thousand crores in subsidies before we can make a dent. As the CEEW says, the gap is “entirely recoverable through targeted communication.” A single, well-designed handholding campaign could move more people into rooftop solar than a massive round of subsidy hikes.

Who actually goes solar

What does a success case look like? How did the roughly 1.4% who actually installed solar panels get there?

Well, there’s one thing they have in common: they’re rich.

Adoption among high-income households runs at about roughly ten times the rate among low-income ones. The typical adopter has an electricity bill about 50% higher than a non-adopter, and runs a much heavier load of appliances, like air conditioners or geysers. For these people, the economics is a no-brainer: they need more electricity, which would otherwise generate higher bills, but a solar installation can cut through those bills fast.

Unfortunately, rooftop solar spreads largely by word of mouth. Word of mouth travels within social networks, and social networks largely cluster by income. If the only pool of adopters is overwhelmingly wealthy and high-consuming, those are the only people to whom word can spread. Left to its own devices, that gap will only widen, with rooftop solar circulating within the affluent, while quietly skipping the low-income and rural households the policy should reach.

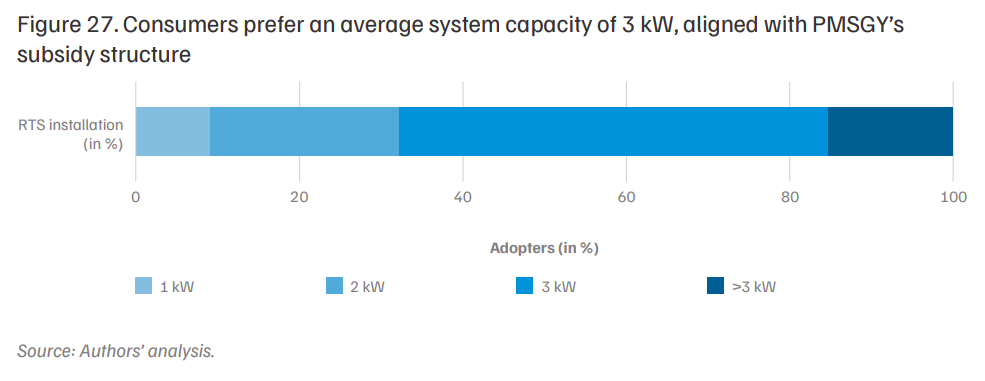

Within those affluent adopters, meanwhile, adoption is underpowered. The PMSGY subsidy is capped at a 3 kW system. This creates bad incentives: even though most adopters’ actual electricity needs are larger than 3 kW, they deliberately undersize their systems to make the most of the subsidy.

Meanwhile, the households the scheme most wants to reach — those with low-consumption and smaller bills — barely have an incentive to do so, because with smaller bills, any installation takes much longer to pay for itself, making such an investment unattractive.

That creates a weird paradox: our current subsidy structure doesn’t do enough to attract those that need financial assistance, while those that could afford it anyway end up under-powering their systems.

What happens after that? Assume a system actually does go up, as intended. Does it actually work?

Installing solar and generating power are not the same thing

Solar energy statistics have a problem: it’s too easy to celebrate statistics on installed solar capacity, without a real sense of how much electricity flows out. Often, the two numbers can diverge wildly. A solar panel can make for “installed capacity” even if it does nothing but accumulate dust. That panel might make it easier to hit the paper objectives of government schemes, without actually doing anything.

The ugly truth is that installing solar power only begins a process of generating renewable energy. After that comes maintenance, cleaning, and the diagnostics that determine whether a system can keep performing for the next 25 years.

This harder task is performed by a fragmented, unstandardised private vendor ecosystem. These vendors can decide the difference between a wasted investment, and years of lower bills. Only, the system rarely works as intended.

Often, a rooftop solar system can break down for the insultingly mundane reason of there being too much dust. That dust, along with similar problems like bird droppings, is the single most common and underrated drag on rooftop solar performance. Dust alone can cut down a solar panel’s efficiency by as much as 60%. And if it continues unaddressed, those panels can suffer localised over-heating, which can crack glass or, in the genuinely bad cases, start a fire.

This shouldn’t be such a big problem, in theory. The PM Surya Ghar scheme comes with five years of free maintenance. Every installer is mandated to provide it. This should cover most houses.

Only, in practice, that coverage doesn’t come close to living up to its billing. The scheme, sadly, never defined what that maintenance actually has to include. It defined no minimum scope, and no required frequency of visits. So in practice, that “maintenance coverage” shrinks to the bare minimum.

The most performance-critical task — cleaning the panels — is routinely excluded, treated as the consumer’s responsibility rather than the vendor’s. All a vendor covers is basic electrical checks. This too is reactive — vendors only show up when something visibly breaks, rather than on schedule.

Worse still, none of this is even free, really, as these costs are often baked into the upfront installation price. And because the vendor has already collected the maintenance money upfront, they have no financial reason to ever proactively show up and service the system.

Most people don’t even realise that this is a problem. Of the 93% of rooftop solar adopters that claim they’re satisfied, half don’t even know they have a maintenance contract. Almost half of them never check how much power their system is producing. They notice their bills drop at first, but think little more of it. Sadly, bad maintenance doesn’t announce itself. A panel loses output slowly and quietly, and a household with no way to track generation simply won’t notice.

To be fair, not every vendor plays it this way. Some are building their whole pitch around the opposite approach — proactive maintenance instead of reactive, apps to track real-time power generation, and savings guarantees that only hold up if the panels actually keep performing.

SolarSquare’s “GoodZero” plan is one example: when you promise a household a guaranteed output, O&M stops being an afterthought and becomes core to the business. This is partly why Zerodha’s Rainmatter has invested in SolarSquare.

What underperformance costs

What happens when a system underperforms?

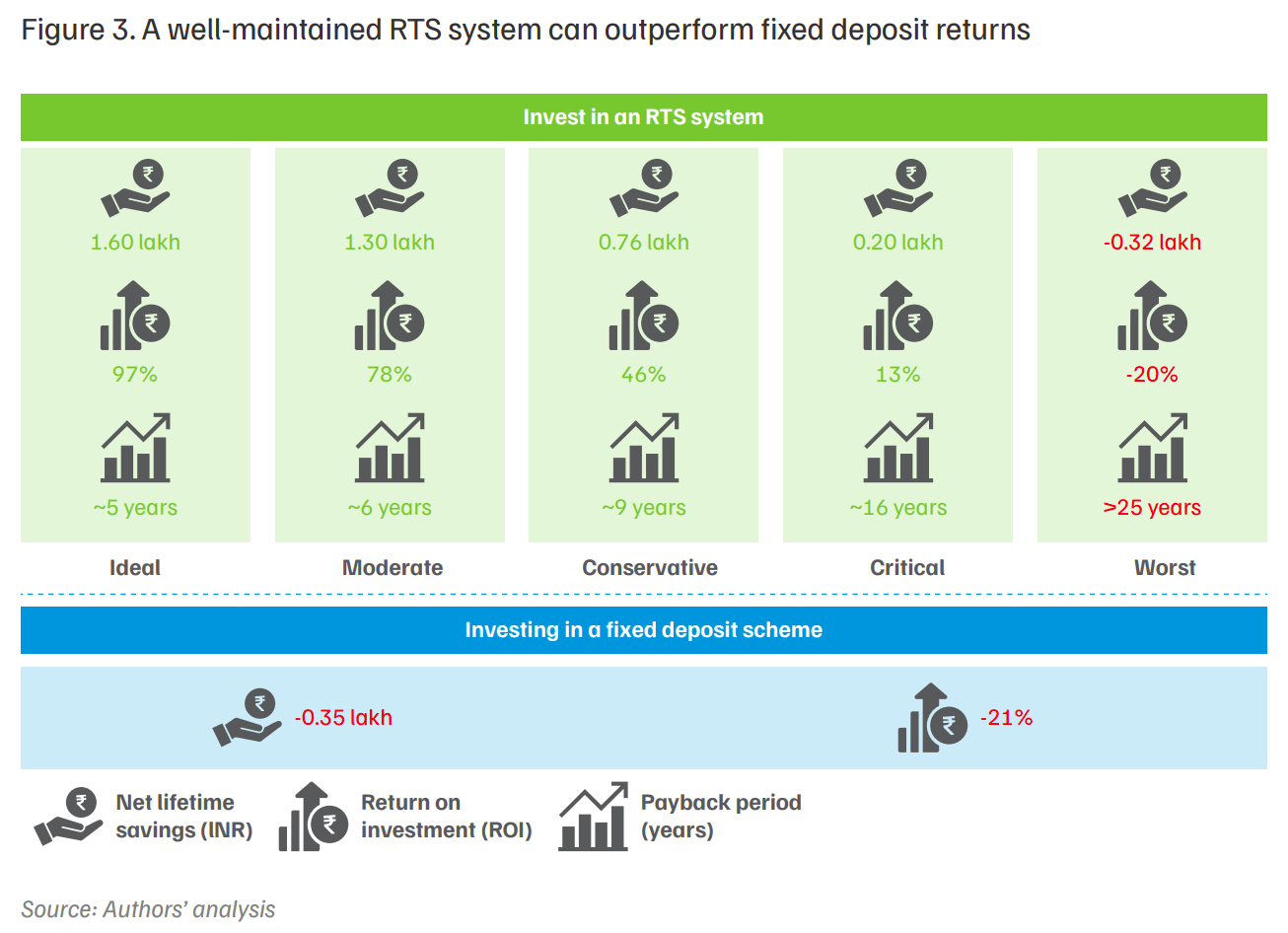

CEEW modelled a well-maintained system against progressively more neglected ones. The damage, they realised, cascades to three groups at once.

Households see a dramatic swing when the system is maintained properly. A well-run 3 kW system pays for itself in about five years, comfortably beating the returns from parking that money in a fixed deposit. A badly neglected one, on the other hand, can stretch the payback past the system’s entire 25-year lifespan. Essentially all of its lifetime savings can vanish.

For the discom, meanwhile, this becomes a lost opportunity. To most discoms, every unit of power they supply to a household is a small loss they have to book. Rooftop solar promises to reduce that burden. Should it fail, however, it causes what the report calls the “grid-rebound effect”: where households simply go back to the grid. This causes a double-whammy — because the discom planned around power that never showed up, it can end up scrambling to buy replacement supply at short notice.

Meanwhile, for the government, that amounts to crores in wasted subsidies, and emissions that are not being cut. Moreover, since many states subsidise residential electricity, the government effectively pays a subsidy twice.

The gap could be a business

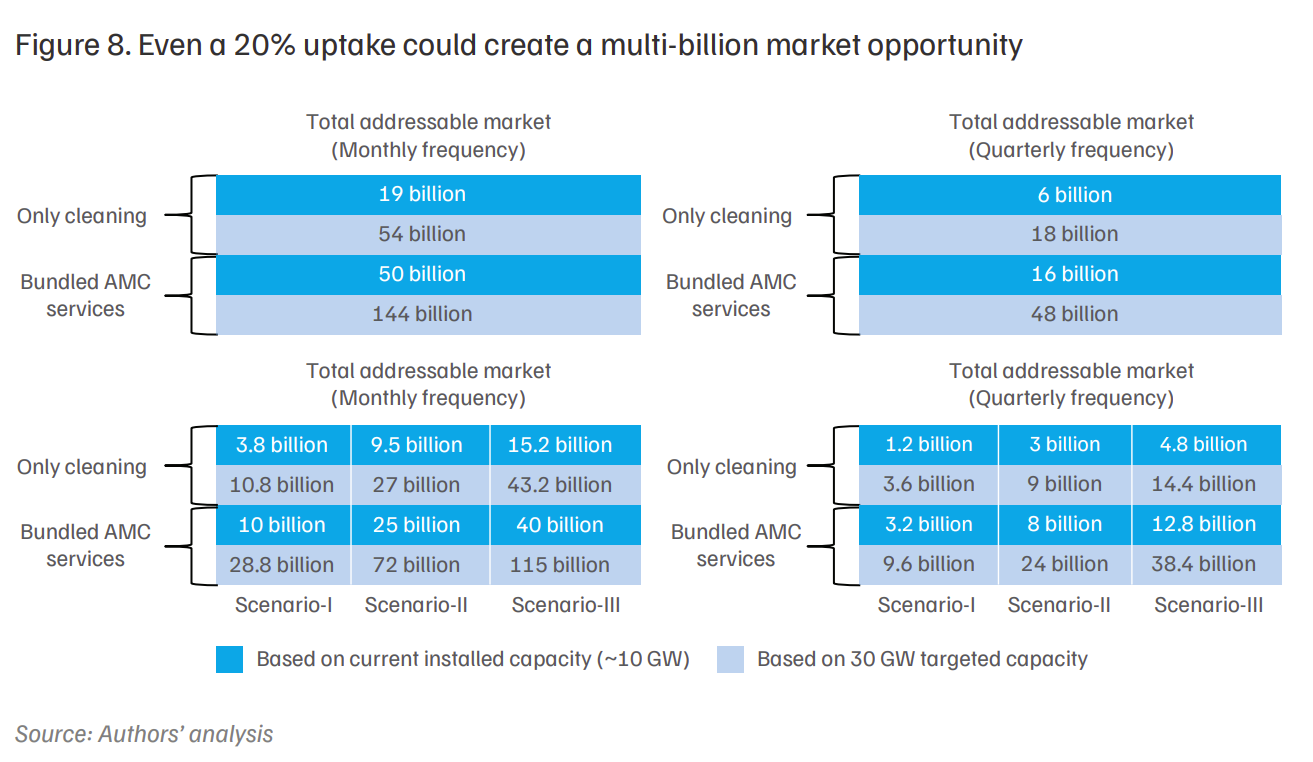

There’s a flip side, though: Every panel installed today, from the moment it’s switched on, is a system that will need cleaning and servicing for the next two decades. That recurring need is a market. As installations scale toward the 30 GW national target, CEEW sizes that market at anywhere from the tens to the low hundreds of billions of rupees a year.

With that come jobs: cleaning, diagnostics, inverter servicing, performance monitoring, and more, across millions of rooftops. To CEEW, if we hit the 30 GW residential target, that could create around 3.3 lakh dedicated jobs in operations and maintenance alone.

Two halves of one unfinished job

India spent a decade learning how to make people want rooftop solar, and with PM Surya Ghar, it largely cracked it. Every solved problem, however, only points you to the next, unsolved one. There are two of those ahead: willing households struggle to get started, while installed systems choke on dust and die down. Neither shows up in installed capacity — the one number everyone tracks.

What happened to the world’s electricity in 2025

Every year, the climate research organisation Ember puts out what is probably the most detailed look at how the world’s electricity system changed over the past year. The latest version of the flagship publication — the Global Electricity Review 2026 — came out a couple of weeks ago. That, as you’ve probably realised by now, is a perennial fascination for us, over at The Daily Brief. And so, we thought we would take you through it.

Naturally, we aren’t going to cover every word of a 119-page report. We’ll limit ourselves to a few themes that genuinely stood out to us. If you’re interested in the energy space, however, we recommend reading the full thing.

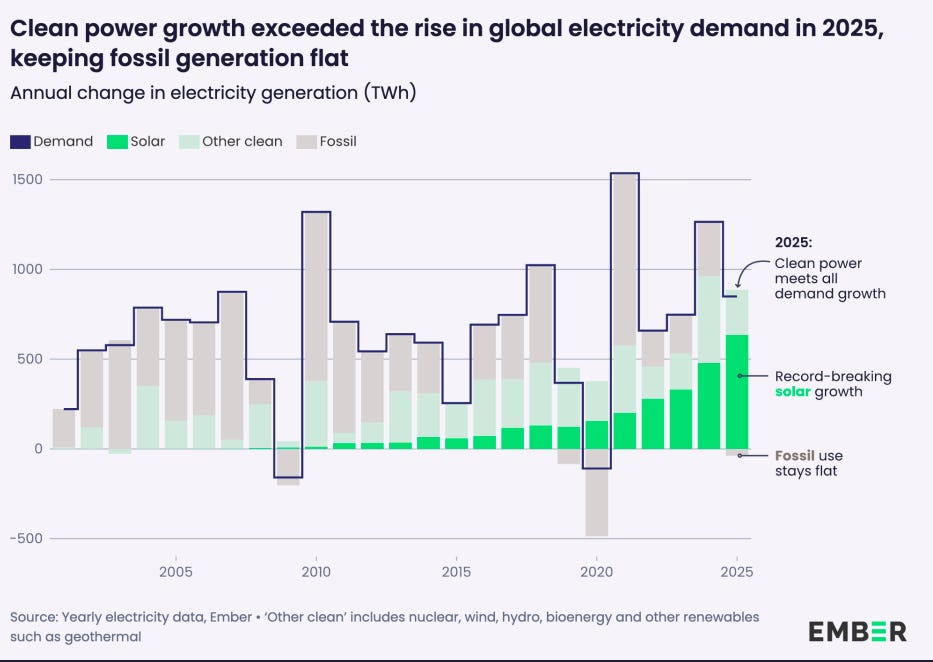

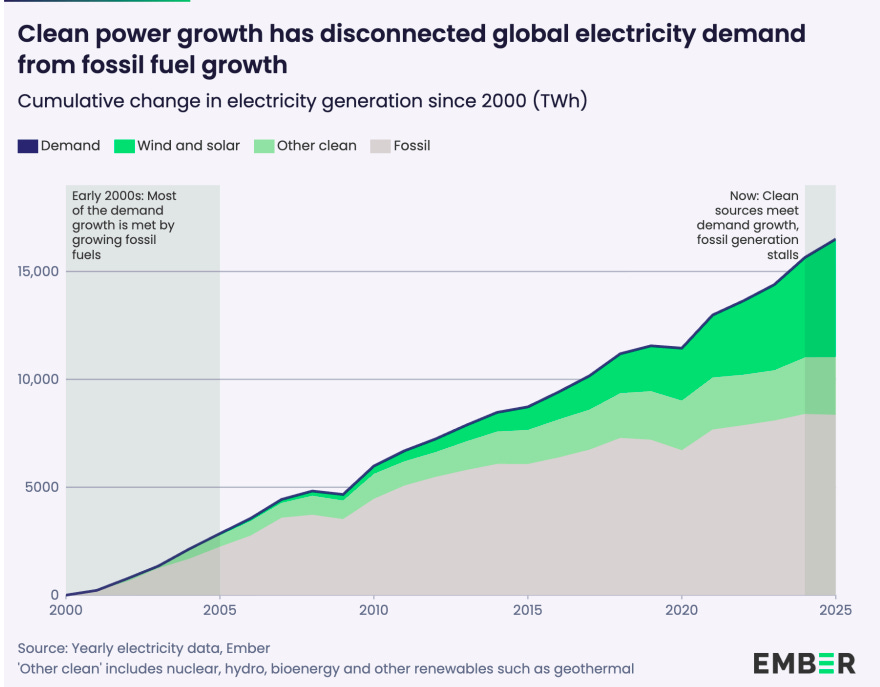

One of the biggest findings of this report sounds deceptively simple: the world generated more electricity last year, without burning more fossil fuels. This has happened four times before — but those years were marked by something unusual: a recession, a pandemic, or unusually mild weather. This was the first normal, anomaly-free year which saw such a shift.

Why is that a big deal? For that, you have to understand how electricity has always worked.

The iron rule that just broke

Electricity generation, as an industry, has been around for roughly 140 years. That entire period was marked by a consistent pattern: as economies grew, people needed more power, and fossil fuels filled that gap. After all, coal and gas were cheap, reliable, and available at scale. Everything else was marginal.

The intensity of that relationship, however, has dipped with time. In the late 2000s, when the world needed more electricity, fossil fuels provided 73% of that additional generation. Between 2015 and 2019, that share dropped to 36%, as renewables started becoming serious contenders. Between 2020 and 2024, it dropped further to 29% of our additional electricity needs.

Last year, the trend finally reached its logical extension: zero.

What, then, took its place?

Renewables, of course. But not all of them in equal measure. Solar energy singularly powered 75% of all new electrical demand on earth, last year. Most of the rest came from wind. Together they covered 99% of new demand.

The sheer scale of solar’s rise is hard to wrap one’s head around.

As recently as 2015 — a short hop in time away — the entire world generated 256 terawatt-hours from solar. Last year it made 2,778 TW-Hr. In a single decade, our solar energy output had grown over ten times as much. This incredible rally shows no sign of slowing either. In 2025, it grew at 30% — in fact the fastest growth rate in eight years despite starting from a much larger base. The world’s solar output has functionally doubled every three years.

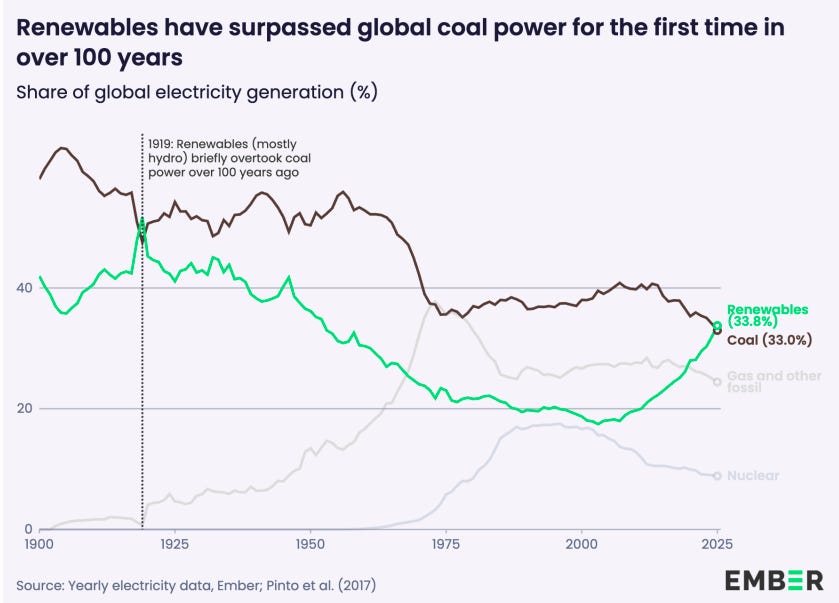

This is also why, for the first time in over 100 years, renewables as a whole generated more electricity than coal did. The last time renewables were ahead was 1919 — when global electricity demand was 300 times smaller than today, and “renewables” basically just meant large hydropower dams. Coal has held the top spot through all of modern industrial history. In 2025, renewables collectively crossed it.

But it’s mostly a China story

If you strip China out of the data, however, the rest of the world’s fossil generation had already been flat since 2018. Europe was retiring coal plants, the US was switching from coal to gas, other economies were mixed. But outside China, there was basically no net growth in fossil generation for seven years running.

China was the one country keeping the global number moving upward. Between 2018 and 2024, China alone added 1,145 terawatt-hours of fossil generation — four times more than India added over the same period. Every year, China’s growth swamped what everyone else was cutting.

Then in 2025, China flipped.

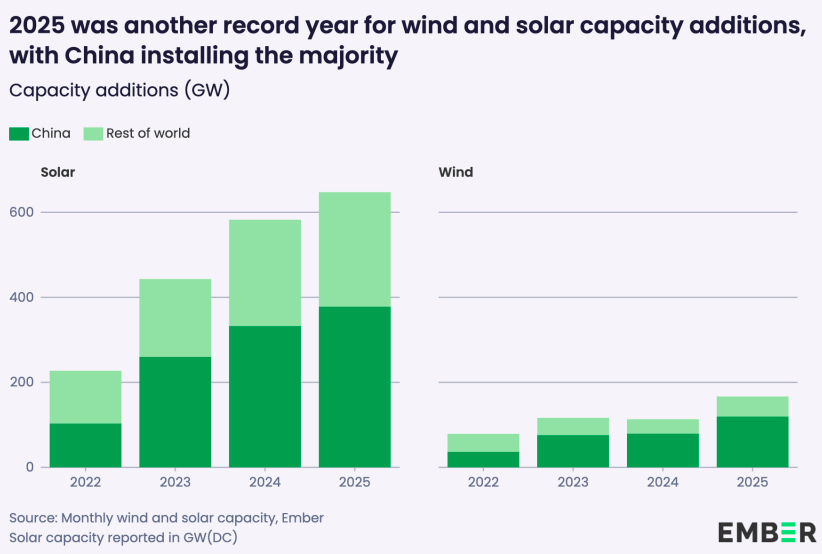

Its fossil generation fell for the first time since 2015. This isn’t because its economy slowed — its energy consumption grew, but its clean energy grew even faster. Solar alone, in China, grew 40% in a single year.

To give you a sense of the scale: China installed 378 gigawatts of new solar capacity in 2025. The United States has built up 274 gigawatts of solar capacity across its entire history. China added more in one year than the US has built in its history.

A more accurate version of the “fossil generation fell globally” story, then, is: China had a historic year for clean energy, and that was enough to tip the global number.

What this means for India

India had its own set of milestones in 2025 that are worth knowing about.

Coal’s share of India’s electricity generation fell from 75% to 71% in a single year. Solar overtook hydropower to become the largest source of clean electricity in the country for the first time ever. It’s now at 9.4% of India’s electricity mix, up from just 5.3% three years ago. India also installed more solar capacity than the United States in 2025, for the first time.

But India’s electricity demand grew just 2.4% last year. That’s the third-lowest growth rate in twenty years. Not because the economy slowed, but because 2025 was an unusually cool year. Summers were much milder than 2024, which had seen brutal heat. Ember estimates that alone reduced electricity demand by about 32 terawatt-hours compared to a normal year.

So what produced the fall in coal was renewables having a record year and demand having an unusually quiet year. Both together. The report itself says the demand slowdown was “likely an outlier.” In each of the four years before 2025, India’s electricity demand grew by more than 100 terawatt-hours. Last year it grew by 49.

Now India does have a big renewable pipeline — 101 gigawatts of solar already under construction, 24 gigawatts of wind, another 23 gigawatts of hybrid projects. Enough on paper to cover two years of expected demand growth. But as we’ve covered before and in the earlier story today, building generation capacity is only half the problem. Actually using it is the other half.

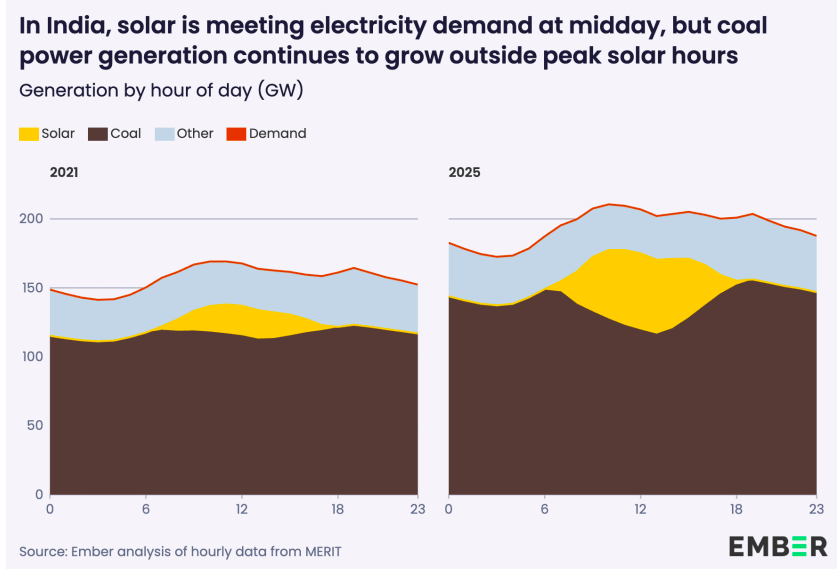

Here’s a concrete example from the Ember report. At noon on the average day in India in 2025, solar was generating over 50 gigawatts — covering about a quarter of national demand during those hours. But then the sun goes down.

From 6pm to 6am, coal still met over three-quarters of India’s demand growth. The evening peak has almost nothing to fill it except coal. We actually covered this in some detail earlier — there were power shortfalls on 13 out of 15 nights in late April, even while midday solar was going to waste.

The reason both happen at the same time comes down to how coal plants work. They have a minimum output level below which they can’t reduce generation without shutting down entirely — and shutting down and restarting is expensive and slow. So even when solar is flooding the grid at noon, coal plants keep running at their minimum because they need to be ready for evening demand. The result is that solar gets curtailed at midday, and coal runs at night regardless. Both wasted, in different ways.

The report notes something that tells you where things actually stand: coal plants in India started inviting bids to install batteries on themselves in 2025. The coal fleet is trying to become more flexible to accommodate solar because there isn’t enough storage yet to replace it at night.

The number that should get more attention

Here’s something that looked very interesting to us. Global power sector emissions in 2025 fell by 0.04%.

Despite solar’s record year, despite renewables crossing coal for the first time in a century, despite China’s fossil generation falling — the actual emissions number barely moved.

Why? Because fossil fuels still generate 57% of the world’s electricity. The system is so large that even a genuinely historic year for clean energy barely shifts the needle. The direction changed — fossil generation stopped growing, which is meaningful — but actual emissions declining significantly is a different story.

We covered the IEA’s World Energy Outlook last year, and the uncomfortable finding there was that even under optimistic scenarios where all stated climate policies come through, we’re heading for 2.5°C of warming. The Ember report’s 2025 data doesn’t change that. What it shows is that things are moving in the right direction. But moving fast enough is a separate question, and the emissions number suggests we’re not there yet.

One more thing

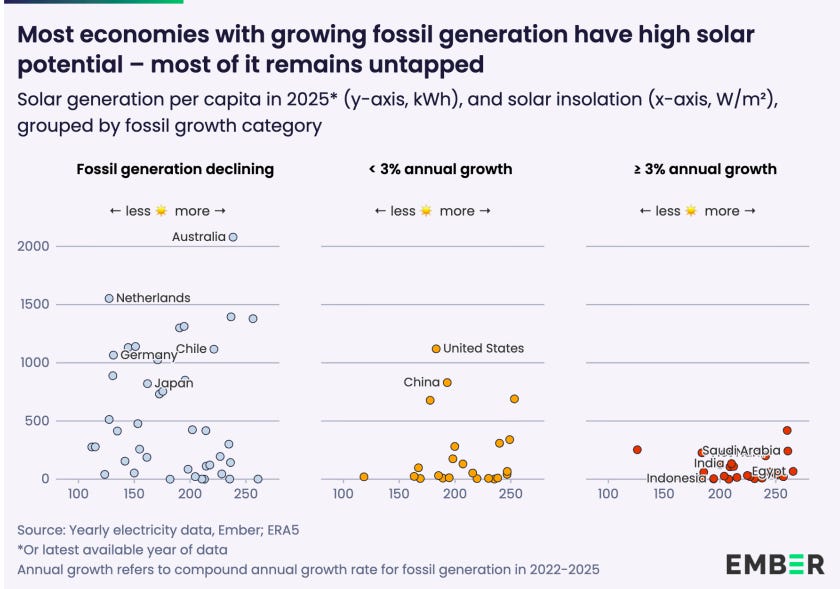

The report makes an observation we found genuinely interesting.

Look at which countries still have growing fossil generation, and you’d expect them to be the ones with no other choice. But that’s the opposite of what the data shows. Almost all of them sit in regions with world-class solar resources. Egypt gets more than twice the sunlight of the Netherlands — and yet the Netherlands generates 1,553 kilowatt-hours of solar electricity per person every year, while Egypt generates 67. Saudi Arabia, Indonesia, Algeria, much of Africa — same story everywhere. The places best suited to solar are the ones leaning hardest on fossil fuels.

And cost is no longer the reason. In 2024, 90% of newly installed renewable projects globally were already cheaper than the cheapest fossil fuel alternative.

So what’s left? Grids that weren’t built for variable solar generation, financing that isn’t reaching the right markets, regulations still written for a coal-and-gas world. These are harder to solve than making solar cheap, and they don’t have a technology fix.

The headline from 2025 is real. For the first time, clean energy grew fast enough to meet all of the world’s new electricity demand without any help from fossil fuels. Ten years ago, fossil fuels were filling 70% of all new demand. That shift is genuine and it matters.

But fossil fuels still generate more than half the world’s electricity. And as the emissions number shows, crossing a milestone is not the same as solving the problem. The direction changed in 2025. Whether the pace changes is the question the next few years will answer.

Tidbits

[1] NVIDIA’s AI PC push could benefit India’s semiconductor ecosystem

NVIDIA has unveiled its new AI-focused RTX Spark superchip, designed for personal AI agents, creative workloads and gaming. Industry experts believe this shift toward AI-first PCs could create new opportunities for India across chip design, semiconductor manufacturing and the broader AI value chain.

Source: The Hindu BusinessLine

[2] Oil India finds another natural gas discovery in Andaman

Oil India has made another natural gas discovery in the Andaman region, strengthening hopes of unlocking India’s offshore energy potential. The find comes as India looks to reduce import dependence and improve long-term energy security through domestic exploration.

Source: Financial Express

[3] India’s economy grows 7.7% in FY26, beats expectations

India’s economy expanded 7.7% in FY26, surpassing estimates and improving from 7.1% growth in FY25. Strong performance in manufacturing and services drove the expansion, although Q4 growth eased slightly to 7.8% from 8% in the previous quarter.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Krishna and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Ajay Srivastava on India’s place in the fracturing global trade order

The rules-based world trade order as we know it is fracturing, with weaponized tariffs and every country scrambling to secure its place in the new paradigm. We recently spoke to Ajay Srivastava, founder of the Global Trade Research Initiative and a former Indian Trade Service official, to make sense of how India is navigating this high-stakes shift. Our conversation dives deep into what Trump’s tariffs actually mean for global trade, why Bangladesh massively outperforms India in garment exports despite fewer resources, why India’s software giants haven’t made a serious bet on AI, and the broken links in India’s textile supply chain. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

You say -

"Worse still, none of this is even free, really, as these costs are often baked into the upfront installation price. And because the vendor has already collected the maintenance money upfront, they have no financial reason to ever proactively show up and service the system"

BUT do you know how much competition is there on pricing of installation alone?

Solar square charges Rs 2,60,000/- for 3 kWp system where as markets have fallen to almost Rs 1,75,000/- and then people expect small vendors to turn up for cleaning when all they are making is a small profit on installing the system. So please don't patronize what solar square is doing rather look at the market condition. Indians are so sensitive to pricing that for 5000 bucks they will change the vendor.

The solution

Is to teach the customer to clean the panels at least once every month as residential environment mostly are pollution free and as for bird droppings solution is to install spikes on the top most part of installation.

Or if customer is ready to pay for cleaning of system small vendors are ready to provide the monthly cleaning but don't expect charity from solar vendors.

Hii am a beginner here, I have one question does anybody know how can Indians apply for the SpaceX IPO?