A green transition needs more than clean energy

Fixing our grid is the harder task

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

We built solar. Now, we must do something harder

The million dollar gas leak under India's coal mines

We built solar. Now, we must do something harder

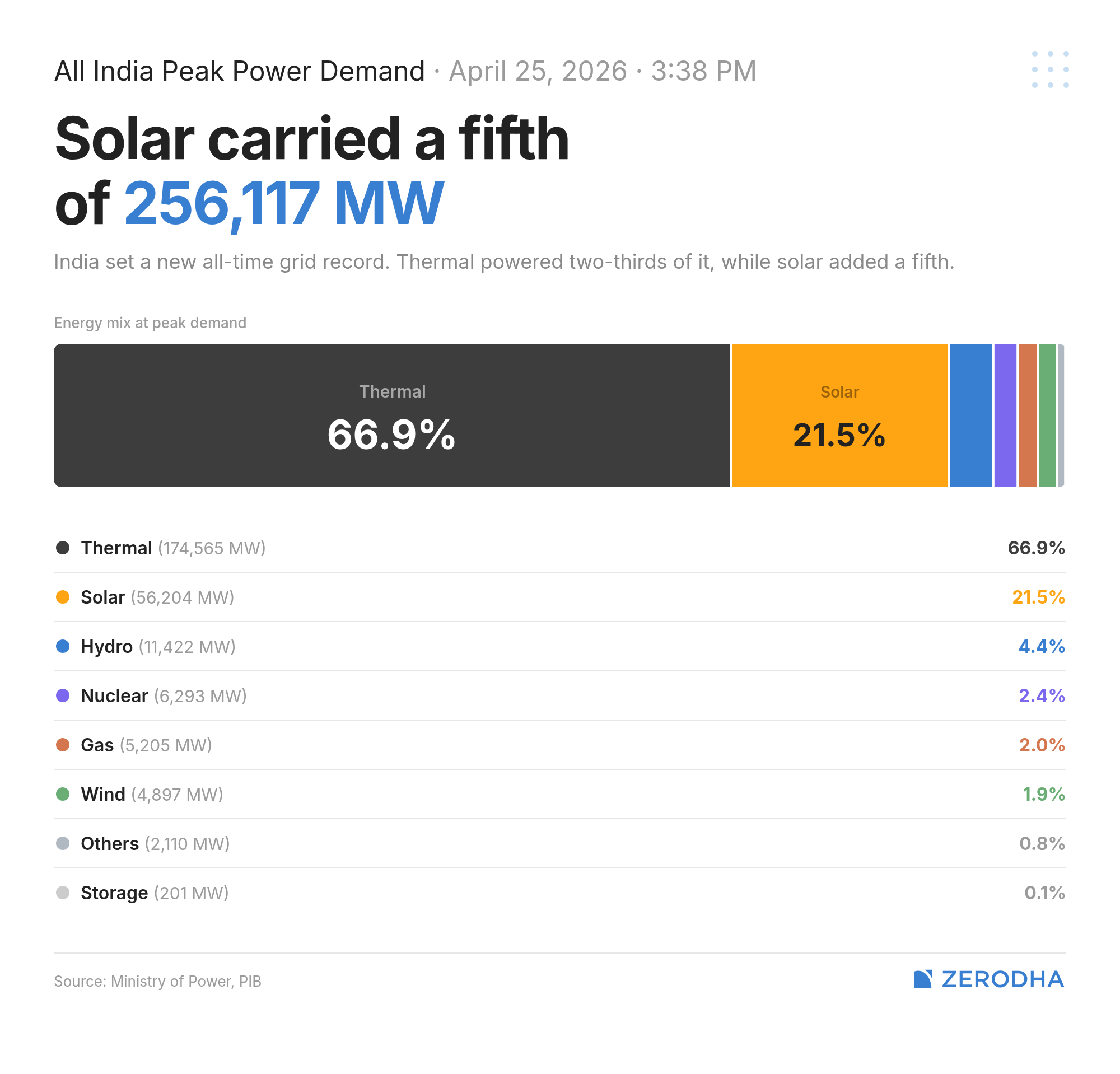

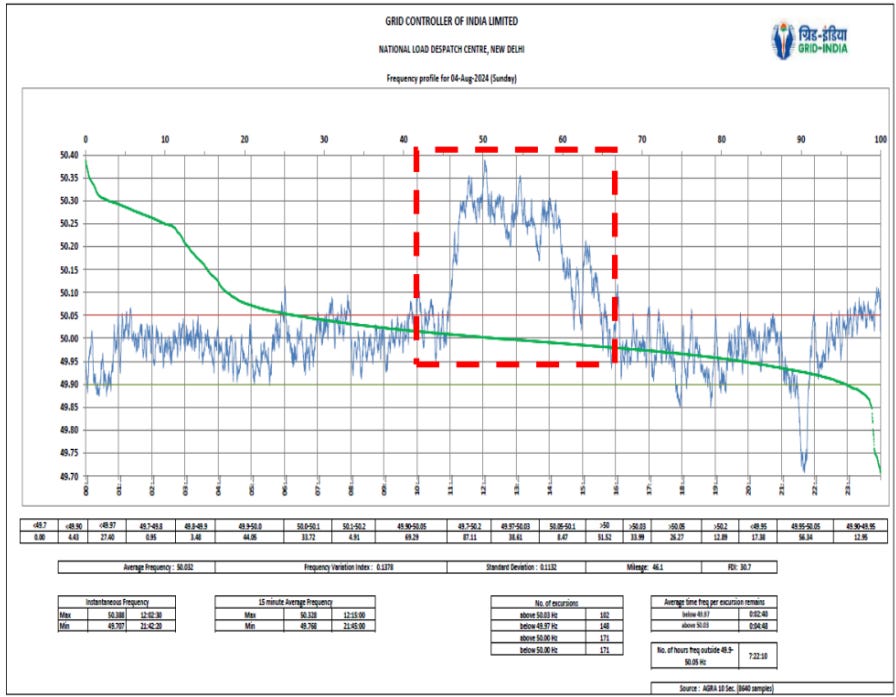

At 3:38 PM on April 25, India demanded more power than it ever had in history. The grid handled 256 GW in a single instant. Impressively, we had enough power to meet all that demand, about a fifth of which came from solar plants. The system had worked.

But the very same evening, once peak demand had already subsided, the system failed. Seven hours after setting its record, India’s power system came 4.2 GW short. The same thing happened the night before as well when, at 10:34 PM, the grid fell 5.4 GW short — we couldn’t find the power to feed the equivalent of 27 lakh rural homes.

In the second half of April, there were power shortages on 13 out of 15 nights. Curiously, those shortages didn’t happen when demand was at its highest — that was earlier in the day. The shortages came later, at night.

You could see this play out in electricity markets as well. Earlier in April, real-time prices on the Indian Energy Exchange collapsed to near-zero on some afternoons. There were times when you could buy a unit of electricity for just one to three paise. On multiple evenings in the same month, meanwhile, prices regularly hit the government’s ₹20-per-unit ceiling.

Our electricity markets are entering weird territory. We’re seeing shortages night after night. But when daylight rolls around, we can no longer handle the amount of electricity that floods in.

From generation to absorption

This points to one fact: our green transition is entering a new phase.

Until recently, the big question was whether India could build solar and wind energy fast enough to meet our targets. We succeeded, and how! By midway last year, less than half of our installed power generation capacity was from fossil fuels. In the last financial year alone, we added a record 55 GW of non-fossil capacity.

Sadly, there’s no time to rest. The work ahead is harder still: we need to learn how to absorb all that new energy into our grid.

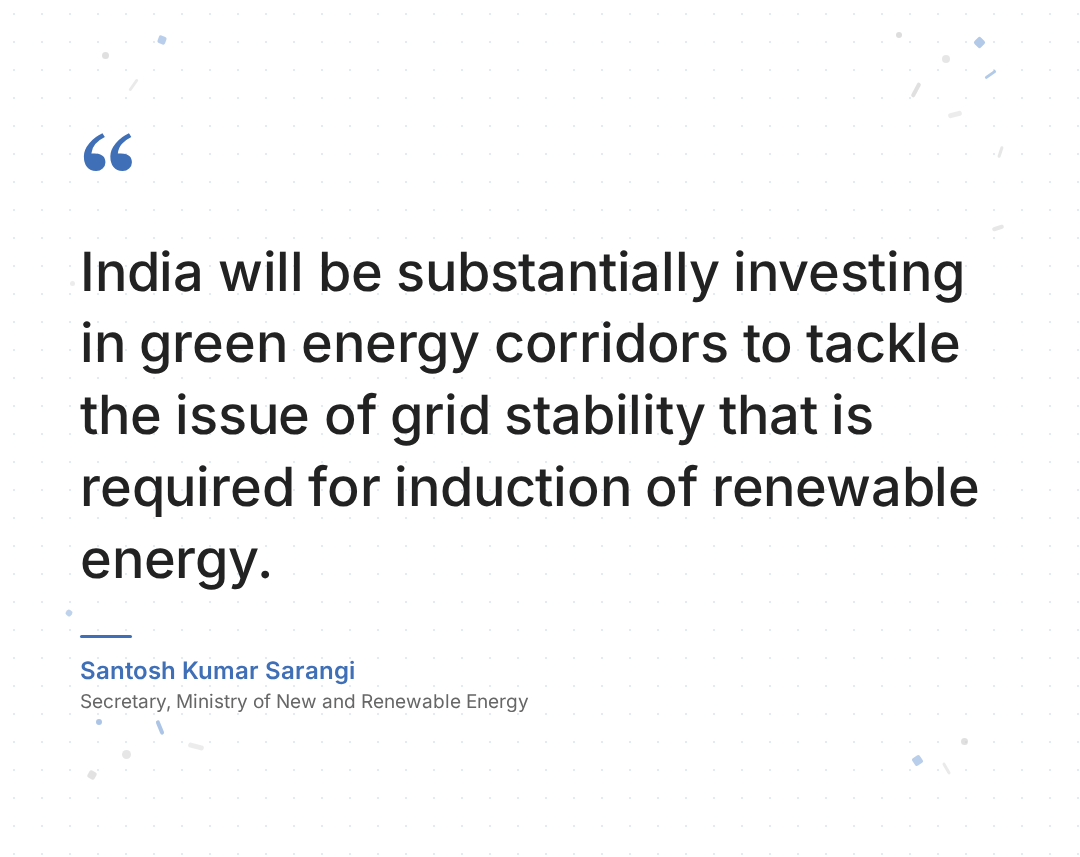

The government has flagged this as its next big priority. As Santosh Sarangi, the Secretary to the Ministry of New and Renewable Energy, recently said, India needs “China-like super-grid planning” to handle the biblical surge of energy ahead: after all, NITI Aayog projects that roughly ~1,800 GW of solar and wind energy will come online by 2050. He then rattled off a long list of missing pieces that India will have to put together: batteries, grid-forming inverters, synchronous condensers, and more.

This new phase is already underway. India recently flagged off its first synchronous condenser — a machine that protects the grid from volatile renewable supply. The Central Electricity Authority (CEA) opened its first public consultation on grid-forming inverter standards this January. Midway through last year, the government signed off on 7.5 GW of battery and pumped storage, although the CEA’s planning document says we’ll need ten times that by 2032.

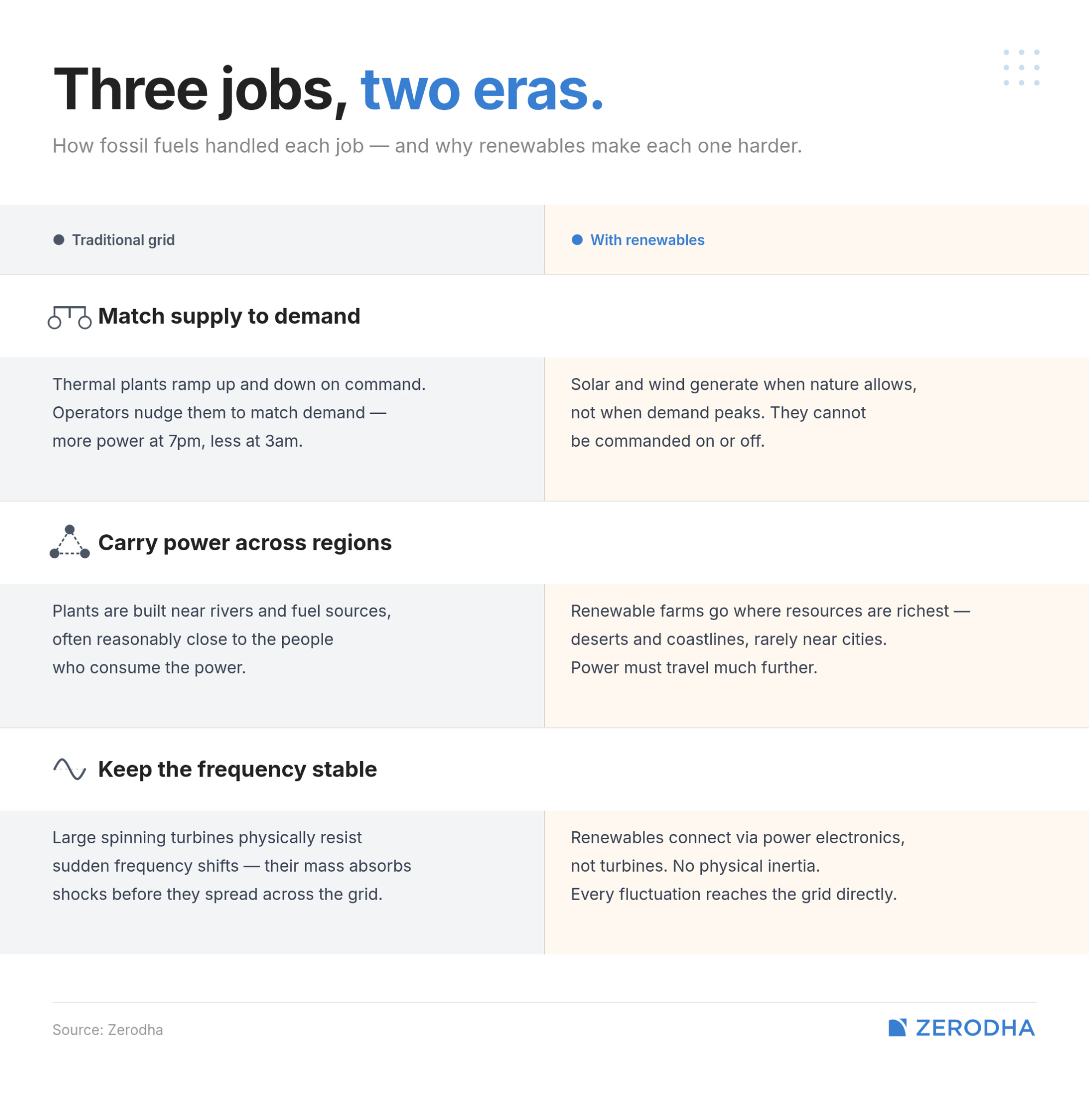

The three jobs of a grid

How does electricity reach your home from a power plant?

There are, of course, many hundreds of kilometers of wires which carry that electricity. But it isn’t only wires. There’s an entire live machine — the “grid” — which has to balance the electricity entering and exiting the system for every second of every day.

This grid has three jobs. One, it has to match supply to demand, by nudging power plants up and down. Two, it has to carry power across regions. Three, it has to ensure that the electricity reaching the system doesn’t flicker second-by-second.

India’s grid was designed around a paradigm of coal, hydro, and nuclear plants. These shared a few characteristics: one, they could ramp their output up and down as desired; and two, they used big, fast-spinning turbines with their own momentum, which physically resisted any sudden changes.

As renewables come online, all three of a grid’s jobs become more difficult. They create electricity when the sun shines or the wind blows, without regard for the schedules of people. Power plants are set up where it’s easy to generate power, which need not be anywhere near a population centre. And they connect to the grid through simple electronics, not turbines, which faithfully transmit every little fluctuation to the grid.

A grid built for our era of renewables will have to solve all three problems.

Moving power through space

India’s solar and wind power comes from a handful of states. Rajasthan, Gujarat, Karnataka, and Andhra together account for the bulk of our solar generation. Coastal Gujarat and Tamil Nadu account for most of our wind. The biggest load, meanwhile, is elsewhere: on our coasts, in the industries towards the south, in the population centres of the north.

The grid, therefore, must move large blocks of power from a handful of generating zones to a much larger number of demand zones.

India has been preparing for this alongside its renewables build-out. Back in 2022, the Ministry of Power had already planned for 51,000 circuit kilometres of new inter-state transmission. This included high-voltage direct current corridors running for over 8,000 circuit kilometres, at a cost of roughly ₹2.44 lakh crore. We’re ramping up our ability to carry surplus electricity between entire regions, with our “inter-regional transfer capacity” set to rise from 120 GW today to 168 GW by 2032.

Sadly, this isn’t enough. The desert state of Rajasthan, for instance, simply can’t push a lot of its solar power out. The Central Transmission Utility recently cited major challenges in connecting as much as 60 GW of renewable energy from Rajasthan to the grid. And connection doesn’t guarantee off-take either. Every day, between 11 AM to 2 PM — when the sun shines the brightest — roughly 4 GW of commissioned renewable energy is switched off because the grid can’t handle it.

We need to build our grid faster.

Globally, China leads the way in building its grid. The State Grid Corporation of China — the world’s largest utility — announced this January that it would spend RMB 4 trillion, or roughly $574 billion, on its grid over the next five years. That’s about $115 billion a year; a number higher than the $108 billion that we planned to spend in total in the decade between 2022 and 2032. This would include 45 ultra-high-voltage lines, spanning more than 50,000 km.

And yet, even China can’t build fast enough. In the first half of 2025, it curtained 5.7% of its solar energy, up from 3.2% just a year ago. In Tibet, where renewable generation is concentrated, more than a quarter of all electricity was shut out.

That’s when China doesn’t have the political economy issues India does. Indian projects are seeing serious issues with land acquisition and clearances, with delays pulling down 25 different inter-state transmission projects.

We’ll eventually have to match China’s scale of planning, while also working through people-centric concerns that are alien to China.

Shift power across time

The daily mismatch we saw this April — power gluts in the day, shortages at night — is simply a feature of using solar energy. The supply of solar energy usually peaks at midday. Demand usually peaks later in the day. The two are necessarily out-of-phase with one another. Ideally, the grid should take the midday solar abundance, and use it to meet evening scarcity.

For that to be possible, we need a way to store that electricity.

We’re getting there, albeit slowly. At the moment, India has little over 7 GW of pumped storage projects in operation, and just over 1 GW of grid-scale battery storage. The government hopes to get roughly ten times as much storage by 2032, in order to serve roughly 411 GWh of energy demand. That isn’t easy, though. Pumped storage projects, for instance, take five to seven years to build. 2032 is too close for us to increase our storage capacity by an entire order of magnitude.

To be fair, storage is becoming easier to build with each passing year. The costs, for one, are falling steadily. In 2025, it took ₹1.48 lakh per MW per month to rent a standard battery. Just one year ago, the same thing would take ₹2.26 lakh — that is, prices fell 35% in a single year. But even so, it isn’t clear that we’ll get enough storage up and running in time.

What options do we have? If you can’t change when electricity is generated, one possibility is to change the time at which people use electricity.

You can nudge people to do so by charging them different rates for electricity, depending on how much supply there is at that time. We’re exploring this option too. India introduced time-of-day electricity tariffs in 2023, mandatory for commercial and industrial consumers above 10 kW from April 2024 and most non-agricultural consumers from April 2025. But sadly, enforcement currently remains patchy.

Keeping the system stable

One of the least visible sides to our green transition is the sheer volatility renewables add. These simply lack the inertia older sources of energy — with their giant turbines — came with. Every flicker in the electricity they generate is passed faithfully to the grid.

This was a small problem when our renewables penetration was low. But around 40% of the energy connected to our grid, now, comes from these simple, inertia-free systems. Across India, there were 68 different times between January 2022 and July 2025 in which more than 1 GW of renewable energy was suddenly lost because too much entered the grid at once. As the Central Electricity Regulatory Commission (CERC) recently found, renewable plants routinely over-inject more power than their scheduled output into the grid.

Too much electricity can be a bad thing. It sends voltage and frequency surging well above safe limits. That overloads the grid, which can strain the system, and trigger disconnections and outages all through.

To deal with surges like this, the grid needs to add inertia: through systems like synchronous condensers or grid forming inverters.

India’s currently setting up the policy framework to make this possible. In 2022, the CERC notified rules around backup grid services, which could help the grid restore balance when things flickered. The CEA is now working on standards for the next step: pushing large battery storage projects to support grid stability as well.

Even as these fall into place, however, the bigger challenge is to bring the hardware in place. We only just commissioned our very first synchronous condenser. It’ll be years before we can get enough online to stabilise the whole grid.

A hard reality

Upgrading our grid is a monumental project. We probably wouldn’t have anywhere near all the hardware we need by 2030, even by the most ambitious commissioning timelines. Until then, we’ll have to live with system-wide strain and weird supply-demand mismatches.

There are some stop-gap answers we can attempt. We could, for instance, invest in making our coal plants more flexible — for instance, making them run at low capacity in the middle of the day. One proposal, for instance, is to run thermal plants at a minimum floor of 40% of capacity, rather than 55% — which will create 34 GW of extra headroom to absorb surging solar energy.

Such solutions come with trade-offs, however. For instance, running thermal power plants below their capacity can damage them. In fact, NTPC recorded 692 boiler-tube leakages between 2022 and 2025, partly because of adjustments like this.

More importantly, this will only buy us time. We don’t have the luxury of simply hoping things will work out. Eventually, we’ll have to transform our grid — ensuring that we can get clean electricity to arrive where it’s needed, when it’s needed, at a frequency the grid can manage. Without that, our impressive build out will be for nothing.

There’s a steep hill to climb ahead. The good news, however, is that the government is signalling its willingness to do just that.

The million dollar gas leak under India’s coal mines

India can’t quit coal. Not yet, anyway.

The country just crossed over 1 billion tonnes of coal production in the fiscal year 2024-25. And the plan isn’t to slow down. The Ministry of Coal wants to scale that to 1.5 billion tonnes by 2030. Coal still powers over 70% of India’s electricity generation and accounts for more than half of our primary energy needs. Even as renewables are expected to take a bigger share of India’s energy mix compared to coal, absolute coal consumption keeps rising.

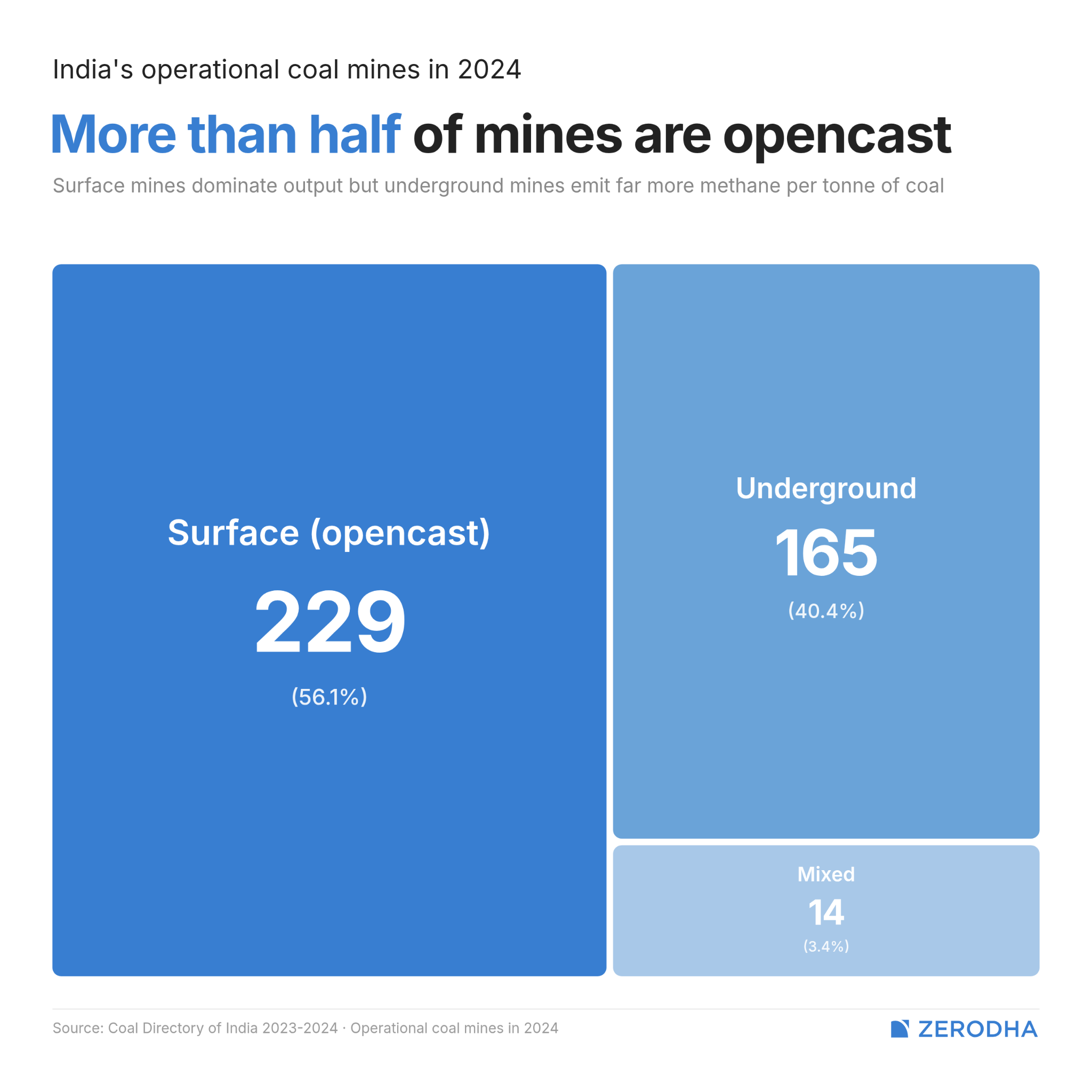

The most consequential part of this expansion is happening underground. India plans to nearly triple underground coal mining output, targeting over 100 million tonnes per year by FY29. Underground mines, while accounting for about 40% of India’s coal mines, produce just 3.5% of total output. They’re small, expensive to operate, and require specialised equipment. But they also sit on top of some of the country’s richest coal beds (or seams), including the coking coal India badly needs for steelmaking.

But there’s a problem with these ambitions.

You see, coal seams inherently contain a lot of methane, a greenhouse gas that contributes significantly to global warming. Mining cracks open those seams, naturally letting out the gas. Over a 20-year horizon, its warming impact is over 80 times that of carbon dioxide. It’s estimated to be responsible for roughly 30% of the rise in the global temperature since the Industrial Revolution.

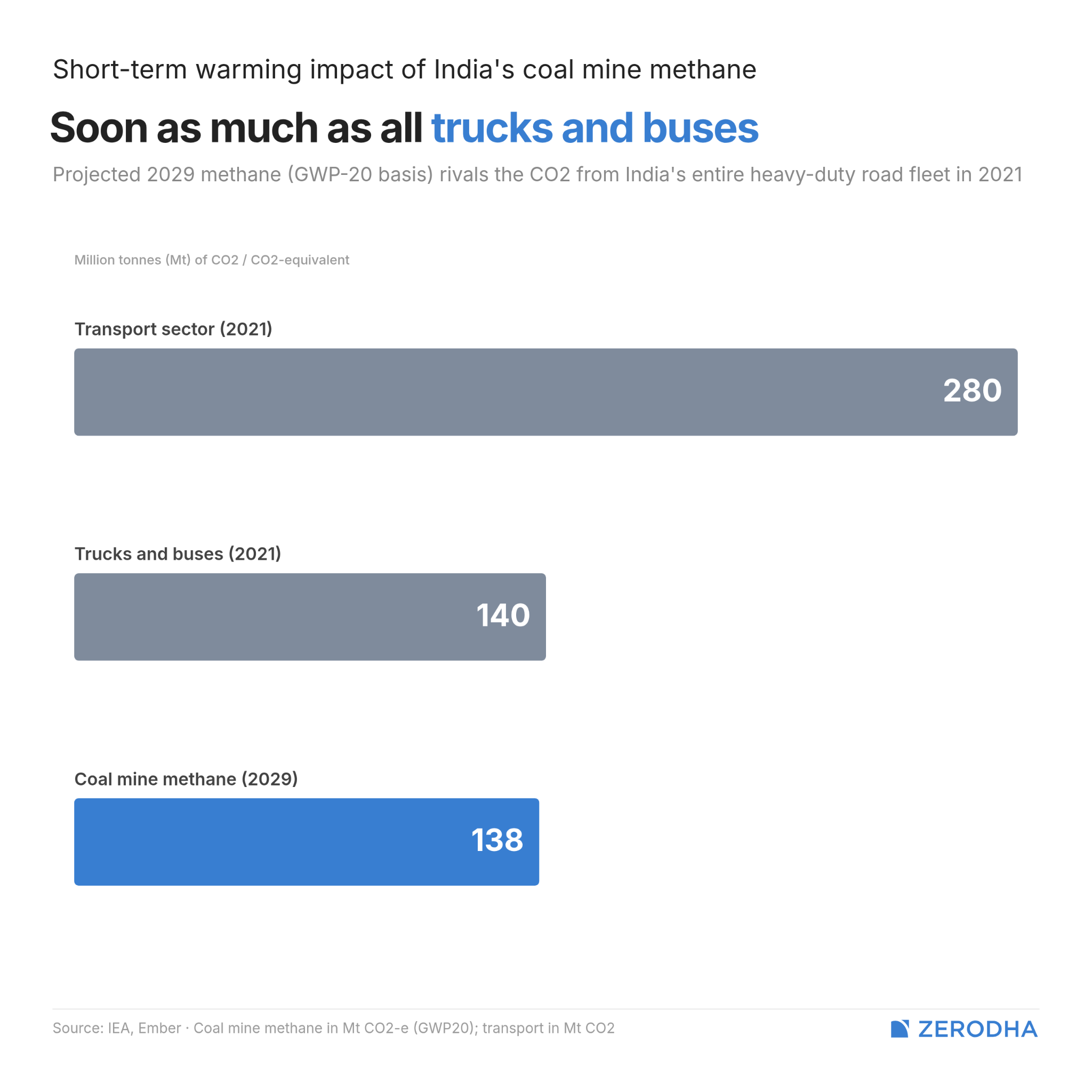

By 2029, Ember estimates that the short-term warming impact of India’s coal mine methane could reach about 138 million tonnes of CO2-equivalent. To put that in perspective, that’s roughly equal to the CO2 emissions from every truck and bus on Indian roads in 2021. And underground mining in particular is a bigger culprit of this than surface mines — despite its low contribution to output, it makes up 15% of methane emissions.

All of this runs in conflict with India’s goal to achieve net zero emissions by 2070. In fact, we have no dedicated policy framework to deal with coal mine methane (or CMM).

But this isn’t merely a story about emissions, or even the technology required to dispose of CMM — which is actually quite proven. The solution to this problem requires going into how coal production is governed by the Indian state as much as anything else.

That’s what a new report by Ember, the energy think tank whose work we often cover, dives into.

Low-hanging fruit

Let’s start with the scale.

Not all fossil fuel emissions come from combustion. A significant share comes from gases that simply escape into the atmosphere during mining, drilling, or transport. These are known as fugitive emissions.

Coal mines account for 68% of India’s fugitive methane emissions from the fossil fuel sector. In 2019, the country reported 810 kilotonnes of CMM. Without any intervention, Ember projects that number could more than double by the end of the decade to over 1,600 kilo-tonnes (or 1.6 million tonnes) annually as coal production — especially underground — ramps up.

What makes the continued existence of this issue so frustrating is that the technology to capture and use this methane productively already exists in the world. And it’s been proven — in India itself.

Between 1996 and 2010, India undertook a pilot project at the Moonidih underground mine in India’s largest coalfield in Jharia, Jharkhand. Three vertical wells were drilled to recover methane trapped in the coal seam. The gas was captured and fed into generators, producing over 10 lakh kilowatt-hours of electricity for the local mine colony. Captured methane can also be injected into local gas grids or used to displace imported natural gas.

The project proved that methane extraction and utilisation from Indian underground mines was technically feasible. Several other such studies followed at other mines, confirming that the approach could work more broadly.

But none of them led to a commercial project. In over a decade since the pilot’s success, zero commercial-scale coal mine methane mitigation projects have been implemented in India.

Who’s in charge?

So if the technology works, why hasn’t anything happened?

United we stand, divided we fall?

The answer mostly lies in the governance structure of coal in India. In essence, CMM in India falls into an institutional no-man’s-land where multiple agencies touch the issue but nobody owns it.

At the top, you have the Ministry of Coal, which sets overall coal policy and production targets, and directly controls three agencies. One is Coal India. Second is the Central Mine Planning & Design Institute (CMPDI), which provides technical oversight and acts as the nodal agency for commercial methane feasibility. Third is the Coal Controller’s Organisation (CCO), which monitors production and coordinates mine closure approvals.

This entire apparatus then liaisons with four other agencies separately:

The Directorate General of Mines Safety (DGMS), which handles mine safety. It classifies underground mines into three degrees based on gassiness, and mandates ventilation and drainage protocols for the more dangerous ones to prevent them from exploding

The Ministry of Environment, Forest and Climate Change (MoEFCC), whose job it is to estimate the methane emissions from projects and decide environmental clearances accordingly

The Director General of Hydrocarbons (DGH) oversees coalbed methane, which is legally treated as an unconventional hydrocarbon — it’s distinct from coal mine methane, even though the gas comes from the same seams

NITI Aayog, for general policy planning

That’s multiple agencies across ministries, each touching a piece of the methane problem, with no single body responsible for coordinating policy or setting standards. As a result, methane regulation in India is entirely safety-driven. There is no standalone methane emission cap anywhere in the system.

Downstream problems

Many of the issues plaguing CMM (and broadly coal management) are downstream of this structure of India’s coal monitoring.

Take, for instance, how we measure CMM data. India’s emissions reporting is built on emission factors derived from field measurements at 16 surface and 83 underground mines. Those factors are then weighted into national averages.

But the actual underlying mine-level data isn’t publicly available. It’s scattered across agencies with no integrated monitoring platform, no standardised reporting framework, and no mechanism for independent verification. You can’t design an abatement policy if you don’t know, mine by mine, how much methane you’re actually dealing with.

The abandoned mine problem is the sharpest illustration of this vacuum. India doesn’t include abandoned mine methane (AMM) in its reporting at all. Their reasoning was that there are very few abandoned mines which also had low production when they were active.

But there are no publicly available ground-level measurements to support that claim. The mine closure guidelines do require a two-year post-closure monitoring period for air quality — but methane isn’t explicitly named, falling ambiguously under the general “air quality“ umbrella. The Ministry of Coal has identified 147 coal mines for closure by 2028, but as more mines shut down this decade, an entire category of emissions remains unmeasured and unreported.

But it’s not like India hasn’t tried to solve this. For instance, in partnership with the US Environment Protection Agency, the Ministry of Coal launches the CMM Clearinghouse to coordinate all of this: streamline approvals, facilitate information exchange, and support methane utilisation projects.

But in practice, it has no regulatory authority and no enforcement mechanism. It can convene, but doesn’t have any power to compel India’s existing governance mechanisms.

Other causes

The governance vacuum isn’t the only barrier, though.

Even where operators might want to act, the economics are discouraging without policy support. Methane capture and drainage require significant upfront capital, and the returns are uncertain when there’s no guaranteed buyer for the gas.

There are also practical challenges specific to Indian conditions. In-seam drilling, the most effective technique for pre-mine methane drainage, is technically difficult given India’s coal geology. Many of our coal seams are thin, steeply dipping, or geologically disturbed, making horizontal drilling expensive and unpredictable.

Additionally, limited gas pipeline infrastructure near coalfields means that even where methane can be captured in meaningful quantities, getting it to market is a separate problem.

What fixing it would unlock

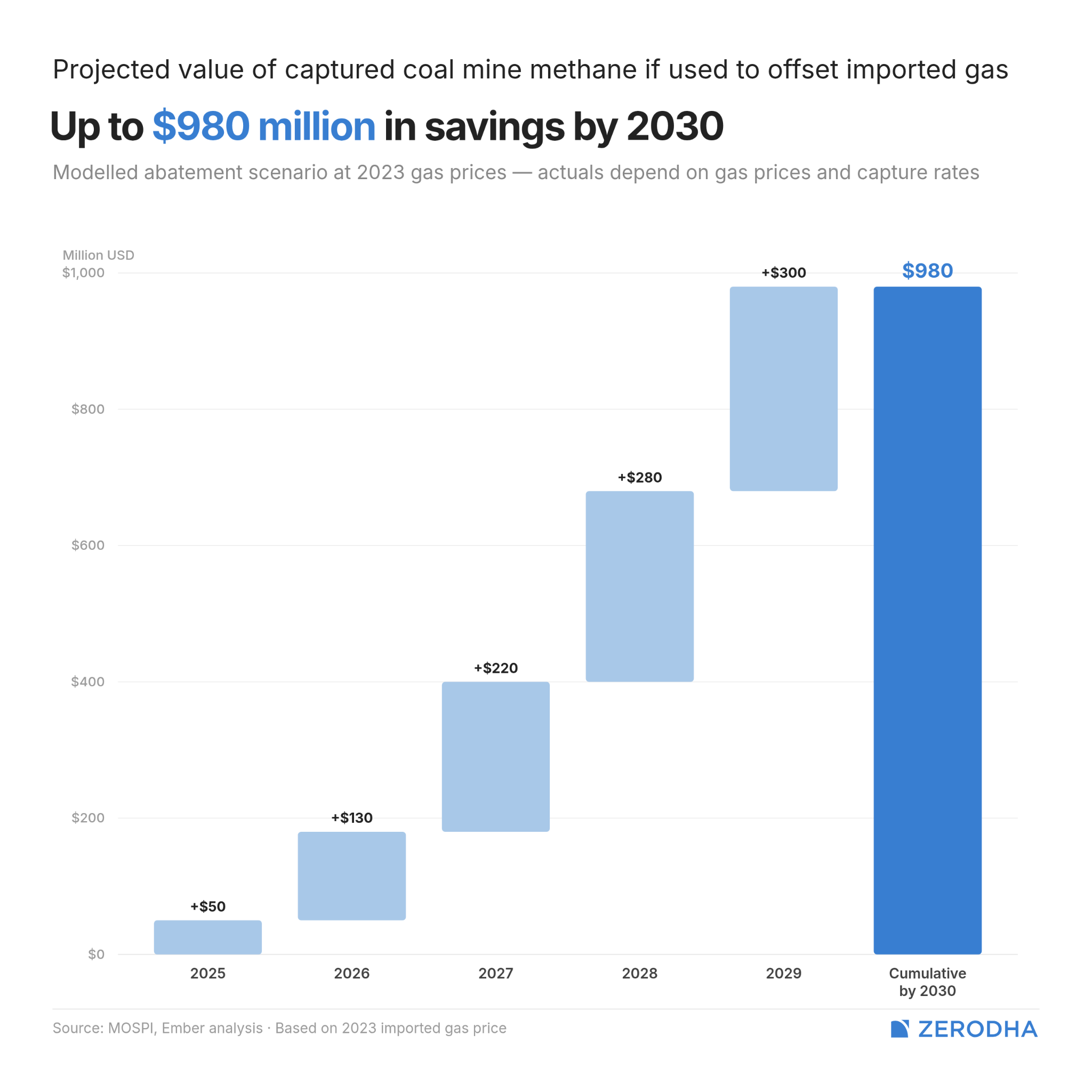

The economics of inaction are stark. India spent over $13.3 billion importing roughly 31 billion cubic metres of natural gas in FY2023-24. Coal mine methane, if captured at scale, could offset a meaningful portion of that.

Ember’s conservative scenario projects that over 1.6 million tonnes of coal mine methane could be captured cumulatively by 2030. If that gas were used for power generation to displace imported natural gas, it could, as per 2020 gas prices, save up to $980 million by the end of the decade. That’s the moderate estimate. If the higher figures from the IEA are realised and the methane is fully utilised, annual savings alone could exceed $1 billion by decade-end.

Beyond import savings, there’s the carbon market angle. If the coal sector is included in future iterations of India’s Carbon Credits Trading Scheme (CCTS), mines that reduce methane below their baselines could generate tradable credits, creating a new revenue stream that doesn’t exist today.

And this exists in other countries. Australia already does something like this through its Safeguard Mechanism, where facilities that beat a baseline of 100 kilotonne carbon dioxide emissions earn credits they can sell. The EU’s methane regulation goes further, setting progressive emission thresholds for coal mines and banning methane venting from drainage stations outright.

Then there are the co-benefits that don’t show up on a balance sheet. Methane drainage before mining improves worker safety — which is, ironically, the entire reason DGMS monitors it in the first place. Reducing methane also cuts ground-level ozone formation, which worsens respiratory health and lowers crop yields in the communities surrounding India’s coal belts.

Conclusion

India’s coal expansion isn’t slowing down — we can’t afford to do so. But every tonne of coal extracted underground releases methane that we know how to capture, know how to use, and have already proven we can handle in Indian conditions. What’s missing is a governance framework that turns proven technology into standard practice.

They say that a little effort goes a long way. In that sense, as the Ember report says, solving how we deal with CMM may be the “lowest-hanging fruit” on our way to becoming more green.

Tidbits

Adani Ports and SEZ (APSEZ) is planning a ₹13,000 crore investment to scale up its marine services business, which includes dredging, harbour tugs, and offshore support vessels. The company is also entering the European subsea cable-laying market as global demand for undersea cable infrastructure surges.

Source: The Print

India has set up a $1.5 billion Bharat Maritime Insurance Pool to provide guarantees to Indian vessels operating in the Red Sea and other high-risk waters, reducing dependence on expensive foreign insurers amid the ongoing West Asia crisis. The pool, backed by domestic insurers, aims to keep Indian shipping competitive at a time when war-risk premiums from London and international P&I clubs have spiked sharply.

Source: PSU Watch

China has moved the WTO to settle a dispute they filed against India’s domestic content requirements and industrial policy for solar cells and modules, arguing they unfairly shut out foreign suppliers. In January as well, China raised complaints to the WTO on India’s incentives for EVs and battery components.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

{kind=link}

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The main problem with a conventional AC grid into which you introduce intermittent power sources like solar (DC to AC) is very clearly explained in this lecture (link below). Solving this problem of maintaining the grid frequency inertia with solar/wind is a non-trivial matter and is extremely capital-intensive. https://watt-logic.com/2026/04/20/green-vs-baseload-the-most-suitable-energy-for-a-developing-country/

Regarding the grid problem, why is no one considering inverting the hierarchial grid architecture? The grids today are designed to distribute power from a central power station to numerous small scale consumers. It's not designed to handle distributed small scale power generators.