The Iran war and India's fertilizer problem

Why are the prices soaring?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The Iran war and India’s fertilizer problem

The Apple-India relationship grows deeper

The Iran war and India’s fertilizer problem

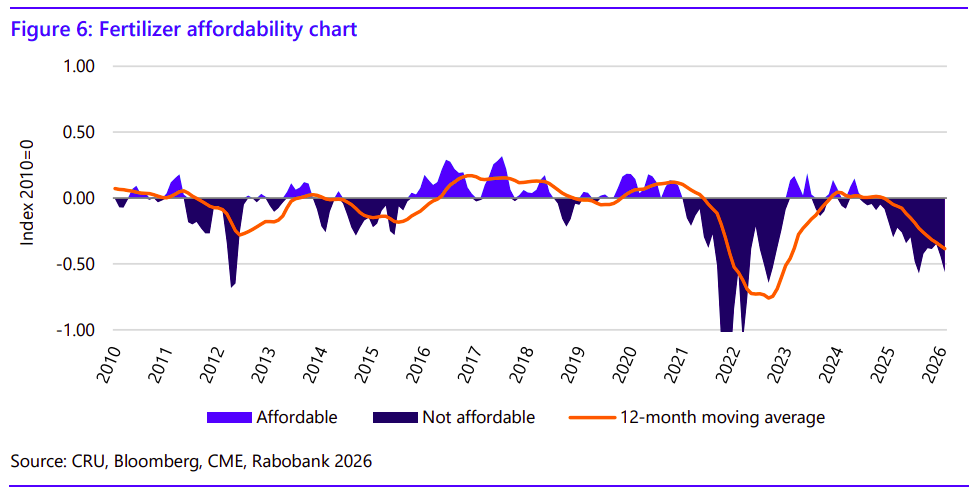

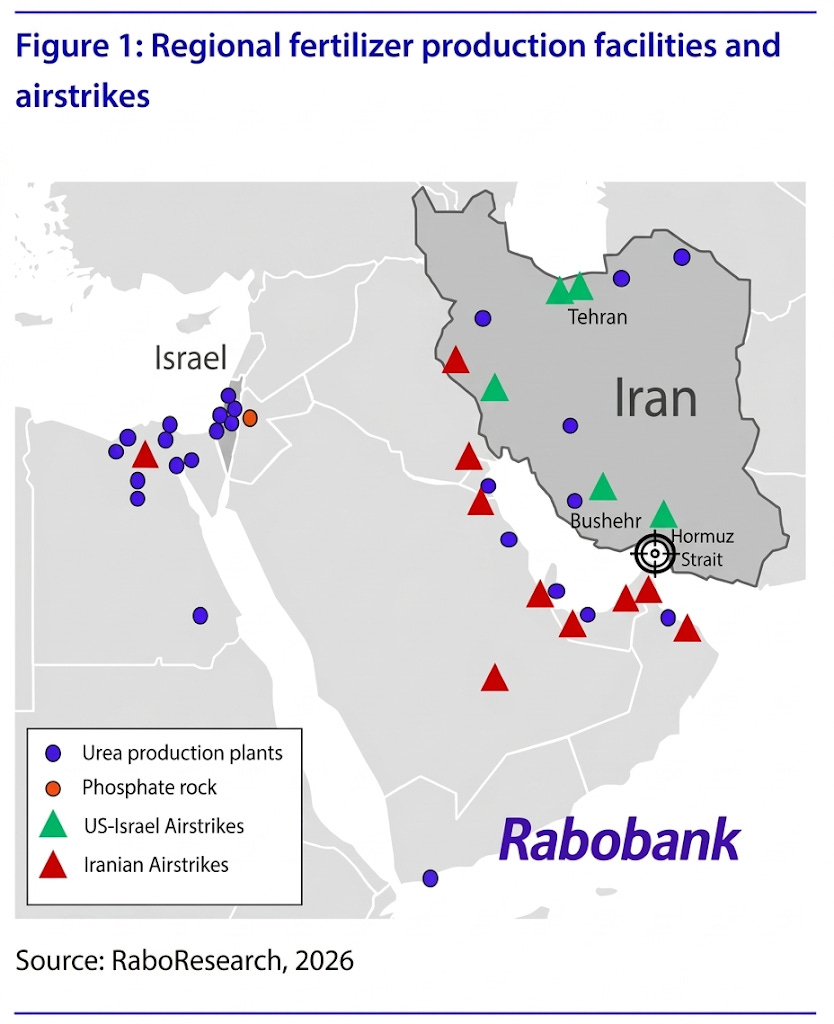

We’ve previously covered how the Iran-Hormuz conflict is disrupting oil flows, shipping lanes, and marine insurance. But, lately, the war is also hitting something closer to the ground: fertilisers. Prices have risen anywhere from 20-30% in a matter of days. The Rabobank’s urea affordability index has fallen to its second lowest level since 2010, next only to where the Russia-Ukraine war had driven it in 2022.

India is one of the world’s largest consumers of fertilizers. A big chunk of what we need — either as finished product or as the gas and chemicals that go into making fertilizers domestically — makes its way through the Persian Gulf. The Strait of Hormuz, to us, isn’t just an oil chokepoint, but a fertilizer one too.

There are many layers through which this shock travels to us. To make sense of them, though, you have to start from what fertilizers actually are.

Start from first principles

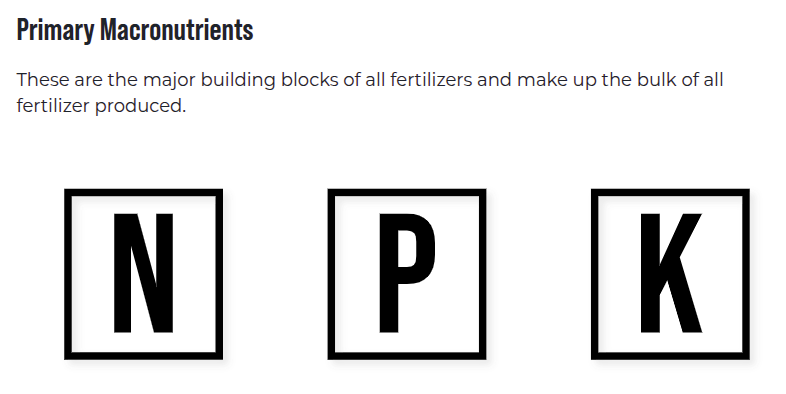

Fertilizers are, at their core, about three primary nutrients: nitrogen (N), phosphorus (P), and potassium (K). Every bag of fertilizer — urea, DAP, MOP, those 10-26-26 NPK blends — is some combination of these three.

Each nutrient has a completely different supply chain, making it vulnerable to this war in a completely different way.

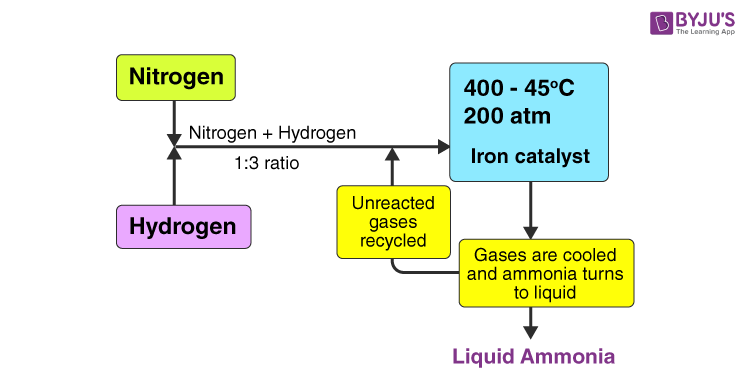

Start with nitrogen. India produces about 87% of its urea domestically. On the surface, this should sound reassuring. But urea is made from ammonia, and ammonia is made from natural gas.

Not powered, mind you. Made.

Ammonia has three hydrogen atoms for every one of nitrogen. One of the cheapest, most abundant sources of hydrogen — at least until we learnt how to break apart water molecules for cheap — has been natural gas. And so, about 70-80% of the cost of making urea is just natural gas, which serves as both feedstock and fuel.

India’s domestic gas supply covers only a portion of what its urea plants need; the rest is imported. So when LNG stops flowing through Hormuz, Indian urea plants don’t just lose a cheap energy source. They lose their primary raw material.

Phosphate fertilizers have a different problem. India imports about 60% of its DAP (phosphate fertilizer), mostly from Saudi Arabia and the Middle East. Only, many of the region’s largest commercial ports sit within the Persian Gulf, where trade has tapered to a standstill.

Meanwhile, the remainder — the DAP we produce locally — is vulnerable too. DAP, too, requires ammonia, which needs natural gas. It also needs sulfuric acid, which is made from sulfur you get by refining oil and gas. Much of the global supply of both raw materials moves through the Strait of Hormuz.

Potash is the least exposed to natural gas. But it’s also something we import entirely. India has no commercially exploitable potash reserves. While the war doesn’t directly hurt these imports, it does affect freight costs, shipping insurance, and cargo timing.

Keep these ideas in mind, because they inform everything that follows.

The pressure points

Together, this creates multiple, linked channels, each reinforcing the others, through which the war spills on to Indian farms.

The raw material for making fertilisers could stay stuck in the Gulf. The EIA estimates about 20% of global LNG trade transits through the Strait of Hormuz. Roughly 83% of that is headed to Asian markets. If those cargoes are disrupted, gas-importing countries like India face physical shortages. It’s not just gas; for instance, a full closure of the Strait could hit sulfur by 44%. And those can ripple the domestic fertilizer industry, as we’ll see later.

Meanwhile, the Gulf is also a fertiliser production hub. Countries directly exposed to the Hormuz disruption account for nearly half of global urea exports. If the conflict persists, the world’s Urea supplies could take a 30% hit. It doesn’t matter if we specifically bought fertiliser from the region. These are internationally traded commodities, which see their prices shoot up as the supply dries up anywhere.

That is, a disruption in the Strait of Hormuz, at once, raises the price of imported urea bags, while it physically constrains India’s ability to make urea at home.

And then, there’s shipping. Even if production is open, and fertiliser stocks are available at the factory, ships could stop bringing it home. The war has pushed marine insurers to pull war-risk coverage, or demand super high premiums, and many ships have decided to stop plying. As the Fertilizer Institute notes, cargo insurance cancellations immediately constrain fertiliser supplies. To what extent? About a third of the world’s fertilizers move through the 33 kilometer wide Strait of Hormuz.

The India transmission chain

In other words, many nodes in a massive relay are breaking down together.

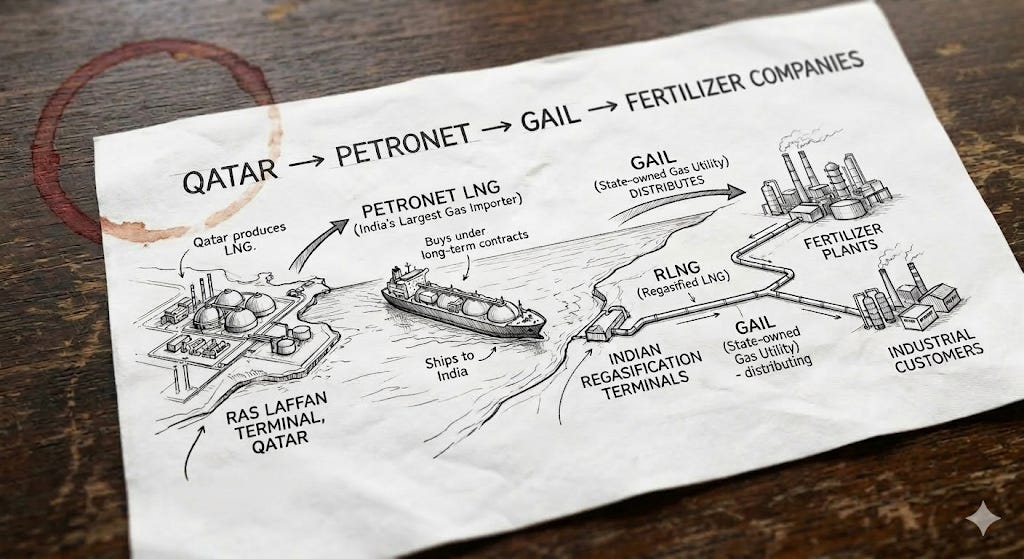

This is how things worked in better times: Qatar produced LNG at its Ras Laffan terminal. Petronet LNG, India’s largest gas importer, would buy it under long-term contracts and ship it to Indian “regasification” terminals. From there, GAIL — the state-owned gas utility — would take this regasified LNG (called RLNG) and distribute it to industrial customers, including fertilizer plants. A single chain connected all of this.

On 3 March 2026, the first link broke. Petronet told stock exchanges that its LNG vessels could no longer safely transit Hormuz to reach Ras Laffan. It invoked force majeure — a legal clause in most contracts that says, essentially, “something extraordinary has happened, entirely beyond our control, because of which it’s impossible to fulfil our promises.” Petronet served these notices on its major customers: GAIL, IOC, and BPCL.

Suddenly, GAIL couldn’t get LNG from Petronet. It still had other gas sources — domestic production, or other import contracts — but one of its biggest supply lines had simply been switched off.

That hit fertilizer plants almost immediately. GNFC — Gujarat Narmada Valley Fertilizers & Chemicals — disclosed that its allocation from GAIL was cut to 60% of its daily contracted quantity, starting 6 March. The company explicitly said this would affect production.

GNFC wasn’t alone — Reuters reported GAIL and IOC had already started reducing gas supplies to other industrial customers too.

By 9-10 March, the government stepped in to formalise what was already happening on the ground.

The Natural Gas (Supply Regulation) Order, 2026 — issued under the Essential Commodities Act, which gives the government emergency powers over essential goods — established a strict priority hierarchy for India’s remaining gas pool. It essentially answered when there isn’t enough gas for everyone, who gets served first?

The answer: households come first. Piped natural gas for cooking, CNG for transport, and LPG production get 100% of their allocation. They’re fully protected. Fertilizer comes second, but at only 70% of the sector’s average gas consumption over the previous six months. The order also bars gas from being diverted from one fertilizer unit to another, even within the same company. Every plant is capped at its own 70%.

Others are hurt too. General manufacturing gets 80%. Refineries and petrochemical plants get the least — 65%.

So, is India in a crisis?

Not yet. The government has stocked up some gas. As of 6 March 2026, our total fertiliser reserves are up 36.5% year on year. How much is that? Using July 2024 kharif sales as a rough benchmark, with some back of the hand calculations, the current stockpile gives you roughly 1.8 months of urea cover, about 3.4 months of DAP, and around 3.3 months of NPK.

But “not yet” is doing a lot of work in that sentence. The Fertiliser Association of India’s director general told PTI that immediate availability looks okay and current stock should cover the forthcoming kharif season. But it also said some shortage in imported fertilisers is expected if the war continues.

What actually happens depends almost entirely on timing.

Kharif sowing picks up with the southwest monsoon in June. DAP is typically applied at sowing for root establishment. Urea comes later, as a top dressing. Fertilisers don’t hit the field right now, in March — but it is the critical stocking and planning window. For now, companies have deliberately moved their scheduled maintenance shutdowns into March, saving gas for when plants need to run flat out closer to June. This gives us some breathing room… but only if the disruption doesn’t outlast it.

If we see a short shock, resolved by mid-April, that mostly just raises import costs. It will be painful, but manageable. But a prolonged disruption that runs into May and June is a different story entirely. That’s when we might see serious shortages.

Farmer price vs system stress

India’s fertilizer situation is tricky to read from the outside.

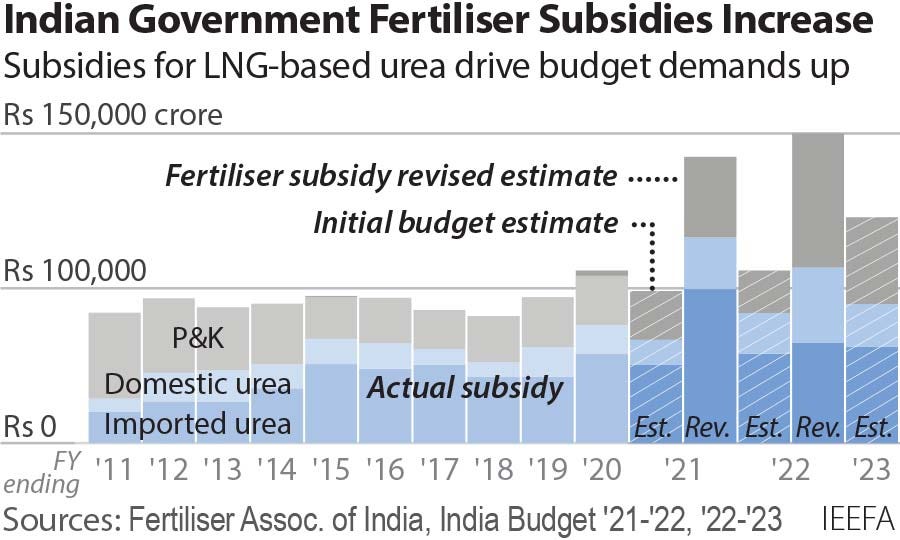

Urea is the only fertiliser with a statutorily controlled retail price. Meanwhile, potassium and phosphate fertilisers sit under the nutrient-based subsidy framework with indicative MRPs. When global prices spike, the first hit won’t be to the farmer at the retail counter. It will be to the government’s subsidy bill, to importers’ working capital, and to the margins of anyone making fertiliser.

The system would look comfortable, given that we have some stock; but underneath the surface, it will become increasingly expensive, more rationed, and more fragile to manage. CRISIL explicitly warns that higher international prices combined with reduced LNG availability would push subsidy needs well above budget. The government had provisionally set its 2026-27 fertiliser subsidy at ₹1.71 lakh crore — a number that was already looking tight before the war.

We faced similar situations back in 2022, when fertilizer prices spiked because of the Russia Ukraine war.

The state absorbs the shock before the farmer does. But its absorption capacity isn’t infinite.

Put it in perspective

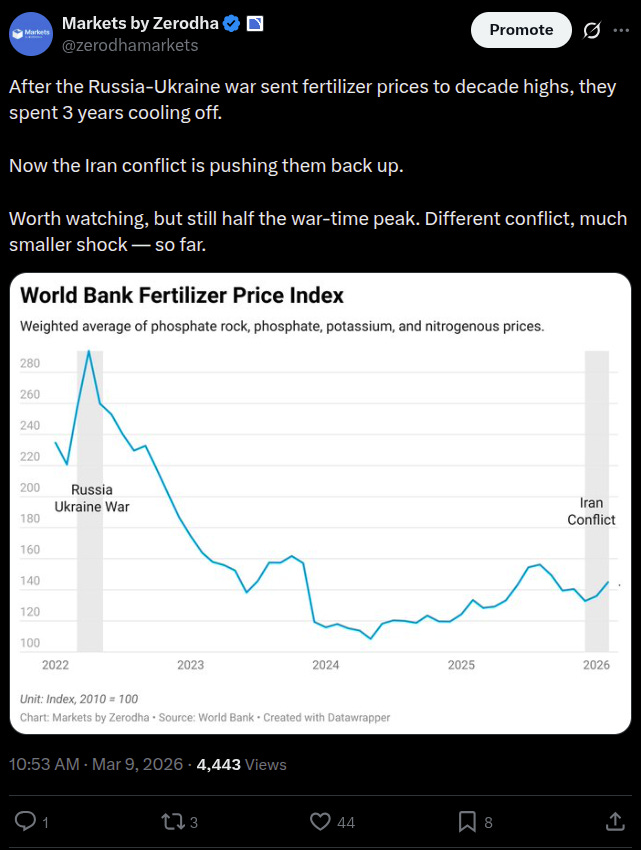

Right now, prices are rising, while supply chains are stressed. Some rationing has begun, but this is not — at least not yet — a repeat of the 2022 Russia-Ukraine fertiliser shock, when urea briefly touched $900 per tonne and global supply chains were broken for months. Current international urea prices are around $540-675 depending on the benchmark. The situation is serious, but it isn’t a full blown crisis.

India’s buffer stocks, too, are materially higher than in 2022, and the lean season provides a natural cushion that wouldn’t exist if this had hit in June.

But it all depends on how long the disruption lasts. If you want to gauge where we are, look at whether Petronet and GAIL restore allocations, whether more fertiliser producers disclose gas cuts, whether ammonia and urea prices stabilise, and whether the Department of Fertilizers’ stockpile keeps replenishing ahead of kharif. If that happens, we will have survived the uncertainty.

But if shortages grind into May and June, this comfortable story can flip into a huge problem — hitting specific states, specific crops, and specific farmers at exactly the wrong moment.

The Apple-India relationship grows deeper

This story starts with a milestone: as of today, India makes around 25% of all iPhones in the world. A decade ago, we hardly registered in Apple’s manufacturing plans.

But the biggest criticism against this is that “making“ is a generous description. Most of the high-value parts inside an iPhone — the display, the processor, the camera module — are still imported, mostly from China. All that India provides is cheap labor to assemble those parts into a phone. By that reading, India is not running an industrial revolution.

However, that framing may be changing.

We’ve never really looked at what Apple’s supplier ecosystem in India looks like. And, it turns out, that has been growing. We know the big names like Foxconn and Tata. But the suppliers sitting beneath them are what really determines whether Apple’s presence in India amounts to something lasting.

Backward linkages

Let’s start with a theoretical framework that will help us think through this story.

A country’s development isn’t just about huge, anchor factories of the kind that a multinational like Apple sets up. What matters more is the economic activity that such a factory pulls in around it — also known as backward linkages.

See, when a large MNC starts sourcing parts from locally-based suppliers, it sets a flywheel in motion. Those suppliers must upgrade to meet the anchor firm’s high standards. That means investing in machinery, management practices, and skills. An industrial base begins to form around the anchor investor.

The hope is that, once enough of a domestic base is built, workers leave to start their own firms, and standards rise across the sector. The deeper the industrial base becomes, the harder it is for the anchor investment to leave the country.

Economists Beata Javorcik and Theodore Moran have shown that, in the most successful cases of development through foreign investments, the metric of success isn’t how big an anchor factory like Apple is. You win when both foreign suppliers are investing alongside the anchor, and — more importantly — local entrepreneurs are also entering the value chain.

On the flip side, FDI can also fail disastrously. A foreign firm sets up assembly, imports almost all its components, exports the finished product, but remains entirely disconnected from the domestic economy. Jobs exist and export numbers look good, but there are no backward linkages, no technology transfer, and no upgrading of local firms. The investment sits in the country like an island.

This is the lens through which we should evaluate Apple’s India experiment — and Apple is known to have strict standards for suppliers. Are Apple’s India operations building strong backward linkages? Or are they stuck at mere assembly, hardly moving beyond it?

Building a cluster

See, a manufacturing ecosystem doesn’t arrive all at once, but builds sequentially in stages. As a country progresses through each stage, the deeper and stronger an industrial base gets, and higher the value captured by a country from every device produced.

For simplicity, we’ll divide India’s iPhone (or phones overall) ecosystem into 4 sequential stages:

First, device assembly;

Second, a sub-assembly layer of mechanical parts, cables, casings, and batteries;

Third, an electronics layer of high-value parts like circuit boards and camera modules;

Lastly, a clustering effect, where all of these stages concentrate in the same geography and begin to compound.

India’s progress through this journey will help us truly answer the question of how Apple’s India experiment is working.

Stage 1 — the anchor firms

The first stage involves large EMS firms like Foxconn and Tata Electronics — we’ve covered how they work multiple times in the past. They make the biggest anchor investments, employing long sets of assembly lines and machines to assemble the final iPhone. They kickstart the whole process.

Foxconn’s long-standing relationship with Apple is well-known — it is the most important iPhone maker. Foxconn has committed billions across several southern states of India: a ₹22,000 crore iPhone assembly plant in Karnataka, a ₹4,600 crore AirPods facility in Telangana, and a plant in Tamil Nadu that has operated since 2017.

But interestingly, Foxconn isn’t just making phone-related investments in India. It has also branched into battery energy storage and EV manufacturing units in Tamil Nadu.

India represents a huge opportunity for Foxconn. They’ve mentioned in their earnings calls how they see India as one of their most important markets. The sunk capital is already huge, and walking away from India can be genuinely costly.

The more consequential development at Stage 1, though, is Tata Electronics. After all, it’s the first indigenous anchor firm, and the second-biggest firm in Apple’s India ecosystem. After making two big EMS acquisitions, Tata now assembles iPhones at scale. Though it may not be as efficient as Foxconn yet, it’s a signal that we are not entirely dependent on foreign contractors for critical assembly work.

An added benefit of this is that Tata’s subsidiaries could even use this foothold to move deeper into Apple’s supply chain — we’ll come back to this later.

Perhaps, the most important signal of success in this stage is this. Initially, Apple’s India operations only made older-tier iPhones. It lagged the China launch of the newest model by months. That gap, however, has now shrunk to weeks, primarily because our anchor factories have picked up speed.

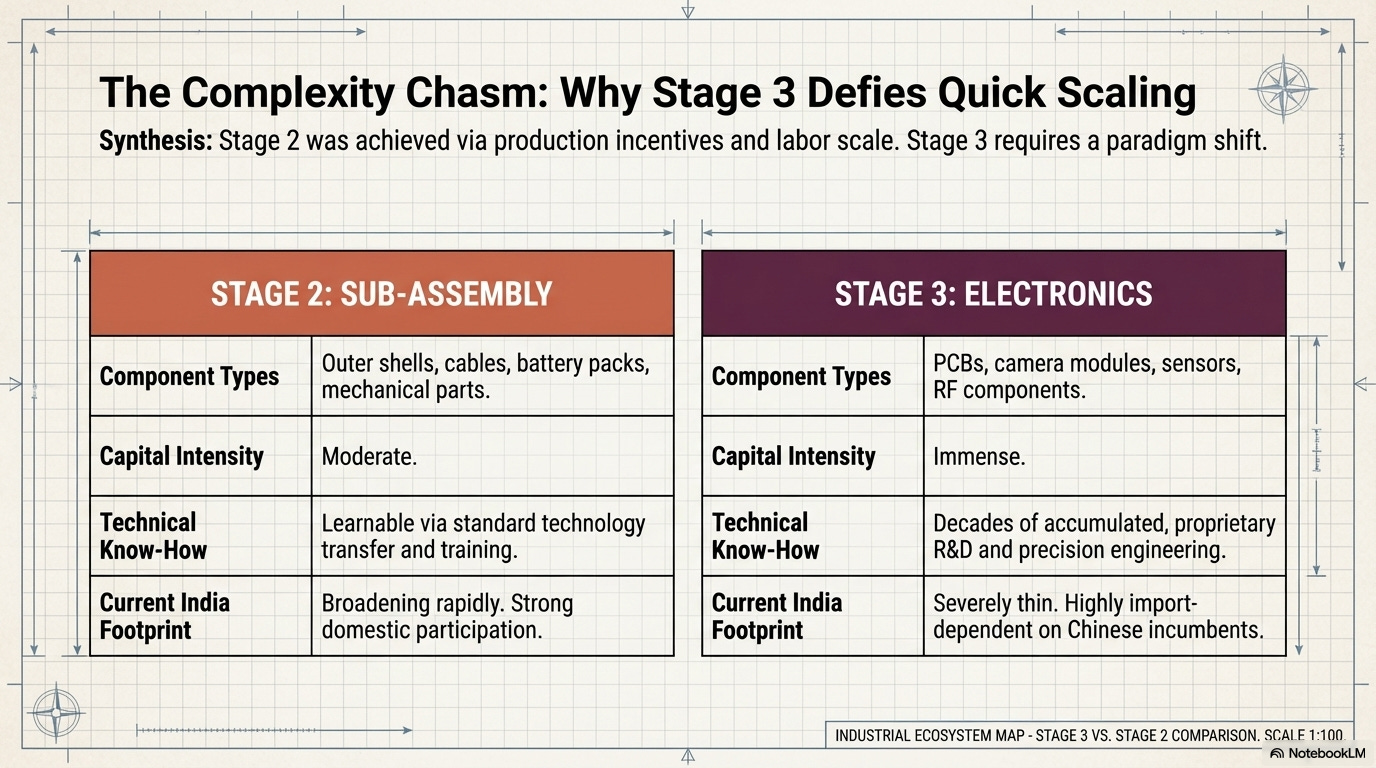

Stage 2 — the sub-assembly layer

The next stage is where the backward linkage story starts to get interesting. And Foxconn’s arrival has done what anchor investments are supposed to do: pull in suppliers.

Apple’s official supplier list in India now includes foreign firms that make power cables, connectors, chargers, battery packs, and phone casings. Some of the major foreign suppliers who have invested in India include YUTO, Jabil Electronics, battery-maker ATL, etc.

Now, these parts are mostly meant for the “outer shell” of the iPhone, and aren’t very complex to make. But they’re necessary, and represent a step-up from stage 1. These firms weren’t independently drawn to India, but came because of their biggest customer, Foxconn.

Moreover, domestic firms are entering this layer too. Take, for instance, the auto ancillary Motherson Group — it has a joint venture with a Chinese firm to make glass-related parts for Apple. Aequs, one of India’s largest aerospace part makers, makes MacBook enclosures and mechanical Apple Watch components.

In this stage, India has genuinely made good progress, capturing more value from an iPhone over time. India’s total domestic value added (DVA) in iPhones now sits between 15–20%, up from single digits a few years ago. In fact, as we’ve covered before, the DVA across Indian phone manufacturing overall has grown significantly before and after the PLI scheme was introduced.

Stage 3 — the specialized electronics layer

Stage 3 — the most technical, knowledge-intensive stage — is still lacking.

Most of an iPhone’s value truly sits in the complex, high-tech electronic parts that it houses — think camera modules, printed circuit boards, sensors, display assemblies, and so on. Building these parts at scale requires not just capital, but years of technical know-how.

Some presence here is emerging. Take, for instance, Corning — the manufacturer of Gorilla Glass. This is no mere glass, and is extremely difficult to make. But, through its joint venture with Indian firm Optiemus Infracom, Corning has made investments in India to supply Gorilla Glass this year.

Or, take Sunny Optical, a Chinese firm making camera modules through a joint venture with Indian firm Celkon. They invested over $300 million in 2023 in an Indian facility meant mostly for Apple. In fact, Titan, the watchmaker — and also a Tata subsidiary — was also in talks to supply the iPhone’s camera module.

But this layer is still really thin. We still import most of these highly-technical, specialized parts from China — which has enjoyed years of dominance here. Moreover, indigenous Indian firms are still underrepresented in it. Progress here won’t come easily or cheaply.

Stage 4 — the clustering effect

If stage 3 is cleared, one can finally expect to build industrial clusters.

Imagine a region where many different factories, their suppliers, and logistics providers just sit a few kilometers away from each other. Now imagine many such regions, or townships. This kind of density creates an economic efficiency that’s unbeatable. Here, a product can go from mere design to mass-production in mere weeks, and product re-designs and repairs are even faster.

The feedback loop in such clusters is infectious as it obviously cuts costs by a huge margin. But it also makes the whole ecosystem extremely resilient over time. China’s dominance in not just electronics but many other industries, for instance, comes from having many such clusters.

In India, there are some initial signs of such clusters. Sriperumbudur in Tamil Nadu, for instance, is the furthest along, with Foxconn’s infrastructure at its core and suppliers beginning to cluster around it. Sri City in Andhra Pradesh is developing.

But nothing in India yet approaches the density and breadth of Chinese hubs. Building genuine clusters requires a lot of patient capital, backed by infrastructure and consistent policy. India is early in this process, and will take years — even decades — to get here.

Unfinished business

While there’s plenty of road left, India seems to have made real progress. Anchor manufacturers are deepening their commitments, both foreign and domestic suppliers are entering the value chain, and India is, slowly but surely, capturing more share of an iPhone’s value.

And, to a degree, India is making moves in the right direction. The Electronics Component Manufacturing Scheme (ECMS), for instance, targets the supplier layer more directly than the first PLI scheme did — and it got an increase in funding in this year’s Budget.

But, beyond large EMS players and a select few suppliers, the domestic side of the PLI story is a little more concerning.Suppliers to a huge anchor factory like Foxconn tend to be MSMEs that often struggle even in day-to-day operations. Yet, India makes things even harder for them.

See, under the first mobile PLI scheme, every firm had to meet a sales and investment threshold. But 80% of all firms selected under the scheme failed to do so, because they were small firms that couldn’t be expected to meet those targets so quickly.

Many of the early applicants to the ECMS scheme were MSMEs. Without adequate support, they’ll not be able to meet Apple’s strict standards for being a supplier. India may even risk being left with an impressive foreign assembly sector sitting on a weak domestic underbelly.

A second problem is geopolitics. For one, China controls and weaponizes inputs India can’t easily replace — like rare earths and precision manufacturing equipment. On the other hand, Donald Trump has also taken direct aim at Apple’s India strategy, telling Tim Cook “we are not interested in you building in India“ and pressing for a US reshoring. Apple moves ahead regardless, but navigating both Washington and Beijing simultaneously will not be easy.

Conclusion

Are iPhones merely assembled in India? The evidence increasingly says no. Domestic value addition is rising. A supplier ecosystem is taking shape, even if unevenly. Indian firms are entering Apple’s value chain at multiple levels. And Apple itself is entrusting India with its more difficult work.

What India hasn’t achieved yet is a meaningful presence in the electronics layer, let alone clustering. Making PCBs at scale, for instance, is not easy, and Indian firms are indeed trying to do so. Those are the harder tests, and in comparison to China, we’re honestly still decades behind.

But every electronics powerhouse today — China, Vietnam, Malaysia — once passed through the phase India now finds itself in. And Apple’s India experiment, by most indications, may only just be beginning.

Tidbits

Trump announced that the US will build its first oil refinery in 50 years in Texas with financial backing from Reliance Industries. Reportedly, this is a “historic $300 billion deal”, which will also help reset Reliance’s historically-tense relationship with Trump.

Source: BloombergMeta has acquired Moltbook, a social media platform launched in late January where AI agents — not humans — autonomously post, comment, and interact with each other. The platform went viral almost instantly, racking up millions of registered bots within days, though it also drew skepticism over fake agents and security concerns.

Source: TechCrunchThe escalating US-Israel-Iran conflict has disrupted Strait of Hormuz oil flows, triggering an acute LPG shortage in India and sending consumers scrambling for electric alternatives. As a result, induction cooktop sales surged nearly 20 times on Amazon India in a single 24-hour window, while quick-commerce platforms like Blinkit and Zepto saw most models sell out across major cities.

Source: The Hindu Business Line

- This edition of the newsletter was written by Kashish and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Though tangential to this topic, it is astonishing that the inventor of the Bosch-Haber Process, Fritz Haber also pioneered in chemical warfare. So on one side he creates process which literally feeds humanity and on the other is responsible for thousands of deaths.

Further, like it or not, fossil fuels are still fundamental to our day-to-day life even if the green activists won't like to hear it.