The cycle of capital goods twists and turns

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The machines that make the economy go

Why central banks never get to do all they want

The machines that make the economy go

For any country that’s truly serious about scaling manufacturing, capital goods are almost impossible to ignore. After all, these are the machines that make other machines — from giant Bharat Heavy Electricals (BHEL) turbines powering our grids, to precision ABB robots automating factories, to CNC machines.

Their performance is a pretty good indicator of the economy’s health. In fact, when someone is talking about capex, you should immediately think of capital goods. After all, the capital goods industry only receives orders when an economy is heavily investing in building assets. And of late, there has been a lot of chatter about India’s capex.

That’s why, today, we’re doing a primer on India’s capital goods industry — what falls under this broad umbrella, and how to make sense of the business dynamics that drive it.

What exactly are “capital goods”?

In practice, “capital goods” is an extremely broad umbrella term that needs a little digging into.

It could include heavy machine tools used for metal-cutting and shaping machines that make precision components. Or, it could mean mining machinery like excavators, cranes, and dumpers that build roads and dig mines. Even power equipment like turbines, boilers and transformers that keep the lights on would make the cut for being called capital goods. And that’s far from an exhaustive list. As per the government, the capital goods sector can be broadly divided into 8-10 major subsectors.

Sectors aren’t the only way capital goods are classified, either. The business model matters, too. Some capital goods firms are product manufacturers – Hitachi Energy India, for instance, makes standardized high-voltage products and transformers. Others could be EPC project contractors — like L&T that builds metro systems end-to-end. Many do a mix of both.

The sector is incredibly varied. It’s not like auto or pharma, where products are more uniform; two capital goods companies might have completely different business models. What ties capital goods companies is that they make the equipment or provide the expertise needed to create other products and infrastructure.

Since it’s such a catch-all category, judging the “size” or growth of capital goods can be tricky. Officially, India’s capital goods sector contributes around 1.9% of GDP, and accounts for roughly 12% of manufacturing output. But within that, conditions can vary widely. Some sub-sectors — say, renewable energy equipment — might boom, while others like old coal-power equipment slump.

Boom, boom, boom

So, why is India’s capital goods sector suddenly at the center of the action? The reason is simple: capex. But the more nuanced answer will require a small history lesson.

For much of the 2010s, this industry languished. The last big capex boom ended around 2011, leaving companies debt-laden and cautious. India’s private sector has been cleaning up that mess since. But, things have changed dramatically in recent years.

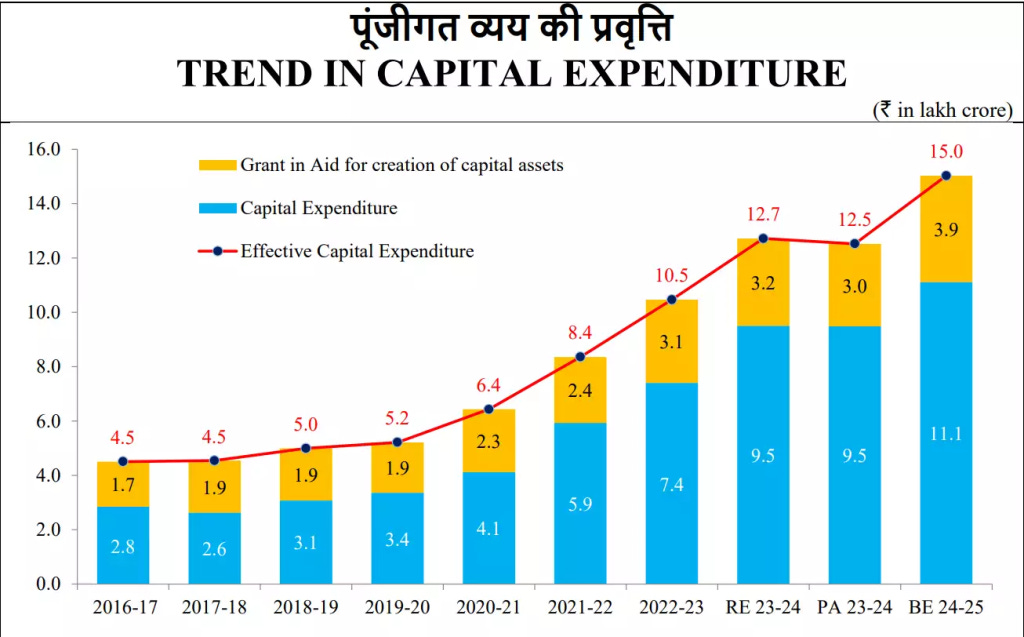

In an attempt to revitalize infrastructure, the government has opened the floodgates of public spending. For FY2024-25, central government capex was raised by ~11% to over ₹10 lakh crore. And in the ongoing FY2025-26, the Budget earmarked an even higher ₹11.2 lakh crore for capex. This is unprecedented in India’s history — a three-fold increase in government capex compared to 2019-20.

Naturally, the capital goods industry is benefitting the most out of this. Its stocks are booming, too. The BSE Capital Goods Index roared back to life, surpassing its 2007 peak after a 14-year gap and solidly outperforming the market in 2020–2024. It’s a dramatic reversal for a sector that underperformed for long.

It’s not just government spending at play, though. Potentially, we might also see a cyclical uptick in private sector capex (albeit from a low base). After years of paying down debt and playing it safe, private firms could slowly regain the confidence to invest again. Even banks are in a better mood: when NPAs are at decade-lows, it’s harder to justify keeping the credit taps shut.

But, will private capex meaningfully revive? We’re not sure yet, though there are some positive signs.

Another structural push is in defence and railways, which have historically been import-heavy areas that India wants to indigenize. On that note, campaigns like Atmanirbhar Bharat are translating into big orders for domestic capital goods players. Put it all together, and you sense that an investment cycle is underway, swinging attention back to capital goods.

But that’s just the macro story. How do capital goods firms actually make money in a capex upcycle? That’s where we get into the nitty-gritties of how a firm in this sector works.

Reading a capital goods company

While learning about them, we realized there are 4 key features that define them.

Start with the end (customer)

The first feature: who ultimately buys their equipment or services? The answer can dramatically affect a company’s fortunes. In India, a huge chunk of capital goods demand comes from government or public sector clients — think state-run power utilities, Indian Railways, PSUs, and so on.

If a capital goods firm mainly serves government orders, it naturally benefits from a public capex boom, but it’s also exposed to slow tender processes and budget politics. These contracts typically go to the L1 bidder — which is the lowest-priced bid that meets the project requirements. This often encourages aggressive underbidding. In contrast, a company selling to private industrial customers usually can differentiate on things other than price: like technology, reliability, and service.

Take BHEL, for instance. Its biggest clients are state thermal power plants, which often pay late and are politically influenced. ABB India, on the other hand, sells a lot to private factories and data centers, where decisions and payments are much faster.

More importantly, as a capital goods supplier, your end-customer’s own capex cycle becomes your demand cycle. If you supply to power companies during a huge grid buildout, your numbers will zoom. But, if you supply to auto OEMs while car sales are sluggish, you’d have a very slow year even as a well-oiled firm. In essence, you may bear some of the risks of the sector you supply capital goods to.

Order! Order!

The second feature is the order backlog: a vital industry metric. It represents the value of orders won but not yet executed, indicative of future revenue in the pipeline. A large order book signals strong demand and multi-year revenue visibility. That’s why investors often cheer when, say, L&T announces a ₹20,000 crore surge in its order book from new highway contracts.

However, not all order books are equal. One must ask: how much of that backlog will realistically convert to revenue (and profits) on time?

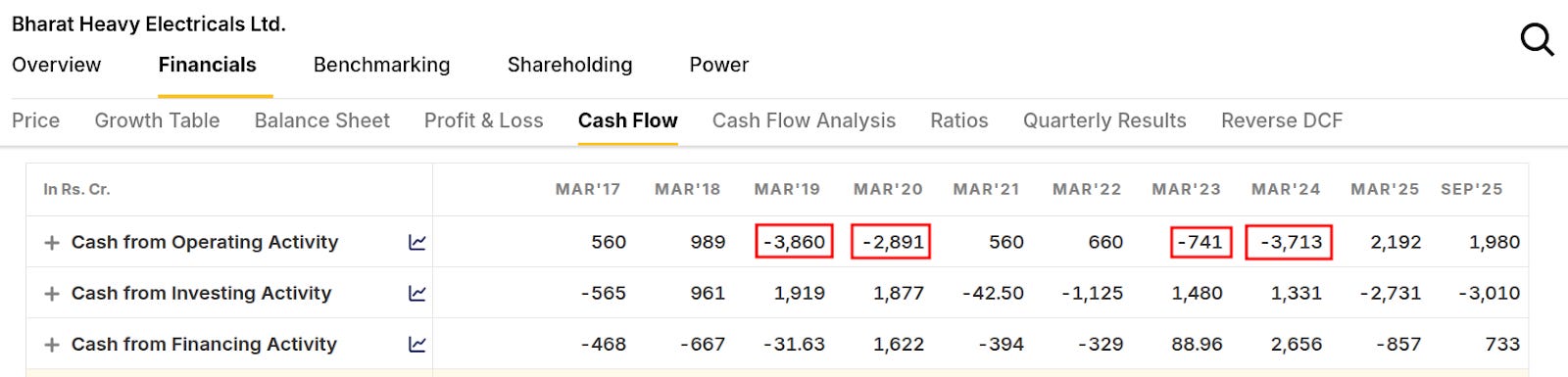

Plenty of cautionary tales have been told on this question. For instance, for years, BHEL touted a gigantic order book and had visibility on future revenue on paper. Yet, due to execution delays, the company’s revenues remained volatile and cash flows dismal. In fact, BHEL had a cumulative operating cash outflow of ₹4,260 crore over the last decade despite its hefty order book.

The lesson here is that an order book is only as good as the company’s ability to execute those orders on schedule. A “high book-to-bill ratio” (orders/revenue) could mean rapid growth ahead, or it could mean a backlog that’s stagnating.

Hello Mr. How Do You Do

The third feature is something we touched on earlier as well: the business model. Is the company primarily a product/OEM (Original Equipment Manufacturer) player, or a project/EPC contractor?

Product companies make standardized equipment, usually in factories, and sell it repeatedly, often in bulk. These businesses tend to have more stable margins and more predictable repeat orders. Once a product is proven, you can sell variants of it to many customers, and the manufacturing process itself gets more efficient over time. The cycle is also shorter: orders can turn into revenue within months, and payment terms are usually clearer.

Project companies, on the other hand, work on one-off engineering projects that involve site work, multiple components, and a lot of services stitched together. That makes the business lumpier and riskier. Projects can take years to execute, and revenue shows up in stages as the work progresses. Many contracts are also fixed-price — which means in case of delays or overspending, the contractor eats the pain. Add in other execution risks — like permits, coordination across subcontractors, and so on — and you get a business where a huge order book doesn’t easily translate to quick revenues or profits.

The risks don’t end there for EPC. In many projects, the company has to spend upfront to keep work moving — like procuring materials, mobilising teams. But, it only gets paid later, usually through milestone-based billing or only after completion. In such a situation, while the project is “progressing” on paper, the cash is still stuck because the customer hasn’t paid yet. The situation gets worse when your customer is the government, which is notorious for delaying payments even more.

This is why project companies aren’t just strapped for profits but also cash.

The Cycle Turns

The last big feature is cyclicality. This sector typically runs in multi-year booms and busts aligned with investment cycles. When the economy (or government) goes big on capex, order books swell, factories run overtime, and profits surge. When investment dries up, these companies feel the heat of revenues stalling and profits shrinking disproportionately. Understanding this rhythm is key to understanding the sector’s past and prospects.

Now, we’re clearly in an expansion phase, arguably the strongest since the 2000s. But it’s worth noting how order flow, revenue, margins, and cashflow each follow their own “mini-cycles” within the broader cycle.

Orders are the earliest indicator — they rise first when a cycle turns, often even before any uptick in actual sales. Currently, total order books being ~2 times that of annual revenue indicates companies are accumulating a multi-year backlog during this boom.

Revenue follows as companies execute those orders. There can be a lag: for example, after winning a big contract, it may take 6–12 months before significant revenue is booked. So revenue growth picks up after orders have already been on the rise.

Margins often improve later in the cycle. Capital goods firms have high fixed costs — like factories, skilled workforce, and R&D. When volumes rise, those fixed costs get spread out over many units, raising profits disproportionately. Early in a cycle, margins may be subdued due to under-utilization or even competitive pricing to win orders. But once backlogs are full, companies can be choosier with new orders and run more efficiently.

Being the last thing that turns up after revenue and orders, margins are also helping in identifying the peak of the cycle. With that in mind, we can’t help but ask: how long can this current cycle run and what could derail it? Right now, we’re probably in the early to middle innings of a multi-year upcycle — public capex still has room to run and private capex might just be beginning.

Conclusion

That, in essence, is how the capital goods industry works.

It’s a lot, but we’ve barely scratched the surface with this primer. There are so many differences within sub-sectors. Defence behaves nothing like power or industrials, the Railways has its own cadence, and so on.

Which is why “capital goods” can be a slightly misleading label. It gives you the big picture, yes. But once you go within sub-sectors, you get a whole new set of questions to answer. What’s imported versus made locally? Where does China matter and where does it not? Which companies have real moats, and which are just riding a capex wave?

We’ll get into all of that in another episode (hopefully). For now, the takeaway for us (and hopefully you as well) is that it helps to think of capital goods as less of a “sector” and more of a lens. It forces you to think in terms of capex cycles, customer quality, execution risk, and — above all — cash.

Why central banks never get to do all they want

Earlier this week, a Substack reader sent us this suggestion:

This one’s for you, Dhiraj.

Central banks tend to be wrapped in mystery, as though they practice some ancient form of sorcery. You might roughly know what a central bank does: it keeps inflation under control, and somehow keeps money systems stable. But if you’re like most people, this is probably where your intuitions break down.

Or, at least, it’s where ours did.

A lot goes into setting a “price of money” for the economy. Central banks work at an economy-wide scale, trying to make decisions that account for millions of moving parts. Every single entity in an economy affects its financial conditions, and managing everything is a profoundly complex problem. How should one even think about something so hard?

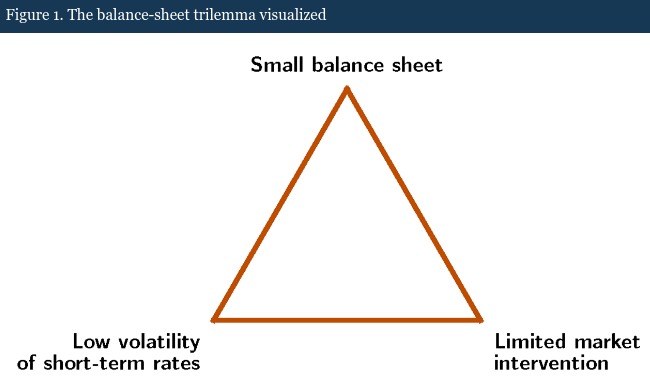

A recent note from the US Federal Reserve helped us step into a central bank’s shoes. It set up a central bank’s role as an impossible triangle — a “trilemma”. In its telling, central banks have to choose two out of three worthwhile things: a small balance sheet, limited intervention, and stable interest rates. They have to make a sacrifice. The note helped us see both, what central banks try to do, and where they hit their limits.

The note was a helpful entry point into the RBI’s inner workings as well. But as we’ll see, the RBI also has some unique constraints and priorities, making these trade-offs even harder.

Three worthy goals

At the heart of any system of money is the balance sheet of its central bank.

In theory, a central bank’s balance sheet, like any other, is just a record of what it owns and what it owes. But both of these are foundational. All of the physical cash circulating in an economy, in theory, is a liability that a central bank owes to the holder. All banks have “deposits” with a central bank — again something it technically “owes” — which is what makes it possible for you to send money from one bank to another.

To balance all these liabilities, central banks have assets. They “own” huge stores of government bonds, foreign exchange reserves, and other claims.

The Fed, basically, is talking about how a central bank sees its balance sheet.

The goals

Now, there are three things a central bank may want.

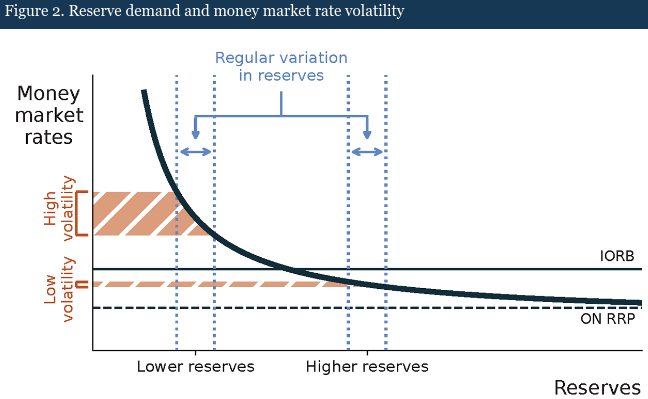

One, it might seek precise control over short-term interest rates. If the interest rates quoted in a market swing around wildly, it’s really hard for a central bank to do much about the financial conditions in the economy. For the “repo rates” they announce actually mean something, a central bank needs to ensure that financial institutions can still fund themselves, for the short-term, at roughly that rate.

Two, it might want a relatively small balance sheet. Ideally, a central bank should be a referee in a financial system; you don’t want it too big a party in the transactions themselves. If its footprint grows too large, it can turn into a counter-party to most of the system, choking the market. For instance, if too much of banks’ money sits with a central bank, money markets can dry up, while the central bank becomes the market’s main tap for money. Similarly, central banks can end up as the main buyer of government bonds in a market, pushing out private investors. This can create distortions.

Three, it might look for the financial system to run itself, by-and-large, with limited intervention. Running itself is, after all, the very job of any market. A central bank should ideally set the rules of the game, and then let things play out, instead of shifting cash and nudging rates constantly. Of course, you might occasionally have a crisis that requires the central bank to become a backstop, but on an ordinary day, the market should be able to stand on its own feet.

The trilemma

These goals, by themselves, make sense. But you can never have all three. At most, you can succeed at two of these.

Here’s one way of thinking about it: the demand and supply of money in the economy keeps shifting. There are days when there are heavy payments and flows between banks, and everyone needs a lot of money to settle these. There are other days where there’s a lot of cash sloshing around the system — for instance, when governments pay out income tax refunds. Sometimes there’s a lot of liquidity in some pockets, and a major scarcity in others.

Left to itself, this would send short-term rates swinging wildly from day-to-day.

That would make it much harder for a central bank to do its job. That leaves it with two options. One, it can tinker with the market constantly — monitoring how much cash there is in the system, conducting regular auctions, buying and selling securities, and more — all to ensure that rates stay exactly where it wants.

Two, it can permanently maintain a thick cushion of liquidity within the system, so that little shifts don’t send rates swinging. For instance, it can buy large quantities of bonds or other assets from banks, adding money to their central bank deposits. Or it can lend large amounts of money to the banking system. This liquidity ensures that banks need not bid for short-term funds in desperation, reducing the amount of day-to-day management. But it also makes the central bank a massive player.

Neither option is perfect. Both involve trade-offs and create different problems. But you simply have to choose what problems you’re willing to live with.

RBI’s triangle: when the trilemma meets Indian realities

The RBI unambiguously chases one metric: the “weighted average call rate”, or WACR.

This is the average rate at which banks lend and borrow from each other, without collateral, for a single night — so that they can meet their legal requirements. It is the “purest” overnight price of money for a bank in India. The RBI’s entire liquidity management framework is built around the indicator. A lot of its monetary policy is a game of bringing the WACR as close to its repo rate as it can.

In the trilemma we began with, this is the goal it sticks the most closely to.

How does the RBI pursue this target?

For one, the RBI creates a “corridor” around the repo rate, and locks the WACR there. Below the corridor is an interest rate “floor”, created through its “standing deposit facility” or the “SDF”. Any bank can park any excess money with it under the facility, for interest paid at 25 basis points below the repo rate. If the market were to quote anything below that, there would simply be no reason to accept those rates.

At the other end, the RBI also enforces an interest rate “ceiling”, through its “marginal standing facility”, or “MSF”. This is a mirror image of the SDF. If you are short of funds, you can borrow money from the RBI under the facility, paying interest at 25 basis points above the repo rate. If the market demands a higher rate for excess liquidity, this removes any reason to approach the market.

Together, these keep the market within a tiny band inside the RBI’s narrow corridor. Interest rates might move in response to the market, but they never deviate more than 0.25% from the repo rate.

But this can make RBI’s balance sheet swell, threatening to make it bigger than the market itself. In fact, many banks treat the SDF as a routine place to park extra funds, instead of being a backstop. Interestingly, they regularly do so even when there’s a liquidity crunch in the market.

But things don’t stop there.

The corridor is just a fence to ensure that rates don’t veer too far off. But it doesn’t guarantee that WACR sticks to where the RBI intended. The RBI isn’t just trying to keep the WACR somewhere in its corridor; it’s trying to keep it hugging the repo rate. If there’s too much liquidity in the system, banks might rarely borrow, keeping rates stuck to the floor for long periods of time. Likewise, in a time of scarcity, rates can settle near the ceiling, with the RBI doing most of the actual lending.

And so, the RBI actively manages liquidity as well. It routinely carries out operations that add or drain funds from the market. If you’ve seen headlines like this that have left you feeling clueless, well, this is exactly what’s happening.

If liquidity levels seem like they could get tight, the RBI carries out “repo auctions”, letting banks bid for temporary funds, offering collateral. Likewise, if we’re heading into times of surplus liquidity, the RBI carries out “reverse-repo” auctions to absorb cash. Follow the news, and you’ll see the RBI repeating these operations again and again.

Let’s take this back to the Fed’s trilemma. The RBI steadfastly pursues only one of its three prongs: of managing short-term lending rates. On the other hand, it’s more lax with the other two, and will accept the consequences that follow. It doesn’t mind having a massive presence in the market. And it is comfortable making regular interventions in India’s money markets.

Moreover, India, like many emerging markets, has circumstances that make this tendency stronger.

India’s extra dimensions

Emerging markets don’t just deal with domestic liquidity problems. They’re dealing with volatile foreign capital — which can bring in a flood of liquidity during good times, while suddenly pulling out when things look risky. A part of the RBI’s job, then, is to make sure these sudden flows don’t shake our financial system. It constantly shores up and sells down its foreign reserves, trying to blunt the moves of the market.

The echoes of this show up in the system’s liquidity.

Consider, for instance, that Indian banks are sitting on large dollar payments, for services that Indian companies have given. The RBI might buy those dollars from them, buffing up its foreign reserves, while paying them Rupees in exchange. That adds rupee liquidity to the banking system. Conversely, it might drain Rupees from the system to sell dollars.

To counter this, the RBI frequently has to “sterilise” the effects of its foreign exchange management. For instance, it might carry out what are called “open market operations” whenever it makes large foreign exchange transactions — buying or selling bonds so that the liquidity picture doesn’t change too much.

For one example, late last year, as the USD-INR exchange rate started going awry — hitting four straight days of record lows, and breaching the ₹91 mark — the RBI began selling its forex reserves to defend the Rupee. It helped the Rupee stage a sudden 1% recovery. To offset this, however, it soon had to step into India’s money markets, injecting ₹3 lakh crore to compensate for the drained liquidity.

This imperative makes RBI’s heavy interventions less of a “choice”, and more of a structural requirement. If you’re a central bank that is active in FX markets, you simply cannot have minimal money-market intervention while keeping the overnight rate tightly pinned. The more forex transactions you make, the more you have to manage your domestic operations.

The bottomline

We know this was a lot. But here’s a single idea to take away: a lot of what the RBI does boils down to a single goal: making sure that short-term lending happens close to the repo rate. Everything else — all the mysterious headlines you keep coming across — are downstream of this fact.

But the Fed’s neat little model reminds us that this comes with trade-offs. There are other worthy goals that the RBI is holding back on, and that choice comes with its own problems.

Then again, there are no perfect answers either.

Tidbits

Netflix’s ad push is finally working

Netflix’s cheaper, ad-supported plan is starting to show results. Ad revenue crossed $1.5 billion in 2025 and could double this year, even as subscriber growth stays strong at 325 million users. Ads are becoming a real growth lever, not just an experiment anymore.

Source: CNBCAWS, OpenAI may anchor TCS’s Navi Mumbai data centre

TCS is in early talks with AWS and OpenAI to become key clients for its first large data centre in Navi Mumbai. The facility will be built with TPG and is designed for heavy AI and cloud workloads. Rising AI demand is pushing TCS to scout more data centre sites across India.

Source: Money ControlMaharashtra plans India’s first thorium-based power plants

Maharashtra is in advanced talks to set up India’s first thorium-based nuclear power plants. Two units are planned to replace old coal plants, offering cleaner and potentially cheaper electricity. If approved, this would mark a big shift in India’s nuclear energy strategy.

Source: Economic Times

- This edition of the newsletter was written by Kashish and Manie.

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thanks guys, very much appreciated :). Also very nice to read about the RBI angle.

hello daily brief i follow you on you youtube and read the article.its really great insight by you guys but how many aritlcle/newspaper do you guys read to cover one in-depth analysis writing, how many finance folks are there to do this.

thank you

best regards

kshithij s hegde