May the thinnest (prices) win?

India’s GLP-1 ambitions face a tough moving target.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

May the thinnest (margins) win?

How do stronger patents impact Indian exporters?

May the thinnest (margins) win?

At Markets, we’ve spoken about the ticking time bomb of the semaglutide patent expiring plenty of times in the past year. Now that the bomb has gone off, so has the potentiality of a war. A price war.

A few weeks ago, Novo Nordisk cut the price of its blockbuster drugs in India by up to 48%. Ozempic, which had been selling for between ₹8,800 and ₹11,175 a month, suddenly costs a fraction of that. Some versions of the same molecule are now available in India for ₹1,290 a month — a 90 percent price collapse, in a matter of weeks.

Novo Nordisk didn’t decide to be generous, though. They were forced to. Its key Indian patent on semaglutide — the molecule behind Ozempic and Wegovy — expired on March 20th. And Indian pharma firms, who had been counting down to this date for years, flooded the market days. Dr. Reddy’s launched on Day 1, followed by Mankind, Zydus, Natco, and Glenmark.

India has followed this playbook for varieties of medicines, from cancer drugs to antibiotics — wait for a patent to expire, make the molecule cheaper, sell it to the world. It’s how we became the pharmacy of the world. Today, India supplies ~40% of US generic drug volume.

So does this mean India has disrupted the GLP-1 market? Have we successfully made the world’s hottest drug — which singlehandedly minted billions for its makers — a cheap generic?

Well, that story is a little more complicated than just saying “yes, we did.”

Why this molecule is genuinely hard to copy

Let’s start with why semaglutide has always been hard to copy.

The GLP-1 hormone that semaglutide mimics is something your body already makes naturally. Every time you finish a meal, your gut releases a burst of GLP-1 — a tiny molecular signal that tells your brain you’re full and your pancreas to release insulin. Scientists identified it in the 1980s and immediately saw the therapeutic potential. The problem was brutal and simple: natural GLP-1 breaks down in your bloodstream in about two minutes. A drug that vanishes in two minutes is not a drug.

Novo Nordisk’s chemists solved this with two modifications to the natural molecule.

First, they swapped one amino acid in the chain for a synthetic variant that the body’s enzymes struggle to break apart, reinforcing the molecule’s most vulnerable point. Secondly, they attached a long fatty acid tail to a specific location. It causes the molecule to latch onto a protein called albumin that floats abundantly in human blood. Albumin is large, stable, and the body’s filtering systems leave it alone. Semaglutide, hitching a ride on albumin, survives for roughly a week.

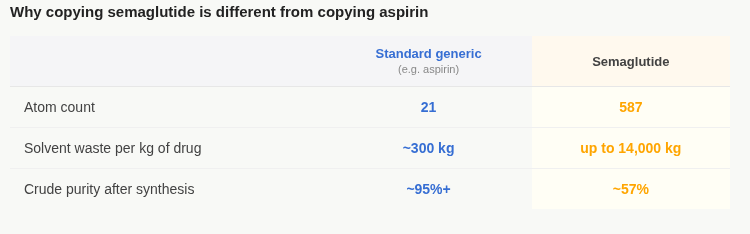

Those two modifications turned a hormone that lasts two minutes into a drug worth $40 billion a year. They also turned what might have been a straightforward generic target into something with nearly 600 atoms that all have to be in exactly the right place.

After all, if you change one amino acid, the molecule might not bind to its receptor at all. If you alter the fatty acid tail, the albumin camouflage breaks and the drug disappears in hours. Even the slightest of errors in three-dimensional geometry — something that might look fine in a basic chemical analysis — and you end up with something that looks like semaglutide on paper but behaves completely differently in a human body. In contrast, aspirin just has 21 atoms, which makes it far easier to copy.

Making a generic version of semaglutide is something else entirely. Even if you theoretically copied the design, how would you ensure that every unit of that design is manufactured perfectly?

The process for making semaglutide is called solid-phase peptide synthesis. You build the molecule’s amino acid chain one unit at a time, coupling each new unit to the growing chain through a sequence of chemical reactions. Each reaction requires specific toxic solvents at every step — these solvents have no easy substitutes. The waste generated in making one kilogram of semaglutide API weighs up to 14,000 kg. A standard small-molecule generic, in contrast, generates about 300 kilograms per kilogram of drug.

Each coupling step has a small failure rate. Even at 99 percent efficiency per step across 31 steps (and that’s a tall ask), only about 73 percent of the chains you’re building come out correctly in theory. That’s an incredulously high accuracy benchmark to meet. Additionally, in practice, state-of-the-art synthesis achieves around 57% purity. That implies that nearly half of what you make is impure in some way, and has to be separated out through rounds of expensive purification.

Plus, the infrastructure for all of this — the synthesis reactors, the high-pressure purification systems, the sterile fill-finish lines — is not what India’s generics industry was built on.

Peptide, riptide

Despite all that complexity, Indian companies did build the capability.

Dr. Reddy’s spent years developing peptide synthesis capacity from scratch — API manufacturing, sterile formulation, and a proprietary injectable pen device, all in-house at its Vizag facility. It launched its own offering, Obeda, on Day 1. Zydus became a manufacturing partner for Lupin and Torrent. Mankind launched with its reach into smaller cities and towns. No one wanted to miss the first day of the impending gold rush.

But then came Canada. Canada is one of the first major Western markets where semaglutide patents had already lapsed/ When Dr. Reddy’s filed to sell its generic there, Health Canada asked both Dr. Reddy’s and Sandoz to provide additional data before their applications could proceed. They couldn’t, and now their launch is pushed down the line.

Now, this isn’t business as usual. It doesn’t happen with standard generics. For a small-molecule drug, proving bioequivalence — that your version delivers the same drug at the same rate into the bloodstream — is a well-worn regulatory path.

But peptide drugs like semaglutide are different. Health Canada describes these as “complex synthetic products” with “possible differences that could impact safety and efficacy” — meaning regulators need to scrutinise not just whether the molecule is present, but whether subtle differences in how it was made, its impurity profile, or its three-dimensional structure could make it behave differently in patients. Indian and Canadian approvals clearly have different regulatory bars.

Moving targets

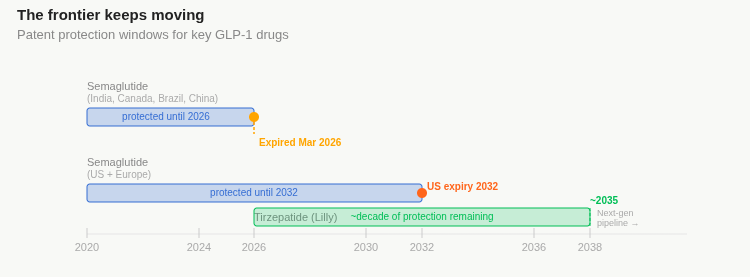

India, Canada, Brazil, China, Turkey — these are the markets where semaglutide is going generic in 2026. Together, they represent a huge share of the world’s population, and an enormous burden of diabetes and obesity. And these markets are indeed already subject to deflation in the price of the drug. real. In February, Novo Nordisk warned analysts its revenues could fall by 5-13% this year because of these expirations.

But here is what Novo Nordisk’s revenue actually looks like. India’s GLP-1 market was worth ~$110 million in 2024. Novo Nordisk’s global GLP-1 revenues last year were over $40 billion — almost entirely from the US and Europe, where patients or their insurers pay $700 to $1,000 a month and have no cheaper option. The Indian market is roughly 0.3 percent of global GLP-1 revenues.

The US patent doesn’t expire until 2032, lending Novo Nordisk 6 more years of exclusivity in the market that drives the vast majority of their semaglutide revenues.

What’s more, while Indian companies were spending years building the capability to manufacture semaglutide, something was already happening in the market they were building toward.

See, American pharma firm Eli Lilly makes Mounjaro, which is based on a molecule called tirzepatide. It does what semaglutide does, but while semaglutide targets one hormone receptor, tirzepatide targets two simultaneously.

In a head-to-head trial in late 2024, tirzepatide beat semaglutide on weight loss outcomes. By October 2025, five months before the Indian semaglutide patent even expired, Mounjaro had already overtaken Wegovy as India’s top-selling GLP-1 by value. Lilly has approximately a decade of patent protection on tirzepatide remaining.

In essence, while generics approach the bottom, the innovators seem to have moved to the next floor.

And the pipeline keeps moving. Novo Nordisk is advancing a next-generation molecule that combines semaglutide with a second hormone and produces substantially greater weight loss in early trials. Both Novo and Lilly have oral GLP-1 pills — daily tablets instead of weekly injections — in late-stage development. If oral versions achieve comparable efficacy to injectables, the competitive picture changes again. Each new drug carries its own decade of patent protection.

Conclusion

On March 20th, 135 million Indians with diabetes were now able to now access a drug that, perhaps, most couldn’t afford at branded prices. One study published last month estimated that semaglutide could theoretically be manufactured for as little as $28 per patient per year as competition scales up. In comparison, in the US, patients still pay an annual cost of over $10,000 (~₹9.3 lakh).

But the framing of India “breaking the GLP-1 monopoly“ is a little more complicated. There are still question marks over how big the addressable market for generics really is. Indian pharma firms are struggling to get over Canada’s rules. The US and European markets don’t open until 2032. And the drug at the centre of all this had already lost its crown in India’s own market before the patent war was even over.

How this race to the bottom unfolds is really anyone’s guess.

How do stronger patents impact Indian exporters?

In 2002, India overhauled its patent system. The Patents (Amendment) Act extended protection from 14 to 20 years, introduced product patents across most technological fields, and brought India’s framework broadly in line with its commitments to the World Trade Organization.

For firms that had spent years navigating an uncertain intellectual property (IP) landscape, the reform made the rules legible. It provided safeguards for industrial R&D efforts undertaken by companies, while also attracting foreign firms to set up shop here.

But not every firm experienced that resolution the same way. A 2025 paper by researchers at IIFT’s Centre for WTO Studies — Qayoom Khachoo, Ridwan Ah Sheikh, and Pritam Banerjee — uses the 2002 Act to ask a specific question: did stronger patent protection actually help Indian manufacturers export more? It looks at the impact of intellectual property rights as an underrated factor in Indian manufacturing.

The hypothesis

Often, a reform in intellectual property isn’t really a uniform shock. It doesn’t land the same way on every firm.

For a company that had been investing in R&D through the 1990s, paying royalties to access foreign technology, and building internal technical capacity — a stronger patent regime changes a lot. It makes the returns on that investment more secure. It makes the firm a more credible partner for multinationals thinking about who to share technology with.

For a company that had made none of those investments, and competed primarily on cost, sourced domestically, and had no particular stake in the IP landscape, the same reform changes relatively little. The environment improved, but they had no accumulated capability to leverage the improvement.

This asymmetry is the core of the paper’s hypothesis. The authors argue that the firms most likely to benefit from the 2002 Act were those that had already demonstrated a commitment to technology before it passed. Prior investment was the largest determinant of subsequent gain.

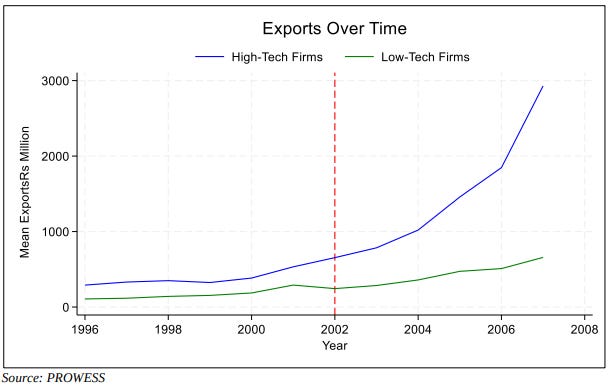

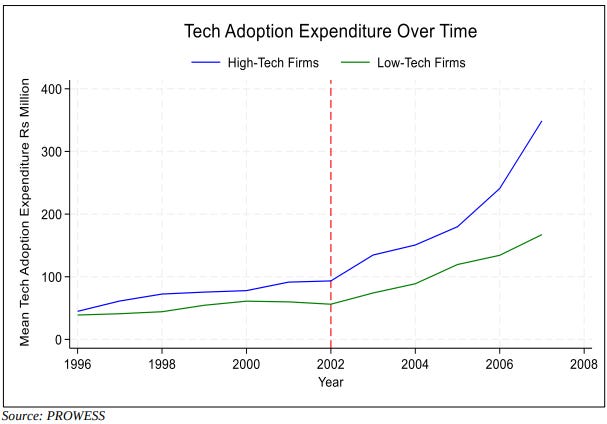

To test this, they use CMIE’s PROWESS database, spanning roughly 2,500 unique Indian manufacturing firms from 1996 to 2007. They split these firms into two groups based on spending on R&D and technology licensing in the years before the reform which happened in 2002. Firms spending above the industry median during 1996–2001 are classified as high-tech. Everyone below is low-tech.

The 2002 Act, then, acts as a natural experiment: it applied to all firms simultaneously, on a fixed date, with no gradual phase-in. Both groups were on similar export trajectories before 2002. Much of the divergence that opens up afterward can plausibly be attributed to the Act itself.

The main finding

So, to answer the original question: yes, stronger patents did help Indian exports. High-tech firms exported ~17% more than low-tech firms in the years following the reform, once standard firm-level controls are included.

Additionally, the reform also increased the gap between how much each type of firm spent on technology adoption. After 2002, high-tech firms saw a more-than-threefold increase in technology adoption expenditure, but low-tech firms didn’t enjoy a similar growth.

Two mechanisms are at play here. One of them is obvious: stronger patents protect a firm’s innovations from being copied abroad, making it safer to sell in foreign markets. But that only partly explains the findings. The more important channel the paper is identifying is how foreign partners behave toward Indian firms.

When IP enforcement is weak, international supply chain partners (like MNCs or specialised input suppliers) are cautious about how much proprietary knowledge they share. Licensing a process, co-producing a component, or entering a joint venture: all involve transferring knowledge the foreign partner doesn’t want to lose. If they can’t trust the legal environment to protect that transfer, they’ll do it on terms that limit how much the Indian firm actually learns.

When enforcement becomes more credible, foreign firms become more willing to bring Indian manufacturers into their supply chains as genuine partners. They’ll share sophisticated inputs and license technology on reasonable terms. This is why the paper frames the export gain as much more than just an uptick in the export shipments. This is integration into the global value chain for a product. They got pulled into more complex production relationships that otherwise, they probably wouldn’t have benefited from.

In fact, high-tech firms didn’t only export more after the reform — their raw material and total imports rose by ~18% as well. What this implies is that domestic high-tech firms are now pulling in specialised inputs that foreign suppliers had previously been reluctant to share.

The nuances

A few caveats complicate the story.

The first involves what happened to imports across the full sample. While high-tech firms imported significantly more, total imports and capital goods imports actually fell across all firms after the reform.

Why did that happen? Well, when patent protections strengthen, foreign technology suppliers also gain bargaining power. They can charge higher licensing fees and restrict who they deal with. For a firm without existing technical credibility, importing advanced machinery became more expensive and harder to arrange. Many shifted toward domestic alternatives, or waited for technology to come through FDI and joint ventures.

These arrangements became more common precisely because stronger IP made multinationals more comfortable investing in India directly. The reform made technology flow more selectively, not more freely.

The second complication is about the low-tech firms. Of the 2,500 firms in the dataset, 62% are classified as low-tech. This is the majority of India’s organised manufacturing sector, the firms that employ the most people. For them, the 2002 reform only modestly helped exports. Their sourcing behaviour was also largely unchanged. The significant export gains that the paper documents are almost entirely a story about what happened to the high-tech minority.

The reform didn’t create technological capacity where none existed — it amplified capacity that was already there. A firm that had spent the 1990s investing in R&D and learning how global supply chains work was ready, in 2002, to run with a stronger IP environment. A firm that had done none of that had no equivalent foothold. Stronger patents gave it more secure ownership of very little.

What this also means is that bigger companies disproportionately benefited from the 2002 reform. After all, they have the advantage of economies of scale, which positions them to absorb high costs better.

The third caveat is tariffs. Higher import tariffs appear consistently across every specification, associated with worse trade performance on both the export and import side. A firm needs access to imported inputs to actually use what a stronger patent regime enables. For the majority of firms operating in protected sectors with limited global connectivity, that access was constrained. In that sense, the paper says, IP reform and trade openness go hand-in-hand.

What this tells us

India is currently running an extremely ambitious innovation policy push. Production-linked incentive schemes are channeling capital into electronics, pharmaceuticals, and semiconductors. The Anusandhan National Research Foundation has been allocated ₹50,000 crore over 2023–2028. The argument underlying all of it is that building a stronger environment for innovation will help Indian manufacturers climb the value chain.

The 2002 Act is the clearest historical evidence we have on whether that holds. And it does hold — but with a catch. What determined whether a firm actually benefited wasn’t the reform alone. It was whether the firm had already done the slower work of building technical capacity before the reform arrived.

If most of our organised manufacturing sits outside the technology-intensive tier when the next wave of reform lands, the same pattern will repeat: real gains, concentrated only where capability already existed. These firms, which are often really small, will need more targeted R&D incentives.

Tidbits

Fintech unicorn Razorpay prepares confidential IPO filing within weeks, targeting $600-700 million raise at $5-6 billion valuation, down from $7.5 billion peak, as FY25 revenue jumped 65% to Rs 3,783 crore but net loss hit Rs 1,209 crore.

Source: ETReutersMultiple states including Andhra Pradesh (Rs 4,600 crore), Maharashtra (Rs 4,000 crore), Rajasthan (Rs 4,000 crore), Telangana (Rs 3,000 crore), and Punjab (Rs 1,300 crore) will borrow through State Government Securities auction on April 21 via RBI’s E-Kuber platform.

Source: ETGold demand during this year’s Akshaya Tritiya stayed muted as prices — up 63% from last year’s festival to ₹1,54,609 per 10 grams — kept jewellery buyers on the sidelines, with volume down even as total spend rose. Demand was lower than normal across most of the country, with the exception of a few southern states.

Source: Reuters

- This edition of the newsletter was written by Aakanksha and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Has the microfinance credit cycle turned?

Has the microfinance credit cycle turned? That’s the question we set out to answer by digging through 144 concalls across 18 companies over eight quarters. Instead of looking at management commentary in isolation, we track how the narrative evolved over time—from peak optimism to a full-blown credit shock, and now signs of recovery. The idea is to connect the dots and understand what really drove the cycle, and more importantly, what the industry looks like on the other side.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Tbh, its really interesting to learn about these market segments where we hear very little about, overall it was a good read.