India's metro ridership problem

And why reality rarely matches up to the projected numbers

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Do people actually use India’s metros?

The great NBFC performance split

Do people actually use India’s metros?

[Edit: The Aqua Line became fully operational only in October 2025. Average weekday ridership in October 2025 was 1.41 lakh — up from the 20,000 cited in the piece, which reflected only the partial stretch.]

Earlier this week, on Monday, we spoke about how metros are built. There were a lot of things that we couldn’t possibly cover in a single story. Today, we will do the second part of that story. We would highly recommend that, before diving into this one, you read the prequel — or, as some of you might already do, summarize it using an LLM :)

To quickly recap, we spoke about why cities need metros in the first place, how they get funded, and why few metros in the world actually make commercial sense. Governments build them anyway because the alternative — letting urban congestion get worse and worse — has its own steep cost.

Today, our questions take us beyond the demand planning side of things, and into the realm of the operations of a metro. For one, what are the bottlenecks faced by builders when they start digging the ground? Secondly, actual ridership numbers are often shorter than what occurs in real life. And lastly, an underrated problem in building metros is related to last-mile connectivity, which often spoils the demand planning done.

Let’s dive in.

Knock knock. Who’s there?

The construction of a metro rarely begins immediately after approval and the appointment of a contractor. There’s a long wait before a single foundation can be sunk, but it’s not without reason.

You see, over the past decades, different agencies and utilities have been laying infrastructure under our roads, but with little coordination between them. There are water and sewage pipes, electricity cables, telecom ducts from a dozen different companies, and gas lines. All of it is invisible from above.

Even for an elevated metro that runs on concrete pillars above a road, you need to sink pile foundations into the earth at regular intervals along the entire route. These are large concrete columns drilled 25-30 meters deep that will eventually hold up the pillars. These pillars, in turn, hold up the viaduct which the trains run on.

However, right where you need to sink a pile, there might be a water main at one and a half metres, or a high-tension cable at three. You cannot drill through any of these — they have to be physically moved first. Since it’s utilities like water and electricity being moved, this process is called utility shifting.

The metro team first has to figure out that the pipe is even there, which requires a combination of deep radar surveys and digging small test pits by hand to see what’s below. Then, if there’s a conflict with a water main, the team approaches the municipal water authority and explains what needs to move. The water authority reviews the proposal, raises concerns, and suggests modifications—maybe the new route passes near a sewage line and needs separate clearance from the sanitation department.

This back and forth takes weeks. Once a route is agreed upon, the water authority has to go through its own internal process. Naturally, this has to be done without disrupting the flow of water and electricity to households. The pipe cannot simply be switched off while it’s being rerouted. You have to build a temporary bypass to keep water flowing, reroute the main, pressure-test the new route, and only then dismantle the bypass.

Now the pile rig can come back to this spot. But maybe, during piling, the team discovers a telecom duct that wasn’t on any map. And this whole process starts over. Utility shifting is one of the major reasons metro projects in India run late.

However, what this also shows is that often, Indian cities don’t have accurate maps of what’s under their own roads.

In well-managed cities like Singapore, every utility authority maintains a precise, constantly updated digital record of everything underground. When any construction project begins, you query this system, get an accurate picture of what’s below, and plan accordingly. In Indian cities, though, no such unified record exists. Each agency holds its own information, often on paper, often incomplete.

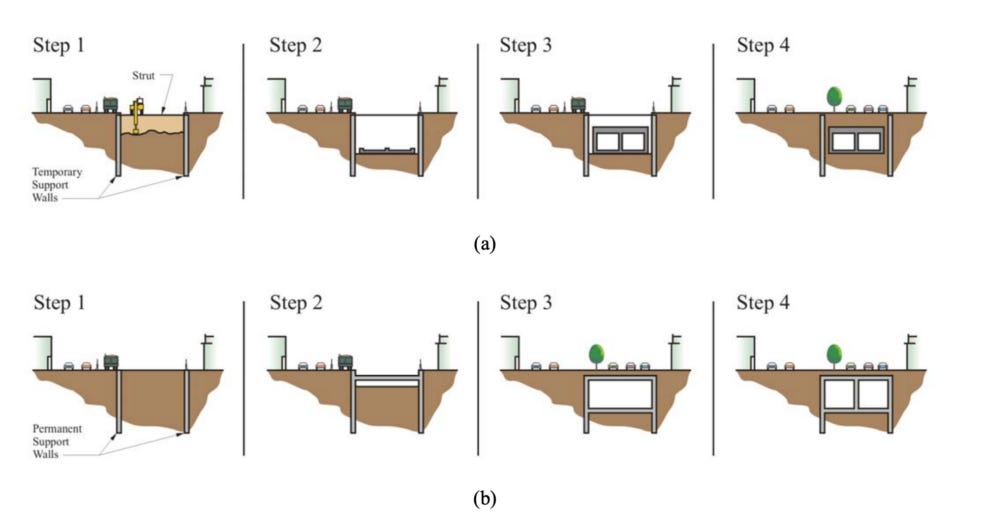

Now, not every metro can run above the ground on elevated pillars. In the densest parts of India, the metro has no choice but to go underground.

For underground stations, you excavate a large pit from the surface, build the station inside it, and restore the road above. This process is called cut-and-cover.

The tunnels connecting one station to the next are bored using Tunnel Boring Machines (TBMs). These are enormous cylindrical machines with a rotating face covered in hardened steel cutting discs. As the face spins, it grinds through the soil or rock ahead, and the broken material gets carried backward through the machine and hauled out to the surface.

Before a TBM drive begins, engineers drill boreholes from the surface at intervals to sample the soil and map what’s below. But boreholes are just sample points. The ground between two boreholes can be completely different from what the samples showed. This lack of information is a huge bottleneck for engineers.

On a good day in decent ground, a TBM advances 10-15 metres. On a bad day,you might encounter unexpected obstacles like more rock or hitting water under pressure — in which case, it barely moves at all. A single tunnel drive of 3 kilometres can take well over a year.

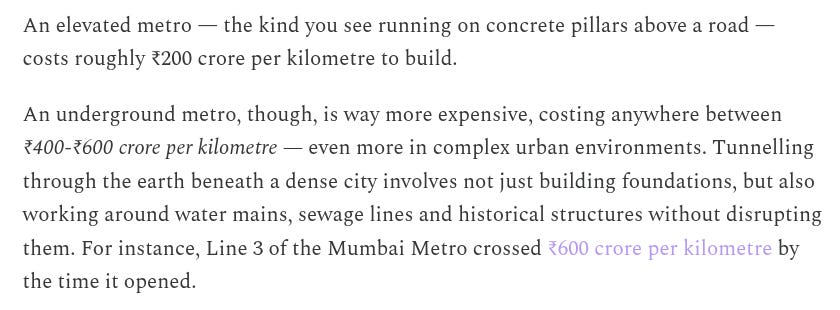

This gap between what maps say and what’s actually there is a version of the same problem we described with utility shifting — Indian cities simply don’t have reliable 3D pictures of what lies beneath them. It’s why underground metro construction costs two to three times more per kilometre than elevated, and why projects with large underground lines often run late.

Do people use metros?

Now, say a metro is built, and its economics are mapped out. Do people actually use them?

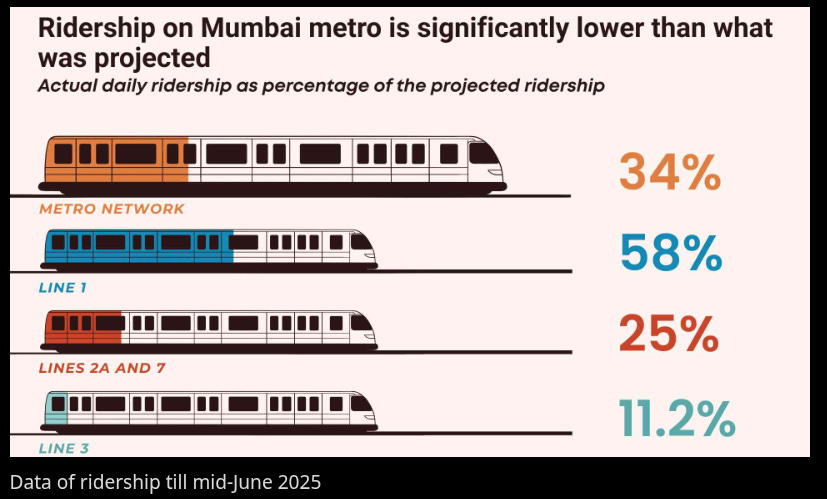

In 2023, IIT-Delhi and the Infravision Foundation published a study that looked at ridership performance across India’s metro systems. What they found was that most Indian metros are running at just 25-30% of their original projections. Delhi — the largest, most mature metro network in the country — is the best performer, and even Delhi is at 47%. A CAG audit found that specific corridors in Delhi’s Phase III were at just 21%.

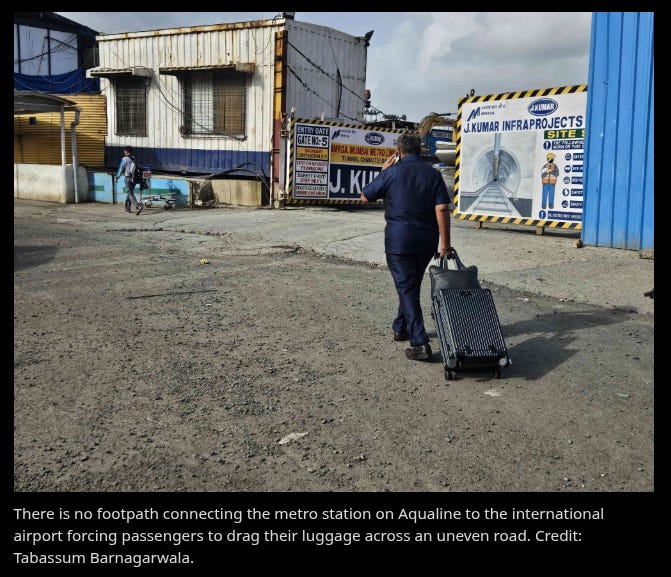

Mumbai’s story is more concerning. The Aqua Line, the city’s first underground metro, which cost roughly ₹14,000 crore to build, averages fewer than 20,000 daily passengers, against a projection of 4 lakh. Across all four of Mumbai’s operational metro lines, total daily ridership is under 7 lakh, against an aggregate projection of nearly 19 lakh. The city is spending over ₹90,000 crore building its metro network, but only getting a fraction of the usage those numbers were built around.

So where do these projections come from, and why are they so consistently wrong?

When a city wants to build a metro, it hires consultants to study travel patterns and build a demand model. The consultants survey people about where they travel, what modes they use, and how long journeys take. From that, they estimate how many trips would shift to the metro if it existed, and project this forward 30 years as the city grows. The resulting ridership forecast becomes the financial backbone of the project — loan sizes, repayment timelines, and government approval all rest on what this model says.

As we mentioned in the previous piece, everyone involved in producing this model has an incentive for the number to be high. The city government wants a high projection because it makes central government approval easier. The consultants want high numbers to please the client and repeat-book them. Nobody in the chain is rewarded for being conservative.

The biggest problem of all

However, even if the demand models were honest, metros in India would still face a problem that no model has properly accounted for: people have to actually get to the station.

When someone decides whether to take the metro, they usually think about the entire journey — getting from home to the station, the ride, then getting from the station to their actual destination. If those first and last legs are painful enough, people may choose to stick to the road, even if the metro is faster in the middle.

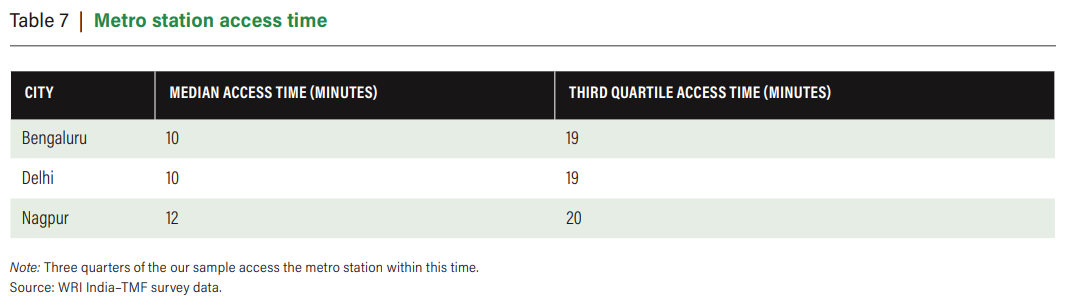

A WRI India study that surveyed 7,200 commuters across Delhi, Bengaluru, and Nagpur found that commuters are only willing to spend about 20 minutes total — including waiting time — on the first and last legs combined. Beyond that, most give up. And that threshold is consistent across income groups and cities.

Outside most stations, hitting that threshold is harder than it sounds. Autos that cluster at the exits often quote flat rates that make the last kilometre nearly as expensive as the metro ride itself. Feeder buses run so infrequently that waiting for one alone can push you past that 20-minute limit — and in many places, they barely exist. And even before you get to an auto or a bus, the footpaths outside most stations are broken, encroached upon, or simply don’t exist — making even the walk to the station exit harder than it should be.

In the end, the metro ends up serving only a narrow slice of commuters for whom the last-mile problem is manageable. The same WRI study found that very low-income commuters are often priced out by the combined cost of the fare, and informal modes of transport fill the gap. Meanwhile, high-income commuters don’t bother because last-mile options are too unreliable and they’d rather just drive.

Conclusion

There is an odd irony running through all of this.

Building a metro is one of the hardest things a city can do. India has gotten reasonably good at it. What we haven’t gotten right is everything around the metro — the maps of what lies underground, the honest demand models, the feeder buses, the footpaths.

These aren’t hard, unsolvable engineering problems. There are issues of coordination. And yet, city after city, that’s exactly where things fall apart. India keeps building world-class infrastructure into a system that isn’t ready to use it.

The great NBFC performance split

In recent editions, we’ve spoken extensively about banks — both private and public — and how they performed in the quarter gone by. Now, it’s time to look at NBFCs.

That is, unfortunately, a trickier job. NBFCs don’t fit neatly into one box. Banks, despite their differences, usually operate within a similar structure. NBFCs don’t. Some only fund those building a house. Some focus their attention on vehicles. Some, on gold loans or microfinance. Even diversified giants, like Bajaj Finance, have a range of specialised business lines that command most of their attention.

That is to say, one can’t treat NBFCs as a uniform category.

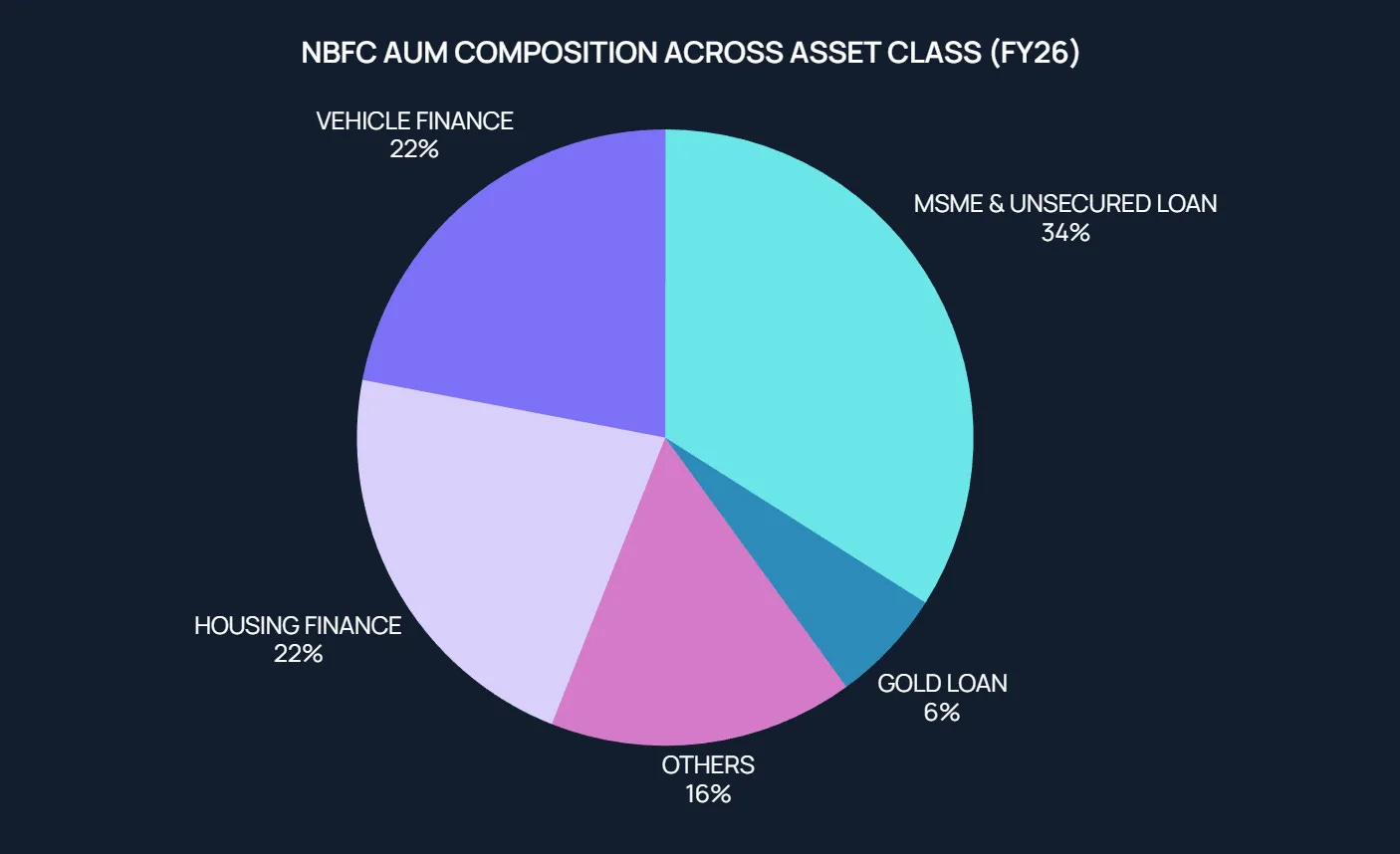

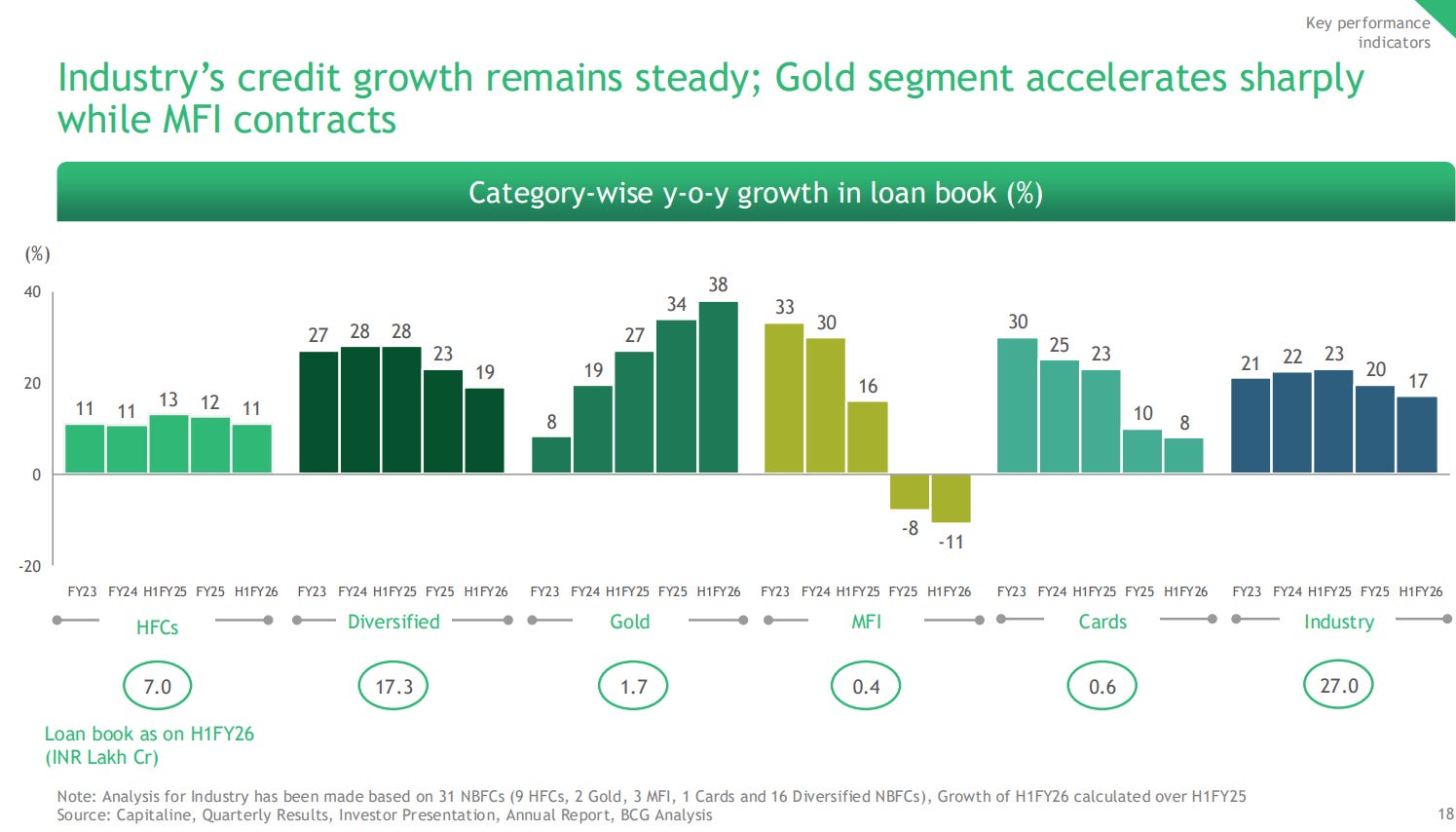

At a headline level, the sector looks perfectly fine — in fact, it shows healthy, steady growth. Its total ‘assets under management’ were up around 18% year-on-year. But this isn’t a single sector — not really.

That is why, once you break it down by company, you see divergences appear. The traditional growth engines — home loans and vehicle finance — are losing momentum. These two, together, account for more than 40% of total NBFC lending. The slowdown is worth noting.

That capital, instead, is moving to very different pockets: loans against property, gold loans, and select parts of unsecured lending. This is visible across the sector; but it’s also visible in how individual NBFCs are adjusting their mix. Account for that, and you begin to see a shift in the direction of credit in India.

That’s what we’re digging into, today.

The housing finance squeeze

We start with housing finance companies, or HFCs.

For years, HFCs followed a straightforward business model: originate home loans, earn a spread, grow your book. It was a fantastic formula — until banks learned how lucrative it could be.

Banks are structurally better suited for this business. They sit on low-cost ‘CASA’ deposits — the current and savings account money people keep with them. This is the cheapest source of money there is, giving them a huge funding advantage. With such cheap capital, banks price home loans aggressively, leaving HFCs cornered. They must now choose: either match the rate and sacrifice margins, or keep your prices, and lose borrowers. Neither option is pretty.

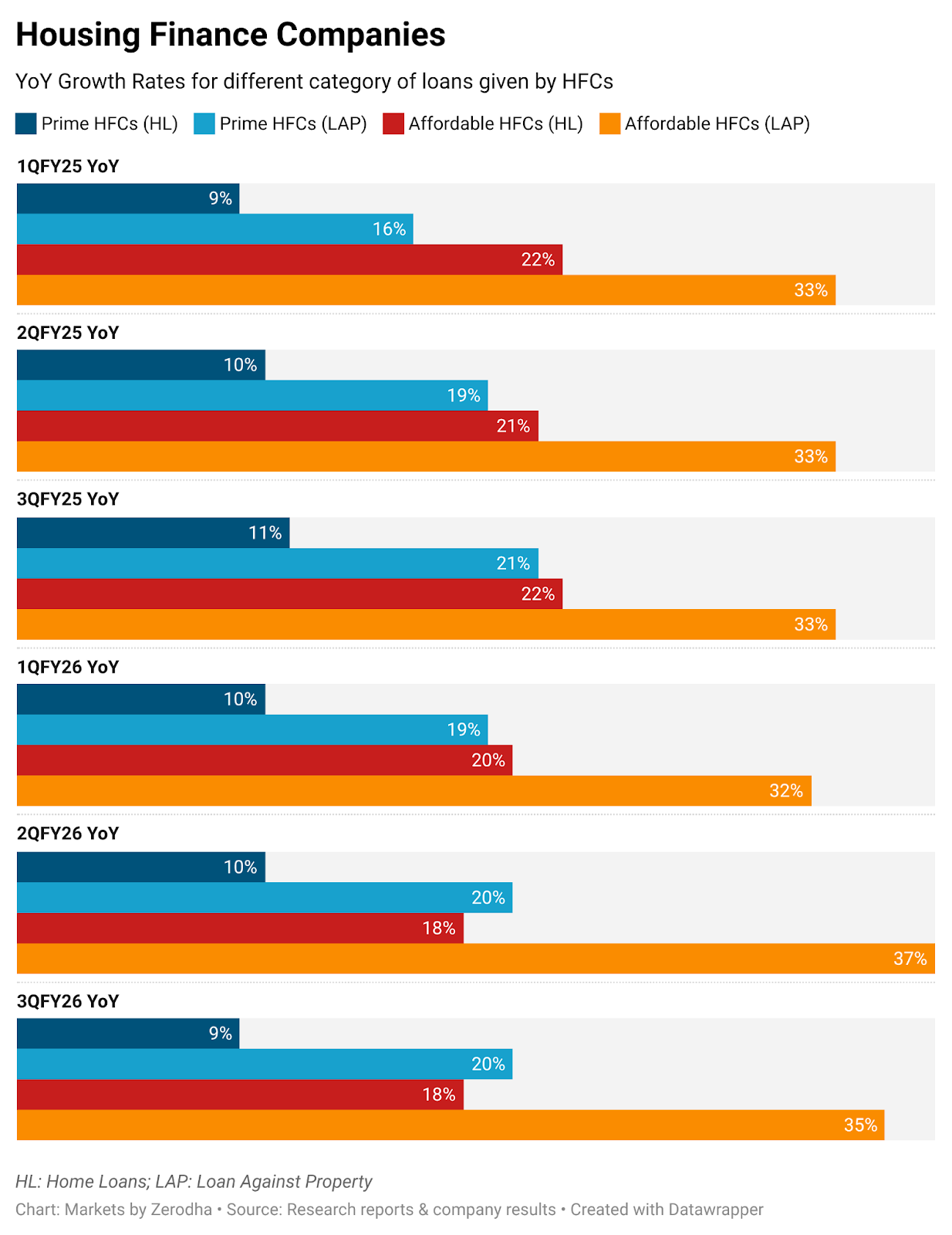

As a result, last quarter, prime HFC home loans — typically above ₹20–30 lakh — grew just 9% year-on-year. That barely outpaces the growth in our nominal GDP. They are no longer expanding their footprint; they’re barely keeping pace with the economy.

So, HFCs have shifted gears. Their growth is now coming from riskier products: loans against property (LAP), construction finance, and lease rental discounting. The LAP books of prime HFCs, for instance, grew 20% YoY — more than double the rate they grew home loans by.

You see something similar in affordable HFCs, which give loans under ₹20–30 lakh. Their home loans grew 18%, but LAP jumped by twice that — 35%.

Take Bajaj Housing Finance, one of India’s largest listed HFCs. On its investor call, the company’s management acknowledged that traditional home loans are lagging, and that they had to pivot to non-home loan segments for growth.

This, too, is just a gambit. If it doesn’t work out, they’ll have to shift to their Plan B, which is assignments. Essentially, they might buy out loan pools from other lenders, and earn whatever spread they can get from there.

This marks a change in the economic logic of HFCs.

It’s usually safe to lend to a salaried employee trying to build a home; few people gamble with the home they’re living in. These other products, meanwhile, are inherently riskier. They tie HFCs’ fortunes to things like real estate cycles, or the cash flows of commercial developers. They do come with a better yield — which is why HFCs can still hold their own in these segments. But it fundamentally changes the risk profile of an HFC.

Vehicle finance: the deflation puzzle

Vehicle finance, last quarter, presented a rather counterintuitive story. The growth in vehicle loans was muted — but on the other hand, vehicle financiers reported better spreads. That is, their loan books weren’t growing, but margins were.

How does that work?

To understand this, begin with why core growth is sluggish. The GST rationalization that brought down effective tax rates on vehicles was a positive for car sales. Volumes jumped across the board, from small passenger cars to large SUVs. But there was a catch: lower taxes meant lower sticker prices. That is, the ticket size of each loan was smaller. Even if a financier was writing more loans, each loan would be for a smaller amount. And so, despite a lot of disbursement activity, their aggregate assets under management were flat!

At the same time, these companies saw their spreads rise mechanically. See, vehicle loans are overwhelmingly given at fixed rates. While the interest rates on home loans, for instance, might float with benchmarks, they stay the same for vehicles. And so, when the RBI cuts rates — as it did all through last year — your home loans might get cheaper, but not the loans for your car.

This was bad news in previous years, when rates climbed and NBFC borrowing costs moved up — squeezing vehicle financiers’ margins. But in 2025, the cycle flipped. The cost of their funds eased. In fact, several large NBFCs have noted a visible compression in their borrowing costs, of roughly 10–15 basis points.

On the other side, their assets didn’t see the same movement reprice down immediately. Many of the loans on their books were given out when rates were higher. This might come down over time, as they start giving cheaper loans after the rate cuts. But when their book is taken together, the blended yield will remain elevated, as their older loans continue to offer better high yields.

That’s why their spreads widened “automatically” last quarter.

This is, however, a temporary tailwind. Soon, they’ll have captured the benefits of their easing cost of funds, as interest rates bottom out. And then, competition — especially from banks — will push fresh loan rates lower, even though their cost of funds will stay the same. And with that, spreads might start falling again.

And so, you’re increasingly seeing vehicle financiers pivot as well, much like HFCs. For instance, Cholamandalam’s SME and home equity (LAP) books grew 33% and 31% respectively, dwarfing its 17% core vehicle growth. Vehicle financiers are turning themselves into diversified lenders, who only happen to have started with vehicle finance. Their rural and semi-urban branch networks are turning into portals from where they can cross-sell higher-margin products to their customers.

Microfinance’s behavioural crisis

On the surface, the microfinance sector has looked ugly for some time. Its assets under management have been shrinking for a while, and its borrower base has also come down. But if you look past the headline decline, there are early signs of stabilisation.

Last quarter, in fact, MFI disbursements grew by 5% year-on-year, and by 9% over the September quarter. Clearly, the sector isn’t “dead.” It had overheated, but after a phase of deleveraging, the sector seems to be making a cautious return to growth, in pockets where it feels confident.

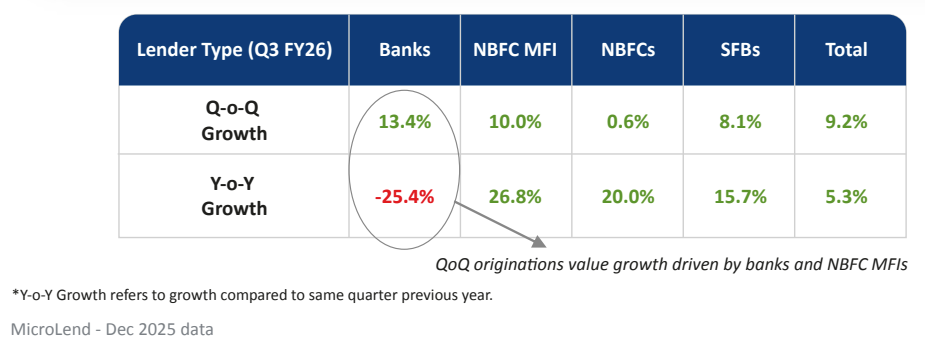

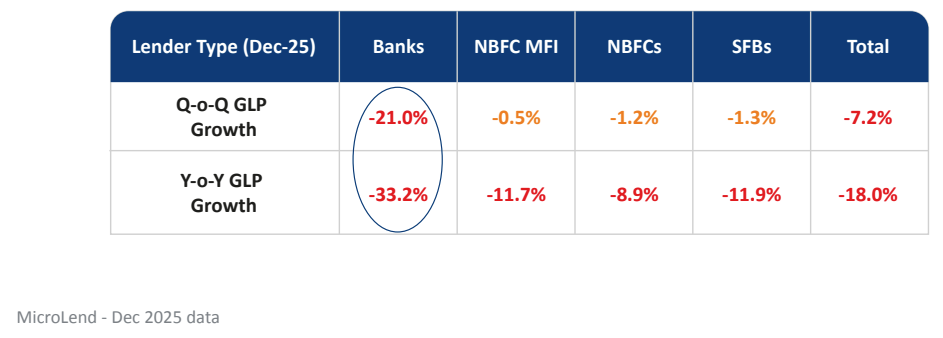

Not that everyone’s back. Banks are still pulling back hard. Their gross microfinance book fell by a stunning 21% quarter-on-quarter. The same universal banks that chased MFI yields in good years are now cutting exposure as fast as they can.

Specialised MFIs, on the other hand, have been far steadier. Their loan book was almost flat, with just a 0.5% sequential dip, and their disbursements actually rose 10% QoQ. The result was visible immediately. These institutions gained market share in a single quarter, taking their slice to 42% of the total MFI market. As the generalist banks vacated the space, the specialists, with their local teams and collection systems built for micro-finance, are reclaiming lost ground.

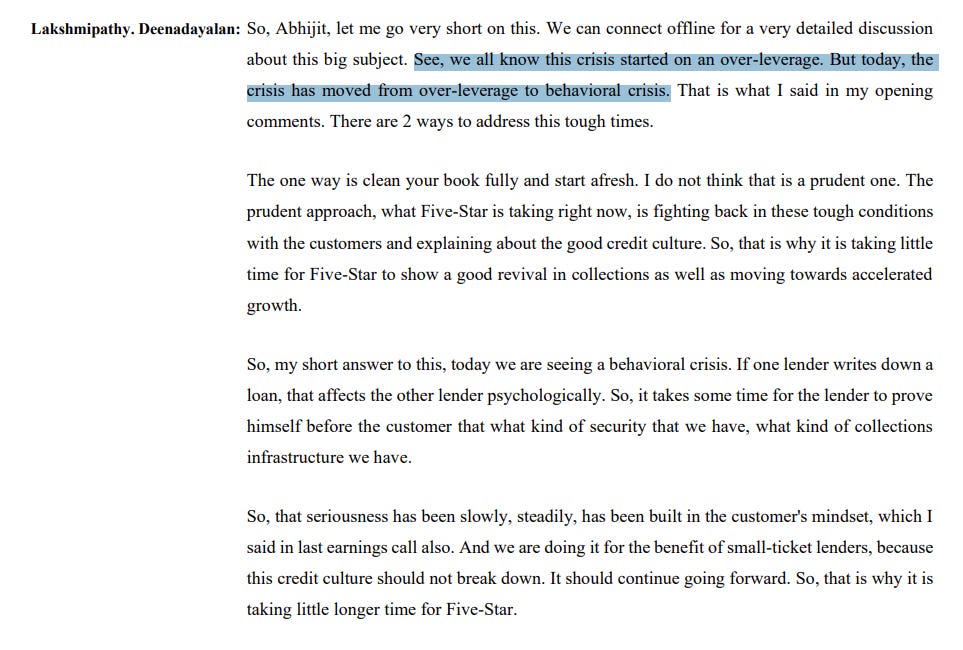

But there’s something dark plaguing the sector: a mindset shift. As Five-Star Business Finance and others have flagged, there’s a “behavioural crisis” afoot in unsecured micro-lending. Earlier, most defaults came from an inability to pay: like a crop failure, a medical shock, or a flood. The borrower wanted to repay; they simply couldn’t. We’re now seeing something different — an unwillingness to pay.

The seeds of this were planted in good times.

When microfinance was booming, too many lenders extended unsecured credit to the same borrowers. This allowed them to enter a ‘debt rollover cycle’ — where they borrowed from one to pay another. But then, regulators tightened rules, while lenders, too, simultaneously pulled back. This “rollover game” broke, causing mass defaults. And as people saw others default, the “social collateral” (or more simply, peer pressure) in group lending eroded. Others, too, felt like they had permission to stop paying. Meanwhile, politicians began talking of loan waivers, accelerating the decline.

This is why almost every MFI player is now diversifying into secured products: micro-LAP, gold loans, and individual lending. The group-lending model isn’t permanently broken, but repairing credit culture is slow work — and until that happens, lenders aren’t willing to sit through the repair cycle with an all-unsecured book.

Gold: the safety valve

As many other segments come under pressure, gold finance has become the sector’s pressure relief valve. The strategic appeal of gold in this environment is obvious. These loans frequently yield over 18%. The collateral, meanwhile, is liquid, mark-to-market, and sits in your vault. To an NBFC, this means near-zero provisioning requirements. That makes gold loans a dream product.

The industry’s gold AUM grew at staggering rates. But most of this growth is mechanical: as gold prices rise, the permissible loan amount per gram of collateral inflates as well, without the NBFCs requiring a single new customer.

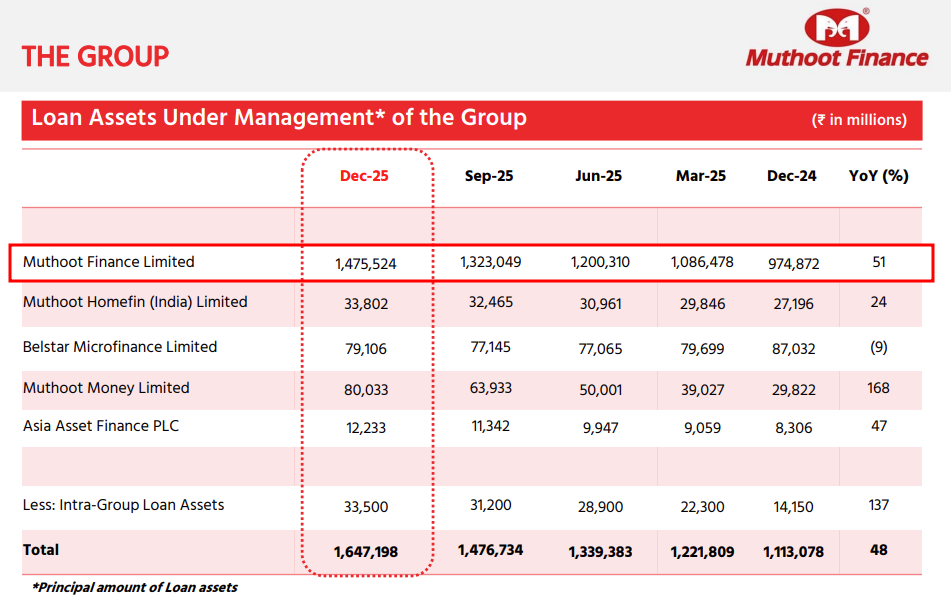

Muthoot’s core gold business, for instance, soared 50% YoY.

Manappuram, burned by its MFI subsidiary Asirvad posting a ₹156 crore loss, pivoted hard back to gold. And in a single quarter, their gold book grew 23%.

The rush to gold, however, carries its own risks. If gold prices correct sharply — say, 15% — the margin calls would cascade through the system. These companies will be forced to auction their collateral, just as the market is falling. And as with the rest of the industry, banks, attracted by the same safety and yields, are piling into gold lending too. This is compressing spreads for traditional NBFC gold lenders.

Meanwhile, these companies’ efforts at diversifying away from gold have largely failed. Manappuram’s vehicle finance GNPA, for instance, has ballooned to 13.7%. Its MFI arm, too, is in intensive care.

What to watch

Here’s the broad picture: gold loans are seeing incredible growth. But this growth may be hiding the fact that underlying credit demand across the economy is weaker than the headlines suggest. That is, gold is a crutch for loan growth. Microfinance, too, is showing early signs of a comeback, But the old staples — home loans and vehicle finance — are going through a rough patch, despite being such a big part of the sector’s identity.

This is not a sector moving in one direction. NBFCs are growing in very uneven ways, largely based on how much risk each management team is willing to take. And that difference in risk appetite is exactly why performance is splitting so sharply across companies.

Tidbits

IDFC First Bank repaid ₹583 crore in full to Haryana government departments after a fraud was discovered at its Chandigarh branch, where certain employees allegedly cleared forged payment instructions in collusion with external parties. We covered it in our earlier piece here.

Source: Economic TimesThe government has launched the second phase of its National Monetisation Pipeline, targeting ₹16.72 lakh crore over FY26–FY30 by leasing out operational public assets — roads, railways, ports — to private players, while retaining ownership and redeploying the proceeds into new infrastructure.

Source: BloombergThe government has launched Bharat Taxi, a cooperative ride-hailing platform where drivers pay ₹500 to become shareholders and earn a share of profits — with zero commissions charged.

Source: Reuters

- This edition of the newsletter was written by Krishna and Kashish.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

This video from The Quint (https://www.youtube.com/watch?v=JkNLUZa5INk) perfectly captures why Indian urban mobility is struggling: we are building isolated projects rather than an integrated ecosystem. To fix this, we must drastically increase bus fleets to support high-capacity Metro lines and transform stations into vibrant "Urban Hubs" filled with eateries and service businesses. Diversifying into non-fare revenue is the only way to keep tickets affordable for the masses while maintaining financial health. Most importantly, we need a "One City" approach where Metro authorities run their own dedicated feeder services and build seamless physical connections between different transit modes. Without solving the last-mile nightmare and unifying our transport systems, our cities will remain trapped in a cycle of congestion.

"Outside most stations, hitting that threshold is harder than it sounds. Autos that cluster at the exits often quote flat rates that make the last kilometre nearly as expensive as the metro ride itself. Feeder buses run so infrequently that waiting for one alone can push you past that 20-minute limit — and in many places, they barely exist. And even before you get to an auto or a bus, the footpaths outside most stations are broken, encroached upon, or simply don’t exist — making even the walk to the station exit harder than it should be."

This is so true. It is such big psychological hurdle.