What it takes to move a city

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

What it takes to move a city

How much wood would a woodchuck chuck if a woodchuck could chuck wood?

What it takes to move a city

At The Daily Brief, for some stories, we often feel like we never have enough time to do justice to them. Today’s story on the buildout of Indian metros is one of them.

Sometimes, even a week will be extremely short to cover a story like this. But the job has always been to cut through the noise, bring ourselves back to the piece, and try to explain things from the very basics. This means we ourselves have to spend a lot of time reading, going ahead, pulling back, going back to the basics again, and so on and so forth, until our explanation feels extremely intuitive.

This was a very ambitious topic for us, even though it may not seem like one. We hope to be doing another story on this as well. We apologize if we miss something in this one!

What we do know is this: with metros, India is in the middle of one of the largest urban infrastructure buildouts, and most people. And the scope and intricacies of these projects is mind-boggling, to say the least.

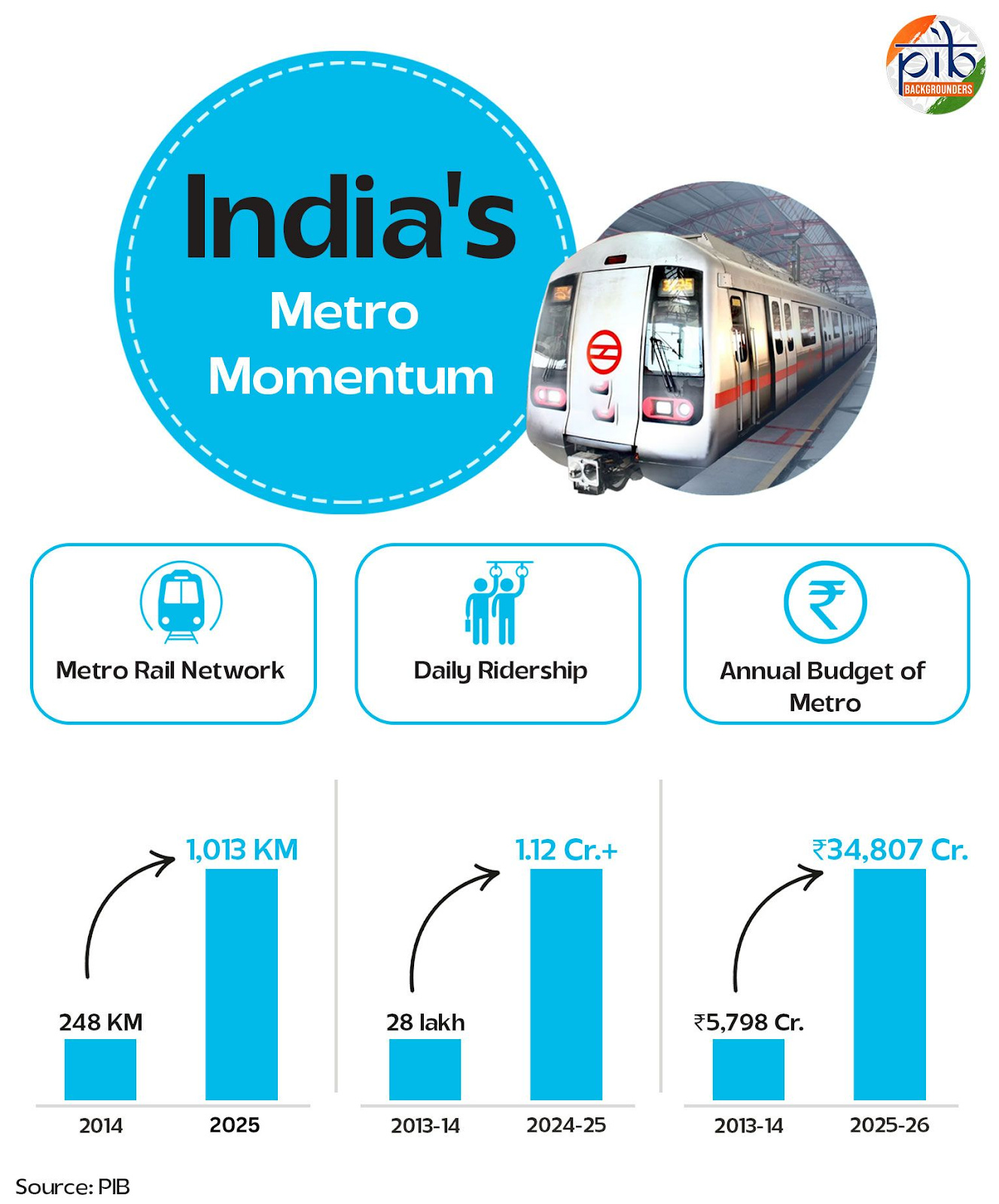

In 2014, India had 248 kilometers of operational metro rail across five cities. By May 2025, that number had crossed 1,013 kilometers across 23 cities. Another 900-odd kilometers are under construction. Entire city skylines have been reshaped. Hundreds of kilometers of tunnels have been bored through the earth under some of the densest neighborhoods in the country.

So, we thought, why not dive into how metros are built?

What makes metros necessary?

Let’s start from the very basics: why do we even need a metro train in the first place?

Think about what happens to a city as it grows. In its early years, a city is small enough that most people can get around reasonably well. The roads have capacity to spare. Buses move at decent speeds. The distance between where people live and where they work is manageable. Transport isn’t yet a huge chokepoint.

Then the city grows. More people move in, more businesses open, and more vehicles appear on the road. However, a road is a shared resource that gets consumed by the very traffic trying to use it. Beyond a certain threshold, every additional vehicle on the road makes the road slower for everyone already on it. A road at 80% capacity might move cars at 40 km per hour. But push it to 100%, and you get, well, Bengaluru-level traffic 🙂

In economic parlance, this puzzle is called the tragedy of the commons. Bengaluru’s population roughly tripled between 1991 and 2011. The roads, the buses, and the bridges were always playing catch-up, and they never quite caught up.

By the time you reach a city like Bengaluru today, average vehicle speeds on some corridors during peak hours have fallen below 10 kilometres per hour. To put that in perspective, a brisk walk is about 5 kilometres per hour. A 15-kilometre commute at that speed takes close to two hours each way. For the millions of people making that journey every day, that’s four hours lost to traffic without much productive work done.

The economic cost of this, of course, is enormous. A research team led by mobility expert MN Sreehari has calculated what those lost hours are worth by taking average wage rates and multiplying by the aggregate hours wasted across a city’s working population. The numbers run into thousands of crores annually for each major city. And that’s only the direct cost represented with the value of time lost. The indirect costs are harder to measure but arguably larger.

What’s more, after a point, adding more roads is hardly a useful solution. In a city as dense as, say, Delhi or Mumbai, there simply isn’t enough open land to build 30 lanes of road. The only way out is to move people through a medium entirely that doesn’t interact with road traffic, and that can carry far more people than any road ever could.

A metro would be a great solution to this problem. It moves people through a dedicated, non-road corridor, which is either at land or beneath it in a tunnel. A single metro line running at full capacity can move 60,000-80,000 people per hour in one direction. In high-demand corridors, the metro often becomes the most-scalable option.

But — and this is important — a metro isn’t the right answer everywhere. It makes economic sense only on corridors dense enough to fill those trains. The industry threshold is roughly 40,000 passengers per hour in one direction.

How a metro gets built and who actually pays

Every metro project in India is supposed to begin with a Comprehensive Mobility Plan. This is a city-wide transport strategy that analyses current and future demand over a 30-year horizon. Simply, it asks whether a full metro is the most efficient solution for this particular city.

This process is governed from the Centre by the Ministry of Housing and Urban Affairs (MoHUA). If a city wants central government money for its metro, it has to satisfy MoHUA’s requirements first. The Ministry won’t release funds unless the city can demonstrate it has done this planning seriously.

In practice, though, the planning often follows the decision rather than preceding it.

See, building metros also carries a lot of political weight. A metro is one of the most powerful, visible signals of the idea that a city has arrived. However, in the excitement of making this known to the world, cities might build metros even when the demand isn’t sufficient. Here, the formal planning process used to justify a decision already made on other grounds.

Now, once a metro project is sanctioned, the entity that builds and runs it is a Special Purpose Vehicle, or SPV — a corporate entity created specifically for that city’s metro. The SPV for the Delhi Metro is DMRC, Bengaluru has BMRCL, Chennai CMRL, and so on. Each SPV is a joint venture between the Government of India and the relevant state government, typically 50-50. This structure gives these entities the flexibility to sign contracts and move at a pace that pure government bureaucracy wouldn’t allow.

The money to build comes from several sources layered together. As shareholders, the central and state governments put in capital, which is essentially a subsidy they don’t expect to recover as a financial return. But the single largest piece of funding for many Indian metro projects comes from multilateral development finance institutions. These include JICA from Japan, the Asian Development Bank (ADB), and so on. These development banks lend the money at extremely low rates than a commercial bank would — that too with a grace period.

These financial innovations are in service of handling the enormous cost of building a metro. And interestingly, the most important variable in metro economics is whether the line runs on the city surface, or underground beneath it.

An elevated metro — the kind you see running on concrete pillars above a road — costs roughly ₹200 crore per kilometre to build.

An underground metro, though, is way more expensive, costing anywhere between ₹400-₹600 crore per kilometre — even more in complex urban environments. Tunnelling through the earth beneath a dense city involves not just building foundations, but also working around water mains, sewage lines and historical structures without disrupting them. For instance, Line 3 of the Mumbai Metro crossed ₹600 crore per kilometre by the time it opened.

And now, the economics

With such massive costs, and the fact that metros are mostly run publicly, it’s probably no wonder that no metro in India makes money in a commercial sense.

Take Delhi Metro, the most-developed system in India. It is able to cover its day-to-day operating costs and even generates some operational surplus. But it still depends on concessional debt and government equity to exist. Most others require ongoing state government subsidy just to keep the trains running.

Much like the Indian Railways, metro ticket prices are a public policy decision, not a business one. If fares rise too high, lower-income commuters, who arguably need the metro most, are priced out. Political pressure keeps fares below the level that would allow full cost recovery. The Metro Railways Act even requires a formal Fare Fixation Committee to govern any change in fares.

So how does one fill the gap? That’s where non-fare sources come in. These include advertising, retail stores at stations, property development nearby, and leasing optical fibre routed through metro tunnels.

The question isn’t whether metros need public money — they do, indefinitely. Nobody expects a national highway subsidized permanently by the state to repay its construction cost from tolls, either. But does the benefit to the city justify the cost? In a city like Delhi, the answer is clearly yes. But, for a metro in a smaller city running at 30% capacity, the calculation is far less comfortable.

This is the tension that governs metro expansion in many tier-1 cities. The need for a metro fundamentally depends on the long-term growth of the city. But, with the pressure to build metros as symbols of development, rather than as solutions to specific mobility problems, success will hardly be consistent.

Conclusion

This piece has covered the basics — why metros exist, how they’re financed, and whether the economics make sense. But we’ve barely touched the surface of what makes this such a rich topic.

We haven’t talked about the tunnel boring machines that grind through the earth 30 metres below heritage buildings. Nor have we talked about how the metro coaches are built, and who builds them. Nor have we discussed what it actually takes to commission a metro line safely before a single passenger boards.

We haven’t even talked about the last-mile connectivity problem. The reason many metro systems underperform their projections isn’t the metro itself. Without bus networks and walkable streets that bring people to the station in the first place, a metro would hardly succeed.

And there is an entire rabbit hole about the politics of alignment — which neighbourhoods get stations, which don’t, and what that means for property values and for who the metro actually serves.

Each of those is a story in itself. We’ll come back to this in a future episode, soon!

How much wood would a woodchuck chuck if a woodchuck could chuck wood?

In one of our team meetings, we came across a piece of news on IKEA’s India expansion plans. We joked that we knew almost nothing about the sofa we sat on. So, we began asking questions.

Our rabbit hole started with the most fundamental building block of the industry: wood panels. This usually means plywood and chipboards which make up your wardrobe, your desks, and other furniture. But the wood panel industry also includes laminates, which, while not made of wood, is just as important.

So this is our attempt at a primer on the industry, which we found incredibly intricate. This means that we were unable to cover everything in a single episode. What we do miss, we hope to cover in another edition.

Building blocks

What are wood panels, even?

When you look at a kitchen cabinet, a wardrobe, or a TV unit, you’re not just looking at wood. Any piece of furniture needs a structural skeleton — which gives it strength and shape — and a decorative surface for color and texture.

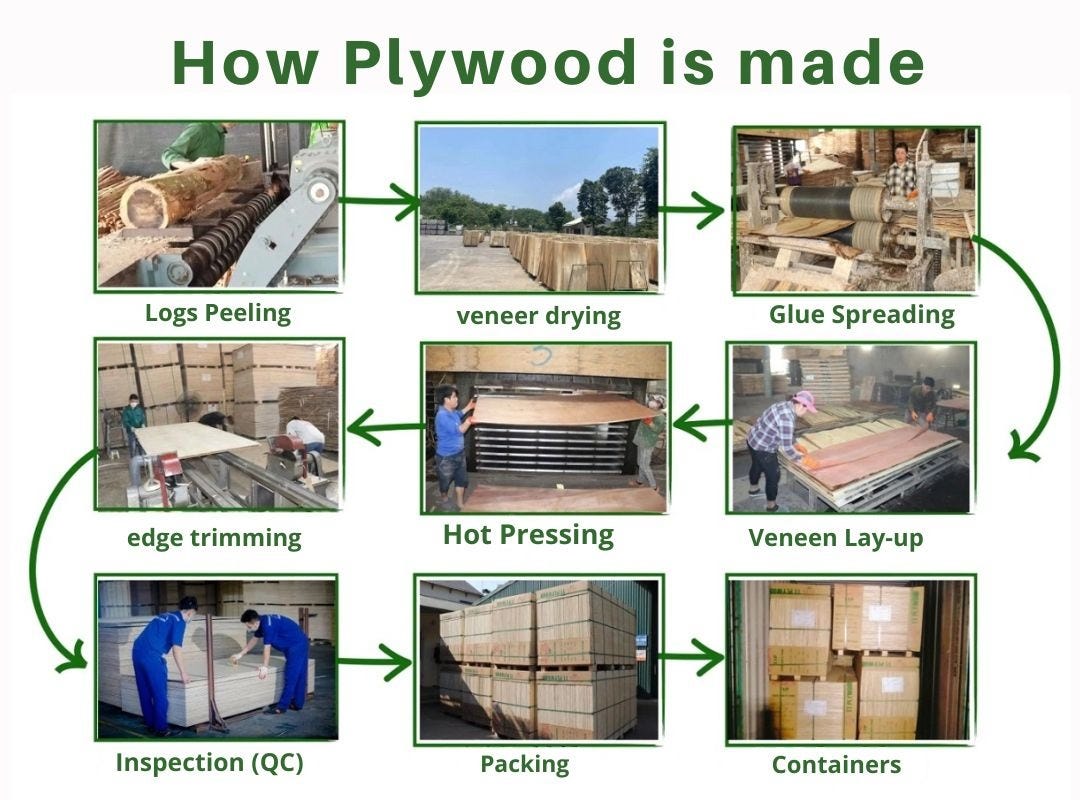

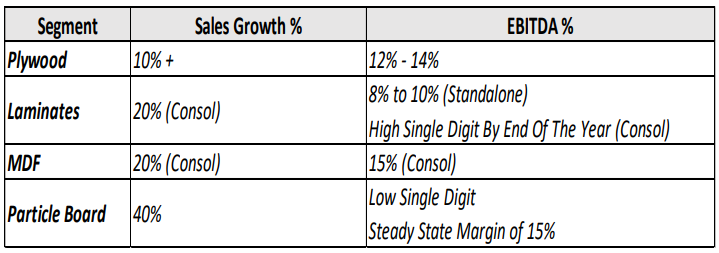

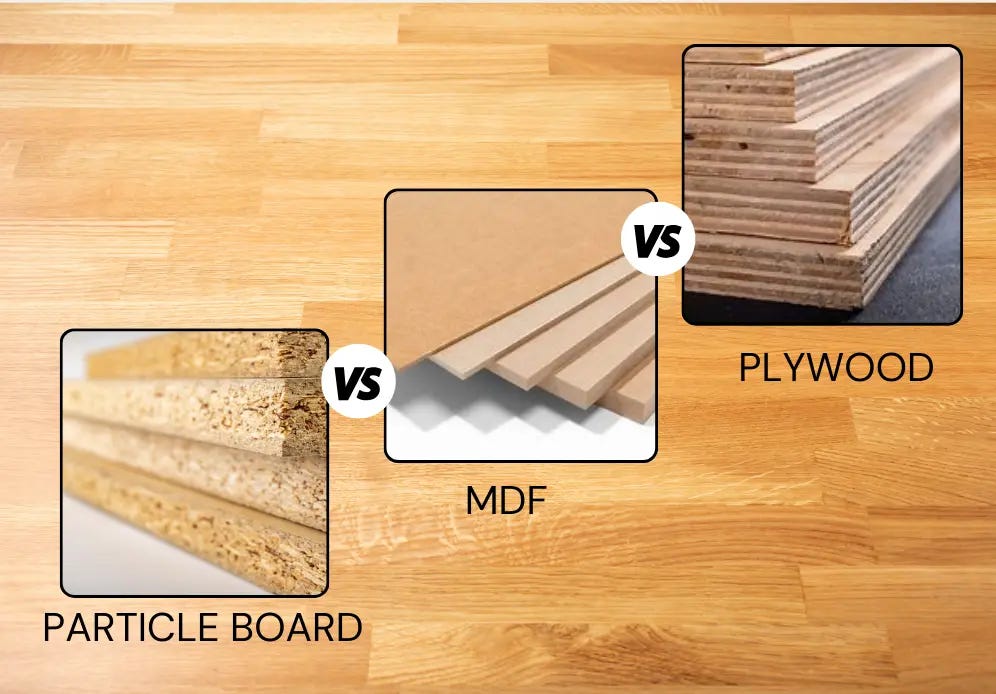

As for the skeletal core, there are three main materials, of which plywood is the oldest, most familiar. It’s the bread-and-butter of India’s top public wood panel makers, like Greenply and Century Plyboards. Here, growth is more stable and predictable, if not fast.

It’s made by peeling logs of wood into thin sheets, layering them and bonding them with resin, and pressing them under heat. This structure gives plywood its strength, making it ideal for your beds, flooring, or anything that needs to bear heavy loads.

Plywood isn’t just one product, either. It varies by the quality of wood used. There are segmentations based on function, too. Marine-grade plywood, for instance, is used in bathrooms and sink units for their extreme resistance to moisture.

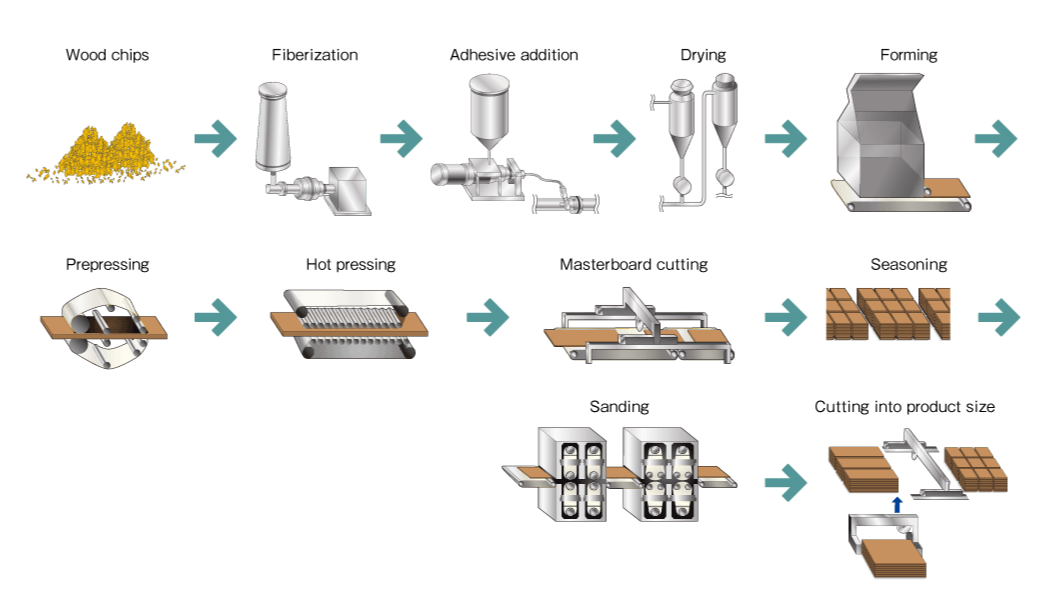

But plywood doesn’t work everywhere. That’s where MDF, or medium-density fibreboard, comes in. Relative to plywood, MDF is a more emerging, rapidly-growing product. Here, wood is broken down not into sheets but into fine fibres. These are then mixed with resin and pressed into a dense, smooth, uniform board.

Because of that uniformity, MDF is excellent for machining. You can carve and mold it into intricate profiles without the wood chipping or breaking out. Plywood, in contrast, is more uneven, with hidden knots and voids, and lacks polish. MDF is the material of choice for factory-made furniture.

But MDF lacks the strength and moisture-resistance of plywood. MDF works for wardrobe shutters and TV panels, which often look and feel polished. But the load of a kitchen wardrobe is best borne by plywood.

The last core material is the chipboard (or particle board), which is made from wood shavings, and sawdust pressed together with glue. Chipboards are flatter and more uniform than plywood, which, like MDF, makes them ideal for automated cutting in large factories. But it’s less dense than MDF and more sensitive to moisture. You cannot carve it the way you can MDF.

However, chipboards are the cheapest of all three. For simple tasks that don’t require heavy weight-lifting or handling water, it works just fine. Much like MDF, chipboards are a fairly new segment where companies expect aggressive growth.

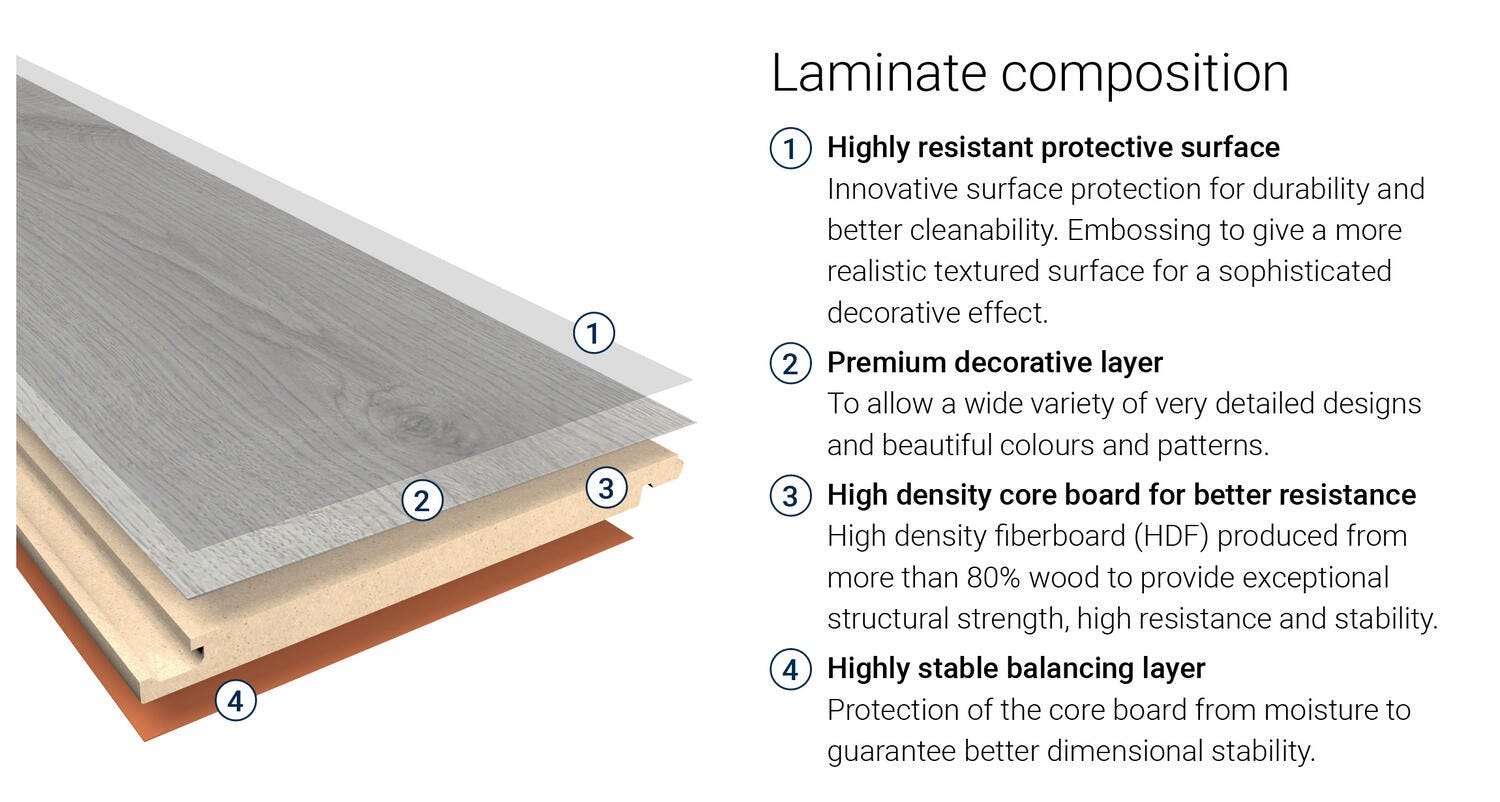

Moving from the skeletal core, we have the decorative laminates. In and of itself, a laminate doesn’t have an ounce of wood. They’re made out of wood pulp or paper, and resin. Their entire purpose is to provide a sheen to furniture that’s ideally resistant to scratches and wear-and-tear. If your furniture is extremely pleasing to look at, the laminate is doing its job.

Who buys this?

Now, who buys these products?

The biggest buyer segment is on-site carpentry, where homeowners hire carpenters to build custom furniture inside the home. Indian homes demand customization while being conscious of the budget. So, they hire a carpenter who does everything from choosing the core and skin to building the sofa or table. This is a very artisanal part of the business, and hardly follows a factory model. The carpenter typically has deep relationships with a few local dealers, built on years of trust and informal credit.

Historically, on-site carpentry has made up over 70% of India’s wood panel market. That, in turn, has meant that wood panels are mostly an unorganized industry in India. Listed players like Greenply and Century effectively compete within just 30% of the whole market.

In contrast, branded furniture manufacturers are the buyers who, unlike singular carpenters, have industrialized furniture. They have off-site factories that mass-produce readymade modular kitchens, wardrobes, and so on. These buyers care about consistency, scale. That’s why they prefer MDF and chipboards over plywood, since machining on them is far easier.

At the moment, this is a small part of the market, but that’s changing — we’ll come back to this later.

Finally, there are institutional and project buyers. Think commercial offices, IT parks, and real estate companies. This segment is specification-driven: architects and interior designers dictate the brand, and payments follow project milestones.

Since wood panels are primarily driven by carpenters’ relationships with local dealers, the distribution of wood panels is incredibly granular and wide.

See, plywood and laminates are sold through vast networks of dealers and retailers. Greenlam, for instance, has around 40,000 trade partners, while Century has relationships with over 3,000 dealers and stockists. These intermediaries hold inventory, extend credit to carpenters and contractors, and essentially act as working-capital buffers for the entire value chain.

This makes the industry exquisitely sensitive to inventory and liquidity management. When dealers face cash crunches, they stock less and pay slower, choking sales even if end-consumer demand exists. In fact, in Q1 FY26, Greenply’s gross debt ballooned to ₹5.4 billion partly due to collection delays and resulting inventory buildup.

For institutional projects and off-site furniture OEMs, though, the moat is relationship-based. Specification teams pitch to architects years before the first order is placed. And furniture OEMs order raw material in bulk.

Edges and margins

Not all wood panels are created equal — and not all margins are either. Yet, there is one critical cost driver common to all that can make or break margins: the cost of timber, the most important input of all wood panels.

Raw material is the biggest line item in the wood panel cost structure. And removing laminates, timber is the biggest chunk of those costs. Our domestic companies don’t have a lot of control over this cost because we import much of it.

For instance, premium Indian plywood relies heavily on imported timber from countries like Gabon, Malaysia, and Myanmar, because our domestic timber doesn’t meet the right quality benchmarks. This exposes plywood-makers to currency fluctuations and global supply chain risks.

Now, what about the margins of each product type? The way each product earns its margins is reflective of where the competitive moat for each product might lie.

Laminates are an interesting paradox. They earn some of the highest gross margins in the industry — Greenlam alone makes over 50%. But their EBITDA margins settle far more modestly at 13-16%. Century, in contrast, guides for even lower 8-10% margins!

The gap between EBITDA and gross margins reflects the cost of selling. See, laminates are a fashion product within building materials. And, as with any fashion product, you need a lot of variety: in color, in whether they’re matte, gloss, or plain, and so on. Greenlam alone offers over 10,000 laminate designs. You can’t sell such a huge variety through a catalogue alone, because customers need to physically see and feel the texture.

That’s where distribution — warehouses, retail relationships, sales — makes all the difference. A good network isn’t just essential to manage the complexity of so many SKUs. It also ensures that, at the front-end, every customer feels handheld and well-informed while making a choice.

MDF usually commands EBITDA margins in the high teens. The reason is operating leverage: MDF manufacturing is a highly automated, factory process. That involves incurring huge fixed costs worth ₹600-800 crore for one plant. However, with more scale, every additional unit produced contributes disproportionately to profit, with EBITDA margins going as high as 25%. The huge capex also keeps out unorganized players.

However, this is cyclical — if demand is low, then all those fixed costs become a burden instead of an advantage. The margins also remain compressed during the period capex is being undertaken.

Chipboards work similarly, too. With a healthy utilization of factory capacity, EBITDA margins can shoot up above 20%. There’s also a natural logistics moat — chipboard is bulky and cheap, so transporting it over long distances destroys economics. A plant in South India has a distinct regional advantage that imports or distant competitors can’t easily erode.

Plywood generally has the lowest margins of the core wood panel products. It is relatively more labour-intensive, involving manual peeling of veneers. Additionally, organized players are squeezed by competition from the unorganised sector, making them more commoditized than MDF and chipboards which require lots of capex. This caps EBITDA margins at 12-14% for even the most efficient players.

Plywood’s moat, then, is brand trust — the biggest signal of quality assurance. Brands like Century’s “Club Prime“ command a premium built on warranty and peace of mind.

The best, most profitable players are able to use their network to cross-sell products. Greenlam’s “matching programme“, for instance, supplies furniture manufacturers with chipboards, laminates, and edge bands that all match perfectly in design. This locks in a customer across multiple product categories.

Two big shifts

Within what we know about the industry so far, two huge shifts are changing the industry’s character.

The first, most important one is the shift from informal to formal. With quality-engineered MDF and chipboards becoming domestically available at scale, factory-made furniture is gaining ground. The boom in commercial real estate demands standardised, high-volume furniture that only factory setups can efficiently produce. Plus, with rising incomes, customers are more willing to pay a premium for the brand name.

But besides industrialization, government regulation is also accelerating this shift with quality control orders (QCOs) and BIS norms. In The Daily Brief, we’ve covered before how QCOs are used to restrict imports. They mandate BIS certification for certain products to ensure they meet a minimum quality benchmark. This, in turn, imposes compliance costs. For branded players, these costs are but a drop in the bucket, but unbranded workshops struggle.

The result is a shift slowly occurring across levels: retail to B2B, carpenter to OEM, plywood to chipboard and MDF.

The second is the push to localise supply chains to reduce import dependence.

To do so, wood panel companies have to invest in planting trees. Greenlam, for instance, undertook sapling distribution drives near its plants in South India, so that over time, the raw material for their chipboards will be secured. Meanwhile, Greenply expects 100% of their raw material for their Baroda MDF plant to be sourced locally. The industry also expects the government’s QCOs to provide further impetus to local supply chains.

However, premium plywood in particular remains in a state of inertia. There, timber imports don’t seem to go down the same way they are for MDFs and chipboards.

Conclusion

The Indian wood panel industry sits at an interesting inflection point. It’s in an upcycle that’s driven by both consumer, commercial and infrastructure demand, along with a shift towards formalization and premiumization. Distribution, it seems, is a big advantage here.

This primer hardly covers the surface — or should we say bark — of things. For instance, what kinds of trees are grown for each product? Or, how have exports fared? We didn’t even get into how the top players differ from each other: Greenlam, for instance, only entered the plywood game just recently, unlike its peers who have roamed there for decades. Most importantly, we’ve barely touched furniture itself!

We don’t know about you, but we’re probably not looking at our office desks the same way again :)

Tidbits

Ashok Leyland to expand LCV network in Western India

Ashok Leyland plans to add 30 new touchpoints in Western India, including Maharashtra, to tap rising demand for light commercial vehicles. The move will improve service reach from every 35 km to every 25 km in the region. The company is betting on infrastructure growth and stronger after-sales support to gain market share.

Source: The Hindu BusinessLineIndian cardamom exports surge on global supply crunch

Indian cardamom exports are set to nearly double to 14,000 tonnes this season after a 50% crop drop in Guatemala created a supply gap. Strong demand from West Asia and Iran has kept prices firm at around ₹2,450 per kg. Exporters call this a “golden window” as India regains global market share.

Source: The Hindu BusinessLineReservoir storage drops below 75% across India

Water levels in India’s 166 major reservoirs have fallen to 61.65% of capacity amid deficient rainfall. All five regions now report storage below 75%, with central India facing the steepest rainfall shortfall. While levels remain above last year’s, the country heads into summer with tightening water reserves.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Krishna and Manie.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

For the metro part, I do agree that the ticket pricing is highly political and the charges cannot be high in order not to push out the very people the system is built for, but I want you to cover the part that how government as an entity can recover costs of an infrastructure project indirectly also, like from political rallies to actual operation of a metro tons of people are employed tons of 'goods and services' are employed and after every expenditure on an infrastructure government earns gst, income tax, and productivity in an economy, so how does these factors come into play, and one more thing i want you to cover is the story of how China used to built high-speed and local mobility infrastructure in middle of nowhere to ultimately have a system automatically/engineered around it, can such thing work in India? And ultimately I love the work you do it's amazing, please keep it up