Indian pharma: lofty aims in the midst of chaos

Expansion, evolution, diversification, and a weight-loss wave.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Indian pharma has lofty aims in the midst of chaos

India’s credit card industry is splitting in two

Indian pharma has lofty aims in the midst of chaos

Indian pharma is going through a period of rapid change.

Yes, US tariffs and geopolitical uncertainty are forcing companies to rethink their geographical mix. But relievingly, the Indian market itself has become the fastest-growing engine for most players. Indian firms are also ferociously working on expanding to other developing markets,

Meanwhile, Indian pharma is in the midst of a generational shift toward chronic therapies — like cardiac, respiratory, diabetes and oncology. One chronic solution in particular, GLP-1, promises to be a gold rush. And two of the biggest acquisitions in the sector’s history landed within six weeks of each other.

Clearly, there’s a lot to unpack this quarter.

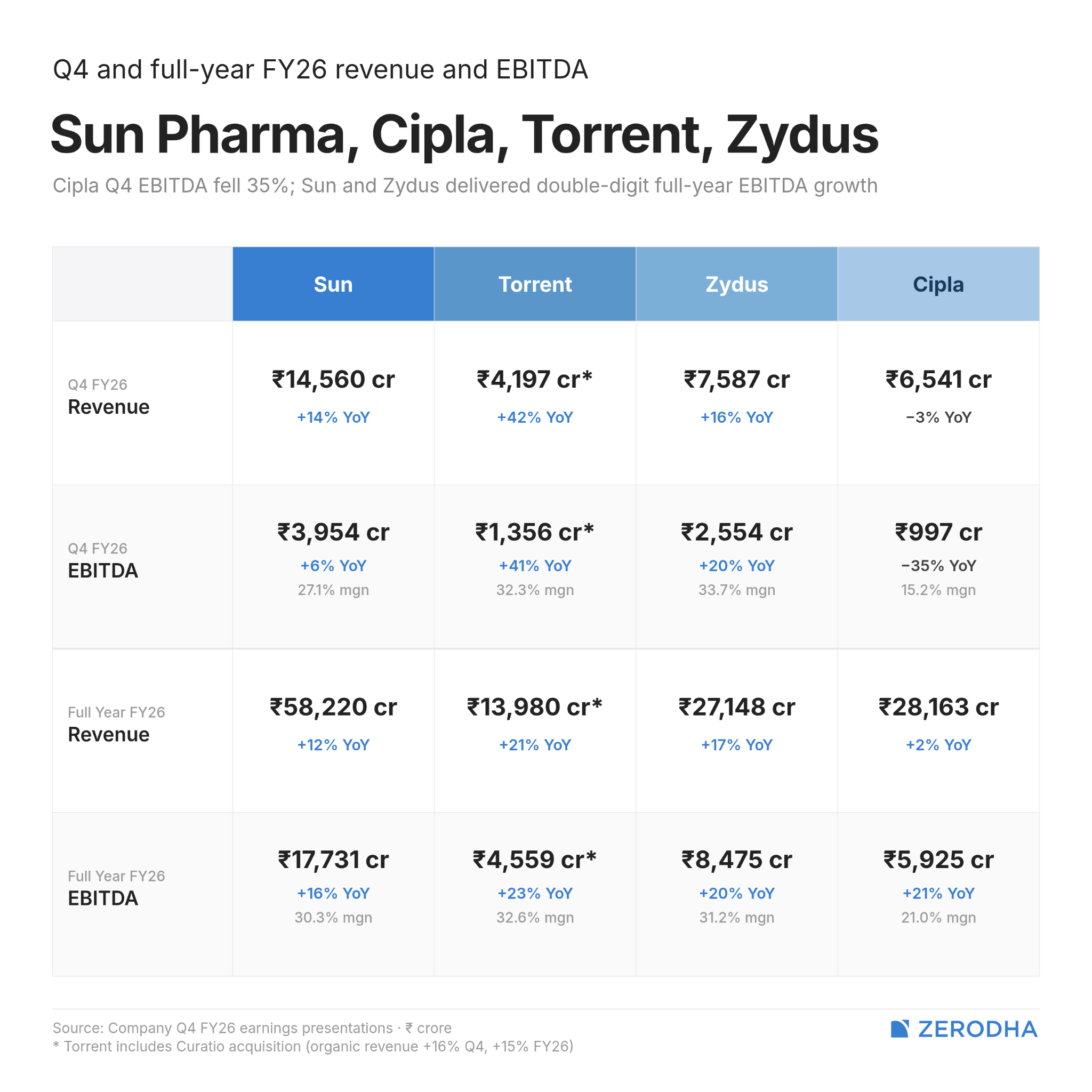

We looked at the Q4 FY26 earnings calls of four of India’s largest pharma companies — Sun Pharma, Torrent Pharmaceuticals, Zydus Lifesciences, and Cipla. All of these companies have points of agreements and divergence on what they think Indian pharma will look like over the next decade.

The numbers matter, of course. Sun Pharma reported ₹14,560 crore in Q4 revenue, up about 14%. Torrent’s Q4 revenue hit ₹4,197 crore, up 42% — though that’s inflated by its JB Pharma acquisition; the base business grew 16%. Zydus came in at nearly ₹7,600 crore, up 16%. And then there’s Cipla, the only one with negative y-o-y revenue growth in Q4.

But, of course, the numbers are secondary to the structural forces driving them. Let’s get into them.

Repeat business

For decades, Indian pharma companies made money selling acute medicines, like cough-and-cold medicines, antibiotics, and painkillers. These are the kinds of drugs you take for a week and stop. These are high-volume, low-stickiness products where brand loyalty is weak and price competition is fierce.

For the last few years, the entire sector has been undertaking a hard pivot towards chronic therapies. That refers to medicines for conditions like diabetes, heart disease, depression, and cancer that patients recurringly, even for years.

That also makes their economics very different. Chronic patients are repeat customers. Doctors prescribe these meds based on long-term efficacy and not just price. And once a patient stabilises on a particular medication, switching is rare.

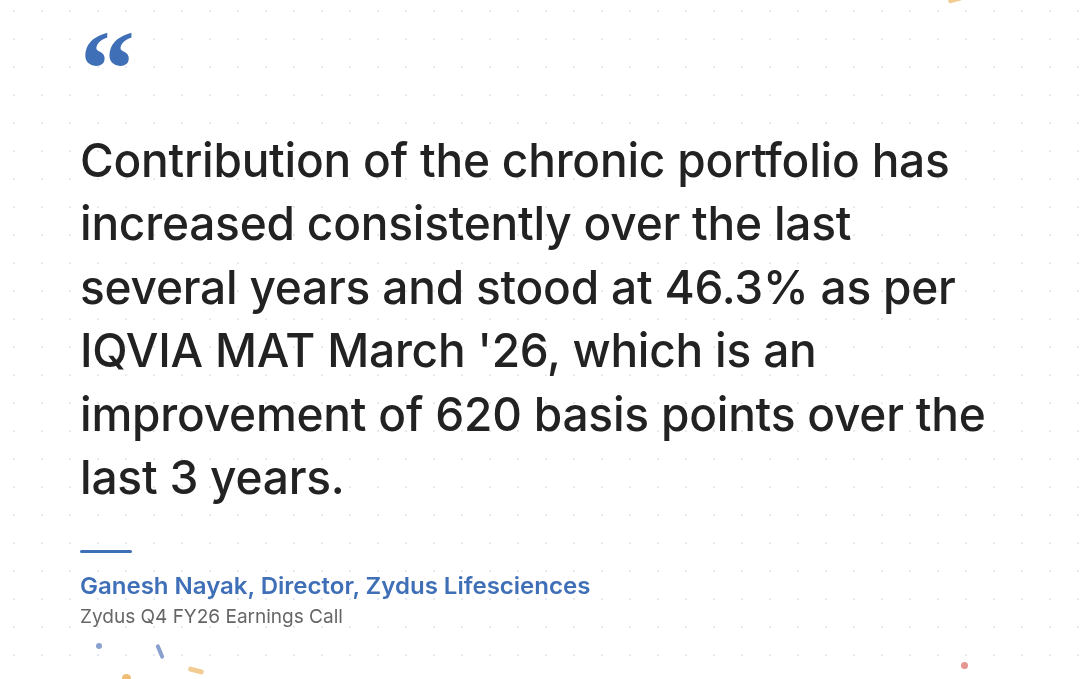

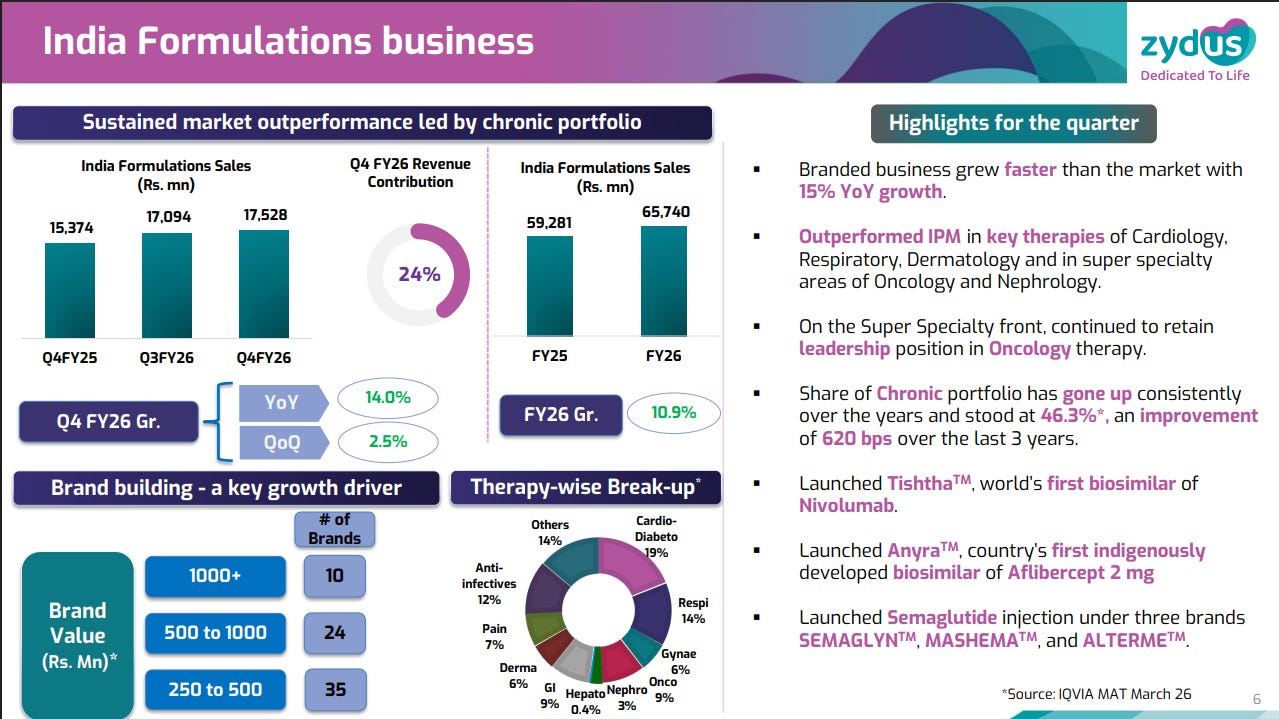

And that shows up in the numbers. Zydus, for instance, has pushed its chronic mix from 38% to 46% in just three years. For both Sun Pharma and Torrent, meanwhile, chronic medicines make up over 70% of their portfolios.

How have all four companies anchored themselves to the chronic shift? There are some commonalities in their strategies, cardiac and diabetes being key among them.

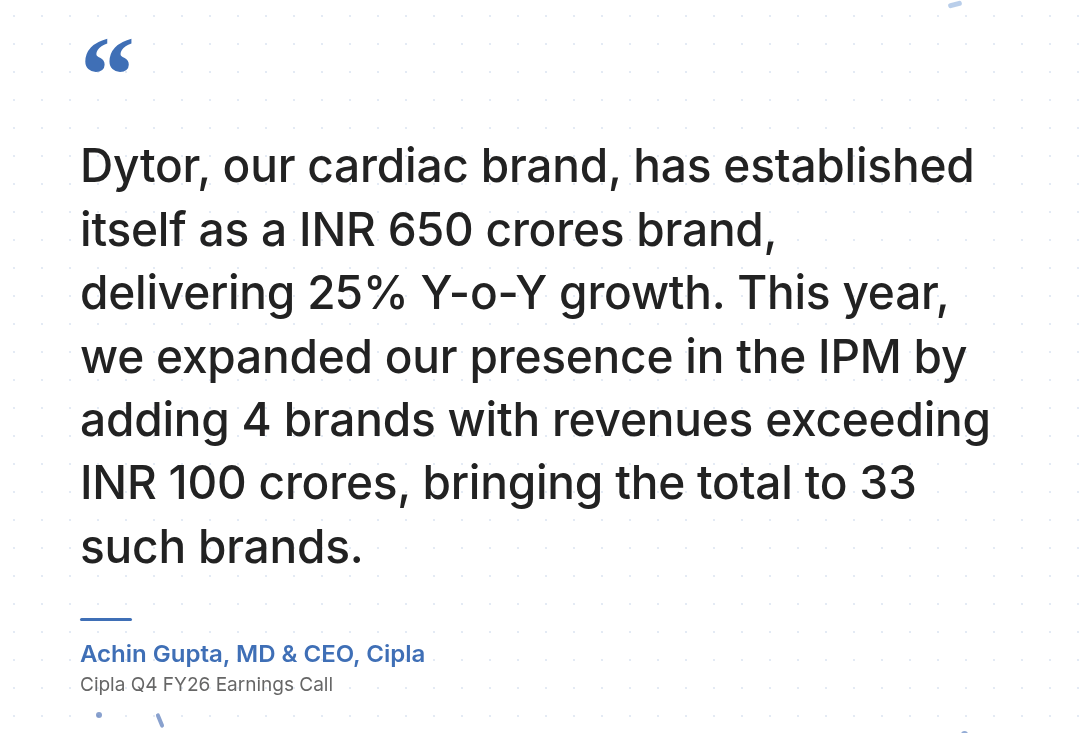

For instance, Torrent has built a fortress in cardiac and gastroenterology. Before their recent acquisition of JB Pharma, those two segments alone made up half its India revenue. Similarly, Sun Pharma consistently ranks #1 in prescription share among Indian cardiologists. Cipla has a cardiac brand called Dytor, which is one of its fastest-growing products at 25% y-o-y.

Similarly, given India’s tryst with diabetes, all major pharma firms have a strong diabetes portfolio. Cardio-Diabeto is Zydus’ largest combined therapy segment, making up 19% of their India business. Cipla’s anti-diabetes segment has seen a 16% annual growth rate over the last few years, and also launched India’s first inhaled rapid-acting insulin product last quarter. For both Torrent and Sun, anti-diabetes products make up around 8% of their India business.

But beyond these similarities, the bets mostly diverge.

For instance, Zydus is the largest oncology player in India. In a previous Daily Brief story, we covered the push from Indian pharma to treat cancer, and Zydus was a key anchor of this story. Earlier this year, it announced India’s first biosimilar of the breast cancer drug Trastuzumab Emtansine.

Sun Pharma, meanwhile, also has a broad portfolio of medicines dedicated to skin cancer, like Unloxcyt, Odomzo and Nidlegy. Sun Pharma is also the market leader of neuro-psychiatry medicines in India — none of its three peers have significant presence here. Neuro-psychiatry usually includes medicines targeted at depressions, strokes, and nervous disorders like dementia and Alzheimer’s.

Elsewhere, Cipla is a leader in respiratory products. Its flagship inhaler Foracort crossed ₹1,000 crore in annual sales this quarter.

The GLP-1 race

One very new chronic solution that has grabbed everyone’s attention is GLP-1.

Not too long ago, the dam of Novo Nordisk’s patent on semaglutide, one of the key molecules that trigger the GLP-1 receptor, broke through. This has launched a brutal competition among India’s pharma firms to build the next big weight-loss drug.

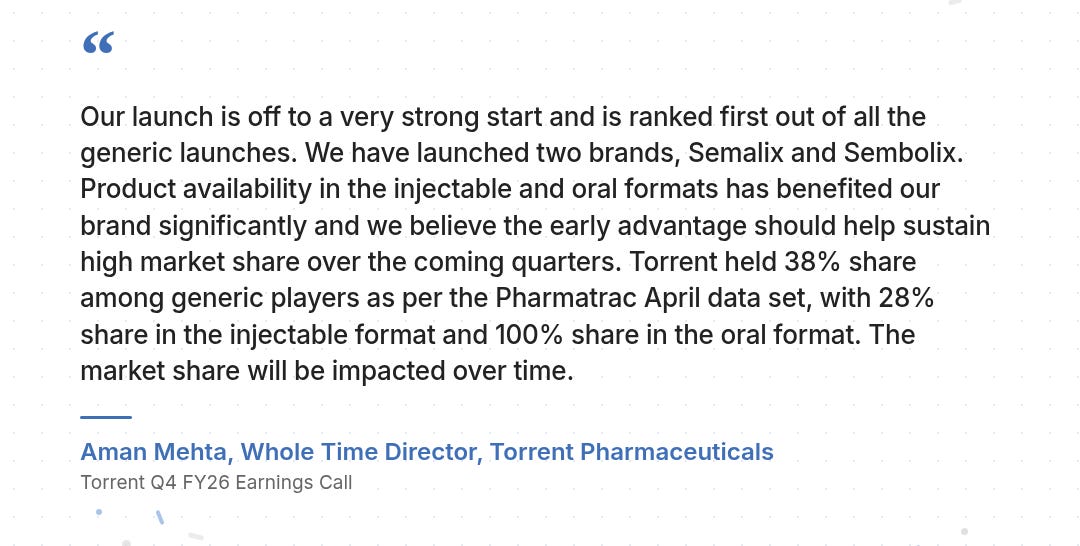

Torrent moved first and fastest. It launched two generic semaglutide brands — Semalix and Sembolix — in both injectable and oral formats, priced at roughly ₹4,000 a month. Within six weeks, it had captured 38% market share among generic players, ranking first in the category. Torrent’s management credited early product availability in both formats and aggressive pricing as the key advantages. Semaglutide will play a significant role in their chronic mix for years to come.

Zydus wasn’t far behind, being only second in market share. It launched three semaglutide brands with a twist: each uses a reusable, multi-dose pen device that lets patients scale up their dosage without switching devices. Zydus also took a different commercial approach by actually licensing its product to both Lupin and Torrent for co-marketing. Interestingly, unlike many of its peers, Zydus has also chosen to make the semaglutide API in-house.

Sun Pharma’s brands Noveltreat and Sematrinity hit the market right at patent expiry. But despite being India’s largest pharma company by revenue, Sun didn’t feature in the early market share data the way Torrent and Zydus did. The Q4 earnings call was dominated by their acquisition of Organon, not GLP-1 execution.

However, unlike its peers, Sun is also investing in its own proprietary GLP-1 drug, GL0034, as well as another GLP-1 molecule called utreglutide. With this move, Sun wants to move to an original formulation rather than rely on generics only to capture more of the value.

Cipla, meanwhile, treats GLP-1 as a whole therapeutic category, of which semaglutide is just one part. On that note, it partnered with Eli Lilly to distribute Yurpeak — which is based on the tirzepatide molecule that Eli Lilly still has a patent on. Cipla’s margins on the product depend entirely on the terms Eli Lilly sets.

Dealmaking and war chests

If FY26 had a defining theme beyond chronic and GLP-1, it was acquisitions. Two transformative deals landed within three months of each other, and they tell you everything about where the sector thinks growth will come from.

First, you have Sun Pharma’s ~$12 billion acquisition of Organon in April 2026 — is the biggest deal in Indian pharma history. As mentioned earlier, their entire Q4 earnings call addressed little besides what this acquisition means for them. And it means a lot.

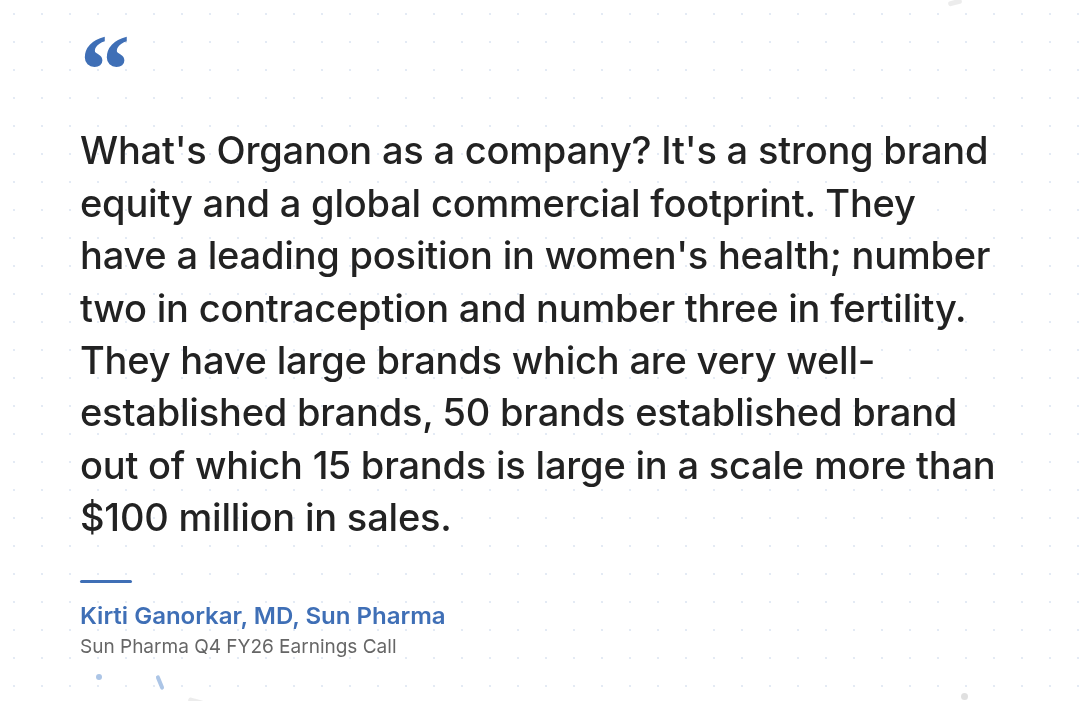

Organon ranks top 3 globally when it comes to contraceptives and fertility solutions for women. It gives Sun a massive leg up in women’s health, where they’ve historically had little presence before. Organon also has a strong biosimilar business, which has grown very fast over the last 5 years.

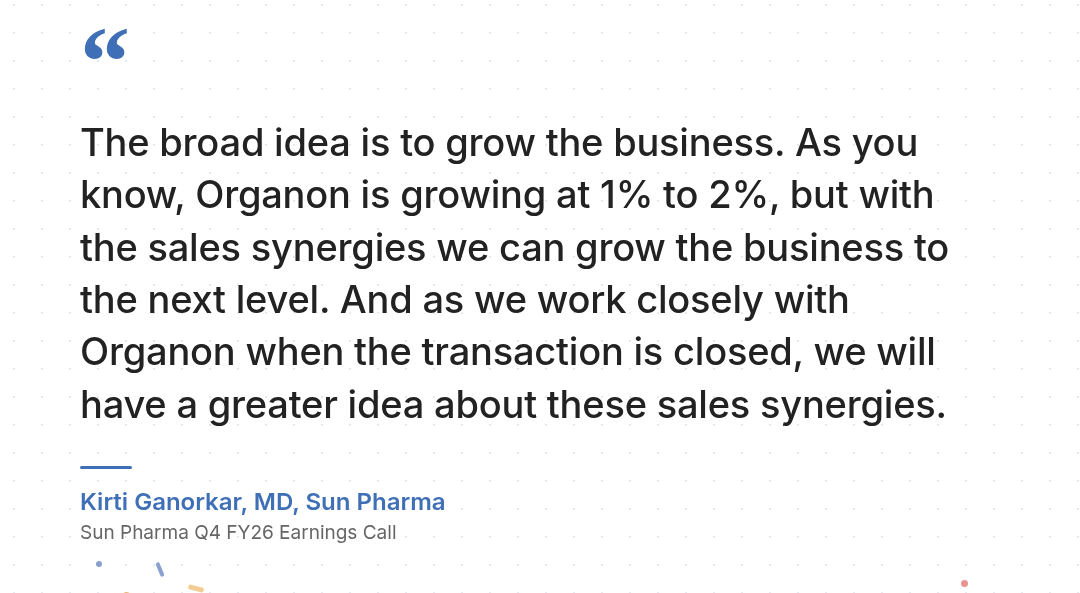

But these synergies are still unproven. The risk of the acquisition potentially not working out is just as real. Sun has a net cash position of $3.1 billion (~₹29,000 crore at current rates) — an already massive war chest. But the debt required to finance this deal will be a significant cash drain. And worryingly, Organon itself has been growing at just 1-2% per year.

Secondly, there is Torrent’s acquisition of JB Pharma, a ₹12,500 crore deal that closed in January 2026. It also poses similar risks as the Sun-Organon deal. The first quarter of consolidation already showed up in the numbers as a 42% y-o-y jump in the Q4 revenue. But Torrent’s leverage has spiked to 2.3x net debt-to-EBITDA. Undoubtedly, cash flow management will be of the utmost importance when it comes to paying off the debt raised for this acquisition.

Then there’s Cipla, sitting on the other side of the table. It ended FY26 with nearly ₹11,000 crore in net cash, yet no transformative deal to show for it. Cipla did make some small deals, like acquiring Inzpera Healthcare for paediatrics, or licensing established Pfizer brands like Corex and Dolonex. But these are bolt-ons rather than game-changers.

When pressed by an analyst about what this cash pile will be used for, management was incredibly conservative, saying that they’re choosing to be selective about which opportunities to pick. As peers consolidate and deploy capital, Cipla’s cash increasingly looks like an option premium it’s choosing not to exercise.

Zydus has shown similar levels of caution. Earlier in the year, they explicitly said that ideally, they would not want their net-debt-to-EBITDA ratio to cross 2x with an acquisition. Between Q3 and Q4, due to some acquisitions and a share buyback, their net debt went up from 3,000 crore to 7,000 crore. But this still kept their ratio under 1x.

The geography shift

There’s an old mental model of Indian pharma: develop drugs cheaply at home, export them to the US and Europe, earn in dollars. That model isn’t wrong, but it’s becoming incomplete.

The domestic Indian market is now, for most of these companies, the fastest-growing segment. India isn’t just a manufacturing base anymore. With 100 million diabetics, an ageing population, and rising chronic disease prevalence, it’s becoming the demand story too. Sun Pharma’s India business grew 14% in FY26, Zydus has consistently delivered double-digit India growth, and Cipla managed between 7-10% across the year.

That’s not to say exports don’t matter. They do, but the global footprint isn’t just limited to the US and Europe anymore.

For instance, Torrent is growing remarkably fast in Brazil, where its revenues showed healthy double-digit growth on the back of new launches in cardiac and CNS therapies. Brazil’s branded generics market operates on similar dynamics to India’s — physician-driven prescriptions, brand loyalty, chronic therapy dominance — and Torrent’s playbook translates naturally.

Sun’s Organon acquisition also opens a door none of these companies have ever walked through: China. Organon has an existing commercial presence in the Chinese market, selling established brands that still command 20-30% market share despite dozens of generic alternatives. Sun’s management sees this as a massive platform.

But the US, historically the crown jewel of Indian pharma exports, is a more complicated picture.

Sun’s US generics business declined 1% in FY26. Cipla’s US revenue was dragged down by the expiry of its lucrative generic Revlimid and a supply crisis with Lanreotide, one of its top three US products. Zydus grew a modest 6% in the US, also due to the expiry of its own Revlimid product.

The sector isn’t abandoning the US, but tariff uncertainty and regulatory headaches only reinforce the shift toward India, Brazil, and other emerging markets.

What’s ahead

So, what do we look forward to in FY27?

Sun needs to prove that Organon — a company growing at barely 1-2% — can be revitalised under Indian management. Torrent needs to show that JB Pharma’s integration delivers the synergies that justify its premium valuation, while managing elevated leverage.

Cipla faces the highest-stakes year of the four: its margin recovery depends on US respiratory launches — generic Ventolin, generic Advair, generic Symbicort — landing on time, and its FY27 EBITDA margin guidance of 18.5-20% has already been cut three times in two years. Zydus needs its multi-engine model — pharma plus consumer plus medical devices plus contract manufacturing — to deliver without becoming too complex to manage.

For all four, the GLP-1 share war in India is just getting started: sustaining early market share as more competitors arrive will be the real test. The next set of earnings calls, in July and August, will give us the first real read on which of these diverging bets is paying off.

India’s credit card industry is splitting in two

You can understand most lending products by looking at their loan book: how big is it, how fast does it grow, what’s the bad-loan ratio, where are margins, and so on.

Credit cards don’t work that way. Most of what makes the business worthwhile — interchange fees from every swipe, annual fees, EMI conversion charges, foreign exchange markups, and so on — is tied to how much customers spend, not to how much they borrow. There’s an element of lending to the business, but that isn’t the heart of it.

Keep that in mind as you think about what comes next.

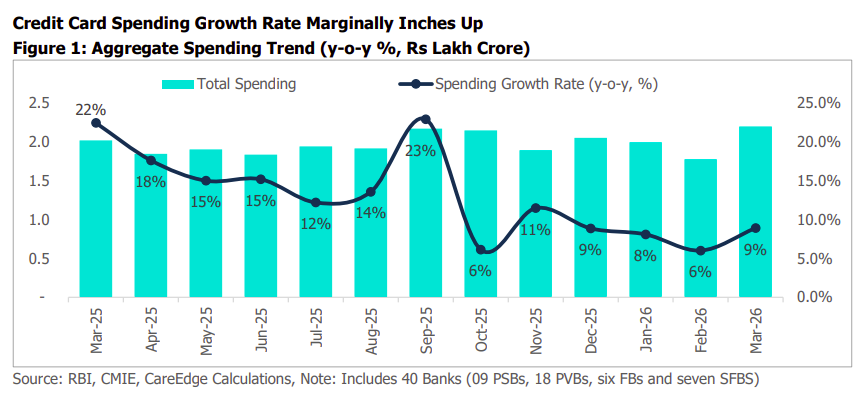

In FY26, total system spends came in at about ₹23.6 lakh crore, which was up 12% year-on-year. That sounds healthy, until you account for how sharply it has decelerated. That growth figure, in FY25, had been 21%. In FY23, it was 47%.

What’s more: per-card, spending barely budged in FY26. The base of cardholders kept expanding, but the average user wasn’t spending more.

What does this tell us? Is the industry just maturing? Or is it a bad time for the business?

Read the FY26 earnings calls of banks and you see more nuance underneath the slowdown, which touches different credit card issuers in different ways. Large issuers, that are part of massive banks, can manage such a slowdown. But smaller specialty issuers, the ones who bet big on credit cards as their only growth play, are hurting.

The big three are managing through

Let’s start with the three issuers that dominate the system.

HDFC Bank — by far the largest issuer — treats its card business as a cross-selling hook rather than a growth engine in its own right. The product sits inside what management calls its “cross-sell thaali“. If a customer opts for any one of these, they become potential customers for the rest of the thaali.

Here, the card isn’t really a simple profit engine. Its value lies in the relationships it builds, the data it generates, and most importantly, the deposits that come with it.

You see, most credit card customers at a large private bank are also account holders, fixed-deposit holders, or mutual fund SIP investors, all through the bank’s platform. Those customers’ account balances are part of what makes the relationship economically viable. For such a bank, the cheapest funding they have on their balance sheet partly comes from those who first walked in for a credit card. That’s a structural advantage that won’t show up in the numbers alone.

Contrast this perspective to that of SBI Cards, which had the standout year of FY26. There, spends grew 29% to ₹4.3 lakh crore, which allowed the company to move its share of system spends from 15.7% to 18.1%. The company actually culled the number of accounts it was adding — with new account additions deliberately falling 12%. And yet, its profits grew by 13%.

Some of this incredible performance probably came from RuPay credit cards, which link to UPI, taking off in smaller towns.

While SBI slowed down their account growth, ICICI Bank did something different — it actually let its card book shrink. Its credit card portfolio contracted 5.6% year-on-year in the March quarter, marking a striking reversal for a bank that, as recently as FY24, had grown the same segment by more than 30%.

This was more than just a seasonal dip. There is industry-wide softness in revolve rates.

That sounds cryptic, we know, and we’ll explain that eventually. But here’s the bottomline: ICICI looked at the economics of its credit card business, and decided not to defend the book, instead letting it contract.

These, however, are big banks. They share the luxury of choosing a posture. A slowdown could touch them, but they can shrug it off.

The bill is coming due

Lets drop below the top three on the issuer table, though. Here, the picture changes sharply.

Take RBL Bank, for instance. Its card book was historically sourced heavily through a co-brand partnership with Bajaj Finance: the latter would source customers, while RBL would hold the credit risk. This was the sort of arrangement that worked beautifully at a time of growth, but can be expensive and slow to unwind when the cycle turns.

But then the arrangement ended abruptly as the RBI tightened the rules around co-branded credit cards.

In March 2024, the RBI clarified that the co-branding partner cannot access transaction data, cannot market the card as its own product, and cannot be involved in any process after the initial issuance. The incentive to enter such arrangements suddenly died. Federal Bank and South Indian Bank were ordered to stop adding new co-brand customers that same month. Then, in December 2025, the RBI reportedly told all partner banks to pause new OneCard issuances pending clarification on data-sharing concerns.

In essence, the RBI mandated that co-branded cards would be a bank product, run on the bank’s terms. The partner no longer had a role.

RBL spent FY26 living through both of these at once. Cards-in-force drifted down from a March 2025 peak of about 48 lakh to around 46 lakh by Q4 FY26. Not just that, the bad loans in the credit card portfolio was a dominating reason for the bank’s higher provisioning cost. In fact, of the ₹684 crore in net provisions on advances during Q4 alone, credit cards accounted for ₹489 crore. A wind down of the credit card business hit hard.

AU Small Finance Bank has been in even more deliberate retreat. The bank scaled up its credit card business aggressively after launching in January 2021, hit 5 lakh live cards by March 2023, and was clocking monthly spends of ₹1,000 crore at the peak. Then the underwriting cycle turned. The card book shrank 19% in FY25, and Q2 FY26 commentary confirmed the calibration was still in progress as unsecured advances (microfinance plus credit card) were down 23% year-on-year.

Now, AU is building its card book off its deposit customer base going forward, not the open market. The bank that issued 50 lakh cards through open-market sourcing has decided that that was the wrong unit of growth to chase.

BOBCARD, the credit card subsidiary of Bank of Baroda, tells a third version of the same story. The company ran a premium co-brand strategy on the RuPay network, and scaled past 10 lakh active users during FY25. But the cost of that scale showed up in the books. Net NPAs jumped more than fourfold from ₹33 crore in FY24 to ₹137 crore in FY25, and return on assets fell sharply.

The pattern across the three is the same. Each built their card business as a standalone growth bet — RBL through a partnership, AU through open-market sourcing, BOBCARD through premium co-brands. Each grew fast in FY22 and FY23. Each is now spending FY26 and likely a chunk of FY27 working off the cohorts they originated during the boom.

The revolver squeeze hits everyone, just differently

Underneath the bifurcation, there’s a problem affecting both the banks and the specialty issuers: the economics of the product itself are getting worse.

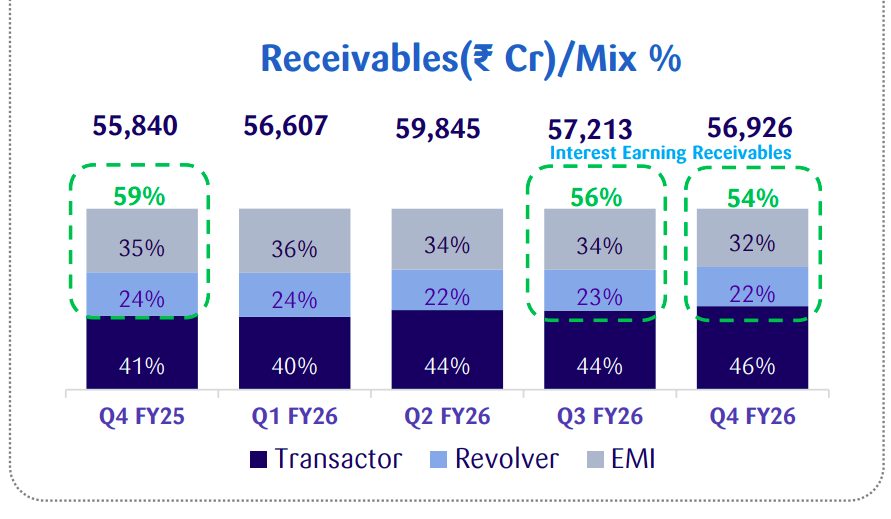

The metric to watch is the revolver mix — it’s the share of card receivables on which the issuer earns the high revolving interest rate. Revolvers are the customers who don’t pay their full bill each month and roll the balance over. They are, by a wide margin, the most profitable customers a card issuer has. The split between revolvers and transactors (who pay in full each month) is the single biggest determinant of credit card profitability.

At SBI Card, the revolver mix has been stuck between 22% and 24% for two straight years, and management now expects a “slight downward bias” in FY27. ICICI’s admission that revolve rate softness is industry-wide, not portfolio-specific, confirms what SBI Card’s numbers suggest.

See, when issuers tightened underwriting in 2024 and 2025, they got rid of the highest-risk borrowers — the ones who couldn’t make ends meet on monthly income and used revolving credit as a bridge. The customers who survived the pruning are wealthier, more credit-tested, and far more disciplined. They use the card for the rewards and the 45-day grace period, then pay in full. Asset quality improves, but the interest income falls.

As one analyst put it on SBI Card’s call, a single percentage point fall in revolver mix translates to roughly 25-27 basis points off the margins. The compensating lever, which is converting outstanding amounts into EMI at lower yields, only partly fills the hole.

This also explains why we have been seeing rewards across the biggest credit card companies going down over the past many quarters.

When the revolver pool is shrinking, there is less money with credit card companies of which rewards are to be given away. It only makes sense to cut them back too.

For the big issuers, the squeeze is manageable — SBI Card is targeting a return on assets of 4-4.5% over the medium term, well above its FY26 print but below the 5%+ the business once posted. For the smaller players, the squeeze is the difference between a viable standalone card business and one that needs a strategic rethink.

What comes next

The pattern across both halves of the industry is the same in one important respect. Everyone is shifting toward existing-to-bank and pre-approved sourcing. HDFC’s cross-sell thali, SBI Card’s banca channel, AU’s pivot to deposit customers — these are variations of the same logic.

Open-market acquisition turned out to be the most expensive way to give out credit cards when the cycle turned, and nobody wants to be exposed to it the same way next time. The fixed-deposit-backed credit cards appearing at the edges of the industry, and the growing role of RuPay credit cards riding the UPI rails for small-ticket spends, are both symptoms of this broader shift in how issuers are willing to onboard customers at all.

The bigger question for FY27 is whether the bifurcation widens or closes. If RBL manages to take care of bad loans of its credit card business by next half of the year as guided, and AU’s turnaround completes in roughly that window, the smaller players might reach the other side. If turmoil sustains, if unsecured stress flares again, if revolve rates keep softening, the gap between the issuers who can absorb a credit cycle and the ones who cannot will keep widening.

Tidbits

The four rounds of petrol and diesel price hike, totalling about Rs 7.5 per litre, have trimmed the losses state-owned oil firms were incurring from selling fuel below cost to close to Rs 600 crore per day, the Joint Secretary in the Ministry of Petroleum and Natural Gas said.

Source: Economic TimesSEBI is reviewing whether listed debt should have disclosure norms similar to listed equity to enhance transparency and investor protection in debt markets, chairman Tuhin Kanta Pandey said.

Source: Hindu BusinessLineIndia’s position as the fifth-largest global market by capitalisation is under threat as Taiwan closes in on the South Asian nation’s spot, powered largely by the rapid rise of TSMC.

Source: Reuters- This edition of the newsletter was written by Manie and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I guess the decline in exports to the US is not structural and might recover in the current financial year.