Indian midcap IT bulks up for a heavyweight fight

Plus: how does the world’s energy report card score?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Indian midcap IT bulks up for a heavyweight fight

The world’s energy report card is out

Indian midcap IT bulks up for a heavyweight fight

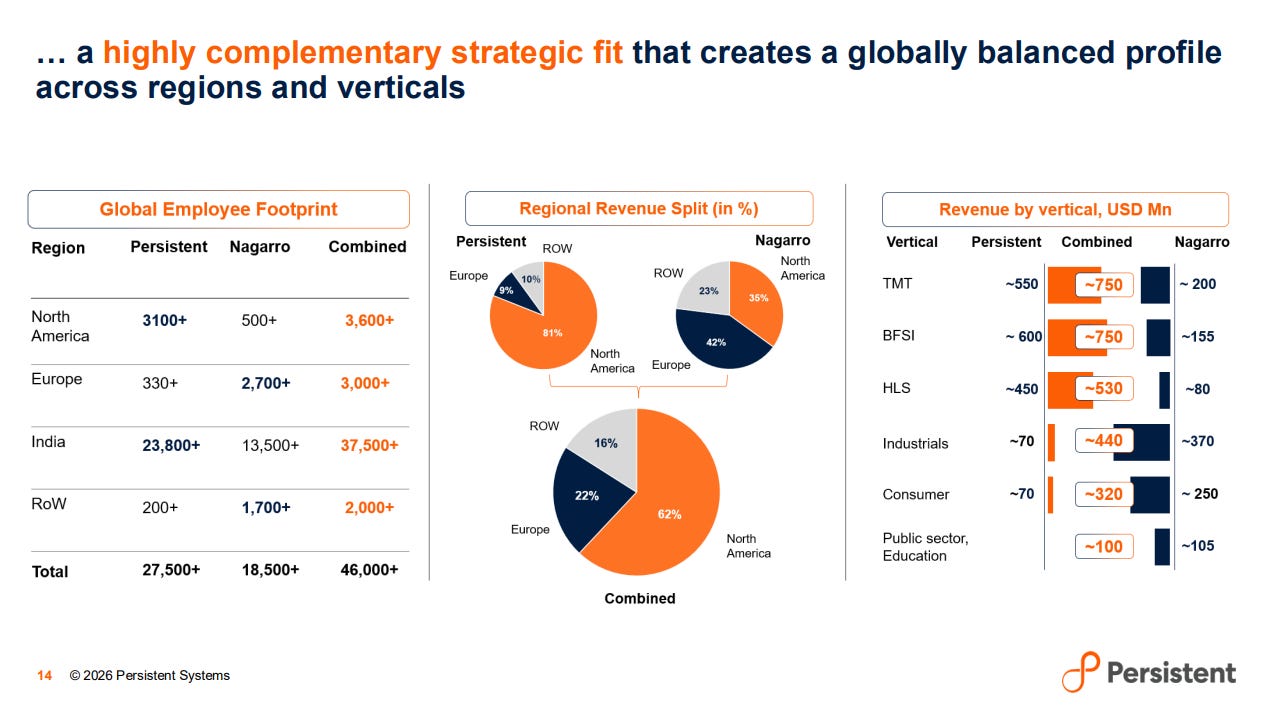

Earlier this week, Persistent Systems, a company we’ve covered all too often in our coverage on India’s midcap IT sub-sector, announced a blockbuster billion-dollar acquisition of Germany-based digital engineering firm Nagarro.

This is the biggest such deal in the company’s history. Nagarro closed nearly a billion dollars of revenue in the calendar year of 2025 (or CY25), while Persistent made $1.65 billion in FY26. With this deal, Persistent might effectively bolster its topline by more than 65%.

But Persistent is no outlier. A few months ago, we covered Coforge’s acquisition of US-based software engineering firm Encora. Similarly, Mphasis also bought a 26% stake in an IT services firm that specializes in providing solutions to the global capability centres of MNCs. And, of course, the larger rivals of these firms — HCLTech, Wipro, and Infosys — haven’t been sitting silently, either.

Much of this trend seems to have been caused by a single earthquake that rhymes with “large-language models”. These acquisitions arrive against the backdrop of the Nifty IT index hitting a 3-year low just 2 days ago because of AI. And mergers and acquisitions usually have a mixed record of success. But right now, they have become one of the most sure-shot ways for IT firms to acquire the one factor that AI might make even more valuable: domain expertise.

With that, let’s look at the Persistent-Nagarro deal, and how it fits in the broader trend of where Indian IT is headed.

An unstoppable machine

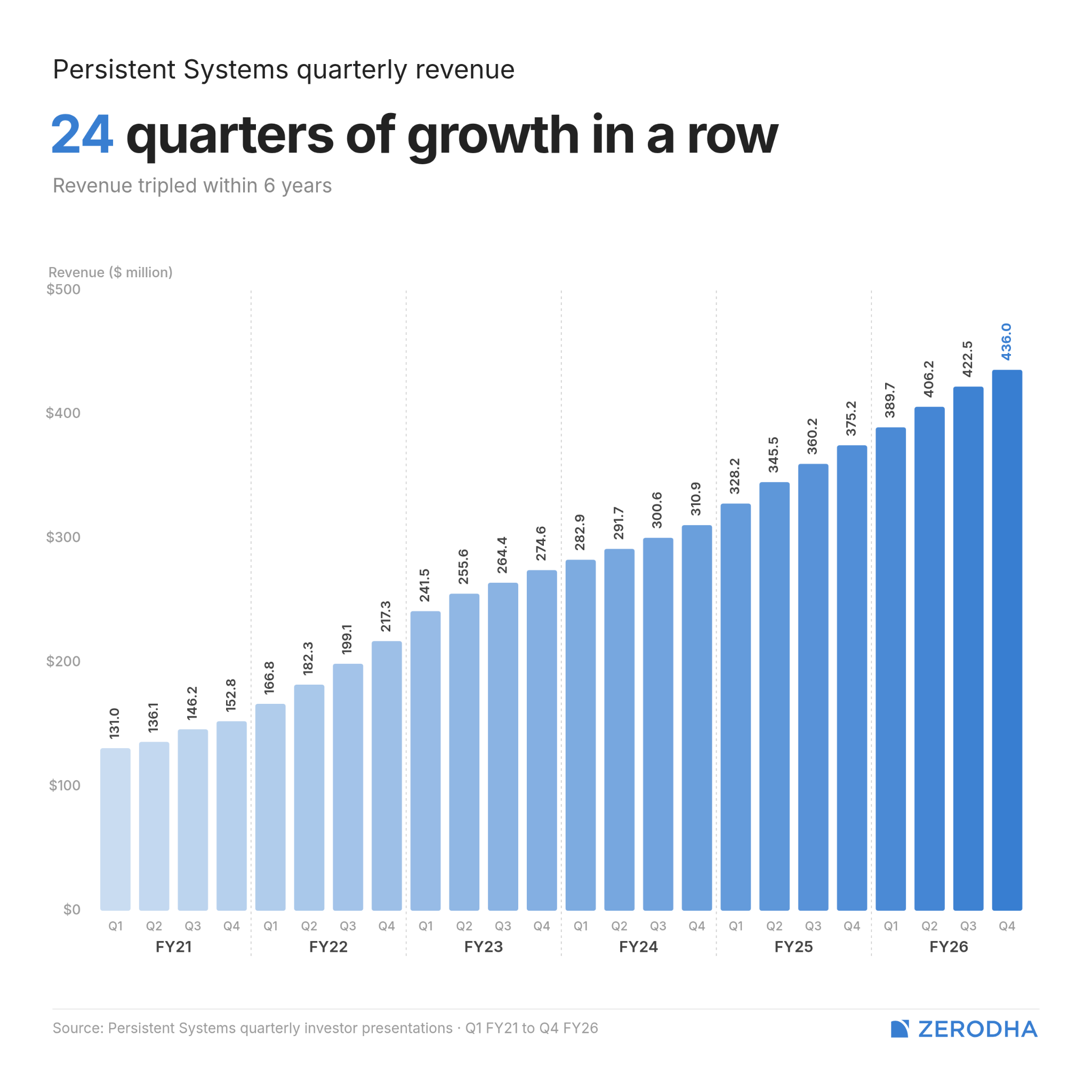

On one side of the equation is a company that, impressively, has only grown for 24 quarters consecutively.

If you’re unfamiliar with what Persistent does, while they’re an IT services firm, they’re not a body-shopping business like much of Indian IT is often characterized. They work with clients closely and actually help design and build software for them, not just provide maintenance and support. They also help conduct full end-to-end enterprise modernization projects, which, by its nature, involves knowing the nitty-gritties of the company’s technology stack.

Now, Persistent’s business is broadly divided into 3 categories of clients.

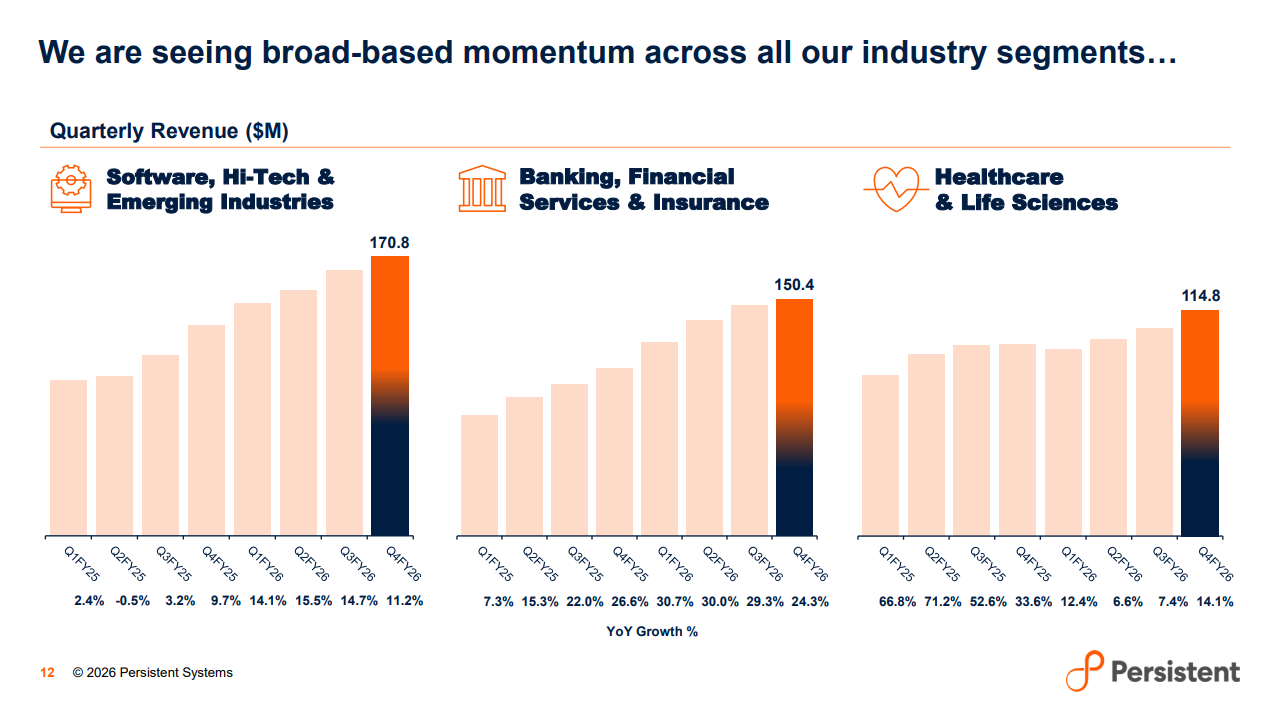

The biggest category, making up 39% of Persistent’s revenues, is “Software / Hi-Tech”, which represents some of the largest tech companies in the world, like Microsoft (who is also one of Persistent’s earliest customers), Salesforce and Amazon. They help develop features on platforms like Azure and AWS which eventually get used by clients in other industries that adopt those platforms. Persistent dominates this sub-sector in India.

It is also this exact area that also puts the company comfortably close to the AI boom, and its impact on how those platforms are built. In our past coverage, we’ve highlighted how Persistent has been much faster in AI adoption compared to its larger peers.

The other two categories are healthcare (which occupies a 26% share), and banking / financial services (which makes 34.5% of revenues). But these two categories are also amongst the most competitive — many of the deals that IT firms are fighting for today lie here. While Persistent’s high shares in these categories — especially “hi-tech” — is a sign of their client relationships only deepening, it also creates an overreliance on just a few sources of revenue. In contrast, Coforge, their peer, is much more diversified.

Persistent also shows signs of overreliance when it comes to geography. Over 81% of its business comes entirely from one country: the USA. However, considering Big Tech and Big Pharma both reside there, that’s as unsurprising as it is risky. Additionally, its top 10 clients make up over 42% of its revenue.

The target

On the other side of this equation is an IT services firm with Indian roots that’s publicly-listed in Germany.

Nagarro started in 1996, six years after Persistent, by an Indian named Manas Human, and only listed publicly in 2020. The structure of the business today is such that it seems to fill Persistent’s gaps.

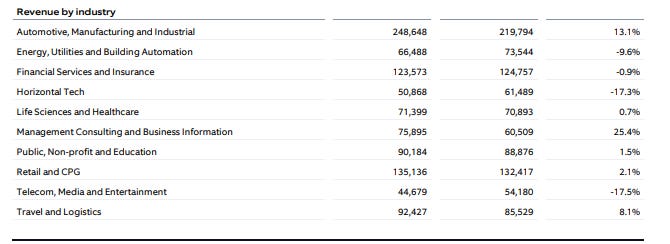

For one, the biggest industrial category for Nagarro is automotive and manufacturing. It makes up 26% of the business. This is followed by consumer products & retail, with a 13% share. They’ve worked with companies like Siemens, Maruti Suzuki, European rental platform SIXT, and even the airports of Dublin and Vienna.

Unsurprisingly, given where most of these clients lie, Europe is its largest geography, contributing 42% of revenues. North America makes up nearly 35%, while the rest of the world is at nearly 23%: Japan makes up a good chunk of this.

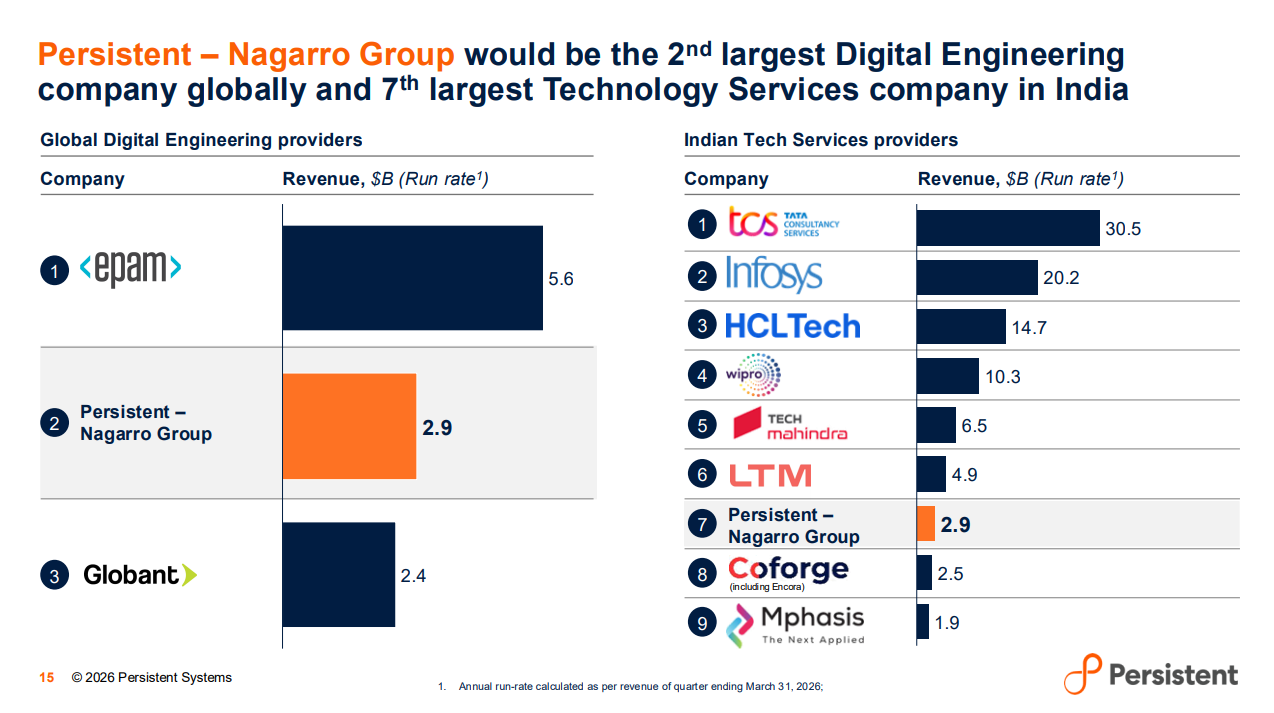

Clearly, with this acquisition, Persistent places its feet firmly in Europe and Japan: geographies that, as we’ve talked about before, have only become more important this year in the wake of unstable American policies. But it also gets capability in industries that it had little-to-no presence in.

But is that worth the whopping 140% premium that Persistent paid for a slowing business like Nagarro?

I went to market and I bought…

You see, Nagarro’s fortunes haven’t been very upbeat of late.

In 2022, Nagarro’s revenues exploded by 56% year-on-year; not coincidentally, that was also a gala time for the fortunes of Indian IT as well. But since then, growth has slowed significantly. Their revenues only grew by 0.5% this year in Euro terms. In Q1 of CY26, their adjusted EBITDA of 12.6%, while improving year-on-year, fell well below their guidance of ~15%. Nagarro attributes this to clients reducing discretionary spending in an uncertain economy.

Interestingly, this was not because of their auto clients. In Q2 of India’s FY26, we’d highlighted how American and European carmakers cut back on investments and R&D spending. This hurt companies like Tata Elxsi and KPIT, which made their money serving these companies. But Nagarro was an outlier in this matter, with auto revenues rising consistently, even growing 11% year-on-year in Q1 2026 when everyone else found it hard.

Yet, Nagarro has been hurting for a while. And that shows up in the landslide their stock has taken since peaking around €200 in 2022, down to around €33 right before this deal. With the premium, Nagarro was valued at €81 a share.

The short-sell squeeze

Now, part of this decline is also owed to Nagarro being squeezed by lots of short-selling.

In 2023, short sellers targeted Nagarro because they believed it had structural weaknesses that would get exposed eventually. For one, since going public, Nagarro expanded aggressively with acquisitions that seemed to underperform, causing overcapacity. Secondly, their revenues didn’t translate well enough to free cash flow: unusual in a cash-rich business like IT services.

Investors also didn’t have full faith in its corporate governance. For instance, their auditor was too small, and not a globally-respected one. None of these were allegations of fraud, though. They were all attacks on the quality of earnings.

However, Nagarro cleaned their act up. The business continued to grow, and they also got KPMG, a globally-respected auditor, to repair its books.

But the pressure didn’t seem to fully go away. Two years later, it was revived by Matthew Earl, a short-seller who was one of the first to point out discrepancies in German firm Wirecard, which turned out to be one of the largest cases of fraud. Earl made a more serious complaint about Nagarro’s accounting issues than the past short-sellers.

However, an independent investigation by law firm White & Case and consulting firm Alvarez & Marsal cleared Nagarro of outright fraud, while suggesting improvements in their governance.

Valuations in the AI world

Yet, even without all this pressure, things would have been bad enough for Nagarro anyway. To make things worse, Nagarro has been unable to escape the AI-led bloodbath that has plagued all of software and IT.

The debate now is whether Persistent made a worthy bid for Nagarro. One way of thinking around this is that since AI depressed valuations across the industry, certain companies have become cheaper targets to buy up and scale. So then, a 140% premium over the current price wouldn’t be so bad if the resulting entity manages to emerge as one of the strongest AI-native services firms of the world.

Sandeep Kalra, CEO of Persistent, has been very confident that Nagarro is a highly-complementary business to Persistent, will contribute to margins eventually post-integration, and will be accretive to earnings-per-share.

But Persistent is acquiring a business with a worse margin (and growth) profile than its own, that too entirely by raising debt of ~$1.5 billion, $350 million of which will be used to refinance Nagarro’s own debt. Persistent’s own cash flow is healthy, but this is still a large number, only reflective of the ambition Kalra has for the joint entity. And it depends primarily on their bet on the direction of AI.

Context is everything

A similar logic underpins the flurry of M&A deals the industry has seen recently.

Earlier this year, the big headline was Coforge’s $2.35 billion acquisition of Encora, designed to vault it into a $2.5 billion company with AI-led engineering capabilities and a US West Coast footprint it had been chasing for years. Since then, Cyient bought TAO Digital, an AI-native data engineering firm, for $218 million. Mphasis acquired a stake in Aokah, which focuses on GCCs.

Among large-caps, Wipro spent $375 million on HARMAN’s embedded software business, while HCLTech acquired Hewlett-Packard Enterprises’ telecom solutions arm.

The common thread tying these acquisitions is something we’ve addressed across Markets by Zerodha: be it our Subtext episode with investor Ameya P, or our past Daily Brief stories on this industry. It’s that AI has made domain knowledge more important than ever.

See, a large chunk of what IT services firms have traditionally sold is increasingly being commoditized. But what AI can’t easily replicate is knowing a specific industry inside out — like the regulatory labyrinth of European banking, or the myriad complications in building a stable data pipeline that makes drug discovery easier and safer simultaneously. That kind of domain expertise doesn’t come automatically with LLMs, but with lots of iterations and accumulation of training data. So, it helps to build client relationships as early as possible.

This is why the deals look the way they do. Coforge bought Silicon Valley product relationships. Persistent bought deep expertise in verticals it had almost no footprint in. Most deals involve acquiring a domain moat that would take much, much longer to build organically in a market that may not give you that much time. It just sounds more convenient to buy domain expertise now, especially now that valuations continue to fall.

There’s also a simpler logic at play. The Nagarro acquisition buffs up Persistent’s balance sheet such that it can stand toe-to-toe against India’s tier-1 IT companies. It was already taking deals away from these companies — this will only intensify the competition.

Conclusion

There is lots of potential in the thesis that is driving most of this M&A activity. Even we at The Daily Brief, with our limited knowledge of AI, can tell you that LLMs are only as good as the context you give them. It’s why so much stress is put on building pipelines that ensure context flows to LLMs cleanly to get your job done.

But this rests on the assumption that knowing an industry inside out will remain an advantage for long enough to justify high price tags. This is an industry where overvaluations burned a few hands a few years ago, and investors may not want a repeat of that in the face of AI.

Moreover, with these moves, midcap IT firms, which were earlier known for being nimble, may find themselves less so. Deciding on a thesis also means locking in what your organizational structure looks like, and all the limits that can impose on you. Just the same way today’s tier-1 IT firms became slow and lumbering.

It’s too soon to say how this choice pans out in the face of a technology whose full shape we’re very far from knowing.

The world’s energy report card is out

Every year, the Energy Institute publishes an incredibly comprehensive snapshot of how the world produces and consumes energy. Its 75th edition just landed, and the energy fiends that we are, we decided to take a peak at what the report says.

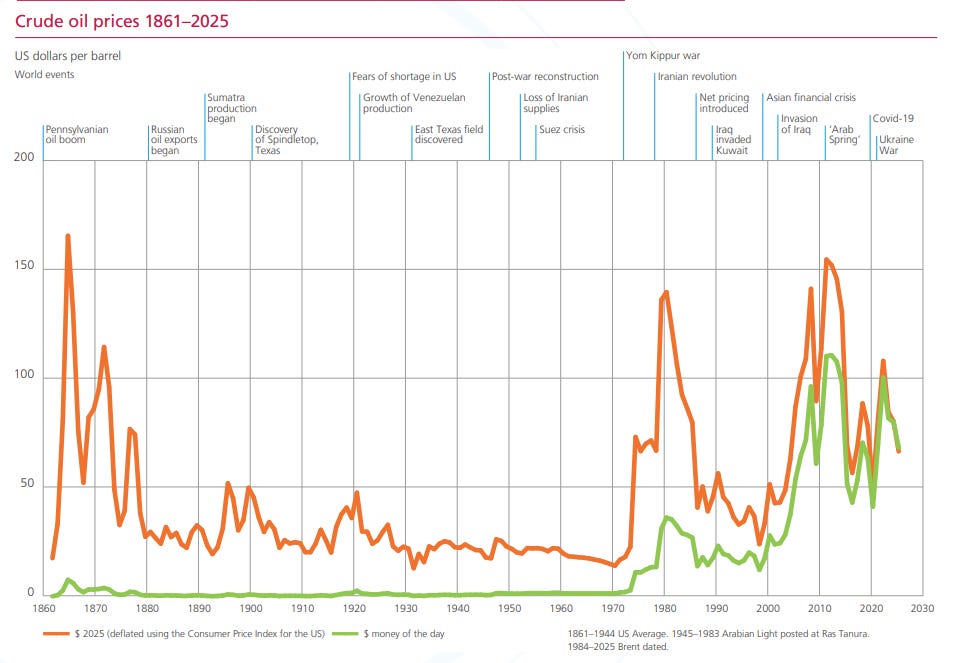

Now, it’s worth noting that this report covers 2025, the year before hostilities in the Middle East led to the effective closure of shipping in the Strait of Hormuz in early 2026. So 2025 becomes the baseline against which that shock, and its still-evolving aftermath, will be measured.

Let’s dive in.

More, more, more

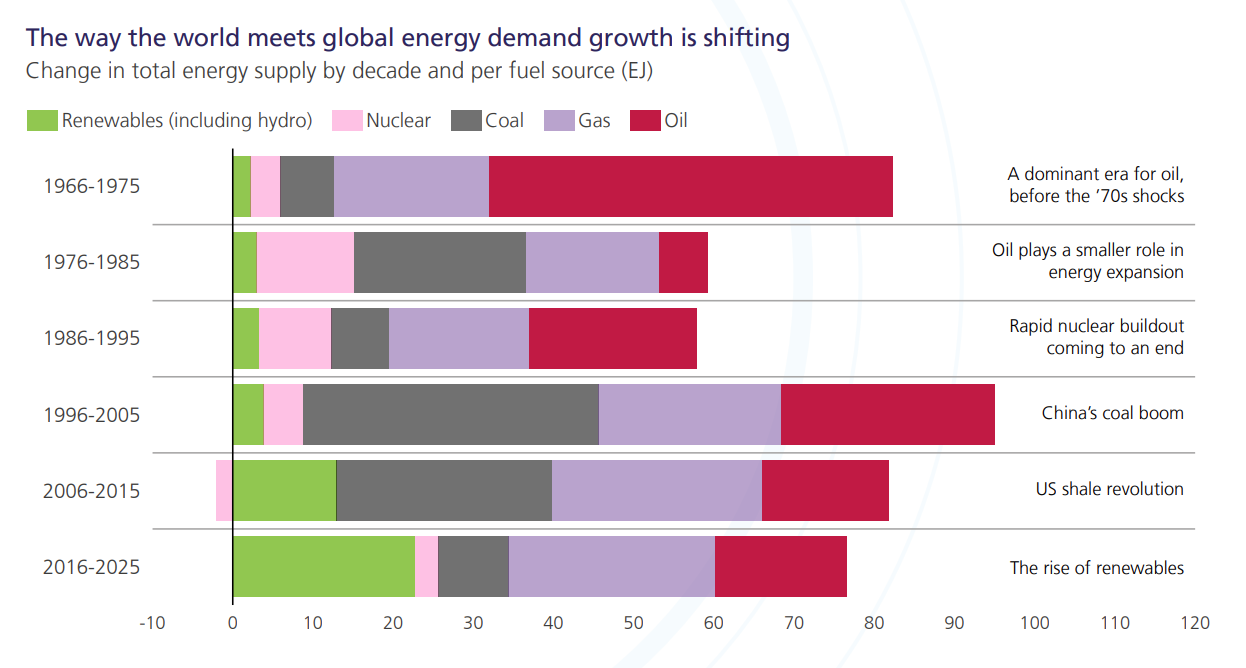

The headline number is that total global energy supply crossed 600 exa-joules in 2025. One exajoule is roughly what the United States consumes in about 4 days, so 600 of them is immense. In 2025, every major energy source, from oil & gas to nuclear, grew. Clearly, the world’s appetite for energy is endless.

Now, fossil fuels still account for 86% of everything the world consumes, and that share has barely moved in years. Renewables are growing fast enough to supply a large chunk of the world’s new demand, but not fast enough to start replacing what was already there. Global CO2 emissions from energy rose 1.1% as a result, reaching close to 36 billion tonnes. Broader emissions tracked by the report, including methane from fossil fuel systems and industrial process emissions rose to ~41 billion tonnes.

There is one important exception to this picture, though. When people say “energy“, they usually picture electricity, but electricity is only about one-fifth of global energy consumption. The rest goes directly to heating buildings, running industrial furnaces, and fuelling ships, planes, and trucks, all of which still mostly run on fossil fuels.

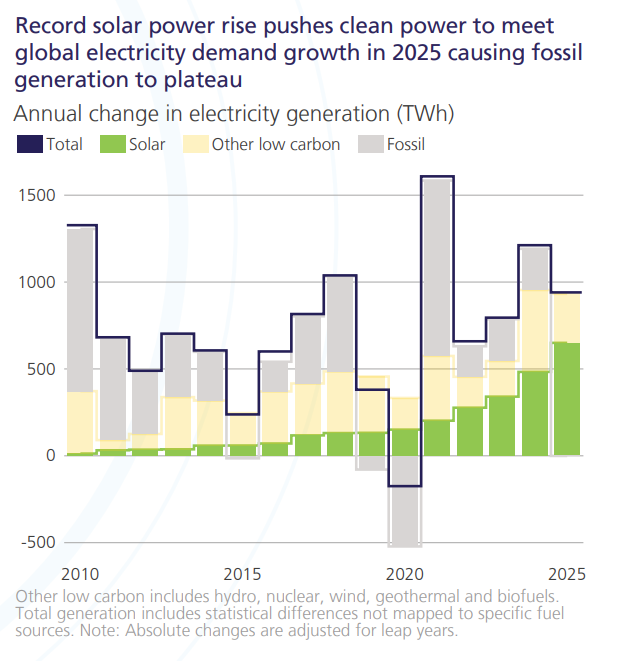

In electricity specifically, renewables did grow large enough in 2025 that they actually pushed fossil generation down for the first time. Renewable sources added more new supply than total electricity demand grew, so fossil generators did not need to fill the gap. And for the first time in history, coal’s share of global electricity at 32.6% fell below clean sources at 33.4%.

The green transition in electricity is certainly solid, but elsewhere, fossil fuels remain king.

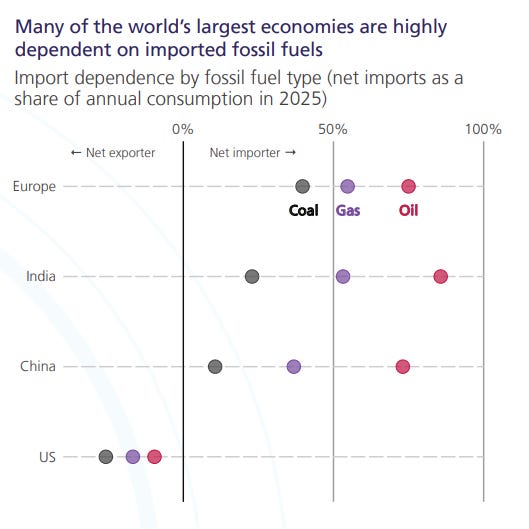

The deeper argument running through the report is about what it costs to depend on imported energy. The authors draw a line to the oil shocks of the 1970s, before which, oil was meeting 61% of all global energy growth.

The OPEC embargo changed that permanently. Countries invested in nuclear, efficiency standards, and domestic production. In the EU, UK, and Japan, oil consumption never returned to its 1979 peak. The report asks whether the 2026 Hormuz closure does the same thing.

What the 2025 data makes clear is how exposed the world still is. India imports 86% of its total oil consumption, while Europe’s ratio is 75%. In each case, a significant share flows from the Persian Gulf. Countries that reduced this exposure — like the US with the shale oil revolution, or Europe with its wind and solar buildout after the Ukraine war — are better positioned to absorb a supply shock.

In a previous story, we also covered how the Strait of Hormuz crisis forced countries to accelerate the clean energy transition.

The renewables revolution

Now, the engine of the electricity shift was solar.

Solar power grew 30% in a single year. Its share of global electricity reached 8.7%, overtaking wind at 8.4% and almost drawing level with nuclear at 8.8%. Solar spreads faster from any other energy technology because it is modular and cheap in a way that power plants are not. A household or a factory can put panels on a roof and start generating electricity almost immediately without waiting for a grid connection.

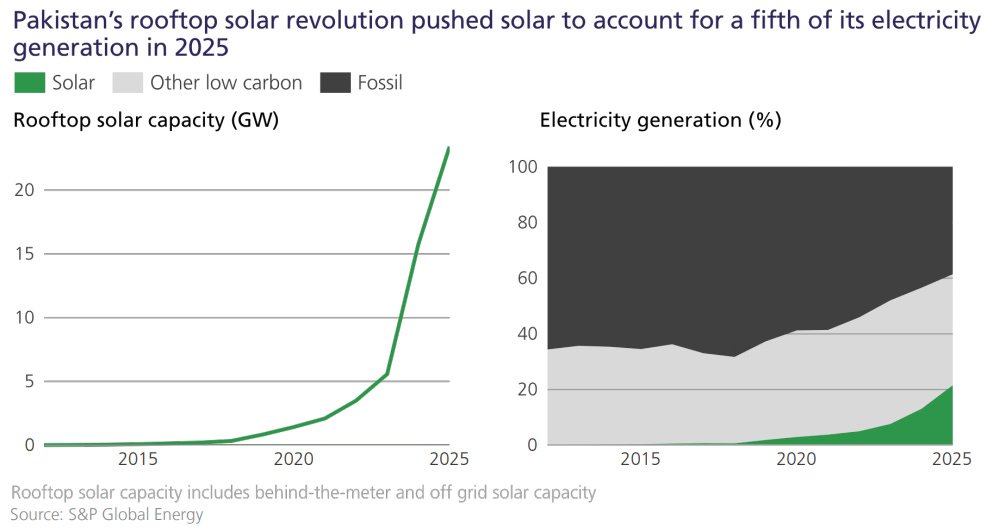

Pakistan is the clearest example in the report of what this looks like at scale.

Between 2021-2025, Pakistan’s share of solar in electricity jumped from 3% to 22%. But that shift happened not because the government built large solar farms. As we’ve covered before, it was primarily because ordinary households put up cheap panels themselves to escape a crumbling national power grid that made power expensive.

But within a few years, enough rooftop solar had been installed that the country no longer needed the gas it had contracted to import. Pakistan has since moved to cancel LNG cargo deliveries scheduled for 2026-2027 and renegotiate long-term contracts.

Battery storage, which makes using solar energy at night even possible, is following a similar curve. Global installed battery storage capacity grew 66% in 2025 to 302 gigawatts. In 2020, it was only about 19 gigawatts. It has grown 16 times over in five years. Without it, you need a fossil fuel plant on standby for when the sun goes down.

Two ends of the world

You might already be tired of hearing this from us, but inescapably, no discussion of clean energy is complete without China. The report calls China the world’s largest “electrostate“, meaning it runs more of its economy on electricity, relative to direct fuel burning, than almost any other large country.

In 2025, China’s coal consumption was flat year on year for the first time in a decade, held in check by a 40% surge in solar generation. More than half of all new cars sold were electric. China has also retrofitted 360 gigawatts of its coal power fleet to ramp up and down quickly, so that coal plants can fill in when solar is not generating rather than running continuously whether it is needed or not. That is how China is managing a grid that is simultaneously adding enormous amounts of solar while keeping the old system running.

None of this means China is definitively moving away from fossil fuels, though.

Oil consumption still grew 2.8%, driven now by the chemicals sector, since plastics, fertilisers, and synthetic materials are all derived from oil, and China makes a lot of those things. China is still the world’s largest coal consumer. The picture is of a country deploying clean energy at a scale no country has matched while keeping its fossil fuel systems intact as insurance.

On the other side of China lies the most powerful country in the world, both literally and metaphorically.

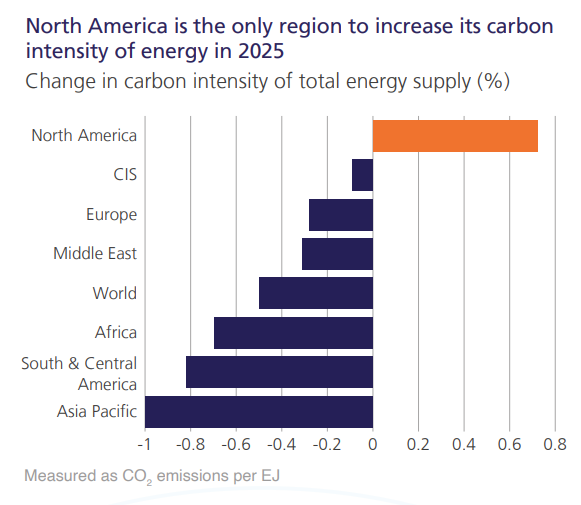

Global energy emissions grew 1.1% in 2025, and the US accounted for more than a third of that entire rise, despite representing only about 15% of global energy supply. US emissions rose 3.2%. In absolute terms, the increase in American emissions was four times larger than China’s.

The cause was an unusually cold winter. Heating demand went up, and a lot of American homes heat with gas. That pushed natural gas prices up by more than 50%. When gas gets expensive, power plant operators switch to coal. After all, generators bid power into the grid based on what it costs them to produce, and whichever fuel is cheapest wins. And in 2025, coal won more bids.

Coal generation increased by 93 terawatt-hours while gas generation fell by 62. North America was the only region in the world to increase the carbon intensity of its energy supply in 2025. This shows how a single cold season can push a country’s emissions sharply upward when most of the grid still runs on fuel whose price moves around.

The Indian story

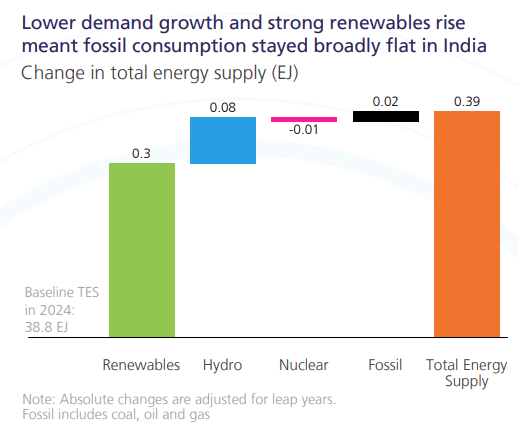

Meanwhile, India’s 2025 data contains a genuine, pleasant surprise.

We know that our economy has been growing at roughly 6-7% a year for the better part of a decade. When a country grows at that pace, it normally burns a lot more energy. But what’s interesting is that fossil fuels don’t take up much of the credit for it!

For the first time since 1965, India’s fossil fuel consumption was essentially flat. Coal grew just 0.6% against a ten-year average of 3.6%. Meanwhile, gas fell by 5.9%, while oil grew 0.3%. Part of it was because of a weather effect of a milder monsoon that reduced cooling demand. But, many of you will already know, there is a structural shift in favor of renewables (particularly solar) at play as well.

More specifically, it’s rooftop solar that has helped. Distributed solar installations grew 40% in 2025 to 43.6 gigawatts, the largest single-year increase anywhere outside China. As more buildings generate their own power they draw less from a grid mostly powered by coal and gas — whose generation did fall. We even covered the rooftop solar revolution recently.

The constraint, though, is the power grid.

India has strong solar resources in states like Rajasthan, but industrial and urban demand is concentrated in states far away. Getting power from where it is generated to where it is needed requires transmission lines and substations that take years to build. The result is that solar capacity is being added faster than the infrastructure to move it around, and coal plants in some regions keep running because the grid cannot yet reach the cleaner alternative.

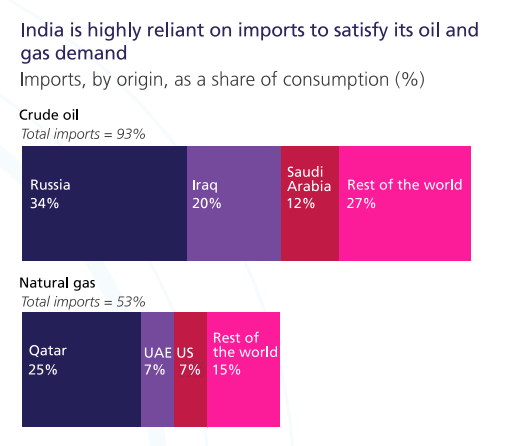

Import dependence remains large. India imported 90% of its crude oil in 2025, with Russia supplying about 34% and the Gulf region another 48%. The Hormuz closure hit India directly through that share. For gas, 53% of supply is imported.

What to make of all this

The honest read is that the energy transition is accelerating rapidly, but somehow still not fast enough. Clean electricity overtook coal globally for the first time in 2025. In the same year, total fossil fuel consumption reached a new record and emissions rose. Both things are true at once, and the tension between them is what the report tries to disentangle.

The 2025 data is now the world’s reference point for how things stood before one of the largest energy supply disruptions since the 1970s. Every number in it tells you something about how exposed different countries were, how fast their transitions were actually moving, and how much of the global energy system was still depending on a narrow channel of water in the Persian Gulf to keep functioning.

Tidbits

[1] RBI funding rules may squeeze proprietary traders

New RBI rules require bank guarantees used for equity trading to be fully backed by collateral, with at least half in cash. Traders expect higher funding costs and lower returns from arbitrage and market-making strategies, with smaller domestic firms likely to be hit the hardest.

Source: Bloomberg

[2] Cabinet clears ₹6,969 crore tunnel linking key Delhi corridors

The Cabinet has approved an ₹6,969 crore, 8.1-km six-lane tunnel connecting Dwarka Expressway with Nelson Mandela Marg in Delhi. The project is expected to improve connectivity between West and South Delhi while generating over 17 lakh person-days of employment.

Source: Business Standard

[3] Kotak Mahindra Bank to acquire Deutsche Bank’s retail business in India

Kotak Mahindra Bank will acquire Deutsche Bank India’s retail, private banking and wealth management businesses. The deal includes around ₹29,000 crore of loans, ₹16,000 crore of deposits and ₹10,500 crore of assets under management, strengthening Kotak’s affluent and SME banking franchise.

Source: The Hindu

- This edition of the newsletter was written by Manie & Krishna.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how large language model usage changed over the past eighteen months, through the public usage data of one busy AI marketplace.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉