Indian IT sees some clarity in the unknown

Breaking down the Q4 FY26 results.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Indian IT sees some clarity in the unknown

Dollar prices and economic pain: What’s actually happening

Indian IT sees some clarity in the unknown

Every quarter, we return to the same questions about Indian IT. And for most of the last year, the answers were some version of “unclear“.

We covered what went wrong in Q1 and a tentative recovery in Q2. Q3 was a more confident showing, but highly uncertain, and not just because of AI.

Now, the Q4 answers are getting sharper, as some companies are speaking more plainly about what’s actually happening to their business. The last quarter also tends to be a reflective moment for management.

So, to finally round up the whole year, we’ll be looking at the results of tier-1 Indian IT firms, particularly focusing on TCS, Infosys, HCLTech and Tech Mahindra (TechM). Later, in another episode, we’ll cover the performance of mid-cap IT firms separately.

We also recommend listening to our recent podcast on Indian IT with technology investor and veteran IT professional Ameya P to gain richer context on what the results mean.

The numbers

Let’s start with the headline numbers.

TCS’ Q4 revenue came in at $7.6 billion (~₹71,000 crore), topping the total FY26 revenue to $30 billion (₹2.67 lakh crore) — which is actually 0.5% less than last year. Meanwhile, the full-year’s operating margin of 25% is the highest TCS has posted in four years. Their AI revenue has reached an annualized run rate of $2.3 billion (~₹20,500 crores).

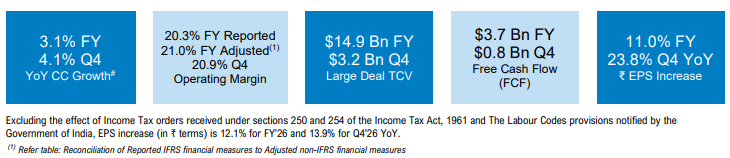

Meanwhile, Infosys’ Q4 revenue grew by 4.1% year-on-year. Its full year revenue is 3.1% higher than last year. Their operating margin has remained close to 21%. Their total contract value for the full year came in at ~$15 billion (~₹1.33 lakh crore), with 55% being net-new business.

HCLTech’s Q4 revenue was up 2.4% year-on-year, amounting to ₹33,981 crores. Their EBIT stood at 16.5%. Now, sequentially, their performance fell quarter-on-quarter due to clients postponing certain projects, but over the year, there has indeed been progression. Moreover, their Advanced AI revenue is up 6.1% from last quarter, standing at $155M (~₹1,430 crores).

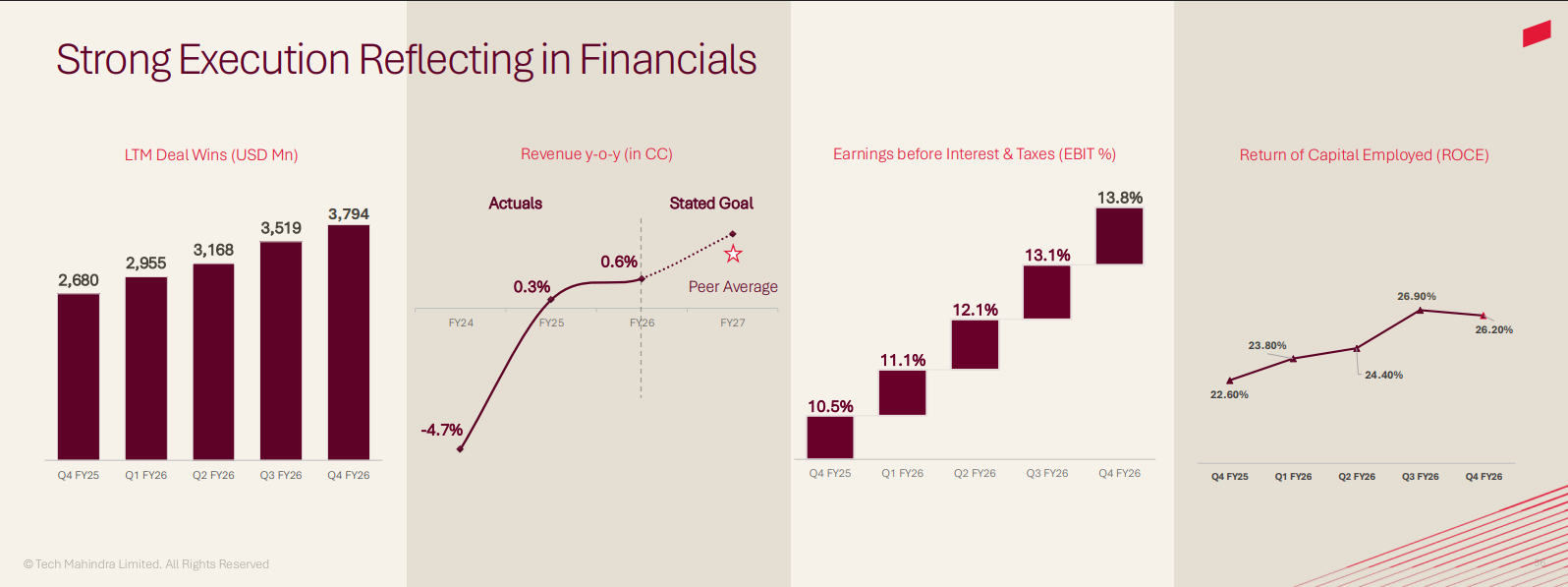

Tech Mahindra’s Q4 revenue grew 2.4% year-on-year to $1.62 billion (~₹15,000 crores), rounding their total year revenue to ~$6.39 billion (~₹56,800 crores). Impressively, this was their tenth consecutive quarter of margin expansion, going from 6.4% to 13.8% in just over 2.5 years.

AI economics

Now, let’s get down to business.

The pricing shift

In our podcast with Ameya P, we spoke about the impending change in the business model of the industry. In particular, with AI, Indian IT’s practice of billing based on headcount will make little sense. Instead, clients will pay IT firms based on the outcomes they achieve.

However, that transition is easier said than done for the industry. One reason for that is this—how do you define the scope of work with outcome-based pricing, when earlier, that scope was defined in terms of manpower-hours?

This quarter, though, we have a far clearer sense of where in that transition Indian IT might be.

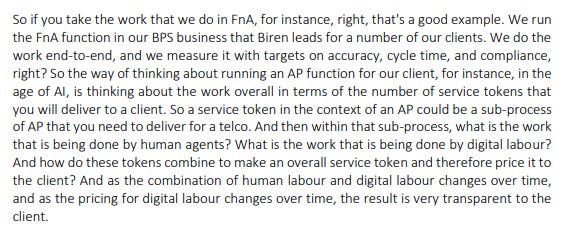

For instance, the most interesting commercial development came from Tech Mahindra. They have rolled out a “service token pricing“ model. Under that, each contract is broken down to individual sub-processes. For each of those sub-processes, the model specifies exactly what proportion of the work will be done by humans versus digital labor. As AI capabilities improve, the pricing shifts accordingly, with full transparency to the client.

In fact, last quarter, Infosys had also explicitly said that they’ve already begun piloting models that incorporate some amount of outcome-based pricing.

However, does that mean a full shift has taken place? Understandably, this is still a phase where IT firms haven’t fully figured it out. After all, in a world where AI is developing at breakneck speed, the same productivity outcome that has a certain price tag today wouldn’t do so tomorrow.

But it’s clear that the business model shift has cleared the pilot phase and is part of real contracts being won by IT firms. TechM’s new, hybrid pricing model accounts for a large chunk of their new business. Last quarter, HCLTech had also attributed a new, outcome-based model to a deal win.

Margin versus growth

Of course, pricing affects margins. But the margin story is a little complicated.

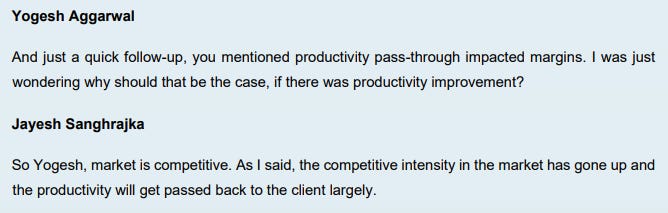

On one hand, the industry seems to agree that AI is already deflating their business. For one, clients have already begun expecting lower prices for the same productivity gains. Secondly, AI has made the market more competitive, and companies have little choice but to pass productivity benefits to clients in order to win deals.

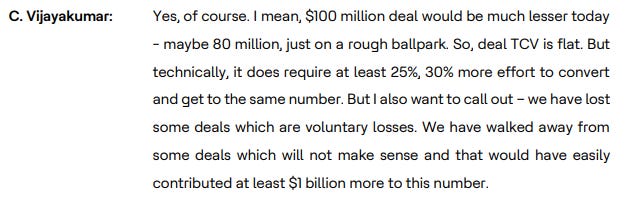

HCLTech’s CEO, C. Vijayakumar put numbers to it: it takes them 25–30% more effort to earn the same revenue, as AI compresses the per-unit cost of each project. It is partly why HCLTech’s new deal wins took a hit this quarter.

On the other hand, though, most companies are aggressively sticking to margin discipline. Infosys and TechM explicitly said that they walked away from large deals that didn’t meet their profit thresholds. And in some AI deals, Infosys has even said that they were able to charge higher prices.

Now, one has to wonder: how can Indian IT afford to commit to their high margins while AI looks to flatten the same?

Well, this margin discipline might partly be a response to AI deflation. If AI is taking away your lunch somewhere, you might want to adjust elsewhere. But if AI keeps compressing the economics of every deal, then margin discipline becomes a shrinking perimeter.

New business

In last quarter’s IT results story, we’d briefly touched upon the new revenue lines that have begun to emerge. This quarter, we have more real instances of what they look like.

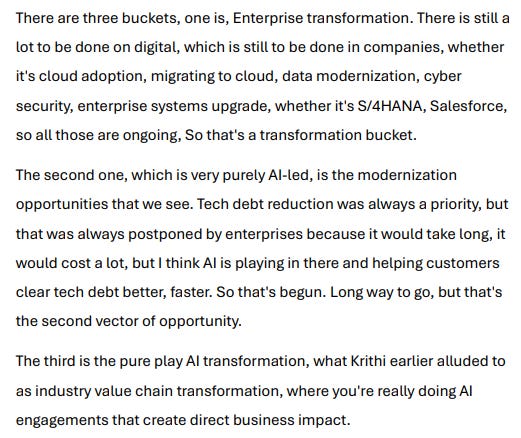

TCS, for instance, has separated its digital transformation work into three broad categories: enterprise transformation, AI-led modernisation, and pure-play AI transformation. The first two are extensions of what these companies have always done, with AI tooling layered in. We’ll use a similar framework to highlight examples of what each type of work might entail.

Enterprise transformation is the old digital work that Indian IT is best known for. It’s getting companies onto the cloud, modernizing their data pipelines, integrating software like SAP and Salesforce. With how software itself is being disrupted by LLMs, enterprise transformation is also bound to get faster with AI.

Meanwhile, AI-led transformation entails using AI to clean up old technology debt. For instance, this quarter, Infosys highlighted how they helped a client migrate three million lines of code written in COBOL to modern microservices using AI models — 60% faster, at 60% lower cost.

The category of pure-play AI is newer, and involves building AI-native products and workflows from scratch. It’s still a small, emerging space, but it’s a category where engineering depth matters in ways pure software work doesn’t.

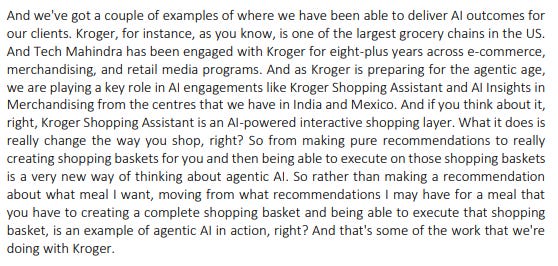

For instance, for American retailer Kroger, Tech Mahindra built an AI shopping assistant that autonomously creates and executes entire shopping baskets. Meanwhile, Infosys implemented AI agents across various sub-functions for the oil giant British Petroleum.

In fact, within this category, physical AI for manufacturing clients is generating serious contracts. For instance, HCLTech deployed its TraceX solution for a US biopharma company to connect physical supply chain processes to AI. Meanwhile, TechM provided a glimpse of how they’re integrating services work for Canadian aircraft maker Bombardier.

However, besides these three, there is also a fourth, completely new category that’s emerging from the AI value chain itself. As LLMs keep on developing, they also help set up infrastructure that spans data centers, cloud platforms (like AWS and Azure), and AI labs themselves. And IT firms look to insert themselves in this chain.

For instance, Wipro has signed a deal with a global tech major. They have engaged Wipro to run and improve its frontier AI models, which will involve training, governing, and running domain-specific validation. This is reinforcement learning work, where you take the baseline LLMs and fine-tune them for specific purposes using deep domain expertise. In fact, in our podcast, Ameya P had highlighted that Wipro was already doing some subset of this work.

HCLTech, meanwhile, plays even deeper in this value chain. It provides data center design and implementation services to hyperscalers building out AI capacity. They also help manage GPU workloads once those centres are live. Perhaps, they also leverage some of their expertise in doing similar work for non-AI data centres in the past.

But that’s not all — there is a more capital-intensive version of the data center playbook. And that is only being executed by one firm: TCS.

Earlier in FY26, to everyone’s surprise, the historically asset-light TCS announced that they were building a new AI data center, anchored by an agreement with OpenAI for 100 megawatts worth of capacity. In the latest earnings call, they’ve hinted that some clients have already committed to buying compute from them — well before the data center is built.

In TCS’ own words, it’s the foundation of a “full spectrum play from infrastructure to intelligence”. The same client could purchase an entire bundle from computing power to software engineering services that TCS is known for. Uniquely, it also makes AI labs like OpenAI not just vendors they purchase subscriptions from, but also their customers who could also buy their workload management services. From its earnings call, TCS seems well aware of the unique leg up owning an AI data center could give them.

The geography is shifting

Now, let’s move onto the geography of the business.

The US remains the largest market for Indian IT, but it is increasingly not the growth market. For one, US discretionary spending has been flat to declining across most of the cohort, and companies are navigating around it rather than waiting for it to recover. But beyond that, tariffs are hurting the budgets of companies based out of the US.

However, as we’ve highlighted in past stories, large-cap IT has been deliberately pursuing a strategy of portfolio diversification.

In particular, Europe has been rising fast in the revenue mix. For instance, 11 of Infosys’ 19 large deals in Q4 came from European clients. TCS won a five-year UK telecom consolidation deal — its first mega-deal of the calendar year in communications. TechM also recorded a robust 8.9% year-on-year growth in its Europe business.

However, there is one caveat to this: the decline of the European auto industry has been a drag on this growth. The EV transition and tariff disruption are choking European auto. Indian IT is dealing with both at once.Every major company flagged it. Wipro called out auto and industrial as the hardest-hit sectors from tariff pressure. Infosys also highlighted headwinds faced by a particular European auto client of theirs.

The Middle East has also been coming up as a theme. However, from the latest commentary, it has become one of the biggest risks to the industry. It hits Indian IT through four distinct channels — employee safety in West Asia, demand for travel and transportation services, crude price volatility affecting energy clients, and a ‘wait and see’ effect freezing the discretionary IT spend of clients. Naturally, it was the most unexpected crisis for them.

At the same time, though, this crisis may have also created some new business for them. For instance, much of the growth of TechM’s manufacturing business was driven by aerospace and defence. Those are precisely the sectors that will see spikes in production during geopolitical volatility.

What next?

The outlook for FY27 is anchored by many questions. How does the transition in how IT contracts are priced go from here? How do companies manage the balance between margins and growth while AI threatens to deflate both old and new businesses? How will TCS’s data center bet pay off before the capex drag becomes visible in margins? And how permanent is the derisking from the US going to be?

There are some questions that we haven’t even properly addressed in this story. How does Claude’s new model, Mythos, change the potential of some of the new AI revenue lines? How does Anthropic’s launch of their own AI services firm change things? And while the hiring picture hasn’t changed since last quarter, the anxiety around it only grows larger.

All we can say for sure is that we expect the results and announcements to be a lot louder in the future.

Dollar prices and economic pain: What’s actually happening

The American Federal Reserve holds the rest of the world under its spell.

For most of the last forty years, whenever the Fed aggressively tightened dollar supply, somewhere far away, in the developing world, something would break. In 1982, the “Volcker shock” pushed Mexico into a debt crisis that took the rest of Latin America down with it. A decade later, the United States increased rates midway through the 1990s. As the dollar grew stronger, one currency after another started collapsing in what was called the Asian financial crisis. In 2013, a single line from Fed chair Ben Bernanke about slowing bond purchases — not even a full-blown rate hike — sent a number of currencies, including the Rupee, into freefall.

Each time, the same sequence of events would play out. The Fed would shrink dollar supply, or even threaten to do so. Immediately, capital from across the world would rush towards the dollar, making it appreciate. Meanwhile, any debt priced in dollars — of which there was plenty in emerging markets — would suddenly cost more to repay. Local currencies would crack, inflation would rise, central banks would rush to defend their own currencies to stop the bleed, and entire regions would suddenly plunge into recession.

So in early 2022, when the Fed began the most aggressive tightening cycle since the 1980s — everyone assumed that emerging markets would be in trouble again. Many forecasters expected the rupee to fall below 90 to the dollar. Foreign investors were expected to flee, crushing our equity markets.

The Rupee did weaken. But there was no catastrophe. Foreign investor flows were choppy, but our markets still reached record highs. The same happened across the emerging world — Brazil, Mexico, Indonesia, the Philippines — all got through this period relatively unscathed.

Why was this time different? Many economists have scratched their head over this question, and they’ve come up with many answers. But a new working paper from the European Central Bank makes an interesting addition to this debate: you can learn a lot by looking at what’s happening inside these countries when a Fed shock arrives.

The anatomy of a Fed shock

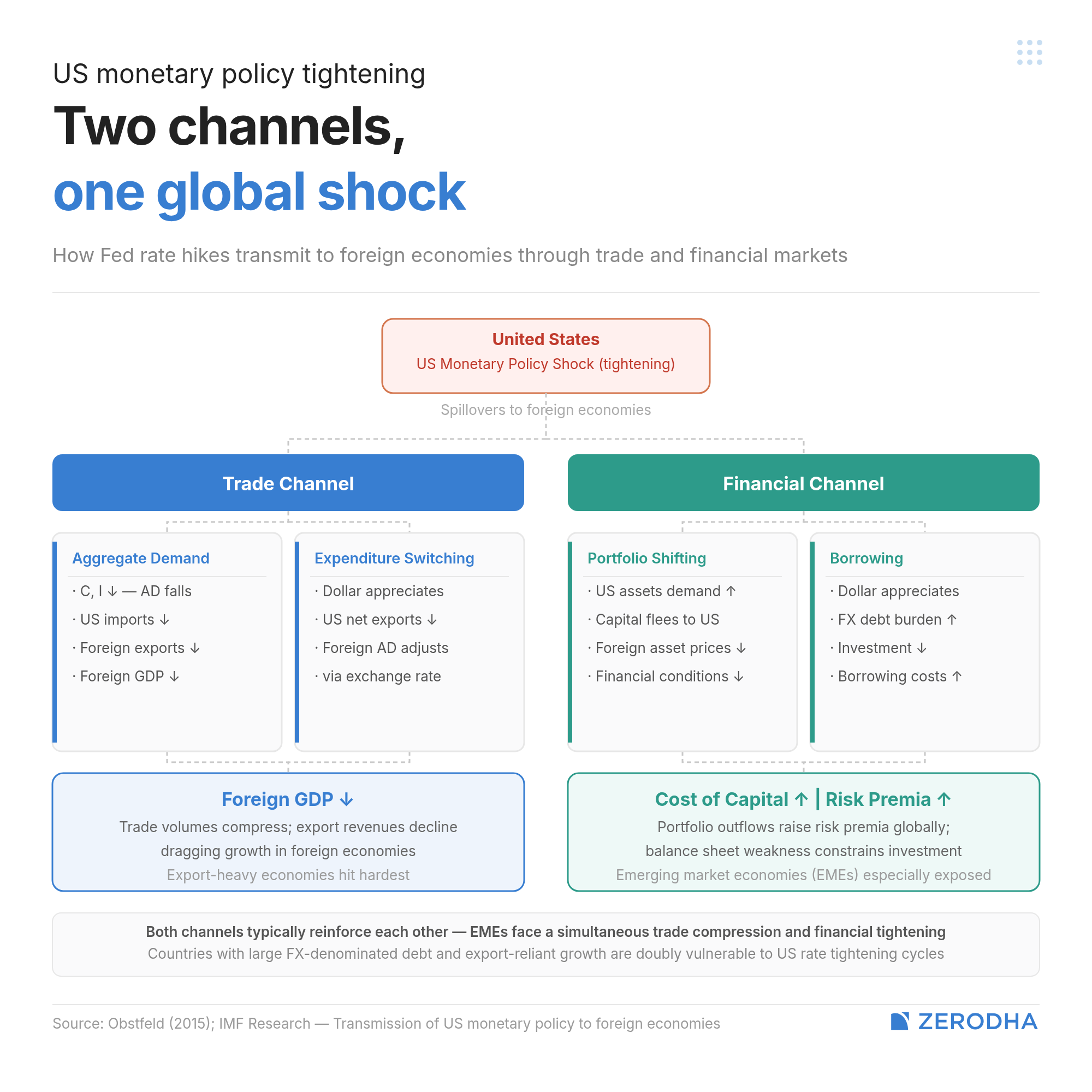

The US Fed sets the price of dollars, just like any central bank does for its own currency. One thing, however, sets it apart: the dollar is the currency of global trade and global finance. When its price changes, the effects ripple out across the world.

This does two things at once.

For one, it douses America’s appetite for trade. As dollars become harder to access, American households and businesses cut their spending, and their imports fall. Anyone that sells to Americans — which includes most of the world — takes a hit on their exports.

At the same time, something deeper, and stranger, starts happening in the financial markets. When the dollar becomes more expensive, you get more money for each dollar you invest. American bonds start paying higher yields. As money starts flowing into the United States, the dollar appreciates, making all other currencies look even worse in comparison. Meanwhile, anyone outside the United States that has borrowed money in dollars suffers.

The economist Hélène Rey called this the global financial cycle. As she noted, the world’s money flows as one. Because of this, the price of assets everywhere all across the world moves together — and the single biggest driver of that movement is what the US Fed does.

Between 2022 and 2024, in theory, this should have pulled capital away from emerging markets and into the dollar. So why did that not happen?

One of the best answers to this came from the economists Şebnem Kalemli-Özcan and Filiz Unsal. As they wrote, the world looked very different when these shocks came. For one, central banks across emerging markets had built genuine credibility over the last two decades. Where it was once assumed that they would embrace inflation to fuel growth, these suspicions had fallen off. On top of that, major emerging markets had sharply cut down private sector dollar debt. When the cycle turned again, emerging markets weren’t scrambling to defend their own currencies — they were simply fixing their own economies.

It was a good answer. But as the ECB paper argues, something else was happening too.

To understand that, one would have to look inside countries. Whenever you look at what’s happening to a country, as a whole, that’s an abstraction. Countries aren’t one thing. Inside any country, large financial shocks touch different people differently.

Speaking very roughly, any country has two kinds of money. Most of a country’s money sits in its territory alone. It is bound up in what people earn and spend, and in their assets — land, gold, bank deposits, and more. This is relatively insulated from global financial conditions. It feels second-order effects; through what happens to people’s jobs and wages when things change. But its value isn’t tied to a Fed signal.

But there’s a smaller pool of mobile money in the financial system. Much of this is directly plugged into the global financial system — through foreign investors, and people investing abroad. That is tied to the global financial cycle. It directly responds to financial signals coming from outside.

What sort of money you own often depends on how rich you are. If you’re living from paycheck to paycheck — largely spending what you earn that month — much of your wealth is probably of the first kind. But wealthier households are more likely to be plugged into global finance. They own more financial assets, watch the markets closely, and respond to signals from abroad. They’re more likely to shift their money according to how the Fed moves.

Now, here’s an interesting theory.

A country where wealth is very highly concentrated is one where people at the very top have a tremendous amount of surplus wealth, while everyone else lives on less. Those are the only people that are properly plugged into the global financial cycle. When the dollar starts appreciating, if those people buy dollar-denominated assets, they actually prosper. Meanwhile, everyone else takes the hit of worse economic conditions.

On the other hand, in a more egalitarian society, people have the means to respond to the dollar tightening. A lot more of their people are plugged into the financial markets. They have the ability to profit from the strength of the dollar. When the dollar appreciates, their own economies may take a beating, but any dollar wealth they create pushes in the opposite direction. Their pain is blunted by the mobile assets they own.

This, of course, was theory. But did it actually work? And what could that tell us about why countries reacted, as they did, to the Fed’s decisions. That’s what the ECB paper tries to study.

The puzzle

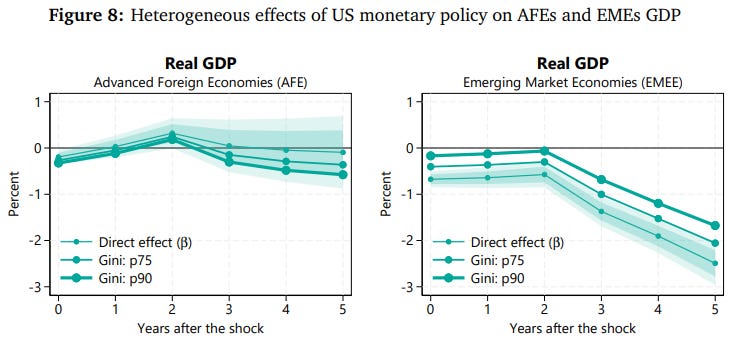

The paper looked at numbers from 87 different countries.

Their findings lined up with their intuition. Countries with higher income inequality see sharper contractions when the Fed tightens. When the global financial cycle is at its trough, the GDP of highly unequal countries falls one-and-a-half times as much as that of more egalitarian countries.

That much was expected.

But then, they split those countries between advanced economies and emerging markets, and their findings broke down. That pattern they expected only held for richer economies — like the United Kingdom, Australia, or the euro area. But once they got to emerging markets like India, Brazil or Indonesia, their findings flipped. The more inequality there is, the smaller the contraction they saw.

It would be a different matter if their entire theory broke. But why did these two groups see the opposite effect? Why did it seem, almost, as though inequality somehow protected emerging markets? Was there a piece we were missing?

To the paper’s authors, the difference came from how easily money could leave a country.

When the US Fed raises rates, and dollar investments grow more attractive, there’s a strong incentive to invest in the United States. Rationally, people would want to send their money there. But does that actually translate into outflows? That would depend on whether a country allows its capital to leave.

Most of the world’s advanced economies have open capital accounts. They allow money to freely enter and leave their territories. When the dollar appreciates, these countries see a flood of money heading out for US assets. That tightens their own financial conditions. Their equity markets fall and credit conditions tighten. Their central banks run into a bind: if they cut rates, capital could flee; if they raise rates, their economy suffers even more. The more concentrated the country’s wealth is, the worse things get.

But as you’ve probably seen first-hand, many emerging markets impose a tremendous amount of friction before their people can access foreign assets. To invest abroad, people must get around capital controls, brokerage costs, currency hedging gaps, weak investment infrastructure, and more. Their people are tempted by the same incentive, but it’s much harder to act on.

With all that friction, it is only the very wealthy that can buy dollar assets. When money is distributed all through the economy, practically nobody can do so.

This creates an air-gap between the country and foreign markets. And that buys their central banks some much-needed breathing room. The country’s central bank, no longer forced to defend its currency against capital flight, can actually cut rates and support the economy. The extra money that brings in simply goes into domestic bonds, or is consumed,

This adds more colour to what Kalemli-Özcan and Unsal had written. There were, in fact, two stories playing out at the same time. On one hand, emerging markets had earned more trust, and had reduced their dependence on foreign debt. At the same time, they kept their domestic capital pools within their territories, preventing them from amplifying these capital flows.

What changes for India

India sits in an interesting place in this picture. Our inequality, according to the paper, is in the very middle of the emerging markets they study. Our wealth isn’t as concentrated as Brazil or South Africa, but is more concentrated than Korea or Japan. Our capital account is partially open, and is opening further. Our Liberalised Remittance Scheme has loosened over time, and sees outflows of roughly $30 billion a year. GIFT City is only expanding our outbound investment options. Our government bonds are now part of global indices. Indian mutual funds with international exposure have grown.

In other words, our connection to the global financial cycle is increasing.

Twenty years ago, our exposure to the Fed’s decisions was simply a matter of how foreign investors behaved. With time, more domestic capital is engaged abroad. That makes our relationship with the world more complicated. There are, of course, many benefits to this openness. But it also changes what happens when the world’s next financial cycle comes around.

Tidbits

United Breweries to Exit Unprofitable States Amid Cost Surge

Kingfisher maker United Breweries, controlling 50% of India’s beer market, plans withdrawing from unprofitable states facing Rs 400-500 crore profitability hit due to glass, aluminium, fuel and logistics cost surge, while state pricing controls in Telangana and Tamil Nadu prevent price increases, with industry seeking 15-20% price hikes.

Source: ETAnthropic Secures SpaceX Data Center Deal, Doubles Claude Code Limits

Anthropic partnered with SpaceX to access 220,000+ Nvidia processors at the Memphis Colossus 1 facility, providing 300 megawatts capacity. This has enabled the doubling of rate limits for Claude Code paid plans, while unveiling AI “dreaming” feature for learning between sessions.

Source: ReutersApple Invests Rs 100 Crore in India Renewable Energy Expansion

Apple announced an initial investment of Rs 100 crore in India to develop over 150 MW renewable energy capacity with CleanMax, sufficient to power 150,000 households annually.

Source: ET

- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Pranay Kotasthane on Navigating the New Uncertain World

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Pranay Kotasthane, one of the sharpest minds we read to understand India and its place in the world. We’ve often featured his insights on this newsletter. This time around, we got him on for a long conversation — one that spans a wide breadth of topics: the world India now has to play in, why the panic around critical minerals is overdone, what’s actually holding back manufacturing, what an India-shaped opening in AI might look like, why Bengaluru feels as stuck as it does, and more. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉