Another fintech giant is going public

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Hello y’all. The Daily Brief turned one yesterday!

We put out our first ever video on July 2, 2024. Back then, we were just trying to convey the little we thought we understood about the markets. Nithin wanted something that would give him a quick wrap-up of what was happening in the markets, and while there was nothing we came across, this was a problem we thought we could solve.

Only, we had no idea how little we knew. And we had no idea how hard it was to comment intelligibly on the markets and the economy every single day. If we did, we never would have started The Daily Brief. Any labour of love, it turns out, is a mass of labour, with fleeting glimpses of love. If only we knew.

Be that as it may — we're deeply grateful we started this. For every single trading day in the last year, if the markets were open, we were here. This has been an educational marathon — in just the last week, we’ve studied everything from how waste is processed, to India’s raging cola wars, to the frontiers of the AI business. And we’ve now had 52 such weeks.

It’s been tiring. It’s also been the single greatest job one could possibly have.

It sometimes feels like we have no right doing something this fun. We aren't experts, after all. We are neither journalists nor economists. We neither give you breaking news, nor can we tell you something that nobody else has thought of.

We’re just nerds on a rampage, out to understand the world.

To us, the markets are utterly fascinating. They're the glue that holds 1.4 billion people together. Every day, hundreds of millions of people make tiny, personal decisions about their wants and needs. All of that chaos somehow comes together in a giant, elegant, economy-wide dance. We’re entranced by what we see, and that’s what we try to convey to you. If there's one thing we can promise, it is that we come to every topic with the love and fascination it deserves.

We know that our delight has reached at least some of you. And we cannot thank you enough for it. We'll keep showing up every day, for as long as you tune in. And on each of those days, we'll promise to stay fascinated.

Love,

Pranav

In today’s edition of The Daily Brief:

Behind the Pine Labs IPO

The New Age of Industrial Policy

Behind the Pine Labs IPO

It’s hard to overstate how dramatically India’s payment habits have changed in just a few years. A decade ago, you needed cash for most purchases. Today, you can even buy chai from a roadside stall by scanning a QR code.

This shift didn't happen overnight. It was built on the shoulders of numerous startups which found their ways around myriad inconveniences — from simplifying merchant onboarding, to creating sound-box speakers — all of which come together in our world-beating payments system.

Out of an estimated 75–80 million merchants in India, more than 60% now accept digital payments in some form. That share is expected to rise to over 80% in the next few years. Underpinning this is a massive layer of infrastructure which helps merchants accept digital payments, which are integrated seamlessly with their billing systems.

Still, only a small fraction of those – around 11% in 2024 – use more advanced checkout devices, like card-swiping machines or specialized payment terminals. There’s still headroom to bring more merchants into that fold. In fact, this number is expected to double by 2029.

That is where Pine Labs comes in. The company has just filed the offer documents for its IPO, giving us the chance to explore a new, fascinating niche.

The niche Pine Labs plays in

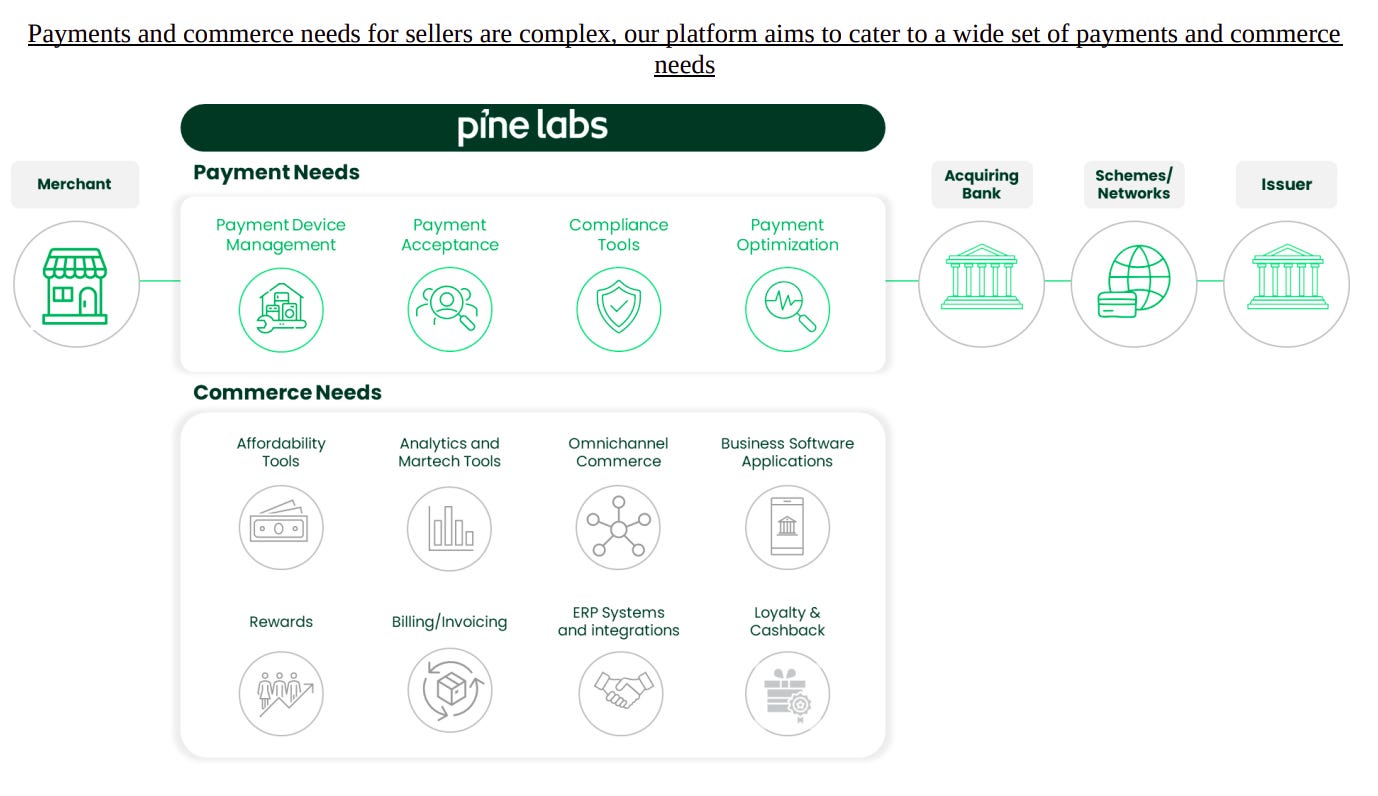

Pine Labs has carved out a unique spot for itself: it provides omnichannel merchant payment solutions.

In plain terms, Pine Labs gives stores the tech they need to accept payments both in-store and online. It also offers them a toolbox of extras to help them grow. The company’s software ties together various payment methods — both online and offline — into one seamless system for the merchant. In fact, if you’ve shopped at a large retail chain in India, there’s a good chance Pine Labs handled that transaction behind the scenes. They provide the small, white machine that probably processed your payments.

This makes them different from many household-name payment players you might use regularly. Paytm and PhonePe, for example, are in a different business — they’re primarily consumer-facing apps that allow quick payments through UPI and online wallets. None of them, according to the consulting firm Redseer, has as integrated a payment suite as Pine Labs does.

Pine Labs’ evolution is linked to how India’s overall payment landscape evolved.

The company began in the early 2000s, supplying merchants those “point of sales” (POS) machines and the software behind them. By the mid-2010s, it had baked “affordability” tools into its POS software — allowing you to pay in installments. This helped merchants boost sales while giving consumers flexible payment options.

Then, Pine Labs ventured into issuing gift cards. In 2019 it acquired Qwikcilver, a leading gift card platform, to enable businesses to issue prepaid cards, loyalty cards and digital gift coupons — like the ones offered by Croma or Westside.

Once it cemented its in-store offerings, Pine Labs set its sights on the online realm. It built out its payment gateway capabilities, allowing merchants to use Pine for in-store, app, or website payments.

Its latest foray came in 2022–23, when the company began to expand to smaller merchants more directly. This was aided by its investment in Mosambee, a startup that worked on enabling payment infrastructure for mom-and-pop shops.

Pine Labs’ set up

Pine Labs has two main business lines — each targeting a different piece of the checkout value chain.

Digital infrastructure and transaction platform

First is its core merchant-facing payments business. This covers everything from its POS terminals in stores, to the software that processes transactions and links wi

h banks. It also processes online payments processing, and offers a suite of merchant tools.

On top of this, it layers some useful “value-added” services — currency conversion for foreign cards, an analytics dashboards for sales, “pay later” / EMI options, and more.

For all this, Pine Labs typically earns fees, charging merchants for its devices and software — either upfront, or as a service subscription. It also takes a tiny cut or commission on the transactions it processes.

Issuing and acquiring platform

But there’s more. If a retail brand offers you a gift card, there’s a good chance Pine Labs’ platform is powering it behind the scenes.

Pine Labs’ second business line allows retailers to issue their own gift cards, loyalty programs, and digital wallets — and even internal employee rewards. It gives them a cloud-based system to create and manage these offerings.

It charges ‘program fees’ for these services. For example, a company might pay Pine Labs to run its gift card program. On top of that, when these gift cards or loyalty points are later used for transactions, Pine may take a small fee per transaction as well.

Generally, Pine earns through long-term contracts with large businesses. In that sense, it’s not unlike software-as-a-service (SaaS) businesses. Growth comes from scale — by signing up more brands and banks, or increasing the volume of cards and points in circulation. This has worked for them very well — in FY 2024, Pine Labs was the market leader in India for gift card issuance by value.

Where could this narrative fall apart?

But this story isn’t without its risks. There are several challenges that could test its success story.

It’s not profitable (yet)

Despite its growth, Pine Labs hasn’t yet seen a full year of profits. The company has consistently recorded net losses in recent years — it’s only between March and December last year that it finally saw some profit. In fact, for most of this time, has also had negative operating cash flow. The core business hasn’t started consistently creating cash.

This isn’t unusual for a fast-growing tech company. But eventually, the company needs to chart a path to consistent profits. While its recent move towards profitability is good news, there’s no guarantee that it’ll last. Until then, Pine Labs is relying on invested funds to fuel its expansion — and that can’t go on indefinitely.

A few big clients matter a lot

While Pine is spread across millions of merchants, not all of them matter as much to its books. A significant chunk of Pine Labs’ revenue comes from just its top 10 customers — who contributed 35% of the company’s revenue. If even one or two of these big clients were to scale down or leave, it could make a noticeable dent in Pine’s business, and derail its move to profitability.

Don’t forget the regulatory risks

Pine Labs works in the fintech and payments sector. And the shadow of the RBI, as we’ve written before, hangs heavy over the industry. While the regulator is moving towards taking a softer touch, it still holds the power to change the fortunes of any payments business overnight. Its rules can change in the space of a day, and that might impact how Pine Labs operates or how much it can charge. We’ve already seen that happen with PayTm Payments Bank and Slice.

The Financial Picture

Finally, let’s break down Pine Labs’ key numbers.

First, the positives.

According to its IPO filing, despite profits being somewhat elusive, Pine Labs’ revenue has been growing steadily. In 2024, the company logged revenues of about ₹1,208 crore. This was roughly a 24% jump from year prior, outpacing many traditional payment companies.

What drove this growth? Mainly, its core payments platform grew, as more merchants came on board and more transactions flowed through its systems. The issuing segment, on the other hand, was relatively flat — inching up only a couple of percentage points. The two business lines, clearly, are growing at very different speeds.

A lot of that revenue is spent on Pine Labs’ fixed and recurring costs.

The company has been investing heavily — in technology, sales expansion, and acquisitions — and those expenses can add up. The company’s "contribution margin" is improving — meaning that each transaction is profitable on a unit basis. But even as its unit economics gets better, its overall operational expenses remain high.

Nevertheless, the sheer volume of its business is impressive — and is expanding rapidly. By the end of 2024, the company had over 900,000 merchants onboard, boosted significantly by the smaller merchants it reached through its Mosambee acquisition. It handled a whopping ₹7.5 lakh crore in payment volume during just the first nine months of 2024.

The digital money flowing through Pine Labs’ systems, in short, is remarkable. But for all these strong metrics, the company doesn’t yet have a history of generating profits.

Conclusion

Pine Labs is at the centre of a huge growth opportunity. As payments in India continue to digitize, it is set to capture a lot of those money flows.

But there are countless companies that vie for the payments space — MSwipe, Ingenico, PhonePe, Razorpay, and many more. With just nine months of profit behind it, Pine Labs isn’t guaranteed to hold them off. If anything, payments infrastructure continues to become increasingly commoditized. Can investors realistically build a solid investment thesis for the sector?

What Pine Labs offers, right now, is promise. The surest path to success is building a defensible moat — and Pine Labs has a moat. What remains to be seen is if it can protect it.

The New Age of Industrial Policy

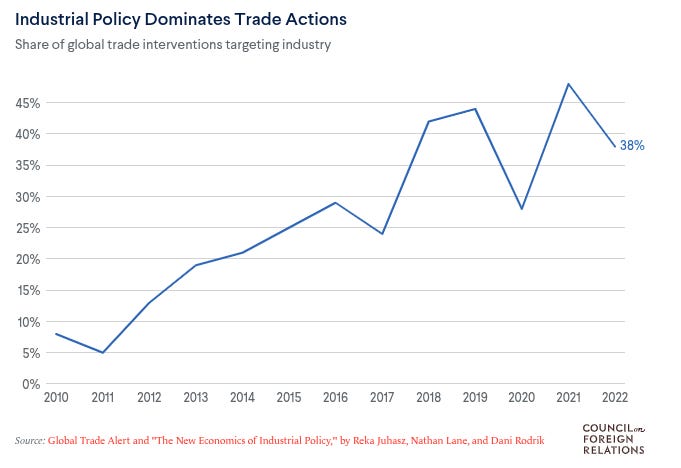

After decades when globalisation seemed inevitable, the world seems to be beating a retreat. Increasingly, countries are turning inwards, attempting to shore up production within their borders.

The most common way they’re pursuing this goal is through industrial policy. What is that? Put simply, it’s when a state uses the tools available to it — subsidies, cheap loans, tax breaks, tariffs, and more — to prop up parts of its industry.

India, of course, is no stranger to the idea. Our License-Raj, after all, was an experiment in trying to plan our way to prosperity. And echoes of that approach continue. Only yesterday, the state announced a scheme worth 1 lakh crore to boost research and development. You’ve probably also heard about our huge outlays for manufacturing-based incentives — although those have been called into question recently.

How should we think about these policies? When do they work, and when do they fall apart? And how is India navigating through them?

We went through a few recent papers — one from the IMF, one from the RAND Corporation, and one from the economist Nathan Lane — to help us explore these questions.

Why do states pursue industrial policy?

Industrial policy has always been a part of countries’ wider national strategies. Making your industry stronger is, at least in principle, a way of making your nation stronger. It comes with three big promises.

For one, industrial policy promises to stop large foreign businesses from rolling over you. The strongest case for this has to do with “infant industries”. A company is at its most vulnerable early in its life, when it is still building relationships and learning the ropes of its business. If, at this tender stage, it has to face off against a large, foreign business with strong networks and a deep well of experience, it could crumble under the pressure. That’s why countries throw up tariffs and import quotas — at least until their own industries have the maturity to survive.

Two, industrial policy helps your industries scale audacious challenges. While private markets take astute short-term risks, they shy away from funding long-term projects with no financial pay-offs in sight. Consider the challenge of creating an entire sector from scratch — it’s risky, and probably won’t yield returns for decades. The financial math makes no sense to a private investor. But a state that’s pursuing other rewards — like reducing foreign dependence — might be happy to provide subsidies and incentives.

When South Korea was trying to build its heavy chemicals industry (HCI), for instance, international agencies simply refused to fund their early efforts. The project seemed fool-hardy from a financial lens; Korea simply didn’t have a pre-existing advantage here. But the state then took over, and managed to create that advantage.

This is crucial if you’re solving pressing problems like climate change. There may simply be no money in many climate-related projects which are worth taking up. In these cases, governments — like China with its EVs — might be able to nudge markets in the right direction.

Most often, though, countries pursue industrial policy for national security and resilience. There are industries that have high social value, or where dependence on foreign companies can leave you vulnerable at the worst possible time. Consider defence manufacturing, for instance. If you depend on foreign powers for your arms, those supplies might be cut off exactly when you need them. Industrial policy promises to save you from that.

How do you get industrial policy to work?

But does this actually work? Well, it does… sometimes.

The IMF found that, on average, sectors that governments target with IP become more efficient and productive than those that do not.

There’s a catch, though. These gains are often short-lived, especially when subsidies go to inefficient firms. This isn’t to say that industrial policy can’t be successful — economist Nathan Lane, for instance, found that South Korea’s chevy chemicals industry doubled its output relative to non-targeted sectors. But these benefits aren’t guaranteed.

There are some choices, though, that can improve how well industrial policy works. Here is what it finds.

Export-orientedness.

Industrial policy tends to create globally competitive firms when it incentivises them for exports. It’s incredibly hard to get foreigners to buy your goods unless you deliver genuine value-for-money. Companies can’t afford to be lazy if they have to grow exports; they actually have to work for them. It is by targeting exports that South Korea, China, and Japan, for instance, created their industrial bases.

India, in contrast, illustrates what can go wrong if you ignore exports. Our approach to industrial policy has always been built around securing India’s huge market for our own companies. Through tariffs and quotas, we tend to stop Indians from importing things, so that they’re forced to give their business to Indian companies. Unfortunately, this just makes them lazy.

Consider this: in 2010, India and Vietnam had similar electronics export levels. Ten years later, Vietnam exported 9x as many electronics as we did. Why? Our protectionism is a big culprit.

Comparative advantage

Another big tool, if you want industrial policy to be successful, is to tailor it to your existing advantages.

Good industrial policies target industries that a nation already has some strength in. For instance, if you’re good at making batteries, you’re likely to do well at making things that use batteries — like smartphones, or EVs. China used this to great success.

Now, countries can create advantages from scratch. That’s what South Korea managed, when it built a heavy chemicals industry from nowhere. But that doesn’t come easy; it requires a massive, well-coordinated effort — run by bureaucrats with great skill. You can’t just hope that your policies create new industries out of nowhere.

Upstream vs. downstream

Finally, good industrial policy targets upstream sectors, which create the raw materials for other industries. If you manage to create a world-beating raw material producer, any industry that buys from it benefits too. Because South Korea mastered steel and other metals, for instance, that boosted their ability to make defense and electronic components. But as we’ll soon see, this can backfire.

The fundamentals

For industrial policy to really work, though, a nation needs to get its fundamentals right.

There are two ways to invest in a country’s growth. There are “horizontal” reforms, where you invest in things that strengthen the entire economy — like land reforms, infrastructure, education, or labor markets. And there are “vertical reforms”, where you target your policies at specific sectors.

The IMF finds that without horizontal reforms, vertical reforms usually fail. You can’t create world-beating sectors if the fundamentals of your economy are broken. Moreover, if it’s growth you’re chasing, Rupee for Rupee, horizontal reforms give you far better returns than vertical ones.

Take China’s AI policy, which appears to have seen some success. Underneath this policy, however, are fundamental advantages. China has a deep base of human capital skilled in computing, maths and science. It can build and connect power plants at scale. It has flourishing MSMEs, which drive 60% of its GDP. It is on the back of all this that it can target artificial intelligence.

If we adopted the very same policy, we might still fail, because we lack the fundamentals for it.

The costs of industrial policy

If you’re trying to spark more growth through industrial policy, these are important factors to keep in mind. Because industrial policy comes with costs.

Over-spending and mis-allocation

Industrial policy is expensive, and it is very easy to get wrong. If mistargeted, it may yield little — even negatively affect other industries — while still costing the full amount. You could find yourself burdened with too much debt, with little to show for it. Low-income nations are particularly at risk of this.

This is harder to manage than it seems. See, industrial policy often bears fruit over decades. Before they kick in, even good policies can seem wasteful. So, when do you stop funneling subsidies and sops to an industry? That line is often blurry.

There are two ways in which a government can make poor spending choices. It can mis-allocate its money within a sector, or between sectors:

Sometimes, you target the right sector, but the wrong company. Take China’s AI policy. While it has made gains as a whole, it wasted a lot of money on failed projects, and gave subsidized AI chips to badly run firms.

Sometimes, you can do everything right for one sector, at the expense of others. For instance, if you protect a sector too much, you could hurt everyone that buys from it. We saw this in our story on Indian steel recently, where the government, by protecting our steel industry from foreign players, made it harder for MSMEs to get raw material.

In short: the government is terrible at “picking” winners.

Why is this? For one, industrial policy is littered with “rent-seeking”. Whenever a government opens its purse strings, the stakes for businesses are massive. If one can just capture that government generosity, the benefits are disproportionate. This corrupts the entire process, as people learn to game the system.

In China, for instance, there’s a recurring problem of bureaucrats using industrial schemes to benefit themselves. South Korean chaebols, similarly, have built themselves around government largesse — tearing the economy into two tiers, with mega-corporations, which benefit from government sops, and a string of small, uncompetitive businesses which do not.

Geoeconomic costs

Finance isn’t the only cost involved, though.

By and large, countries expect each other to play fair when it comes to matters of trade. If you over-use subsidies or export incentives to manage your economy, that can anger trading partners. International organisations like the WTO, for instance, forbid many types of industrial policy. If you protect your industry too zealously, you can fuel a “tit-for-tat dynamic”, escalating trade tensions.

When the EU subsidised its champion airplane-maker, Airbus, for instance, it stemmed the growth of US-based Boeing. In response, the US subsidized Boeing. Both sides ended up dragging each other to the WTO, and slapping each other with tariffs — only to eventually call a truce when their squabble gave China the chance to catch up.

Episodes like this can come in the way of international cooperation. As countries feel threatened by each other, they try to bring supply chains back within their borders — which requires even more industrial policy. Countries can end up spending wastefully, while cutting down the market their firms can access — leaving everyone worse off.

India’s industrial ambitions

India has pursued industrial policy since our independence — trying everything from cheap loans to import tariffs. During the License-Raj, of course, we tried to manage our entire economy, leading to unmitigated disaster. But even after we reformed our economy in 1991, we have never stopped using industrial policy.

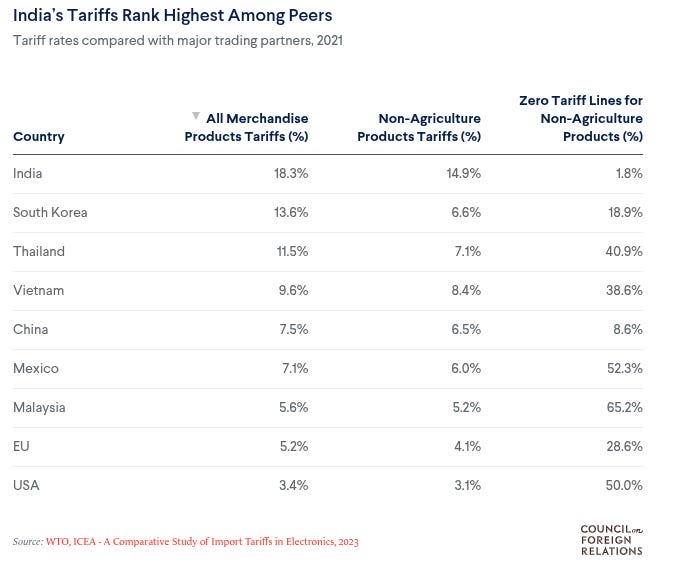

Consider this: even today, we have the highest import tariffs among our peers.

The results, of course, have been mixed.

Despite ambitious production-linked incentives (PLIs), for instance, manufacturing’s share in our economy in 2024 was exactly where it was in 2014 — at 17%. Only 2 out of the 14 sectors we targeted through these schemes actually took off. And even in electronics, one of our biggest success stories, China, Israel and Vietnam surpass us by far.

Why did we fail? Perhaps it’s because we didn’t have the funds to really solve this problem. But as we’ve spoken about before, our fundamentals need a lot of work. From the lack of cheap credit, to antiquated labour laws, to the high cost of logistics, we have severe horizontal problems, which keep us from taking off.

Meanwhile, there’s little coherence to our industrial policy. We’ve created schemes across industries that we don’t have an advantage in. Consider our subsidies for battery manufacturing — the scheme was launched three years ago, with an outlay of ₹18,000 crore. But there was no industrial base that the scheme plugged into. As a result, we’ve made little progress, while a measly ₹24 crore has been disbursed so far.

Audacious projects like this require an adaptable bureaucracy. Instead, our policies are marked by delays, red tape, and labyrinthine requirements. For now, our outlook to industrial policy continues to bear the mark of the “Licence Raj”.

In a nutshell, we’re trying, and failing, to pick winners.

Industrial policy is not going to go away anytime soon. And it has its uses. But such policies also carry costs. If we hope for any success, we will have to learn to absorb those costs sustainably.

TIDBITS

Updates to the topics we covered in our recent hospital story keep coming in. Fortis Healthcare's stock has risen 11% over three months, after the company said it will add 900 hospital beds next year. The company expects double-digit revenue growth in FY 2026 as more patients fill their hospitals and their diagnostics business performs better.

(Source)

We addressed why the Indian job market might be broken. But there is some good news. The Union Cabinet has approved the Employment Linked Incentive (ELI) Scheme with an allocation of ₹99,446 crore, aiming to create over 35 million jobs between August 2025 and July 2027. The scheme offers wage subsidies to first-time employees and financial incentives to employers, focusing on sectors like manufacturing and skill development.

(Source)

The Indian government has also given us reason to provide an update on our R&D story too. The Union Cabinet has approved the Research Development and Innovation (RDI) Scheme with a ₹1 lakh crore fund to boost private sector investment in strategic and sunrise sectors. The scheme offers long-term, low- or no-interest loans and equity support to foster innovation and technology adoption.

(Source)

And the developments to our monthly AI round-up never stops! HCLTech has entered a multi-year strategic partnership with OpenAI, marking a significant development in India's IT sector. This collaboration grants HCLTech direct access to OpenAI's advanced AI models, including ChatGPT Enterprise and APIs. These models will be integrated into HCLTech's platforms such as AI Force and AI Foundry, enabling the company to offer scalable AI solutions to enterprise clients across various industries

(Source)

Following up on our defense story, Reliance Defence, a subsidiary of Reliance Infrastructure, has partnered with U.S.-based Coastal Mechanics Inc. (CMI) to establish a ₹20,000 crore Maintenance, Repair, and Overhaul (MRO) facility in Nagpur. This joint venture aims to modernize and extend the life of over 100 Jaguar and MiG-29 fighter aircraft, 20 Apache attack helicopters, and L-70 air defence guns.

(Source)

It’s not just Reliance making moves in this space though. The Adani Group has acquired an 85.1% stake in Air Works India for ₹400 crore through its subsidiary, Adani Defence Systems and Technologies Ltd. Established in 1951, Air Works is India's largest privately-owned aircraft Maintenance, Repair, and Overhaul (MRO) company, operating in 35 cities with over 1,300 employees.

(Source)

- This edition of the newsletter was written by Kashish and Manie.

📚Join our book club

We've started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we'd love to have you along! Join in here.

🧑🏻💻Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We've been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls "polycrisis" thinking to connect the dots.

Frames for a Fractured Reality - We're struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze's "polycrisis" concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We're facing humanity's most profound identity crisis as AI matches our cognitive abilities. Using "disruption by default" as a frame, we assume AI reshapes everything rather than living in denial about job displacement that's already happening.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

A deep, heartfelt thank you to all of you who work daily to bring out this really stunning stuff. It's the first thing I read daily. It gives me a feeling that I am improving 1% regularly by going through this.

Thank you for keeping this going. I read every post. It is such a nice little habit. This is the type of social media I like. 👏