A record year for public-sector banks meets a turning point

Change and preparing for change are the only constants

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

A record year for public-sector banks meets a turning point

The meeting that cost 2.5 crores

A record year for public-sector banks meets a turning point

We covered private sector bank results this quarter, and PSU banks the quarter before. A reader of our newsletter wrote in asking if we’d round out the picture with Q4 PSU numbers. The answer, of course, was yes.

The story from last quarter was a show of strength like no other. Public-sector banks became more profitable (with SBI having its best-ever quarter), they began competing aggressively in the retail segment where private banks roam the land, and their asset quality improved.

However, certain risks flagged back then are coming into play now. For one, margins are compressing as the rate-cut cycle finally catches up. Secondly, deposit costs aren’t falling the way banks expected. And a new RBI accounting rule arriving in April 2027 is making every bank rethink their provisioning.

That’s what we’re seeing with the earnings calls of SBI, Bank of Baroda, PNB, and Union Bank.

The headline numbers

But before we explain what all of this means, let’s talk numbers.

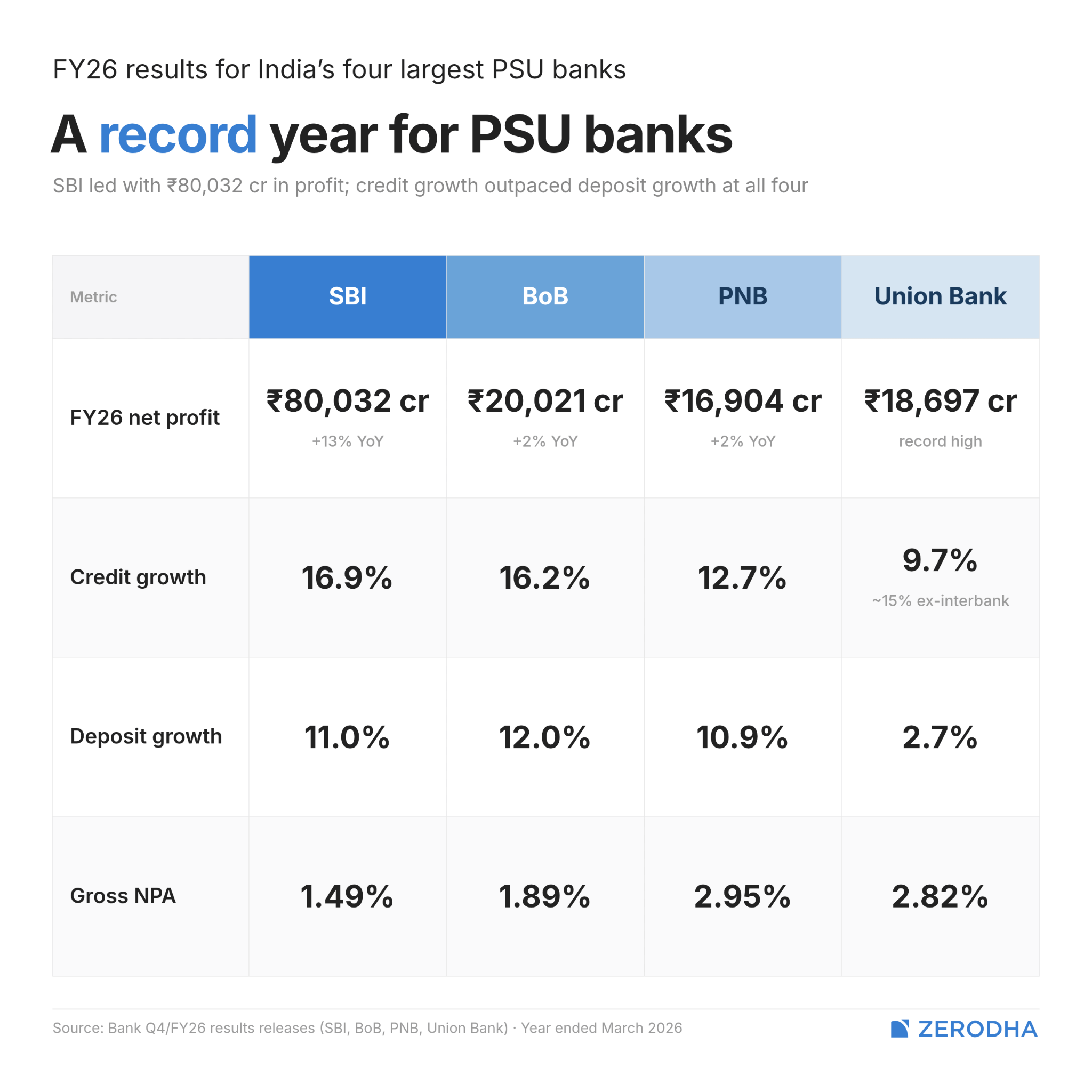

This has indeed been a record year for PSU banks. SBI made ₹80,032 crore for the year, up nearly 13%. Bank of Baroda crossed ₹20,000 crore in profit for the first time ever. PNB and Union Bank also both posted their highest-ever quarterly profit.

Credit grew by double digits at three of the four — SBI at 16.9%, BoB at 16.2%, and PNB at 12.7%. The outlier, Union Bank, is at 9.7%. But that’s because it sold off a large part of its under-performing inter-bank loans book. Excluding that, the underlying growth is closer to 15%.

But on the other side of the balance sheet, deposits grew slower everywhere — in the 9-12% range at three banks, and just 2.7% at Union Bank, which has been actively replacing bulk deposits with retail funding.

Asset quality is in good shape, with gross NPAs under 3% across the board, and net NPAs below 0.5% everywhere. Provision coverage — the share of bad loans for which banks have already set aside money — is 97% at PNB, 94% at BoB, and a more modest 74% at SBI. That last number will matter later.

PNB shared one statistic that captures how structural the shift has been: of the ₹12.46 lakh crore disbursed across all its loan books since July 2020, cumulative NPA is just 0.40% of disbursements. The mix has also shifted toward secured retail — BoB’s personal loans grew just 8.7%, well below the 19-20% growth in auto and mortgage, while SBI’s gold loan book grew 100% to cross ₹1 lakh crore.

Capital is also comfortable across the four, with capital adequacy ratios between 15% and 18%. None of the banks needed to raise fresh equity to fund growth.

The rate cut finally caught up

Now, let’s move on to the structural forces.

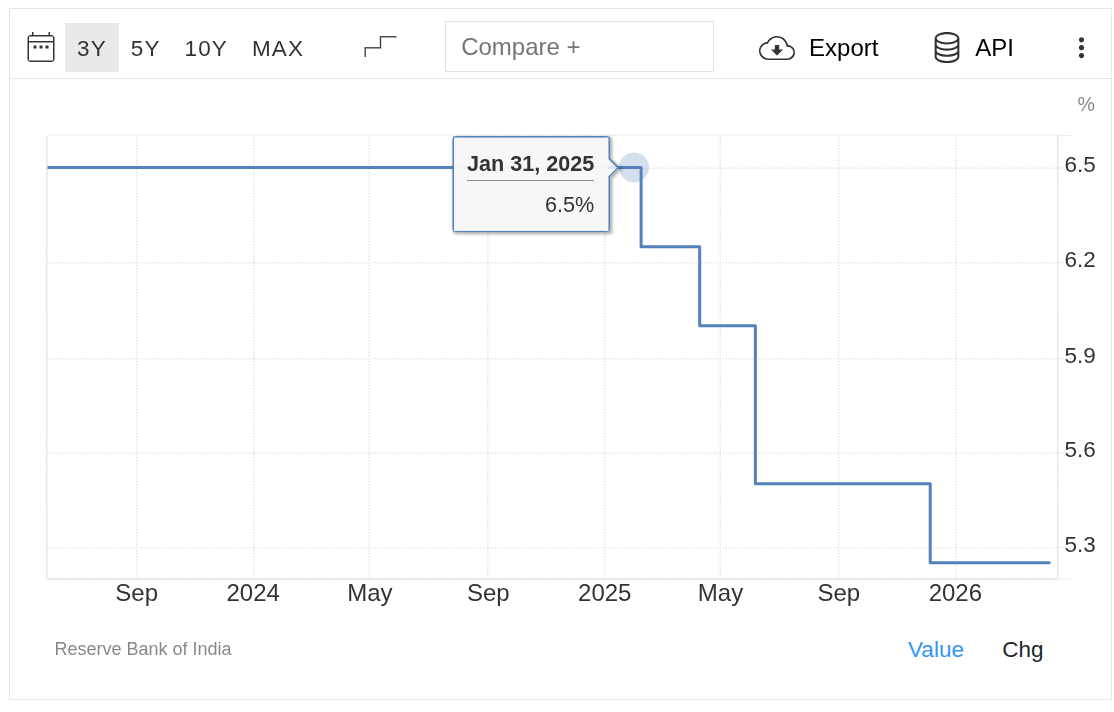

Between February and December 2025, the RBI cut the repo rate by a cumulative 125 basis points. The December cut landed mid-quarter, so Q3 only absorbed three weeks of impact, leaving Q4 to bear the full brunt.

That hit shows up in the net interest margins of the banks. And the mechanics of that are simple.

See, loans linked to the repo rate reprice within weeks of a rate change by RBI. But deposits move much more slowly. The rate a bank pays on your fixed deposit is locked in when you open it, so even after the RBI cuts rates, banks keep paying out at the older, higher rates until the FDs mature. They’re also slow to cut the rates advertised to new depositors, because customers will simply move their savings to whichever bank is still paying more.

So when the repo falls, asset yields drop first, and the cost of funds catches up gradually. The squeeze in between is what shows up as margin compression. And that showed up clearly in the banks’ numbers — enough to impact their outlook for the new fiscal year.

SBI’s domestic NIM came in at 3.03%, down from the 3.21% range earlier in the year. Bank of Baroda’s domestic NIM at 3.04% pushed management to mute its outlook for FY27’s margins to a 2.75-2.95% range. Union Bank’s full-bank NIM slipped from 2.91% a year ago to 2.70%. PNB took the deepest hit at 2.47%, missing its 2.8-2.9% guidance by enough that the bank had to temper its expectations for the year ahead.

But what made Q4 harder than the rate cut alone would suggest is a story that PSU banks have been absorbing for the last two years.

The T-bill trap

For a while, public sector banks have been facing a margin problem in their corporate loan book. During the low-rate period of 2020–22, top-rated companies had strong bargaining power because banks were competing to lend to them. They used that power to push banks to price their loans using Treasury bill (T-bill) yields instead of MCLR, which is a bank’s internal lending benchmark.

That push effectively changed the banks’ control of their own margins.

How so? Well, MCLR is a bank’s internal lending benchmark. It usually falls only when the bank cuts its own deposit rates. MCLR-linked loans only reprice every six or twelve months, and only if the bank touches deposit card rates. But T-bill yields move more directly with market rates. T-bill linked loans reprice within days of any change in the underlying yield, which itself tracks the repo.

That means that, in a falling rate cycle (like recently), the T-bill linkage is dramatically better for a borrower because it automatically lowers rates. But banks get squeezed.

In SBI, for instance, the share of EBLR-plus-floating-rate loans (or loans linked to external benchmarks) in its corporate book moved from 43% to 49% in Q4 alone, with most of the incremental growth T-bill linked. Bank of Baroda acknowledged the same dynamic.

The strategy at both banks now is to convert these T-bill linked corporate loans back to MCLR at renewal to protect margins. What also helps is that the next leg of corporate growth banks are gunning for — like data centres, battery storage, transmission, etc — typically requires structured composite financing rather than standard term loans, which could give banks more pricing flexibility at renewal.

The deposit wall isn’t budging

If lending rates didn’t help, neither did deposits. BoB’s management called the cost of deposits “sticky”, while PNB said deposit rates remained elevated through April with little sign of moderation.

The strategic response is identical at all four banks: shift composition. Move from bulk deposits, where the cost touches 7-8%, to retail term deposits and the current and savings account base (CASA), which is the cheapest funding any bank can raise.

SBI and BoB nudged CASA up modestly. Union Bank stood out, lifting CASA 2.7 percentage points in six months while shedding about ₹70,000 crore of bulk deposits in the process. PNB was the laggard, as CASA was stuck at roughly 37% for four straight quarters — not what management had hoped for.

The deeper challenge is that while composition is improving, the level of cost isn’t. Retail term deposit competition has intensified across both PSU and private banks. Deposit rates do eventually catch up with repo cuts, but typically with a lag of another quarter or two.

The ECL countdown

From April 1, 2027, the RBI’s Expected Credit Loss framework, which we covered a few months ago, kicks in.

Today, banks provision for losses only once stress shows up — a loan turns into an NPA, then provisioning follows. But under ECL, banks will have to provision for forward-looking expected losses across the entire book, including loans that look perfectly healthy today but might go bad in the next few years.

Every CEO on these calls declined to quantify the impact of ECL. The closest anyone came was BoB, where management said an earlier estimate of roughly an 18 basis point impact on credit cost still seems aligned. Union Bank said that its earlier estimate of around ₹4,300 crore in one-time transition shortfall still holds. SBI and PNB only said that the transition would be smooth and manageable.

However, banks did build buffers accordingly. BoB created a ₹1,500 crore floating provision in Q4 alone. Union Bank set aside ₹700 crore. PNB added ₹270 crore to take its total floating provision to ₹2,045 crore. SBI didn’t add a fresh provision but, by one analyst’s count on the call, it already carries about ₹29-30,000 crore of buffer.

All four banks said the same thing: these buffers aren’t specifically for ECL, just general cushions. But doing it right before the transition year, plus the refusal to quantify the ECL impact, tells you that they are made for ECL itself.

This is also where the variation in coverage ratios matters. PNB and BoB at 97% and 94% have already set aside money against almost all their bad loans, so they have less to do under ECL. SBI at 74% has more catching up to do, which is why its large buffer matters.

The watch list

Of course, beyond the balance sheet, the West Asia situation came up on every call.

Across banks, India’s largest ceramics cluster in Morbi, Gujarat, came up more than once, hit by higher commercial gas prices that have made production uneconomic for smaller units. Remittance flows have softened. Banks are certainly going to be watchful of the situation over the year.

But as of yet, nothing structurally broke for any bank because of the crisis.

Part of it is because of a new cushion. The government launched ECLGS 5.0, a new ₹2.5 lakh crore credit guarantee scheme aimed at MSMEs in stressed sectors, with a separate ₹5,000 crore carve-out for airlines. Under ECLGS, the government takes the credit risk on covered loans, which lets banks lend to stressed segments without worrying about the asset quality hit. SBI says its customers qualify for up to ₹70-80,000 crore under the scheme, but expects only 30-40% of that to actually be drawn.

The year forward?

What FY27 will test is whether the structural improvements are deep enough to absorb three adjustments at once. One is NIMs settling at a lower base than the cycle peak. Second is the ECL framework arriving in the fourth quarter, and lastly, whatever the geopolitical environment delivers.

Most of the fundamentals seem, from the buffers to the loan book, seem solid enough to withstand all these forces. They’ve had a great year, which they’ve also used to prepare for these conditions.

But the question is what the new steady-state looks like once the cycle settles. Will domestic NIMs stabilize around 2.5-3%, or trend lower as the corporate book continues to lean external-benchmark? When ECL actually arrives, will the impact prove smaller than the buffers being stockpiled — and if so, what gets done with the excess?

The meeting that cost 2.5 crores

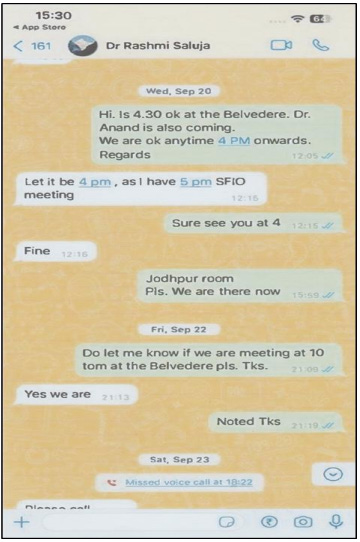

It was the afternoon of September 20, 2023.

Three people sat down at a table at The Oberoi in Delhi. The hotel was booked in the name of Dr. Anand Burman, the chairman of Dabur, who had flown into India just for that meeting. Across him was Dr. Rashmi Saluja, then the Executive Chairperson of Religare Enterprises. Along with Burman was Arjun Lamba, a representative of the Burman Group.

That the meeting happened is not in dispute. There were mobile tower records, hotel invoices, and WhatsApp messages: all showing a meeting scheduled between Saluja and Lamba, with Burman added at the last minute.

What did they talk about, however? That’s at the heart of SEBI’s final order in a major insider trading investigation.

According to Burman and Lamba, they were telling Saluja how the Burmans were five days away from announcing an open offer to take control of Religare. According to Saluja, they discussed something else — a possible directorship for Lamba, and her own future as chairperson.

Either way, the next morning, Saluja sold ₹17.45 crore worth of Religare shares. Then, the morning after, she sold another ₹17.25 crore. Four days later, an open offer was announced, and Religare’s stock dropped 7%.

A bid to control Religare

Dr. Rashmi Saluja had run Religare since early 2020. She joined the board in December 2018, became its independent chairperson the following June, and was elevated to Executive Chairperson in February 2020. This wasn’t a tiny business; it was a behemoth — a non-banking finance company, listed on both major exchanges, with subsidiaries in lending, insurance, and broking — the most valuable being Care Health Insurance.

The Burman family, meanwhile, were the promoters of Dabur. They had quietly been buying Religare shares for years through four different investment vehicles. By the end of June 2023, they collectively held about 14% of the company. Midway through August, three of those entities bought another 7.5% in a single block deal worth ₹534 crore. Suddenly, the family owned roughly 21% of Religare — making them the company’s largest shareholder by a wide margin.

The deal also brought them just shy of a regulatory threshold. Under Indian law, anyone that acquires 25% or more of a listed company has to make an “open offer”: inviting any of the remaining shareholders to sell their shares as well, at a fixed price. After all, it’s hardly fair if you bought shares in a company trusting one management, only to find that someone else sneakily took over the company.

On the morning of September 25, 2023, the Burmans announced such an offer: they would buy an additional 26% of Religare, at ₹235 per share.

Only, on the previous trading day, the stock had closed at almost ₹272. The Burmans’ offer was 13.5% below the market.

The price had been set by a regulatory formula. The law takes many inputs into account while setting the price for an open offer. That formula threw up a price of ₹218. The Burmans’ price of ₹235 was a small bump above the floor, but it was well below where the market had pushed the stock after weeks of takeover speculation.

If you knew that an offer was coming, in theory, this was a good reason to get out of the stock. Its price had been pumped up by rumours. The Burman’s bid would land below market price. Anyone that didn’t sell would hold part of a company controlled by someone that had just declared a low valuation. The stock would reprice toward the floor.

That is roughly what happened. On the day of the announcement, Religare closed at ~₹253 — down almost 7%. The next day, it dropped to just over ₹245. It would drift downwards for the next month and a half.

What do we know

Was that why Dr. Saluja sold her stock, though?

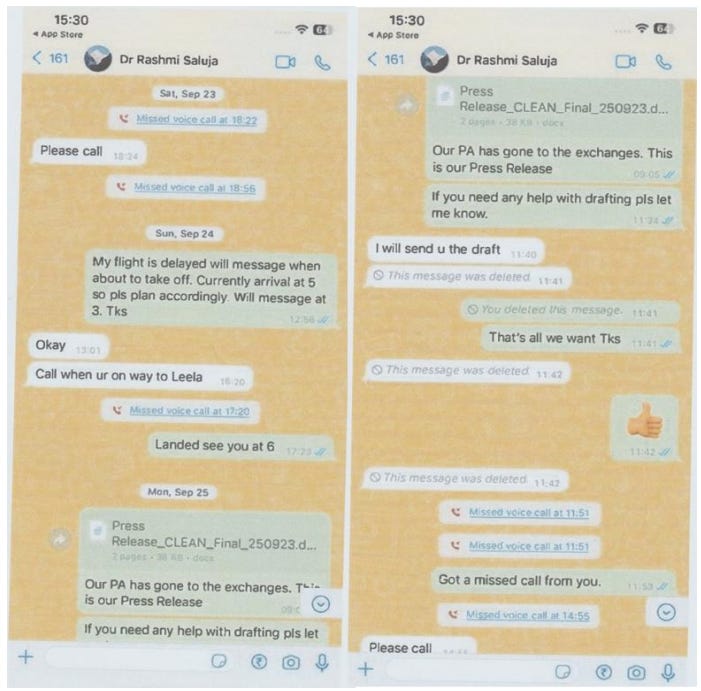

It’s impossible to know beyond a doubt. There was no record of what they spoke about, at their meeting at The Oberoi. They didn’t exchange any messages writing down what was said. All SEBI had were fragments.

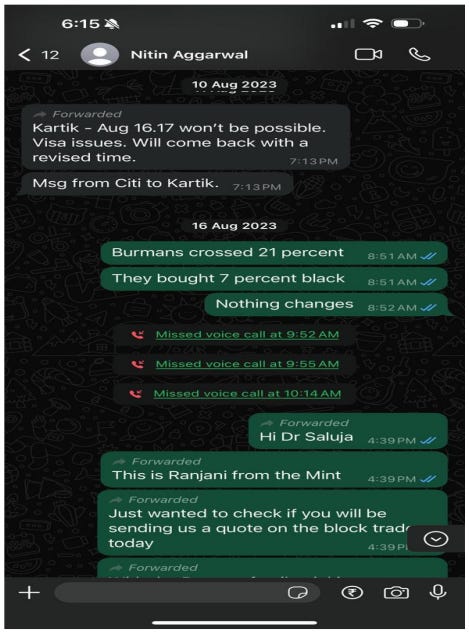

The first fragments were from August. By then, the Burmans’ acquisition was visible in the market. On August 16, when the block deal went through, Saluja messaged her CFO about the Burmans crossing 21%.

That very afternoon, she sent Burman himself a congratulatory message: “It’s a great strength to us.“

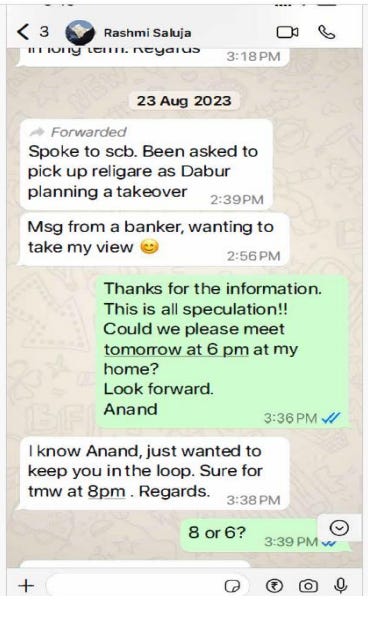

Then, a week later, Saluja forwarded a banker’s message to Burman and Lamba, speculating about Dabur planning a takeover of Religare. Both replied claiming it was all “speculation”, but anyone could tell that something was afoot.

The three met at The Oberoi, late in August. At that time, they told her that the Burman family had no open offer plans. And then came the fated meeting on September 20.

Interestingly, her decision to sell her shares came before the meeting. At 11:08 AM, Saluja had applied to Religare’s compliance officer for pre-clearance to sell 15 lakh of her own Religare shares. Clearance came through at 11:26 AM. Not only had she not met Dr. Burman at this point — this was an hour before she even knew he would be at the meeting.

That evening, they all met. What happened at the meeting, though, is unclear. Dr. Burman claimed he came to India specifically for this conversation, because of the significance of what he would convey. They met for around 45 minutes. That was when, according to his affidavit, Dr. Burman informed Saluja of the family’s intention to launch the offer. Lamba, too, confirmed this version of the facts.

Dr. Saluja claims that things went differently. The meeting, she says, was about a nominee directorship. The Burmans, she claimed, wanted Lamba on Religare’s board. She told Burman that Lamba lacked merit, and Dr. Burman should come on the board himself. To her, there was no mention of an open offer.

The next morning, however, she sold 6.53 lakh Religare shares on the exchange, at just above ₹267. That was 14% of the trading in Religare stock on the NSE, that day. The morning after, she sold another 6.40 lakh shares at around ₹270. This, again, was 14.5% of the Religare trading the NSE saw that day. In all, she had made almost ₹35 crore over those two days.

These two days were the only days she traded on the exchange in the seven months SEBI investigated.

Then, the open offer was announced. Religare’s stock dropped 7% by close. Saluja messaged Lamba that day, talking about Religare’s official press release. None of her messages expressed any surprise at the open offer.

The defence

That was the evidence SEBI went on to accuse Saluja of insider trading. Saluja, however, had a different version of the events.

The spine of her argument was the pre-clearance she sought. There was a clear record of her telling her own compliance officer, in writing, that she would sell her shares. This was before she knew she would be meeting Dr. Burman that evening.

By all accounts, she needed that money. On October 3, less than two weeks after the share sale, she exercised stock options in Care Health Insurance, Religare’s unlisted insurance subsidiary, for just over ₹39 crore. She still holds those shares. If she really thought the Burman takeover would tank Religare’s shares — and eventually end her own tenure at the company — why pour the proceeds straight back into one of its subsidiaries?

This case sat in a wider context. The Burman’s takeover would soon be awash in corporate intrigue. Many parties would get involved in the ugliness, making accusations and counter-accusations. Many regulators would scrutinise the deal. This insider trading complaint, too, would emerge out of this churn.

Could you then trust it? Could you sustain the case based on a statement by Burman and Lamba, who were part of the corporate ugliness? They were the ones that supposedly conveyed secret information to her. Was it fair to charge her on their own testimony?

There were many other defences she would put up. Could SEBI really be sure?

How SEBI landed it

SEBI doesn’t claim certainty that she traded on insider information. But it didn’t have to.

SEBI was effectively arguing one thing: that Dr. Saluja was in possession of insider information. If that was the case, and she traded on it, she would have gone against the law. That was all they had to prove: that she had information.

Unlike a criminal case, it didn’t have to prove this beyond any reasonable doubt. It just had to show the “preponderance of probability” indicated that she did. If all the facts, taken together, suggested that she was more likely than not to have this information, SEBI’s case would be through.

At this legal standard, SEBI’s fragments alone would do the job, if stitched together well enough.

SEBI could claim, for instance, that it didn’t matter if she got a pre-clearance for her trades. After all, when she did so, she had to promise to her compliance officer that she would not make those trades if she came into possession of inside information. It was all conditioned on her continued ignorance.

It also didn’t matter if she invested that money into Care Health. She may have done so anyway if, back then, in early October, she still believed she could manage the transition with the Burmans. It may have been a naive investment, but it wasn’t evidence that she was innocent.

SEBI came with WhatsApp records, the mobile tower data, the hotel invoices and the trading pattern. That, it believes, was enough to make the case stick.

The order

SEBI has now ordered that Dr. Saluja disgorge almost ₹2 crores — the difference between what she got for her shares on September 21 and 22, and what she would have got if she had sold after the open offer was announced.

Additionally, a penalty of ₹40 lakh was imposed on her. It was legally allowed to penalise her by as much as ₹25 crore. The ₹40 lakh, in comparison, seems like a minor amount. It hasn’t tagged on any further punishments: there’s no market debarment, and no prohibition on holding more directorships.

The long saga of corporate intrigue, meanwhile, carries on.

In February 2025, Religare’s shareholders voted Saluja out of the company. About 97% of the votes cast were against her reappointment. She left its board on February 7. The Burman family completed their open offer, became Religare’s new promoters, and reshuffled the board.

Arjun Lamba, whose sworn testimony was the spine of the insider trading finding, was appointed an Executive Director of the company earlier this month.

Tidbits

The Securities and Exchange Board of India (SEBI) on Thursday proposed a wide-ranging overhaul of regulations governing exchange-traded derivatives, including commodity derivatives, aimed at simplifying compliance requirements and reducing duplication for exchanges and clearing corporations.

Source: Hindu BusinessLineAir India posted a loss of S$3.56 billion, or about $2.8 billion at current exchange rates, in 2025-26, Reuters reported, citing the annual financial statements released by Singapore Airlines on Thursday. The loss marks Air India’s biggest annual loss since the airline was acquired by the Tata Group in 2022.

Source: Business StandardThe Indian rupee fell to an all-time low on Thursday, pressured by stubbornly high oil prices and persistent portfolio outflows that have strained the current and capital balances of Asia’s third-largest economy. The rupee fell 0.2% to 95.9575 per U.S. dollar, eclipsing its previous record low of 95.7950 hit on Wednesday. It closed at 95.7625, down marginally from its previous close.

Source: Reuters

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Your story from Apr. 11, 2025 discusses why state banks are seeing late margin compression compared to pvt. banks (share of MCLR-linked loans are much higher in state banks)

Thanks