Who said what about The Fall of the US, Bonds vs Stocks, and Recession Warnings

Hello, I’m Kashish Kapoor and welcome to Who said what?—the show where we dive into interesting comments from notable figures across the world, whether in finance or the broader business world, and explore the stories behind them.

I’m filling in for Krishna this week. Now, I know I’m not nearly as quirky or sarcastic as he is, but I’ll do my best—so go easy on me.

Last week, Krishna took you through some of the most memorable quotes from Indian business leaders.

This time, I’m flipping the script.

Today, we’ll explore what global heavyweights like Jamie Dimon, Howard Marks, and Aswath Damodaran have been saying lately—and why it matters.

Let’s get started.

Jamie Dimon has a few things to say

Jamie Dimon, the CEO of JPMorgan, recently published his annual letter to shareholders. And it’s quite long. He talks about so many things but here, I want to focus on the five things that really stood out to me.

1. Geopolitics and National Security

Here’s how Jamie starts that section. He says:

“We face the most perilous and complex geopolitical landscape since World War II.”

Now that’s not just dramatic—it’s very deliberate. He’s saying the world today is more dangerous and unpredictable than it has been in nearly 80 years.

Why? Because a lot of the global systems that kept things stable for decades—like NATO, the United Nations, trade deals, and military alliances—are being tested. He writes:

Hegemony basically means dominance. In this case, American leadership in global politics and economics. And Jamie’s warning that countries like Russia, China, Iran, and North Korea want to break the global order that the U.S. helped build after World War II. That order made trade smoother, kept wars at bay, and gave the world a framework to work together.

But now—with the war in Ukraine, conflict in the Middle East, cyberattacks, terrorism, and growing military power in China—he’s worried that we’re moving into a world where every country is out for itself.

And he says the link between economic power and military power is tighter than ever:

“We must recognize that economic warfare often precedes military warfare.”

So if America loses its economic edge—its technology, its trade relationships, its energy independence—then it also becomes more vulnerable militarily. And that, for Jamie, is the real danger.

2. Inflation, Interest Rates—and the Risk of Stagflation

Here’s where things get really interesting. Jamie says:

Translation? Inflation isn’t done yet.

Let’s go back to basics. Inflation means prices going up—your groceries, your rent, your fuel. And to control that, central banks raise interest rates—making loans more expensive, which - they hope - slows down spending.

Most people assume that inflation will soon fall and rates will come down. But Jamie’s not so sure.

Why? Because there’s a lot of money being spent on things like rebuilding supply chains, investing in clean energy, expanding the military, and reshoring industries back to the U.S. All of that is good in the long run—but it pushes prices up in the short term.

And then comes the word that really matters: stagflation.

He doesn’t shout it, but he warns that it’s a possibility. Here’s what he writes:

Stagflation is a nightmare scenario: high inflation, but low growth. Your salary doesn’t go up, but prices do. And that’s incredibly hard to fix—because if you raise interest rates to control inflation, you hurt growth even more.

Jamie’s warning that this could be where we’re headed if we’re not careful.

3. America’s Fiscal Position: A Giant Warning Sign

This is where Jamie sounds the loudest alarm. He says:

“Profligate fiscal management has led to huge deficits and bad outcomes.”

Now, “profligate” just means reckless spending. And by deficit, he means the government is spending way more than it earns—almost $2 trillion in 2023 alone.

Jamie isn’t just saying we spend too much. He’s saying we spend poorly.

That’s half a trillion dollars of taxpayer money that may never come back. And it’s just one example. He also talks about how we treat infrastructure like an expense—rather than an investment—and how both parties keep kicking the can down the road.

Then he drops this chilling line:

In other words, if foreign investors lose faith in America’s ability to manage its finances, they could pull out. That would raise borrowing costs, weaken the dollar, and shake up the entire economy.

4. On China’s Economic Strategy vs. America’s

Jamie doesn’t sugarcoat things here. He says:

Let me explain what that means. See, China has been playing a long game. It’s invested heavily in infrastructure, dominated global manufacturing, secured control over critical minerals, and expanded its influence in Asia, Africa, and Latin America.

But Jamie isn’t blindly praising China. In fact, he talks about their weaknesses too—like a real estate crisis, an aging population, and tight government control that sometimes hurts innovation.

Still, he’s making a bigger point: China is strategic. And America can’t afford to be complacent. He writes:

“We do not need to fear China—we just need to get our act together.”

That means: fix their roads, invest in clean energy, support science and research, and rebuild manufacturing. He believes America has the better hand—we have energy, innovation, strong private companies, and a culture of entrepreneurship. But they are not using that hand wisely.

5. On Tariffs and Global Trade

Jamie gets pretty detailed here—and a bit critical. He says:

Let’s simplify that.

Trade is how countries buy and sell from each other. America used to lead global trade efforts—signing big trade deals and opening markets. But in recent years, it’s pulled back. And while that was meant to protect American workers, it also created a vacuum. Countries like China have stepped in and signed more trade deals globally.

Jamie’s not saying we should go back to free trade at all costs. But he’s also warning against going too far in the other direction. Because when governments overuse tariffs or subsidies—essentially putting taxes on imports or giving handouts to local businesses—it can mess with the economy.

He puts it like this:

In other words, if everyone starts lobbying for their own special subsidy, the whole economy gets bloated and inefficient.

He also links trade to debt. Over the last 20 years, America has run a $12 trillion trade deficit. That means they’ve bought way more from the world than they’ve sold. And to pay for that, they’ve borrowed.

“Foreign investors now own $30 trillion of U.S. securities—up from $6.3 trillion in 2005.”

That’s a big number. And it means that other countries have more financial control over the U.S. than ever before. If they stop buying their debt, the whole system could wobble.

There are so many more things that he talks about which I haven’t even touched upon here, it’s definitely worth checking out. Here’s the link to the newsletter.

Howard Marks on the current market

A month ago, Howard Marks — the legendary investor and co-founder of Oaktree Capital — wrote a memo saying that credit (like bonds and loans) looked more attractive than stocks. And then… the world turned upside down.

Tariffs were slapped on. Stock markets fell sharply. And the economic order that had more or less held steady for decades? That’s now looking shaky. He recently gave an interview to Bloomberg to talk about all this. And what he said was striking.

“This is the biggest change in the environment that I’ve seen probably in my career.”

From Global to Local

For most of the past 80 years — especially after World War II — the world economy moved toward globalization. Countries became more connected. Trade grew. Goods became cheaper. And, as Marks says, that lifted almost everyone’s standard of living.

“The Italians make the pasta. The Swiss make the watches.”

It’s a simple way to describe a big idea: Every country does what it’s best at and trades with others for the rest. That system worked well for decades.

But now, that’s changing.

With new tariffs and a more protectionist tone from major countries, especially the U.S., Marks says we’re moving toward a world that’s more closed off — where countries want to make more things themselves. That might sound patriotic, but it also means one thing:

Higher prices. And more inflation.

The Inflation Problem

Marks explains it like this: for 25 years, prices of things like TVs, washing machines, and other durable goods in the U.S. actually fell by 40% after adjusting for inflation. That’s because so many of them were imported cheaply from abroad.

Without globalization, that benefit disappears.

“If we don’t have world trade, we don’t have that benefit.”

So yes, tariffs might help some local industries. But they also make everyday goods more expensive — and that’s not good for consumers or inflation.

Why Credit Still Looks Better Than Stocks

Despite all this turmoil, Marks still believes that credit looks like the better bet. Six weeks ago, high-yield bonds (which are riskier but offer higher returns) were giving 7.2% annually. Now they’re closer to 8%. And unlike stocks, these investments come with a specific promise: you’ll get paid back with interest — unless the borrower defaults.

“With debt… what you see is what you get.”

In 47 years of investing in non-investment grade (i.e. risky) bonds, Marks says 99% of the companies he lent to paid him back. That’s a solid track record. And it's a level of predictability he doesn't think stocks can offer right now.

Don’t Count on 10% From Stocks

There’s a popular belief that stocks give 10% returns over the long run. But Marks points out that this average only holds true under certain conditions — like when stock prices (measured by something called the price-to-earnings ratio or P/E) are at normal levels.

Today, the P/E ratio is high. So history tells us that future returns may be much lower — somewhere between 2% and 7% a year.

“You shouldn’t expect historic returns.”

In other words, stocks might not be the sure thing people think they are.

Is This the Time to Buy? Or Run?

With stocks falling and prices looking cheaper, should you be buying?

“Bloomingdale’s just put everything on sale.”

Marks says that’s what’s happening in the stock market — things are cheaper. But just because prices are lower doesn’t mean they’ve hit bottom. And there’s no way to measure whether they have. The world is too uncertain.

“It’s like a snow globe. Everything’s been shaken up.”

Is America Still the Best Place to Invest?

Marks says yes — but with caution.

The U.S. still has a strong economy. But he’s worried about some changes. For example, the rule of law might not feel as strong. Outcomes are less predictable. And most of all, America keeps piling on debt.

He compares it to someone with a golden credit card:

“There’s no credit limit. The bill never comes.”

That’s how the U.S. has behaved. But if investors around the world lose confidence — in the dollar, in U.S. Treasury bonds, or in the government’s discipline — then that bill might finally come due. And that would be serious.

So What Now?

Marks doesn’t offer simple answers. But he does offer perspective.

When markets fall, most people panic and run. But that’s exactly when great investors start looking closely. As he says, it makes no sense to say:

“‘I bought it when it was ₹100, now it’s ₹90, so I’m not buying anymore.’”

If anything, that’s the time to pay attention — even if it’s scary.

Because in a world that feels like a snow globe, the one thing investors can do is stay calm, think clearly, and look for the opportunities that all that chaos leaves behind.

Aswath Damodaran on crisis

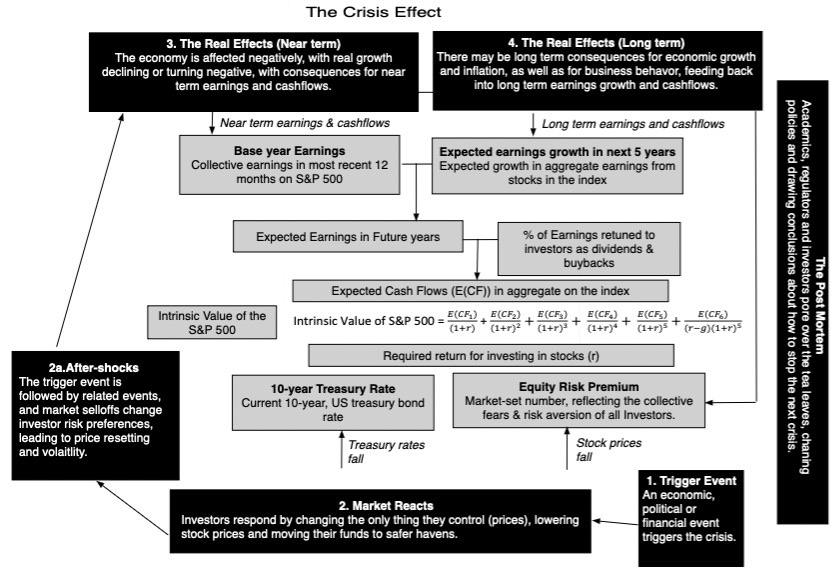

Aswath Damodaran wrote a piece recently that really stood out—not just for how he broke down what’s happening in the markets right now, but for how he framed the idea of a crisis. He called it “Anatomy of a Market Crisis” and in it, he shared a way of thinking about market meltdowns that I found both simple and powerful.

He says that every crisis tends to follow a cycle. It starts with a trigger—some event that shocks the system. It could be economic, political, or financial. And then investors react the only way they can: they start selling. Prices fall. Risk premiums rise, which basically means investors now want more return to take the same amount of risk. Money rushes into safer places like government bonds or gold. And slowly, the impact spreads from markets into the real economy.

Businesses pull back. Consumers cut spending. Growth slows down. Sometimes, there’s a full-blown recession. Over time, even after the panic fades, expectations about long-term growth or inflation might shift permanently. That’s what happened in 2008 after Lehman collapsed. It’s what happened in 2020 after COVID broke out in Italy.

And now, Damodaran says, it’s starting to happen again—with tariffs.

He wrote this just after a new round of massive tariffs were announced by the US. And while this isn’t the first time we’ve seen tariffs under Trump, the scale this time is wild. These aren’t just about China anymore. The tariffs are aimed at almost every major trading partner the US has—big and small. Countries like Canada, Mexico, even allies in Europe and Asia.

And it’s not just about protecting American industries from unfair competition. This time, the tariffs are based on the trade deficit—which means any country that exports more to the US than it imports is being penalized, regardless of whether they're actually doing anything “unfair.”

The markets, understandably, freaked out. Within two days, US stocks lost over $5 trillion in value. Technology stocks alone lost nearly $1.8 trillion. Risk premiums jumped. Investors started demanding higher returns for holding stocks. Bond spreads widened, signaling that lenders were getting nervous too.

So if you go back to Damodaran’s framework—trigger, market reaction, aftershocks, and eventually, economic slowdown—we’re right at the beginning of that cycle.

The trigger was the sudden and broad tariff announcement.

The market reaction has already started.

And now, we’re bracing for the aftershocks.

What might those look like? Well, other countries could retaliate by slapping their own tariffs on US goods. Or they could shift their supply chains to avoid dealing with America at all. Investors might start pulling money out of US stocks. Global companies that rely on open trade may have to completely rethink how they do business.

Even if this doesn’t cause an immediate recession, it could lead to long-term damage. Tariffs can raise prices for consumers. They can disrupt supply chains. They can create uncertainty, and businesses hate uncertainty. All of this could slow down economic growth—not just in the US, but globally.

Damodaran even says, and this is important, that if we measure success not by how big the economy gets, but by who gets what slice of it, then maybe—maybe—tariffs could help workers gain more relative to capital. But that’s a very different way of looking at things.

So, is this a full-blown crisis yet? According to Damodaran, not quite. But we’re in the early stages. And if we continue down this road—with tit-for-tat tariffs, global uncertainty, and falling investor confidence—it could turn into one.

And here's what’s wild. Trump seems to be doubling down. In recent weeks, he’s floated the idea of universal tariffs—a baseline 10% duty on all imports. It’s not a targeted measure anymore. It’s a blanket tax on the rest of the world.

He argues that this will protect American jobs, bring manufacturing back, and make trade more “fair.” But almost every economist disagrees. They say this will raise prices, hurt consumers, and could spark global retaliation.

If this is the opening act, then Damodaran’s crisis cycle gives us a chilling preview of what Act Two and Act Three might look like. And we’ve seen this movie before.

So the question is—are we walking into another slow-moving crisis, this time built not around a virus or a bank collapse, but around tariffs and trade wars?

And if so, what do markets—and more importantly, people—need to prepare for?

Please let us know what you think of this episode 🙂

We’ll analysed article. I feel all three are right in some ways. No doubt what has happened goes against any normal economic and political norms but Trump could have done it more prudently instead giving shocks to the market which was not needed. It doesn’t help the normal tax payers of US and nor does it help the supply chain.

What US did in the meantime is to stop the USAID, good action(if it’s fully implemented for not changing Govt and NGO’s they employed to do so!!)

Next not to interfere through their agencies to start war cry unnecessarily, not listen to some highly objectionable advise from their closest allies!!

There are brilliant economists in US from whom the govt can take prudent advise. I think DOGE is doing its job and as per newspaper report I believe they have saved about a trillion already—good for them.

Above all it remains to see “ how to solve a problem like Maria”…???!! Whimsical decision and “licking”____ doesn’t help. Shock treatment to economy might shock the country itself.