What SEBI found in Suzlon's books?

And why was it fined ₹29 crores?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

How Suzlon survived by selling to itself

The cost of defending the rupee

How Suzlon survived by selling to itself

In March 2014, Suzlon Energy sold one of its businesses for ₹2,000 crore — about 26 times what that business was worth on its own accounts.

It would have been a remarkable sale, but for the fact that the buyer wasn’t some outside investor. It was a subsidiary it had set up itself. In a year when its group was bleeding money, the company booked a profit of nearly ₹1,923 crore. In an order dated 29 May 2026, SEBI looked at that sale, and a handful of similar deals, calling them what they were: a way for a company on the edge of collapse to look healthier than it actually was.

You probably know Suzlon as one of the Indian market’s great turnaround stories: a wind-energy company that fell to a penny stock, before clawing its way to becoming a near-₹80,000 crore giant. This is the story of how it bought the time to do just that.

A fight to stay alive

To understand why it would bother dressing its books, you need to understand how close Suzlon came to going under.

Suzlon was founded in 1995 by Tulsi Tanti, a textile businessman who got into wind energy to solve his own factory’s power problems. From there, it spent the 2000s becoming one of the world’s largest wind-turbine makers. It did this the risky way: borrowing heavily to buy companies abroad, including a German turbine maker called Senvion.

Then, the 2008 financial crisis hit. The company’s overseas markets froze. Orders dried up. Nobody wanted turbines when the world was melting down. Only, their debt didn’t go anywhere. By the early 2010s, Suzlon owed banks well over ₹13,000 crore.

Things were desperate. And so, in 2013, its lenders stepped in with what’s called “corporate debt restructuring”, or CDR. They effectively gave it more time and gentler terms, rather than force it into bankruptcy. In March 2013, a consortium of 19 banks led by State Bank of India restructured roughly ₹9,500 crore of Suzlon’s debt.

But that rescue came with conditions. Suzlon had to sell assets, raise fresh money, and crucially, keep its balance sheet from looking too broken. Their net worth — or the amount of money they would be left with if they sold everything and paid off all their debts — could not drop below zero. If that happened, the conditions of the restructuring would be breached, and the arrangement would come crashing down.

This has become an existential matter for Suzlon. No matter how the broader business fared, it needed its accounts to look good, and for its net worth to stay positive.

Selling a business to yourself

And so, in 2014, Suzlon sold its operations-and-maintenance arm — the unit that services wind turbines after they’re installed. The business was worth about ₹77 crore on Suzlon’s own books.

But then, Suzlon sold it, in one lump, to Suzlon Global Services — a wholly-owned subsidiary — for ₹2,000 crore. Somehow, in shifting the company from one arm to another, it had recorded a profit of ₹1,923 crore.

There was no way Suzlon Global Services could actually pay any of that. It was barely more than a name on a piece of paper. Its assets at the time amounted to just ₹4 lakh. Over the next many years, it would somehow manage to push ₹700 crore into Suzlon’s bank accounts.

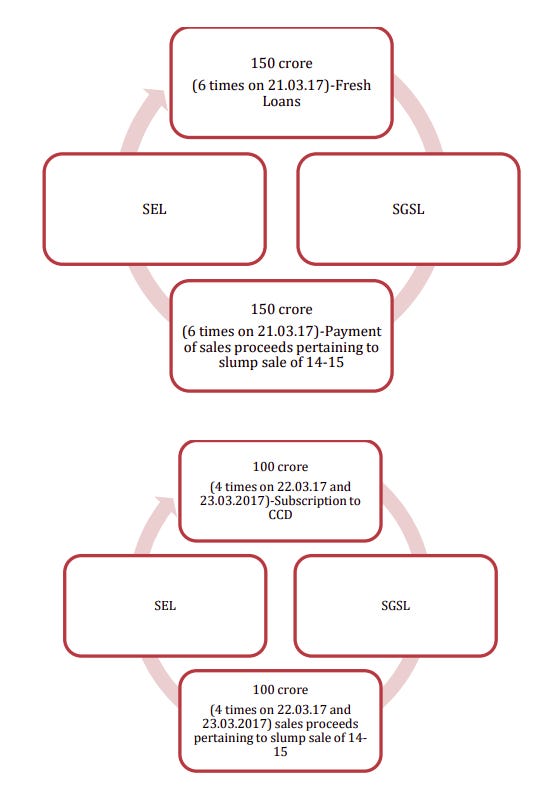

That still left ₹1,300 crore in unpaid dues. And so, the company constructed a ruse, effectively making it seem like the money had all been paid. Over the period of a few days in March 2017, Suzlon and its subsidiary moved money back and forth between their accounts. The same funds would go out and then come straight back, again and again. Each loop would be recorded as a ‘payment’.

Imagine I give you a ₹100 note, and then ask you to return it immediately, over and over again. Each time you give me the note, I write down “paid ₹100” before sliding it right back. If we do this long enough, on paper, I can make you “pay” me any amount of money — whether or not I’m any richer by the end. That’s what Suzlon did.

Of course, this didn’t increase Suzlon’s bank balance. But that was never the point; the point was to get rid of an awkward line in their accounts. For all those years, according to Suzlon’s books, its subsidiary “owed” it ₹1,300 crore. This circular exercise let Suzlon erase that line. On paper, the old sale was closed, Suzlon just happened to give it another ₹1,300 crores in routine loans that year, and bought convertible bonds from it.

Bygones were now bygones, Suzlon had successfully booked a ₹1,923 crore paper profit, and the new loans were something to be dealt with later.

Why go to all this trouble? To keep their net worth from hitting zero. The very next year, Suzlon recorded a loss of ₹6,000 crore in assets it had finally admitted were impaired. Had it not inflated its net worth just in time, that impairment would have pushed its net worth below zero. The conditions of its debt restructuring would have been breached, all its loans would instantly come due, and everything would fall apart.

The number juggler

It would be one thing if Suzlon did this once.

To SEBI, though, the larger problem was that this quickly became a pattern.

In 2015-16, for instance, it sold its shares in Suzlon Global Services — the buyer in its last deal — to yet another subsidiary: Suzlon Structures. This brought in an extra paper profit of about ₹830 crore.

Then, it got even more creative.

The company had a Dutch subsidiary, for instance, that was in need of a loan. To guarantee that loan, Suzlon asked the State Bank of India to issue a ₹4,050 crore “letter of credit”. If there were ever a default, the lenders would go to SBI for money, who would in turn recover it from Suzlon. In 2016-17, Suzlon showed this in its books honestly, as a contingent liability: money it may have to cough up in case things went wrong.

But then, it slowly began to disappear from its books. The next year, it became an “insurance contract” instead, and was quietly dropped from its contingent liabilities. But the bill would come due in October 2019, when the subsidiary would default on the loan.

The same sort of thing would happen again and again.

For instance, the value of one of their subsidiaries, SE Forge, kept fluctuating in its books. One year, it wrote down its investment in it, essentially declaring it worthless. The very next year, while scrambling to raise money, it declared that the business had recovered and added the value back again. Later on, it wrote the investment down yet again.

Suzlon had given loans to SE Forge as well. But with some accounting alchemy, those loans would turn into “investments”.

Or take Suzlon Gujarat Wind Park. Suzlon claimed to “invest” ₹1,200 crore of fresh capital in the company. But all that money circled right back. Meanwhile, just ten days later, that ₹1,200 crore “investment” was sold to another subsidiary for ₹192 crore.

As these allegations piled up, Suzlon tried taking cover under technicalities. In each case, they had appointed reputable valuers, and had the “deals” approved by their board, and by shareholders. Everything was disclosed to stock exchanges. Independent auditors had given their seal of approval. Everything was thoroughly stamped and signed.

SEBI, however, brushed that aside. If you were trying to dress up your books, it didn’t matter if you followed all the procedures carefully. It didn’t matter if the company eventually emerged as a profit making entity, and no investor was harmed. You can’t mislead people with your accounts, no matter how impressive your paperwork is.

What does it all cost?

Suzlon almost got away with all this scott-free.

SEBI had looked at this matter before. In 2019, It began an investigation, asked for a forensic audit, and asked Suzlon’s executives for an explanation. Last year, however, SEBI’s adjudicating officer cleared all of them. They found no violation, and no penalty. The matter seemed dead.

It wasn’t.

SEBI has the power — although used rarely — to reopen and revise its own officers’ decisions if it finds them wrong and damaging to the market. The clean chit didn’t make sense. SEBI took it down, and looked at the matter more strictly.

That said, for all that drama, the final bill is small.

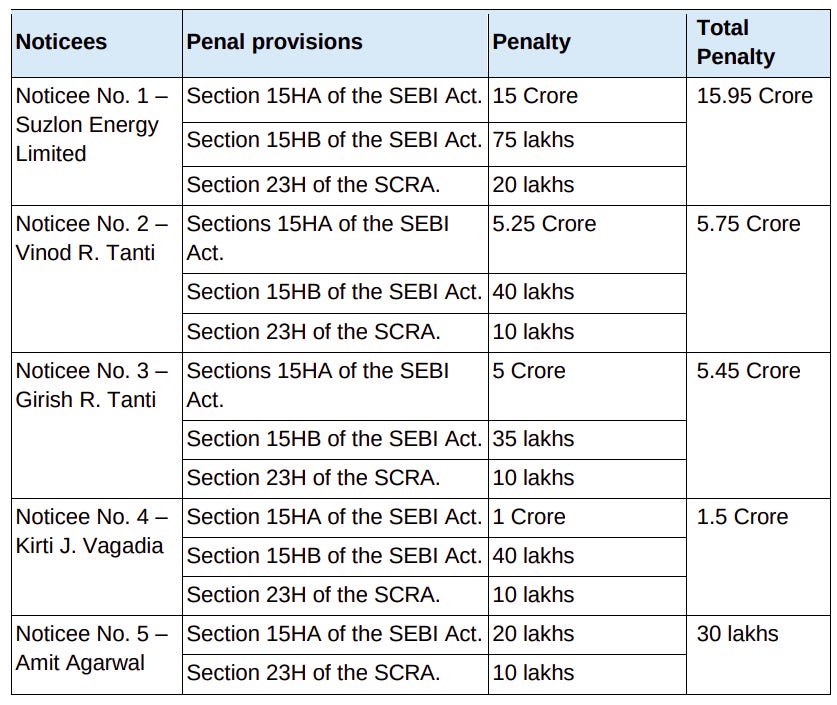

SEBI fined the five parties a total of about ₹28.95 crore. There’s no market ban, and no demand to redo the old accounts.

Suzlon is now a company worth close to ₹80,000 crore, earning over ₹2,000 crore a year. The fine, to them, is a rounding error. That’s probably why the stock barely budged when order came out.

For less than ₹30 crore — a pittance — Suzlon managed to keep itself alive for long enough to crawl out of destitution, and survive until the renewables industry finally took off. In 2022 and 2023, it raised actual equity of ₹1,200 crore through rights issue where shareholders put in real cash. It used that money to clear its debt for good. Finally, the company genuinely had a positive net worth.

In 2020, when the company was gasping for air, the stock was worth just ₹1.58. Any investor that bought in, then, multiplied their money many times over, as the stock reached high fifties.

Regardless, the company will appeal SEBI’s order to the Securities Appellate Tribunal. That shall be the next chapter in a fascinating saga.

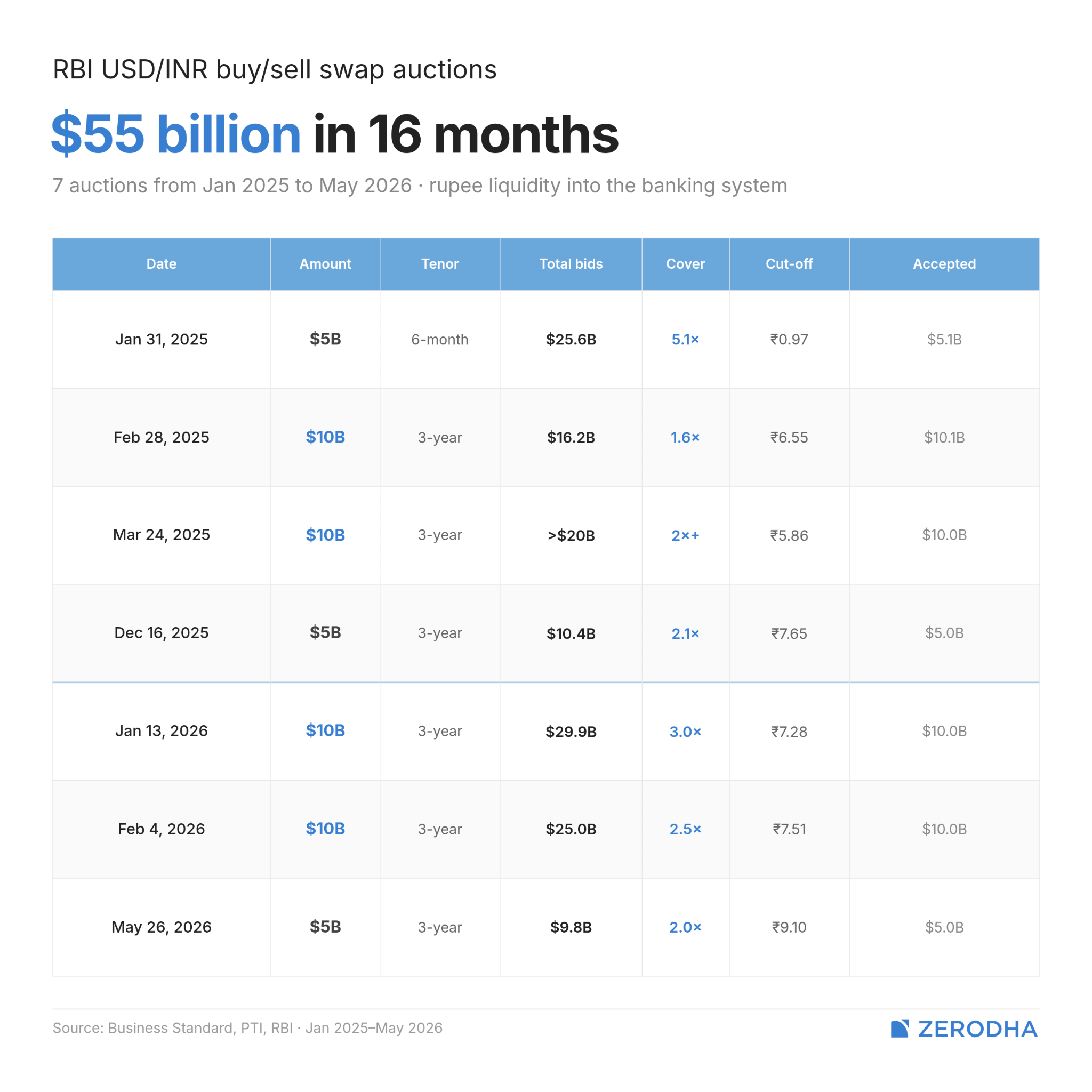

The cost of defending the rupee

On May 26, the Reserve Bank of India conducted a $5 billion USD/INR buy-sell swap auction with a three-year tenor. 254 bids came in from banks, totalling $9.8 billion — nearly twice the amount on offer. The RBI accepted 141 of those bids at a weighted average premium of ₹9.20 per dollar.

If you understood none of these words, don’t worry, we also struggled a little when we started looking into the swap. In simple terms, what it means is that the RBI wants to sell rupees and buy dollars from Indian banks, and do the reverse transaction three years later at an agreed upon rate.

So if the banks sell $1 to the RBI for the current exchange rate — say, ₹95 — they’ll buy back the same dollar amount at a premium of ₹9.20 over the current exchange rate. That premium is the price banks were willing to pay the RBI to borrow rupees for three years, using their dollars as collateral. And, given that it was nearly doubly oversubscribed, clearly, the banks wanted rupees a lot more than dollars.

But why would the RBI conduct such an operation? How does it affect the various objectives that the RBI sets for itself in a given timespan?

Well, because much of this swap has something to do with the RBI’s defense of the rupee since 2024.

Let’s zoom out a little bit. As we covered before, since 2024, well before the Strait of Hormuz crisis, India’s rupee has been under pressure due to a worsening import bill, plus the persistent selling of Indian equities by foreign investors. Repeated tariff announcements from the US didn’t help. And then, a historic oil shock has only accelerated the decline.

The RBI defends the rupee by selling dollar reserves for rupees. In FY26 alone, RBI net-sold a record $53.13 billion in the spot market. But every dollar it sells sucks rupees out of the banking system. Defending the rupee, in other words, comes at a cost. And that cost is a domestic liquidity crunch.

The swap auction is how the RBI tries to fix that crunch. But understanding why it needs to fix it — and why the fix might be creating its own problems — requires understanding what the RBI is actually juggling.

Swiss Army knife

The RBI, at any given time, has many different objectives to reach. However, the achievement of one of them usually pulls back the other. The central bank, then, manages multiple jobs that often pull in divergent directions.

For instance, on one hand, the RBI is the custodian of the rupee. It manages the exchange rate and protects the rupee from sharp appreciations or depreciations against the dollar, the global reserve currency. On the other hand, it also manages rupee liquidity, making sure that domestic banks have enough rupees to lend and create credit.

The problem here is that the main tool for the first job often creates a setback in the second.

Here’s what happens. When the RBI sells dollars to prop up the rupee, it receives rupees in return. Those rupees exit the banking system. If the RBI is selling billions of dollars every week, the cumulative drain is enormous. Banks find themselves short of rupees, and interbank lending rates spike.

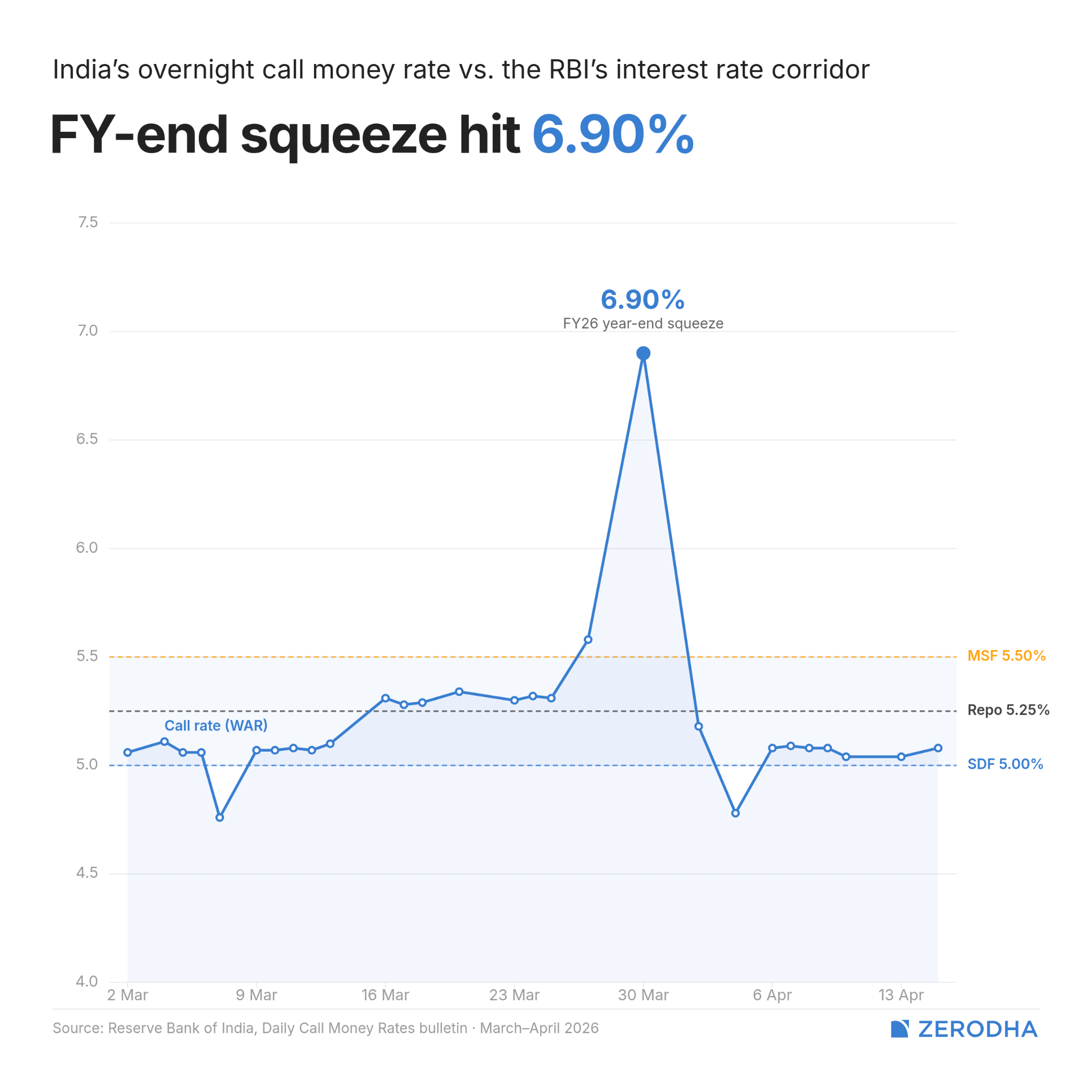

The RBI usually tries to keep the call rate — the rate at which banks lend to each other for very short time periods — close to the policy corridor surrounding the repo rate, which is usually 25 basis points above or below the repo rate. Currently, that band is 5-5.5%. The call rate had spiked to 6.9% towards the end of March 2026, reflecting a deep liquidity crunch.

So the RBI needs a way to put the rupees back in. But it also needs to keep defending the rupee. And it needs to do both without looking like it’s running out of ammunition.

That’s where reserves come in. India holds roughly $690 billion in foreign exchange reserves — among the largest stockpiles in the world. In theory, the RBI can sell dollars when the rupee is weak and buy them when it’s strong.

But here’s the catch: our dollar reserves have become what Indian economist Rajeswari Sengupta calls a “barometer of macroeconomic health”. When the headline number falls too fast, markets get more concerned. Foreign investors may also read it as yet another distress signal and pull money out faster, which weakens the rupee further. In a weird doom loop, the intervention creates the very conditions that undo itself.

Now, instead of selling dollars today and watching the reserves fall, the RBI can promise to deliver dollars sometime in the future — say, 6 months from now. This is a forward sale. No reserves leave the vault today, and the headline reserves number stays intact for now.

But a forward sale only defers the need to deplete reserves. It doesn’t make the problem disappear completely. When the contract matures 6 months later, the RBI has three choices. One, it can deliver the dollars, which means reserves finally fall. Two, it can buy dollars in the spot market to fund the delivery — but that means buying dollars, which pushes the rupee down, the opposite of what it wants. Or, lastly, it can roll the same contract into a new forward, only kicking the obligation further into the future.

Over the past two years, the RBI has leaned heavily on the third option. Its net short forward position — the total value of dollars it has committed to deliver in the future — has swelled from roughly $10 billion in early 2024 to an estimated $103 billion by end-March 2026. That’s $103 billion worth of dollars the RBI has promised to deliver but hasn’t yet.

This is the hidden cost of defending the rupee. The headline reserves say $690 billion, but $103 billion of that is already spoken for. And another $115 billion is in gold, which is valuable on paper, but isn’t liquid enough to be sold quickly.

The side door

So, how does the RBI’s swap auction come in here?

Here’s what actually happened on May 26. Banks sold $5 billion of their dollar holdings to the RBI at the prevailing spot rate (~₹95.44 per dollar). The RBI credited around ₹47,700 crore to their accounts. The banks agreed to buy those dollars back three years later at the spot rate plus a premium of ₹9.20 per dollar.

For the RBI, this accomplishes several things at once. It puts a huge amount of rupees back into the banking system, addressing the liquidity hole that its forex intervention created. And now that the RBI has bought dollars, it also temporarily adds $5 billion to the headline reserves. Such a move might also let the RBI manage its forward book by converting shorter-dated bilateral forward obligations into a clean three-year commitment.

There is usually another secondary, but important reason as to why RBI may conduct a swap: to help temper future expectations about the availability of the dollar.

For instance, with the Strait of Hormuz crisis, naturally, everyone’s worried about the future. It could be a prolonged crisis, it could be a war, who knows? Those worries manifest themselves in the forward exchange rate — in fact, the one-year forward USD-INR rate briefly touched ₹100 per dollar just last week. So, to help bring down the forward rate, the RBI might conduct a swap. In fact, even after this auction, the three-year forward premium fell from ₹9.25 to ₹9.

What’s the banks’ end in this trade? They may have dollar deposits and export receivables that they don’t need immediately, compared to rupees. More importantly, the counterparty in this swap isn’t just another bank — it’s India’s central bank. That makes the credit risk essentially zero.

Usually, such a swap can take place without an auction. Bilateral swaps still happen a lot more often than swap auctions — they’re business-as-usual liquidity operations for the RBI. But an auction is usually done when the scale of the swap is huge, and when the RBI wants to know a market-clearing price.

See, this auction had a cut-off of ₹9.10, meaning every bid below that was rejected; 113 banks didn’t get in. The fact that the weighted average premium of ₹9.20 was higher than the cut-off tells you most successful bidders were willing to pay even more. This is a market showing its hand.

From novelty to necessity

The buy-sell swap auction is not a very new instrument, but its current frequency is unprecedented.

The RBI started the format in March 2019 under then-Governor Shaktikanta Das. The context was a routine liquidity deficit — banks needed rupees, and the RBI had exhausted its bond-buying capacity. The first $5 billion auction was oversubscribed 3.3x. A second followed in April 2019.

Then, the RBI used it again in March 2020, just as COVID began, but in the opposite direction. In this case, the RBI actually sold dollars to banks during the pandemic, when the global market was desperately short of dollar funding.

The current cycle is different in both scale and urgency. Since January 2025, the RBI has conducted seven buy-sell swap auctions — totalling at least $55 billion. The January 2025 auction alone was oversubscribed five-fold, with $25.6 billion in bids against $5 billion on offer.

Interestingly, over time, the premium bid by banks has risen. The weighted average premium banks paid has climbed steadily across these auctions: ₹6.73 in February 2025, to ₹7.51 in February 2026, to ₹9.20 now. Each auction is more expensive than the last.

The escalation tells you something about the scale of the problem. The RBI keeps needing to come back to the auction window because the underlying cycle hasn’t broken: it sells dollars to defend the rupee, which drains rupee liquidity, which forces it to inject liquidity via swaps. But that, in turn, builds up its forward book, which erodes future reserves. Each round trip leaves the balance sheet a little more encumbered than the last.

Looking ahead

The swap auction is sophisticated plumbing. It puts rupees where they’re needed, it avoids the visible stigma of reserve depletion, and it buys the RBI time until the external pressure on the rupee reduces. But it doesn’t fix the underlying problem.

The rupee’s weakness reflects both structural and cyclical pressures. India’s dependence on imported energy is one such structural vulnerability, while recent foreign portfolio outflows have added to the pressure. No amount of swap auctions changes that equation.

The RBI can keep doing this for a long enough while. It has the reserves to withstand that kind of pressure. But what complicates the equation is the market’s expectations of where those reserves should be.

The cost of that then becomes deferred to a bill that only comes in the future. The question that remains is how large that bill might get before the market starts paying more attention to it than to the headline reserves number.

Tidbits

Myanmar’s President Min Aung Hlaing is visiting New Delhi, and the government is looking at this as a significant opportunity for India as we aim to secure rare earth minerals from the neighboring country, a resource currently dominated by China.

Source: Economic Times

2. Factory output grew at 4.9 per cent in April as against 5.7 per cent during the corresponding month of last fiscal, the Statistics Ministry reported on Monday. This is the first print under the new base year of 2022-23.

Source: Hindu BusinessLine

3. The Russian government has imposed a ban on aviation fuel exports until November 30 2026. The decision has been take to to ensure stability in the domestic fuel market, the government said.

Source: Business Standard

- This edition of the newsletter was written by Kashish and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thanks for a very lucid explanation about dollar-rupee swap by RBI. Nice 👌 Wonder if this affects BoP management in any way

So these ppl kept jiggling there books to show the company is some what healthy, and then actually because profitable later on, and just got a slap on the wrist for misleading people😭😭🙏