The trade breaking the RBI's rupee defence

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The trade breaking the RBI’s rupee defence

India builds castles of glass

The trade breaking the RBI’s rupee defence

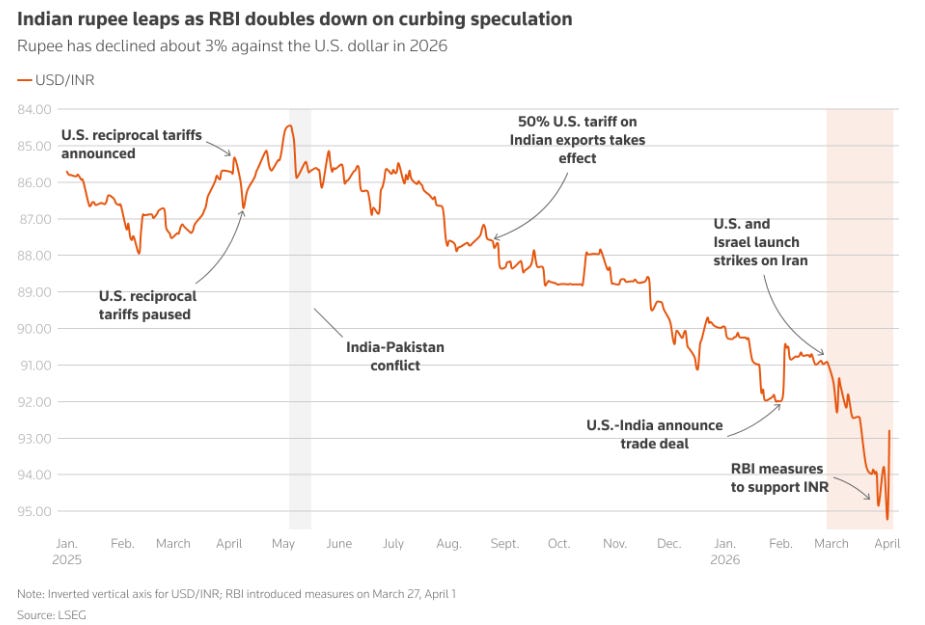

On March 27, 2026, the Indian rupee crossed ₹95 to the dollar for the first time in its history.

Consider what that number means. India imports nearly 90% of its oil. All of it is priced in dollars. When the rupee falls, every barrel we buy automatically gets more expensive, even if the dollar price of oil hasn’t moved. A rupee at ₹95 versus ₹85 a year ago means India would spend roughly 12% more rupees for the same amount of oil in a world where oil prices were stable. As you know, they weren’t. That sends up our fuel costs, transport costs, and eventually the costs of most things we buy. The rupee’s value isn’t an abstract financial number — it’s tied to our cost of living.

Oil, by the way, is just one thing we import.

The rupee fell through March for two reasons at once. The Iran war pushed Brent crude prices above $110 a barrel, widening our oil import bill significantly. Meanwhile, foreign investors were pulling money out of Indian markets, converting their rupees back to dollars and leaving — which meant a lot of the rupee was being sold at once. Both forces pushed in the same direction at the same time, and the rupee began losing ground fast.

But that’s perhaps something you already know. What made things even more complicated, though, was something happening inside India’s banking system: a trade that had grown to enormous scale, that was making the RBI’s attempts to defend the rupee significantly less effective than they should have been.

How the rupee is traded

The rupee trades in two completely separate markets. These operate under different rules, with different participants, in different time zones.

The first is India’s onshore forex market. This is the regulated market inside India where banks, companies, and foreign investors buy and sell rupees and dollars. Think: an Indian company that needs to pay a foreign supplier in dollars, a foreign fund bringing money into India to buy stocks, or an IT exporter converting dollar earnings back to rupees — they all come through this market. Only banks licensed by the RBI as “authorised dealers” can participate in the wholesale interbank layer of this market, where the actual exchange rate is discovered in real time. The RBI participates here too, buying or selling dollars to prevent the rupee from moving too fast in either direction.

But there’s also an offshore Non-Deliverable Forward market, or NDF. This exists because of India’s capital controls: rules that restrict who can hold rupees, and how money moves in and out of the country. Consider this: a foreign investor who has put money into Indian stocks has rupee exposure. If the rupee falls, their investment loses its dollar value. They naturally want to hedge against that. But doing so through India’s onshore market requires documentation, RBI compliance, and restrictions that make it all cumbersome.

So, over the years, banks in Singapore, London, and Hong Kong created a workaround: a contract that lets you bet on where the rupee will go, but doesn’t actually involve the rupee changing hands. Instead, this settles entirely in dollars. This is what makes “non-deliverable forwards”: they’re “non-deliverable” because no rupees are actually delivered. These are dollar bets on the rupee’s direction. They trade entirely outside India’s jurisdiction, beyond the RBI’s direct control. Today, the offshore NDF market in USD/INR sees trades of roughly $40–50 billion a day — larger than India’s onshore market.

Arbitrage

Ideally, the onshore rupee price and the offshore NDF price should roughly be the same. They’re both pricing the same currency, after all. But they’re not always identical. One market has the RBI’s thumb on it and the other doesn’t. In periods of stress, when global investors turn pessimistic about the rupee, the offshore NDF market often prices the dollar slightly higher than the onshore market does. In a sense, this is the price the free market actually places, compared to the partially managed onshore price.

This, however, opens the doors for a trade.

That gap — even if it’s a small one, of 40-50 paise — can be a money machine for anyone with access to both markets. If you contract to buy dollars at ₹93 in India, and lock in a forward to sell them at ₹93.50 in the NDF market offshore, the difference is yours to make. You’re no longer taking directional bets on the rupee. It doesn’t matter if the rupee eventually moves to ₹90 or ₹100. You’re just making money off the gaps that crop up between two markets that don’t talk to each other.

This sort of trade, that exploits the differences between two prices of the same thing, is called “arbitrage”. Indian banks, with operations both onshore and offshore, were perfectly placed to make these trades. They began running this trade at an enormous scale. According to estimates from market participants and analysts cited by MUFG Research, the total size of such positions across the banking system had grown to somewhere between $30 and $40 billion.

There’s a benefit to such trades: they patch unconnected markets together. But it created a problem for the RBI. Every time the RBI would intervene to smoothen the price of the rupee in the onshore market, selling dollars to defend the rupee, banks would absorb a portion of those dollars and make arbitrage trades outside. Instead of trading inside its wall garden, the RBI was trading against speculators across the world, by proxy.

It was, in effect, pumping water into a bucket with a hole.

What the RBI did

And so, on March 27, the RBI issued a directive to all authorised dealer banks: your net open position in the rupee — your unhedged exposure to movements in the USD/INR rate — cannot exceed $100 million at the end of each business day. Banks would have to comply with this by April 10.

Before this, banks could set their own limits with board approval, at up to 25% of their regulatory capital. For a large bank, that could mean an open position of anywhere between $500 million to $1 billion. The new rule was a hard cap, uniform across every bank regardless of size, and it was dramatically smaller than what the big players had been running.

To comply, banks had to unwind their arbitrage positions. This meant they had to carry out the trades in reverse: agreeing to sell dollars in the onshore Indian market, while simultaneously buying back their positions in the offshore NDF market.

This selling of dollars, onshore, was exactly what the RBI wanted. The more that dollars were sold in India, the more the rupee strengthened.

The backfire

Only, that wasn’t all that was happening. Every trade a bank made onshore was matched by a parallel trade abroad. And that other leg had an unintended effect.

As banks sold dollars in India, they rushed to close their positions outside. That sent things in the opposite direction abroad. With every bank rushing to close out their positions at the same time, the NDF price of the dollar spiked, even as the onshore price fell. Which meant that the gap between the two markets — normally a few paise wide — blew out to over a rupee on March 30.

A price gap of that size between two markets doesn’t stay open for long. As long as it exists, it’s a shining prize for anyone that can trade both markets: free money on tap.

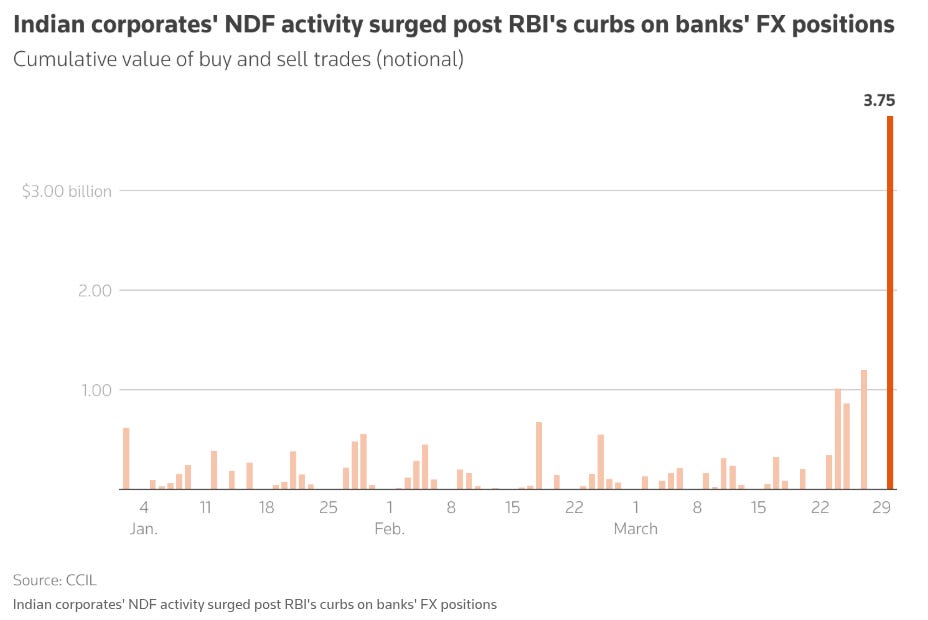

Naturally, Indian companies — importers and conglomerates with treasury operations, with access to both markets — spotted it immediately. They could now run the same trades as the banks once did: buy dollars cheaply onshore, and contract to sell them at the higher NDF price offshore. With such a large gap in sight, and nobody else to step in, this was an unexpected pay-day.

According to data from the Clearing Corporation of India, their corporate clients’ trading volumes in the NDF market hit $3.75 billion on March 30 — roughly seven times that of a normal day.

The rush was biblical. And because all these companies were buying dollars in India to run it, they were adding to dollar demand in the onshore market, pushing the rupee down. That was the day the rupee hit ₹95.20 — its all-time low.

The RBI had failed to stop the pressure on the rupee. It just moved that pressure from banks to corporates.

The second move

To reach the off-shore markets, corporates had to go through banks. This was the pressure point the RBI went for next.

Late on April 1, the RBI banned banks from offering rupee NDF contracts to any clients — Indian residents or foreign. They could no longer offer new NDF contracts, nor could they rebook cancelled forward contracts. In one move, the RBI shut off the corporate arbitrage channel entirely. Companies that had been running the trade now couldn’t access the off-shore NDF market through their banks.

Only, this created a new problem for banks that hadn’t finished unwinding their own positions. Their exit route — using corporate arbitrage flows to reduce their own exposures — was now closed. The banks that had already moved on March 30 were through. The ones that had waited, however, were now stuck, having to exit positions in a market that knew how much pressure they were under, and would milk them for all they were worth.

Overall, though, the double intervention worked. The rupee staged its largest single-day gain since 2013 on April 4, recovering to around ₹93.10. We’re writing this on April 8, when it’s trading at around ₹92.60. That’s still weaker than where it began the year, but far from the record lows of ten days ago.

What this means

The RBI’s interventions mean that the rupee is steadier today. But its fundamental problems haven’t disappeared. The offshore NDF market was quoting those prices for a reason, and those haven’t gone anywhere. Oil prices remain elevated. Investors still look at India with a weary eye. The RBI’s regulatory force removed a specific category of speculative pressure. Its restrictions targeted what market participants can do. But that’s different from resolving the underlying trade and capital flow dynamics that created the pressure in the first place.

What the last two weeks showed is something worth sitting with: a central bank with over $650 billion in foreign exchange reserves, intervening actively in its own currency market, could not do enough to stop the rupee from hitting an all-time low. It took two rounds of regulatory restriction — limiting what banks could hold, then banning a product category entirely — to stabilise things.

It may have turned the tide for now, but the problems haven’t gone anywhere.

India builds castles of glass

Of all the things that the current crisis at the Strait of Hormuz could disrupt, somehow, to our surprise, glass was one of them.

In Firozabad, India’s glassmaking hub, gas-supply cuts linked to West Asia disruptions have forced producers to slash output by as much as half and raise prices by ~20%. Around 200 small and mid-sized factories in the town are at risk. Sectors that depend on glass packaging — like beverages, pharmaceuticals, and cosmetics — are feeling the squeeze, though the severity varies by region.

Of course, it got us thinking about how little we know about glass, especially how it’s made. The crisis is most acute in segments that rely on continuous furnaces and gas-dependent clusters.That matters because glass is not one industry: flat glass, containers, solar glass, bangles, fibres, and specialty glass each use different processes and face different constraints.

With that, let’s dive into how glass is made.

So, what is glass?

Glass is not a crystal. In a crystal — like diamond or table salt — atoms sit in a neat, repeating pattern. It is an amorphous solid: its molecules are frozen in a disordered state, like a liquid cooled so fast it never got the chance to organise. It’s solid, but at the atomic level it has the structure of a frozen liquid.

At the core, its recipe is simple, consisting of three items: silica sand (which is 70–75% by weight), soda ash (which lowers the melting point from 1,700°C to about 1,500°C), and limestone (which stabilises the glass so it doesn’t dissolve in water). This formula gives you soda-lime glass, which accounts for roughly 90% of all glass produced.

Change the recipe, and you change the glass. If you replace some soda with boron oxide, you get heat-resistant borosilicate glass, which is commonly used in food containers. If you add aluminium oxide instead, you get aluminosilicate, which is the foundation behind your phone’s screen protector.

How a sheet of glass is made

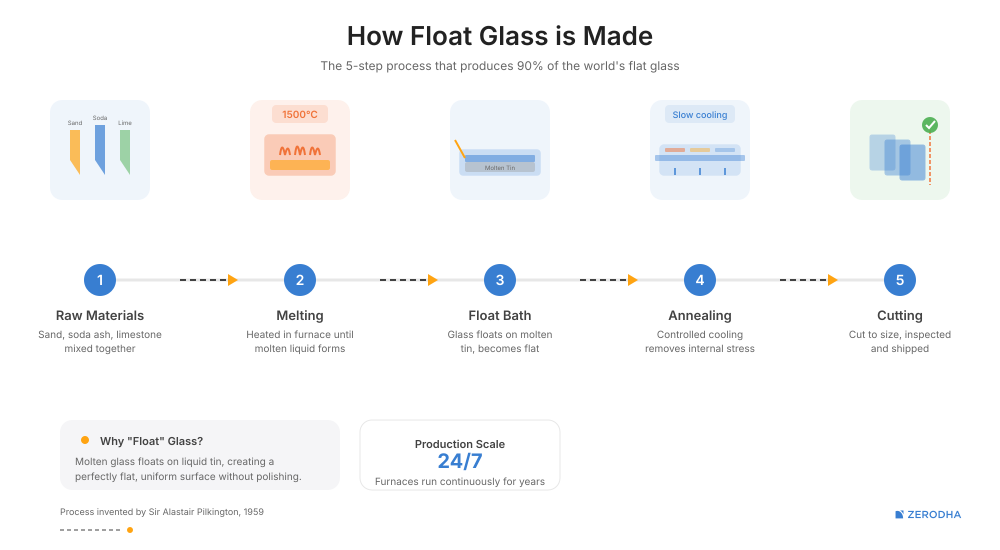

The dominant process for making flat glass is the float process.

Raw materials — such as sand, soda ash, limestone, and recycled glass (or cullet) — are blended and fed into a furnace at around 1,500°C. The molten glass is then poured onto a bath of liquid tin. Since glass is lighter than tin, the glass floats into a perfectly flat ribbon. It enters the tin bath at ~1,100°C and leaves as a solid sheet at ~600°C.

The ribbon then passes through a controlled-cooling oven called an annealing lehr. Finally, this glass gets cut. This entire process from furnace to cutting station is called a float line, and it runs non-stop for 10 to 15 years. These plants don’t shut down easily.

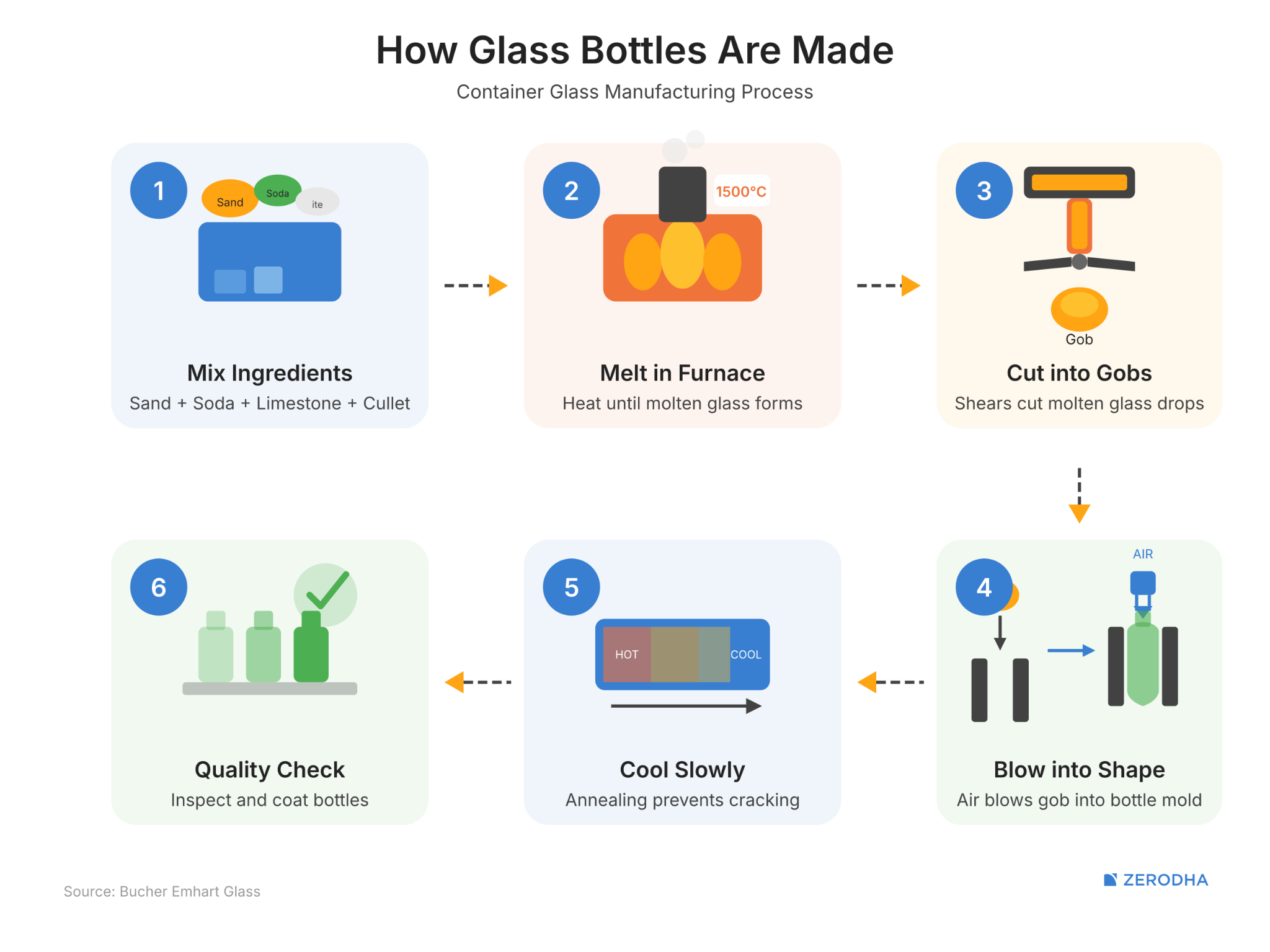

Container glass, meanwhile, works differently. Molten glass is cut into gobs, dropped into moulds, and blown into shape. Like float furnaces, container furnaces run continuously at extreme temperatures. But container plants tend to be more dependent on piped natural gas and can’t switch fuels easily. When gas is cut, they can’t just idle the furnace — letting it cool risks billions of rupees in restart costs and weeks of downtime. That’s why the current energy disruption hits container glass harder than other segments.

Fibre glass has an even more different route: molten glass drawn through hundreds of tiny platinum-alloy nozzles into continuous filaments. Same base material, very different manufacturing lines.

Molding into shape

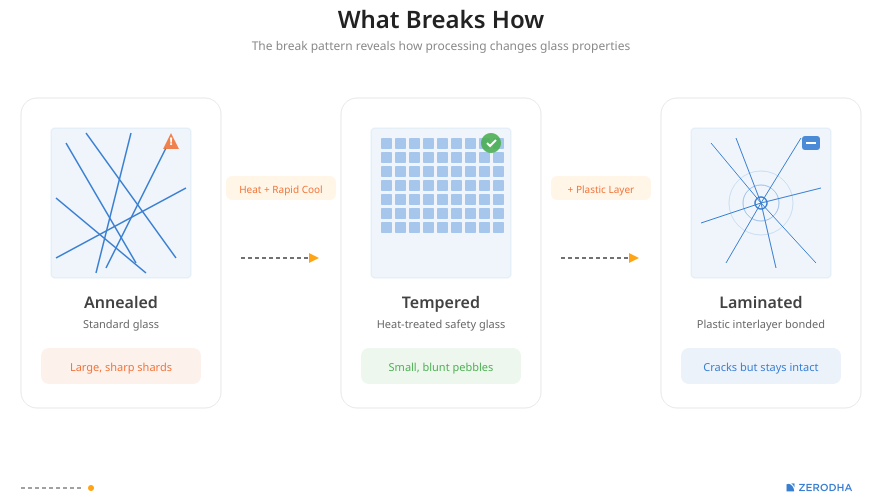

Have you ever wondered why a window pane shatters into long, dangerous shards, but a car’s side window crumbles into smaller, blunt pieces. Similarly, while a windshield cracks into a spiderweb pattern, a phone screen survives drops onto concrete.

That’s where we dive into the various finished forms of glass once it’s processed.

Annealed glass is the default. This is your regular window pane or drinking glass. After forming, it’s slowly cooled to relieve internal stresses — which makes it easy to cut, drill, and work with. But when it breaks, it breaks into large knife-like shards. Cracks start with even tiny surface flaws like scratches or even tiny impurities. And once a crack starts, nothing stops it from worsening.

Tempered, or toughened glass is what you find in car side windows and shower doors. Here, a sheet of annealed glass is heated to over 600°C and then rapidly cooled. The outside cools and solidifies first; as the interior slowly contracts, it pulls the outer surfaces into compression. This compressed surface is much harder to crack. But when tempered glass does fail, all that stored tension releases at once — it detonates into hundreds of small, blunt-edged fragments instead of long shards.

Meanwhile, laminated glass is what goes into your windshield. Two layers of glass are bonded with a plastic layer sandwiched between them, using heat and pressure. When it breaks, fragments stick to the plastic instead of collapsing — hence why windshields form a spiderweb pattern before truly breaking.

There are other forms of glass that we won’t get too deep into. Chemically strengthened glass — the family that includes Corning’s Gorilla Glass — protects your phone screen. Borosilicate glass is what’s used in food containers and laboratory equipment.

India’s ingredients sourcing problem

Making glass requires a steady supply of a few key raw materials. India’s position on each of them is different, and understanding those differences tells you a lot about our industry’s constraints.

Silica sand is the backbone. India does have large sand deposits, but the glass industry doesn’t just need any sand. It needs high-purity silica with low iron content — even small amounts of iron create an unwanted greenish tint. Saint-Gobain, for instance, operates a sand purification plant in India to clean silica sand and strip out excess iron.

Environmental restrictions on sand mining add another layer of complexity — research on mining operations in Shankargarh, Uttar Pradesh has documented groundwater depletion and environmental damage from mining and washing processes.

Then, there’s soda ash. Globally, roughly 45% of all soda ash produced goes into glass, and India has domestic capacity, too. GHCL’s Gujarat facility, for instance, produces about 1.2 million tonnes a year, while Tata Chemicals’ Mithapur facility recently crossed 1 million tonnes.

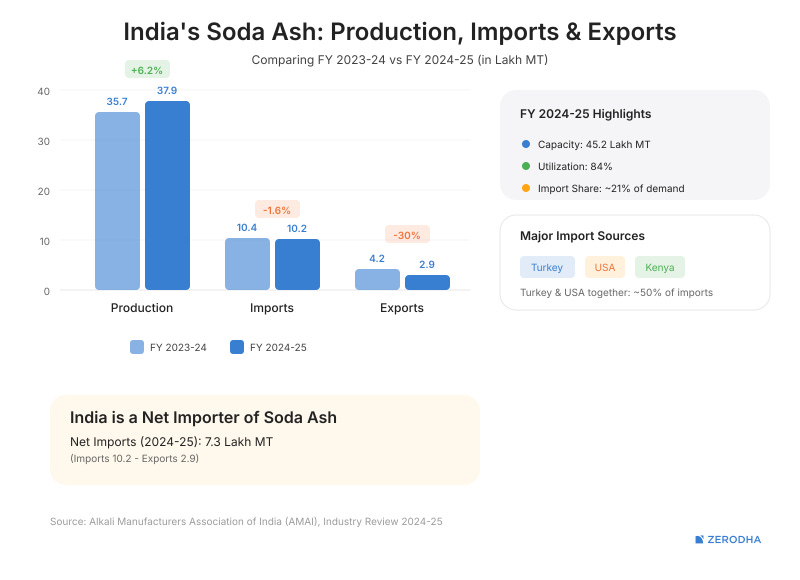

Yet, India remains a net importer of soda ash. China, the US, and Turkey together account for about 81% of world production.

As far as limestone and dolomite are concerned, India produced ~450 million tonnes of limestone in 2023–24 and is broadly self-sufficient. The constraint here is less about availability and more about consistently obtaining low-iron grades of the materials.

Borates are the wildcard. Boron chemicals make borosilicate glass possible, and they come from geologically concentrated deposits, most of which we don’t have. India is among the world’s top importers of refined borates.

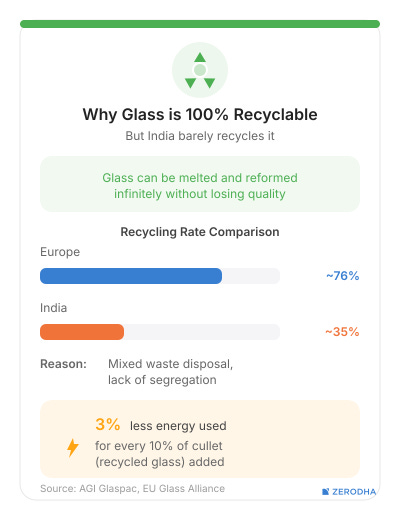

Lastly, there’s cullet, or recycled glass. Using cullet saves raw materials and cuts energy. For instance, one tonne of cullet saves ~1.2 tonnes of new inputs, and every 10% increase in cullet use reduces energy consumption by roughly 2.5%. But glass recycling in India remains underdeveloped. Cullet has to be clean, colour-sorted, and free of contamination, and the infrastructure to do that is not yet in place at scale.

Who makes India’s glass?

India’s glass industry isn’t one industry. It’s a collection of sub-sectors with different players, different economics, and different problems.

In flat glass, the major names are Saint-Gobain, Asahi India Glass, Gujarat Guardian and Gold Plus. These are capital-intensive operations — after all, new float lines cost hundreds of crores and expand in lumpy steps. Energy is an additional structural cost burden since furnaces run continuously at very high temperatures.

In container glass, the picture is more fragmented. AGI Greenpac is a leading player with over 2,000 tonnes of daily capacity across multiple plants. Hindustan National Glass (HNG), once a dominant force, went through an insolvency process. PGP Glass operates in the specialty segment.

Container glass is also the sub-sector most exposed to the current crisis. When GAIL reduced gas supply to Firozabad, producers had no easy fallback. What made things harder was that higher-emission fuels were banned in the city, because of its proximity to the Taj Mahal. As we’ve covered recently, India’s gas system is heavily exposed to the crisis in West Asia.

Solar glass has become an important sub-sector, sitting inside India’s larger push for domestic solar manufacturing. Borosil Renewables describes itself as India’s first and only solar glass manufacturer. The segment has already seen trade-policy protection: India imposed a five-year anti-dumping duty in May 2025 on imports from China and Vietnam.

What’s ahead

Glass melting is energy-intensive by nature, and India’s dependence on imported gas means every conflict or disruption in West Asia becomes a production crisis at home. But the sector is exploring electric melting, hybrid furnaces, and hydrogen combustion as alternatives.

In 2024, for instance, AIS signed a long-term agreement with INOX Air Products to supply green hydrogen to its Chittorgarh float-glass plant, which the company says could reduce carbon dioxide emissions by ~1,250 tonnes annually.

But these are still early moves. Hydrogen is being tested in glass furnaces, not yet used widely at full commercial scale, and electric melting remains economically challenging in many cases.

India’s glass consumption is rising with urbanisation, construction, automotive production, and the solar buildout. Whether the industry can keep pace depends on three things: dependable energy, consistent raw material quality, and scalable recycling. Right now, all three are works in progress — and Firozabad is a painful reminder of what happens when even one of them breaks down.

Tidbits

Iran War is China’s Global Payments Debut The conflict with Iran is accelerating China’s push to settle oil trades in yuan, bypassing dollar-dominated payment rails. It could mark the moment China’s alternative financial plumbing gets its first serious stress test at scale.

Source: BloombergTCS Posts Rare Annual Revenue Drop TCS reported its first annual revenue decline in recent memory, with macro headwinds and weak discretionary IT spending outweighing a decent quarterly beat. The result signals continued caution among global clients on large tech contracts.

Source: ReutersJio-bp Has No Plans to Raise Fuel Prices Jio-bp’s CEO confirmed the company is holding fuel prices steady despite global crude volatility, likely a mix of competitive pressure and demand sensitivity. With margins already thin at retail pumps, any hike risks losing volume to state-run OMCs.

Source: Reuters

- This edition of the newsletter was written by Krishna and Vignesh

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Understanding the oil market ft. Rory Johnston

A month-long closure of the Strait of Hormuz, a critical route for ~20% of global oil, has severely disrupted supply, triggering fuel shortages and panic across Asia, with India already facing an LPG crunch. While a ceasefire offers relief, the deeper issue is systemic dependence on a single chokepoint. To unpack this, we spoke with Rory Johnston, an oil market expert known for his typically bearish, adaptive view. Despite past shocks, he sees this disruption as fundamentally different and far more concerning.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Very detailed explanation on how the RBI is managing the rupee movement! We've portrayed the same thing in brief for a quick read here - https://www.linkedin.com/posts/dailyequity_rupee-geopolitical-rbi-activity-7447274881802665985-p9RB?utm_source=share&utm_medium=member_android&rcm=ACoAACTJ5WABzdFZ7bVT6Y3OFy9K17dGjUSc1cg

Thanks!

Hi, I am a big fan of your posts. I read them regularly. I also write quite often you can check my profile. I would love to have your feedback. Currently, I am looking for an internship in this field, so if you have any opportunity, I would love to be a part of your team.