The Indian EMS industry moves up and sideways

While managing a few squeezes

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s EMS companies are building their way out of thin margins

How the Hormuz crisis changed oil markets

India’s EMS companies are building their way out of thin margins

A few months ago, we published a primer on how India’s electronics manufacturing services (EMS) business works.

The takeaway was that EMS is a notoriously unforgiving business — razor-thin margins, heavy dependence on government subsidies, and working capital cycles that can make or break a company. But we also noted that it’s a business that extends far beyond smartphones: home appliances, medical devices, railway signalling systems, EV components, and more.

The latest quarterly results for three of the biggest Indian EMS firms — Dixon, Kaynes, and Syrma SGS — are out. These aren’t competitors in the traditional sense. Dixon, the largest of them all, is the high-volume consumer electronics giant; Kaynes focuses on complex industrial, automotive, and aerospace systems; Syrma straddles both worlds with a growing tilt towards defence, railways, and healthcare.

But they all operate under similar constraints that define all EMS companies. How do you build a durable, profitable business when your core job is assembling someone else’s product?

Their answers, this quarter, are converging in interesting ways.

The numbers

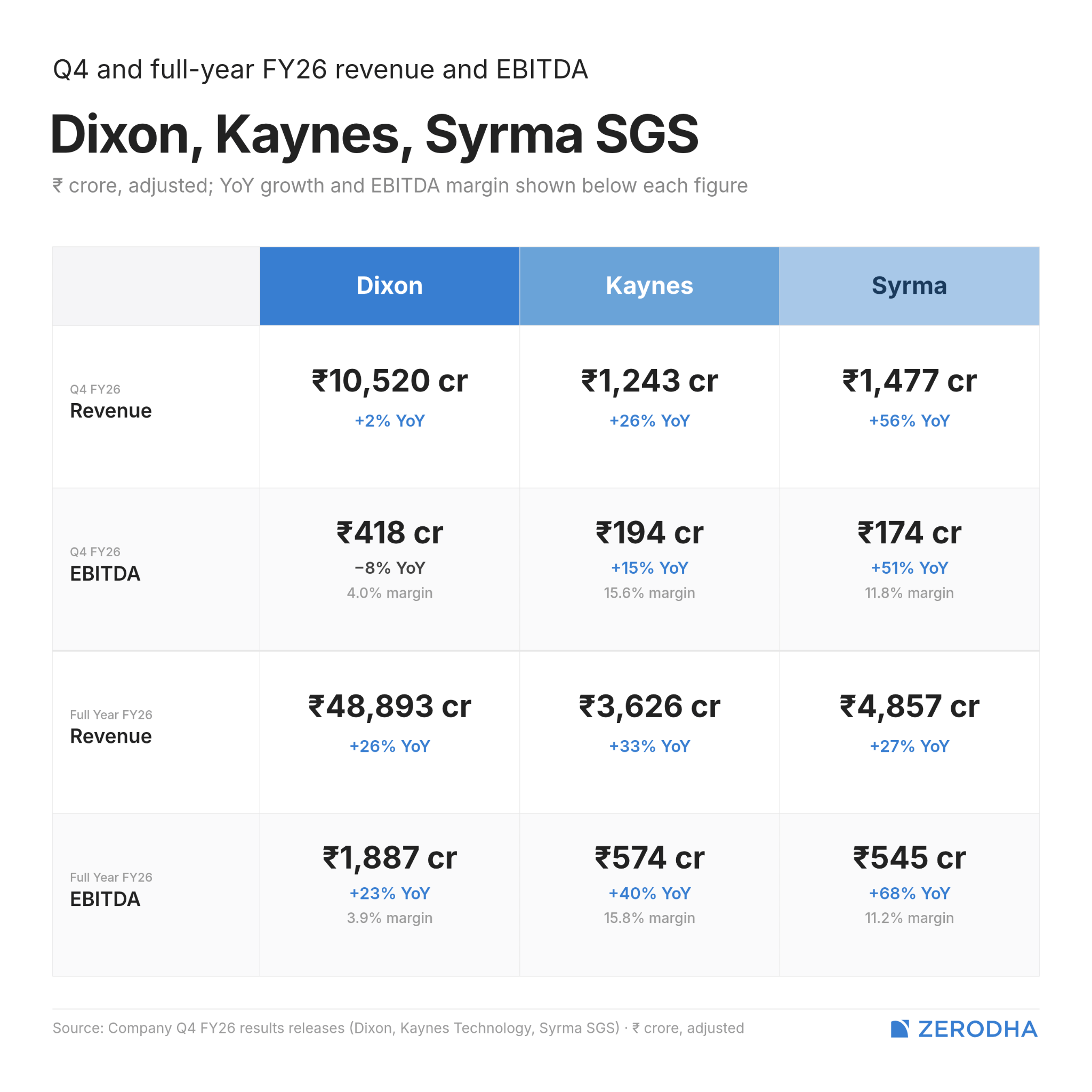

As per its adjusted numbers, Dixon posted Q4 revenues of ₹10,520 crore, with an adjusted EBITDA of ₹418 crore and a PAT of ₹192 crore. Dixon’s EBITDA margin sits around 4%, with PAT margins closer to 2%.

FY26 consolidated revenue hit ₹48,893 crore, up 26% from last year, actual adjusted EBITDA surging 23% to ₹1,887 crore and PAT rising 20% to ₹845 crore. While that’s healthy absolute growth in profits, the margin share of revenue shows the brutality of being in the business. That’s the reality of being India’s largest mobile phone assembler.

Kaynes reported Q4 revenues of ₹1,243 crore, up 26% year-on-year, with an EBITDA margin of 15.6% and a PAT margin of 7.3%. For the full year, Kaynes delivered an EBITDA margin of 15.8% and a PAT margin of 10% — comfortably the highest among the three.

But the quarter didn’t fully meet market expectations. Management pointed to the West Asian conflict — supply chain delays, project timing shifts, and last-minute customer deferrals disrupted the cadence of revenue recognition even as the order book remained strong. Kaynes didn’t offer specific revenue guidance for the year ahead, but was unambiguous about intent, saying:

“We will outgrow the market, penetrate every segment, and double the market’s growth rate. That is our commitment.”

For Syrma, Q4 revenue came in at ₹1,477 crore, a 56% jump from the same quarter last year. Operating EBITDA hit ₹174 crore at an 11.9% margin, and PAT surged 67% year-on-year to ₹119 crore. IT and railways, in particular, went on a tear — up 182% year-on-year.

The margin gap between these three tells you everything about what kind of electronics you assemble. Dixon’s 4% EBITDA margin reflects the highly-commoditised nature of the mobile phone business. Kaynes’ 15.6% reflects the premium of serving complex, high-reliability sectors like aerospace and industrial electronics. Syrma sits in between.

But, of course, none of them are content with where they stand today.

Upstream, downstream, sidestream

As we said last time, as an EMS company, the best way to escape low margins is to capture a bigger part of the value chain. In other words, vertical integration, where you don’t just assemble products, but also start making the components that go into them.

Vertical integration

Dixon’s playbook here is heavily dependent on joint ventures (JVs). They’ve taken a 51% stake in Q Tech India, a maker of camera modules for brands like Samsung, Motorola, and Vivo. Currently at 70 million units a year, Dixon hopes to scale the camera module business to 180-190 million units annually.

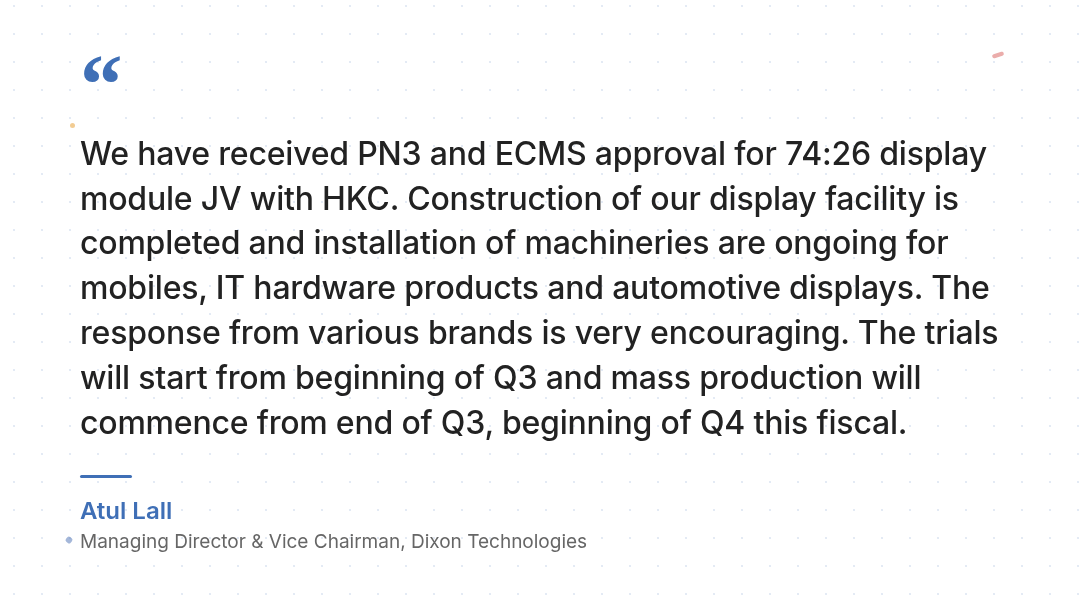

Recently, they also cleared a 74:26 JV with China’s HKC to build a display module factory, where construction is complete and machinery is being installed. A 60:40 JV with Taiwan’s Inventec for SSDs and memory modules. Even a new wholly-owned subsidiary, Dixon Electrocorp, to get into lithium-ion batteries.

Management expects 70-80% of their business to be integrated into the component landscape by FY28. Dixon’s bet is that JVs with global technology leaders give them the fastest route to making that happen.

Kaynes’ strategy is a little different, though. When Kaynes partners with a global company, it offers them a small minority stake — strictly under 20% — to give them “skin in the game“ while retaining firm control.

Their vertical integration push is also aimed at two areas that sit much deeper in the electronics supply chain.

First, semiconductor packaging: they have an OSAT (outsourced semiconductor assembly and testing) facility in Sanand, Gujarat. Second, is bare-board, high-complexity PCBs, made at a massive multi-layer facility in Chennai, for smartphones, telecom, and aerospace.

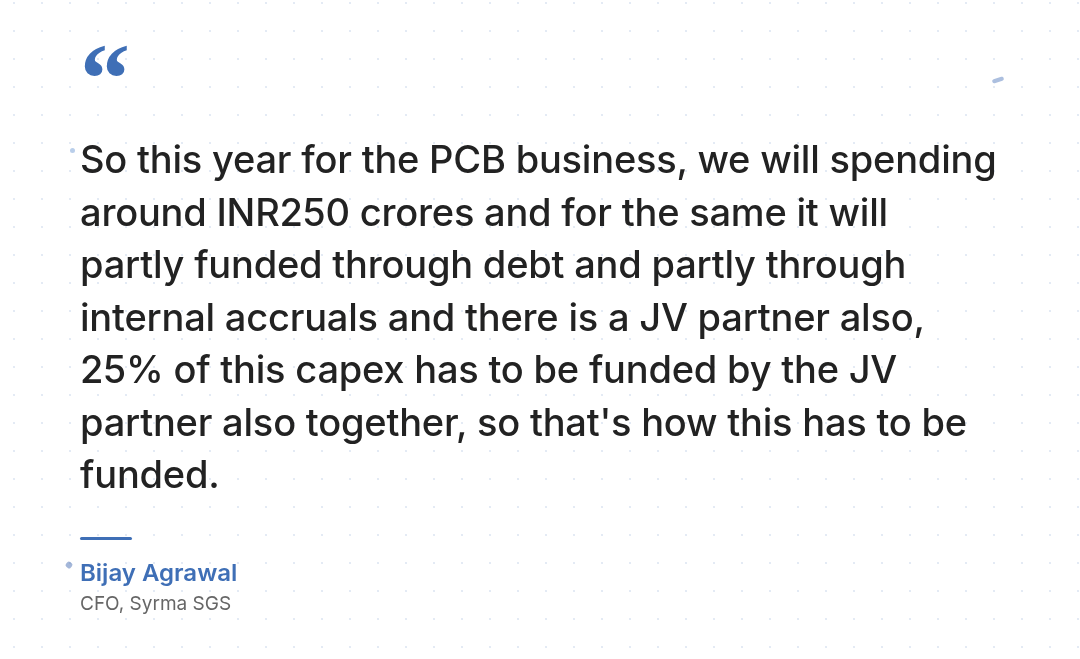

Syrma’s approach is a mix of both. They’ve formed a 75:25 JV with South Korea’s Shinhyup Electronics to manufacture multi-layer bare-board PCBs. But unlike Kaynes, Syrma is starting conservatively with standard multi-layer and single-layer boards for automotive and industrial applications, deliberately avoiding the complex boards that Kaynes is chasing. The logic is to capture the “low-hanging fruits” first — PCBs for automotive lighting, infotainment, industrial appliances — and graduate to higher-complexity boards later.

They’ve also received approvals to move into copper-clad laminates (CCLs) and flexible PCBs in a second phase, running up the total cost of both phases to ₹800 crore. In our primer on how PCBs work, we covered how CCLs make up the biggest cost driver of any PCB. This is a highly strategic acquisition on Syrma’s part to control as much of the PCB value chain as possible.

Horizontal integration

Then there’s the horizontal push — expanding into entirely new product categories and end markets.

Dixon’s telecom business, for instance, scaled from ₹700 crore in FY24 to ₹5,000 crores this year. More notably, it’s planning to enter the high-end specialty EMS space — aerospace, defence, medical, industrial — the exact territory where Kaynes and Syrma already operate.

Kaynes, meanwhile, has been on an acquisition spree. For instance, they bought a Canada-based EMS player named August Electronics, which will give them a manufacturing footprint in North America. Additionally, they also bought Austria-based Sensonic to deepen their railway capabilities.

Most importantly, they acquired a smart metering business which was earlier their client. This brings them into a completely new category where they don’t just manufacture the meter but also handle installation and maintenance.

Syrma’s horizontal moves are equally ambitious. Railways, defence, and renewables are the three frontiers. For instance, they bought a 60% stake in Elcome, which plants their flag in naval systems. They also recently planned to enter solar inverter manufacturing through a JV, but dropped the plan and will pursue a greenfield project instead.

One new category common to all three is data centres. Dixon is in discussions with Inventec to manufacture servers. Kaynes is receiving more orders for high-performance computing servers. Syrma is supplying data centre motherboards and power management units. The data centre boom driven by AI spending is pulling all of them into the same orbit.

Cash in, cash out

All this expansion costs money and ties up working capital. How each company manages that cash cycle is where their business models diverge most sharply.

Dixon is the efficiency machine. It ended FY26 with a working capital cycle of negative 8 days — meaning it collects cash from customers before it pays suppliers. For a company doing over ₹10,000 crore in quarterly revenue, that’s remarkable discipline. It’s also a function of the business: consumer electronics assembly is a fast-turning, high-volume game, and Dixon plays it better than almost anyone.

Syrma showed strong improvement. Its net working capital cycle came down from 69 to 63 days, or 58 days excluding the Elcome acquisition. For the year, the company generated operating cash flow of ₹290 crore (or over half its EBITDA), which helped it move from a net debt position to a net cash position of ₹467 crore.

In fact, they’ve explicitly said that they’ll sacrifice top-line growth if their working capital is threatened. After all, this is a business where everyday cash is just as important as the margins, and perhaps even harder to come by.

Meanwhile, Kaynes sits on the other, more cautionary side of that reality.

On a consolidated basis, its receivables ballooned from ₹521 crore to ₹1,300 crore. The culprit was their smart metering acquisition. Kaynes manufactured the meters, but state governments dragged their feet on installations. And since Kaynes only gets paid upon successful installation, the cash sat locked up.

Their standalone EMS business is still efficient at 54 days, but the smart metering drag pushed consolidated working capital days much higher. Management is now deploying supply chain finance, vendor-managed inventory, and invoice discounting to improve the numbers.

The macro squeeze

Two external forces tested all three companies this quarter.

The first is the global memory chip crunch. Since AI data centres are consuming enormous amounts of memory, global suppliers have been redirecting capacity away from consumer devices. This has driven up memory prices sharply.

In particular, this hits Dixon the hardest. Dixon acknowledged a 50-70 basis point margin impact from this, compounded by the expiry of the original PLI scheme for mobiles. Their fix, which is backward integration into components, is the right long-term answer, but there’s a lag of 6-8 months before new factories ramp up. Until then, Dixon is absorbing the hit.

Kaynes, notably, is insulated from this problem entirely, since they don’t operate in consumer electronics.

The second is the Strait of Hormuz crisis. Conflict in the region disrupted shipping routes, drove up logistics costs, and increased basic metal prices, affecting all three companies.

For Kaynes, it caused direct project deferrals. For Syrma, it raised input costs, though management noted that pass-through clauses in their contracts will eventually cover it. Syrma is also banking on the recently signed EU-India Free Trade Agreement as a structural tailwind for their European exports. With an engineering facility in Stuttgart, Germany, they’re positioned to capitalize on it.

Conclusion

Indian EMS players have sufficiently established scale in their core businesses. But for them to be truly globally competitive, their backward integration bets across display modules, semiconductor packaging, bare-board PCBs will have to start paying off. All three companies have identified FY28 as the year in which they expect those investments to show up in the margins. Of course, policy consistency also matters, as the PLI scheme for electronics components has also taken effect.

Meanwhile, their balance sheets will not just have to handle their expansion, but also the external macroeconomic squeezes that come along with it. It will take a while for the capex to meaningfully contribute to margins, much less be operational. And if the external crises get worse, then the industry as a whole will have to pull up its straps.

How the Hormuz crisis changed oil markets

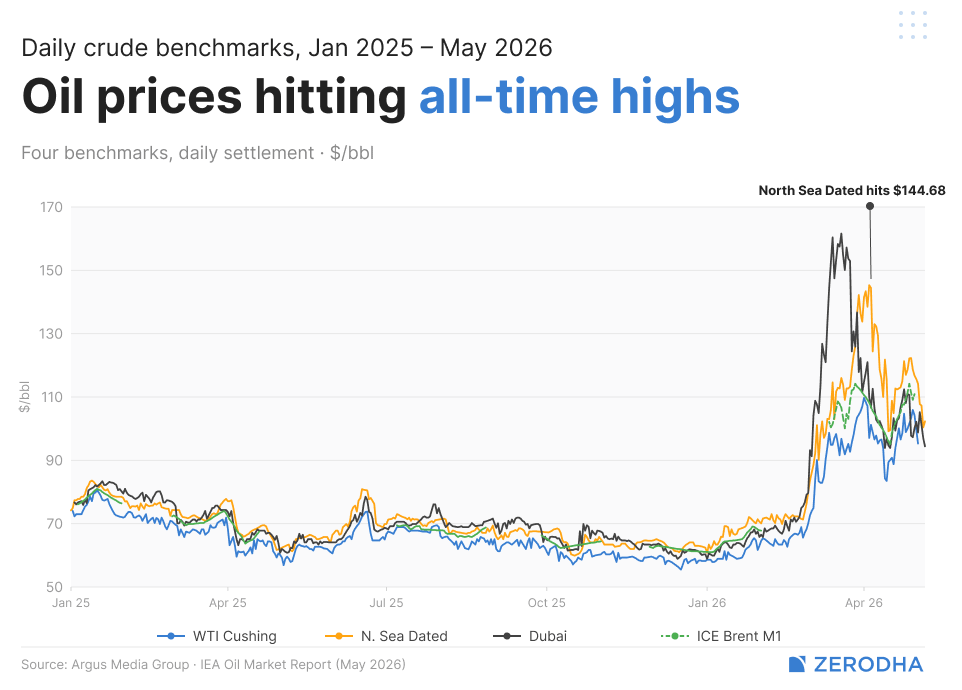

On 7 April this year, the price of a single barrel of North Sea Dated crude oil touched its highest point ever: $144.68 a barrel. The last time it came anywhere near that number, it was right before the Global Financial Crisis in 2008, when world-changing events like the rise of China, combined with intense speculative fervor, briefly made everyone imagine a future where oil would cost $200 a barrel.

But that was a different time. People were bidding oil up back then because they were in a world where demand was relentless. The new record is different. It comes out of a world where an acute Middle Eastern crisis has choked the world’s oil supply.

As far as we can see, peace is nowhere in sight. Even if it did arrive, and a complete ceasefire took hold, it would take an extra two to three months for global oil markets to return to normal. The threats would have to cease, the tankers stranded in the Gulf will have to transit again, and port schedules will have to return to normal.

For now, Iran has strewn the Strait of Hormuz with mines, and is planning to run a bitcoin-based protection racket to let ships through. In short, we’re stuck for the foreseeable future.

We’ve often talked about the Hormuz crisis on The Daily Brief. A recent IEA report, however, supplies the first real accounting of how, exactly, those risks have materialised. The picture isn’t pretty. The world needs about 104 million barrels of oil a day, but we’ve recently lost roughly 12.8 million barrels in supply. That is, one in every eight barrels that used to show up to global markets is now missing.

To the IEA, this is an unprecedented supply shock. A region that produced a third of the world’s oil till February has seen half its production collapse. We’ve never seen something like this.

What does a moment like this mean for the world? Let’s dive in.

Filling the gap

There’s a beautiful thing about markets: when something breaks down, they don’t just sit quietly in the dark. They reorient and scramble to adapt.

We’re seeing this play out in the world’s oil markets at this very moment.

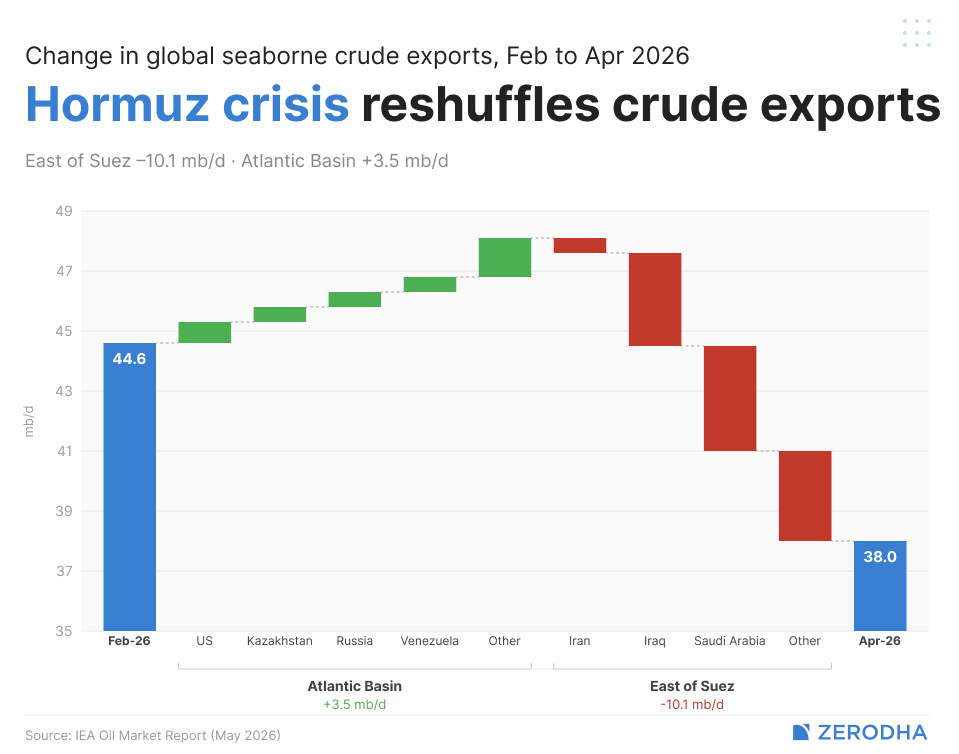

Since the Hormuz crisis broke out, the amount of oil being loaded on ships at Gulf export terminals has fallen by roughly 10 million barrels daily. That’s a glaring hole, sized at roughly one-tenth of the world’s oil needs.

In response, though, roughly a third of that gap has been filled in with oil from elsewhere. As the crisis unfolded, the Americas ramped up their output. A range of Atlantic producers — the United States, Brazil, Canada, Venezuela, and more — along with Kazakhstan, started pushing out an extra 3.5 million barrels a day.

Meanwhile, others began buying less oil. Asia’s four biggest oil destinations — China, Japan, Korea, India — each cut their crude imports by an unprecedented 7.2 million barrels a day. India’s purchases alone fell by roughly 0.8 million barrels daily. All four countries voluntarily ran their refineries on less crude or started drawing down their own stocks. This demand destruction effectively shut three-fourths of the gap.

The biggest player in this crisis-era adjustment was the United States. American crude production hit a record 14 million barrels a day in April, with exports touching a record 5.2 million barrels a day. For the first time in over fifty years, the country turned into a net exporter of crude oil. Brazil, meanwhile, leaned back on its huge new offshore platforms, setting its third consecutive production record at 4.4 million barrels a day.

Even Venezuela — after shuttering most of its oil production after years of sanctions — saw a revival under its new American patrons. It began exporting as many as 1.12 million barrels a day, often with Indian refiners as its eager customers.

The IEA expects a surge of new capacity in what it calls “the Americas Quintet” — the US, Canada, Brazil, Guyana, and Argentina. In all, these countries will add an extra 1.5 million barrels of daily supply this year. This new capacity will replace roughly one in every eight missing barrels of supply. That isn’t enough to fill the gap, but it is some relief.

When the crisis began, one may have expected Russia to be one of its biggest beneficiaries. But Ukrainian drones made sure that didn’t happen, hitting major refineries across the country. Russian refineries are now processing 400,000 fewer barrels of crude a day. Instead, the country is forced to sell raw crude instead. Russian crude exports have gone up 250,000 barrels a day, while its petrochemical product exports — diesel, jet fuel, naphtha — are at their lowest level in the IEA’s records.

And it is in those petrochemical products that the crisis is actually making itself felt.

Barrels versus molecules

Crude oil is a raw material. By itself, there’s barely anything it’s useful for. It only becomes useful when it is processed at a refinery into specific products — petrol for cars, naphtha for plastics, LPG for kitchens, and so on.

Different kinds of crude oil make different products, in different proportions. What you make out of heavy sour Saudi crude is very different from what you can make with light, sweet American crude. The kind of crude you start with, and what your refinery was built to produce, fundamentally changes your output.

This is why the Hormuz crisis is so complex. The Gulf did not just export crude; it exported enormous volumes of these refined and semi-refined products. Many of the world’s economies were built around the expectation that finished molecules, ready to use, would keep streaming out of the Gulf. The chemical plants of Japan and Korea were built around Middle-eastern naphtha. India’s cooking gas push was built around Middle-eastern LPG. And so on.

When Hormuz closed, the supply of those specific molecules disappeared. Even if you can reroute crude oil tankers, you can’t magically create the same products.

The IEA looks at four product channels where those shortages are at their most painful.

One of the worst is naphtha; which goes into most of the world’s plastics and chemicals. The war pushed Middle Eastern naphtha exports down to just a fifth of its original supply — from 1.2 million barrels a day in 2025 to 260,000 barrels a day in April. Chemical plants across Asia are now running at deeply reduced rates. As the IEA notes, demand for naphtha in the region has fallen to depths last seen during the 2008 financial crisis.

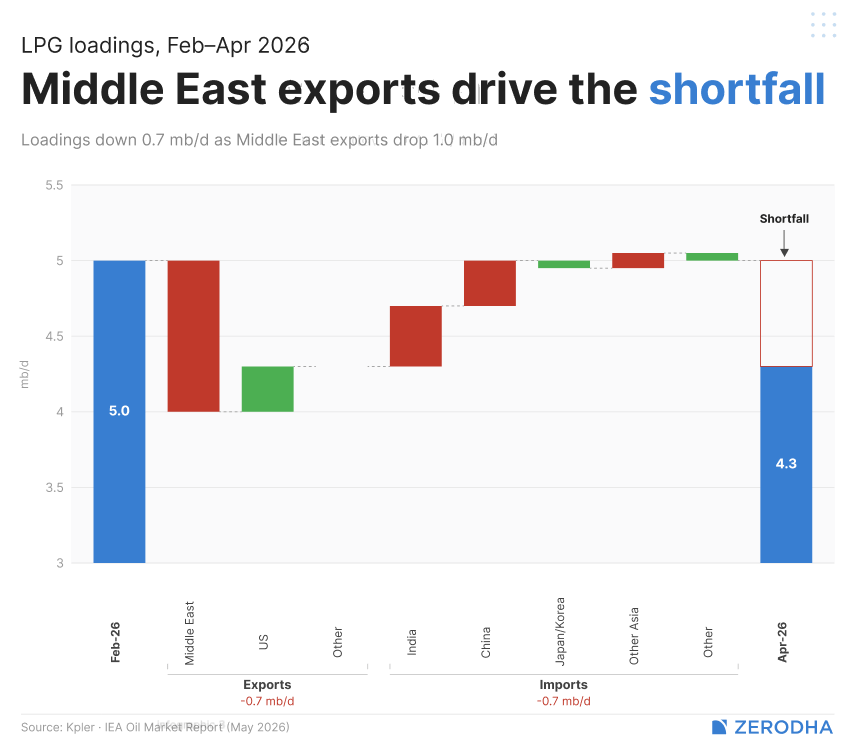

The next, as you’re probably familiar with, is LPG — the cooking gas for most of the developing. Middle-eastern LPG supply, too, has dipped to a fifth of pre-war levels, dropping from nearly 1.5 million barrels a day to just 270,000. The United States is trying to ramp up its LPG exports, and now accounts for 69% of all seaborne LPG supply. But as you’ve probably seen around you, it isn’t nearly enough. India has been hit the hardest, with LPG arrivals more than 40% below where they were in January-February.

Something similar is happening with jet fuel. The Middle East used to be the world’s largest source of aviation fuel, supplying about 400,000 barrels a day in 2025 — 330,000 of which would go to Europe alone. In April, the Middle-East could only dispatch 70,000 barrels a day. Europe had to scramble for alternatives, while prices nearly tripled. The continent once sourced three-fifths of its imported jet fuel from the Gulf, but in April, its imports dropped to just 60,000 barrels. Meanwhile, European flights contracted 2.1% year-on-year in April just as summer travel was supposed to take off.

Arguably the most consequential, though, is diesel. The war halved Middle Eastern diesel exports from 1.4 million barrels a day to 700,000. As a result, Africa, which imports two-thirds of the diesel it consumes, was slammed — with imports down by roughly a third compared to last year. That diesel once ran trucks, generators, farming equipment, and supply chains. In rich countries, the shortage is an inconvenience priced into freight rates. In emerging markets, particularly in Africa, this could become a food and logistics crisis.

None of these gaps can be plugged with more crude alone.

The buffers are draining

The terrifying thing, though, is that we haven’t seen the worst of it.

So far, the world has pulled through this crisis by burning through its safety net. That is why we haven’t seen rationing and riots across the world. But this comes with a ceiling. The world’s observed oil stocks have fallen by 246 million barrels since the war began. For perspective, that’s roughly how much oil the entirety of India would use over seven weeks, all gone in two months of the war. April alone saw stocks drop by 170 million barrels, or nearly 6 million barrels a day — a record draw.

Governments are selling oil out of their stockpiles, moving about 90 million barrels of oil into commercial markets. They’ve also reduced the minimum mandatory stocks that oil companies have to hold — letting an extra 74 million barrels into commercial markets.

Moreover, major Gulf producers — Saudi Aramco, ADNOC, Kuwait Petroleum — own large stockpiles of crude oil sitting in tanks inside consumer countries like Japan, Korea, India, and China. Countries have taken to drawing on these stocks as well. Japan, for instance, has already drawn roughly 25 million barrels from Saudi-owned stocks at Okinawa and Kiire.

For now, this has worked. But it isn’t clear that it will continue to do so.

Under the IEA’s base case — where there’s a ceasefire by early June, and flows gradually resume through the third quarter — the world will see a cumulative oil deficit of 900 million barrels by September. To rebuild those buffers, the world will need an extra million barrels a day of oil every single day for the next three years, on top of demand.

The fact is, we’re nowhere close to the end of the global oil shock. Even if peace finally arrives, the tremors will continue. Hormuz will have to be opened, its mines will have to be cleared, shipping will have to resume, refineries will have to be repaired, reserves will have to be refilled, and so on.

There’s a lot of work ahead, even in the best case scenario. Let’s hope the war ends soon.

Tidbits

Reliance Industries negotiating with CATL and other suppliers to procure battery energy storage system parts for Jamnagar facility, supplementing Xiamen Hithium partnership amid roadblocks, shifting focus to sourcing products leveraging China’s battery manufacturing scale after previous CATL technology transfer talks collapsed, as India’s storage market projected to reach 336.7 GWh by 2035.

Source: BloombergInternational Energy Agency chief Fatih Birol warned commercial oil inventories depleting rapidly with only weeks remaining due to Iran war and Strait of Hormuz closure, despite 2.5 million barrels per day strategic reserve releases, as global inventories fell record 246 million barrels in March-April, with IEA now forecasting 3.9 million bpd supply shortfall in 2026 versus earlier surplus projection.

Source: ETVodafone Idea outlined three-year plan to generate Rs 1.08 trillion through rising operating earnings, SBI-led bank consortium funding, tax recoveries and promoter support, to cover Rs 49,000 crore spectrum dues, Rs 45,000 crore capex and Rs 5,000-6,000 crore annual interest payments, while Q4 ARPU increased to Rs 174 from Rs 172 with 192.8 million subscribers.

Source: Mint- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

If you’re a woman who feels intimidated by the world of money, In Her Interest is meant for *you*.

Most women share a complicated relationship with money.

On one hand, women are expected to be exceptionally good with it. They manage household budgets, track expenses, stretch money, save for emergencies, and make a hundred tiny financial decisions every month.

When money conversations turn more formal, though; when they shift to investments, insurance, taxes, or business finances, they suddenly defer to someone else — a father, husband, brother, the family CA, or “the finance person” in the family.

To us, this weird duality seems to creep in because most women have never had a friendly, low-pressure place to learn their way around it.

That’s what In Her Interest, a Zerodha initiative, is trying to create. In Her Interest hosts small, in-person sessions where women can ask normal money questions without being judged, sold to, or drowned in jargon. The next few sessions cover finance for entrepreneurs in Gurugram, smart money management in Mumbai, investing basics in Pune, and the basics of mutual funds in Hyderabad. If you’re a woman who has been meaning to get a little more comfortable with money — or know someone who might — this is a fantastic place to start!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉