The dance of oil and the US dollar

The quiet fade of the petrodollar

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The dance of oil and the US dollar

The price of free water

The dance of oil and the US dollar

You’ve probably been hearing a lot about the petrodollar lately.

For over 50 years, most of the world’s oil trade has been executed in dollars. Every country that needed oil first had to acquire US dollars. Every country that sold oil accumulated those dollars, and then recycled them into US Treasury bonds. These bonds financed American deficits at cheap rates. This self-reinforcing loop was one of the most powerful structural props of the dollar’s global position.

However, the power of this mechanism, it seems, has diminished since then.

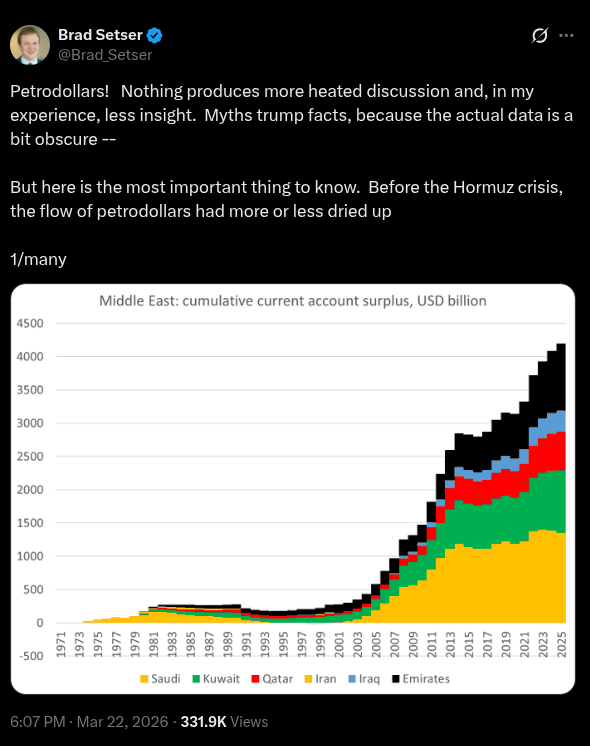

We saw a provocative thesis from Brad Setser, a former US Treasury economist. He said that the flow of petrodollars has “more or less dried up”. And this was even before the Strait of Hormuz crisis stranded much of the world’s energy supply.

In essence, he says that global oil trade isn’t as powerful a pillar for dollar dominance that it used to be.

Now, make no mistake, the American dollar is still the primary mode of deciding how oil should be priced. But then, what does the declining flow of the petrodollar even mean? And how does the current oil crisis change things?

Deal with the devil

Before we get into Setser’s thesis, let’s take a trip in time to understand how the petrodollar emerged.

In 1973, a coalition of Arab oil-rich countries, led by Saudi Arabia, halted oil exports to the US. They had cut supply in retaliation for American support of Israel, sending oil prices skyrocketing overnight.

The US economy, which imported a huge chunk of their oil, and was already struggling with high levels of inflation, now also saw huge fuel shortages. Moreover, even besides the high costs of imports, their currency was already under strain. By then, the global Bretton Woods standard, which the US had underpinned, had broken down, and other countries’ trust in the American dollar was low.

However, the crisis also handed Washington a strange opportunity.

See, Saudi Arabia had a problem of its own. With sky-high oil prices, it saw abnormal profits and tons of dollar reserves. However, that surplus got spent on things like construction and real estate, which aren’t tradeable. It couldn’t easily direct those funds into productive, tradeable things like clothes and toys. Without rising productivity and oil profits flowing only to a narrow section of society, Saudi had little escape.

This is a classic case of what economists call Dutch disease, where a resource boom overwhelms a country’s capacity to productively invest the proceeds. The dollars were piling up with nowhere useful to go. Both the US and Saudi Arabia needed an outlet.

That’s when William Simon, the US Treasury Secretary came up with an idea that would change global oil trade forever. It wasn’t exactly a contract set in stone, nor was it made public immediately. But basically, Washington had made “special commitments of financial confidentiality“ to the Saudis.

So while there aren’t handwritten details of the deal, here’s what the commitments amounted to. In exchange for US military protection and guaranteed weapons sales, Saudi Arabia agreed to price all its oil exports in US dollars and recycle its surplus oil revenues into US Treasury bonds. It would get a productive outlet for all the dollars it couldn’t use anywhere, plus a chance to build up its defense. The US, meanwhile, secured its energy needs.

Eventually, other oil-rich countries also followed Saudi’s footsteps. Now, the entire world would have to hold dollars to buy oil. That solidified the dollar’s status as the universal currency of oil (and global) trade. And then, those same dollars would be recycled into US treasuries, allowing the US to raise debt at extremely-cheap interest rates.

This deal had turned into a feedback loop that was near-impossible to undo. It is what many call America’s “exorbitant privilege“ — the ability to borrow in your own currency, at artificially cheap rates, because the whole world had no choice but to use the dollar. And Gulf nations like Saudi Arabia have accumulated massive amounts of dollar reserves since then.

Peak oil?

Let’s fast forward from 1973 to today, when petrodollar flows seem to have plateaued.

Last year, we covered how the world was facing a glut of oil. That had crashed oil prices down to $60–70 per barrel of oil.

At those prices, Brad Setser found that the exporters weren’t generating enough dollar surpluses to begin with. If anything, Saudi Arabia was actually running an external deficit. They were selling much of this oil below their fiscal break-even price. On aggregate, the two largest oil producers of the world, Saudi Arabia and Russia together, generated essentially zero petrodollars last year.

But here’s the thing: that doesn’t mean the dollar became less important.

Petro-equities

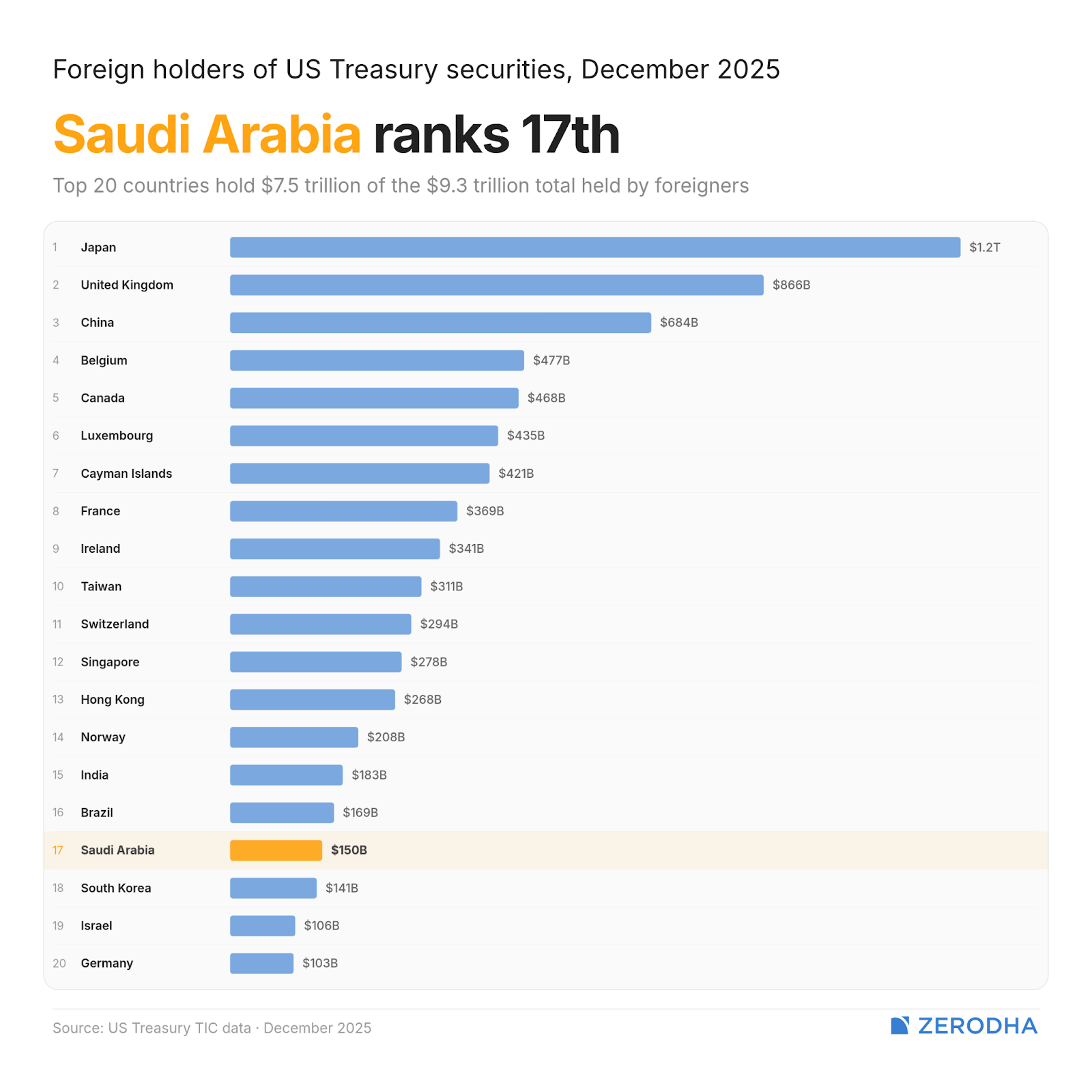

Lately, dollar surpluses haven’t been going to US treasuries like they used to. Gulf states no longer park most of their oil windfalls in US safe assets like treasuries and bonds — Saudi Arabia is the biggest of them, yet ranks 17th in the whole world.

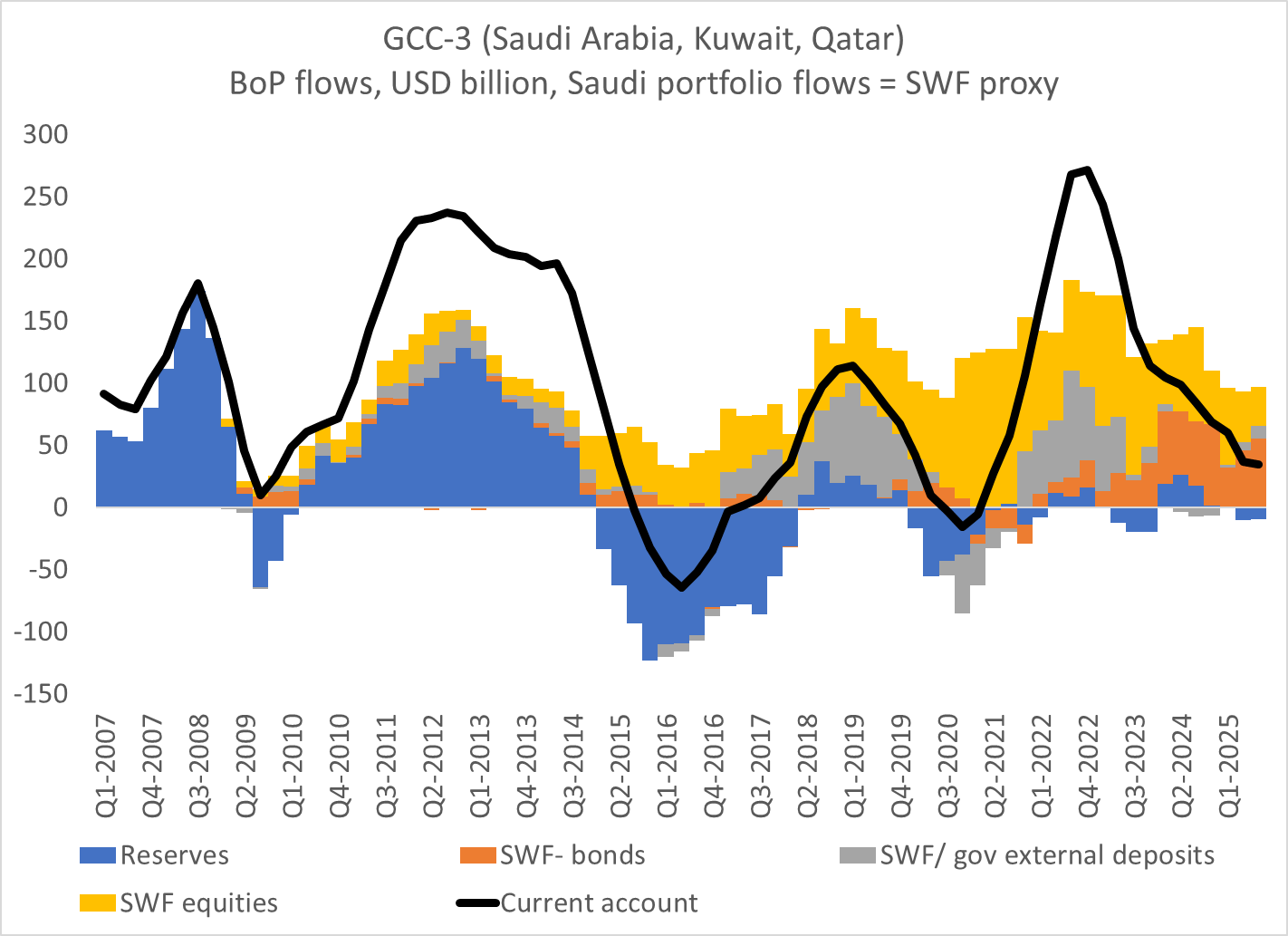

Rather, Gulf states channel their reserves through their own sovereign wealth funds (SWF) into global equities — or petro-equities.

For instance, Saudi’s PIF is one of the largest SWFs in the world, and holds billions of dollars in equities. Many of those stocks also happen to be American — like Big Tech companies, often considered among the healthiest assets in the world. The Gulf collectively controls over $4–5 trillion in SWF assets, with ~70% in equities, not fixed income.

This attempt at diversification by Gulf countries like Saudi Arabia and the UAE is one of the key reasons why the older petrodollar mechanism has basically broken down. However, that doesn’t mean they left the dollar ecosystem — on the contrary. Apple and NVIDIA are just as dollar-denominated as a Treasury bill.

The manufacturing dollar?

There is another structural shift that, while not directly related to oil, is just as important to the dollar.

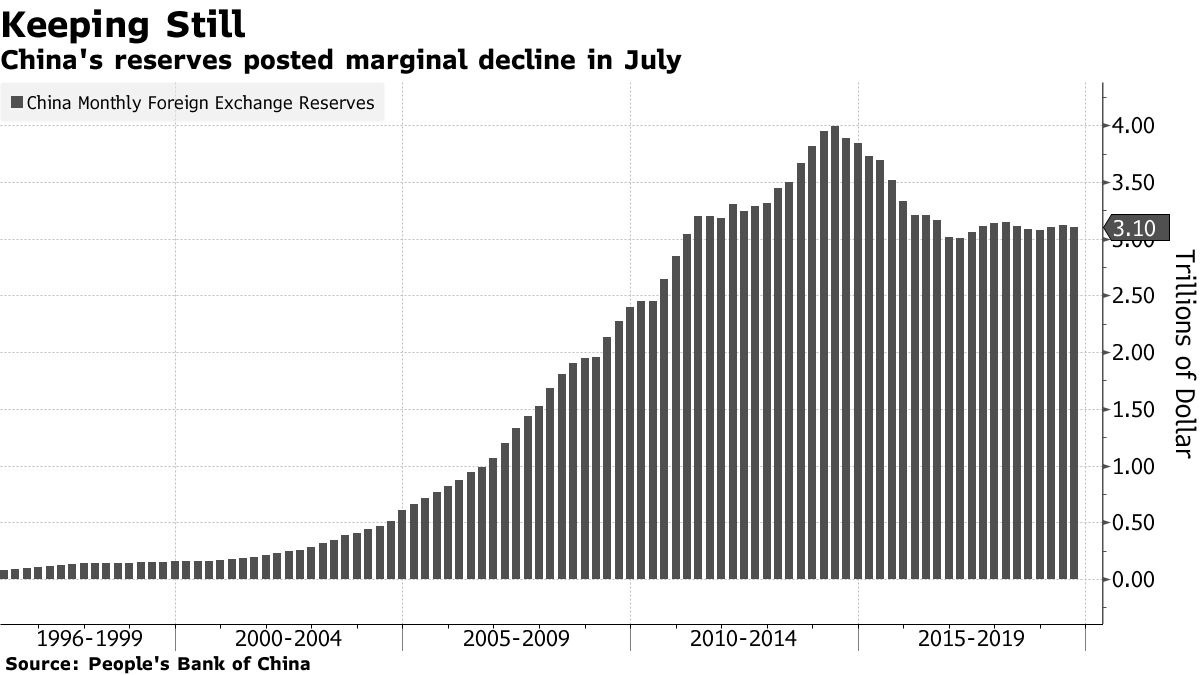

Not long ago, the Gulf had actually stopped being the primary engine of global dollar liquidity. Instead, the center of gravity had moved to the manufacturing-heavy economies of East Asia.

Countries like China, South Korea, and Taiwan collectively run reserves worth trillions of dollars. They had built up their economies by exporting productive, tradeable goods to the US, and generating dollars in return. They’re among the biggest owners of US treasuries today. Their sheer scale had made the petrodollar a sideshow.

It wouldn’t be a stretch to say that the world’s strongest manufacturing-led economies — especially China — now help prop up the dollar’s status. You might even call this the manufacturing dollar.

Here’s the picture you get when you add all this up: while the petrodollar became less important over time, the dollar itself hadn’t. It just no longer needed oil to stay on top; it had simply found other avenues. The dollar is used in 88% of all global foreign exchange transactions today.

Rhyme or repeat?

Today, the world is faced with what is perhaps the biggest oil shock since the one in 1973.

The Strait of Hormuz is the chokepoint through which ~20% of global petroleum flows every day. The conventional expectation from a Hormuz closure is a classic petrodollar moment: oil prices spike, Gulf exporters rake in dollars, those dollars flow into US assets, and the cycle reinforces dollar dominance.

But, in the new reality of the petrodollar, the consequences couldn’t be more different.

The Gulf countries whose oil exports are physically cut off by a Hormuz closure include Iraq, Kuwait, Qatar, and the UAE. Higher prices are meaningless to them if they can’t ship. Some may have to draw down existing reserves to cover government spending. This would actually reduce dollar assets in the system instead of adding to them.

According to Setser, Saudi Arabia may be able to find a different route that bypasses Hormuz. But even with higher prices, it needs oil well above $91 per barrel just to balance its budget, and oil isn’t there yet. With an SWF already borrowing to fund megaprojects, meaningful petrodollar recycling would require a sustained, dramatic price spike.

The actual winners from a Hormuz-driven shock, Setser says, are Russia, Kazakhstan, Azerbaijan, and Norway — oil exporters whose routes are untouched by the crisis.

But those windfalls won’t recycle into US Treasuries, either. Russian reserves are sanctioned. Central Asian states have limited dollar-recycling infrastructure. Norway’s sovereign fund buys US assets, but as a passive global investor, not as a structural supporter of the dollar system.

Perhaps, the biggest losers are in Asia. Higher oil prices balloon the energy import bills of India, Japan, and South Korea — shrinking their dollar surpluses. India’s own foreign exchange reserves are under significant strain, as we find ourselves selling the dollars we have just to keep the rupee propped up.

Changes and constants

The petrodollar gave the dollar its dominance through compulsion. Countries held dollars because they had no choice — oil was priced in dollars, and that was that. Saudi Arabia didn’t need to believe in American institutions. It just needed to sell crude and buy US treasuries in return.

That system doesn’t hold the strength that it used to. But in place of it exists a $35 trillion offshore dollar ecosystem and US equity market depth. These are institutions with global confidence and structurally more durable.

And even then, the petrodollar hasn’t fully gone away. They’re still invested in American assets — just their nature has changed. Many Gulf nations still store huge amounts of dollar reserves, even if their flow has reduced. Moreover, what if oil prices spike to such a high rate that Gulf countries generate obscene levels of dollar surpluses?

Be it 1973 or 2026, the dollar has remained constant, and will continue to be so for a good while.

We’re going to pause for a minute, here, to recommend another podcast.

If you’re a regular here, you know we absolutely love the million tiny details and factoids that go into making an actual business. But while there were fascinating projects that looked at international businesses through a microscope, India was largely ignored.

This isn’t because we didn’t have incredible businesses worth studying; just that nobody put in the work.

That is, until our friends at The Ken went for it. They’ve just started Intermission; a podcast that takes a deep, unhurried look at some of India’s most enduring companies. For their first episode, they did an incredibly seven hour long dive into Asian Paints. It is dripping with detail: from how the company began in a tiny Bombay garage, to how the second World War gave them their first break, to the incredible data-led innovations they made — decades before the rest of India’s business world caught on.

We’re getting nothing for talking about this, by the way. It’s just an incredibly cool project. We cannot be more thrilled to see things like this come out of India. Check it out!

The price of free water

The Sunday that just went by was World Water Day.

The day usually passes with well-meaning appeals — conserve, recycle, be mindful. But at this scale, problems can be so vast, and so existential, that it’s hard to do much more than despair. We’re not going to do that.

Instead, we’re looking at a recent report by the World Bank, which reframes a large part of the problem as a structural puzzle. The report argues that when it comes to agriculture, the world’s water crisis is not just a story about scarcity, but one about mispricing.

Growing food, across the world, is beset by contradictions. Many countries, including ours, are constantly drilling deeper into their scarce groundwater to grow food that is exported. Others sit on abundant, barely used water resources, but still import their food. These contradictions exist because water, in most of the world, isn’t treated as a resource, but as commons that everyone has a right over. Water is often priced at zero, or close enough. And tragically, commons are almost always mismanaged. The cost of that free water is deferred onto others.

Today, we’re going to understand the lens the World Bank applies here. No matter how you think about climate issues, it’s a worthy lens to have in your toolkit.

The gap

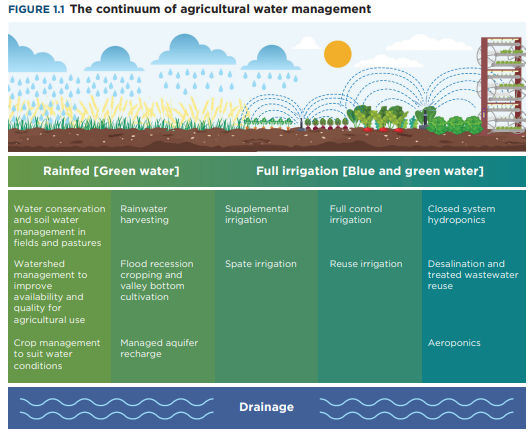

Agriculture uses more freshwater than any other human activity, by a wide margin.

According to the report, roughly 87% of all agricultural water is what hydrologists call “green water”: or the wetness in our soil that comes from rain, which crops absorb directly. The remaining 13% is “blue water”: water drawn from rivers, reservoirs, and underground aquifers, which then goes to fields through irrigation. While nature provides green water, where blue water goes is controlled by humans.

That tiny share of blue water punches above its weight. Less than 7% of the world’s total agricultural area is “irrigated land”, but that tiny sliver produces two-fifths of the world’s food. This is because rainfall can’t be timed like irrigation. Blue water can be delivered at exactly the right time, during specific growth stages when crops need it most. And so, the productivity of every litre goes up. You get more food per unit of water, and per unit of land.

There’s a problem, though: when humans direct water, they rarely think about how long they can do so sustainably.

The report estimates that today’s agricultural water management practices can sustainably feed about 3.4 billion people. We’re pushing it above 8 billion. By 2050, it will cater to close to ten. That is, we don’t have enough water to support half of today’s global food production. That’s a huge shortfall. We’re meeting it by eating into tomorrow’s water reserves: extracting groundwater faster than it recharges, using river water beyond what ecosystems downstream can absorb, or expanding farmland into areas that previously supported other ecosystems.

To us, this is an economic problem. Water is a scarce resource. In an ideal world, it would go to those who could use it the best.

Only, today, the world’s water is terribly misallocated. In some places, water scarcity isn’t a problem at all. Large parts of Sub-Saharan Africa, for instance, dramatically underuse their available water. Only 7% of the continent’s cultivated land is irrigated, despite shallow aquifers that could support up to 40 million hectares of new farmland. At the same time, other regions — parts of the Indian sub-continent, the Middle East, or North Africa — extract water far beyond what nature replenishes. Here, we’re tearing into aquifers that took millennia to fill.

That is, this isn’t just a simple problem of the planet lacking water for food. The truth is more interesting: too much water is being used where it is scarce, and too little is used where it is abundant. Something is off with the economic signals of agriculture: they point the opposite direction from what hydrology demands.

The four problems

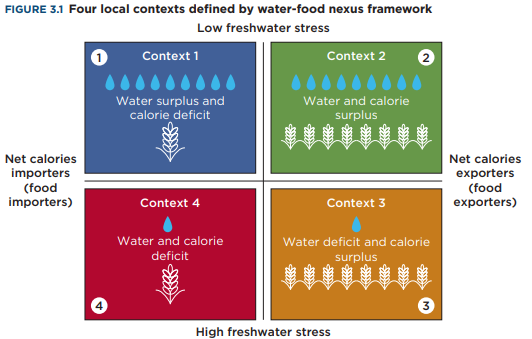

Here’s how the World Bank thinks about this. You can divide the world’s countries along two axes: how much water stress it faces, and whether it imports or exports food. This creates four quadrants: each showcasing a different relationship between water and food.

There are water-secure countries that import food. Much of Sub-Saharan Africa falls here. To them, there’s an opportunity ahead: they could expand irrigation, grow more food domestically, and reduce their dependence on imports. They already have the water: they just need the infrastructure, and the investment to use it.

Then come water-secure countries that export food — like France, or Peru. These are in the most comfortable position: they’re utilising their resources, but have headroom for more.

At the opposite end of the ledger are water-stressed countries that import food — like Morocco, or Spain. These are doubly vulnerable. They’re dependent on others for food; and they cannot farm their way out, because they don’t have the water for it. They’re constantly making painful decisions on where their water belongs: farms, cities, or nature.

But then, there’s the most interesting quadrant, and the one we care for the most: water-stressed countries that export food. India is here, alongside countries like Chile and Pakistan. There’s an inherent contradiction here: we’re using water we cannot replenish, to grow food we do not eat.

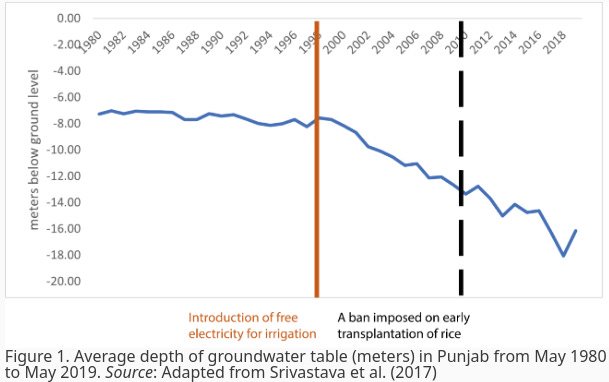

Consider India; last financial year, we exported roughly 20 million tonnes of rice, to over 170 countries. We have been the world’s largest rice exporter since 2012. Producing a kilogram of rice, in India, requires roughly 3,000–4,000 litres of water. That’s far higher than the world average; a result of the ‘continuous flooding’ under which paddy is grown in Punjab and Haryana. In that sense, when India exports rice, it’s actually exporting roughly ~50 billion m3 of water a year.

This is sending us, eyes open, into a terrible shortage. In Punjab, for instance, groundwater extraction runs at ~150% the speed of natural recharge. More than four of every five of its groundwater blocks are classified as “over-exploited”. Borewells that reached water at 30 feet, a decade ago, now need to go down as much as 200 feet.

This is a problem of bad incentives.

Hydrologically, Punjab is a bad place to grow rice. But the government has guaranteed paddy procurement, at an ever-increasing price. This makes rice the lowest-risk crop. Meanwhile, the government also provides free, unmetered electricity, which power 14 lakh tubewells — each of which run with no marginal cost.

And so, while every individual farmer is behaving rationally, the collective outcome hurts everyone in the long term. The World Bank’s report calls situations like this an “unsustainable contradiction.”

Breaking the deadlock

We aren’t unique in this. The world over, governments treat farmers as beneficiaries of a government scheme rather than customers of a water service. Water management, almost everywhere, follows the same pattern: design, build, neglect, and rebuild. There’s no attempt at cost recovery. There are no systems for measuring what is happening, and no regulatory body setting or enforcing standards. There’s also no attempt to maintain irrigation systems.

That creates twin problems. On the one hand, since nobody gains from maintaining water systems, these regularly degrade and break down. There’s no guarantee that, as a farmer, you’ll get water. If you do, on the other hand, there are no checks on overusing water.

This is an incentive problem. We know how to engineer irrigation systems, but because we see water as a political hand-out, we barely think about creating water institutions. There’s nobody that decides the price of water, who is accountable for its delivery, or who keeps the infrastructure alive.

The fact that we haven’t made these institutions, though, doesn’t mean they can’t exist.

The country of Georgia, in 2023, gave its energy and water regulatory commission the additional mandate of overseeing irrigation. Canal water, in effect, was now treated the way a regulator treats electricity or piped water. Farmers were charged tariffs for the full cost of operating and maintaining the system. This allowed for creative interventions: for instance, farmers who organised into ”water user groups” and took over parts of canal maintenance were given discounts. In other words, it flipped the incentive problem, creating financial rewards for better management.

The report has many such examples. World over, countries that have invested in institutions have managed to improve irrigation services, generate higher yields, and push farmers to make smarter investments. Without them, you get expensive government-funded assets that nobody takes care of.

What it would take

These institutions are going to become increasingly important as we head into the future. According to the World Bank, we’ll need to spend enormous amounts of money modernising irrigation, and making unsustainable irrigation systems more efficient. This will cost roughly 24 to 70 billion dollars a year over the next quarter century; coming to a total of somewhere between 600 billion and 1.8 trillion dollars through 2050.

We know, that sounds like an impossible amount of money.

But consider what the world already spends on agriculture. Across 90 countries studied by the World Bank, governments spent almost half a trillion dollars in agriculture in just 2023. Of that, about $27 billion went to irrigation. Three-quarters of the rest went into subsidies and price supports — the kind of spending that, in many countries, actively incentivises the misallocation the report describes.

With better institutions, we can channelise the same sort of spending into better results. The world needs, at least in part, to redirect money it is already spending — away from subsidies that encourage water-intensive farming in the wrong places, and toward the institutional and physical infrastructure that could make water-efficient farming viable.

Of course, none of this is simple. Redirecting agricultural subsidies is among the most politically difficult things a government can do, anywhere in the world. For instance, expert committees have been asking Indian states to rationalise power subsidies for decades, but the political incentive of keeping them around is simply too big.

But the counterfactual isn’t that the status quo continues indefinitely. It is that our aquifers run dry, and food systems slowly become unproductive. That future will be far harder to manage than a subsidy reform.

Tidbits

LPG supply strain

Oil companies may start filling only 10 kg in standard LPG cylinders instead of 14.2 kg to spread limited supply. Shipments via Hormuz are nearly halted, and supply is tight with only one day’s stock recently arriving. LPG use has already dropped 17% in early March.

Source: The Economic TimesKotak eyes Deutsche Bank India retail business

Kotak Mahindra Bank is set to buy Deutsche Bank’s India retail unit for about ₹4,500 crore. The deal includes branches, wealth assets, and retail/MSME loans. This continues Kotak’s push to grow its retail banking presence.

Source: ReutersGold prices crash sharply

Gold has fallen about 12% in a week, erasing all gains this year. Prices dropped due to fears that central banks may raise interest rates to tackle oil-driven inflation. A stronger dollar is also hurting gold demand.

Source:Business Today

- This edition of the newsletter was written by Manie and Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Fundamentally, we need to move away from Rice and Wheat crops who consume tons of water while nutritionally also not wholesome and move on to millets. These crops were initially promoted to tackle starvation during green revolution. Until strict policy decisions are taken, water will continue to be unsustainably used.