Social media's new legal problem

Product liability comes for the internet era

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The social media trials

Understanding the rupee’s nosedive

The social media trials

Last week, two juries in two American states delivered landmark verdicts against Meta within forty-eight hours of each other.

In New Mexico, investigators posed as children under fourteen on Instagram — only to be contacted by adults almost immediately. A jury saw this as clear evidence that Meta misled consumers about how safe their products were for children, ordering $375 million in penalties.

At almost the same time, in Los Angeles, another jury found that Meta and YouTube had designed their platforms negligently, letting them trap teenagers in addictive spirals. The case had run, with much fan fare, for the better part of five weeks — with Mark Zuckerberg himself testifying for two whole days.

Mark Zuckerberg heading out of court

The cases marked an interesting shift: so far, social media companies had been challenged on what users posted there, and the law almost always helped them skirt the issue. But there’s a new generation of cases where, increasingly, they’re being challenged on how the platforms themselves are built. That has been harder to shake off.

These cases target many of the things you and I have seen before, lakhs of times, that have become all but invisible. Why is there no bottom when you scroll, or no indication of how far you’ve gone? Why are you getting notifications in the middle of the night, at times that you shouldn’t be awake but are? Why, after just half an hour on an app, do you feel like you can’t get off it? Why are adults able to message children with no real controls?

These aren’t instances of offensive content; they’re engineering decisions. It’s the sort of thing companies haven’t always been sued for. But now that they are, they might find a minefield ahead.

The shield that protected internet companies

The legal foundation of social media was built in 1996. That was when Section 230 of the Communications Decency Act came into force.

This was when the very first generation of internet companies were coming to life. For the first time, you could create a platform where anyone at all could come and post something of their own. Their post would automatically appear on your platform, without you having to decide that it would. This was entirely unlike anything we knew to that point: radio, newspapers, television; everything else necessarily had gatekeepers. The internet did not.

This opened new doors. It laid the seed for everything from Instagram, to YouTube, to Reddit — but it came with a problem: what if you were made liable for whatever was found on your website? After all, if a magazine published something problematic, its publisher could be dragged to court. Why not a website publisher? Unless you vetted every single thing on your website, you could get into some nasty legal trouble.

The United States, however, created Section 230 as a “safe harbour” for its internet companies.

This law, functionally, ensured that internet platforms were legally not considered publishers. They were merely conduits. What they were creating was infrastructure, through which other people’s speech would flow. The content itself belonged to the user; the platform just gave it a space to exist. If someone was hurt by it, that harm came from the creator of that content, not the platform where they saw it.

Section 230 turned into the foundation of the internet. It ensured that a company like Facebook could not be sued for what its users posted. That was the only way it could grow to its current size. If lawmakers had decided differently, we would have a very different internet; with many small, heavily moderated websites.

The same logic slowly percolated to legal systems across the world. From the EU’s e-Commerce Directive of 2000, to India’s Information Technology Act from the same year, most internet laws that followed came with safe harbour provisions.

For the next two decades, when internet platforms were challenged in court for something they featured, the legal system would always point to the content creator. The platform would have to take down anything they were asked to, but that was where their responsibility ended.

Were social media companies clean?

Section 230 was, arguably, a necessary compromise. But as internet algorithms grew more complex, slowly, it was becoming harder to argue that the platforms were perfectly neutral.

What appears on your screen, when you open a social media app, isn’t just a random selection of what has been posted. It is chosen, sequenced, and timed by an algorithm. It is presented in a format that the platform decides. Those algorithms usually push you in a direction that serves the platform’s interest, not yours. They aren’t just passive; there are active engineering choices being made here.

So, if the platform causes harm — say, it pushes a teenager into addiction or depression — is it not at fault? What if there wasn’t any specific post that created the problem, but how the algorithm selected and delivered it? What if the way the app scrolled was designed for addiction? What if it specifically pushed particularly incendiary content, which took a constant emotional toll but kept people glued to their screens? These design choices are made consciously, in service of a business model. What responsibility do they come with?

This is the conceptual shift legal systems across the world are slowly inching towards. They’re slowly zooming out of whether individual posts are legally acceptable — to study social media platforms as systems. If a single post harms a user, that’s one thing. But if the product design causes foreseeable harm in how it presents those posts, that’s a different matter altogether.

At that point, it’s no longer a matter of media regulation at all. It’s a question of product liability: the kind of law that makes car manufacturers responsible for seatbelts, or pushes pharmaceutical companies to give warnings around side effects. Companies are responsible for the consequences of any dangers their products come with.

This idea started coming together, in the United States, back in 2021. Snapchat had come out with a ‘speed filter’ — a feature that displayed how fast users were driving. Teenagers started using the app behind the wheel, and in one such stunt, three died in a car crash where a teenager was driving at 107 miles-per-hour. The court found that there was no question of applying Section 230 here; this was clearly a result of the platform’s own design choices.

The same idea has since taken root elsewhere. The EU’s Digital Services Act, which came into force the same year, required platforms to assess and mitigate risks arising from how they were designed. Similarly, the UK’s Online Safety Act required platforms to consider specifically how their algorithms and functionalities affect users. Australia, meanwhile, simply banned children under sixteen from having accounts at all.

Across the world, slowly, platforms are losing what once felt like blanket protection.

What catalysed this shift? In great measure, it was what we learnt about the sheer extent to which platforms were willing to turn a blind eye to harm.

Meta researchers, for instance, joked internally that Instagram was a drug, and “we’re basically pushers.“ Other internal documents showed that the platform worsened the body image issues of one in three teen girls. The platform understood, perfectly well, that their users didn’t really know how to get around any of this. According to Facebook’s own estimates, one in eight of its users — hundreds of millions of people in the aggregate — had lost control over how much time they spent on the platform.

It wasn’t just Meta. TikTok’s internal documents, for instance, showed that it would only approve features that helped people manage their time if it reduced time-on-app by no more than 5%. That is, if a user spent four hours a day on the platform, it would only be fine with shaving off twelve minutes. This was despite the fact that it knew just how addictive the platform was, and how it could push people into suicidal states of mind.

Others, too, were willing to look past similar problems.

The issue wasn’t simply that harm had occurred — that companies had studied it, measured it, and then let it slide in order to boost engagement. This was where their liability came from.

How the world is responding

You’ve probably seen a constant stream of headlines, particularly since the beginning of this year, about rulings against social media companies. For now, most of these centre on a specific type of harm: how these apps harm the physical and mental safety of minors.

That is the culmination of this legal shift.

In February 2026, for instance, the European Commission told TikTok that the way the app was designed — with infinite scrolling, autoplay, and push notification systems — was inherently addictive, in a way that violated the law. The company has been ordered to change the basic design of its service. A new investigation into Snapchat on similar grounds followed soon after.

Meanwhile Brazil’s new internet law – the “ECA Digital” — kicked in this month. This bans social media companies from profiling the behaviour of minors to serve them content. It also requires them to ensure safety-by-design.

And then, there were the two cases Meta lost last week.

Currently, Indian law remains within the older content-specific framework. Recent legal changes — like amendments to India’s IT Rules — focus entirely on how quickly a platform removes flagged content, or the safeguards they must take around AI-generated material. So far, no discussion on the design of social media products has entered Indian law.

But here, too, early signs of that shift are visible. A parliamentary committee report tabled this month — on cyber safety for women — recommends that platforms be required to meet “safety-by-design standards” to protect the mental health of young users.

The big shift

We don’t want to be dramatic. This isn’t the death of social media or anything.

Any case on social media comes wrapped in all kinds of legal complications. Platforms’ involvement in any case is usually subtle, encoded in algorithms that are hard to decipher, and any legal suit can very quickly turn to questions of freedom of speech and expression. We aren’t expecting any large-scale legal pushback to social media any time soon.

But the shift is worth noting. One of the persistent features of the internet era is how the law has struggled to keep up with the sheer speed and intensity with which platform companies operated. The cases were so complex, and the allegations so abstract, that it was hard for legal systems to understand how to pin any blame on them.

They’re finally converging on an idea: look at how they engineer themselves. Things could soon get very interesting.

Understanding the rupee’s nosedive

A year ago, if you needed to send money abroad — to pay a child’s university fees, or to settle a dollar-denominated invoice — you would have exchanged rupees at around ₹85.5 to the dollar. Today, that same dollar costs a little over ₹94, making a lot of Indian imports more expensive. In turn, that has raised the prices of electronics, medicines with imported ingredients, and even airline tickets that cost more because of pricier aviation fuel.

Much of the coverage around this frames this as an oil story. The Middle East war pushed oil above $100 a barrel, India’s import bill swelled, and the rupee fell. And for what it’s worth, that’s true. But it’s only a part of the story. What makes India’s situation specifically worse than most of its neighbors.

The rupee was already the weakest in Asia.

In the last year, most Asian currencies strengthened against the dollar over this period. This means the dollar got cheaper for those countries, which reduces pressure on their central banks and makes their imports less expensive.

But India went almost exactly the other way.

The rupee weakened by 10%, making it the worst-performing major currency in Asia by some distance. And critically, most of that weakness arrived before the war. The conflict began in late February — by that point, the rupee had already slipped from ₹85.5 to ₹91. The war then accelerated what was already happening, pushing the rupee past ₹93 in under four weeks. That’s the near-vertical line on the chart, indicating the nosedive it took when it met a major external shock.

Clearly, there’s a part of this depreciation that cannot be explained by the oil shock alone. And that’s what we’ll be getting into first.

How the exchange rate works

See, every time India imports something — oil, electronics, gold — the importer needs dollars, which means selling rupees. More import demand means more rupee-selling, which means the rupee gets cheaper. Conversely, every time a foreign investor buys Indian stocks or bonds, they are buying rupees, which supports the currency.

The RBI sits in this market as a stabilizer, selling dollars from its reserves when the rupee is falling too fast. For instance, India’s foreign exchange reserves fell from $728.5 billion in the week ending February 27 to $709.8 billion by March 13 — a drop of nearly $19 billion in two weeks. Much of it was due to the RBI selling dollars to prop up the rupee. It’s difficult for the RBI to reverse the underlying forces. At best, it can hope to slow them down.

Now, India imports about 85% of its crude oil. When prices spike, importers need more dollars, and the rupee weakens. Simultaneously, foreign portfolio investors get nervous and pull money out. For instance, foreign portfolio investors pulled $10.8 billion out of India in the first eighteen days of March alone — roughly the entire year’s outflows crammed into three weeks.

But as per research by MUFG Bank, one of Japan’s largest banks, framing this purely as an oil story misses India’s deeper vulnerability. India’s exposure to the Middle East runs through at least four other channels that are less visible, but are already transmitting the crisis into the Indian economy.

Four horsemen of the rupee apocalypse

The first channel is LPG — the gas in the cylinder in your kitchen.

Most of India’s LPG comes from the Middle East. Now, crude oil can still be rerouted: India has been buying Russian crude in bulk at a discount since 2022. But LPG can’t switch paths as easily. It requires specialised refrigerated tankers, the global spot market for it is thin, and India’s import infrastructure is deeply tied to Gulf sources.

The second channel is natural gas.

Around 60% of India’s imports of liquified natural gas (LNG) travel through the Strait of Hormuz. Most of that comes from a single country — Qatar. Unlike oil, and much like LPG, you cannot simply divert an LNG tanker. The infrastructure is built around fixed receiving terminals, and switching suppliers takes months or years.

When the Strait became unsafe, Petronet invoked force majeure on March 3, a declaration that extraordinary circumstances had made its contracts impossible to fulfil. As we covered before, GAIL immediately began rationing gas to industrial customers.

The third channel flows from the second. Natural gas is the primary raw material for urea, India’s most widely used fertilizer. Cut the gas supply and domestic urea production could fall. But that’s not the end of the story.

See, beyond urea, the Gulf nations also account for about 40% of India’s finished fertiliser imports — far more than most other Asian economies. That, in turn, impacts on food production costs significantly. MUFG flags this as a delayed risk: the shock arrives in March, but its effect on food prices will only become visible when the kharif sowing season begins in June and farmers are buying fertilizer they may not be able to afford.

The fourth channel is remittances. More than half of all Indians working overseas are based out of the Gulf region. Then, it’s no surprise that around 30% of the money Indians working abroad send home comes from there, too. These remittances partially offset the current account deficit every year by bringing dollars steadily into the economy. But if the crisis disrupts employment and earnings for Gulf-based Indian workers, those flows shrink.

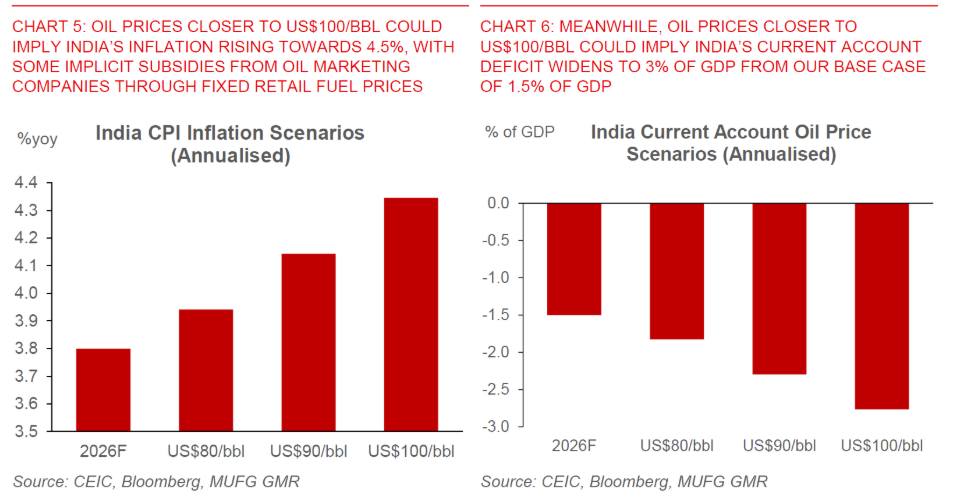

What the numbers show

MUFG estimates that every $10 rise in oil prices widens India’s current account deficit by about 0.4 to 0.5 percentage points of GDP. India’s current account deficit was already 1.3% of GDP in the third quarter of this financial year. If oil holds around $100 a barrel, MUFG estimates the deficit could widen to nearly 3% of GDP. That means India structurally needs more dollars than it earns, and the exchange rate must keep adjusting to reflect that.

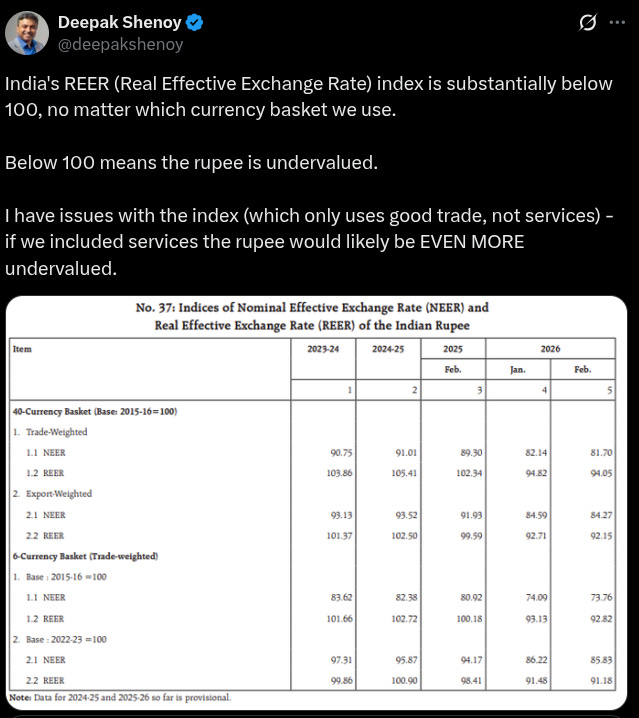

The RBI has its own measure of the rupee’s overall value, called the Real Effective Exchange Rate (REER). It tracks the rupee against forty trading-partner currencies and adjusts for inflation differences. Above 100 means overvalued relative to historical average; below 100 means undervalued.

The REER fell from 102.3 in February 2025 to 94.1 in February 2026. Indian goods and assets are currently on sale for the rest of the world. Deepak Shenoy of Capitalmind has pointed out that even this reading likely understates the undervaluation, since the index only accounts for goods trade and not services — and India’s services exports are enormous.

Conclusion

If the rupee is clearly undervalued, a recovery should be expected. But the forces driving it down are currently stronger than the valuation forces that would normally pull it back up.

When a currency falls this far, the standard expectation is self-correction. Indian exports get more competitive, capital is attracted back in by cheap valuations, and the currency recovers. If the REER data is to be believed, this correction is overdue.

But that recovery requires the world to believe the worst is over — that oil will fall and supply routes will reopen. None of that is settled, and the duration of the crisis is the one variable nobody can predict. If the Strait remains disrupted into May, the effects compound. Each week of constrained LPG supply, each fertiliser plant running at 65% capacity — these are not separate problems. They arrive through different pipes but they are all flowing in the same direction.

The RBI’s own March 2026 Bulletin is candid about the limits of what it currently knows. The analysis, it says, “primarily pertains to the month of February and as such does not cover the full impact of the Middle East conflict. The impact of the conflict would be covered more in the next issue once the data for the month of March are available.”

Basically, the institution responsible for managing the rupee is telling us that the worst of what has happened in March has not yet been formally measured.

India carried vulnerabilities that existed before today. But the crisis in West Asia made them visible all at once.

Tidbits

[1] India’s first large private gold mine set to start in Andhra

Commercial production is set to begin at the Jonnagiri gold mine in Andhra Pradesh—India’s first large private gold project since Independence. Output is expected at ~600 kg by FY27, with plans to scale to 2 tonnes annually, potentially making it India’s largest producer and reducing import dependence.

Source: Business Standard

[2] CCI clears MUFG’s ₹39,618 crore stake in Shriram Finance

The CCI has approved MUFG’s ₹39,618 crore investment for a 20% stake in Shriram Finance—the largest FDI in India’s financial sector. The deal will boost Shriram’s capital base, lower funding costs, and help it compete more aggressively in MSME, gold and retail lending.

Source: BusinessLine

[3] Govt keeps RBI’s inflation target at 4% till 2031

The government has asked the RBI to maintain retail inflation at 4% (±2%) for another five years till March 2031, extending the current framework. The move ensures policy continuity and stability, with inflation targeting remaining India’s core monetary policy approach since 2016.

Source: The Hindu

- This edition of the newsletter was written by Pranav and Krishna.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

This is so well written, it's the first post I've read from your account and I'm definitely looking to read more