SBI Funds is going public

Plus: Why it’s so hard to gather land in India

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

SBI Funds is going public

Why it’s so hard to gather land in India

SBI Funds is going public

SBI Funds Management’s IPO opens today, and it comes to market as the largest asset manager in India. It has held the top spot since 2021, and the prospectus opens with a very big number: it manages around ₹29.5 lakh crore.

But there’s a catch.

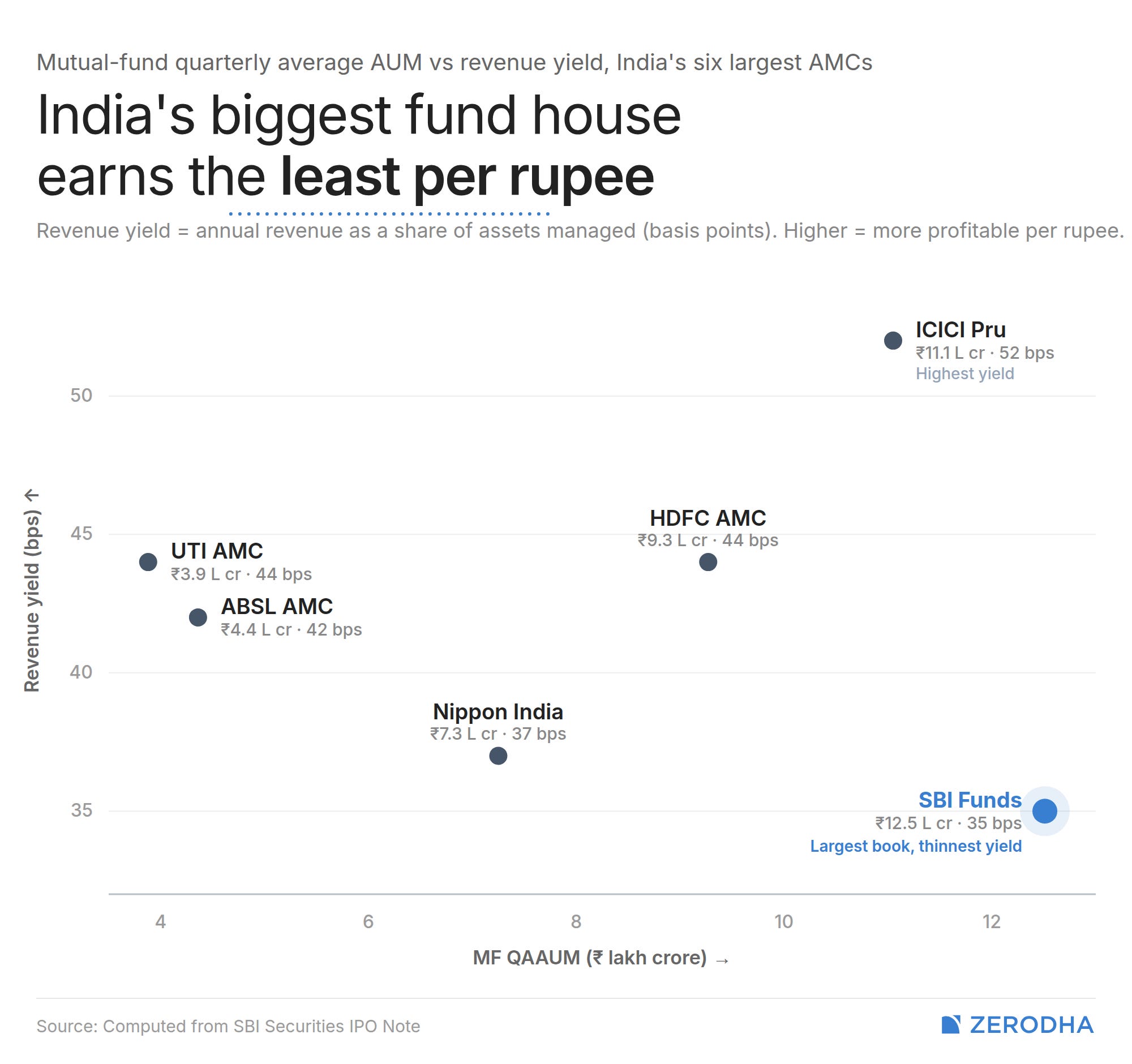

While SBI manages more money than its peers, ICICI Prudential or HDFC AMC, it earns less revenue than them. This is not a knock on the company, but a signal that “largest” is a slippery word in this business. The SBI Funds business is far more nuanced than the headline assets-under-management (AUM) number.

When ICICI Prudential’s AMC listed last year, we used its prospectus to walk through how an asset manager makes money in the first place. We won’t repeat the basics here. This piece is about what makes SBI its own kind of animal.

Not all AUM is the same money

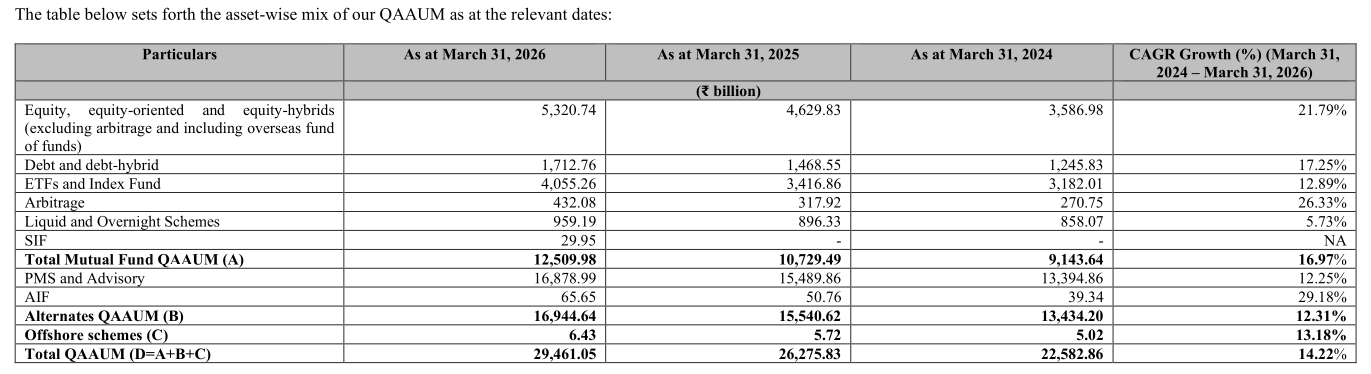

Start with that ₹29.5 lakh crore.

It isn’t a single pool. Only about ₹12.5 lakh crore of it is actual mutual-fund money. The bigger chunk of roughly ₹16.9 lakh crore sits in portfolio management services (PMS) and advisory. SBI is, in fact, the country’s largest PMS manager, with close to 40% of the market.

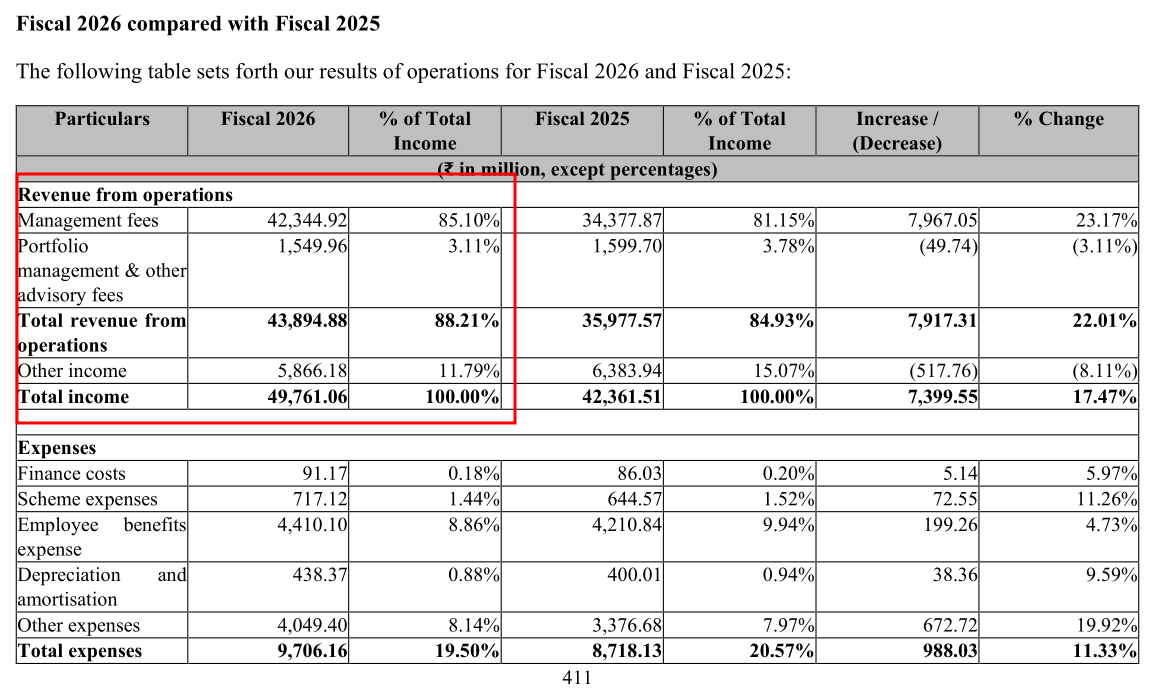

That sounds like a diversified franchise, but of SBI’s roughly ₹4,400 crore in operating revenue, around 96% comes from the mutual-fund business. That enormous PMS-and-advisory book brings in only around ₹155 crore of profit: measly in relation to the revenue.

The reason is that most of it is low-margin institutional money — basically, statutory and provident-fund-style mandates from EPFO that arrive in gigantic size but pay next to nothing. For context, our back of the envelope calculations tells us that, SBI earns around 35 paise a year for every ₹100 mutual funds it manages. On everything else, it earns close to a single paisa.

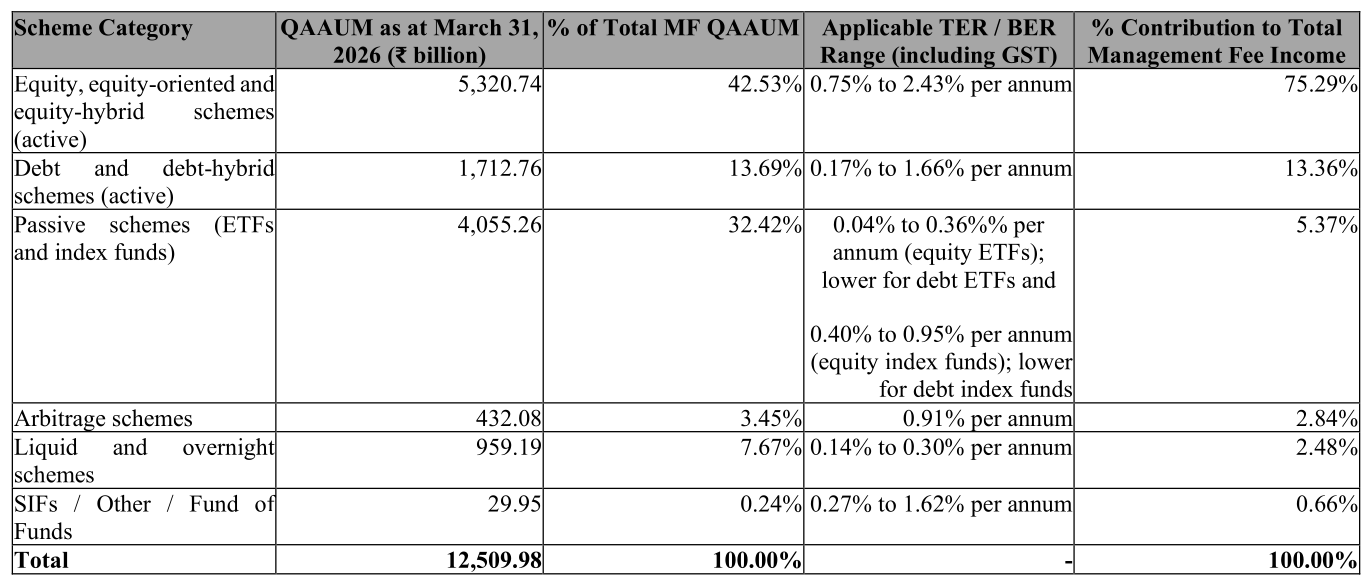

Clearly, not all AUM is the same, and that’s true even inside the mutual-fund book. Active equity funds, where a manager actually picks stocks and charges a real fee for it, make up about 42.5% of the mutual-fund AUM but throw off roughly three-quarters of its fees. Passive funds, which are index funds and ETFs that just track a benchmark cheaply, are about a third of the book but contribute barely 5% of the fees. A rupee parked in an active equity fund is worth around ten times a rupee parked in a passive one.

This is the thread that explains why SBI’s peers seem to fare better on revenue. While it earns about 35 basis points on its mutual-fund assets, ICICI earns around 52, and HDFC around 44. That gap is easily explained by what kind of money each one holds: active equity is a much larger portion of the book for ICICI and HDFC compared to SBI’s.

None of this makes SBI a worse business, but just a different one. It got to be the biggest partly by piling up low-hanging fruit like huge passive and institutional books. But the trade-off is that that’s exactly the money that drags down what it earns per rupee. Simply, this is a volume-rather-than-value play.

The one number moving in its favour

If that were the whole story, SBI would look like a giant slowly being out-monetised. But the mix has been shifting, and in the right direction.

Between FY24 and FY26, SBI’s equity-oriented assets grew at 22% a year. In comparison, its passive assets grew around 13%, and its low-fee liquid funds crawled along at under 6%. The share of equities in the mutual-fund book rose from 39% to 42.5%; passive’s share actually fell. As a result, the fee it earns on each rupee climbed up.

The shift might sound small, but it’s also why SBI’s revenue compounded at nearly 28% a year over that stretch, even though its assets grew only about 17%. The company didn’t just gather more money; the average rupee it manages became more valuable.

What the prospectus doesn’t tell us is how much of this is SBI winning new customer money, versus a rising stock market simply lifting the value of what it already held. A bull run flatters both the mix and the fee yield without proving the company is taking market share.

The real edge

In asset management, price is a weak weapon. Fees are largely set by the regulator, while competitive pressure does the rest, so nearly no one has pricing power. What you can control is cost, and this is the one dimension where SBI is genuinely, measurably ahead of everyone.

SBI’s operating costs run at about 8 basis points of assets, the lowest among the ten largest AMCs (all of which operate on 10-25 basis points). Its core operating margin sits near 79%. Once the research team, the compliance systems, the technology and the distribution machine are built, another ₹10,000 crore of assets costs almost nothing extra to run. The whole thing is a fixed-cost factory, and SBI’s is the biggest and cheapest one on the street.

Now, the top three AMCs have held roughly 40% of the market for years, and small, nimble players have been gaining share. But the mid-sized firms in between have been steadily squeezed, with their combined share sliding from about 41% to 36% in five years. There are giants at one end, niche specialists at the other, and a thinning middle class. In a world where fees only ever fall, the least efficient managers get squeezed first, and SBI’s cost base means it can absorb that pressure longer than almost anyone.

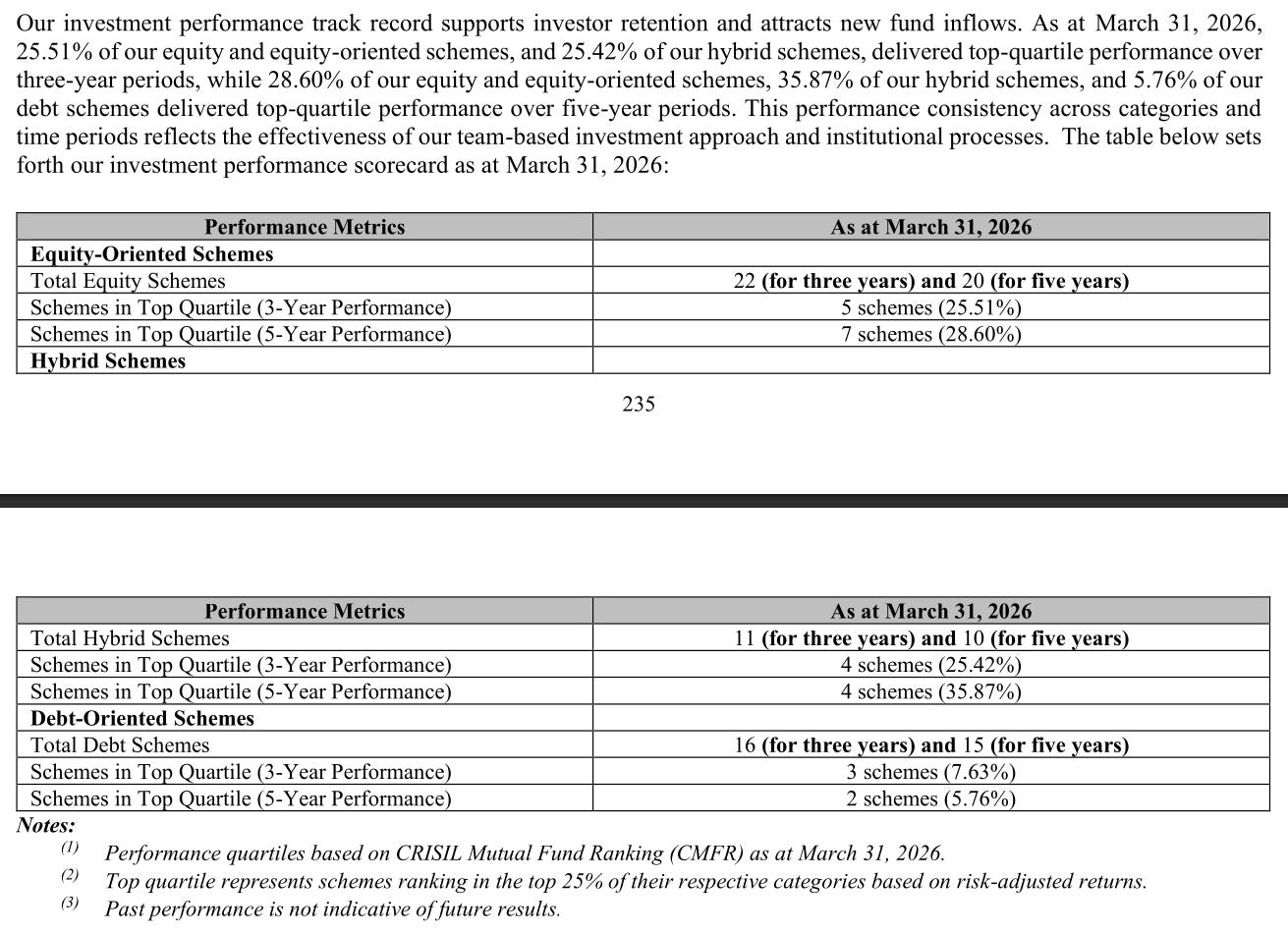

Also, notice what the moat is not. It isn’t investment brilliance. SBI’s own disclosures show about a quarter of its equity schemes land in the top quartile of performance.

What that means is SBI became the biggest AMC in the country without demonstrably beating its peers at investing. That’s the clearest possible evidence that in Indian asset management, distribution and trust is equally, if not more important than just performance.

The reach goes wide, not deep

The second half of the moat is distribution, and it’s strongest exactly where the industry is thinnest: outside India’s biggest cities.

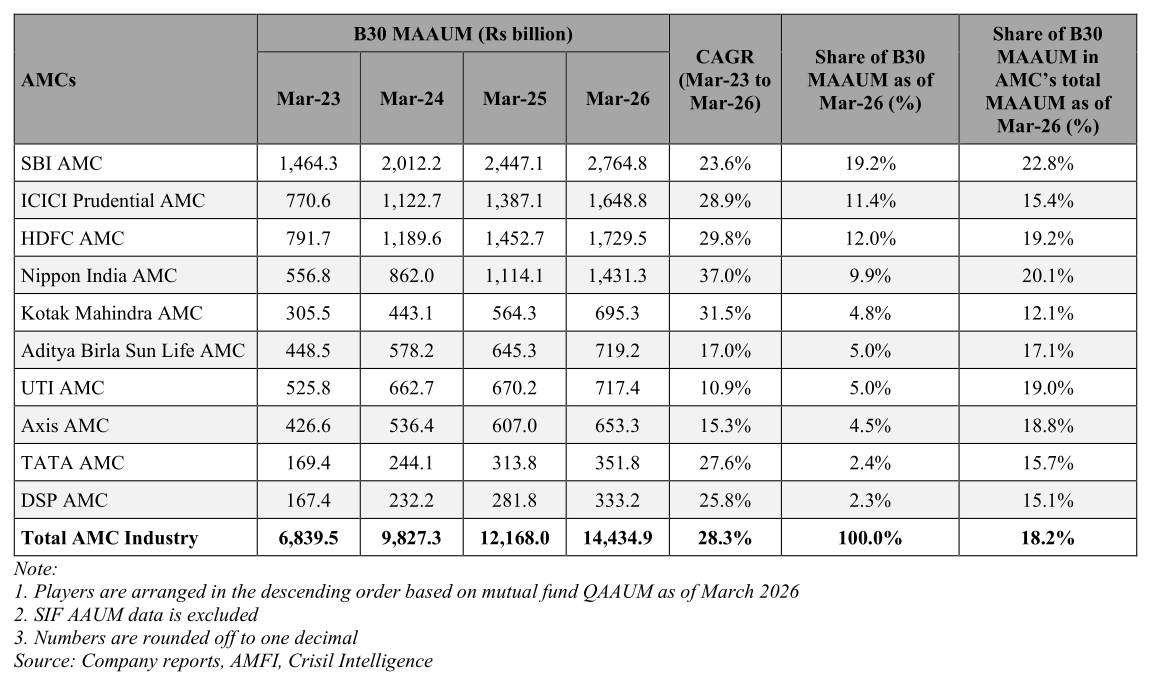

The RBI classifies everything beyond the top 30 cities as “B30“, and this is SBI’s home turf. B30 makes up about 22.8% of its assets against an industry average near 18%, and about two-thirds of its systematic investment plans originate there. In smaller towns trust matters more, making it difficult for SBI’s peers to replicate this success.

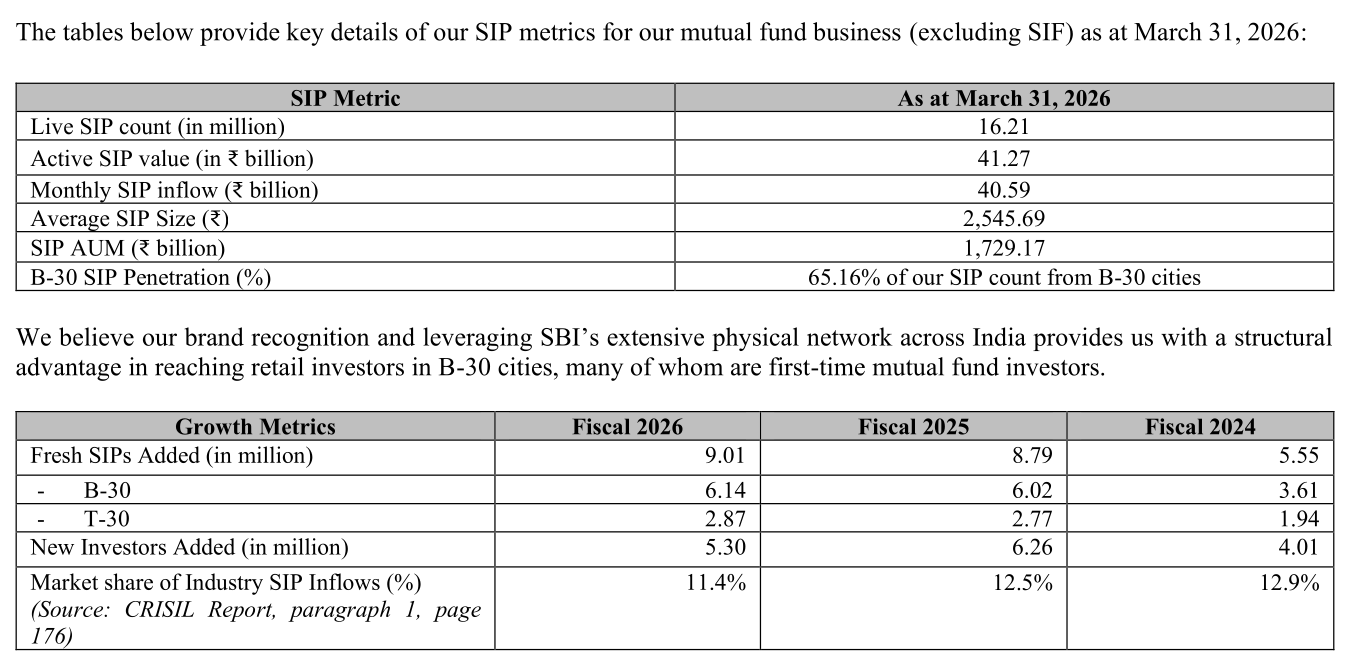

But that reach shows up as breadth far more than depth. SBI runs about 1.6 crore live SIPs pulling in roughly ₹4,000 crore a month, and has about 15.5% of the industry’s SIP accounts but only 11.4% of its SIP money. The average SBI SIP is roughly a quarter smaller than the industry’s. Its share of SIP rupees has also been slipping, from 12.9% in FY24 to 11.4% in FY26.

So, it’s winning accounts faster than it’s winning money. That also corroborates with the higher market share in B-30 cities, because those cities are likely to have investors starting their journey with smaller amounts. But it also points to data where SBI needs to nudge small tickets upward, adding step-ups, and selling more products per customer.

Growth levers

An AMC has only two real levers: manage more money, or earn more on the money it manages. SBI is already number one on the former, so raw asset growth is the slower, defensive game. The richer lever lies in the latter, which is a mix of a) converting its vast low-fee base into higher-fee active equity, and b) affluent-customer products.

That mix explains all the shiny new categories in SBI’s prospectus. It touts leadership in specialised investment funds (a new SEBI-created category), fast growth in alternative investment funds (AIFs), offshore products including GIFT City offerings.

These are genuinely higher-fee businesses but every one of them is tiny today. Its 28% share of the SIF market is a share of an industry barely ₹10,000 crore in size, and its AIF book is about 0.2% of total assets. This is optionality, not earnings. For now, SBI is still a scale-and-cost story rather than a premium-fee one.

Pushing the other way is a headwind that lands right after the numbers on display. FY26, the last year in the prospectus, happens to be the best-looking year in the book, with the highest fee yield, the highest margin, and the fastest revenue growth. But all of this predates SEBI’s new Base Expense Ratio (BER) framework, which took effect on 1 April 2026, and will trim what levers funds can charge. FY26 shows none of it. But at SBI’s scale, the number can be unforgiving because every single basis point shaved off its fee yield is worth about ₹125 crore of revenue.

Reading the numbers

A couple of the celebrated headline figures need a second look.

The first is which profit to use. SBI reported PAT of about ₹3,067 crore, but that includes income from its own treasury and investment portfolio. Minus those, the fund-management franchise itself is closer to ₹2,606 crore. That’s pure operating profit.

The second is the eye-catching 43% return on equity, up from about 34% a year earlier. Some of that jump is mechanical rather than a genuine leap in profitability. Ahead of the IPO, SBI Funds paid out a dividend of roughly ₹5,515 crore — about 1.8 times its annual profit — funded partly by selling its investment portfolio. That shrank the company’s equity base from around ₹8,300 crore to under ₹6,000 crore. So a smaller denominator increases the return-on-equity ratio even if the underlying business hasn’t changed.

Beyond these numbers, though, at the very core, SBI Funds is a very particular kind of business. It’s not the best stock-picker, nor is it a proprietary tech platform. But it is a trust-and-cost machine that works at a scale nobody else can match.

The conundrum the IPO poses is whether SBI can turn its enormous base of small, low-fee relationships into higher-value ones faster than regulation, while also managing the mix between active and passive that determines what it earns on every rupee of AUM.

Why land is a nightmare in India

Land, in India, can be a nightmare.

Just last month, a thousand tractors rolled into Gandhinagar. Farmers across Gujarat were protesting the high-tension power lines being run across their fields to carry electricity out of the state’s solar and wind projects.

In 2015, the newly divided Andhra Pradesh tried to build a new capital city in Amravati without taking anyone’s land by force. Farmers pooled some 34,000 acres, anticipating that the new capital would make their land appreciate. But the project soon fell into an extended limbo, sparking half a decade of protests. When it returned, the state had to acquire around 1,800 acres compulsorily from those that lost trust in the scheme.

Sometimes, land is acquired, only to lie vacant later. Karnataka, for instance, had acquired a plot of land for an infrastructure corridor in 2008. Only, it stood vacant for the next seventeen years, until the Karnataka High Court asked for it to be released once again.

Often, if land is not vacant, it’s bogged down by corruption and malfeasance. In Greater Noida, for instance, the national auditor found that nearly half of around 2,580 plots the government had acquired lacked a working unit, while the rest had irregularities of all sorts — from payment issues to unauthorised transfers.

For our economy to develop, we need land to go into productive projects. Only, the process of acquiring land regularly falls apart, at multiple junctures. In fact, we have no idea how bad the problem even is. There’s simply no public data on how India’s land is put together, and in what manner. Information is scattered across separate sectoral systems, which have never been put together.

There are at least two challenges we see, however: how does one assemble land, and how does one turn that land into something you can actually build on. This is what we’re discussing today.

Hurdle 1: Getting land

Of all the things a flourishing economy needs, land is arguably the hardest to put together. You can’t manufacture it. You can’t move it from place to place. From highways to factories, everything needs an unbroken block of land, often just in the right place.

Only, getting that land often feels impossible. Large parts of our country are split into innumerable, tiny parcels of land. It’s hard to know who any parcel of land belongs to. There’s no authoritative record that tracks every inheritance, sale or family partition. Even government land records don’t prove ownership over land. In many places, in fact, there’s a clear mismatch between what a map shows, and what the registers say.

Even if you know who to buy land from, there’s no guarantee you’ll get it.

There is, of course, the problem of hold-outs — a fact that exists everywhere land is privately held. Imagine you’re building a factory that needs 200 plots of land in one continuous stretch. You could get 199 of 200 of those plots, and yet, if a single owner in the middle says no, the whole project could stall. The more fragmented that land is, the worse the problem gets. In India, where land is often shared by several people at once, this gives a large number of people a veto over any project.

To complicate things further, even if you can agree to buy land, there are state rules that can come in the way. Some states, for instance, restrict purchases of farm land by non-agriculturists. Others set ceilings. There are few guarantees that you can get the land you need.

What can one do? Often, the answer is to get the government to do that dirty work.

This began with an old 1894 law that granted the British colonial government the power to compulsorily take people’s land away. Instead of having to hunt for each land owner and strike a separate voluntary deal with them, this law allowed the government to set up a single compulsory process for a tract of land — and once that was done, it could simply take possession. All the old claims that were attached to that land would fall off. The government would get clean title, while any old disputes over land would become disputes over who was owed compensation. This land could then be used for public works, industrial estates, townships, or projects whose eventual users were private companies.

The colonial-era law was replaced in 2013, by a statute that made acquisition more demanding, expensive and consultative. It even asks governments to take only the minimum land needed, and to lease rather than buy where they can. But the fundamental power — of taking people’s land without seeking their consent — was retained.

To be clear, this is not unique to India. Most parts of the world permit compulsory acquisition of land, at least as a backstop. In England, official guidance tells authorities to make a genuine effort to buy by agreement — but if negotiation fails, in parallel, they also prepare a compulsory purchase order.

The question, in India, is why that backstop has become the ordinary route to get land.

Hurdle 2: Owning land alone doesn’t let you build

Let’s say you own a factory, and the state has given you a hundred acres of claims-free land. The hard part still isn’t behind you. Ownership is only one of the rights you need over land — you also need permission to use the land how you want.

If you’ve bought farmland, for instance, it has to be formally converted to industrial or residential us in the government’s revenue system. Separately, your use of that land needs to conform to the area’s master plan. Both are run by separate agencies. The parcel could clear one test and fail the other. You can convert your field and still find the plan doesn’t permit a factory there; the plan can zone your area for industry while the revenue record still calls it farmland.

This mismatch is changing in some states. Late last year, for instance, Karnataka reformed its revenue rules — now, if a master plan demarcates an area for industrial development, it can be converted from agricultural to industrial land without special permission from the deputy commissioner. But this only goes to show how bad things were before.

At around the same time, the Karnataka high court was dealing with a different variant of the same problem: it found that land records, forest boundaries and planning zones worked on completely different maps, which described the same parcels differently. Highlighting this as a systemic failure, it asked the government to unify these into a single record.

Effectively, you can do everything right — buy the land legally, from the right person, at a fair price — and still not have a right to develop that land as you see fit.

This is separate from the other touchpoints where you must interact with the government. You need a road to the site, and power and water to the edge of it. Depending on the project you may also need environmental approval, pollution-control consent, forest clearance, or permission to draw water. Separate agencies control all of this. Much of it is discretionary — and a clearance from one doesn’t guarantee approval from the next. There’s no way to simply look at a map and know what one can do.

Hurdle 3: Why develop when you can hoard?

Because these issues were formidable, India built a class of institutions — often in the form of industrial development associations, like KIADB, MIDC, or the Noida authority — to get around them.

These entities assemble a contiguous site, designate it for industry, lay the internal roads and utilities, divide it into plots, and allot those plots on lease or sale. What they offer isn’t land alone, but land with most of the legal and physical work already done. That is a massive relief for any investor.

But this, too, can break.

For one, Take KIADB. The state auditor found it holding around 6,600 acres of developed land lying unused, and more than 30,000 acres undeveloped. Some of it is lying waiting for infrastructure, some is tied up in litigation, some is held for later phases. At every stage — possession, building approval, production — there were fewer and fewer plots that had gone through. The body, the auditor found, even lacked a proper inventory of what it owned.

What holds projects like this up?

The story of Greater Noida gives us a hint. Industrial plots are cheap by design — sold at an administered price meant to lure industry. This, however, makes the plot worth more than it cost, almost from the first day. For many allottees, it paid more to hold on to an industrial plot without building than actually building anything. These became speculative assets. If you build a factory, you take on demand risk, construction risk and years of sunk, illiquid capital. But instead, you could keep the empty plot, wait for the area around it to develop and values to climb, then seek a transfer. Authorities failed to cancel these allotments and take the land back.

Authorities, it turned out, acquired only one skill — acquiring land and allotting it. This was politically rewarding. The work of cancelling idle allotments, clawing land back, and fighting lawsuits, on the other hand, is thankless. And so, they never managed to succeed at actually ensuring that somebody actually built on that land.

Is there another way?

If we want to break away from this logjam, what other models can we follow?

The best alternative is land pooling. Here, a number of farmers can give their land into a common pool. The government can turn part of that pooled land into roads, drains and public space. Some can be sold to raise revenues. The rest can be handed back to the original owners. The plots are now smaller, but with roads, water and power, can be worth much more.

Some parts of India already have such programs in place. Gujarat, for instance, has used town-planning schemes to reshape its cities this way for decades.

This is a gentler method than taking land outright. But to run such programs, you need trust. Take the case of Japan, which has followed this model for over a century. Its land pools begin with a credible, binding plan, and precise land records. It then has rules around valuation and settlement, so that nobody feels cheated. And it has run these programs through authorities that have won a reputation of delivering. If you can’t win trust, pooling projects can fall apart — as one saw in Amravati.

Moreover, pooling only works in some types of projects. For infrastructure projects — like highways or power lines — you often need a thin but long strip of land. Sometimes you need even less. For underground pipes, for instance, you just need a right to lay and maintain the pipe, and nothing else.

A fundamental challenge

Land acquisition, to some extent, is a challenge that simply can’t be wished away. Most countries across the world deal with some variation of these problems.

But there are ways of doing it better. India has routinely reached for the heaviest answer to the challenge of collecting land. This is often because of failures elsewhere down the line: inaccurate data, unreliable authorities, byzantine regulation, and more.

Put differently, the challenge in gathering enough land, in India, isn’t the availability of land itself. It is everything else it takes to actually build on it.

Tidbits:

1. India’s ONGC is planning to build a massive 175-million-ton strategic oil reserve to strengthen the country’s energy security. This major infrastructure project aims to act as an important buffer against future global oil supply disruptions.

Source: Reuters

2. Bangladesh is building its first nuclear power plant, a $13 billion project that could eventually supply up to 15% of the country’s electricity. This move aims to cut their dependency on imported fossil fuels and is being closely watched as a test case for other developing nations who want to adopt atomic energy.

Source: Bloomberg

3. Russia is facing domestic fuel shortages and is now indirectly importing petrol produced in India. The fuel is being routed through international traders rather than direct sales.

Source: ET

4. Apple has filed a lawsuit against OpenAI, claiming that former Apple engineers stole confidential trade secrets about unreleased products when they left for the AI company.

Source: The Guardian

5. Investments in Indian equity mutual funds bounced back strongly in June, jumping up to 26% after hitting a one-year low in May. Most of this new money went into funds that support small and medium-sized businesses rather than massive corporations.

Source: Reuters

- This edition of the newsletter was written by Kashish & Pranav

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s retail lending landscape has transformed, using credit bureau data to reveal why lenders are moving away from unsecured loans and betting increasingly on collateral-backed credit.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

The Chatter by Zerodha

Our team at Markets spends a lot of time reading earnings call transcripts and listening to management interviews. Along the way, we come across plenty of interesting insights that are worth sharing.

That’s what The Chatter is for.

It’s a weekly newsletter where we dig through what India’s biggest companies are saying and bring you the most interesting insights into businesses, industries, and the wider economy.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉