India's DISCOMs posted a profit. How real is it?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

What’s behind India’s state discoms recording a profit?

India is finally pricing banking risk

What’s behind India’s state discoms recording a profit?

If there’s one institution in India that carries the reputation of a perpetual money pit, it’s the state discom. For decades, these entities have been racked with inefficiency, political interference, and an endless cycle of losses and bailouts. Though the faults don’t entirely lie in the discoms themselves, their name is synonymous with poor financial performance.

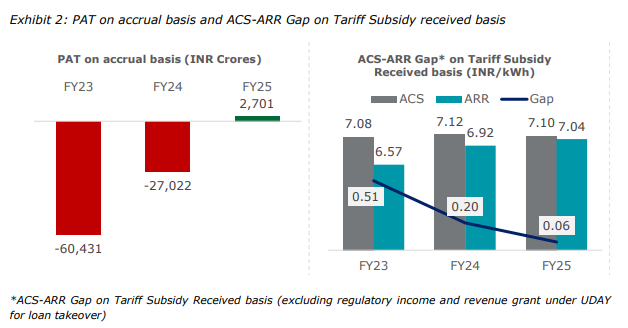

So, when the Ministry of Power recently announced that in FY25, DISCOMs had collectively recorded a profit-after-tax of ₹2,701 crore, it took us by surprise.

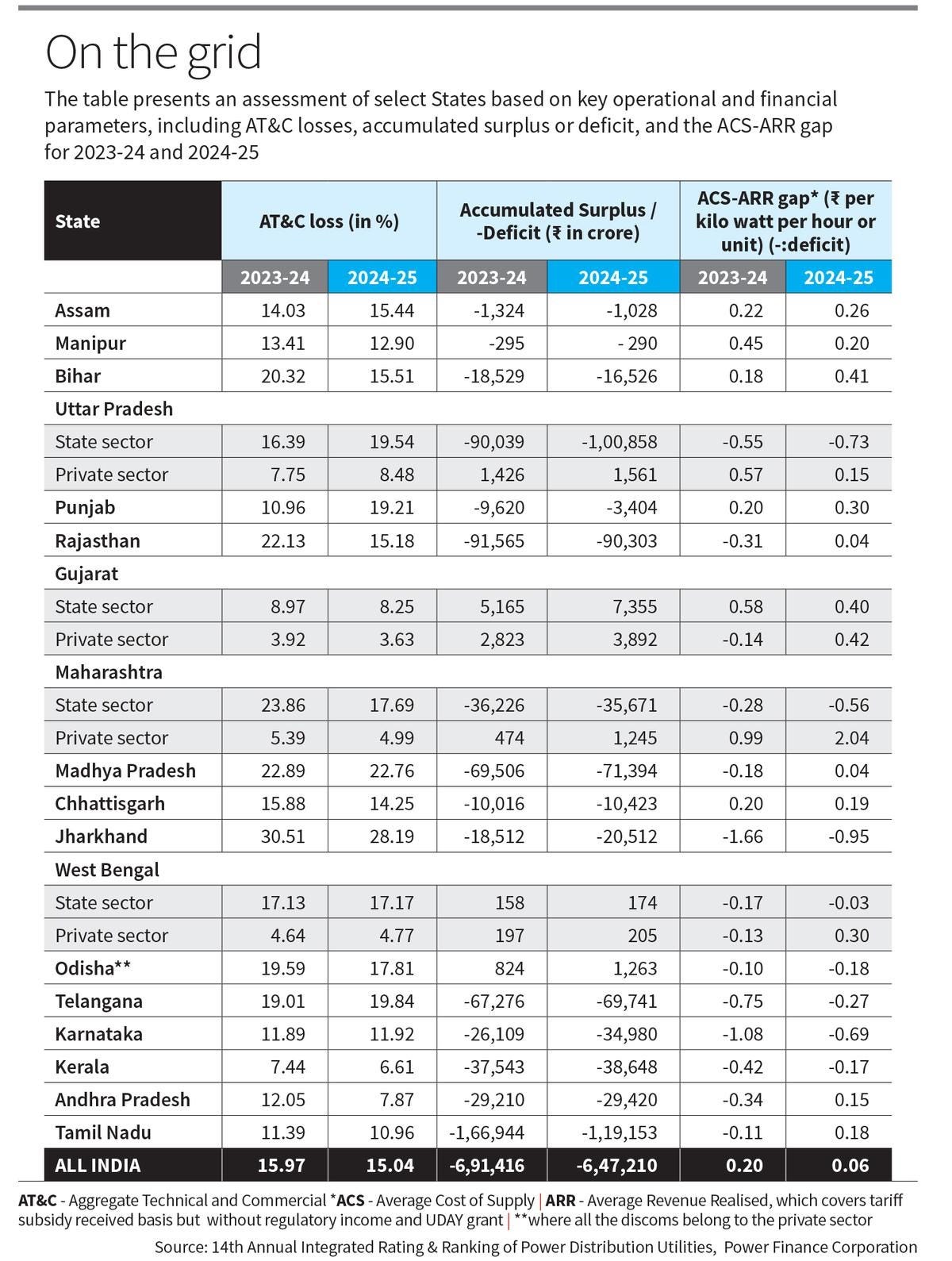

On many metrics, discoms seemed to have done well. Outstanding dues to power generators crashed 96% in 4 years, from ₹1.4 lakh crore in 2022 to just ₹4,927 crore now. The ACS-ARR gap, which measures how much it costs a DISCOM to supply a unit of power versus what it earns from selling it, narrowed from ₹0.78 per unit in FY14 to just ₹0.06 in FY25. These are remarkable improvements by any means.

Perhaps, there were some early signs of this. In September 2025, CRISIL reported that state discoms are likely to cut their operating losses by over 30%. And there have been recent tailwinds to support such a change in fortunes. For one, India is about to launch a new Electricity Policy to revamp our electricity sector — primarily our discoms. In the past few years, we’ve introduced many policies to improve the finances of discoms.

But, there’s always a but. As we’ve covered in our primer, discoms have a history of cosmetic turnarounds that mask deeper structural fragility. We can’t help but ask: how much of this profit is real, and how much is a paper gain?

Old dog, new tricks

Let’s start with one of the most persistent problems in India’s power sector: DISCOMs not paying both power generators and power transmission companies.

For years, DISCOMs would buy power from generators — both state-owned and private — and then delay payments for months, sometimes years. By 2022, outstanding dues to power producers had piled up to ₹1.4 lakh crore.

This wasn’t just a DISCOM problem, though. It cascaded through the entire value chain. Discoms got paid late by consumers, which trickled down to generators. Generators, meanwhile, couldn’t pay coal companies, and the whole system groaned under a mountain of unpaid IOUs.

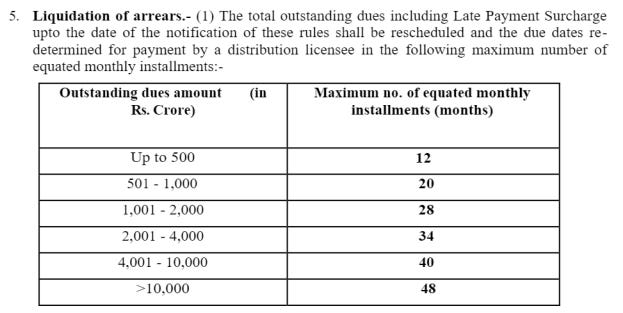

To try and break this cycle, in June 2022, the Ministry of Power introduced the Late Payment Surcharge (LPS) rules. This offered discoms saddled with late payments a way out, but with a strict conditionality.

The “way out” was a graduated liquidation schedule, where discoms could convert their legacy dues into EMIs. The payment timelines were scaled by the size of the debt. If, for instance, the discom owed less than ₹500 crore, it had 12 months to clear up. Those owing over ₹10,000 crore got 48 months.

The underlying condition, though, was severe. If a DISCOM failed to clear current bills within one month of the due date, it would lose access to the inter-state transmission network. Basically, some of its lights could go out.

Thirteen states opted for the liquidation schedule. The results, at least on paper, were dramatic. Outstanding dues to generators fell 96% — from ₹1.4 lakh crore in 2022 to just ₹4,927 crore by January 2026. Payment cycles, it seems, improved from 178 days in FY21 to 113 days in FY25.

But these improvements came with a massive caveat: these dues didn’t disappear because discoms suddenly started earning enough cash to pay their bills. Instead, they were cleared through a restructuring of their existing debt.

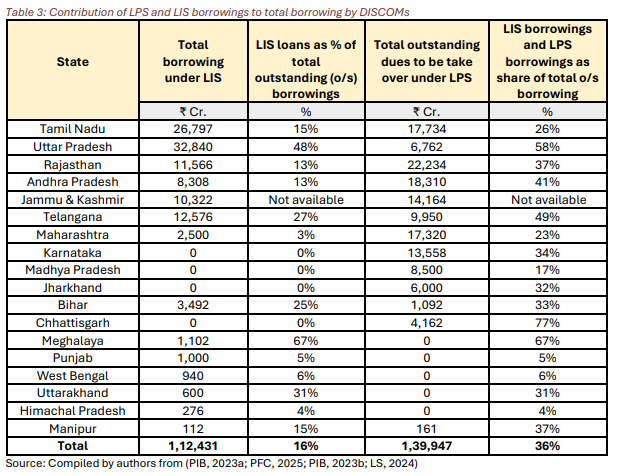

See, in order to meet the LPS deadlines, most state discoms financed their payments by fresh 10-year loans. They were taken from two public financial institutions — the Power Finance Corporation (PFC) and Rural Electrification Corporation (REC). The interest payments under the new loans were lower than what discoms would have otherwise borne if they were late. These loans amounted to ₹1,13,737 crore, covering 81% of the total legacy dues targeted by the LPS rules.

In the pandemic, the government had introduced a similar plan called the Liquidity Infusion Scheme. The total borrowing under these two schemes reached approximately ₹2.52 lakh crore — or 36% of the total borrowings of discoms. And the borrowing is heavily concentrated, with 74% of this debt made up by seven states — Tamil Nadu, UP, Rajasthan, Andhra Pradesh, Telangana, Maharashtra and Bihar.

What’s particularly concerning is how these loans were even made possible. The standard financial norms typically cap DISCOM working capital borrowing at 25-35% of annual revenue — precisely to prevent taking on too much debt. But, the government classified LPS and LIS loans as being “additional“ to these ceilings, effectively allowing DISCOMs to bypass the earlier debt limits. Additionally, many of these loans are backed by guarantees from the state governments, giving PFC and REC the security to lend to them.

In essence, this was a debt swap or restructuring, where two things changed. One, instead of power generators, the liabilities of discoms were now owed to the PFC and REC, spread out over 10-year loans. Two, the maturity and interest rates of the new loans changed.

But, this new debt is only limited to clearing what the discoms owe other entities. It cannot be used for capex. Prayas Energy, an energy-oriented think-tank found that in eight major states, 44-86% of total borrowing is now used for working capital instead of upgrading infrastructure. The interest burden from these loans alone consumes ~5% of the respective state DISCOMs’ total expenses.

On similar lines, some state governments directly assumed the losses of their respective DISCOMs onto their own books. This cleans up the DISCOM balance sheet but simply transfers the liability to the state exchequer.

The RDSS effect

Besides the LPS rules, another important policy driver that impacted the profits was the Revamped Distribution Sector Scheme (RDSS).

The RDSS represents a shift from the older approach of bailing out discoms wholesale. It’s designed as a performance-linked programme: DISCOMs don’t get the money just for existing. To access central funds, they must meet specific pre-qualifying criteria, like: publishing quarterly accounts on time, clearing subsidy dues, reducing transmission (or AT&C) losses, etc.

However, the RDSS doesn’t just target discoms. A massive bottleneck that discoms face is that their own state government often delays subsidy payments to them, even if the discom is eligible. So, the RDSS made a carrot-and-stick policy for state governments. The only way states can qualify for grants, the policy says, is by clearing their dues to discoms. And the grants are massive — worth over ₹97,000 crore.

The policy had the intended effect. States like Andhra Pradesh, Telangana, Madhya Pradesh, and Punjab cleared nearly all subsidy dues from the past three years. Subsidy realisation — which is the amount actually dispersed in cash versus the subsidy promised — improved from 97.45% in FY24 to nearly 99% in FY25. This massive injection of the arrears of discoms formally being recognised as real income is one of the biggest drivers of discom profit.

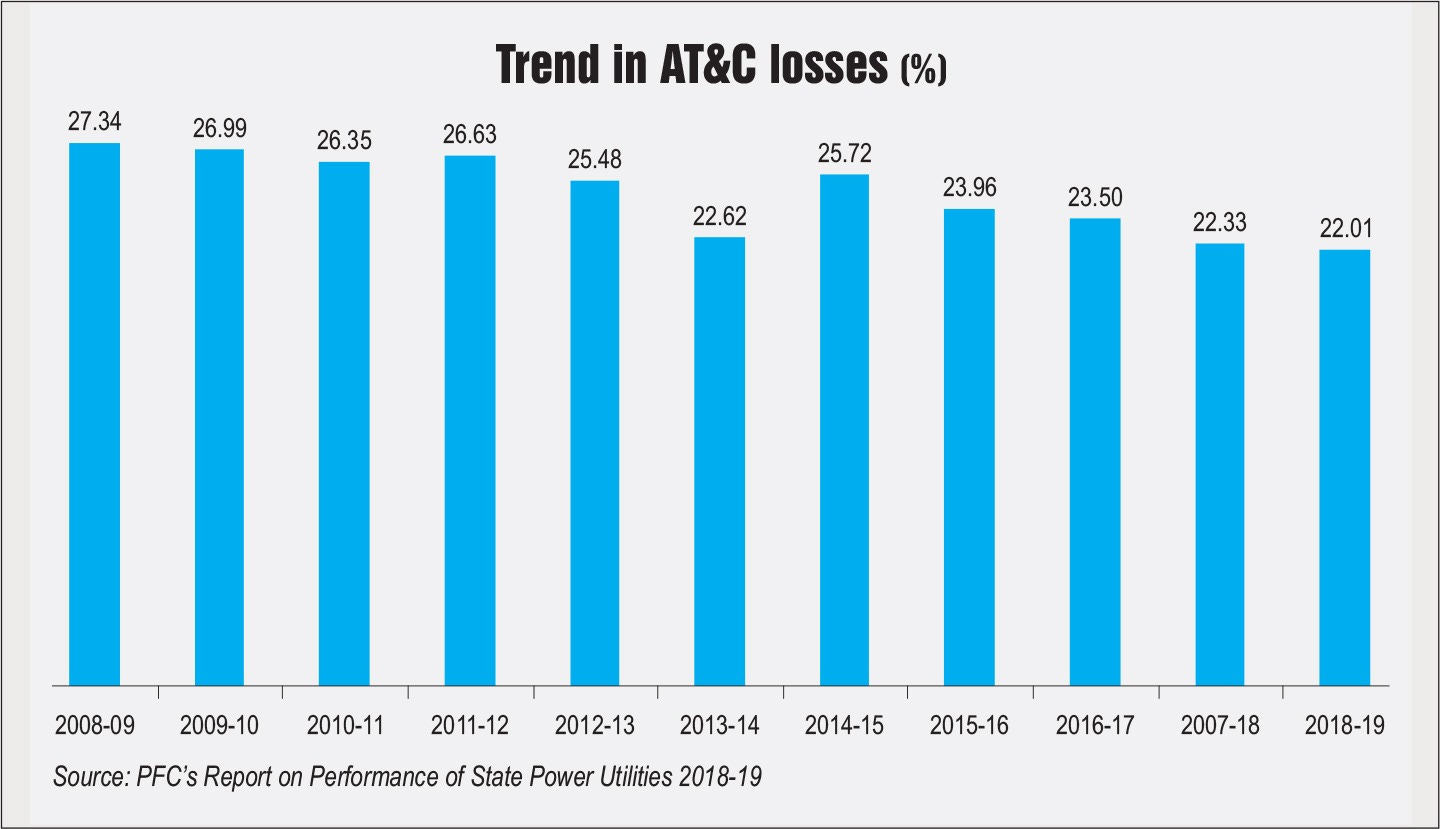

The RDSS also made discoms themselves operationally better. AT&C losses fell to 15% in FY25, hitting the scheme’s target range of 12-15%. For contrast, in 2016, AT&C losses were at nearly 24%. Meanwhile, billing efficiency improved to 87.59%. Reducing power theft and billing inefficiency directly improves a DISCOM’s bottom line.

But, this performance does come with two asterisks.

For one, as per Prayas, in FY24, states like Maharashtra, Rajasthan, and Karnataka showed renewed shortfalls in subsidy payments. Meanwhile, Andhra Pradesh and Telangana consistently met their arrears.

What this might mean is that the initial cleanup of arrears to discoms may have just been a one-time effort to grab grants. States might just revert to their old pattern of promising subsidies to discoms and then not paying them. That, perhaps, is why the success of this policy so far has also been uneven across states.

Secondly, the recorded profit might mask whether a discom has actually improved operationally. For instance, Tamil Nadu’s main discom was only able to record a profit for two reasons: it finally received its subsidy, and the state government assumed its losses. Without those line items, it would have still been in the red.

That being said, this may also paper over problems that are specific and unique to that state, and can’t be solved easily by central policy.

The issues that remain

Beyond these schemes, there are other nails that poke holes into the narrative of the discoms achieving strong financial health.

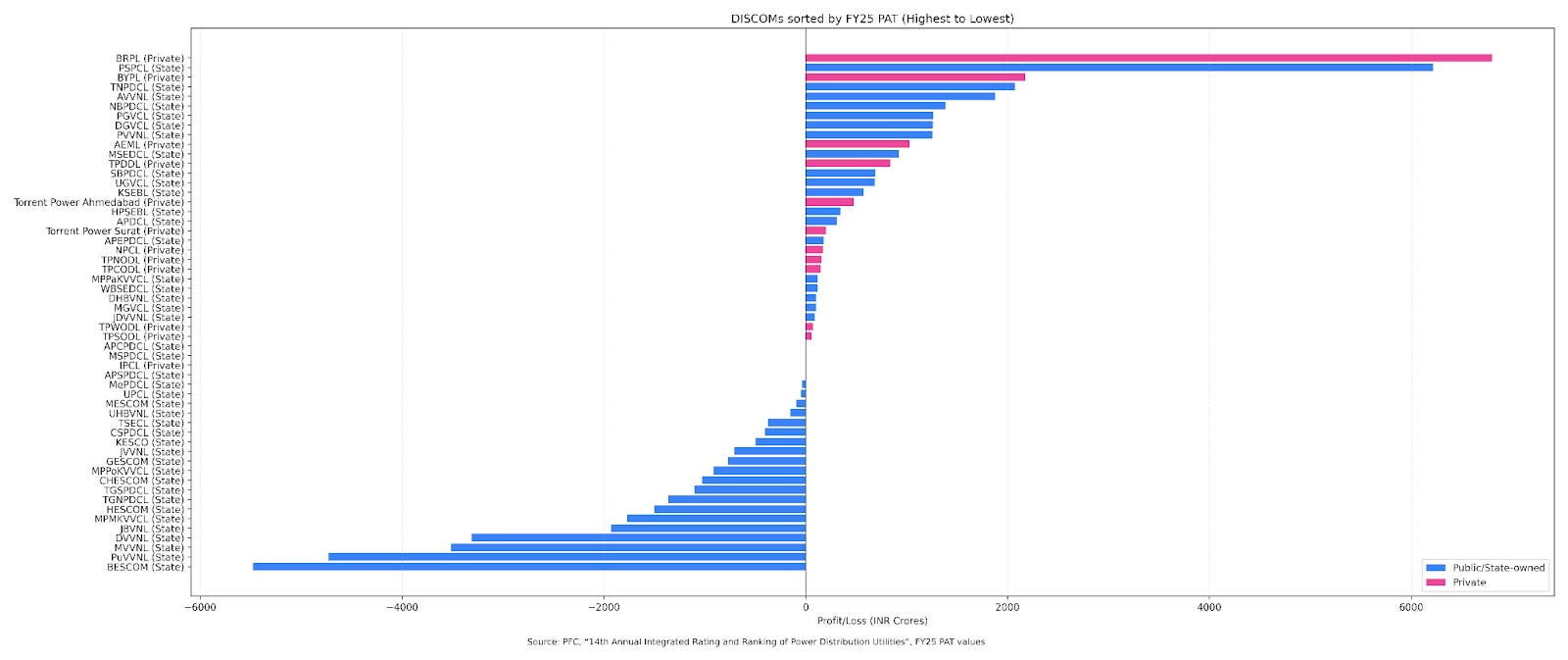

Let’s start with who the strongest discoms were. Much of this turnaround in discoms, it seems, was driven by private operators, not public ones. In the 14th Annual Integrated Rating of Utilities, every private discom was seen to have recorded a profit. But, nearly half the public utilities listed losses in the books this year. The largest loss this year was that of the Bangalore Electricity Supply Company (BESCOM).

The struggle of state-owned DISCOMs also continues because the LPS and RDSS don’t address some of the biggest issues weighing them down.

Perhaps, the biggest among these is power procurement. After all, buying electricity accounts for 70% of a DISCOM’s total costs. Discoms remain locked into rigid, long-term contracts with thermal generators that often require payment for capacity regardless of whether the power is used. These legacy contracts force DISCOMs to buy expensive coal-based power even when cheaper solar and wind alternatives are available. Neither the LPS rules nor RDSS touch procurement reform.

Secondly, there’s the tariff problem. Tariff hikes are politically explosive and regulators frequently buckle. Moreover, this differs heavily from state to state. Tamil Nadu, for instance, went six years without a tariff revision in the last decade.

But without a tariff hike, discoms will find it very hard to repay their dues, which will keep adding up over time. In five major states, 40% of outstanding consumer dues are more than three years old — effectively bad debts that may never be recovered. DISCOMs have no real power here, trapped between regulators who won’t raise tariffs and state governments that won’t fully compensate for the difference.

Conclusion

It’s too early to declare victory.

The discom profit is significant, and reflects many much-needed wins in Indian electricity. But these wins were built primarily on a debt swap, subsidy arrears being cleared, and accounting improvements.

Reforms like the LPS rules, RDSS and so on have been building for years. India is forcing change in its DISCOMs, and that matters. But deeper structural problems like rigid procurement contracts and increasing tariffs remain untouched. Until those are addressed, this profit is best understood as the first milestone on a much longer, steeper road.

India is finally pricing banking risk

There’s a body called the Deposit Insurance and Credit Guarantee Corporation (DICGC) — which ensures that if your bank collapses, at least some of your money stays safe. It essentially runs an insurance scheme for your money. In return for that promise, banks pay DICGC a premium.

For a long time, this deposit insurance system ran on what seemed like a simple principle: banks paid the same premium rate for any deposit, regardless of how safely it was run. That era of flat rates is ending. A few days ago, DICGC announced the implementation of what it called a “Risk-Based Premium” (RBP) framework, which kicks in on April 1.

We know, this sounds like a boring, technical change, about a random fee that banks pay. The consequences, however, could be profound. This could upend the incentives of India’s banking sector. Fundamentally, it makes safety cheaper. That makes this simple fee change a governance reform and a competition reform rolled into one.

But for that, let’s start from the top.

Why flat pricing is unstable economics

If you’re a regulator, a flat insurance premium is an easy, no-nonsense approach to have.

If you’re a bank, it’s unfair.

To understand why, let’s borrow an example from health insurance. Imagine a 40-year-old diabetic smoker who’s never exercised, and another 20-year-old who runs marathons and treats his health like a job. If both were charged the same for insurance, you’d get skewed outcomes. The young marathoner would probably find insurance prohibitively expensive — even if they did buy it, it would feel like a hefty tax. The diabetic smoker, on the other hand, would effectively have their healthcare costs subsidised. The different charges the two pay are, in effect, by design.

Banks work the same way. When every bank pays the same rate, safer banks effectively subsidise those that are badly run. That might be politically convenient for a while, but over time, it skews everyone’s incentives. Weak banks don’t fully bear the cost of the risks they take. Meanwhile, stronger banks are effectively punished for being careful.

India has been aware of this mismatch for years. As far back as 2015, a committee recommended moving to a differential premium system, clearly laying out the fairness and moral hazard issues we currently have. All of that’s finally being put into practice.

What exactly changes from April 1, 2026

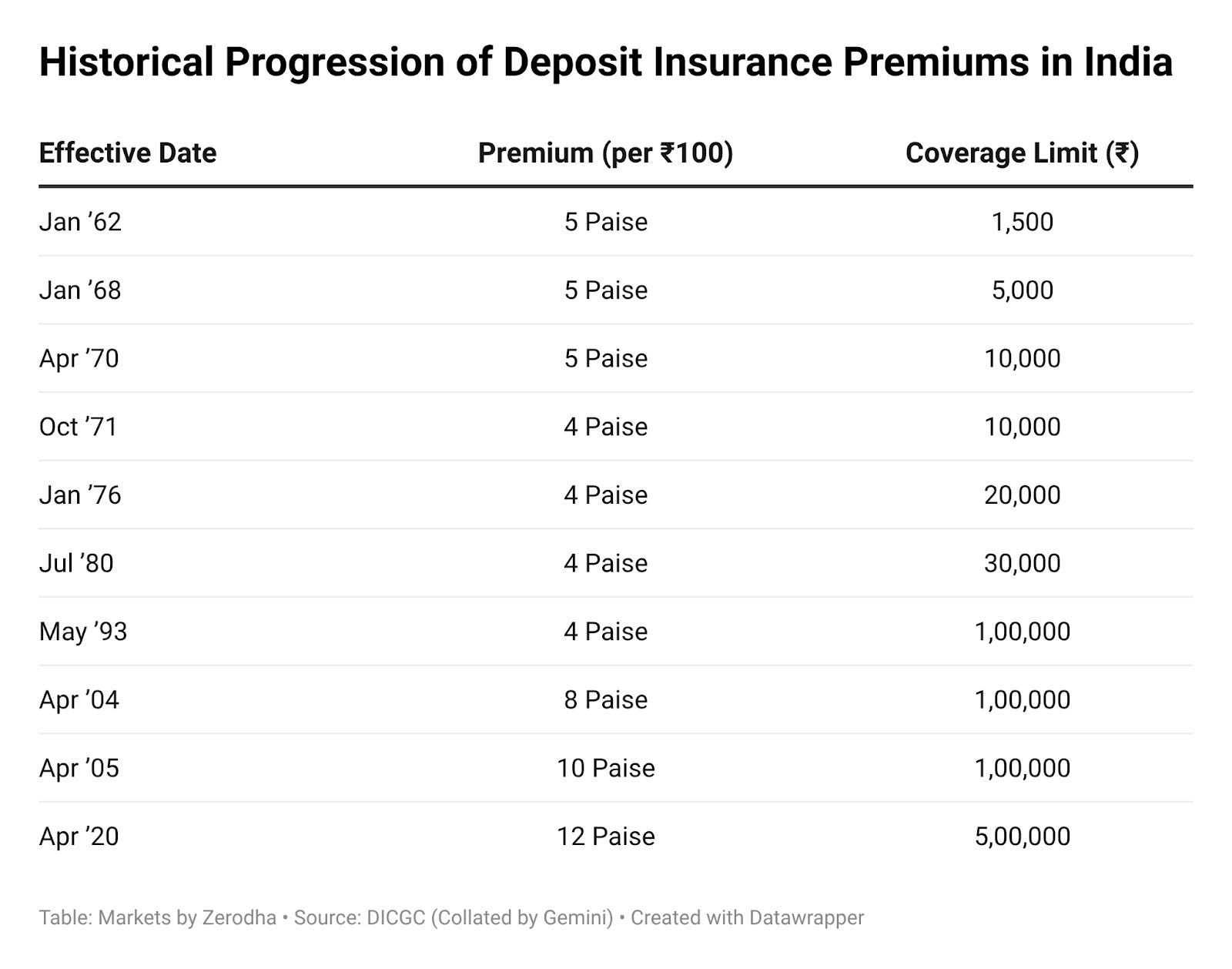

Right now, every bank pays DICGC 12 paisa for every ₹100 of deposits it holds. That’s much higher than the rate when DICGC was set up in January 1962, of 5 paisa. It has steadily climbed since.

The new change, however, does away with that flat rate entirely.

The new framework has several moving parts here, but the core is simple.

Four risk categories, four premium rates, two assessment models

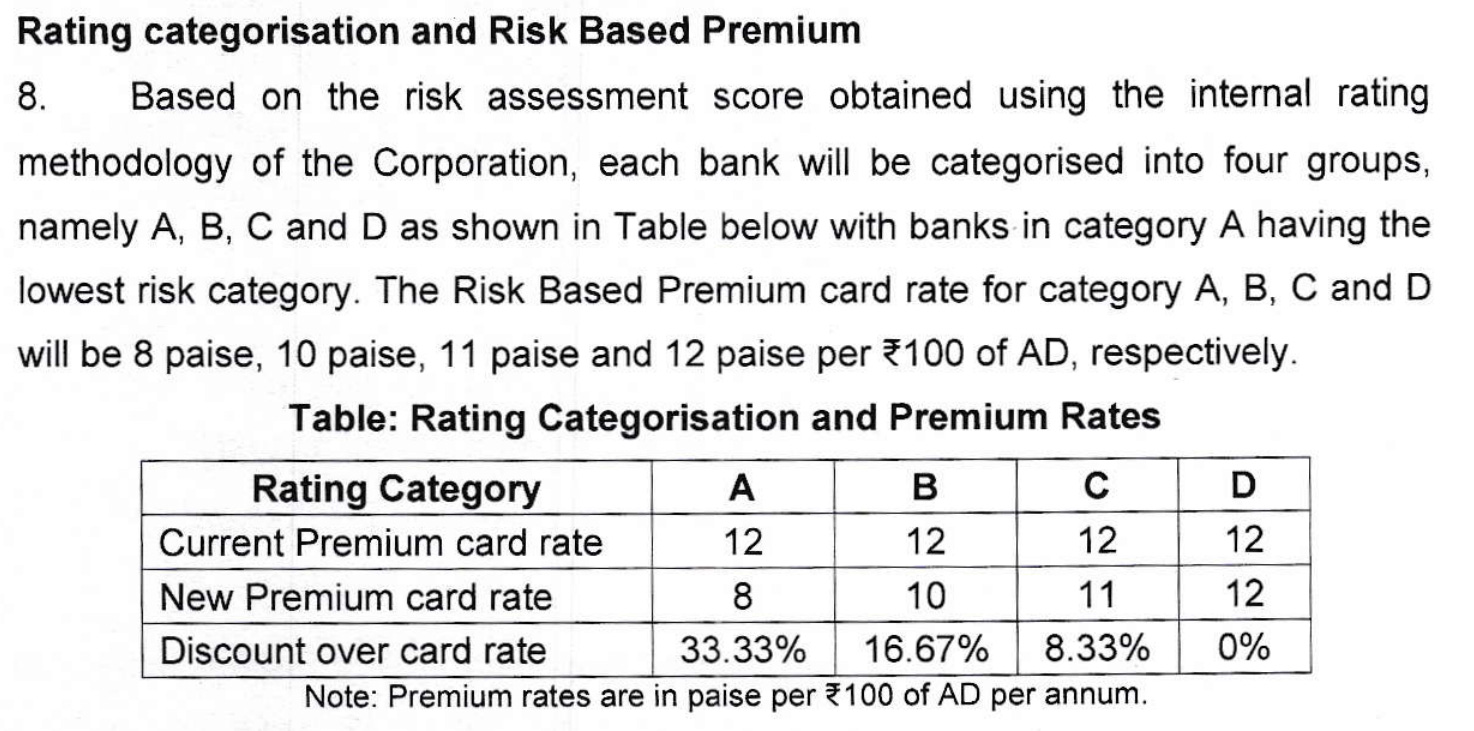

Under the new framework, India’s banks will be slotted into four categories — A, B, C, and D. A is the safest. D the riskiest. The premium a bank pays will depend on where they sit.

Instead of a flat fee, the safest banks will get up to a one-third discount on the standard 12 paisa rate. Banks rated ‘B’ and ‘C’ get a smaller discount. Banks rated ‘D’ pay the same. That is, the framework isn’t increasing the burden on riskier banks by increasing their premium. But it’s rewarding safe ones for their responsible conduct.

How does DICGC decide who goes where? First, it places the banks in one of two tiers, depending on its size. Then, it judges you according to your category:

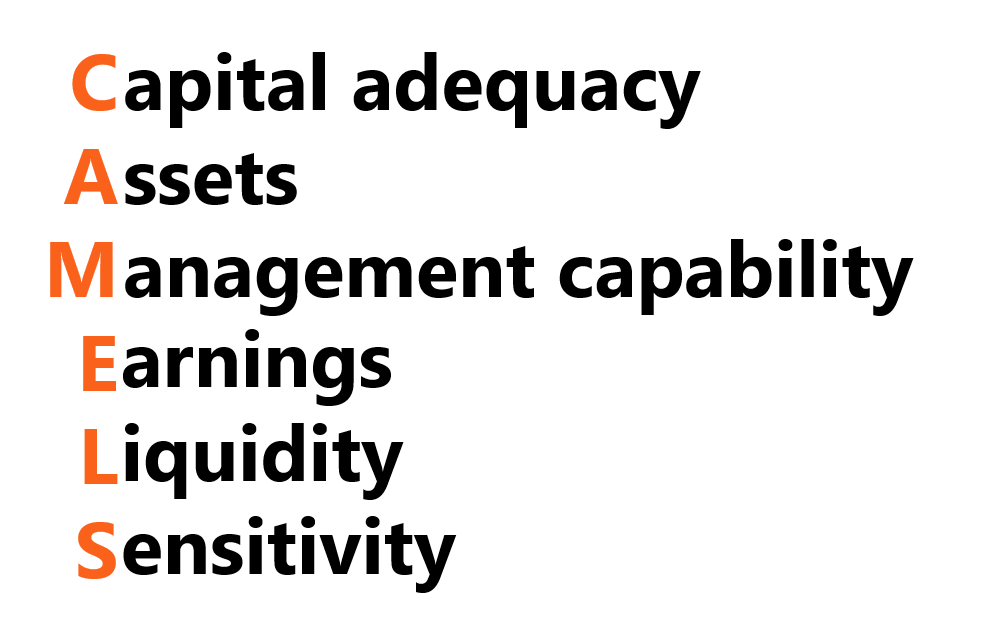

Tier 1 covers Scheduled Commercial Banks, other than RRBs. These banks will be evaluated using a mix of indicators, including what’s called the ‘CAMELS’ framework — a global method that evaluates banks across a range of parameters. RBI already uses this framework for supervision. Now it will also influence insurance pricing.

Tier 2 covers Regional Rural Banks and urban and rural cooperative banks. Here, CAMELS will still matter, but the quality of governance gets extra weight. After all, in smaller, locally run cooperative banks, weak governance is often where financial trouble festers. The regulator is effectively saying: if your governance is shaky, your insurance bill should reflect that.

Vintage incentive

There is also an additional “vintage” benefit. This is an extra “discount” given to banks for long periods of good behaviour. If you’ve been a good bank for 25 years, you get another 25% discount on your premiums. As soon as something goes wrong, though, it resets to zero.

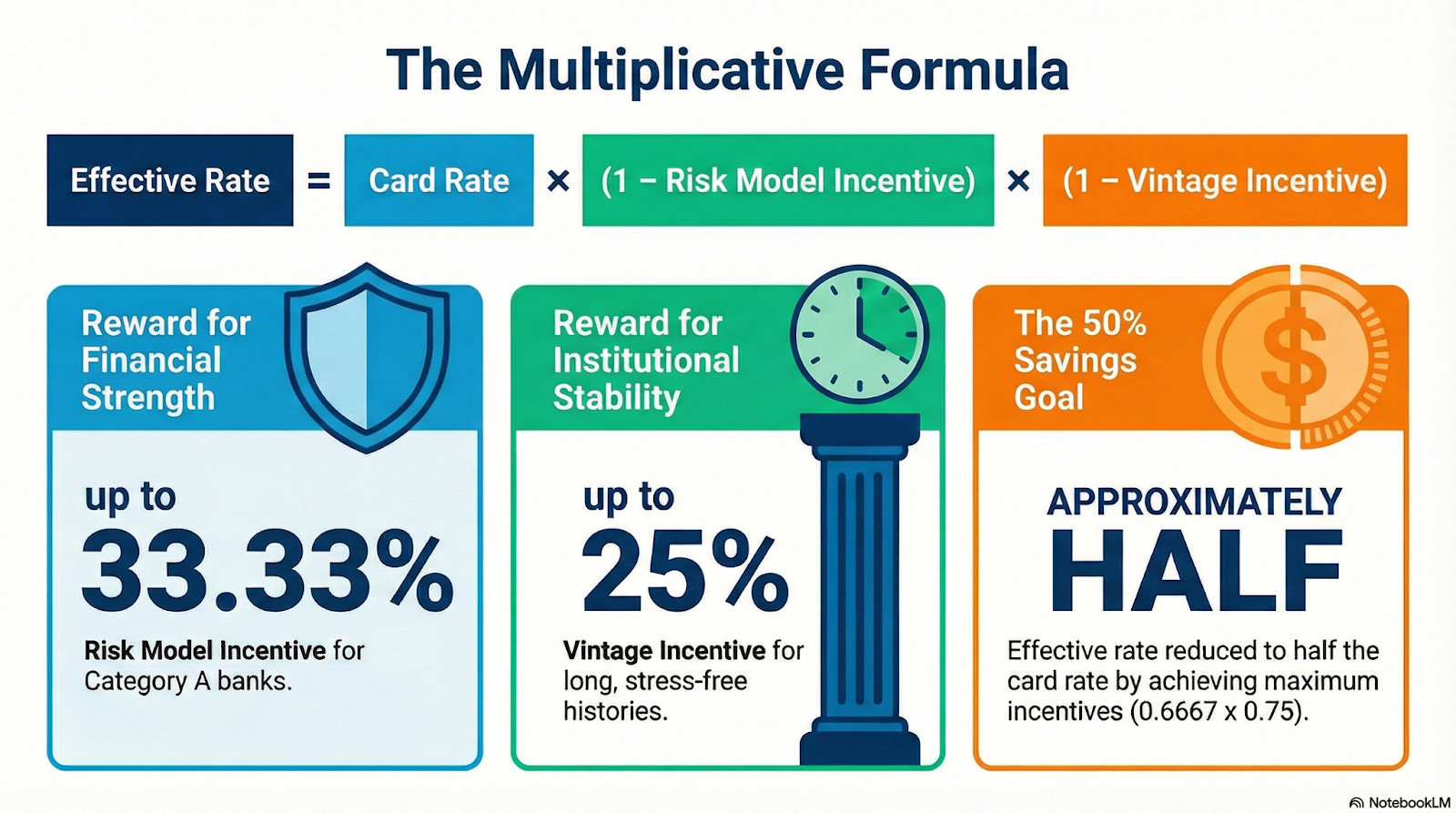

The effective premium that banks pay, then, will be the card rate of 12 paise, with a discount for both how safe you are, and how long you’ve been safe for. If a bank that gets A rating (33.33%), and hasn’t been a problem for 25 years (25%), it effectively gets 50% off on the 12 paisa rate card.

Carve-outs and constraints

Now, there are a lot of carve outs for this rule. There are some banks — like local area banks and payment banks — that don’t get a rate cut, simply because there isn’t enough data. There are others that don’t get a discount, including urban cooperative banks under RBI’s scanner. And DICGC has the discretion to cancel your discount if there’s an adverse development.

The implications

Those were the technicalities. Now, let’s dig into what this actually means.

This is a huge relief for banks that are already well-capitalized, well-run, and structurally low risk. Here’s a rough, back-of-the-envelope example: in FY25, SBI paid over ₹5,400 crore to DICGC as insurance premium. Under the new framework, assuming it gets the maximum discount, that bill will be halved. It’s a saving of ₹2,700 crore — more than the lifetime profits of many smaller banks. That gives SBI a massive buffer.

In FY25, commercial banks contributed 94.72% of the DICGC’s premium collections. Cooperative banks contributed just 5.28%. But when it came to claim payouts, it was the opposite. As of March 2025, DICGC had settled cumulative claims of ₹10,954 crore for 389 cooperative banks. It had just given out ₹296 crore for 27 commercial banks. That is, for years, India’s stronger commercial banks effectively funded a system to bail out cooperative banks. If large commercial banks now qualify for lower effective rates, that cross-subsidy weakens by design.

Moral hazard

But that’s only half the story. There’s a more uncomfortable angle to this.

For weaker institutions — especially those already dealing with governance issues or thin balance sheets — this framework effectively adds pressure. If they don’t qualify for discounts, they sit at a permanent cost disadvantage versus stronger peers. That puts them on the back foot while competing for deposits, and makes it less likely that they make a profit.

This can push them in two ways. Ideally, you have the best of all worlds. Banks clean up, reduce risk, tighten governance. But equally, they might take on more short-term risk to protect earnings. Both outcomes are plausible, depending on how tough and consistent supervision actually is. If banks think they can get away with more risk, chances are, they’ll try.

The big question is this: can this new regime actually cure moral hazard?

Moral hazard is when someone takes extra risk because they don’t bear the full downside — usually because there’s a safety net. Think of a CEO that is promised a “golden parachute” if they’re ever fired, and therefore is cavalier with risk. The argument, here, is that a flat fee creates such a moral hazard, allowing poorly run banks to work with impunity. The new framework, then, should do away with it.

Is that actually the case?

To be clear, risk-based pricing definitely nudges incentives in the right direction. But sadly, a simple price change doesn’t guarantee better behaviour either.

The big problem, here, is that you can’t price what you can’t see. Banking, by its nature, is opaque. A bank’s risk isn’t always visible in real time. Numbers can be delayed; problems can be hidden. Things can stay bad for years until they blow up. So, the DICGC’s ratings are essentially given by looking in the rear-view mirror. By the time you realise that a bank was taking too much risk, it might already be too late.

This is why pricing can’t do the job alone. It has to be backed by tight supervision and quick action. If the rating model lags reality, or if governance deterioration isn’t caught early, the new regime, despite looking neat on paper, will underdeliver in practice.

That was the experience of the FIDC, which is the American equivalent of the DICGC. The U.S. used to have a similar flat fee, before it moved to risk-based pricing in 1993. That wasn’t a silver bullet, however. It had to spend decades recalibrating its framework, adding adjustments for large and complex banks. India should assume the same path — that it will take years of refinement to make this system useful. Right now, all we have is a foundation.

Competition and consolidation

There’s a third possible outcome of weaker banks feeling the squeeze of higher prices — especially if they can’t fix governance or improve asset quality fast enough.

Instead of dramatic failures or hidden risk, this can show up as consolidation. Without a clear path to competitiveness, banks may seek a quiet exit through a merger or acquisition. RBI has been nudging the system in this direction anyway — consider, for instance, the voluntary amalgamation scheme for UCBs launched in 2020. In fact, that kind of consolidation may even be the point.

The confidentiality paradox

Beyond the pricing changes, there’s an interesting design choice that the new framework comes with: a bank’s rating is secret. DICGC has said a bank’s risk category will be shared only in strict confidence with its MD or CEO. They can’t disclose their category publicly. They can’t use it for marketing. In fact, they can no longer even disclose the exact premium amount they pay in the notes to accounts, like we saw with SBI! They’ll only make a generic compliance disclosure.

Fundamentally, the regulator wants to avoid a self-fulfilling panic. Imagine a bank is tagged “D”, which then makes depositors jittery, precipitating a bank run. A bad rating, then, run could trigger the very crisis the system is trying to prevent.

But that comes at the cost of less transparency for the market. Depositors and analysts don’t have a potentially useful signal about the risk underlying a bank.

How to judge the reforms?

It’s too early to say how these reforms actually work out for the banking sector. In fact, the regulator itself isn’t sure yet — the new framework will be reviewed at least once every three years.

But there are a few signals you can watch out for.

Watch for pricing pass-through. Do well-run banks start giving better deposit rates and more competitive lending terms? If that’s the case, look for deposit-share migration. Do deposits slowly drift toward stronger banks because their funding economics improve?

On the regulator’s side, keep an eye on DICGC’s fund adequacy. Does it improve, stay stable, or come under pressure once differential pricing kicks in? Does collecting less from the safest banks leave a hole that matters?

Together, this should give you a sense of how the framework evolves.

Tidbits

Kerala rolls out India’s first graphene policy

Kerala has approved India’s first full graphene policy to attract investment and become a global hub for graphene research and manufacturing. It’s backing this with incentives like a 50% lease subsidy for units in government parks. The state also plans a graphene industrial park in Palakkad and a ₹200 crore Digital Innovation Centre.

Source: The Hindu BusinessLineCentre launches ₹1 lakh crore “Urban Challenge Fund”

The Union Cabinet has cleared a ₹1 lakh crore Urban Challenge Fund to push big-ticket city infrastructure. The Centre will fund 25% of project costs, but only if cities raise at least 50% from markets—forcing more private capital and reforms. The government says this could unlock ₹4 lakh crore of total urban investment over five years.

Source: ET BFSIIndiGo to hire 1,000+ pilots after December disruption

IndiGo plans to hire over 1,000 pilots after a December 2025 crew shortage led to 5,000+ flight cancellations in a week. The problem worsened after tighter DGCA duty-and-rest rules, and regulators said IndiGo hadn’t scaled hiring/training fast enough. Now, the airline is expanding training and adding buffers like more standby crew and schedule slack.

Source: Business Standard

- This edition of the newsletter was written by Manie and Kashish

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉