How the rupee grounded Indigo’s profits

And why the next quarter could look worse

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Marred by turbulence: Indigo’s Q4

What does better access to Indian banking really do?

Marred by turbulence: Indigo’s Q4

For years, Indigo Airlines’ would post rather predictable results. Aside from moments like the COVID rupture, its growth seemed mechanical. Quarter over quarter, the airline would add planes, more passengers would choose it, and more profits would flow through. And with a market share so large that it catered to two in every three Indian flyers, Indigo’s story was the story of Indian aviation as well.

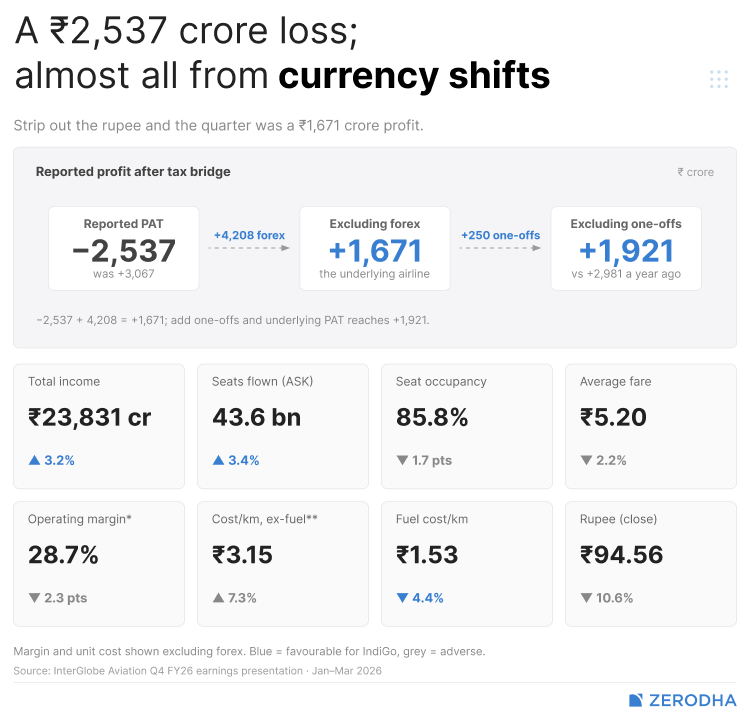

Recently, however, that story appears to have gone awry. In December, the airline’s operations suffered a catastrophic failure, leaving hundreds of thousands of passengers stranded in airports across the country. Then, in the March quarter, Indigo reported a massive loss — bleeding just over ₹2,500 crore in the three months. This was a sharp reversal in fortunes; the same quarter one year ago, it had profits of ₹3,000 crore.

There’s a simple version of this story: that the company is in trouble.

That isn’t what we think is happening. Very little of this loss, from what we can tell, has to do with flying planes. But it does tell us a lot about the peculiar risks of Indigo’s business model — the way it interacts with fuel prices, the Rupee, and everything happening in the world outside.

The quarter in numbers

From its topline alone, Indigo seemed to have a normal quarter. Its revenues barely moved one way or another — rising by a few percentage points, to about ₹23,800 crore. It was roughly the same last year.

Shift your eyes to its bottom line, however, and its post-tax profits have cratered, from a healthy profit last year, to a ₹2,500-crore loss.

How did a business with roughly the same sales figures as before see its profits collapse? There are two parts to this story. Most of the damage came from something the airline had little control over — a collapse in the rupee. But there’s a quieter story in there: one where India’s leading airline has a slightly softer belly than a year ago, tortured by the Iran war and the long shadow of its December nightmare.

Two airlines; one set of books

IndiGo, like most airlines, lives between two currencies: most of what it earns is in rupees, but most of the money it owes is priced in dollars. An overwhelming majority of its planes are leased, and those leases, along with the cost of maintaining that fleet, are all billed in dollars.

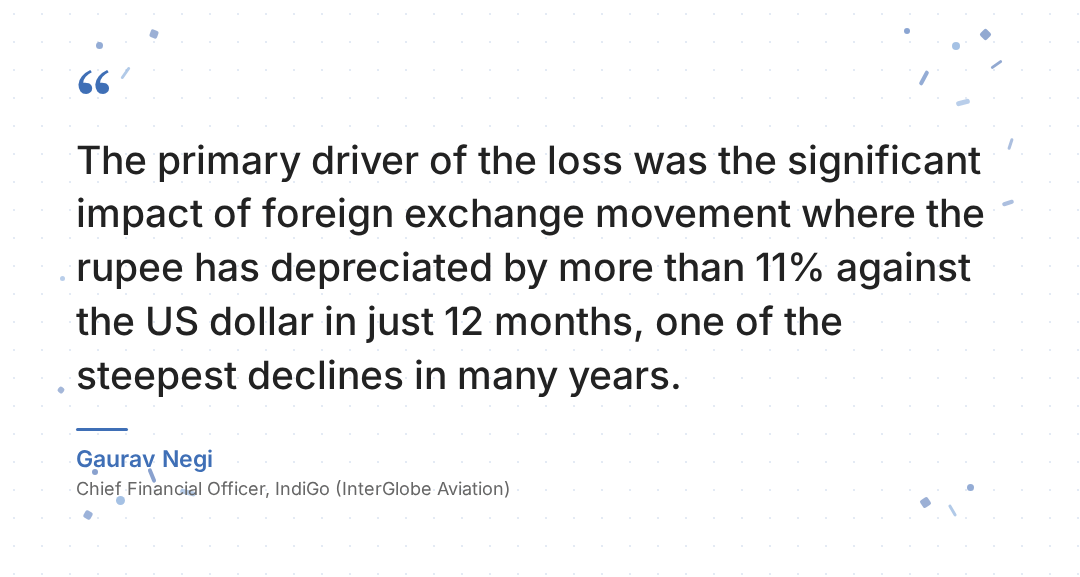

It’s always a challenge to manage the split. But in a quarter where the rupee saw one of its steepest falls in memory — sliding by ~5% in just three months — its dollar-based bills suddenly pinched much more than before.

That isn’t just true for bills that were due this quarter. Under accounting rules, if you have a dollar-linked liability on your balance sheet, and it suddenly looks much larger in rupees because of the exchange rate, that’s a loss you need to book immediately — even if the money itself is to be paid off over years.

For Indigo, that translated into a sudden paper loss of ₹4,800 crore; enough to pull its quarter into the red.

Strip currency movements out, and the picture looks much better. Without it, the airline saw a profit of around ₹1,670 crore. That too, was only after some one-off charges — like a ₹250-crore provision the airline had to make to accommodate the new labour laws. Set that aside too, and the company made a profit of ₹1,920 crore.

That figure is much less worrying.

Then again, it’s more than ₹1,000 crore short of the ₹2,980 crore it made in profits the same quarter last year. You can see signs of that all through the company’s business. The company’s core operating margin — what it keeps before major fixed costs like aircraft rentals or interest — slipped from about 31% to a little under 29%. Its seat occupancy dipped slightly, as did the average fare for the seats it did fill. At the same time, its costs per kilometer, other than fuel, went up by more than 7%.

That is, even once you strip out all the quarter-specific weirdness, the airline did have a softer quarter, even if it wasn’t drowning in losses.

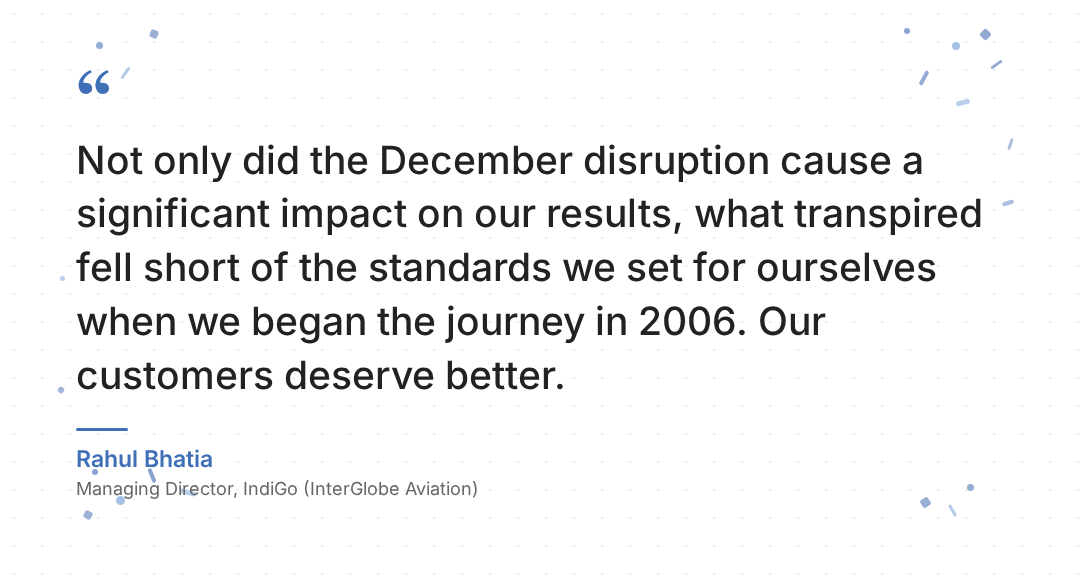

As the airline’s management admitted, the sceptre of its December catastrophe weighed on the company. Early in the quarter, the memory of those days cost the airline some market. It did start clawing that share back by January itself. But the memory of that crisis still lingered.

The exposure underneath

There’s one question worth asking the company: why was the company so vulnerable to a currency hit. Why did one bad quarter for the rupee blow a half-billion dollar hole through its balance sheet?

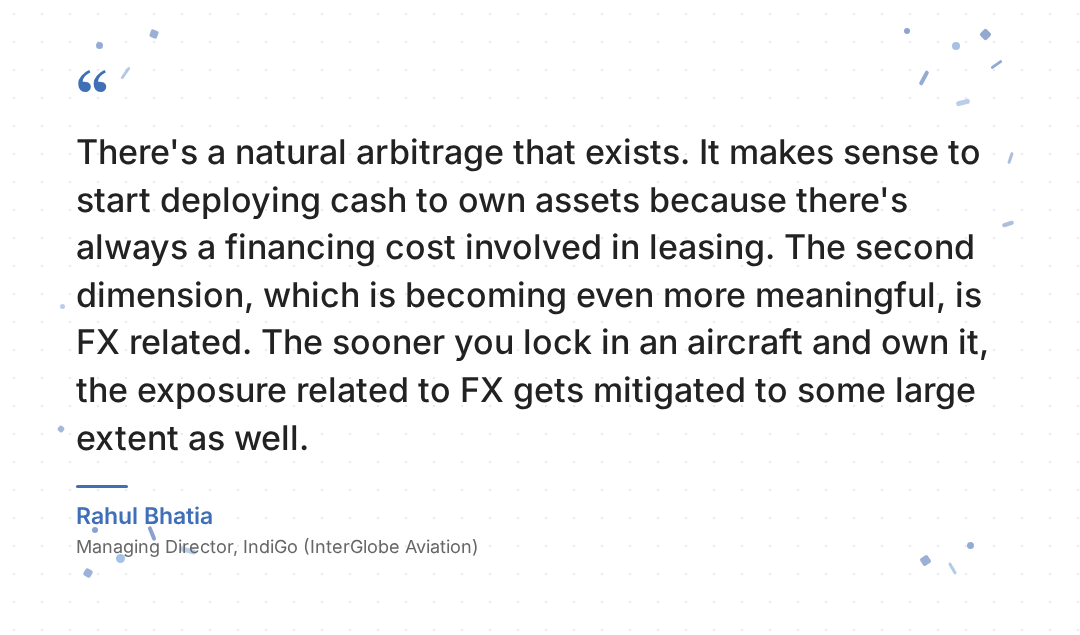

The answer, it turns out, is fundamental to Indigo’s business model. Indigo has always kept its books light. It has overwhelmingly leased its planes rather than buying them, so that it could expand quickly, while keeping enough cash on hand. This is how it became the giant it is.

Only, these leases are overwhelmingly denominated in dollars, which ties Indigo’s fortunes to the USD-INR exchange rate. All told, IndiGo’s net exposure to dollars amounts to about $10 billion. A 5% dip, then, mechanically burnt through half a billion dollars.

The airline is beginning to rethink its approach, however.

A year ago, it owned fewer than ten of the planes it flew. Today it owns thirty-six. It has also been prepaying aircraft loans, routing money through a financing arm in Gujarat’s GIFT City. It even skipped a dividend this year to help fund this shift. This is partly simple arithmetic: it’s paying more in financing those loans than the interest it earns on its cash. Prepaying just makes sense.

But partly, this is all meant to fix its interest exposure.

This move is still early. For the 36 planes it owns, it still leases over 400 — it is still overwhelmingly a company that leases planes. But it does point to a shift in philosophy: a company that was once laser-focused on staying asset-light is coming to terms with the costs of that approach.

Will that shift work? That question will be answered over the course of years.

A quarter out of time

There’s another serious issue that was obscured, somewhat, in the company’s March quarter results: the Iran war.

Just as Indigo started recovering from its December crisis, this new crisis erupted. Almost one-fifth of the airline’s total capacity — 160 daily flights to the Gulf and Europe — came within its cross-hairs. Roughly four-fifths of that simply stopped. Over January and February, Indigo was flying 10% more than a year ago. After the Iran war broke out, that dropped to just 3%.

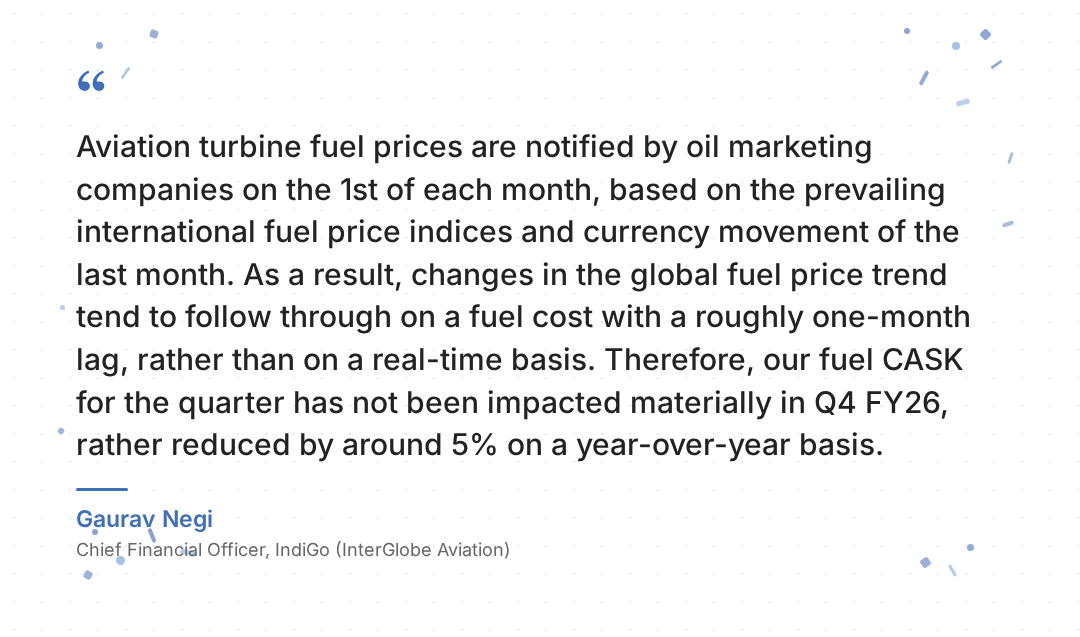

The bigger problem, however, was jet fuel. Fuel is the single biggest cost for an airline. Even in normal times, two-fifths of an airline’s costs are just fuel, and a crisis can send that fraction far higher. When the war broke out, crude prices began rising rapidly. Jet fuel prices went up with it. Over those three months, they went up two-and-a-half times: from ₹60 a litre to ₹142.

You don’t yet see that in Indigo’s numbers. In India, jet fuel prices adjust with a lag of a month, so the company hadn’t seen the full brunt of those costs when the quarter ended. But that grace period closed with the quarter. Next quarter, you should expect those prices to bite.

In short, the March quarter results describe a time that has already disappeared into the past. The challenges have only mounted since. The rupee has weakened further, while fuel prices have remained high.

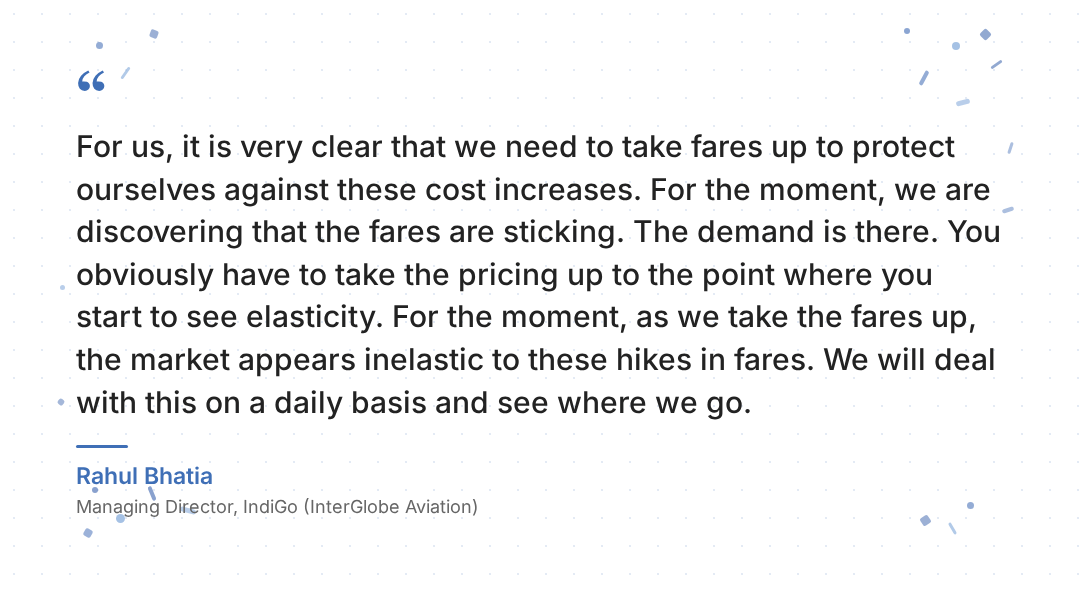

To cope with this, Indigo has started passing those costs on to its customers. So far, its passengers have been willing to foot the bill. This is something the company will keep testing — increasing fares until they hit a point where this stops working. Chances are, your next flight will be much more expensive than your last.

The government, however, is trying to bring back some stability.

A couple of days after Indigo‘s results, the government approved a ₹10,000-crore fund, intended to keep the price of domestic jet fuel at ₹75.60 a litre. This fund will help state oil companies absorb the price rises for now, and recover it at a later date, when prices come back down.

After the dust settles

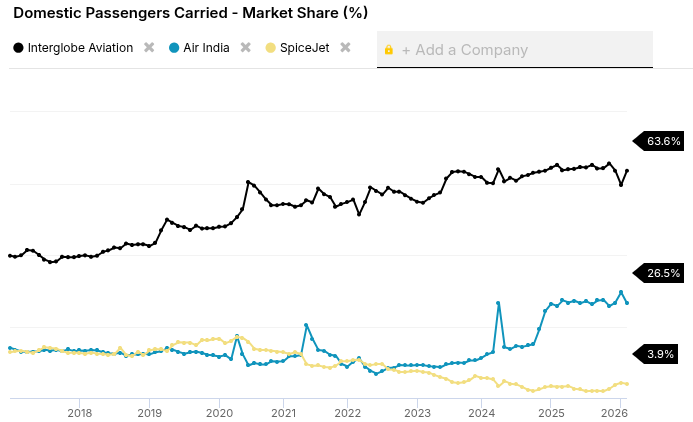

None of this gloom changes a fundamental fact, however: Indigo is still India’s biggest airline. It still carries two of every three Indian air passengers. In a year where it looked as though it was stumbling, it still carried a record 123 million people.

If recent events hit Indigo, it hit its rivals much harder. Over June and July, for instance, Indigo plans to cut around a tenth of its flights. But at the same time, Air India — facing the same headwinds — is cutting more than a fifth of its schedule. Indigo might enter a lean phase by its standards, but unlike its rivals, it still has more than ₹51,000 crore of cash to ride such crises out.

There’s nobody, yet, who can threaten Indigo’s crown.

What does better access to Indian banking really do?

By any standard metric, India has made enormous strides in getting financial services to its people. Around 80% of Indian adults now have a bank account. UPI processed over 23 billion transactions in May 2026 alone.

But here’s a question we don’t fully have the answer to: what does all of this actually do?

When a bank branch opens in a village, or a farmer downloads a payments app, does it change the way they farm, the risks they take, the shocks they can absorb? The relationship between expanding financial access and improving economic outcomes — especially in rural India, where nearly half the workforce still depends on agriculture — is one that’s surprisingly hard to pin down. Financial inclusion is easy to measure in terms of accounts opened and credit disbursed. It’s much harder to measure in terms of what it changes on the ground.

A new paper published in the Journal of Banking and Finance, by researchers Liang Bai, Camille Boudot-Reddy et al., takes a serious crack at this question. They study one of the largest bank branch expansion programmes any single country has ever undertaken — the Indian government’s drive to force banks into rural India during the 1980s. It is as natural as an experiment can get.

Did they make farmers more productive? Did they improve their access to liquidity? Those are the interesting questions the paper seeks to explore. And the findings are very intriguing.

The experiment

To understand the paper, you need to understand the sheer scale of what India attempted. That needs a small history lesson.

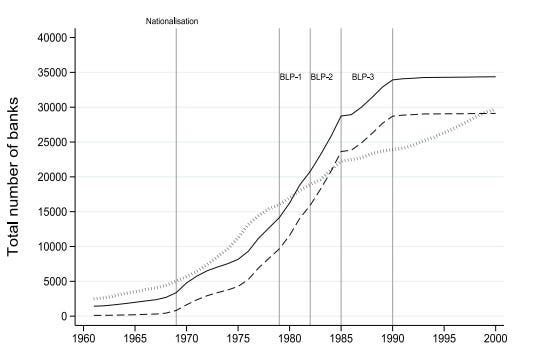

After nationalising 14 commercial banks in 1969 and another 6 in 1980, the government controlled over 90% of the country’s banking business. And it decided to use that control for a specific social mission: getting banking infrastructure into the underserved corners of the country.

The thinking behind it was that once you put a bank in every underserved district, rural prosperity would follow. Farmers would save more, borrow for better seeds and fertiliser, invest in irrigation, and produce more.

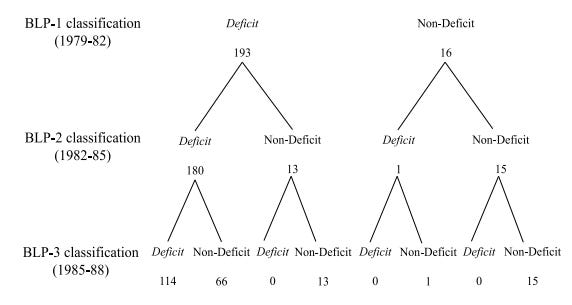

So, to conduct this expansion, between 1979-1990, the Indian state undertook three Branch Licensing Policies (BLPs). To find the parts of India that should qualify for such a program, the RBI calculated a simple ratio for every district: rural population (RP) divided by number of bank branches (BB). Any district where that ratio exceeded the national average was labelled “deficit“.

Then, these deficit districts were put on a branch expansion programme — new banking licences were issued exclusively for unbanked locations within them. At the end of each three-year period, districts were reclassified based on their updated ratios, and the cycle repeated.

Over the decade, around 12,000 new rural bank branches were opened across the country, growing at a rate of around 10% a year. The average population-per-branch ratio plummeted from 53,000 people per branch in 1979 to just over 15,000 by 1988.

What makes this programme particularly valuable is that bank growth in a given district during the 1980s was determined primarily by a bureaucratic formula — its deficit status — rather than by market forces.

In a normal setting, studying the effect of bank branches on farming is messy, because banks don’t open branches at random. They go where the money already is, or where they expect it to be. That means you can never be sure whether a district did well because the bank arrived, or whether the bank arrived because the district was already doing well. But due to the deliberate lack of market factors in their design, the BLPs mostly sidestep this situation naturally.

Moreover, after 1991, the government changed course toward liberalisation. This also meant putting the brakes on public-sector banking expansion and prioritizing financial discipline. Branch growth in previously-unbanked locations flatlined completely, even as branches in already-banked locations continued to grow. If banks had been going to these rural areas because they saw commercial opportunity, they would have kept going, but they didn’t. The BLP expansion was primarily policy-driven.

What the banks didn’t do

Now that we know how the experiment worked, let’s look at the headline metrics being tested.

The primary result the researchers check is output: did more bank branches boost agricultural output or input use on average? The answer was broadly no.

Yields and total production showed positive signs, but the effects were statistically weak. Farmers didn’t dramatically ramp up their use of fertilizer, expand the land they irrigated, or shift to new cropping patterns in any meaningful way. And if they did, you couldn’t attribute it to the BLPs. But there was one notable exception — there was an increase in the adoption of high-yielding variety (HYV) seeds.

So, why did HYV seeds in particular benefit, but not overall agricultural output? The paper’s explanation is that access to banking does boost liquidity.

The strongest evidence is that households accumulated more savings. That gave them a larger financial cushion, even if it wasn’t enough to finance transformative investments. The paper estimates that the BLP program increased savings by roughly ₹400 per household over the decade. That was enough to buy HYV millet seeds, which cost about ₹200, or to cover some fertiliser, which ran to about ₹1,000 for an average holding.

But a groundwater irrigation pump — the kind of investment that could genuinely transform a farm’s productivity — cost around ₹4,000 at the time. And without expensive irrigation, farmers couldn’t undertake large-scale planting in the dry winter season that can significantly boost annual income. There was also no significant shift toward riskier cash crops like cotton, sugarcane, or oilseeds.

In other words, banks didn’t make farmers more adventurous in what or when they planted. On average, farming in banked districts looked a lot like farming in unbanked ones.

If this were the whole story, the paper would be a cautionary tale about the limits of supply-side financial inclusion. But it isn’t.

Climate resilience

The paper’s most important discovery is primarily about what happens when things go wrong.

See, in India, the monsoon season runs from roughly June to September. But its importance extends well beyond the summer Kharif harvest. The monsoon replenishes groundwater aquifers, fills tanks and reservoirs, and saturates the soil with moisture. All of this stored water is what the winter Rabi season, which runs from October to March, depends on for irrigation. Wheat, barley, chickpea, mustard, and sesame are all winter crops, and they need water that the monsoon left behind.

So when there’s a bad monsoon, it doesn’t just hurt you once. A drought year depletes the water reserves that the next season’s crops need, creating a one-two punch: first the summer harvest suffers, and then the winter harvest suffers too, because the irrigation water simply isn’t there.

The researchers tested whether bank presence affected this cascading relationship — specifically, whether faster bank growth weakened the link between a bad monsoon in one period and poor agricultural output in the next. And this is the most important finding of the paper.

In districts with faster bank branch growth, the damage from rainfall shocks was significantly less persistent. Farmers in these districts were better able to keep irrigating and planting through the dry winter months, even after a drought year. The magnitude of this effect is large: a 10% increase in bank branches was sufficient to reduce the yield impact of a standard negative rainfall shock by roughly 45%.

How did this work in practice? The paper points to irrigation — specifically, to the fact that farmers in districts with better banking access could afford to substitute stored rainwater with costlier groundwater pumped from wells. But if they didn’t have enough to own one, what did they do?

Well, by the 1980s, a groundwater rental market had begun to emerge across rural India, where pump owners hired out their equipment to neighbours. In fact, as per a survey by the National Sample Survey Organisation which covered 82 million farming households, 21 million owned an irrigation pump while 24 million reported hiring irrigation services from others. Even modest access to savings or credit could make the difference between renting some pump time and watching your winter crop wither.

The data also shows that bank presence specifically attenuated the link between bad monsoons and winter cropping. In districts where banks grew faster, farmers continued to plant Rabi crops even after poor rainfall — instead of abandoning the winter season altogether, which is what happens when households lack the liquidity to pay for irrigation in a drought year.

So the banks didn’t make farming more productive in normal times. But they made it dramatically less fragile in bad times. They acted as a buffer that absorbed the shock of a bad year and prevented it from cascading into the next one.

By the metric of output alone, India’s 1980s branch expansion looks underwhelming. But if the question is whether financial access improves the climate resilience of rural households, the answer from this paper is a clear yes.

What this means today

India is more financially included than it has ever been. Jan Dhan accounts, UPI, and digital banking have reached corners of the country that the BLP programme’s architects could never have imagined. But climate variability is also getting worse — monsoons are becoming more erratic, and rural India still depends heavily on rainfall for its livelihood.

This paper suggests that financial access may matter most not for its average effect on productivity, but for its role as a shock absorber. If that’s right, it reframes what we should be measuring when we talk about financial inclusion. Not just how many accounts were opened or how much credit was disbursed, but whether, when the next drought hits, farmers have enough of a cushion to plant again the following season.

Tidbits

Aurobindo Pharma has entered the biologics contract manufacturing space with the launch of TheraNym, a Rs 1,200-crore facility in Telangana. US pharma major MSD is the anchor customer for the plant, which will produce biologic medicines for global markets.

Source: Economic TimesThe OECD has raised its growth forecast for India by 20 basis points to 6.3% for the current financial year (FY27), up from its earlier March estimate of 6.1%. While the multilateral institution cautioned that energy price shocks and West Asia tensions are rekindling inflation, it maintained that the Indian economy remains resilient even as growth moderates from the 7.6% recorded last fiscal year.

Source: Business StandardIndia recorded an 18% increase in foreign direct investment (FDI) inflows during FY26, with total investments reaching $58.85 billion. Singapore retained its position as the largest source of FDI equity capital, while inflows from the United States more than doubled year-on-year, reflecting sustained global investor confidence in India’s digital economy, manufacturing capabilities, and long-term growth potential. Source: India Briefing

- This edition of the newsletter was written by Manie and Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The ₹2,500 crore loss is misleading. Strip out the rupee-driven accounting hit and IndiGo made ₹1,920 crore. The real story is $10 billion of dollar exposure with no hedge — the same asset-light model that built the airline is now its biggest liability. And the fuel pain from the Iran war hasn’t even fully landed ye

Ruppe depreciation+ Fuel price hike + December crisis= Deadly Poison for Indigo airline.