A little boy comes for India’s monsoons

How El Niño reshuffles global economic activity

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

A little boy comes for India’s monsoons

The uncertainty behind India’s car emission rules

A little boy comes for India’s monsoons

This month, America’s National Oceanic and Atmospheric Administration issued an El Niño Watch. It’s a formal signal that conditions are becoming favourable for El Niño, the climate phenomenon, to develop. The opposite, La Niña, which gave India an above-normal monsoon in 2025, is fading. By August, there’s a 62% probability that El Niño conditions will be underway.

El Niño is far from being a distant weather phenomenon for anyone, including India. It disrupts the Southwest Monsoon winds that Indian rains depend on. That, in turn, increases the occurrence of heatwaves, depressing agricultural output, lifting food prices, and straining the power grid. Its impact on the Indian economy is almost decisively negative.

But interestingly, El Niño isn’t negative everywhere. It also creates winners — including, counterintuitively, parts of India’s own power sector. And the effects that originate thousands of kilometres away, in the copper mines of Chile and the soybean fields of Argentina, eventually wash up on Indian shores through changes in the prices of imports.

Let’s dive in.`

A little boy roams the Pacific

In English, El Niño literally translates as “the little boy”. But, boy oh boy, in no way is it little as far as its climatic impact is concerned. And for that, let’s take a little lesson on oceanography.

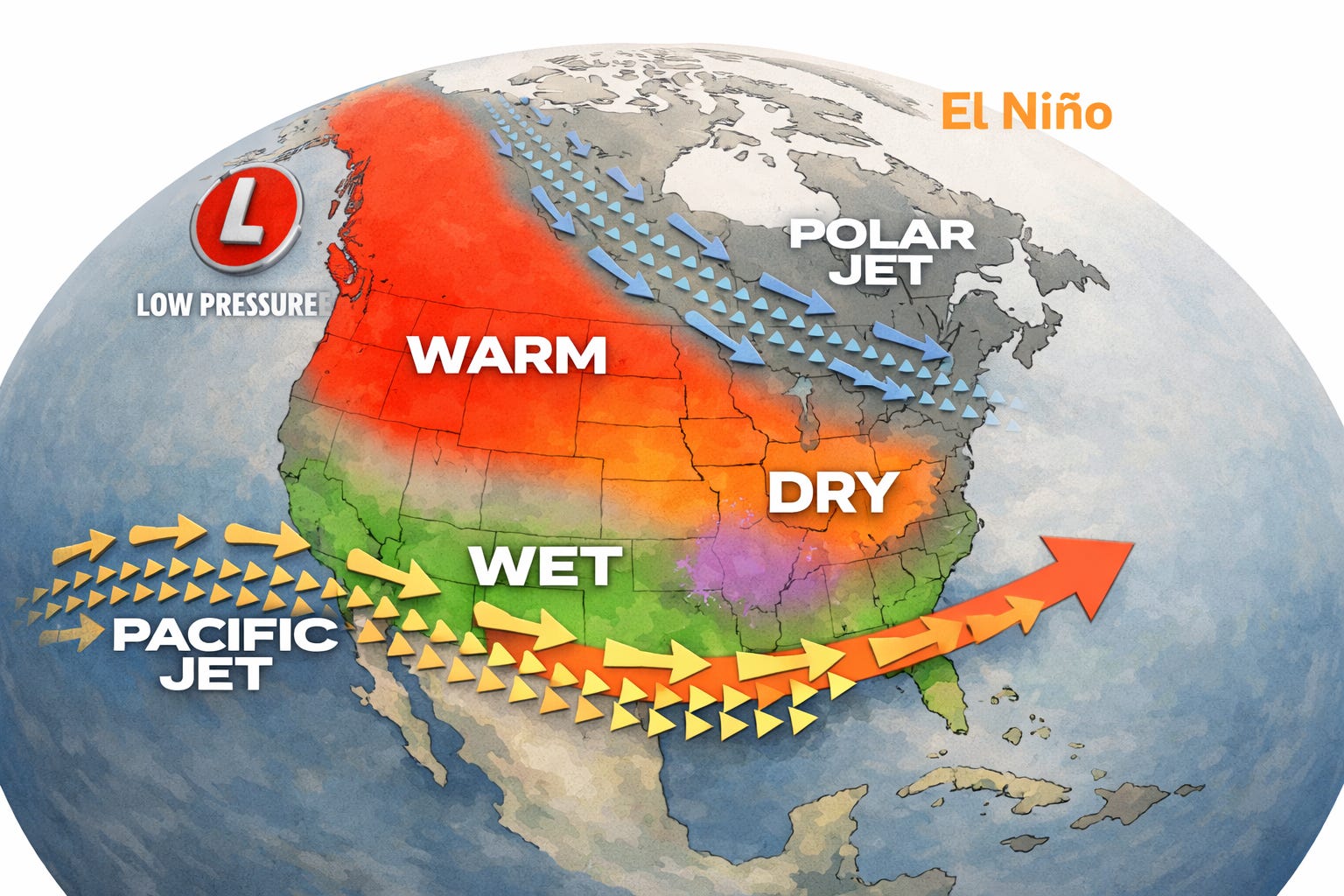

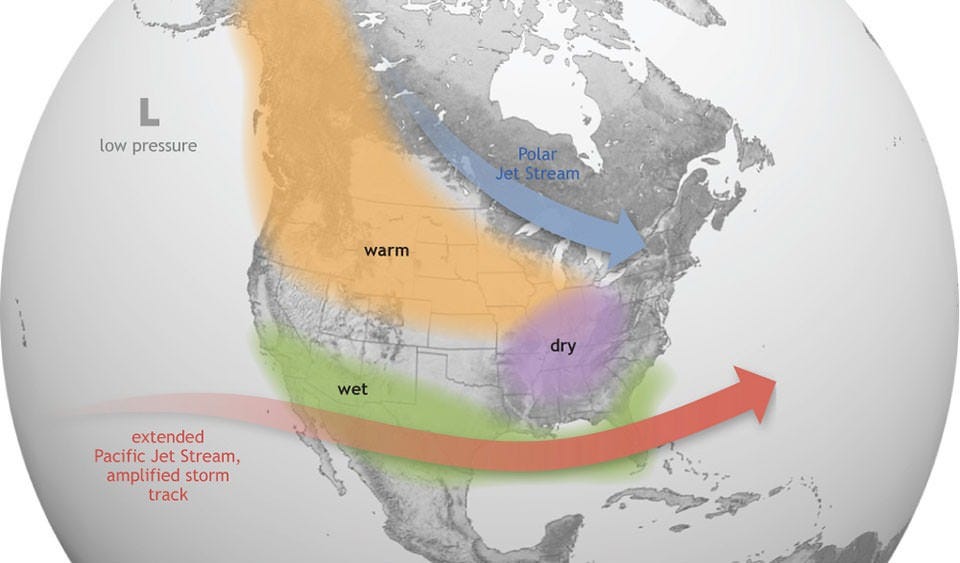

See, in a normal scenario, strong winds push warm water towards Asia, keeping the eastern Pacific (near North and South America) relatively cool. This huge movement of water splits the world into two halves of the Pacific Ocean.

On one side, you have the Western Pacific — the warm pool in the Asia-Pacific region. Eventually, the warmth makes the water evaporate into moisture, which turns into the expected rain of the July-September season, by countries like Indonesia, Sri Lanka, and India. These are also countries that, by virtue of their closeness to the Equator, generally receive a lot more heat anyway.

Meanwhile, the region around the Americas — the Eastern Pacific — remains cool and dry, almost autumn-like.

But when The Little Boy arrives, it plays spoilsport to this whole thing.

In El Niño, every few years, this wind movement weakens. The warm water sloshes back east, and sea surface temperatures in the central and eastern Pacific Ocean rise abnormally — sometimes by 1°C, sometimes by 2-3°C in a strong event. Around twenty-six El Niño events have been recorded since 1950.

Instead, you now have rains around the Americas, while most of South and Southeast Asia experiences dry heatwaves. The drought zones are mostly concentrated in the Asia-Pacific: India, Australia, Indonesia, all receive below-normal rainfall. Meanwhile, the Atlantic basin calms down, and areas like California, the American Southeast, and Argentina receive rainfall they would not otherwise get.

La Niña is the other extreme of this. Here, the moisture around the Asia-Pacific regions becomes so warm that it creates excessive rainfall. So India experiences abnormal levels of heat and humidity in this case. Our recent stretch of above-normal monsoons was La Niña-influenced, and have even caused overflowing in many cases.

Now, what you shouldn’t be mistaking them for is climate change. Both these phenomena are simply the function of the physics of heat flows. However, while climate change may not be their cause, it could be a catalyst that could amplify their effects further.

Thunderstruck

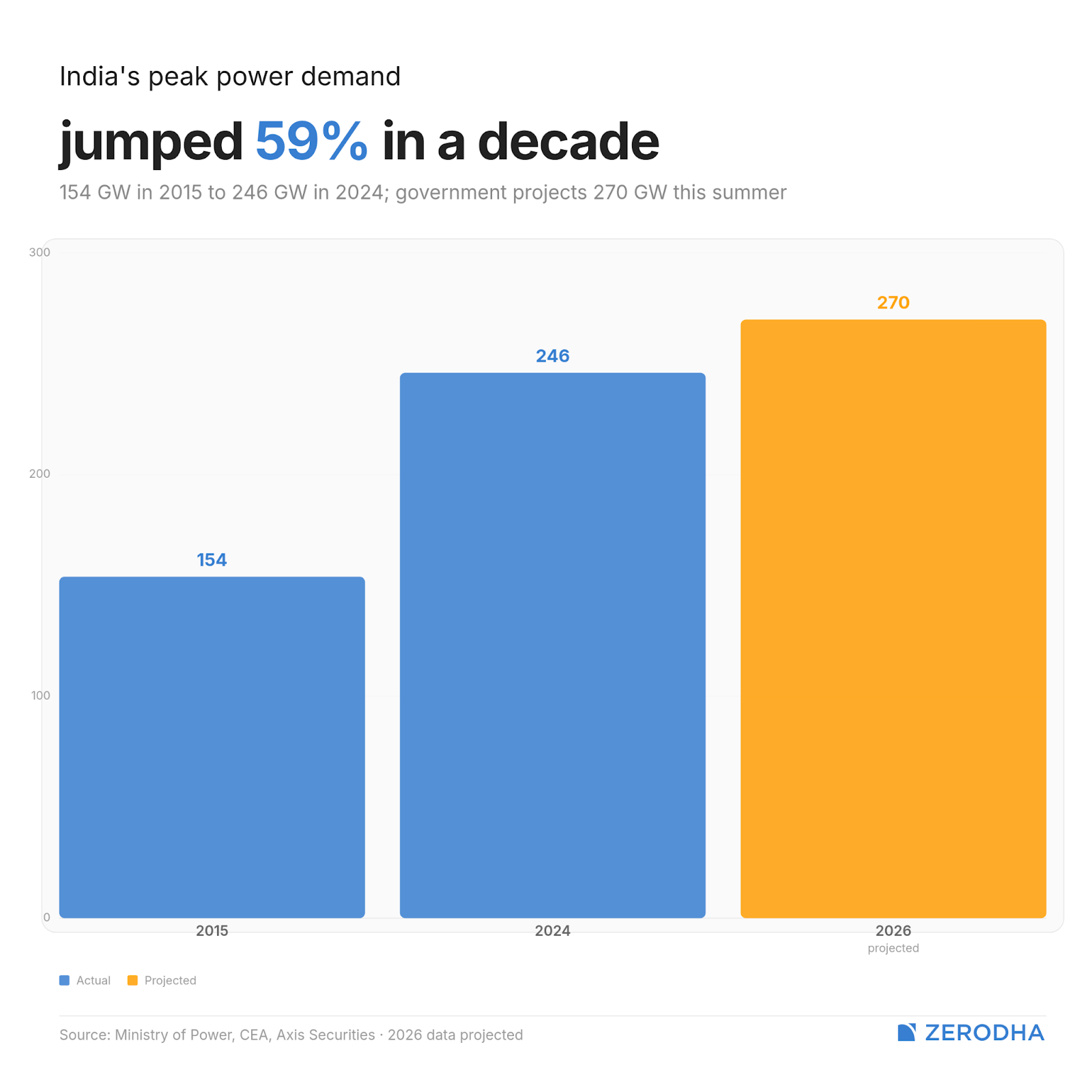

For India, the most immediately quantifiable impact of El Niño for India is on the electricity grid.

The 2023-24 El Niño event contributed directly to what became the hottest year on record for India, with average temperatures 0.65°C above the 1991-2020 baseline. Delhi’s Mungeshpur area, for instance, hit an unprecedented 52.9°C. Temperatures that extreme will require ACs and coolers running at full capacity, across millions of homes and offices, for weeks at a stretch. And that means more power.

India’s peak power demand has been climbing fast. It stood at 154 GW in 2015; by 2024 it had reached 246 GW, a 59% surge in under a decade. The government is already projecting 270 GW for this summer — an 8% jump over the all-time high. During the peak heatwave months of April-June 2024, electricity demand ran 10.8% higher than the same period the year before, with ACs accounting for almost a third of that year-on-year increase in May alone.

El Niño impacts our power demand through two simultaneous mechanisms. On the demand side, hotter summers drive more cooling load. On the supply side, a weaker monsoon drains the reservoirs and river catchments that hydroelectric plants depend on. During the first half of 2024, hydro generation fell 8% year-on-year as the lingering effects of the 2023-24 El Niño starved catchment areas of rainfall. Coal stepped in, as coal-fired generation rose 10% in H1 2024, and gas-fired output jumped 50%.

El Niño’s impact on our energy mix is indubitably one-sided: it increases our power demand while also forcing us to be more reliant on non-renewables like coal and even oil and gas. But, in recent times, solar complicates the story a little.

How so? Well, a suppressed monsoon means fewer clouds over India’s major solar-generating states — Gujarat, Rajasthan, Maharashtra. During the above-normal 2025 monsoon, solar irradiance actually fell 3-10% in those regions compared to long-term averages. But in an El Niño year, you’d have a surplus of energy from the Sun being out almost all day.

In La Niña years, the dynamics reverse. FY2024-25 saw coal generation growth at its slowest since COVID — just 2.8% — because better hydro output and renewable growth absorbed most of the base load increase. La Niña dampens the thermal sector’s windfall, while El Niño hands it one.

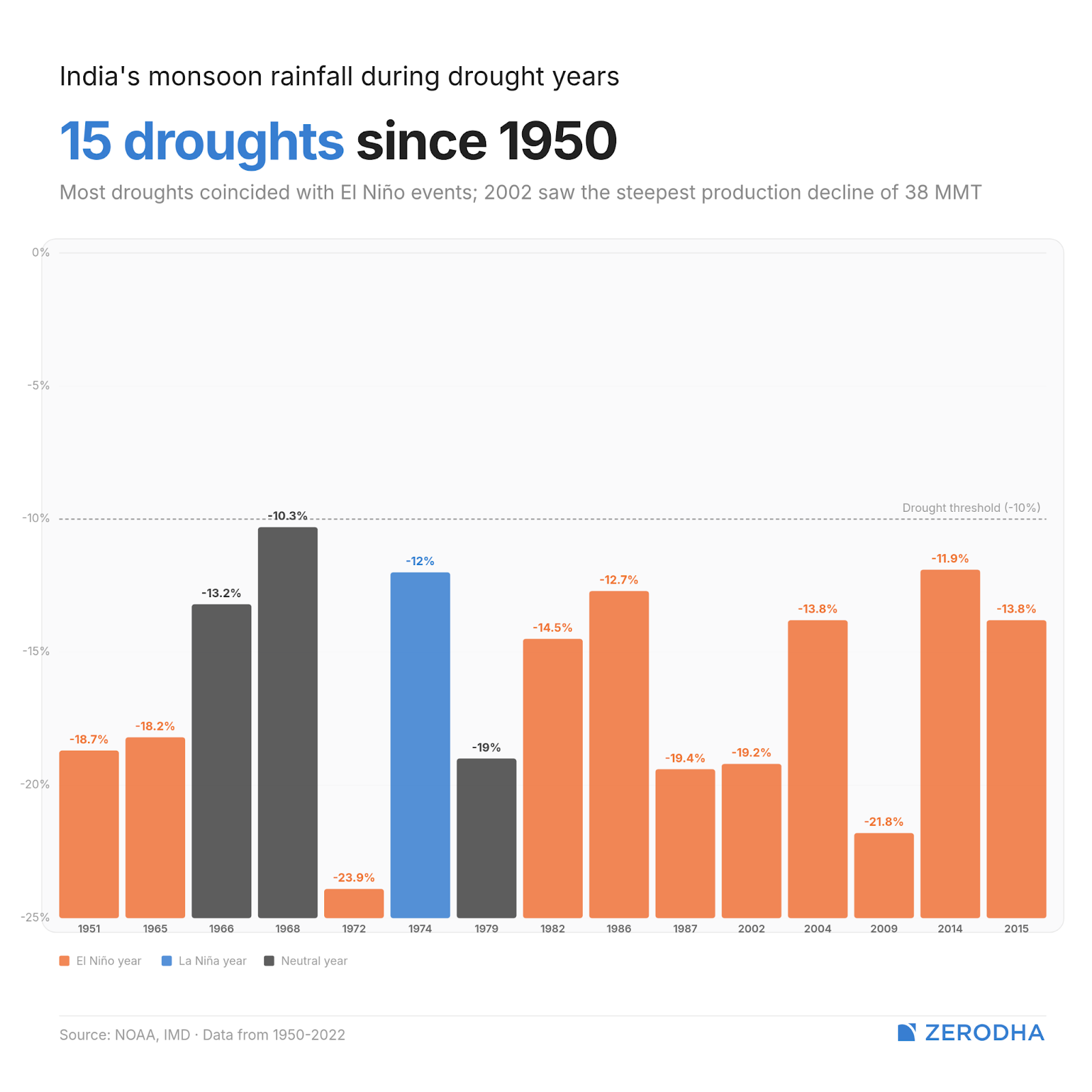

Beyond the power grid, India’s agricultural output takes a severe hit under the El Niño. Historical data from ICRIER going back to 1951 shows that 11 of 15 moderate-to-severe El Niño years resulted in a contraction of India’s agricultural output, with an average 9.7% drop in monsoon rainfall and a 5.7% fall in kharif foodgrain production.

A global reshuffle

El Niño’s economic reach extends well beyond India’s monsoon. It is a powerful shaper of agricultural output and commodity prices globally — and some of those distant reshufflings eventually arrive in India through what it imports.

We’ll mostly divide the effects into regions experiencing drought due to El Niño, and regions that get high rainfall due to it.

High and dry

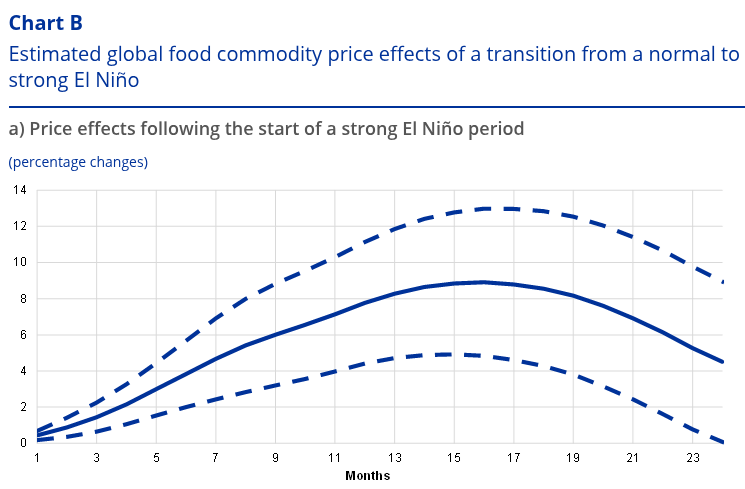

The broad pattern in drought-affected regions is consistent with what we see in India: weaker harvests leading to higher food prices, lower hydroelectric output, and greater reliance on fossil fuels. An analysis of El Niño events from the 1970s onward found that global food commodity prices rise by around 5% in an average El Niño year, with the effect lasting 6-16 months — and food is often the strongest driver of inflation. Energy prices also climb, as the same hydro deficit that hits India’s grid hits grids everywhere else, and coal and crude fill the gap.

For India, rising global food prices land with unusual force on our imports. Food makes up close to half of India’s CPI basket — far higher than in advanced economies, and comparable only to other large developing nations like Indonesia and Thailand. When palm oil (which India mostly imports from Indonesia) gets pricier because drought has hit Sumatra, Indian consumers feel it almost immediately.

Indonesia’s mining sector is also a victim of the drought El Niño brings to it. Indonesia is the world’s largest nickel producer, and its mining depends heavily on hydropower. When river levels drop, power output falls, and nickel production gets curtailed, which pushes its prices up. India has little nickel of its own, and in such a situation, we’re at the mercy of higher nickel import prices.

Nothing burns like the cold

However, the high-rainfall situations create a different set of economic effects — some obvious, some less so.

In the US, El Niño brings welcome rains to drought-prone California, benefiting water-intensive crops like almonds, avocados, and limes. The east coast of the US also sees fewer hurricanes, compared to the normal situation. The IMF found that the US is one of the few large economies that typically sees positive GDP effects from El Niño, largely through these agricultural and storm-season channels.

Argentina benefits from the same moisture redistribution, with heavier rains driving a bumper soybean harvest. Argentina exports ~95% of the soybeans it produces, so a bigger harvest keeps global soybean prices lower than they would otherwise be. That’s a genuine benefit that even India, a major importer of soybean oil, takes advantage of.

But high rainfall isn’t always a blessing. In some cases, it can completely halt economic activity.

For instance, El Niño brings heavy rainfall to Chile’s normally-dry, desert-heavy and mountainous regions. These are also areas where the country’s largest copper deposits sit. But as the mountain roads flood, mines become difficult to access and even shut down. As a result, global copper prices rise. In almost every way, this is an inversion of what Indonesia’s mining sector goes through.

India doesn’t have many copper reserves of its own. And it needs copper for cables and transformers. This, of course, inflates our import bill only further.

What India has learned to absorb

On balance, The Little Boy is bad news for India. The agricultural hit flows through a predictable chain, and since food makes up close to half of India’s CPI, that chain runs fast and deep. The global commodity effects compound it through import channels that have little to do with our domestic conditions.

Historically, one counteracting force to the El Niño has been another phenomenon called the Indian Ocean Dipole (IOD). Unlike El Niño, which acts across the world through the Pacific Ocean, the IOD only acts on the regions around the Indian Ocean. We won’t go into detail on how it works. But what you should know is that a positive IOD signals positive Indian monsoons, while a negative IOD will amplify the El Niño’s drought-like conditions. For what it’s worth, we can’t be fully dependent on the IOD to neutralize the El Niño.

What moderates the agricultural damage, and has done so increasingly over decades, is irrigation. In 1965, a drought with an 18.2% monsoon deficit caused foodgrain production to fall 19%. But in 2015, a nearly identical 13.8% deficit caused only a 0.2% fall. The difference was irrigation cover expanding from 21% to 53% over those fifty years. India has learned to absorb El Niño’s agricultural punch far better than it once did.

As for power, it makes us more reliant on non-renewables, dampening hydropower on one end while increasing coal and oil usage. However, there is a possibility that this might change with our solar buildout.

These aren’t forces that are caused by the extremities of climate change. However, climate change has made them more unpredictable, and often more negative in impact. The question for 2026, then, is how far our resilience extends.

The uncertainty behind India’s car emission rules

On the morning of February 10, 2026, executives from India’s major car companies walked into a meeting at the Ministry of Heavy Industries expecting to finish a conversation they thought was nearly done.

The Bureau of Energy Efficiency (BEE) had been consulting the industry for over a year on the next phase of India’s Corporate Average Fuel Efficiency (CAFE) rules. The executives had studied the draft, made their positions clear, and were ready to move toward a final notification.

Instead, BEE presented a version of the rules that none of them had seen before. SIAM later wrote to BEE formally noting that this was the third materially different proposal in under two years, shown to members “for the first time” at that meeting. The rules that are supposed to govern India’s car industry from April 2027 — now just over a year away — still don’t exist in final form.

How CAFE works

Let’s start with what the CAFE norms do.

If you make cars in India, the government doesn’t look at how efficient any single model is. It looks at a manufacturer’s entire fleet, calculates a weighted average CO2 emission level across all of it, and checks whether that average stays below a prescribed ceiling.

So for instance, if you sell a lot of heavy SUVs, which are considered more polluting, you might need to offset them with cleaner cars — like EVs, hybrids, small petrol hatchbacks. Fall short and you pay penalties under the Energy Conservation Act. In practice, the heavier your fleet, the harder compliance tends to be.

India has done two rounds of this already: CAFE 1 from 2017 set a fleet-average cap of 130 grams of CO2 per kilometre, CAFE 2 from 2022 tightened that to 113 grams. CAFE 3, which was drafted in September 2025 and is expected to run from April 2027 through March 2032, may tighten it further still.

Now, the September 2025 draft sets each manufacturer’s allowed average using a formula that links to the average weight of their fleet. Heavier fleets got a slightly more lenient ceiling, while lighter fleets face one that’s more demanding. Manufacturers can also pool their fleets with other manufacturers and be treated as a single entity.

The reason BEE has been confident enough to keep tightening its proposals is the compliance data it has collected under CAFE 2. For instance, Tata Motors’ Passenger Vehicles recorded fleet emissions of 95.1 grams per km in FY24 against a permitted target of 119.7 grams — a cushion of over 24 grams, driven by its EV and CNG-heavy portfolio. Maruti Suzuki came in at 103.6 grams against a target of 109.2 grams.

BEE’s conclusion from the data was that the gap between targets and actual emissions has been widening across the industry. To them, that suggested the industry can handle tougher standards.

That’s where the conflict between SIAM and BEE begins. But even before that, the September 2025 draft had already divided the industry.

Heavyweight clash

The provision that consumed most of the public debate is a single paragraph in the September 2025 draft, which reads:

“Considering the limited potential for efficiency improvements in petrol vehicle models with an unladen mass up to 909 kg, engine capacity not exceeding 1200 cc and length not exceeding 4000 mm, said motor vehicle model shall be eligible to claim...a further reduction of 3.0 g CO₂/km in its manufacturer-declared CO₂ performance.”

What that means is a small, light petrol hatchback would effectively get a compliance advantage — treated as emitting less than it actually does. And Maruti Suzuki controls roughly 95% of this specific segment.

At the formal SIAM vote on November 7, 15 companies voted against the exemption, and only 4 firms supported it: Maruti, Renault, Toyota Kirloskar and Honda. Most of the industry argued that such a provision benefiting just 4 firms isn’t a public interest measure. Moreover, they said that incentivising lighter cars risked reversing India’s safety progress, since no car currently under 909 kg carries a Bharat NCAP rating.

Meanwhile, of those 15, Tata didn’t oppose stricter CAFE norms. However, they didn’t think that petrol-based cars in particular should get such exemptions. Rather, emissions should be curbed through the use of green technologies like EVs and CNG — which Tata has a healthy portfolio of compared to the competition. Moreover, they also argued that by virtue of the new CAFE formula, lower-weight cars already get an advantage.

However, the 4 firms who supported the proposal make up 63% of India’s passenger vehicle production, which mostly includes small, affordable cars bought by the Indian middle class. Maruti aggressively pushed for the exemption. In fact, in the first CAFE 3 draft released in June 2024, Maruti was frustrated with the lack of any meaningful exemption for small cars.

We covered Maruti’s side of this argument in depth in a previous Who Said What episode.

Uncertainty and indecision

BEE published the first CAFE 3 draft in June 2024. In September 2025 came the substantially revised second draft with the 909-kg exemption. By December, JSW MG Motor, Tata Motors, and Kia had written directly to the PMO opposing the carve-out. The SIAM vote left the industry body unable to present a unified position. And by January 2026, Toyota Kirloskar was publicly asking the government to issue a clear, final notification soon so the industry could plan.

Then came February 10. BEE’s third draft dropped the 909-kg exemption but introduced annual tightening targets. The industry-wide emission ceiling fell from 92.5 grams per km in FY28 to 77.08 grams per km by FY32, versus the 113 grams under CAFE 2 today. And BEE suggested reducing the limit every year.

SIAM’s email to BEE on February 19 set out the frustration plainly: significant variations from previous versions, seen for the first time at that meeting. The industry body called for a single target of 89.6 grams per km for the entire five-year period — the same block structure used under CAFE 1 and CAFE 2. Even Tata, the most vocal in favour of tougher targets, said through a spokesperson that annual tightening “could be challenging” and supported SIAM’s call for a clearly-defined CAFE-3 target.

At Mahindra’s Q3 FY26 analyst meet, an analyst asked the CEO whether the proposed norms were achievable given Mahindra’s current EV portfolio. His answer: “Okay, let me take the question on which there’s no answer, which is CAFE.“ It wasn’t an evasion, but rather a reflection of how hard it is to plan billion-rupee investment decisions against nonstop policy flip-flops.

In March, the government shared an internal compliance assessment for the first time at that meeting. Tata was projected to meet CAFE 3 targets consistently. However, Maruti and Hyundai were expected to be struggling. Meanwhile, Mahindra expected to miss targets in the first three years. The same report said the government is now considering pushing back the April 2027 start date entirely.

A difficult conundrum

BEE’s data shows every major carmaker has been meeting CAFE 2 targets with a growing cushion — evidence, BEE argues, that the industry can handle tougher standards. But the PMO’s own internal assessment shows at least three major manufacturers may be unable to comply under the current CAFE 3 framework.

Both things are true simultaneously, and they don’t resolve cleanly against each other. After all, CAFE 2 is a standard the industry adapted to over years, while the February 2026 proposal is a step-change that the data suggests several manufacturers genuinely aren’t ready for.

The whole point of a tightening standard is to push companies toward investments they wouldn’t otherwise prioritise. But there’s a difference between a standard that stretches an industry and one the industry can’t plan toward because it keeps changing. Powertrain decisions get made three to five years before a car reaches the market.

By the time the rules are finalised, many of those decisions are already locked in. If the target formula is still being negotiated just over a year before the regulation is supposed to kick in, those decisions have already been made in a vacuum.

The industry isn’t asking for the standard to disappear. It is asking for certainty about what the standard will say. That is not an unreasonable ask. But what’s clear is that let alone the government and industry conflicting — the industry itself is fragmented on what CAFE 3 should look like. And it won’t be easy to get alignment on what the standard should be.

Tidbits

The government launched a RELIEF scheme for exporters hit by the Middle East conflict. With the Iran war disrupting shipping routes, pushing up freight and insurance costs, and closing key Middle Eastern markets, the government has rolled out a scheme called RELIEF to support affected exporters. Details are still emerging, but it’s expected to include credit guarantees for small businesses and targeted support for sectors like textiles and gems & jewellery.

Source: MoneyControl

The rupee slid to 92.94 against the US dollar on Friday — a new all-time low. The culprit is the same as it’s been all month: surging crude oil prices from the Iran war, persistent FII outflows, and a hawkish Fed that held rates steady this week. The RBI has been intervening to prevent a sharper slide, but with Brent crude still hovering around $107 a barrel, the pressure isn’t going away.

Source: Bloomberg

SBI Funds Management has filed a DRHP with SEBI files for an IPO, which is entirely an offer-for-sale — SBI will offload 12.83 crore shares (a 6.3% stake) and French partner Amundi will sell 7.54 crore shares (3.7%), for a combined 10% dilution. No fresh shares will be issued. Market sources peg the issue size at roughly ₹12,500 crore, which would value the company at around ₹1 lakh crore. SBI Funds manages over ₹16 lakh crore in AUM and commands a ~15.5% market share.

Source: Business Standard

- This edition of the newsletter was written by Manie and Krishna.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Dude, you explained the el Nino El nina effects better than my freaking geography teacher back in the 90s!!

The sooner we move to stricter emission standards, the faster we will reduce vehicular emissions.

I don't think there should be exemptions for anyone - small cars especially. There's enough technology in the world to meet CAFE norms. Our markets are big enough for any major Auto OEM to invest.