Gold, securitised

Why India hasn’t taken to electronic gold receipts (EGRs) yet.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Gold, securitised

Indian alcobev keeps the spirits alive

Gold, securitised

In December 2025, SEBI Chairman Tuhin Kanta Pandey publicly said that the framework for Electronic Gold Receipts, or ‘EGRs’, needed a review.

EGRs are SEBI-regulated securities that have been trading on BSE since October 2022. Only, the SEBI Chairman wasn’t content with how the product was faring. Its adoption hadn’t met expectations; it hadn’t become the gold price discovery benchmark it was designed to be. Some GST-related issues kept creating friction in how they worked.

Five months later, though, on May 4, 2026, NSE launched its own EGR segment anyway.

This adds yet another item to India’s confusing menu of gold products. Indians can buy physical gold — which is pure and battle-tested, but comes with problems ranging from storage to liquidity. There are a host of fintech apps that let you buy ”digital gold”, but that sits outside SEBI’s rulebook, as we covered in November. There are Sovereign Gold Bonds — a promising offering that was shelved in February 2024 because they became too expensive for the government to keep issuing. And finally, there are Gold ETFs that give you price exposure but no physical gold, something that’s emotionally important for us Indians.

The EGR was supposed to solve all those problems. These were regulated, liquid, tradable products that give you both price exposure and physical ownership, should you want it. This was supposed to be India’s most ambitious gold-related experiment since SGBs were introduced a decade ago.

But do they actually fulfil that promise? And why doesn’t the very regulator who created them think they’re working yet?

What an EGR actually is

It all started when, in December 2021, the Ministry of Finance notified Electronic Gold Receipts as being “securities” under the Securities Contracts (Regulation) Act, 1956.

That single technical change gave birth to a whole system.

The notification put EGRs in the same legal category as listed shares. It signalled that EGRs weren’t a commodity like physical gold, nor were they a contract for gold, like MCX futures. They were actual securities. To give you a sense of how big a deal that is, the crypto industry has been pushing for cryptocurrencies to be recognised as securities for years, hoping for the legitimacy it brings. That was a status EGRs were given on a platter.

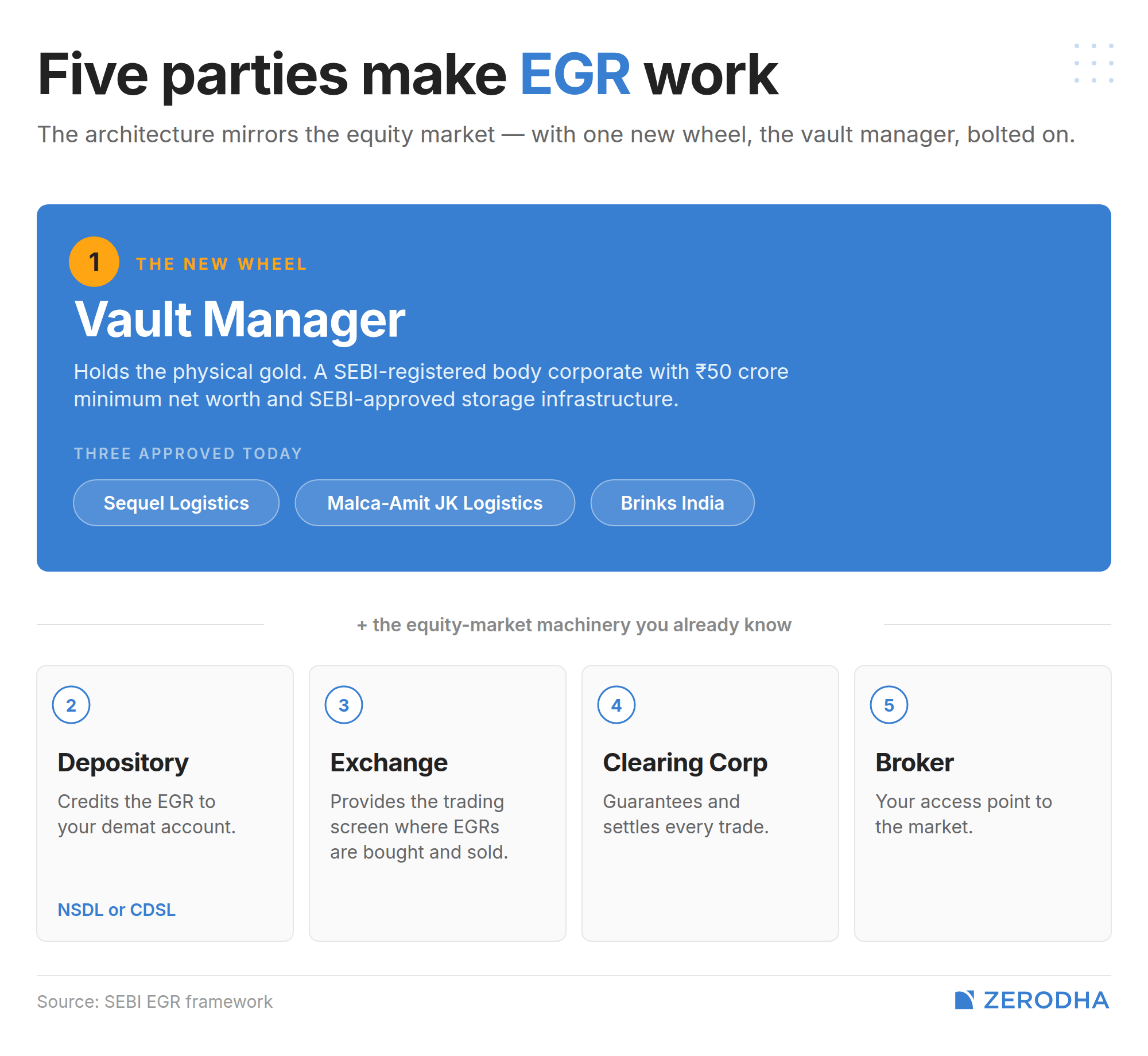

A week after that notification, SEBI came out with the Vault Managers Regulations, 2021, creating the new class of intermediaries. The next month, SEBI issued the ‘Gold Exchange Framework’, which defined how the product would actually trade.

It was putting together a system that connected five parties. SEBI-registered ‘vault managers’ — body corporates with a net worth of at least ₹50 crore, with SEBI-approved storage infrastructure — would hold physical gold. As of today, there are three: Sequel Logistics, Malca-Amit JK Logistics, and Brinks India.

These vault managers would provide a foundation on which standard capital markets institutions would operate. The EGRs built atop those deposits would sit in your demat account, in the depository system. Exchanges would provide a trading screen that you would access through a broker. Clearing corporations would guarantee and settle trades. It was an architecture that deliberately mirrors equity markets, bolted on to gold rather than shares.

EGRs have a lifecycle that SEBI divides into three “tranches”.

Tranche 1: Creation

EGRs are created when physical gold enters the system. A depositor — anyone from a jeweller, to a refiner, to a bank, to even a retail investor with a gold bar — would bring physical gold to a vault manager. Not any gold, though: it has to be freshly imported, or refined by an exchange-approved domestic refinery. It must meet either the international benchmark — LBMA Good Delivery Standard — or India’s own India Good Delivery Standard.

The vault manager weighs and assays the gold. They certify its purity, check its documentation for traceability, and then log everything into a system depositories have built, so that all parties can see and reconcile everything. Once gold is locked in, the vault manager creates an EGR in the depositor’s name, which the depository credits to their demat account.

The single most important rule of the whole framework was that a vault manager cannot create an EGR without physical gold being present in its vault. To enforce this, the vault manager and the depository reconcile records continuously, and the depository periodically inspects vaulted gold physically. Unlike “digital gold”, this guarantees that investors are safe from counterparty risk, because of the certainty that every EGR was backed by gold.

Tranche 2: Trading

From this point, EGR behaves like a share that you can trade on the exchange. There are two things that make this system work: fungibility and interoperability.

EGRs are fungible; i.e. they aren’t tied to a specific bar’s serial number. If you deposit gold and an EGR is created, that goes into the system, where all bars of a type are considered identical. If you withdraw later, you’ll get gold of the same purity and weight, but it probably won’t be your specific bar. That lets them become interoperable. Gold deposited at one vault location could be withdrawn from a different location, or even from a different vault manager.

In other words, India’s securitised gold effectively becomes a single national pool. That’s what makes it tradable. In a sense, the identity of any one bar of gold is dissolved. It just becomes an ISIN with some broad details.

There are two ‘series’ of EGRs, based on their purity — 999, which is 99.9% pure, and 995, which is 99.5% pure. These can be traded in denominations running from 100 milligrams to 1 kilogram. Those denominations need not be what the depositor actually puts in. If a jeweller deposits a 1kg pure gold bar with the vault manager, that can trade as 100 units of 10 grams, without any change to the gold itself.

Keeping gold in a vault isn’t free, though, and vault managers aren’t doing charity. So, vault managers levy a storage per-gram, per-day fee on every EGR holder. This is built into the system itself. SEBI requires every vault manager to publish its rates on its website, which are baked into the EGR record at creation itself. Brokers collect these charges from an investor’s account and pass them to the depository, which then remits it to the vault manager. This is the same pipeline through which corporate actions on shares flow.

This system ensures that, unlike with digital gold, you know exactly what you’re paying.

EGRs can also be moved off-market. They can also be pledged as collateral against a loan. Some day, this might help create a system of instant digital gold loans. India already has a massive gold loan market built almost entirely on jewellery valuation by branch staff. EGR loans could become a more sophisticated, standardised version of that. But that’s still in the future.

Tranche 3: Conversion

EGRs expose you to the price of gold, much like a Gold ETF. But crucially, they also let you take the gold home if you’d like.

A holder can place a withdrawal request with their depository. The depository then checks that storage charges have been paid, before forwarding the request to the vault manager. The vault manager arranges delivery of physical gold, while the depository simultaneously extinguishes the EGR from the investor’s demat account.

But there’s friction here. A 3% GST is levied at this point, because as soon as gold is physically delivered, the system legally treats it as a “sale of goods”. On the flip side, though, if you send someone an EGR itself, that isn’t taxed like a gold transaction. There’s no GST.

With income tax, it’s the opposite. According to rules of the Income Tax Act, converting physical gold into an EGR — or vice versa — is not a “transfer”. A conversion doesn’t create capital gains. On the other hand, if you transact in EGRs, that is taxed like any listed security. So, long-term capital gains kick in after 12 months at 12.5%, compared to 24 months for physical gold.

Why it hasn’t worked yet

BSE launched its EGR segment during muhurat trading in October 2022. Three and a half years later, though, trading volumes are so thin that researchers genuinely struggle to compare them meaningfully against Gold ETFs.

What went wrong?

The most obvious is awareness and enablement. Unlike ETFs, which have seen marketing campaigns and YouTube explainers, EGRs simply weren’t publicised enough. Meanwhile, most brokers that handle the vast majority of India’s retail demat accounts had not enabled the EGR segment. Without that, retail can’t actually buy what NSE is selling.

But there’s a deeper problem: vault infrastructure. India has just three approved vault managers, who run out of a handful of locations, mostly in metros — Mumbai, Delhi, Ahmedabad, Chennai. EGRs are premised on uniform pricing across India: one national gold price, discovered through exchange trading, that replaces the patchwork of city-level jeweller quotes. But that promise has to rest on something physical. To create an EGR, you have to bring gold to a vault. To take delivery against one, you have to collect gold from a vault. Someone in Coimbatore or Lucknow can buy and sell EGRs on the exchange, but the moment they want to deal in physical gold, they have to find a way of transporting it safely to a metro or back.

For “one national price” to mean something across the country, EGRs need a vault network that reaches deep into Tier-2 and Tier-3 cities. Until that happens, every withdrawal or deposit from outside major metros carries a massive logistics tax.

Then, there’s GST.

When physical gold first enters India or moves between commercial players (refiners, importers, traders), it attracts GST. They would normally claim input tax credit on this — that is, they would recover the GST they paid by setting it off against the GST they collect on their own sales. But that doesn’t work with EGRs. Once gold gets converted into an EGR — a security — it stops being a “good” for GST purposes.

And then, when it’s eventually converted back to physical gold and withdrawn, GST applies again at 3%. The transitions in and out of the security wrapper create complications that nobody has solved.

The result is that institutions — the very people who should be creating EGRs in bulk and providing liquidity — find the process more painful than it needs to be. And when institutions don’t show up at scale, trading volumes stay thin. The market becomes illiquid, with wide bid-ask spreads. And that makes the entire product unattractive.

What this is, and isn’t

What India has built, on paper, is impressive. In practice, though, it comes with last mile problems and regulatory issues that threatens its survival. And not enough people are interested, yet, for things to be fixed.

Investors that simply want a play on gold prices can simply go for Gold ETFs. Indeed, that’s a more liquid market with better price discovery. Meanwhile, the product is riddled with too many issues for those who want regulated gold exposure with the option of physical delivery at the end.

Can NSE’s new issue change that, though? Can it get enough people interested that the other problems are ironed out? We’ll be watching earnestly.

Indian alcobev keeps the spirits alive

We’ve been tracking India’s alcobev industry for a while now. We broke down the complicated liquor game earlier this year, looking at how state-level policies can make or break an entire market overnight. Then we covered the Q2 FY26 results, where premiumisation and backward integration were the stories that mattered.

In the last quarter of the year, the same structural themes are still at play: premiumisation is accelerating, state-level regulations remain a wildcard, and companies are diverging sharply in how they’re handling it all. But a new variable has entered the equation. The war in the Middle East, the closure of the Strait of Hormuz, and surging aluminium prices have introduced a cost shock that is hitting one corner of this industry far harder than the rest.

We’re looking at two spirits and a brewer — Radico Khaitan, United Spirits (USL), and United Breweries (UBL) — to explain what’s going on.

The numbers

Let’s start with the numbers.

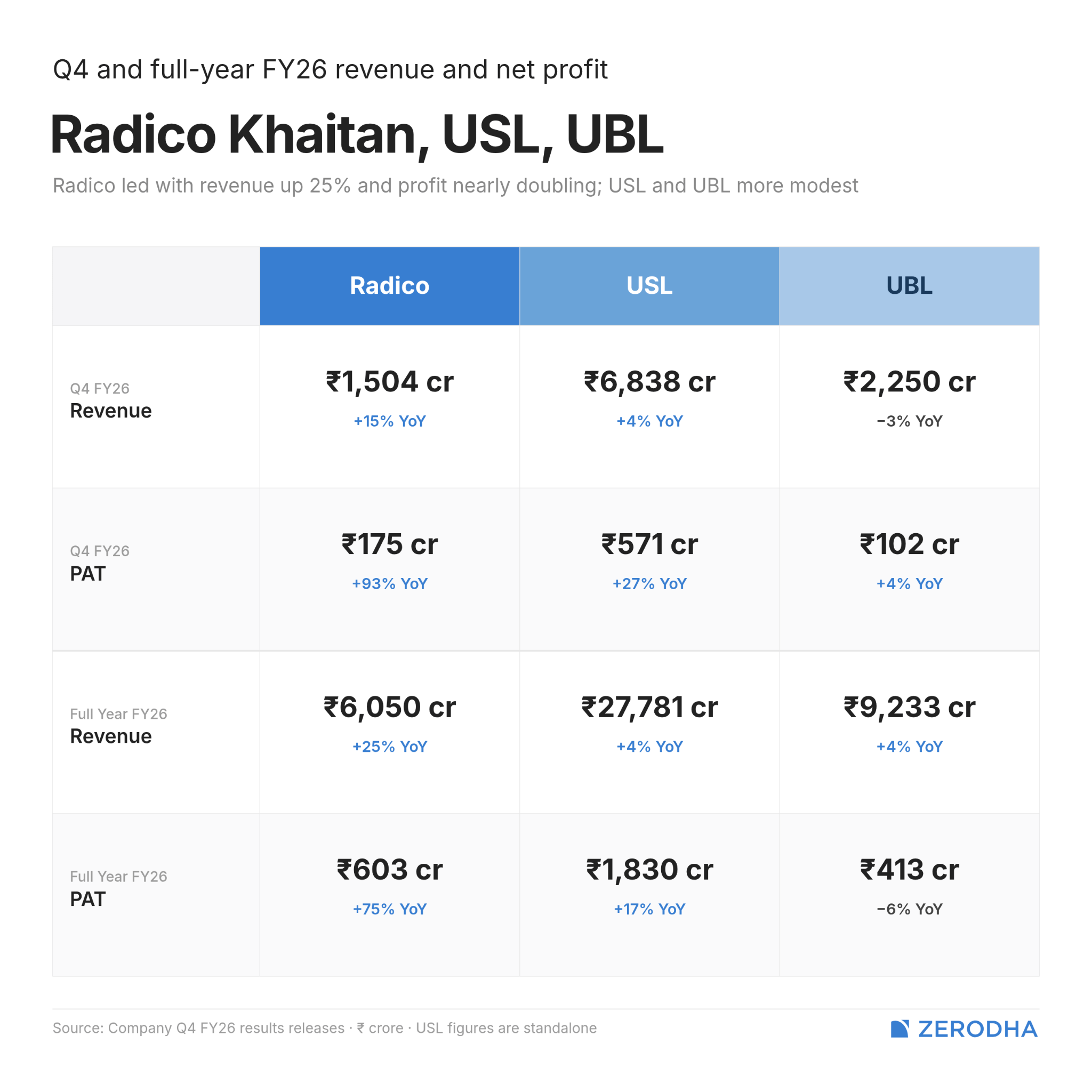

Radico Khaitan continues its streak of being the fastest-growing of the three. Its Q4 revenue came in at ₹1,504 crore, up 15% year-on-year. Its net profit nearly doubled from Q4 FY25 to ₹175 crore, and its EBITDA margins expanded from ~13% to 19% — its highest-ever quarterly EBITDA margin. For the full year, Radico’s revenue rose by 25% y-o-y to cross the ₹6,000 crore milestone for the first time, and its net profit grew by a whopping 75% to over ₹600 crore.

Meanwhile, United Spirits had a more muted (but resilient) quarter. Operating revenue grew by 4% to ₹6,838 crore, and EBITDA rose 17% to ₹591 crore. The reported net profit of ₹571 crore was up 27%, but that’s flattered by a one-time ₹219 crore tax refund benefit. Strip that out, and you’re looking at a more modest quarter.

For the full-year, operating revenue went up 4% to nearly ₹27,800 crore, while PAT margins were at 6.4% — higher than 5.7% in FY25.

United Breweries’ Q4 revenue fell 3% to ₹2,250 crore despite volume growing 4%. Operating margins compressed to about 6%, down from 8% a year ago. Net profit was ₹102 crore, barely up 4%. For the full year, PAT came in at ₹413 crore, down from ₹442 crore in FY25. However, considering that two quarters ago, their volumes fell in regions with a rain shock, this was a noteworthy comeback for them.

Premiumisation: three Indias, one direction

The premiumisation trend in Indian alcobev is not new — we’ve covered it in every edition. But Q4 FY26 adds a useful framework for thinking about it.

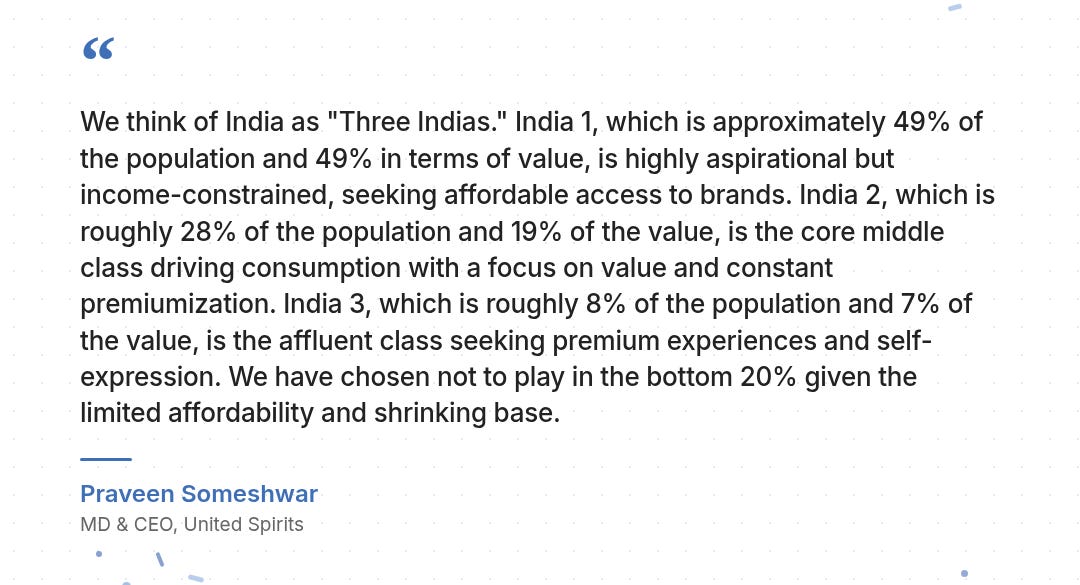

United Spirits, in its earnings call, laid out what it calls the “Three Indias”. In their view, India 1 is about 49% of the population — aspirational but income-constrained. India 2 is the core middle class, about 28%, constantly upgrading what they drink. India 3 is the affluent 8% — spending big on single malts, tequilas, and craft spirits. USL has chosen to exit the bottom 20% of the market entirely to focus on these three rising tiers.

This is also the operating principle behind what all three companies are doing.

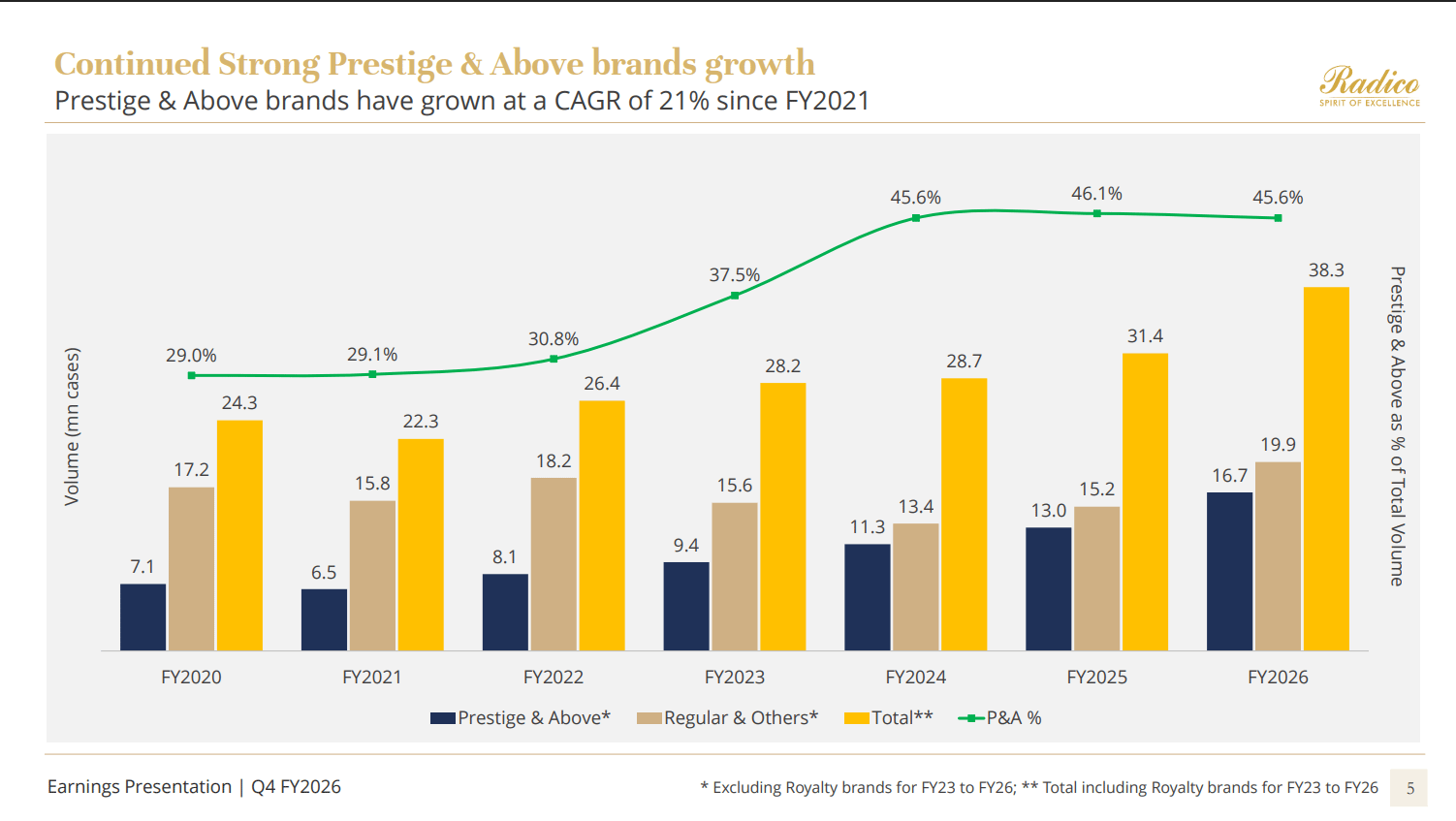

Radico’s “Prestige & Above“ (P&A) segment, for instance, grew volumes by 28% this year, and now accounts for almost 70% of sales by value. Its luxury portfolio — which includes Rampur single malt, Jaisalmer gin, and so on — delivered ₹475 crore in Q4 revenue, up 40% from last year. Management is targeting 25% growth in this portfolio next year.

United Spirits is executing a similar playbook from a more mature base. Its P&A segment now makes up more than 90% of net sales. Smirnoff crossed 1 million cases for the year, with Q4 alone contributing more than 400,000 cases. Don Julio tequila became the fastest brand in USL’s portfolio to cross ₹100 crore in net sales, and has already captured a third of the Indian tequila market. India is now the third-largest global market for Johnnie Walker by volume.

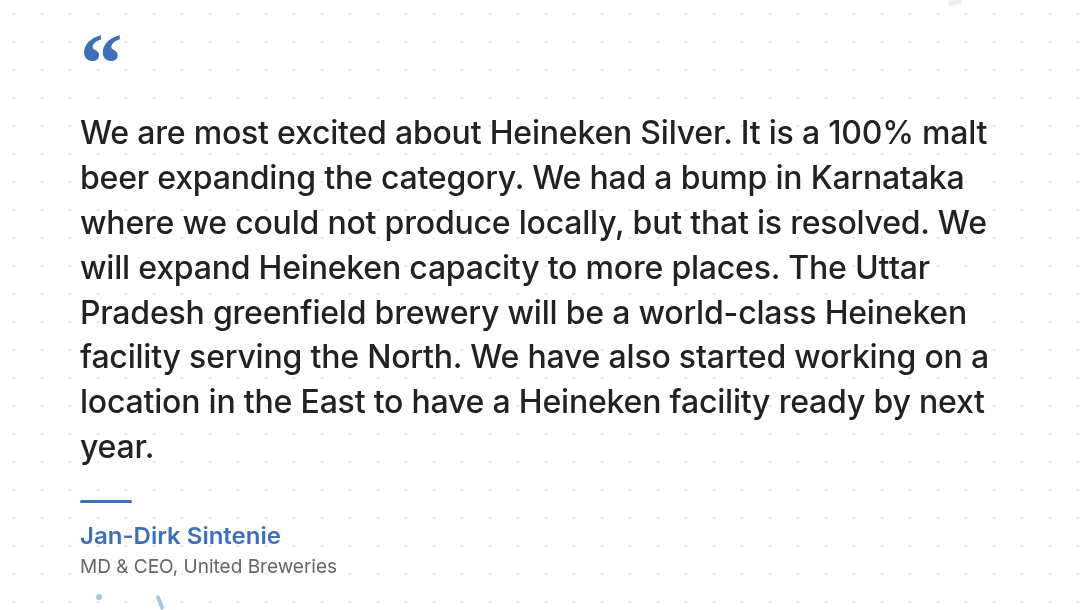

Even United Breweries, which had the weakest overall quarter, saw its premium segment grow 16%. Heineken Silver, a 100% malt beer, is UBL’s big bet, and the company is localising production across eight breweries to protect margins on it. But premium still makes up less than 10% of UBL’s total portfolio. It’s far behind the spirits players in that regard.

What’s clear is that Indian consumers — especially Gen Z — may be choosing to drink less but drink better. Pocket-sized 180ml and 200ml formats are making premium brands affordable for first-time trials, creating an entry ramp into premium brands without the full-bottle commitment. This is structural, not cyclical. And each company has plans to further increase the number of brands under their P&A umbrella.

The state-level maze

But if premiumisation is the structural tailwind, state-level excise policies have been, for all of last year, the obstacle course.

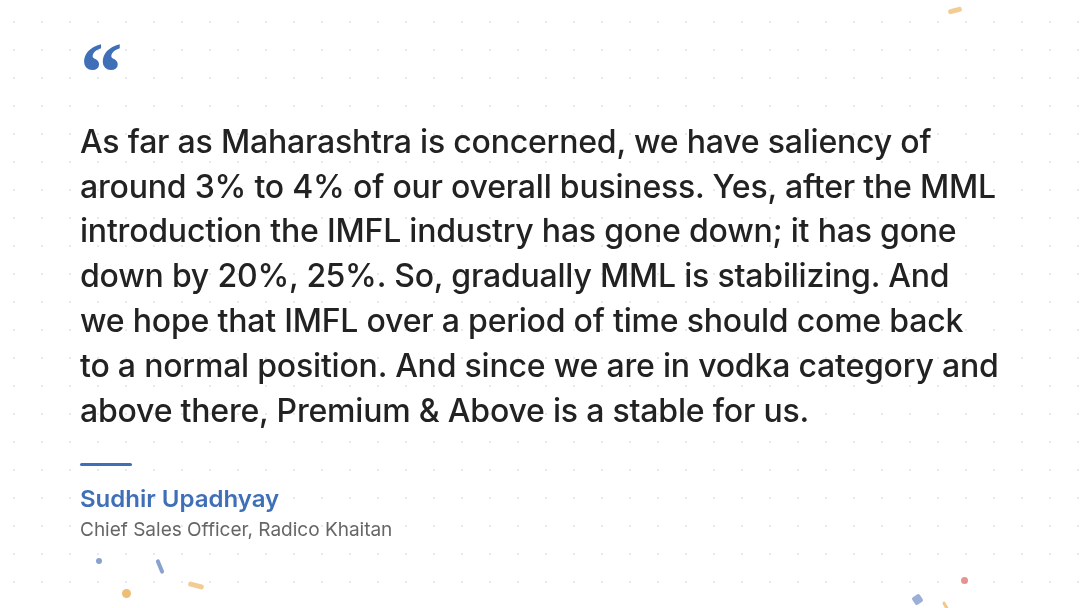

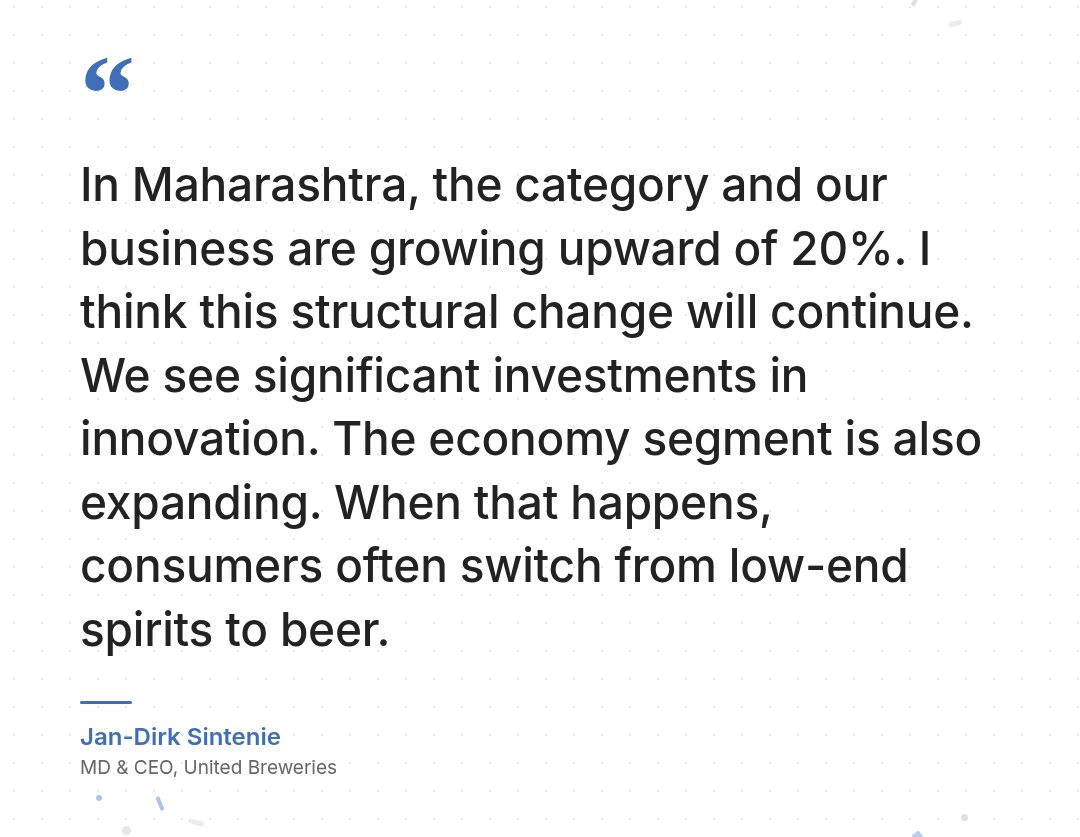

For instance, Maharashtra’s “Maharashtra Made Liquor” (MML) policy has been the biggest disruptor. The capped excise duty hike pushed regular spirit prices up by as much as 80%, while premium labels saw only a 10% increase. As a result, industry volumes in the state have dropped by roughly 20%.

Each company has responded differently.

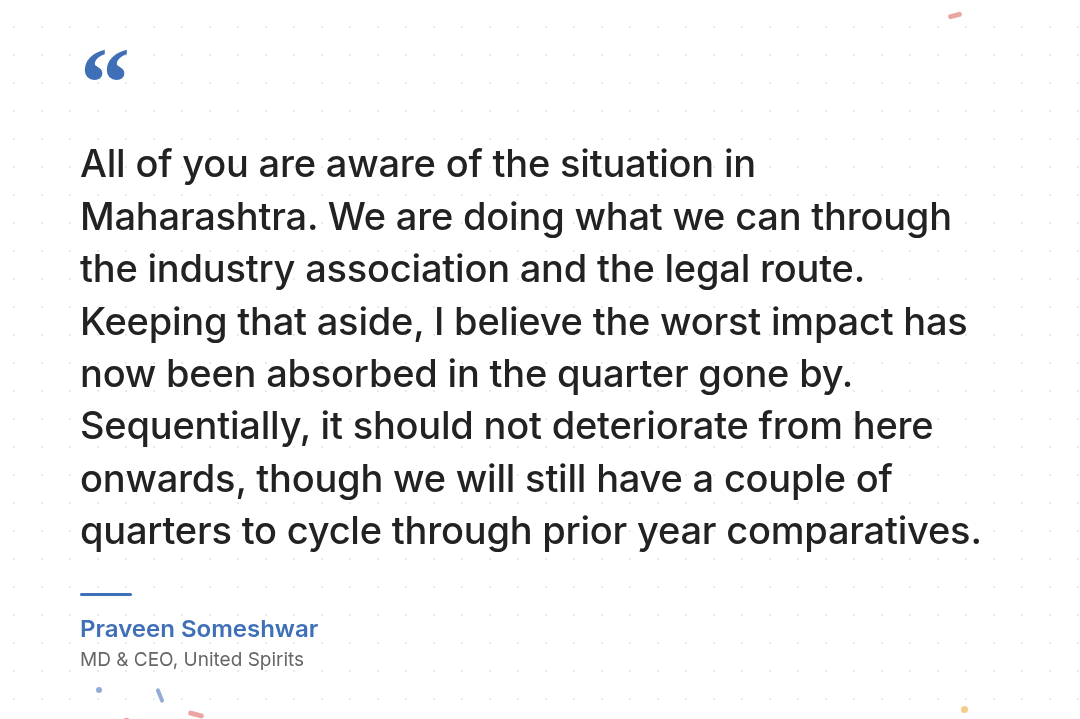

United Spirits, which has no MML play, took the hit directly. Its mid-range brands like McDowell’s and Royal Challenge saw prices jump roughly 35% two quarters ago. But management says the worst of the shock was fully absorbed this quarter.

Radico, by contrast, entered MML through a joint venture last quarter, and is actually targeting a 10% market share in the category.

Now, beer was exempt from the tax hikes entirely, which, for UBL’s beer-heavy portfolio, meant incredibly good fortunes. It reported more than 20% growth in the state as consumers switched from newly expensive spirits to beer.

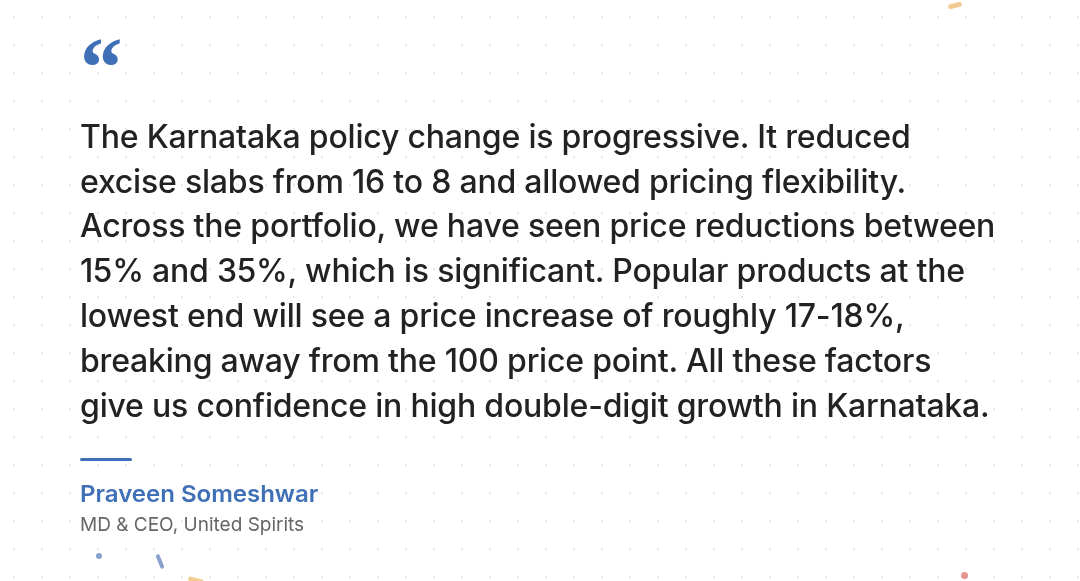

Karnataka, meanwhile, moved in the opposite direction. Progressive reforms reduced excise slabs from 16 to 8, effectively dropping premium spirit prices by 15-35% while raising the floor on cheap liquor. Both USL and Radico see this as a major tailwind for premiumisation.

Andhra Pradesh, meanwhile, is settling into its new normal after last year’s dramatic reopening to private retail. Radico went from 10% to 30% market share in one year, but both Radico and USL are now dealing with the base effect — year-on-year comparisons look soft because last year’s numbers were inflated by that initial rush.

The takeaway is the same as always: in Indian alcobev, the national story is the sum of 28 different state stories. And you can’t evaluate any company without understanding the policy hand it’s been dealt.

The geopolitical squeeze

No results story this quarter would be full without a mention of the crisis at the Strait of Hormuz. It has introduced a cost shock that is hitting the Indian alcobev industry — and one company in particular. And that difference is simply explained by why the crisis matters more to beer than spirits.

See, beer cans are made from aluminium, and aluminium prices were already climbing before the war, driven by rising demand from electric vehicles, solar panels, and data centres. Pre-war, global prices hovered around $3,200 per tonne and the market was already facing a modest supply deficit.

When the Strait of Hormuz closed, Middle Eastern aluminium output — about 9% of the global total — was suddenly cut off from European and American ports. Aluminium Bahrain, which operates the world’s largest smelter, cut production, and prices surged to a four-year high of $3,500 per tonne.

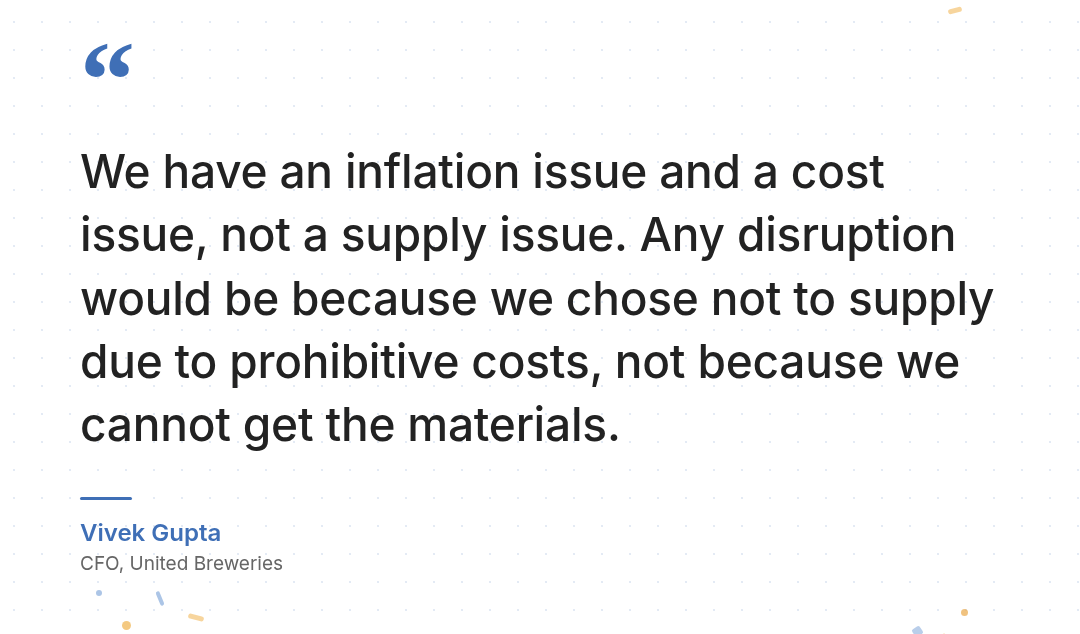

Naturally, that means UBL was hurt the most out of all three. Management has explicitly flagged a potential ₹400-500 crore cost impact over the next two to three quarters — driven by aluminium, energy costs, and shipping disruptions. The company has already stopped selling cans in Telangana because the margins no longer make sense, and its market share in the cans segment there has dropped to less than 2%.

That being said, UBL doesn’t face a shortage of cans. The only reason they may cut back on beer cans is because there are no incentives for them to sell those cans.

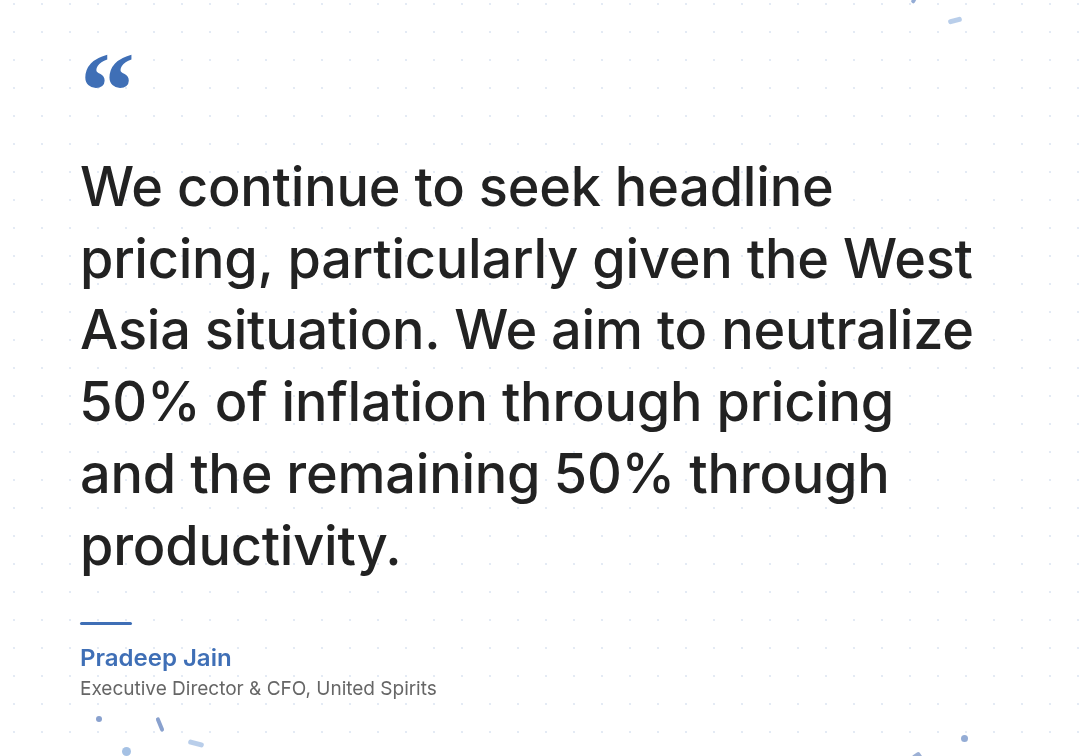

United Spirits faces a more manageable squeeze. Packaging makes up about a third of its costs, and the company expects a hit of 1.25-1.5% to gross margins. Their plan is to offset part of it through price hikes (especially in newly-liberalised states like Karnataka), and half through productivity improvements.

Radico, meanwhile, is the most insulated of the three. Around 90% of its power and fuel comes from captive biofuel, so it’s fairly independent of global energy price swings. It has seen a 15% spike in glass bottle costs, but is absorbing this by using smaller packs which use less glass. It is still guiding for an impressive 125 basis points of EBITDA margin expansion next year.

There’s a potential tailwind on the horizon too: the India-UK Free Trade Agreement, which is expected to slash import duties on Scotch whisky from 150% to 75%. USL is the most obvious beneficiary, since it would make its Scotch portfolio (which relies on imports from Scotland) significantly more competitive.

What’s next

The Indian alcobev story is playing out at two speeds. There’s a massive structural tailwind from premiumisation, and some state-level policies are actively encouraging it. But co-existing with it are prohibitive regulations in other states, plus the headwinds from geopolitical supply chain shocks.

Among the three, Radico has the most momentum, with a high premium mix, margin expansion, and a near-debt-free balance sheet. USL is the resilient franchise, also holding their own in the premiumization wave. UBL is the one under pressure — premium growth is real but it’s too small a slice, and the Middle East cost wall is enormous relative to its profitability.

Tidbits

The Central Board of the Reserve Bank of India approved a record surplus transfer of ₹2.87 lakh crore to the central government for 2025-26, aided by a sharp rise in income and a larger balance sheet.

Source: Hindu BusinessLineState-run Steel Authority of India Limited (SAIL) is working on an ambitious capital expenditure plan of more than ₹35,000 crore over the next two financial years, driven largely by capacity expansion projects at its IISCO, Bokaro and Bhilai steel plants.

Source: Business StandardThe Government of India announced an 8% stake sale in the PSU lender Central Bank of India via an offer for sale (OFS). The government may additionally exercise an oversubscription option to sell more shares depending on investor demand.

Source: LiveMint- This edition of the newsletter was written by Kashish and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

If you’re a woman who feels intimidated by the world of money, In Her Interest is meant for *you*.

Most women share a complicated relationship with money.

On one hand, women are expected to be exceptionally good with it. They manage household budgets, track expenses, stretch money, save for emergencies, and make a hundred tiny financial decisions every month.

When money conversations turn more formal, though; when they shift to investments, insurance, taxes, or business finances, they suddenly defer to someone else — a father, husband, brother, the family CA, or “the finance person” in the family.

To us, this weird duality seems to creep in because most women have never had a friendly, low-pressure place to learn their way around it.

That’s what In Her Interest, a Zerodha initiative, is trying to create. In Her Interest hosts small, in-person sessions where women can ask normal money questions without being judged, sold to, or drowned in jargon. The next few sessions cover finance for entrepreneurs in Gurugram, smart money management in Mumbai, investing basics in Pune, and the basics of mutual funds in Hyderabad. If you’re a woman who has been meaning to get a little more comfortable with money — or know someone who might — this is a fantastic place to start!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉