An inventory high before a pricing hangover

Oil companies brace for a terrible quarter

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The boom before the storm: Q4 at the oil marketing business

Cracks in the half-full glass of Indian dairy

The boom before the storm: Q4 at the oil marketing business

On May 13, HPCL reported its March quarter results. It was a record: the highest quarterly profit in the company’s history. IOCL reported its results five days later, on May 18, celebrating its strongest year ever: with record throughput, record sales, and profits nearly thrice as high as the year before. The very next day, on May 19, BPCL released their own results: these weren’t spectacular, but they were way better than expected, given a massive impairment charge the company had to book.

None of them sounded happy on their investor calls, though.

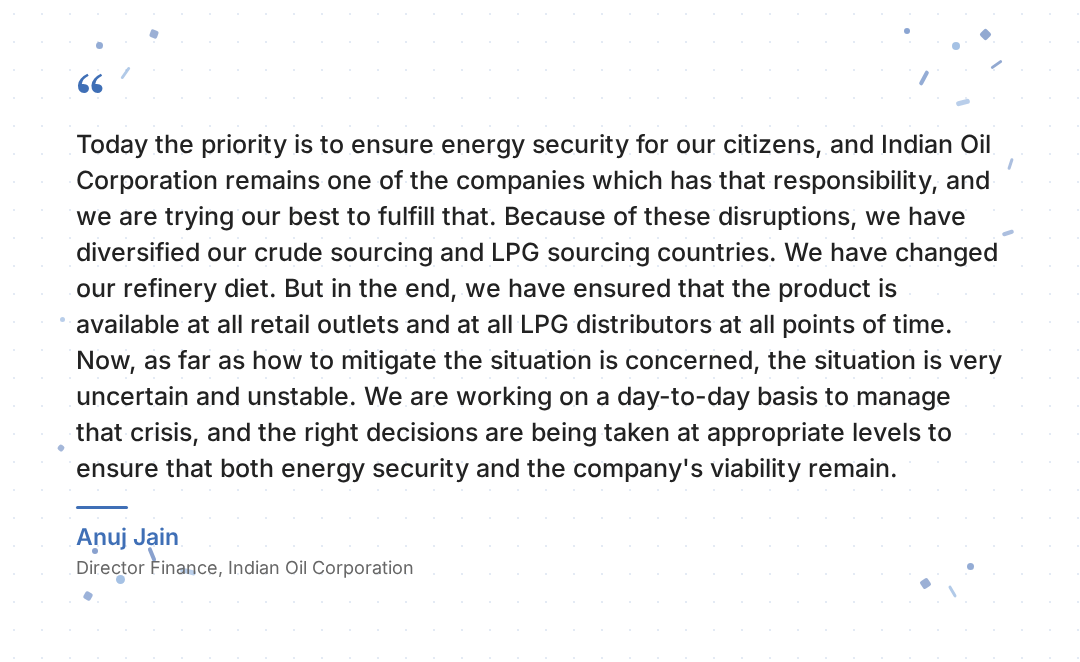

As they spoke about their March quarter results, the context for the following quarter had already been set. The Hormuz crisis and soaring oil prices were already wrecking their economics. Together, they were bleeding roughly ₹1,000 crores a day. The government hiked prices for the first time in four years, only to hike them again within the same week. But the losses wouldn’t stop.

These companies’ latest numbers, in other words, tell you very little about how they’re currently faring. But they do tell us where they were before, and how well they were placed when the shocks arrived.

The boom: An exceptional quarter

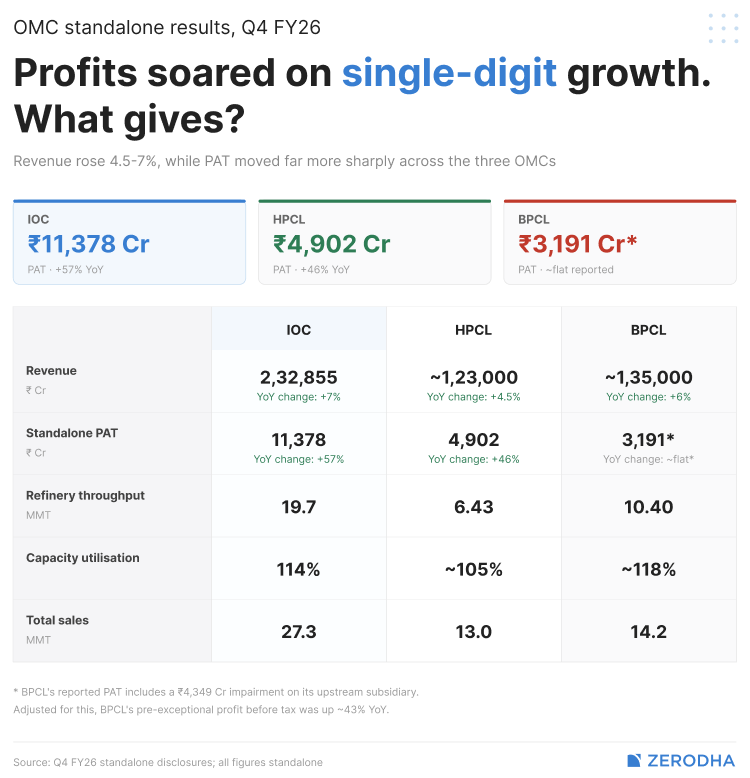

The three companies we’re covering — IOCL, HPCL and BPCL — all saw their revenues grow in the mid-single digits. They had steady throughputs and steady volumes. And yet, their margins had soared, bringing in historic profits.

The largest of the three, IOCL, saw its quarterly standalone revenues grow 7% from a year earlier, to cross ₹2,33,000 crore. It ran over full capacity — at nearly 114% — processing 19.7 MMT of crude. Its sales were up modestly for the quarter too, at 27.3 MMT. None of this pointed to its wild surge in profits, though. At nearly ₹11,400 crore standalone, they had grown by 57% over the same quarter last year.

Something similar happened at HPCL, the smallest of the three. Its standalone revenues were up about 4.5%, to around ₹1,23,000 crore. Its refineries pushed through 6.4 MMT of crude, roughly the same as last year. Its sales edged up just 2%, to 13 MMT. And yet, its standalone profit — at about ₹4,900 crore, was up 46% over the same quarter one year ago. This was, in fact, the highest the company has ever posted in a single quarter.

BPCL, the markets knew, was supposed to have a bad quarter. The company was taking a large accounting hit — it had to write-down almost ₹4,350 crore on an overseas oil exploration bet, after a deepwater project in Brazil was delayed by almost two years. That was always going to kill its profits.

Without that, though, its story too was typical for the industry. Its standalone revenues were up about 6%, to roughly ₹1,35,000 crore. Its refineries were pushing through 10.4 MMT of crude, while its sales grew about 4%, to 14.2 MMT. Yet its pre-exceptional profit — before considering its huge investment write-down — was up about 43% over the same quarter a year ago. BPCL also ended the quarter with the strongest balance sheet of the three: with its standalone more than halving in a year, to below ₹10,500 crore, against investments worth over ₹18,000 crore.

These were spectacular results for a mature sector. But something was beginning to crack.

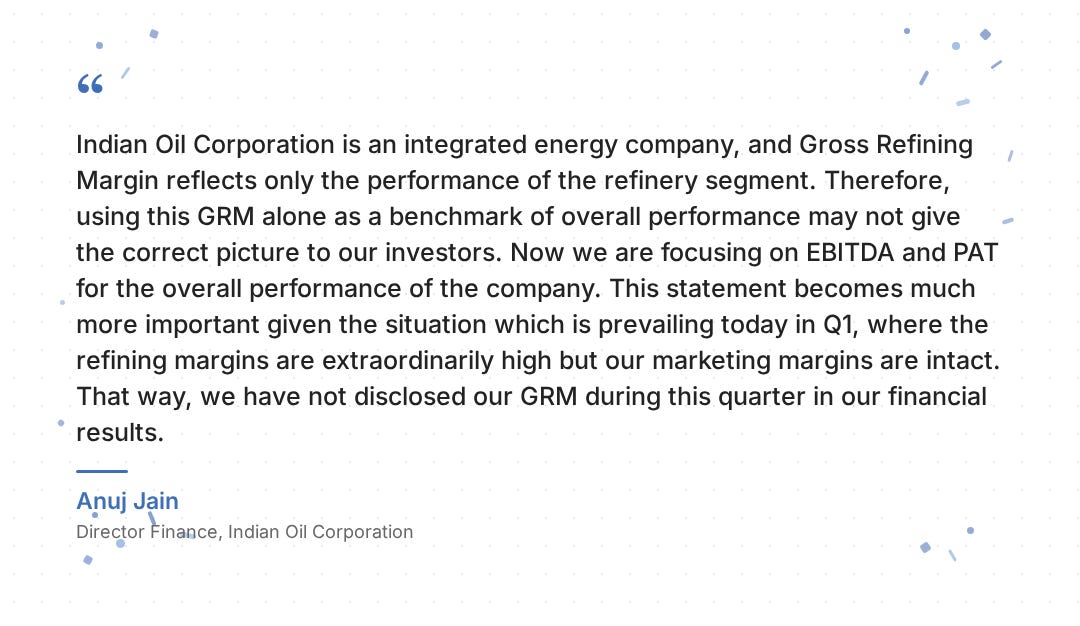

There were a few hints of that in the quarter results alone. For one, IOCL — the largest — chose not to report a number that analysts tracking these companies always looked for: its gross refining margin. As its management explained, it simply didn’t make sense in an environment like this. Their refining margins could look extraordinarily high, even if the company was losing money.

There was another hint, though: those massive profits, themselves, were ominous.

Why Q4 was the last good quarter

Two-thirds of the way into the March quarter, the Middle East erupted in conflict. Crude prices surged. As IOCL’s management said, the Indian crude basket rose from about $64 per barrel to $83 over the quarter — a 30% jump in less than three months.

But oil companies don’t buy crude and refine it the same day. They procure crude weeks-to-months in advance, store it, and run it through their refineries over many weeks.

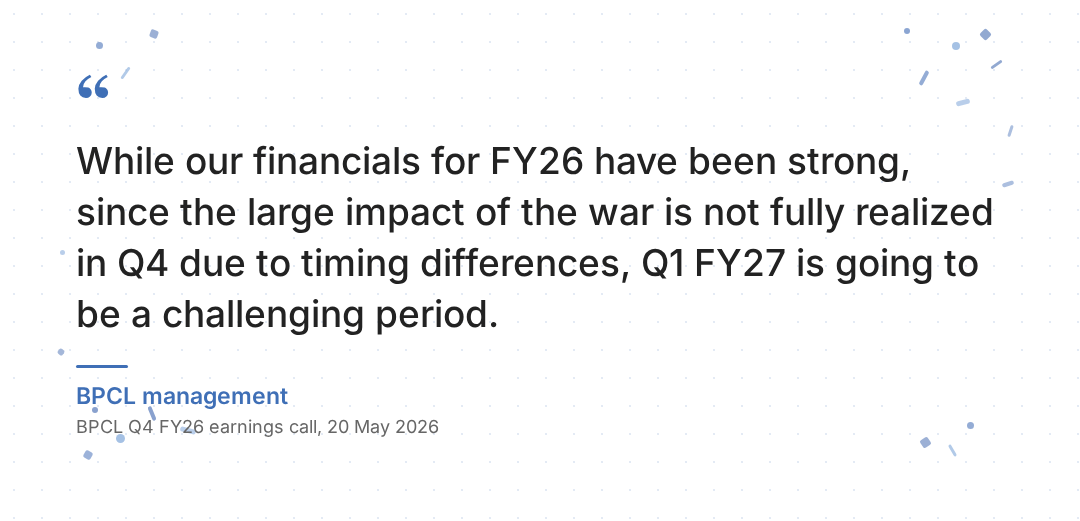

In the March quarter, most of the petroleum products that IOC, BPCL and HPCL sold were made from crude they purchased before the crisis. That was a very different time, with very different economics. All three refiners’ margins had risen all through FY 2026. By the time the March quarter rolled around, all three were structurally in a better place than they had been in the same quarter a year before.

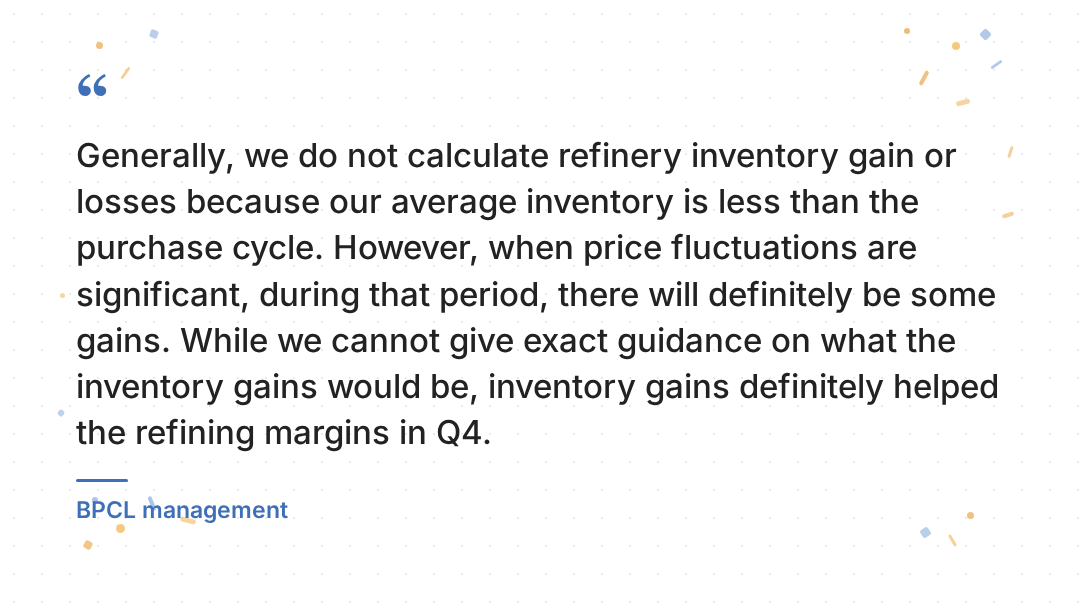

Once the war broke out, for a few brief weeks, these companies enjoyed “inventory effects.” They priced their raw crude at the pre-crisis rates they bought it for. But once it came out of their refineries, their inventories of finished products — of the refined petrol, diesel and other fuels they planned to sell — were all valued at post-crisis international benchmarks. Notionally, this looked like a huge profit for their refining arm.

Their cheap crude inventories would empty out over the course of the quarter, of course. But the quarters’ numbers by themselves were insulated from the war.

But that would only last for so long. As the war dragged on, the cushion would deflate, the inventory gains would vanish, their costs would climb, and those profits would come tumbling down.

But there’s another side to this coin: these companies’ refining arms might have made paper profits, but to the books of their marketing arm — which are separate — those over-priced finished product inventories become the input cost. Their revenues, meanwhile, are bound to the government’s price ceiling. Right now, that ceiling is well below what their inventories are priced at. Their “inventory effects” will soon bite the other way. Today’s paper profits are losses for tomorrow.

That, however, is a story for another quarter.

The first cracks

Where will the crisis show up, when it does?

The first big crack will come through cooking gas.

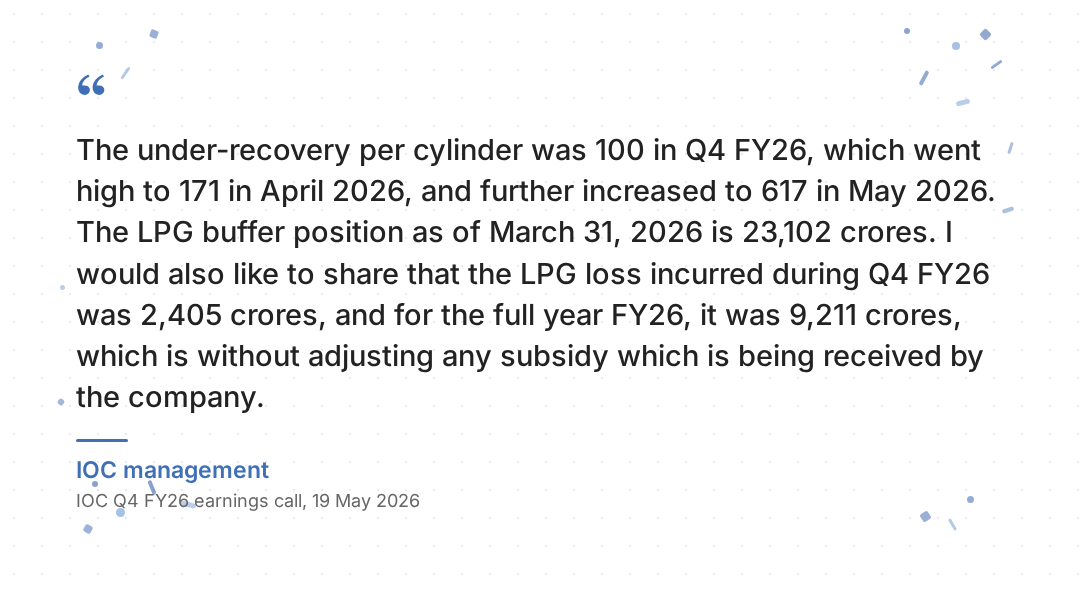

OMCs usually make a small loss on every gas cylinder they sell. Through the March quarter, for instance, IOCL lost ₹100 on every cylinder they sold. That loss would soon start climbing, however. By April, it was losing ₹171 per cylinder. By May, it was losing ₹617. The others, too, saw a similar escalation. In two months, these companies’ per-cylinder losses will go up six- to eight-fold.

This was only to be expected. After all, the entire gas supply chain had blown up.

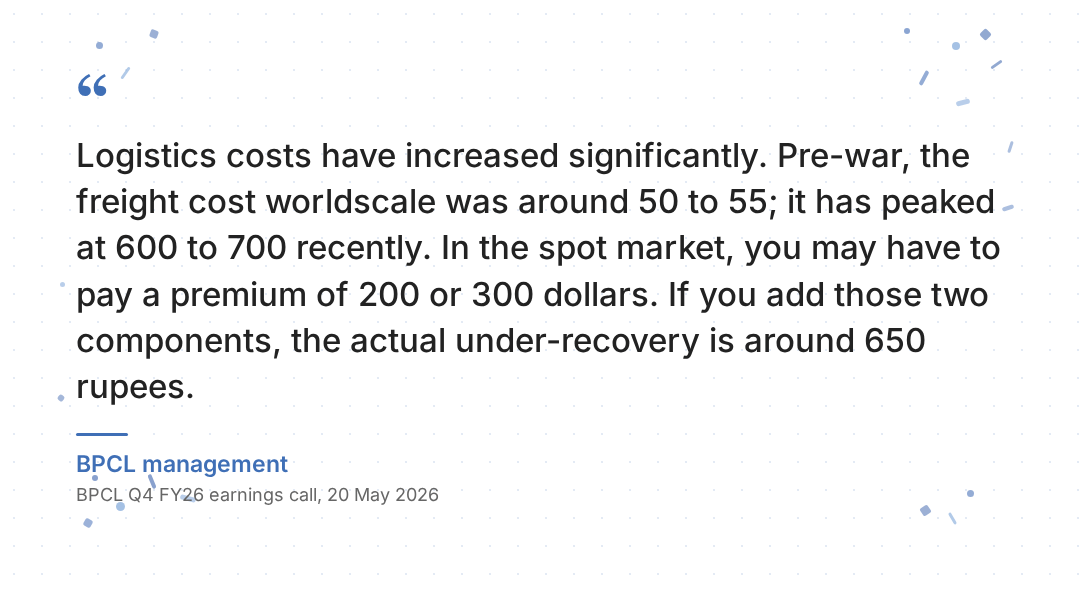

OMCs used to secure their LPG based on long-term contracts from the Persian Gulf, on prices linked to Saudi rates. That LPG would reach India after going through the Strait of Hormuz. Once that route was choked, though, they had to rush to find alternatives. They were now scrambling to find gas in spot markets from across the world — the United States, Indonesia, Nigeria, Angola — where prices had already been bid up by $200-300.

Worse still, they were getting this gas from further away, often spending more on transport. As BPCL’s management noted, for instance, their freight costs jumped roughly twelve-fold.

Ideally, the government compensates these companies for the massive losses they had taken. Well before the war broke out, it had already announced a sector-wide compensation scheme earlier in the year, paying OMCs thousands of crores in monthly installments to make up for their LPG losses. That scheme, however, was designed for a world where they lost ₹100 per cylinder. But things were growing far worse.

OMCs usually carry their per-cylinder losses on their books as a “negative buffer,” expecting that the government will eventually make them whole. In effect, those buffers tell you what the government owes. Those buffers were large before the war. They started climbing faster in the March quarter. By the end of March, for instance, IOCL was already carrying ₹23,102 crore in accumulated LPG losses.

As the crisis gets worse, those buffers are likely to skyrocket before the government can pay them down.

The coming storm

At least LPG comes with a hope of compensation, however. Petrol and diesel, on the other hand, have no compensation scheme at all.

In theory, the Indian government doesn’t regulate the price of fuel. Companies are free to set the pump price as they like. They can pass elevated prices through to the public and protect their books. In practice, though, the government is a majority shareholder in all three companies. Any price hike needs political sanction.

Since 2022, the government had kept retail petrol and diesel prices frozen, even as global crude prices were swinging wildly. Once the crisis hit, however, that was no longer feasible. The losses were soaring too quickly.

At first, the government tried absorbing the hit itself, giving OMCs some breathing room. In the last week of the March quarter, it cut excise duty on petrol by ₹10 per litre, bringing it from ₹13 to ₹3, and cut diesel excise to zero. This would give OMCs a higher share of what consumers paid at the pump. At the same time, however, it started adding windfall taxes to fuel exports, capping any upside these companies would see in higher international prices. The crude oil coming into India, it signalled, was meant for Indians.

But OMC losses kept mounting. On May 15, for the first time in four years, OMCs finally raised the prices of petrol and diesel by ₹3 a litre. The hike didn’t go far enough, however. Four days later, they added a second, smaller hike of about 90 paise.

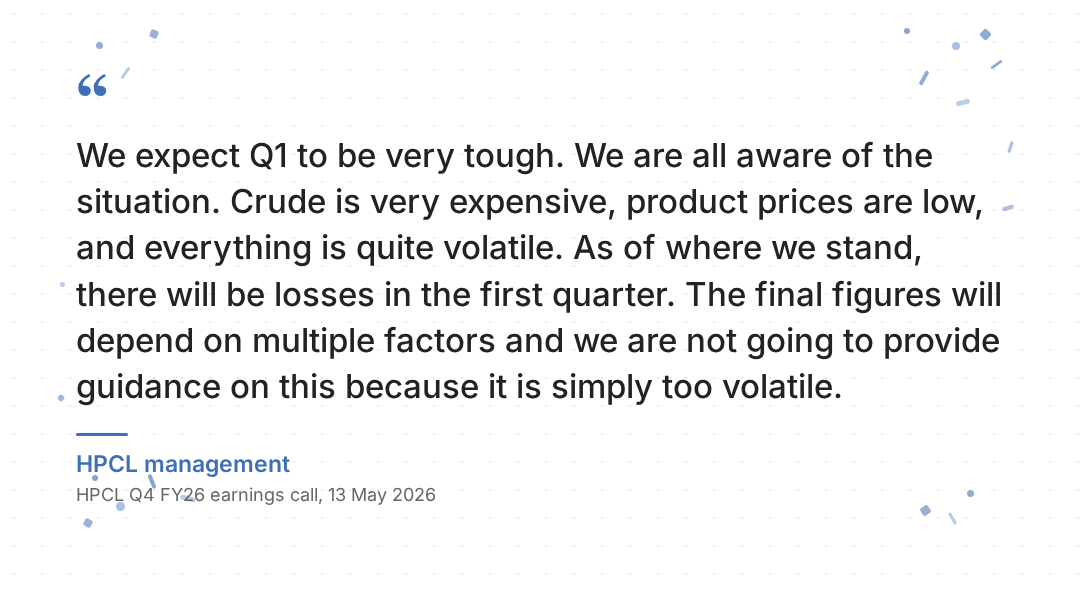

These hikes lower the pain, but only marginally. According to CRISIL, even after these hikes, OMCs are losing roughly ₹10 per litre on petrol and ₹13 on diesel. These hikes, if anything, are just the beginning. To some analysts, if the stand-off continues and oil prices stay above $100, you should expect hikes as high as ₹20 per litre if these companies are to stop losing money.

For now, the crisis has no end in sight.

What comes next

That’s the ugly aftermath of a quarter that, on paper, looked incredible. These companies may have made record profits, but as Petroleum Minister Hardeep Puri said, the losses these companies could see in a single quarter might wipe out the profit they made over an entire year.

The path ahead, all three companies have signalled, will be painful.

In retrospect, this March quarter may look like a peak. After posting record years, three months from now, these companies may well report some of their worst quarters in a decade.

Cracks in the half-full glass of Indian dairy

We’ve covered the Indian dairy business a few times now. We broke down how the industry works when Milky Mist filed for its IPO. Then we looked at the Q2 FY26 results of the industry, where a weak monsoon season contributed to rising milk costs, while a structural shift to value-added dairy products was also underway.

With the last quarter of the year, the picture has become more tainted.

Revenue grew almost everywhere, but profitability collapsed for some, while barely holding up for others. A brutal milk shortage, a geopolitical crisis halfway across the world, and the relentless push into higher-value products, all collided in the same quarter.

We’re looking at four companies this time — Hatsun Agro, Heritage Foods, Dodla Dairy, and Parag Milk Foods — to see where the Indian dairy business is heading.

The numbers

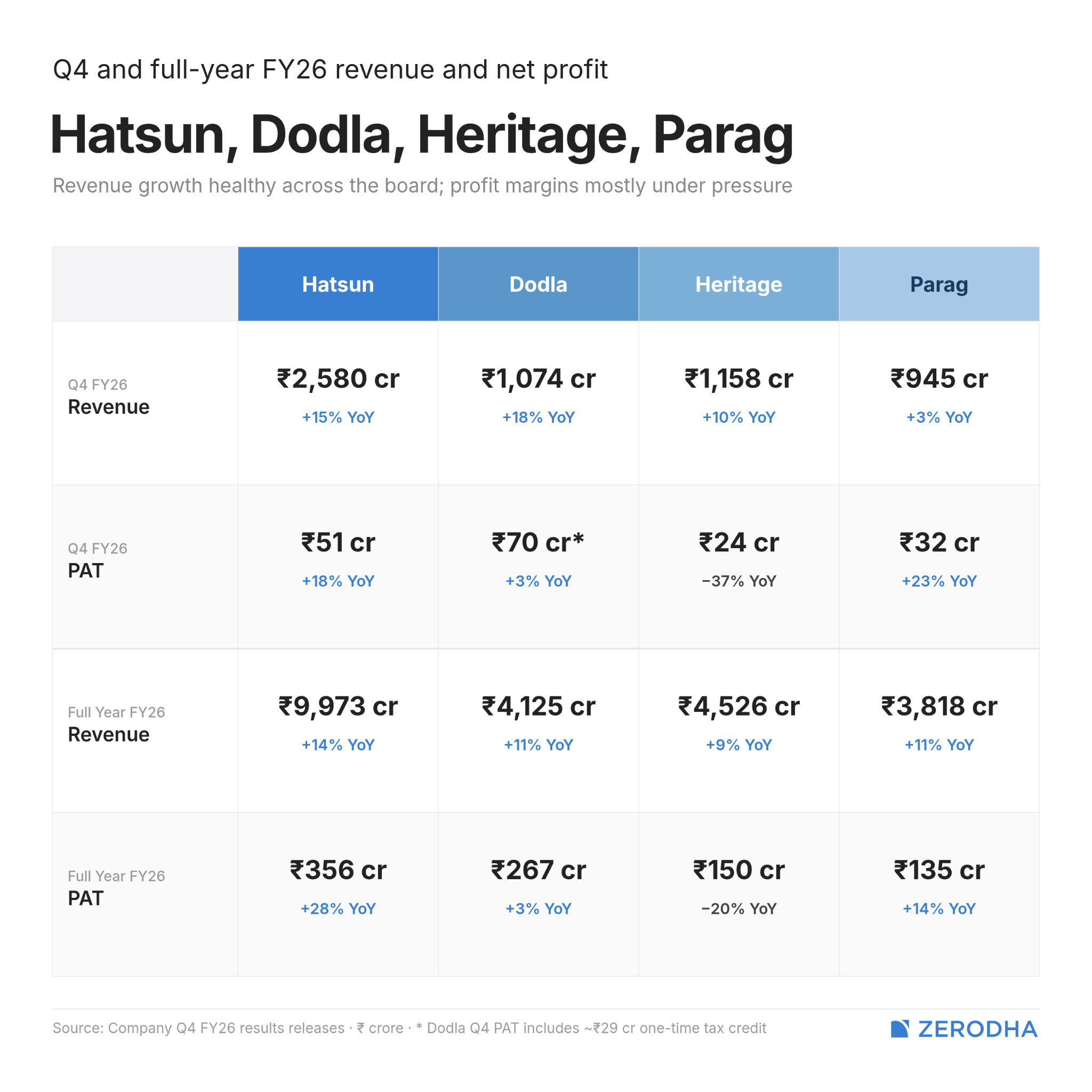

Hatsun Agro, India’s largest publicly-listed dairy company, continues to be the most consistent performer. The total Q4 revenue came in at ₹2,580 crore, up about 15% from a year ago, with net profit rising 18% to ₹51 crore. For the full year, FY26 revenue grew by ~14% to ₹9,973 crore, with net profit jumping 28% to ₹356 crore.

Meanwhile, Dodla Dairy posted its highest-ever quarterly revenue at ₹1,074 crore, an 18% jump — also the fastest top-line growth in this group. The headline PAT is nearly ₹70 crore — hardly 3% higher than the same time last year, while also including a one-time tax credit of about ₹29 crore. For the full year, revenue grew 11% to ₹4,125 crore, but net profit barely budged at ₹267 crore.

Heritage Foods grew revenue 10% to ~₹1,158 crore, but everything below the top line fell apart. EBITDA dropped 35% to ₹52 crore, with the margin compressing from 7.6% to 4.5%. Net profit crashed 37% to ₹24 crore. For the full year, revenue rose 9% to ₹4,526 crore, but PAT fell 20% to ₹150 crore.

For Parag Milk Foods, revenue grew just 3% y-o-y to ₹945 crore — the slowest in the group — but net profit surged 23% to ₹32 crore, while EBITDA margins have largely remained stable around 8.3% compared to Q4 FY25. For the full year, revenue grew by 11% year-on-year to ₹3,818 crore, with net profit rising 14% to ₹135 crore. By revenue, this was their best year ever.

The pattern is mostly clear: everyone grew revenue, but operational profit margins either fell, or just remained stagnant. There was little question of margin expansion in relative terms, even if the absolute numbers grew.

The milk shortage

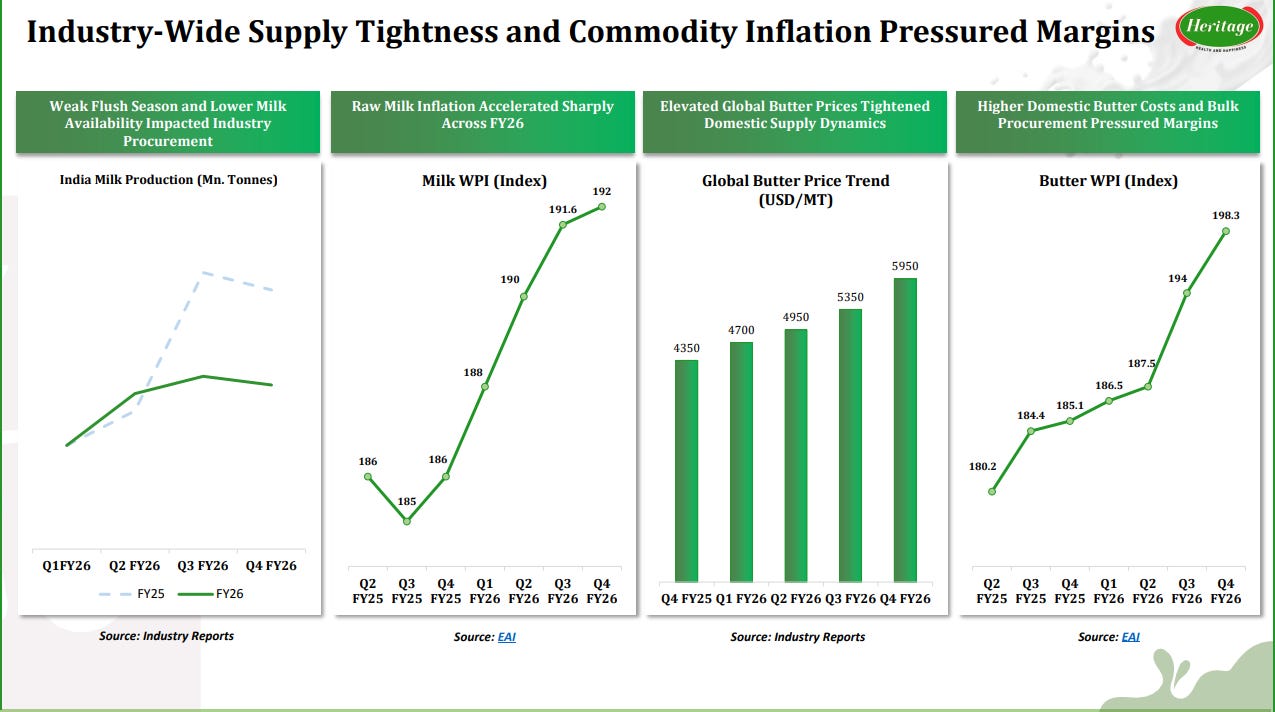

The biggest reason for this pattern is one that has haunted most of FY26: a shortage of raw milk.

See, India’s dairy industry has a natural rhythm. Every year, the cooler months, which are roughly October through February, bring what’s called the “flush season.” Cattle produce more milk when temperatures drop and green fodder is abundant. Dairy companies use this window to build up inventory, stockpile butter, and lock in lower procurement prices. The flush is the foundation on which the rest of the year is built.

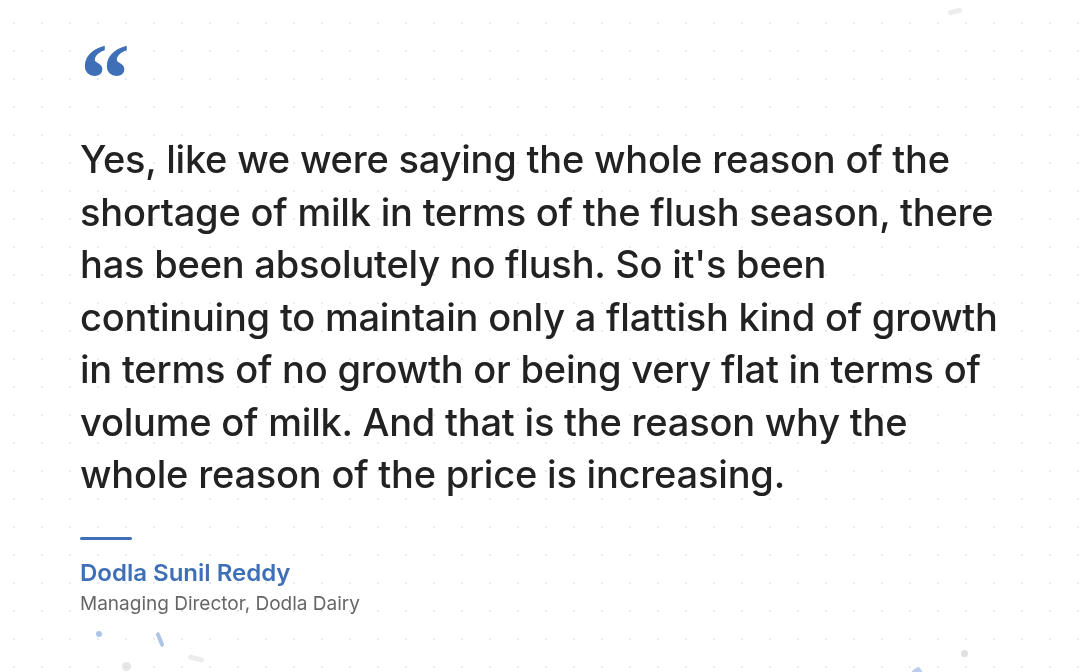

But this year, there was virtually no flush. Dodla’s management even said so last quarter.

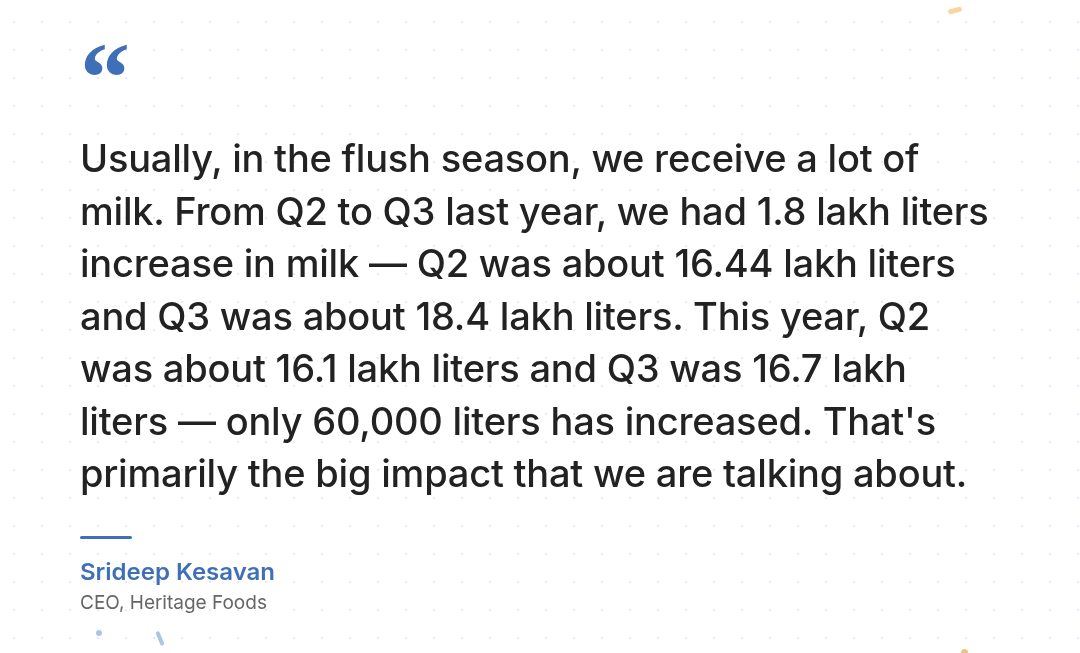

Erratic and excessive rainfall across several key states, particularly Andhra Pradesh and Telangana, stressed cattle so badly that milk yields dropped. Last quarter, Heritage even quantified this: between Q2 and Q3 of an average year, a normal flush previously brought an incremental 2 lakh litres per day in procurement. But this year, that same increase was a mere 60,000 litres.

The shortage created a vicious cycle, one we highlighted in our story on the Q2 results. Earlier in the year, companies exported domestic milk fat to capture high global prices, thereby depleting butter reserves. To compensate, companies had to buy even more liquid milk just to extract cream, further squeezing an already tight market, and leading to a surge in the average milk procurement prices for everyone.

For instance, Parag’s costs rose up by 15% year-on-year to ₹42 per litre, while their volume growth remained weak — even declining in core categories. Meanwhile, Dodla’s prices rose up by ~10% to ₹41 per litre, and Heritage paid 8% more, moving up to ~₹47 per litre.

This is also the biggest driver behind the recent price hikes undertaken by Amul and Mother Dairy. That’s never an easy move in a country where milk prices are politically explosive. Private companies face the same pressure: they can’t pass on the full cost to consumers without risking a volume hit.

So, how did each company navigate this?

Well, some things were common across the board. There was unwillingness to have consumers bear the full brunt of a price hike, for fear of losing market share. Everyone also increased their marketing investments. Most importantly, they doubled down on their ongoing shift towards selling more value-added products (VAP), which we will get into in detail soon.

Yet, there were certain divergences in strategies, which also led to some variation in outcomes.

For one, somehow, Dodla posted its highest-ever quarterly milk sales volume in the midst of this. How does one achieve that during a milk shortage?

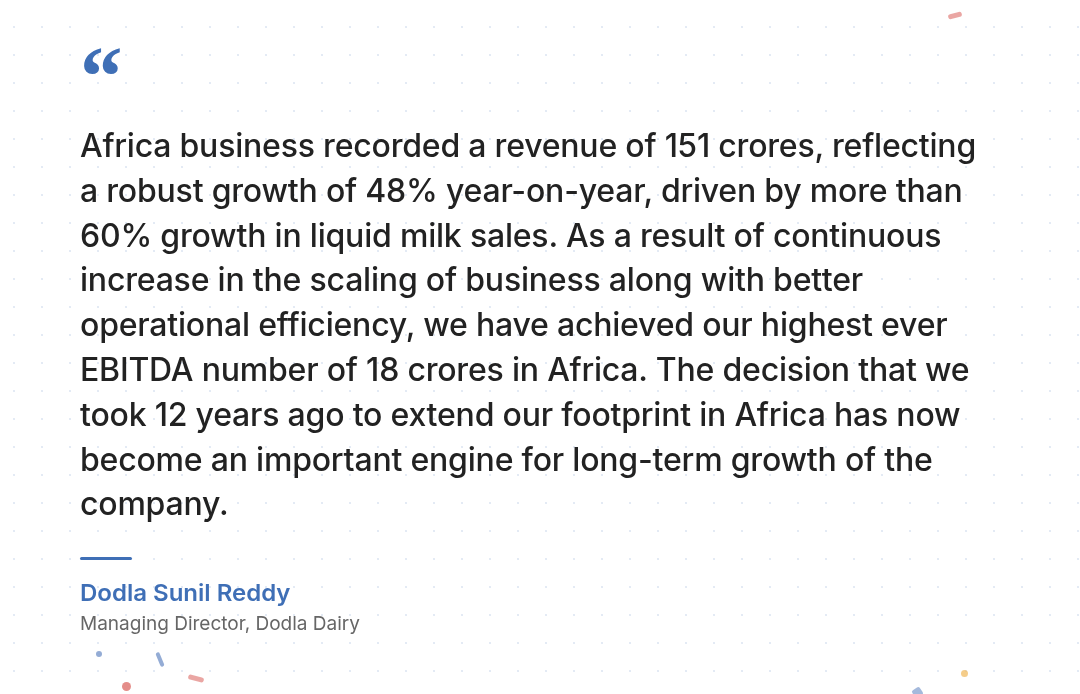

Two major factors made this possible. For one, over the year, they built up buffer inventory when supplies were better. Secondly, they diversified themselves across India, including Tamil Nadu, Karnataka, and Maharashtra. On that note, they also acquired OSAM Dairy, which plugged them into Eastern India’s procurement network. And they didn’t just remain within India’s borders: their Africa business grew by 48% year-on-year.

However, Dodla’s operating margins didn’t escape this crisis, falling steeply from 9.2% in Q4 FY25 to 5% this quarter.

Heritage absorbed the pain more directly. Their milk procurement volumes fell 7% to 16.38 lakh litres per day. To protect farmer loyalty during the crunch, Heritage kept procurement prices high, while passing only a partial increase to consumers. The average selling price rose just 4%, nowhere near enough to offset the 8% jump in procurement costs. Of course, that led to a similar margin collapse.

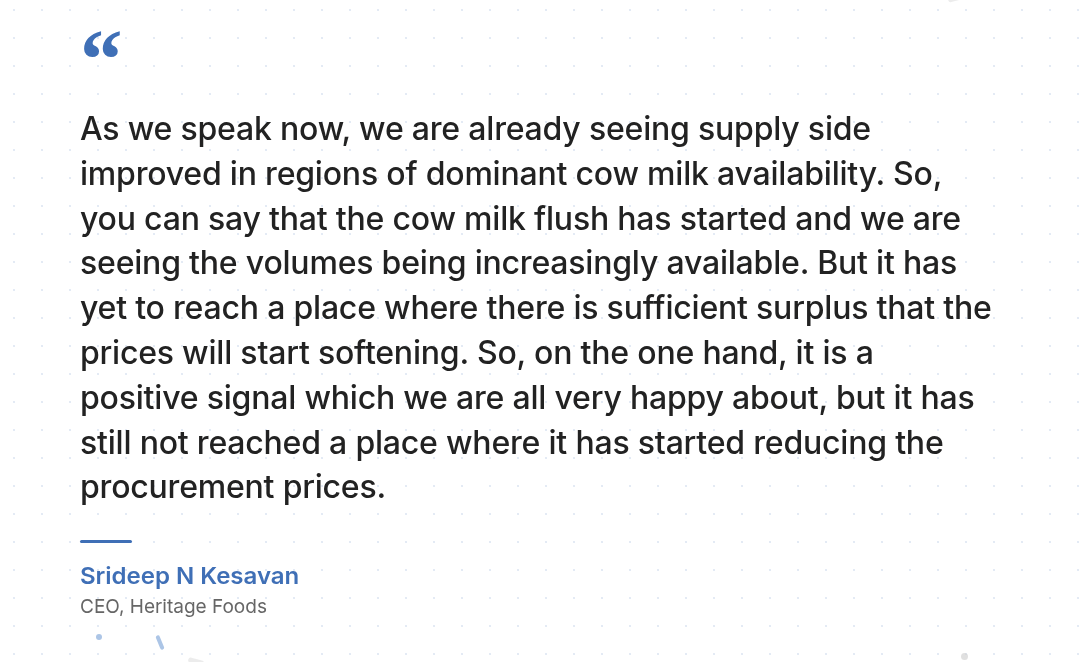

The companies expect some relief in the near future, though. Heritage pointed to the start of a potential “cow flush“ already underway in some places. With milk prices this high, farming is profitable enough to incentivise higher production, which should gradually ease procurement costs. Dodla observed something similar as well.

But two massive risks loom. To begin with, as we’ve covered in one of our recent stories, the world is expecting a Super El Niño, which could suggest an intense summer that could dry up fodder and water that cows need. On top of that, there’s the situation at the Strait of Hormuz, which we’ll eventually get into as well.

Value addition

Part of the answer to the milk shortage problem lies in the long-term industry shift away from simple, liquid milk to value-added products (VAP). Selling curd, paneer, ice cream, or whey protein offers higher margins and more pricing flexibility.

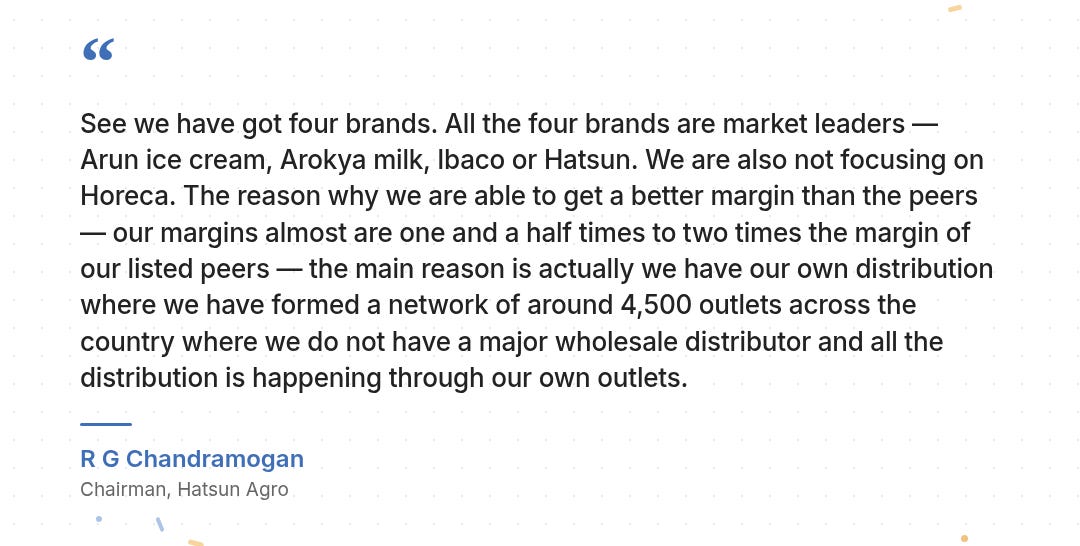

Hatsun leads here by a wide margin. Nearly half its revenue comes from VAP, anchored by the Arun Ice Creams brand, which is why it earns EBITDA margins roughly double what Heritage or Dodla manage.

For Heritage and Dodla, the mainstay is curd, accounting for about 70% of each company’s value-added revenue. Heritage pushed its overall VAP contribution to 41.9% of quarterly revenue (including consumer fats), up from 36.8% a year ago, driven primarily by growth in paneer and ice cream. Heritage is betting big on ice cream in particular with a new plant at Hyderabad.

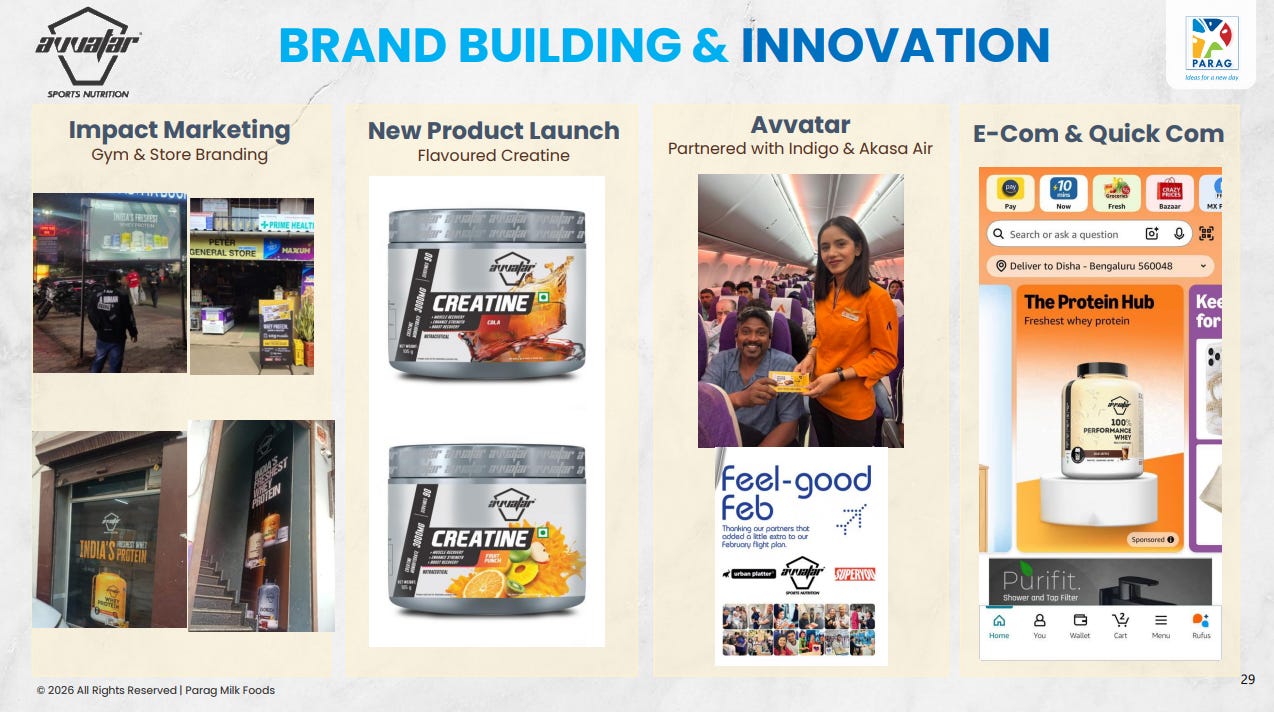

But the most interesting VAP move came from Parag, and it’s about whey protein.

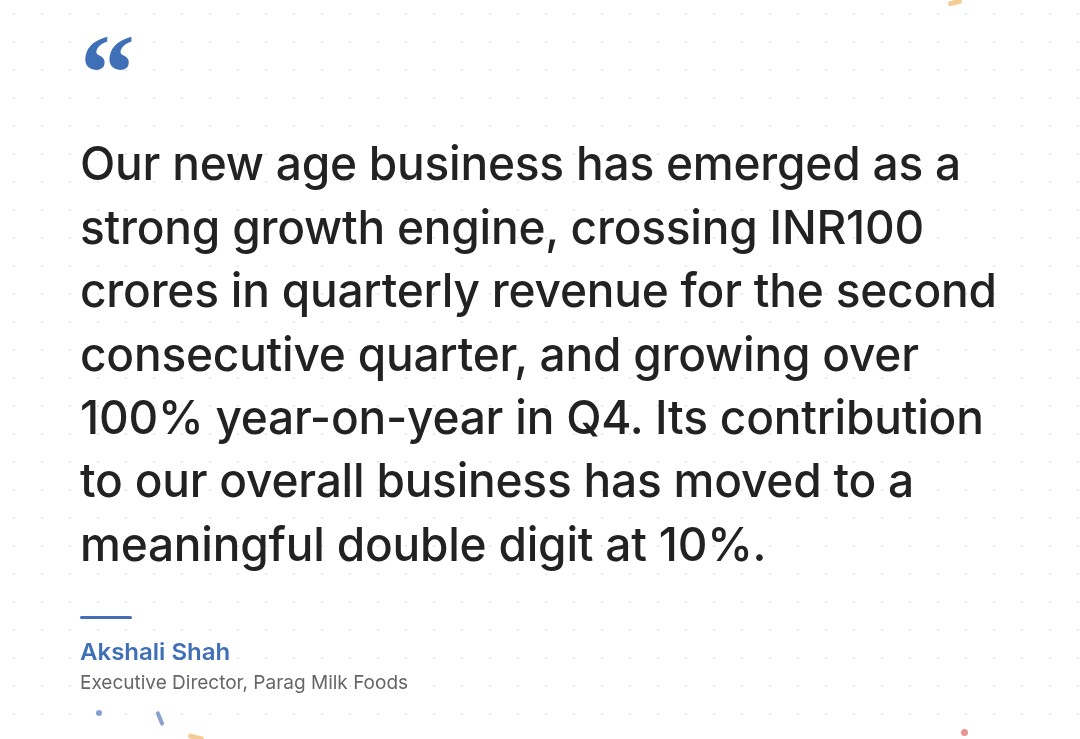

You see, Parag runs Avvatar, a whey protein brand. Since whey is a byproduct of cheese production — and Parag holds a 35% market share in cheese — they have a built-in raw material pipeline that competitors can’t easily replicate. The “New Age” segment, which includes Avvatar and their premium milk brand, grew more than 100% year-on-year this quarter, and now makes up over 10% of total turnover.

In fact, this is also why Parag was the only company to expand profitability this quarter despite modest revenue and volume growth.

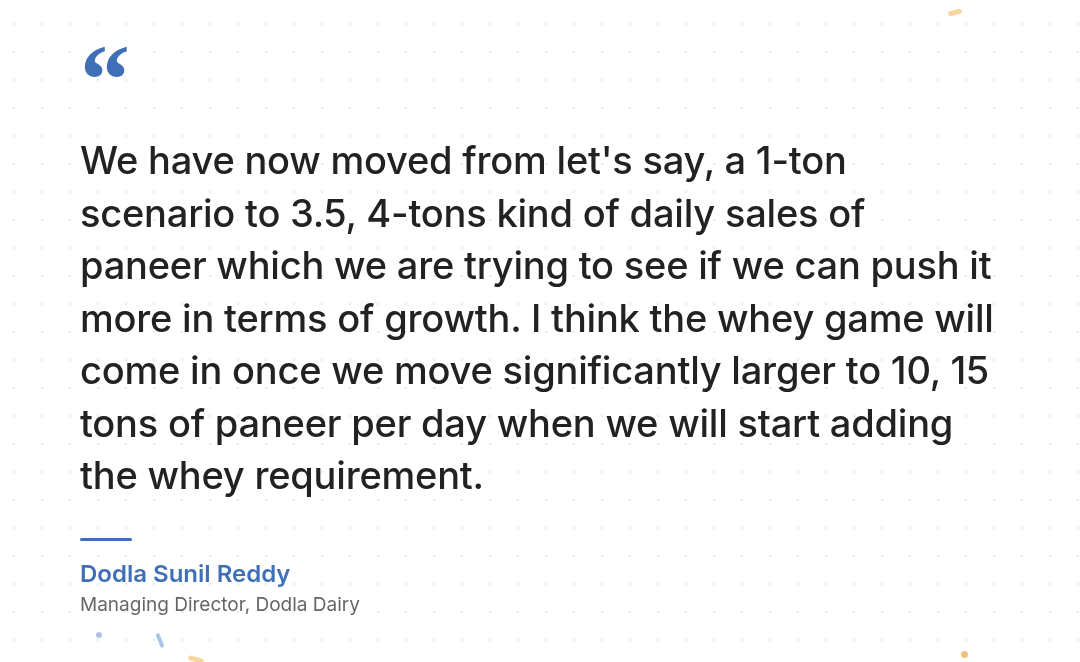

Its competitors, meanwhile, seem to be playing catch-up. Heritage launched a whey-based drink called GlucoShakti in Q1 of FY26, but haven’t yet disclosed a full portfolio strategy like Parag. As of last quarter, Dodla is yet to have enough paneer production at scale which can help generate sufficient whey.

Within VAP, the other big shift is the retreat from B2B bulk commodity sales. Selling butter or skimmed milk powder in bulk to institutional buyers is low-margin work that doesn’t build a brand. And every company unilaterally followed this strategy, instead shifting resources to selling VAP directly to customers.

Dodla, for instance, took this to its logical extreme: its bulk sales went from ₹38.4 crore in Q4 FY25 to literally zero this quarter. They’d rather use the butter internally for their own consumer products than sell it at commodity prices. Heritage saw a 70% decline in bulk fat revenue for the year. Hatsun heavily credits its lack of dependence on middlemen, wholesalers and institutions like hotels and restaurants as to why it makes better margins on its ice-cream:

The Strait of Hormuz effect

At last, we have the crisis at the Strait of Hormuz.

The most direct hit of the crisis is on packaging. Every litre of milk comes in a plastic pouch, and plastic is a petroleum derivative. Dodla, for instance, reported a 30% surge in packaging costs. Parag flagged the same, and raised the prices of their milk pouches accordingly.

Hatsun faces an additional problem. Ice-cream cones require gas to manufacture, and gas supply has, of course, become erratic due to the crisis. But what helps Hatsun is that it also manufactures some of its own polythene films in-house, which partially insulates it.

Then, there’s the livestock feed angle. Dodla and Heritage both operate subsidiaries that manufacture cattle feed that dairy farmers buy to feed to their cows. These serve as loyalty loops, keeping farmers tied to their procurement networks. But cattle feed production depends on the fertilizer urea, which is made primarily from natural gas. And now, gas has become harder to come by.

This doesn’t just raise feed costs, though. It also threatens crop yields, which rely on fertilizers. That, in turn, further affects fodder supply for cattle. Dodla’s management specifically cited the uncertain “impact on agriculture from urea production” as a reason for cautious margin guidance.

In Dodla’s earnings call, an analyst also pointed out a small irony: if crop failure pushes farmers away from agriculture, they often shift resources toward livestock, potentially improving dairy procurement. Management agreed with the theory but wasn’t willing to bet on it.

The crisis has also stalled international expansion. Parag, for instance, had plans to build a depot in the Middle East, but now those plans are on hold indefinitely. Dodla’s Africa business faces higher freight costs that make planning difficult.

Conclusion

The next few quarters will mostly be shaped by forces that are hard to predict and impossible to control.

El Niño threatens to undo early signs of a supply recovery. The Strait of Hormuz crisis is keeping packaging, feed, and freight costs elevated. And every company is simultaneously pouring money into brand-building, all while margins are under pressure.

The most controllable variable is the shift toward value-added products. The hope is that the bet will, over time, create enough margin cushion to weather cycles like this one. Of course, within VAP, certain products (like protein) are growing much, much faster than others. So the specific VAP strategies also matter significantly in determining who can escape relatively unscathed when the next shock hits.

Tidbits

[1] Govt clears ₹5,500 crore floating solar + battery storage scheme

The Finance Ministry has approved a ₹5,500 crore scheme to support floating solar projects integrated with battery storage systems. The plan aims to help states expand renewable capacity while improving grid reliability through storage-backed clean energy. The proposal now awaits final Cabinet approval.

Source: PowerLine

[2] PFC’s 30-year NPCIL loan may reshape nuclear financing

A ₹26,000 crore, 30-year loan from PFC to NPCIL is emerging as a benchmark for financing nuclear power projects in India. Policymakers and industry stakeholders say long-tenure loans are essential because nuclear plants involve very high costs and long construction timelines.

Source: BusinessLine

[3] NCDEX launches India’s first weather futures contract

NCDEX will launch RAINMUMBAI, India’s first SEBI-approved weather derivatives contract, on May 29. The product will help sectors like farming, construction and power utilities hedge against unpredictable rainfall and monsoon risks using Mumbai rainfall data.

Source:The Hindu

- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

If you’re a woman who feels intimidated by the world of money, In Her Interest is meant for *you*.

Most women share a complicated relationship with money.

On one hand, women are expected to be exceptionally good with it. They manage household budgets, track expenses, stretch money, save for emergencies, and make a hundred tiny financial decisions every month.

When money conversations turn more formal, though; when they shift to investments, insurance, taxes, or business finances, they suddenly defer to someone else — a father, husband, brother, the family CA, or “the finance person” in the family.

To us, this weird duality seems to creep in because most women have never had a friendly, low-pressure place to learn their way around it.

That’s what In Her Interest, a Zerodha initiative, is trying to create. In Her Interest hosts small, in-person sessions where women can ask normal money questions without being judged, sold to, or drowned in jargon. The next few sessions cover finance for entrepreneurs in Gurugram, smart money management in Mumbai, investing basics in Pune, and the basics of mutual funds in Hyderabad. If you’re a woman who has been meaning to get a little more comfortable with money — or know someone who might — this is a fantastic place to start!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thank you for the extensive coverage of Q4 numbers across different industrial sectors.

Great article as always. One note: add the shared PAT numbers of the four companies. Parag's 135Cr number is overstated by ~24Cr because their tax rate is 11% for FY26, compared with 27% for the others. They carry forward the ~532Cr loss in 2022.