Amazon goes for the quick commerce pie

Plus: a cursory look at all the recent regulatory changes to Indian banking and finance

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Amazon goes for the quick commerce pie

A sweep of the recent regulatory changes in India’s financial system

Hi, folks. Today is our 500th episode of The Daily Brief, and it’s also been two years since we started Markets by Zerodha.

A big thank you to each one of you who’s reached out to us since we started — who watches us every single day. We’re very grateful that you find this valuable❤️

Amazon goes for the quick commerce pie

Flipkart and Amazon were the original heavyweights of the e-commerce business. If you asked us who would lead the quick commerce race, back in 2020, they would probably be the obvious answer. They had everything from seller relationships to warehouse networks. How could they not win?

Of course, that isn’t what happened. The industry was borne out of food deliveries, not e-commerce — when Swiggy started experimenting with deliveries under an hour. Then, out of nowhere, the upstart Zepto famously launched with its 10-minute delivery promise. Soon thereafter, the new avatar of the once-fledgling Grofers, Blinkit, took an unmistakable lead.

These are now the three industry champions. From whatever we’ve read and the people we’ve spoken to, it practically seems impossible to beat them at this point.

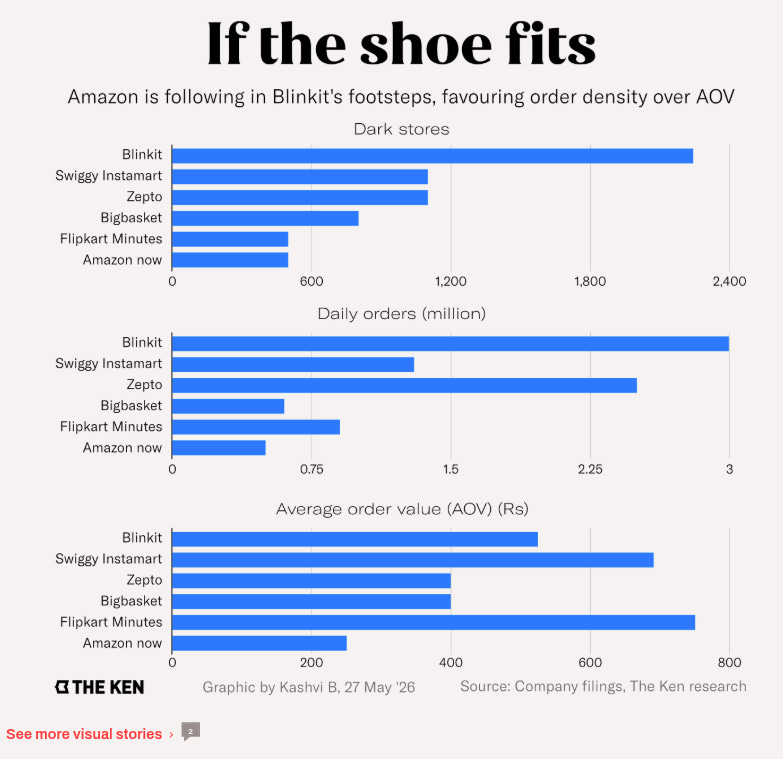

Still, given the sheer volume of action in the space, many new players have jumped into this race anyway: led by Amazon and Flipkart. In fact, that push seemed on the top of Amazon CEO Andy Jassy’s mind, when he visited India last month — when he announced that the company will take its quick commerce service, Amazon Now, from 100 cities to 300. That’s a massive commitment for a company that currently just has around 500 dark stores in India. Meanwhile, Flipkart’s quick commerce arm, Flipkart Minutes, went from basically nothing in mid-2024 to over 1,000 dark stores today.

That’s the story we’re telling today.

The industry was finally growing up

Before we get there, though, it helps to understand why today’s incumbents feel as confident as they do right now.

The three companies that dominate quick commerce today have spent years losing money on every single delivery. That spending is, in part, why they have the positions they enjoy — with Blinkit capturing almost half of all orders, Zepto a third, and Swiggy, just short of a fifth. This enormous spending blitz is all but baked into how the business works. Each delivery costs these companies roughly the same, whether a customer spends ₹200 or ₹5,000. These companies braved that cost anyway to get people to order. They kept discounting and offering free deliveries, even when the order value was well below what was worth it for them. That was the cost of creating this market.

But over the past year, the giants have started tightening their belts. They introduced platform fees and handling charges, raised the minimum order value you need before a delivery is free, and pulled back on discounts.

It paid off. Blinkit reported its first operating profit in the January-March 2026 quarter — ₹37 crore in adjusted EBITDA. Swiggy Instamart said it was on track to achieve “contribution margin breakeven” by the June 2026 quarter — a fancy way of saying it would stop losing money on each individual order, even if the overall business has large overhead costs it is yet to cover. Zepto finally found the confidence to file for an IPO. The quick commerce industry, for the first time, looks like it might be stabilising.

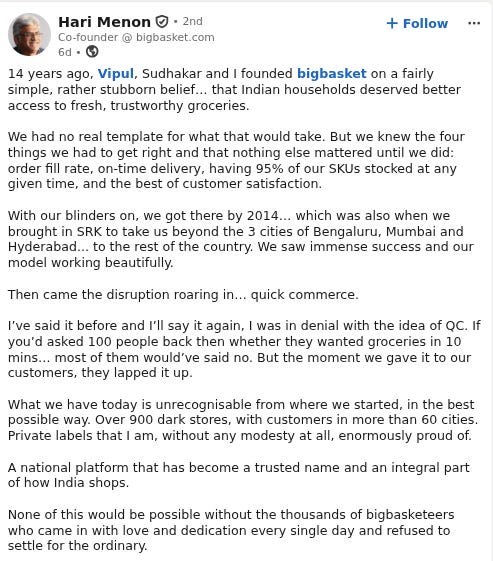

But the thing that captures this moment the best, perhaps, came from outside these companies. In June, Hari Menon — who built BigBasket from scratch in 2011 and grew it into Tata’s grocery platform with over 900 dark stores — stepped down as its CEO. In his farewell LinkedIn post, he wrote that he had been in denial about the idea of quick commerce for a long time. The idea of a ten minute delivery seemed absurd and unnecessary at first, and even consumers didn’t know this was something they would like. But they did.

BigBasket was, really, a pioneer of grocery delivery in India. It saw the entirety trajectory of the sector, from start to finish. This admission was, in a way, the ultimate sign of quick commerce’s ascent.

The person who replaced Menon, by the way, spent eleven years at Amazon before this.

Why Amazon is really here

Just as the incumbents are starting to mature, however, the old guard is making a brand-new bid for the business. Why? And why now?

There’s a cynical answer: that Amazon simply spotted a fast-growing market and decided to barge in. It’s probably not entirely wrong. But this explanation from Jignanshu Gor, a director at the brokerage Bernstein seems more interesting. As he told Moneycontrol: “till quick commerce was largely focused on groceries, Amazon India’s core e-commerce business was not particularly affected. But now that most players are selling tens of thousands of SKUs across categories, the threat to Amazon’s broader e-commerce business in India is much larger.“

In other words, the old guard didn’t step into quick commerce’s turf. It was quick commerce that began eating up their market.

Quick commerce started out as an online version of a regular kirana store: basic groceries, delivered in ten minutes. If you were baking a cake late at night, and suddenly needed eggs at 11pm, you opened Blinkit.

But then, the category kept expanding. Blinkit’s product range in Delhi NCR, for instance, went from 35,000-40,000 items a year ago to 80,000 today. From a kirana store, it practically turned into a huge on-demand mall. You can now get everything from electronics, to furniture, to fashion in minutes. As they grew, quick commerce stopped being a grocery business, turning into an e-commerce business that was a hundred times faster. Quick commerce now accounts for 20% of all e-commerce in India, and it’s growing at 50% a year.

Premium urban customers who once bought everything on Amazon slowly shifted their household spending to Blinkit or Zepto. Amazon Now is essentially an attempt to win them back.

This isn’t their first attempt

Interestingly, both Amazon and Flipkart have tried fast delivery in India before. Neither could make it work.

Amazon briefly ran Amazon Food, a restaurant delivery business. It shut the service down in December 2022, after spending two years, and on-boarding about 3,000 restaurant partners including McDonald’s and Domino’s. Never, in that time, was it close to competing with Zomato and Swiggy. Flipkart tried something similar in the past, but it never quite worked.

That said, those were different businesses. Amazon Food was after restaurant delivery, which is a completely different operating problem. Flipkart previously attempted scheduled grocery delivery, not ten-minute quick commerce.

This time around, both are trying to play to strengths they’ve spent a decade building: supplier relationships, fulfilment networks, and trusting customers.

Take Amazon. It already has a 49% stake in More Retail, and access to Amazon Fresh’s supply chain in 300 cities. It just slashed commissions to zero on products under ₹1,000 — an attractive proposition for brands that are already paying blended take rates and advertising fees as high as 40% on Blinkit.

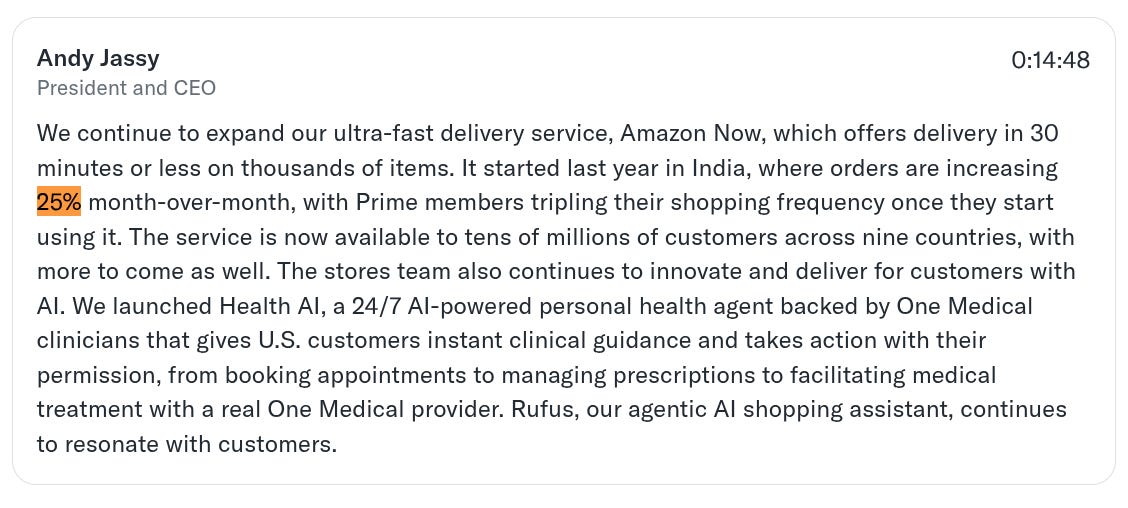

There are some signs it could really become something. One brand founder, for instance, told The Arc that Amazon Now already accounts for about 20% of his total Amazon sales. On the Q1 2026 earnings call, Andy Jassy said that orders in India are “increasing 25% month-over-month” and that Prime members are “tripling their shopping frequency” once they start using the service.

We haven’t seen something that hopeful out of Flipkart yet. But as Walmart’s Kathryn McLay, said at a Bernstein conference, Flipkart won’t trade away market share and future growth for the sake of profitability. In other words, it’s willing to spend its way to growth.

You can see that spending in action. Amazon Now is offering cashbacks of ₹50, ₹100 and ₹200, depending on order size. Flipkart Minutes is pricing about 10% below Blinkit across categories. What could this firepower do?

Why the incumbents aren’t playing along

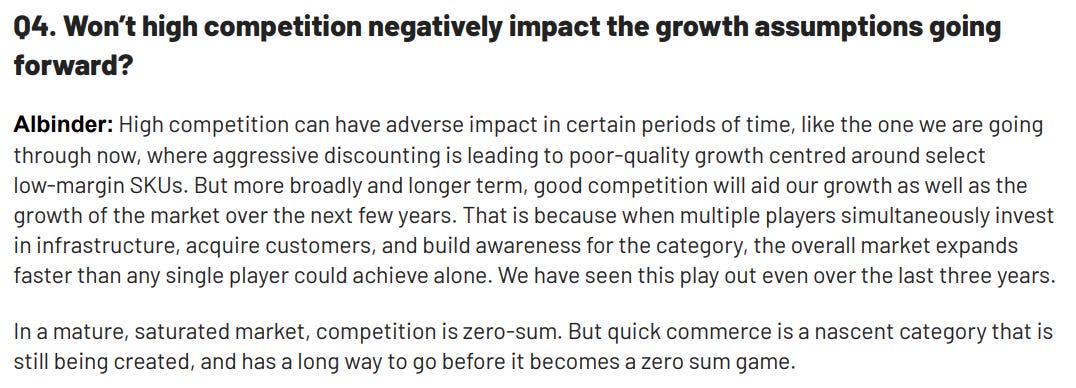

There’s a twist, however: even as the old guard encroaches on their turf, services like Blinkit and Instamart aren’t trying to match them. Having spent years building the unit economics they now have, they don’t want to give it up to new competitors.

In fact, they even claim that doing so is a bad idea. Albinder Singh Dhindsa, Eternal’s CEO and Blinkit’s founder, recently claimed that aggressive discounting pushes quick commerce companies to poor-quality growth, forcing it to subsidise low margin products.

Or as Swiggy group CEO Sriharsha Majety told Economic Times, quick commerce is a commoditised market: you either compete on price, or on what all you stock. And to him, cutting prices didn’t make sense.

Consider the views of Deepinder Goyal, who built Eternal — the company that acquired Blinkit and took it to the top — before stepping down earlier this year. To him, Blinkit was profitable, with half the market. Everyone else, meanwhile, was burning cash at an incredible rate — as much as $2 billion for $5-6 billion dollars worth of orders. That is where a company like Amazon, too, is playing.

What’s harder to answer

Then again, one remarkable just how much money the old guard could pour into this fight, if they wanted. That alone makes them a threat.

Amazon, for example, has more than $140B in cash. Flipkart has the American retail giant, Walmart’s backing. Both have both made their priorities explicit. Amazon India’s country head Samir Kumar told ET the company was “aiming for market leadership in quick commerce.“ Walmart’s Kathryn McLay claimed Flipkart won’t trade market share for profitability. Neither company cares much for how sustainable these businesses would be, right now. They’re in it to win.

Perhaps the worst hit will be Zepto, simply because of the timing around these pushes. It’s trying to go public at exactly the moment Amazon and Flipkart are opening hundreds of dark stores in the same cities it operates. Their presence makes its IPO story harder to tell to investors — even if they’re big now, who knows what happens three years down the line.

Then again, maybe there’s space for everyone. The broader market, after all, is massively underpenetrated. $11B sounds large, but it’s still less than 2% of India’s total grocery spend. The incumbents have built strong businesses for the premium urban customer.

Quick commerce has now gone through a few distinct phases. At first, nobody knew if the idea would even work. Then, nobody thought it could ever make money. Now, the question is whether the companies that built it can hold on to it.

Every time one question is answered, it seems, the next only looks harder.

A sweep of the recent regulatory changes in India’s financial system

Every year, SEBI, the RBI, IRDAI and the rest of India’s regulators keep pushing out rules. Some to make our lives a little easier, most to make the financial system a little sturdier. Individually, none of them is hard to keep up with. But zoom out to a six-month window and you realise just how much has shifted, and it’s not easy to remember all of it. We’ve covered a lot of these changes as they landed. Still, ask anyone to list what changed since the start of the year and they might just draw a blank.

So here’s what we’re going to do. The RBI’s latest Financial Stability Report has a chapter that rounds up every regulatory change of the past several months, across banking, markets, insurance and forex. A lot of it is genuinely too technical or too niche to matter. So, rather than recite the list it’s more useful to step back and notice that the changes cluster around a handful of things that would matter to us.

Let’s dive in.

The problem of banks that wait for the crash

Indian banking has always had a backward-looking relationship with risk. Under the current RBI rules, a loan that’s being paid on time, irrespective of there being a possibility of default and stress, is a “standard asset“ and it carries only a small, flat general provision. Only if and when payments are missed for 90 days does the RBI require the loan to be recognised as stress, reclassified as Non-Performing Asset (NPA), and provided for. And even then, the amounts are fixed percentages for the type of loan given, not real estimates of how much the bank actually expects to lose.

So risk gets sized up after it has crystallised, not before. The fixes this year make banks reckon with risk earlier, and make them pay for the risk they actually carry.

The big one is a change in how banks provision for bad loans. The RBI is scrapping this old incurred-loss framework and moving to what’s called Expected Credit Loss, or ECL. It’s a system where banks have to estimate upfront how much of their lending is likely to sour, and set money aside for it in advance, whether or not there is delay in payments. Loans get sorted by how much their risk has worsened since they were made, and provisioning rises as a loan deteriorates before a default.

It’s the same philosophy the rest of the world adopted after the 2008 crisis, and it adjusts a bank’s reported profit against the risk sitting underneath it. This regulation will officially come into effect on April 1, 2027 and collectively, banks are expected to absorb a one-time hit of ₹60,000 crore.

The second fix works on the same instinct of risk management from a different angle.

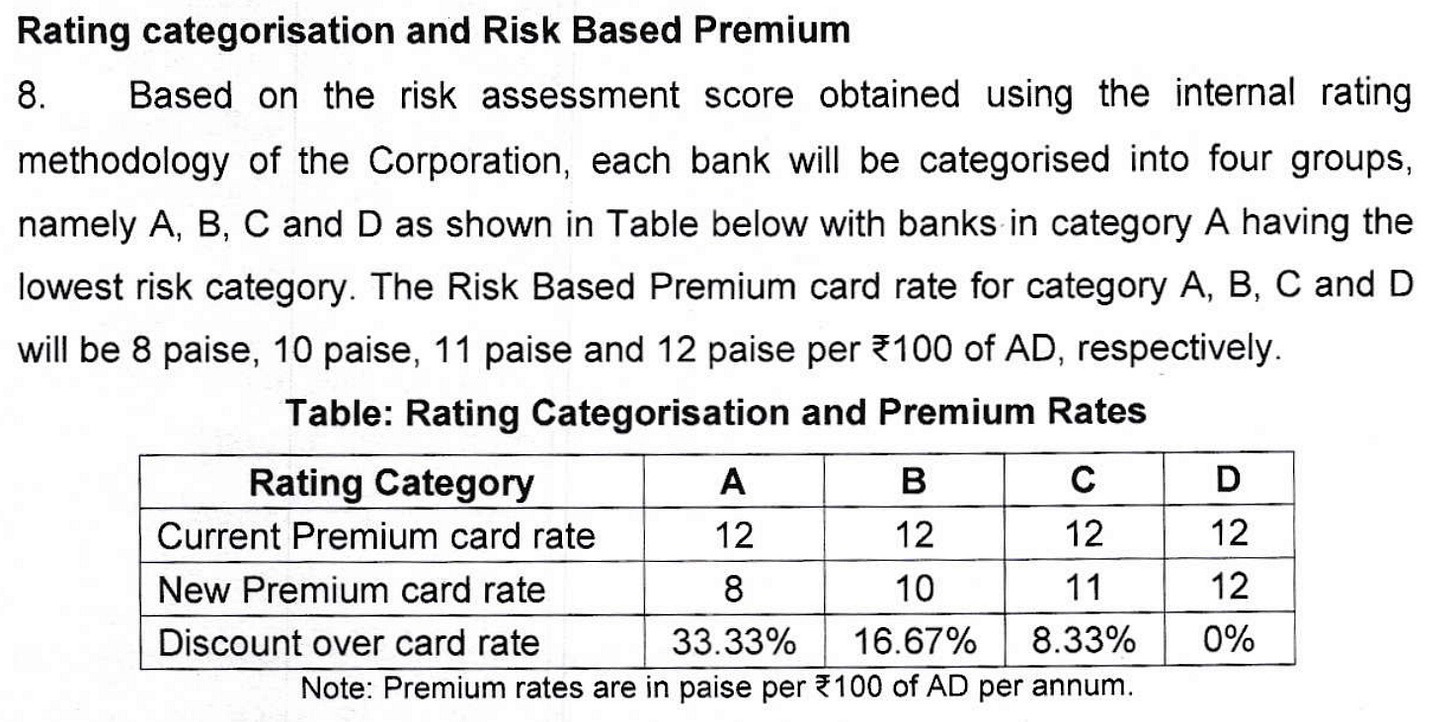

See, every bank in India used to pay the exact same price for deposit insurance, which is the cover that guarantees your money in the bank is safe up to ₹5 lakh, even if the bank fails. The premium for this is a flat 12 paise for every ₹100 of deposits with banks, whether they are the country’s most conservative lender or a co-operative that is one bad year from collapse.

That flat rate forced good banks to subsidise reckless ones. Now premiums are being tied to how risky and well-run each bank is. Now there will be a discount for those that have paid premium for years without ever filing a claim. Suddenly, bad behaviour shows up as a bigger bill.

How much does this actually fix the problem? A fair amount, in principle. Both changes sharpen the incentive to behave, which is exactly what a reactive system was missing. But neither is a magic shield.

King dollar

The second cluster of changes is about our vulnerability to the rupee’s swings against the dollar, and relatedly, to foreign money that can flood in and rush out in a mood.

Through early 2026, the rupee came under genuine pressure, and regulators reached for two very different kinds of fix. One was to stop the bleeding now, while another to reduce the exposure over time.

The immediate fixes were defensive, and there were a lot of them. The centrepiece was dollar-rupee swap deals.

When a bank raises a dollar deposit from an NRI, it takes on currency risk. Basically, it owes those dollars back in a few years, but in the meantime it wants to convert them into rupees and lend them out at home. If the rupee weakens over that stretch, buying the dollars back to repay the depositor gets expensive. That risk alone is often enough to keep banks from chasing foreign deposits in the first place.

The RBI’s swap tempers that risk. The bank hands its dollars to the RBI now in exchange for rupees, and the RBI commits to returning those dollars at a fixed, pre-agreed rate at maturity. So now, the currency risk is parked on the central bank’s books instead of the bank’s. This makes raising dollar deposits safer.

The next lever made those non-resident deposits even more profitable to hold. Normally, a slice of every deposit a bank takes has to sit idle. It must be held as cash with the RBI, or parked in government bonds rather than being lent out to earn a return. The RBI temporarily waived that requirement on these fresh foreign deposits, so banks could put every rupee of them to work. The better the economics, the harder banks chase the deposits, and the more dollars flow in.

A third set of moves was about curbing speculation. When a currency is sliding, traders and banks pile on bets that it will fall further, and the selling itself drags the rupee down — a self-fulfilling spiral. So the RBI clamped down on the banks placing those bets. It capped how large a net position on the rupee any single bank could hold overnight: a bank buys and sells the currency all day, and the gap between the two is its standing bet on where the rupee is headed. The RBI limited that gap to $100 million per bank at the close of business — small enough that no one bank could push the market around.

These were all emergency steps. The slower, structural fix was about the kind of foreign money India attracts.

The worry was that too much of foreign money that came was nimble, opportunistic capital that, when things go south, would leave just as quickly as it came. The old caps on foreign holdings of government bonds tried to manage that by limiting how much could come in at all. But a cap is indiscriminate, holding back patient and hot money alike, and the fiddly rules attached to it actually deterred the biggest, most patient investors who need scale and certainty before they’ll commit.

That’s where the Fully Accessible Route (FAR) for bonds enters.

By opening a class of bonds foreigners can buy with no ceiling at all, FAR made Indian debt eligible for global bond indices, which bring in passive, benchmark-tracking money that stays as long as India is in the index. Importantly, that’s steadier than the discretionary flows the caps had been holding back. Extending FAR to bonds of 15, 30 and even 40 years, plus sovereign green bonds, doubles down on that, since forty-year paper is what pension funds and insurers buy.

That being said, does this money show up in size? So far, opening the door widened the pool of buyers, but it doesn’t truly manufacture demand for forty-year Indian debt.

Regulation against innovation

The third cluster is perhaps the most relatable to ordinary people.

You’re probably well aware of scams that arrive as Telegram groups promising guaranteed returns and slick “advisors” flashing fake credentials on Instagram. You might also be aware of cloned trading apps that impersonate real ones, or insurance apps selling you some hidden cover that you never asked for and don’t need.

These deceptions are evolutions of old, physical tricks that went digital. And with that shift, it has become harder to regulate them. The old model of waiting for someone to complain, then investigate, simply can’t keep pace with harm that spreads at the speed of a feed.

The fix here is a shift in tactics: regulators picking up the same tools as the people causing the harm.

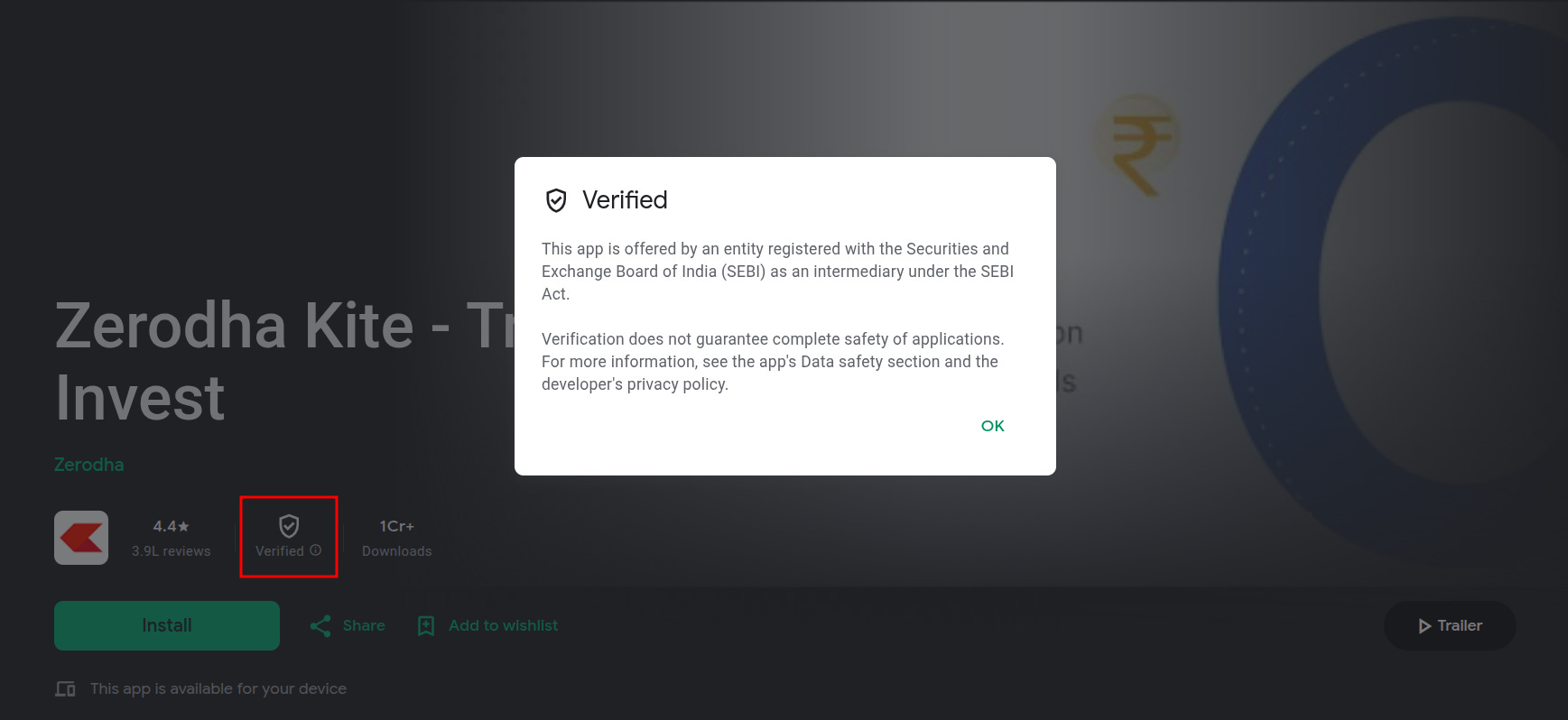

On the markets side, SEBI made two moves against digital fraud. It partnered with Google to put a “Verified“ badge on the Play Store apps of genuinely registered brokers, so you can tell a real app from a scammer’s clone. This one is already live beginning with stockbroker apps, more than 600 of which have been badged so far, and it’s set to widen to other registered intermediaries over time.

In the same push, SEBI says it has had more than 60 fake trading apps pulled from the app stores and flagged well over a lakh misleading pages for takedown.

SEBI also switched on an AI system that scans social media in real time to flag guaranteed-return claims, fake certifications and impersonation automatically, instead of waiting for a victim to file a complaint.

In insurance, IRDAI went after the incentives. Alongside convening insurers and hospitals to untangle the systemic mess in health claims, it did something genuinely unusual: it tied 50% of an insurance company’s top executives’ variable pay to customer-facing outcomes, like how fast they settle claims, how quickly they resolve grievances, and, remarkably, the elimination of “dark patterns“ that nudge you into buying cover you don’t need or make cancelling deliberately painful.

These are all real upgrades that shape behavior at a large enough scale.

A few smaller ones worth pocketing

Three changes don’t fit a theme but are worth filing away.

For one, if you once bought shares in physical form and lodged a transfer request that never went through. Many got stuck on documentation issues before SEBI stopped physical share transfers in 2019, after which changing ownership required the shares to be in electronic form. SEBI has opened a one-time window until February 2027 to re-lodge them and finally get the shares moved into your name and dematerialised.

Then, the RBI set up a committee to make India’s financial system quantum-safe, on the logic that a powerful enough quantum computer could one day crack the encryption protecting every bank transaction, and it’s better to prepare early than scramble late.

Third, the pension regulator approved NPS Swasthya, an experiment that lets you use the machinery of your retirement account to cover medical bills. By doing this, the regulator acknowledges how often a big hospital bill can wreck a retirement plan in the first place.

None of these were about grand new schemes. The more interesting question is which of these holds once the pressure that prompted them fades.

Tidbits:

Adani and Abu Dhabi’s IHC are building a $11.5 billion aluminium plant in Odisha that will add 2 million tonnes of annual capacity.The project could shake up India’s aluminium sector as demand is set to hit 8.5 million tonnes by 2030.

Source: ETThe World Bank has upgraded Sri Lanka to an upper-middle-income economy, just three years after the country’s worst ever economic crisis. Vietnam was also upgraded to the same status in the same round.

Source: The HinduThe Indian government is planning stricter rules for VPN providers, requiring them to set up an office in India and appoint compliance officers who can respond to law enforcement requests.

Source: Indian Express

- This edition of the newsletter was written by Krishna & Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s digital economy got here, through the data buried in Jio’s IPO filings.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉