A 10-minute parcel comes for Dalal Street

Will Zepto’s IPO deliver?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Will Zepto’s IPO deliver?

Can this memory supercycle shed its own skin?

Will Zepto’s IPO deliver?

The quick commerce race in India has really narrowed down to three players: Blinkit, Swiggy Instamart, and Zepto. Of the three, only Zepto wasn’t a public company.

Until now. Zepto has officially filed its IPO papers. And of course we had to cover it.

The q-com industry has evolved in interesting ways to get here. It was Swiggy that actually first experimented with instant deliveries, back when the idea felt novel. When it launched in 2021, Zepto went further by making the 10-minute promise the entire product and branding itself around that. But Blinkit, which started as Grofers and completely reinvented itself, ran away with the market. Nobody has been able to close the gap with them since.

In the last quarter of FY26, Blinkit processed almost 274 million orders from 2,243 dark stores across more than 200 cities. Zepto processed 210 million from 1,139 stores across 66 cities, while Instamart did 112.6 million. That puts Blinkit at around 46% of all quick commerce orders, Zepto at 35%, and Instamart at around 19%. The market these three are competing over is worth about $11 billion — that’s still less than 2% of India’s total grocery spend. And Zepto’s bet is that there is more room to grow.

The headline numbers

Let’s get into the numbers in Zepto’s IPO filing.

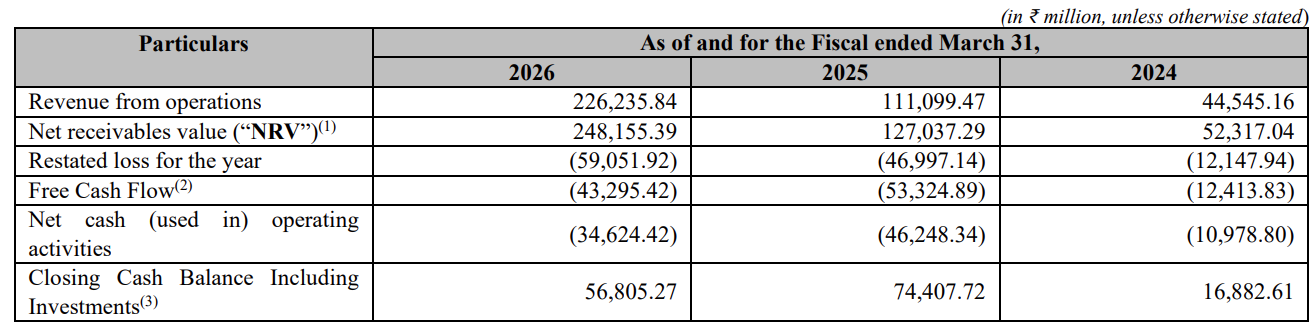

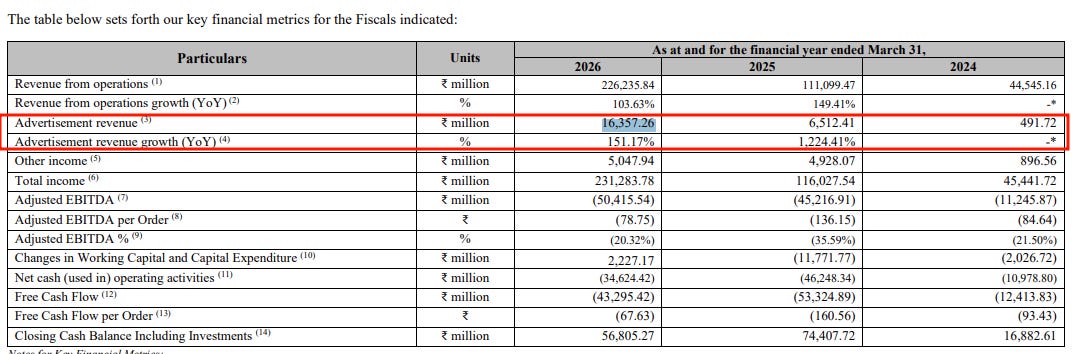

Zepto’s revenue went from almost ₹4,500 crore in FY24 to roughly ₹11,000 crore in FY25 to about ₹22,600 crore in FY26. Losses, meanwhile, went from ₹1,215 crore to ₹4,700 crore to ₹5,905 crore.

The revenue numbers come with a caveat, though. That impressive jump from FY24 to FY25 includes an accounting change.

You see, in January 2025, Zepto shifted from a marketplace model to a principal model. Before that, when you ordered ₹500 of groceries, the company only counted its service fee in revenue, which is the ₹50 it earned for storing and delivering your order. After the shift, it started counting the full ₹500, because as per accounting rules, when a company physically controls the goods it sells, it has to book the whole transaction.

This is also why, rather than merely revenue, Zepto measures its business using a measure called Net Receivables Value (NRV). NRV includes the actual value of all orders on the platform, plus advertising income and subscription fees, all with taxes included.

In comparison, Blinkit uses Net Order Value (NOV) while Swiggy uses Gross Order Value (GOV). Both track the value of orders placed and are calculated differently from each other too. It’s worth keeping in mind that they are not the same metric, so comparisons between all three firms must be done with caution.

The money flow

Now, how does money change hands with each delivery?

When you place an order, you pay Zepto the full amount. Zepto then pays the Merchant Partners, who are the suppliers of those goods. That leaves Zepto with a gross margin of about ₹72 on a typical order.

That ₹72 then has to cover getting the order to your door. About ₹46 goes to the delivery partner as pay. Around ₹34 goes to the cost of running the dark store, which includes rent and paying the pickers and packers. Combined, that easily exceeds ₹72. In one order, just the act of delivering the goods loses money.

Zepto tries to make up that difference by ad placements. Every time you see a sponsored listing or banner on the app, a brand is paying Zepto for that placement. The IPO papers show us what this business looks like for the first time: Zepto earned ₹49 crore in FY24, ₹651 crore in FY25, and ₹1,636 crore in FY26. In FY26, Zepto earned more from advertising than it spent on its own advertising.

Add it all up and Zepto lost about ₹79 per order in FY26. In FY25, that number was ₹136.

The basket problem

A structural challenge that any q-com player faces is that the unit economics of delivery are immune to the order size.

As per The Arc, Zepto’s average order is worth about ₹330, Blinkit’s is ₹525, and Instamart’s is ₹700. But getting a ₹330 basket to your door costs the delivery partner roughly the same as a ₹525 one. The last-mile expense doesn’t shrink just because the order is smaller. Blinkit earns 59% more per order to cover that same cost. That, of course, is why each player has a minimum order value requirement.

Interestingly, though, Zepto’s answer isn’t to get customers to spend more per order. The bet is wholly on volume: pushing more orders through each dark store. The more orders a store processes, the thinner the fixed costs get per delivery. The idea is to go deeper in the 40 cities you’re already in, add more dark stores in the same neighbourhoods, and watch the per-order cost fall.

In Q4 FY26, Zepto was averaging 2,140 orders per dark store per day, up from 1,325 in FY24. Instamart, in comparison, has almost exactly the same number of dark stores as Zepto, but processes barely half the orders from them. Zepto is running its stores at nearly double the productivity.

A chink in the armor

There is another important factor in Zepto’s business that affects its economics, and that has to do with its ownership structure. But the problem doesn’t start from there. Bear with us for this explanation.

See, quick-commerce platforms have mostly worked as marketplaces. Merchant Partners own the goods in the dark stores and the platform connects them to customers. Blinkit has moved away from this, directly buying and owning all stock in its dark stores.

When you own the inventory, you buy directly from brands in bulk. You plan supply for all your stores, across the country, in one order. That buying power means cheaper prices from brands. It also gives you more control over what’s on the shelf.

You might even think owning all that inventory would require a lot of cash upfront. But in q-com, inventory moves so fast that the cash doesn’t stay tied up for long. A packet of biscuits that arrives at a dark store in the morning is typically sold and delivered by evening. Compare that to a regular retailer where goods might sit on a shelf for weeks. The faster the inventory turns, the less working capital gets stuck in it.

However, Zepto cannot do this because of India’s FDI rules.

Our law states that a company that is majority foreign-owned cannot hold inventory for direct retail. Zepto is classified as a foreign-owned and controlled company. This is why investors like Motilal Oswal have been steadily buying higher stakes in Zepto. The more domestic ownership it builds, the closer it gets to running an inventory-led model like Blinkit, and the better its economics improve.

Show me the money

Zepto has ₹5,680 crore in cash and liquid investments as of March 2026. It has no debt and has been funded entirely by investors, who have put in over 20,000 crores since the company started.

The reported loss of ₹5,905 crore is not the same as the cash Zepto actually burned. Some of it exists only on paper — when Zepto fits out a dark store it spends the money once but accounting rules spread that cost across several years, and stock options given to employees are recorded as expenses even though no cash leaves the bank. Strip those out and the actual cash Zepto burned was closer to ₹4,329 crore.

There is also a working capital dynamic worth understanding. When you order on Zepto, you pay immediately. But Zepto does not have to pay its suppliers straight away — it settles those bills over 30 to 60 days. As of March 2026, Zepto owed its Merchant Partners and suppliers about ₹3,725 crore that it had collected but not yet paid out.

On the other side, brands and partners owed Zepto ₹2,424 crore in unpaid fees. The fact that what Zepto owes is larger than what it is owed weirdly works in its favour. Customers pay first, suppliers get paid later, and in that gap, Zepto is always sitting on more cash than it technically needs at that moment.

Conclusion

At its core, quick commerce is a logistics business dressed up in a retail interface. The margins are thin, the costs are operationally intensive, and it’s hard to say if the advertising income, while growing fast, will make up a meaningful share of the business. There is probably a ceiling on how much brands will pay to reach a grocery app, though where exactly that ceiling sits is an open question.

All of the real economics come from order density and scale, which means every metric is load-bearing. If volume softens in a city, or a competitor runs a discount campaign, or delivery costs tick up, the per-order math moves very quickly in the wrong direction.

We will be watching how these economics evolve as another young q-com company hosts a historic listing.

Can this memory supercycle shed its own skin?

If you’ve ever wondered why Jensen Huang, the CEO of NVIDIA, is seen spending so much time in South Korea, you’re not alone.

Last week, Huang was seen eating Korean barbecue with executives from LG Group, SK Hynix, and Naver. At SK Hynix’s Computex booth, he signed a wafer of next-generation memory chips. On it, he wrote three simple words: “Please Make More“.

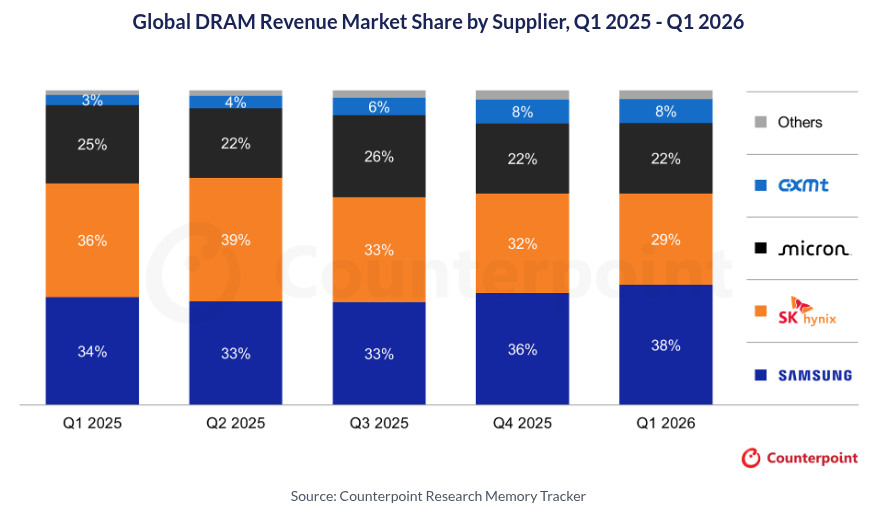

Samsung, SK Hynix and Micron, the Big Three of the memory industry, are doing numbers like never before. SK Hynix posted a 72% operating margin in Q1 2026 — higher than NVIDIA’s 65%. Samsung became only the second Asian company, after TSMC, to be worth a trillion dollars. Micron’s revenue more than tripled year-on-year. The results of Samsung and SK Hynix propelled South Korea over India as the world’s sixth-largest stock market.

All the while, all of them are struggling to fulfill demand. There is an acute shortage of the AI memory chips that drove these numbers. It’s why Huang wrote those words.

Meanwhile, China’s CXMT, a company that barely registered on global rankings a few years ago, has climbed to 8% of the global DRAM market. YMTC, another Chinese firm, increased its share in the NAND market from 8% to 13% in a year.

There’s a lot happening. The world’s most powerful tech CEO is flying to East Asia to personally lobby for more chips, and two Chinese firms are climbing the ranks by picking up what the leaders left behind.

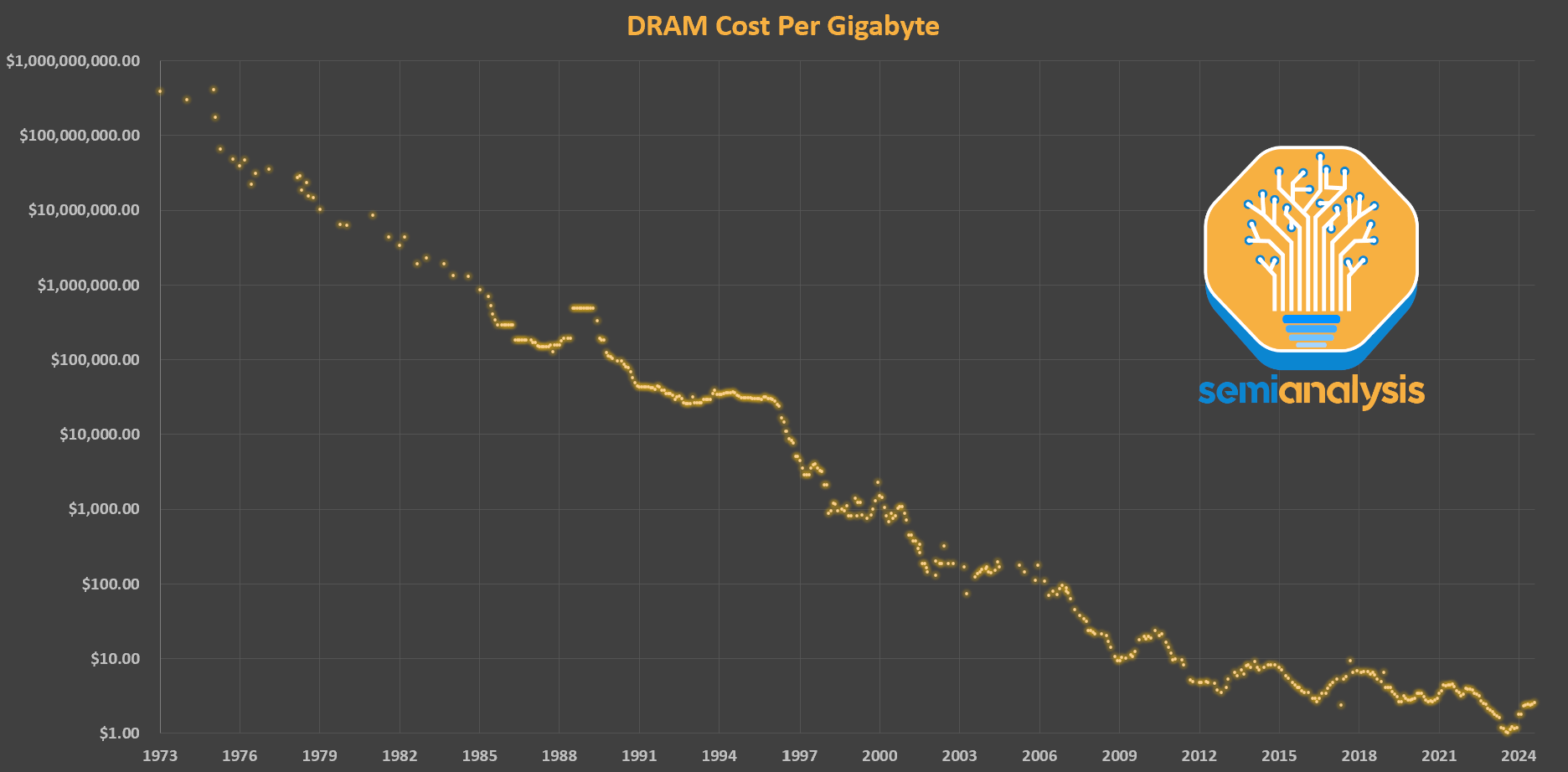

In our memory primer from last year, we saw how the industry has been scarred by decades of boom-and-bust cycles that incumbents couldn’t predict on time. Every memory supercycle of the past ended the same way: manufacturers built too much capacity in response to a consumer technological innovation, supply overwhelmed demand, and prices collapsed.

But now, the industry’s biggest players are saying this cycle may not follow the old script.

Let’s look into what’s materially changed this time, and how different the tune they’re now singing truly is.

Towering research

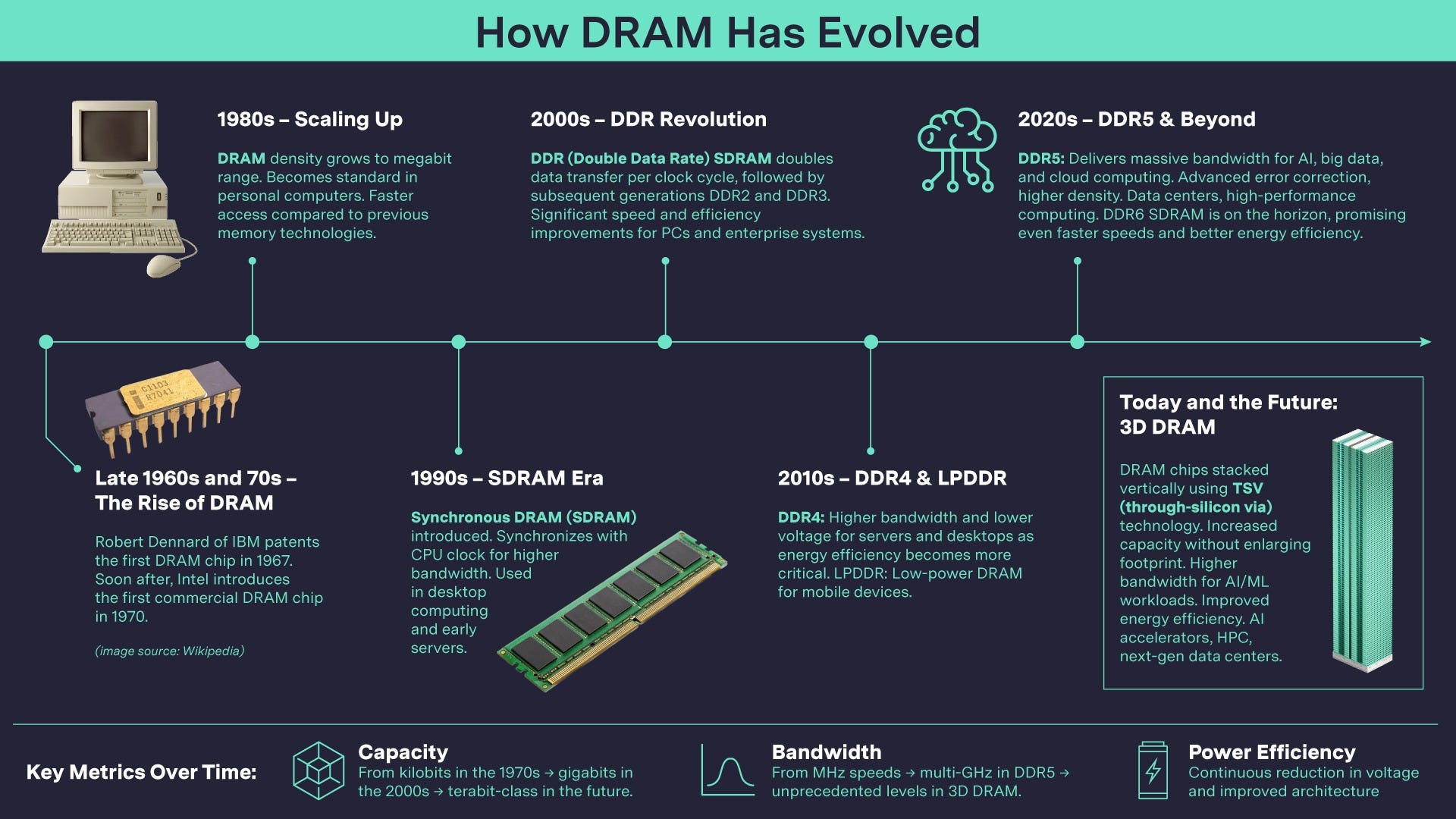

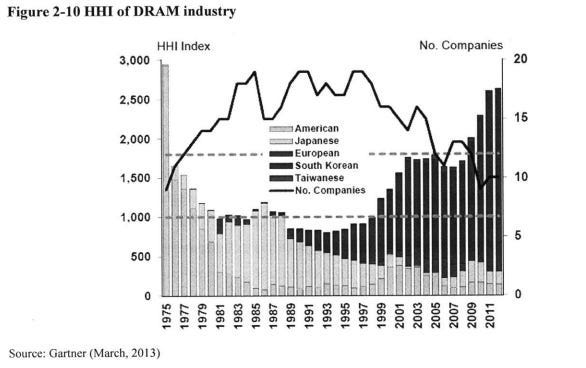

We recommend reading our earlier primer to understand the basics of how memory chips work. But if you don’t have the time for that, the most important thing you should know is that for most of history, memory chips were a commodity business.

There was no big difference between a DRAM chip made by Samsung or that by Micron. PC makers didn’t differentiate significantly between them, except on price. Then, the most sure-shot way that memory chipmakers could compete was by increasing the density of memory contained in a given two-dimensional surface area. In fact, until the 2000s, DRAM density doubled every 18 months.

But this horizontal scaling hit a wall. Over the past decade, DRAM density has only doubled once.

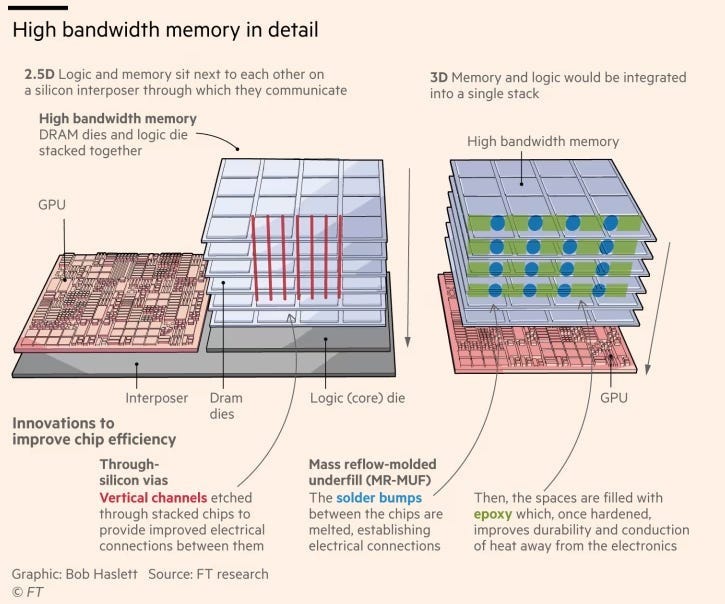

What was the response to this problem? Well, the industry decided to go vertical. Instead of squeezing more memory bits onto a flat 2D surface, manufacturers began stacking DRAM chips on top of each other. That’s what high-bandwidth memory is: a 3D skyscraper of memory dies, typically 8-16 layers tall.

Most importantly, unlike past DRAM chips, HBM is not a commodity. That’s primarily because of how complex vertical stacking is.

Each die that comes off a silicon wafer has an uneven surface. That was okay as long as the DRAM contained one die. But stacking up multiple uneven surfaces with perfect alignment is not easy. Those dies have to be connected via thousands of microscopic vertical interconnects called through-silicon vias. Doing this for 8 dies alone is incredibly hard and error-prone — a single bug renders an entire stack useless. That’s why producing one gigabyte of HBM consumes 3-4 times the silicon wafer area of standard DRAM.

There is also the advanced packaging that HBM entails which adds to this complexity. But we won’t get into the details of that here.

All of this makes HBM difficult and expensive to make at scale. In fact, SK Hynix built the first HBM device back in 2014. But it was overkill for even the most powerful computing tasks back then.

What changed was AI. With models scaled to billions of parameters, inference required moving vast quantities of data within milliseconds. Traditional DRAM fell short of doing so, but HBM could. Yet, supply of HBM is so far behind current demand, primarily because making it at scale with minimal errors is one of the hardest manufacturing processes in the world.

What’s more, HBM is only getting more complex, not less. That has to do with how designing an HBM product is a massive collaborative effort that starts with NVIDIA.

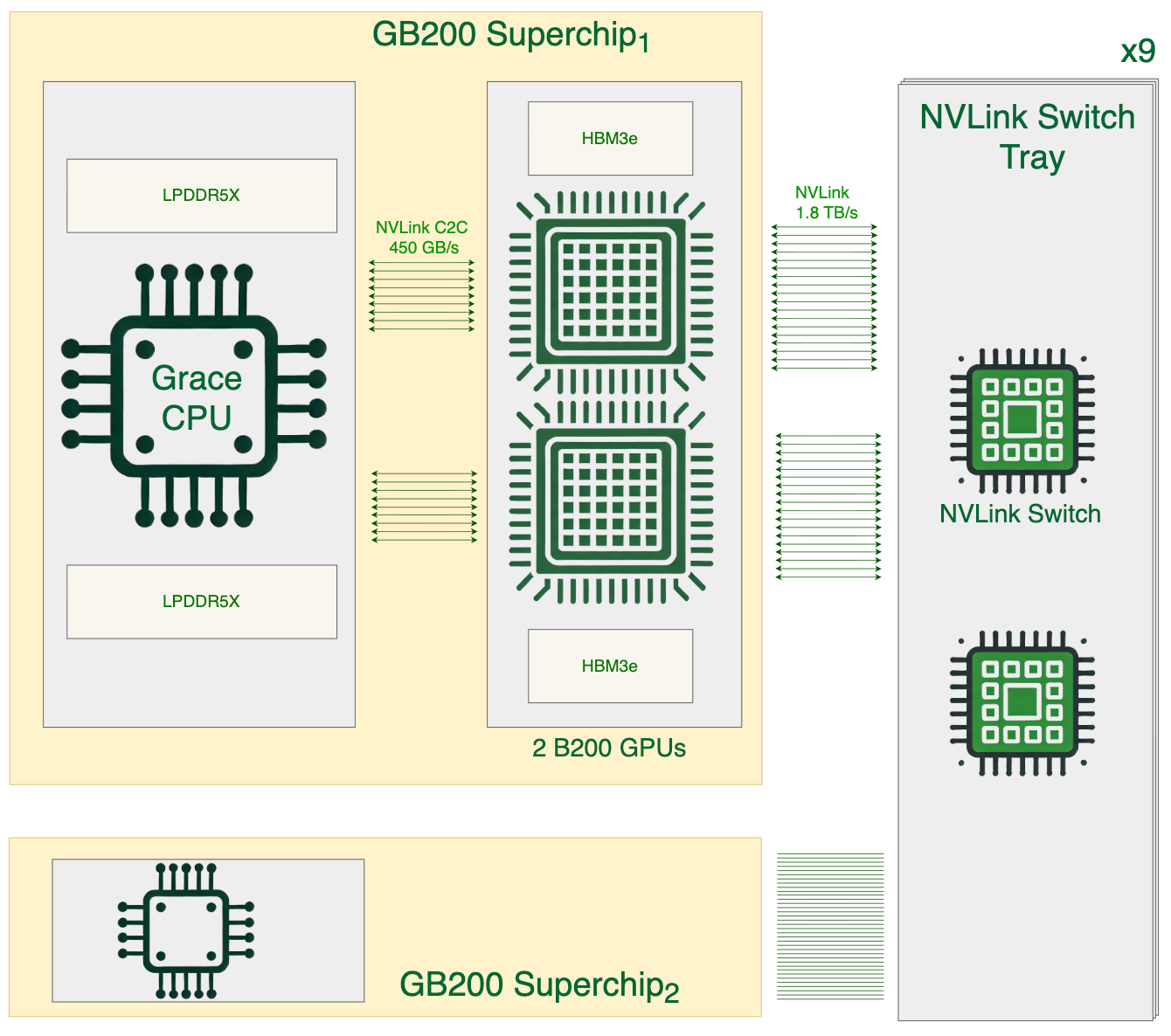

You see, NVIDIA doesn’t just make GPUs anymore — it designs entire rack-scale AI supercomputers of which GPUs are one part. For example, a single GB200 NVL72 rack contains 72 NVIDIA B200 GPUs, 36 NVIDIA Grace CPUs, networking hardware, and over 13 terabytes of HBM. These racks are assembled by contract manufacturers like Foxconn, while the GPU and CPUs are made by TSMC. Both the CPUs and GPUs need memory made by SK Hynix and Samsung.

TSMC, Foxconn, and memory chipmakers all have to work in lockstep with NVIDIA’s architecture, and that means a lot of pressure-testing. In fact, Samsung failed NVIDIA’s HBM3E qualification repeatedly, only passing in late 2025. This level of co-designing only entrenches how insurmountable it can be to make HBM right now.

A historic lock-in

The second structural change in the AI-driven memory cycle is in how memory is being sold.

For decades, DRAM pricing was negotiated on a quarterly or even monthly basis. Suppliers and their customers — like PC makers and phone manufacturers — would haggle over prices based on whatever the supply-demand balance looked like at that moment. A volatile spot market ran alongside, setting real-time prices for smaller buyers. HBM, when it existed at all, followed an annual negotiation cycle. Nobody locked in supply for more than a year. The industry was too volatile for either side to commit beyond that.

Now, that has changed. Since late 2025, just for HBM, all three major memory makers have shifted toward 3-5 year long-term agreements with their biggest customers. And there are two reasons for this, both of which are interlinked.

Firstly, remember, the industry wears the battle scars of past boom-and-bust cycles. Those were driven by volatility in the open market. Long-term contracts, in contrast, give them a visibility over revenue that the industry never had before. If you have committed volumes at fixed prices for three years, you can plan capex more rationally and avoid the panic overbuilding that caused prior busts.

But this shift was partly made possible because of the second reason: the biggest buyers of memory chips have changed.

They are no longer consumer brands with volatile, short-cycle demand like Lenovo or Xiaomi. They’re now hyperscalers like Microsoft, Google, Meta, and Amazon, making multi-year, multi-billion-dollar capital investments in AI infrastructure. These companies have long planning horizons and deep pockets. They can commit to long memory procurement contracts because their data centre buildouts are also long.

This also means that this memory supercycle is most likely going to be bigger and longer. Which makes sense, since the AI capex boom which the memory cycle is strongly linked to has turned gigantic.

Ghosts of supercycles past

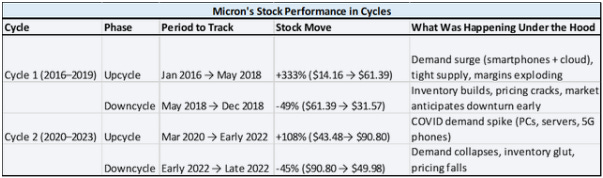

But a bigger, longer cycle doesn’t mean the boom-and-bust cycle goes away. If anything, it could be more pronounced. And it doesn’t help that the memory industry’s history is littered with moments like the current one, where everyone expects “this time to be different”.

In 2017-18, Micron’s operating margin hit 49%, the three-player oligopoly was supposed to guarantee pricing discipline, and cloud demand was supposedly endless. Then revenue fell 30% and Micron’s stock dropped 56%. In 2021, chipmakers expected they would have better control over this cycle. But by 2023, they were proven decisively wrong, as Samsung had cut production by half.

The pattern is consistent: demand surges, manufacturers pour tens of billions into new fabrication plants, the fabs take years to build, and by the time they’re online, the market has shifted.

The long-term agreements with hyperscalers are partly a response to this puzzle. After all, if demand is locked in with fixed contracts, a sudden bust for memory players becomes harder. But long-term contracts don’t eliminate forecasting errors. They simply move them, or shift the risk of procurement to someone else — in this case, that’s the hyperscalers.

The capex ramp of HBM is mind-boggling. Samsung plans to expand memory capacity by 50% this year. Micron is investing $25 billion in capex this year alone. New fabs from all three are scheduled to reach volume production by 2027 or 2028. All are building simultaneously based on the same demand signal.

But if hyperscalers scale back on data centre investment because AI monetisation disappoints, memory makers will have tons of excess capacity sitting idle, and immense profits could quickly turn into devastating losses.

To complicate the cycle further, there’s another variable that’s ramping up competition against the Big Three memory players.

The China problem

The current market structure of memory chips is being threatened by two companies that represent China’s bid for memory chip self-sufficiency. CXMT and YMTC.

CXMT’s first quarter revenue in 2026 was over 700% more than Q1 2025, and the profit earned in Q1 2026 was ten times that of the profit of all of 2025. It is also preparing for the largest Chinese IPO since 2022. YMTC, China’s leading NAND flash maker, is also heading toward a public listing.

Now while CXMT is closing on Samsung, their memory chips are still 2-3 generations behind. They only achieved technology parity for HBM3 recently, while the others have moved on to HBM4. And they only expect volume HBM3 production to catch up by the end of this year. Part of this gap exists because of US sanctions on Chinese firms.

But China’s angle isn’t at the leading edge, either. It’s in the commodity memory that Samsung and SK Hynix are vacating. As they redirect their old DRAM fabs toward HBM, there’s a growing void in mainstream DRAM for PCs and phones. CXMT is filling that void, and the profits from mainstream DRAM, as Samsung itself noted, are now higher than that of HBM.

What makes this particularly interesting is the partnership between both Chinese giants.

Now, YMTC has spent years perfecting a technology called hybrid bonding. They expect it to become the next frontier for making HBM: as the stacks grow taller, it becomes essential for tighter, more thermally efficient interconnects. YMTC holds a strong patent portfolio here, although primarily meant for NAND, which serves a completely different purpose from DRAM or HBM.

Yet, Samsung has begun licensing hybrid bonding patents from YMTC for their own NAND products. A sanctioned Chinese company holding a patent that even Korean leaders need is certainly worth noting.

The risk China poses isn’t a near-term one. But in commodity DRAM, the segment that still accounts for around 80% of global memory volume, a well-funded Chinese manufacturer scaling into the gap left by the Big Three could break pricing discipline at the low end.

That’s the classic mechanism by which government-backed capacity expansion has disrupted this industry before. Japan did it in the 1980s to the US, then South Korea wiped out Japan in the next two decades. China may be running the same playbook.

Conclusion

There’s no doubt the nature of the current memory supercycle has changed. Unlike other memory chips, HBM is not (yet) a commodity. The shift to multi-year contracts is also a significant change.

But that doesn’t mean a boom-and-bust cycle has disappeared. Three companies are building simultaneously on the same demand signal. The void their move to HBM has, in turn, been filled by China. Given their history of ramping up capex in any industry at blinding speed, they may become a huge catalyst for this cycle to go bust.

Willy Shih, a professor at Harvard Business School who studied memory cycles, told Fortune: “Anytime people show me these curves that just go to the sky with no end, that never continues forever. This too will pass“. Throughout capitalism, every new technology, from the railroad to EVs, has gone through this trajectory. As the saying goes, the more things change, the more they stay the same. Lest we forget, that may still be true for memory.

Tidbits

Auto ancillary Bharat Forge has revealed that it is now working with three of the world’s top five chipmakers and is manufacturing components for lithography machines — a critical part of semiconductor equipment. The move aligns with India’s Semiconductor Mission, which has attracted over ₹1.65 lakh crore in investment commitments.

Source: MoneycontrolVietnamese EV maker VinFast is investing ₹7,000 crore in the second phase of its Thoothukudi facility in Tamil Nadu, adding dedicated production lines for electric two-wheelers and buses. The expansion is part of VinFast’s broader $2 billion commitment to Tamil Nadu, with e-bus production targeted for August 2026.

Source: ETAhead of the third round of airport privatisation, the civil aviation ministry has recommended limiting bids per operator to prevent monopolisation. One option on the table would cap a single entity at two blocks (roughly four airports), with the second-highest bidder getting a matching right if the same player tops a third.

Source: The Hindu

- This edition of the newsletter was written by Krishna and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Decoding Bain’s India Venture Capital report with the authors

Bain & Company’s annual India Venture Capital report is one of the most rigorous deep dives into the country’s opaque private markets, and this year’s edition is themed Warm Currents and Cold Seas. We sat down with co-authors Aditya Shukla and Aditya Muralidhar to look beyond the slides and unpack what is actually happening on the ground. Our conversation goes into how private market data is built without a Bloomberg equivalent, how the LP landscape and family offices have shifted over the last six years, why VC held steady while PE faced headwinds, the unexpected explosion of quick commerce, and the mounting pressure on SaaS companies to figure out AI. Read the key takeaways on Subtext:

Watch the full podcast episode below, where the authors of the Bain report discuss the nuances of India's venture capital ecosystem and the future of startup funding

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Was doing the math on the Zepto DRHP by taking Bernstein report (released end of lastvl year) as base. When I was dividing FY26 daily orders by their 1,139 year-end stores, it won't get you to their claimed 1,677 Orders/Day/Store.

The reality: They use 'operational dark store days.' Factoring in 169 opens & 59 closures, the average strictly isolates the exact days a store was live.

Why add this complication when the orginal orders vis-a-vis orders from 'operarjomalndark stores' weren't much of difference? Would appreciate the answer.

"Before that, when you ordered ₹500 of groceries, the company only counted its service fee in revenue" - Could you please share where you are inferencing this from within the DRHP? The para which mentions change in revenue recognition before Jan'25 ends with "We also earned revenue from the sale of goods to wholesalers and retailers as part of our procurement and distribution operations." I think what changed in Jan 2025 was the legal structure between parent and subsidiaries and not the difference between commission vs gmv revenue.