Abid Hassan on why we’re on the brink of an economic crisis

Hi, Krishna here again. Last weekend, I wrote about how we kicked off our new limited series, Baby’s First Bear Market. The idea is simple: I’ve never actually lived through a real bear market because I only started investing during Covid, when almost everything went up. But now, with stocks dropping all around, it finally feels like we’re in the thick of one. I’m left wondering, “Do I sell everything? Double down and buy more? Or just hang tight?”

In the first episode, I spoke with Deepak Shenoy, founder of Capitalmind, who grounded me with his big-picture view of market cycles. For this second episode, I spoke with Abid Hassan, founder of Sensibull.

If there’s anyone who knows how to handle rough markets, it’s Abid. He graduated during the 2008 crisis (which terrified most people out of finance), lost massive amounts in the markets multiple times—going bankrupt thrice—and still found a way to keep trading.

Basically, Abid has been through the ups and downs—so I wanted to pick his brain on what a young investor like me should do when everything suddenly goes south.

Here are some of the things that stood out to me in our our conversation.

Should I just sell everything and go FD?

This is one of the first things I asked him. His answer was quite simple. He said that if you’re older—say you’re in your 40s or 50s, with some life goals and limited time until retirement—playing it safe might be wiser. Because if you’re that close to the finish line, one financial meltdown could set you back for good.

But if you’re 22 like me, it might not make sense to panic-sell. Abid says this:

90% of the money you’ll ever have is still coming after 30 anyway.

Whatever I have in the market right now is basically a small fraction of what I’ll earn over my entire life. He did add a caveat, though: Never invest money you need soon. If you’re going to use that money, it should be safe, that absolutely belongs in something stable (like an FD).

This meltdown might be long—or it might not. Nobody really knows.

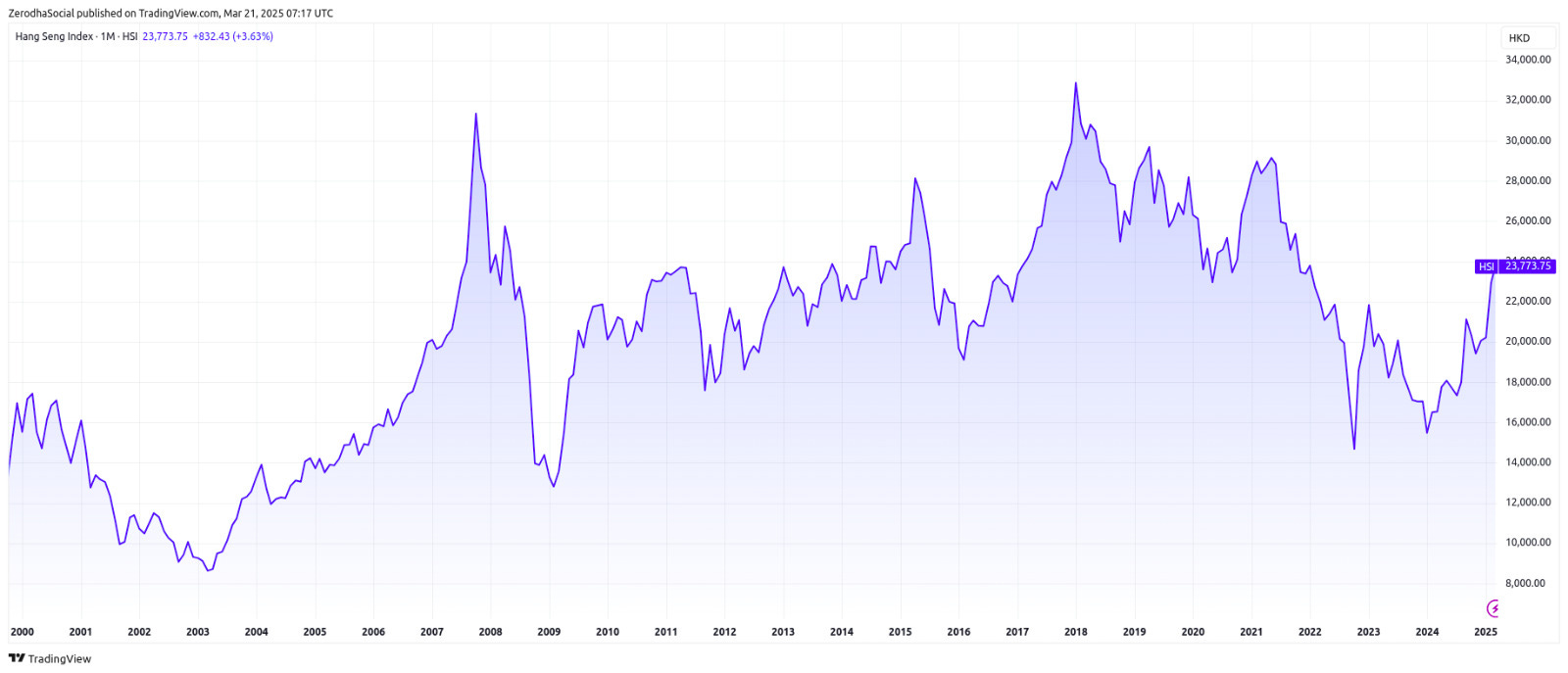

I asked him something like this, “How bad could this get? Is it going to be 2008 2.0?” He laughed and said we don’t really know how long or how deep a correction can go. Sometimes we get these quick dips that recover in months, and sometimes we get multi-year slumps—like Japan’s so-called “lost decades,” or the Hang Seng taking around 7 years to claw back to pre-crash highs.

His bigger point, though, was: Why did we go up 200% post-COVID in the first place? The world printed insane amounts of money, and that money chased every asset class—stocks, real estate, gold, even crypto. So if we soared beyond reason, it’s only natural that we correct at some point. It’s not always about “the markets are broken”; it can just be a reversion to sanity.

I lost 80% in a single day

One of the stories from Abid that he shared was how he once bet nearly all his savings on a single-stock futures trade. This was back in 2017, when he didn’t have much money left (he’d poured most of it into starting Sensibull). The trade went horribly against him, and in one day, poof—80% of that capital was gone.

He joked about not knowing how he’d pay rent, but that experience was brutal enough to change how he trades forever. Now he only does “hedged trades,” mostly options spreads, where the absolute worst-case loss is capped from the start. It’s his insurance against those nightmare scenarios.

His takeaway for a first-time investor like me was crystal clear: always respect the possibility that you could be wrong, because the market can humble you any day.

Markets can remain irrational longer than you can remain solvent - John Maynard Keynes

2008 changed how he sees everything.

Abid was at Citibank then, fresh out of IIM, when the entire financial world pretty much blew up. He said this was the headline on The Wall Street Journal in 2008 said this:

That hammered home the message: Nothing is guaranteed. Big banks can collapse in days. And that’s exactly what happened—Lehman literally vanished, Merrill got absorbed, and AIG needed a bailout. People lost jobs overnight. Abid says if you’ve seen that with your own eyes, you don’t take safety for granted ever again. He told me about a friend who left Lehman’s London office on Friday, flew to New York over the weekend, and by the time he landed on Monday, Lehman was kaput. That’s how fast the floor can vanish under your feet.

Because of that, Abid approaches markets (and his own finances) from a place of “survival first.” He’d rather miss out on some upside than be completely blindsided by a meltdown.

He said this:

Once you see that happen to what were supposed to be invincible institutions, you don’t assume anything is safe anymore.

That’s also why he’s comfortable missing out on “big rallies.” Because after you see banks vanish and markets plunge 50–60%, you realize how nasty it can get when the market really decides to crash. And you don’t want to be all-in if/when that moment arrives again.

Why he’s mostly in FDs and bonds right now.

I found it fascinating that someone who literally runs an options-trading platform isn’t actually betting big on equities at all or anything else that gives massive returns. He’s sitting in FDs or government bonds, where he makes a steady 6–7%. And if he does trade, it’s usually smaller, hedged positions.

He admitted that maybe he’s missing out on upside if the market rallies hard from here. But that’s fine—he’d rather not risk a meltdown wiping out a big chunk of his wealth. He’s seen that movie one too many times. He’d rather preserve his capital and wait for a moment when things feel, in his words, “more sane.”

Don’t trade for money; trade to get good

This is something Abid said throughout our conversation. I told him I’ve dabbled in trading a few times, and I see a bunch of my friends trying to make quick money by trading. His response was: If you’re getting into trading solely to make a quick buck, especially with small capital, the odds are stacked against you. You’ll be pushing risk too high, or you’ll stress out for minimal gains.

Instead, he argues trading is a fantastic way to learn about risk management, discipline, controlling your emotions, and discovering your flaws (like greed, fear, and impatience) that bubble up under pressure. If you do it with small enough money—money you can afford to lose—it becomes an invaluable crash course. But if you’re in it just for the cash? Probably not the best plan, unless you truly want to be a full-time trader.

Gold isn’t automatically safe

We touched on gold, because that’s the classic question when markets feel shaky. Abid pointed out how in 2008, even gold initially tanked about 30% in USD terms. Of course it recovered later, but that first plunge caught a lot of “gold is safe” people off guard.

He’s not against gold, but he said if we face a really deflationary shock, all assets can drop together at first. For Indians, the rupee weakening can offset some of gold’s price moves, but it’s still not guaranteed to be a smooth ride. His bigger point:

Don’t assume any single asset is bulletproof in a crisis.

Focus on your main hustle

I obviously asked him what I can do right now to boost my future returns. He basically said: “Forget trying to beat the market with 1–2 lakh rupees. You’ll make more money from improving your career prospects, or building a solid skill set, or exploring a side project that can scale.”

If you still want to learn markets, that’s cool—just don’t bet the farm. Keep an SIP going, or invest in safer avenues, or trade tiny amounts to understand how it all works. But he said a lot of times, young investors expect to double or triple small trading accounts, and that’s where the blowups happen. The better approach is to keep your biggest focus on your actual job or startup, which can hopefully multiply your income far more than a short-term trade ever could.

Hope you enjoy this conversation as much as I did 🙂

Is he giving caution about trading only or both trading and investment?