A new chapter in the delivery wars

Speed ahead or stop to think?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Delivering differently: Q4 at Eternal and Swiggy

Do India’s midcap IT firms see a gold rush?

Delivering differently: Q4 at Eternal and Swiggy

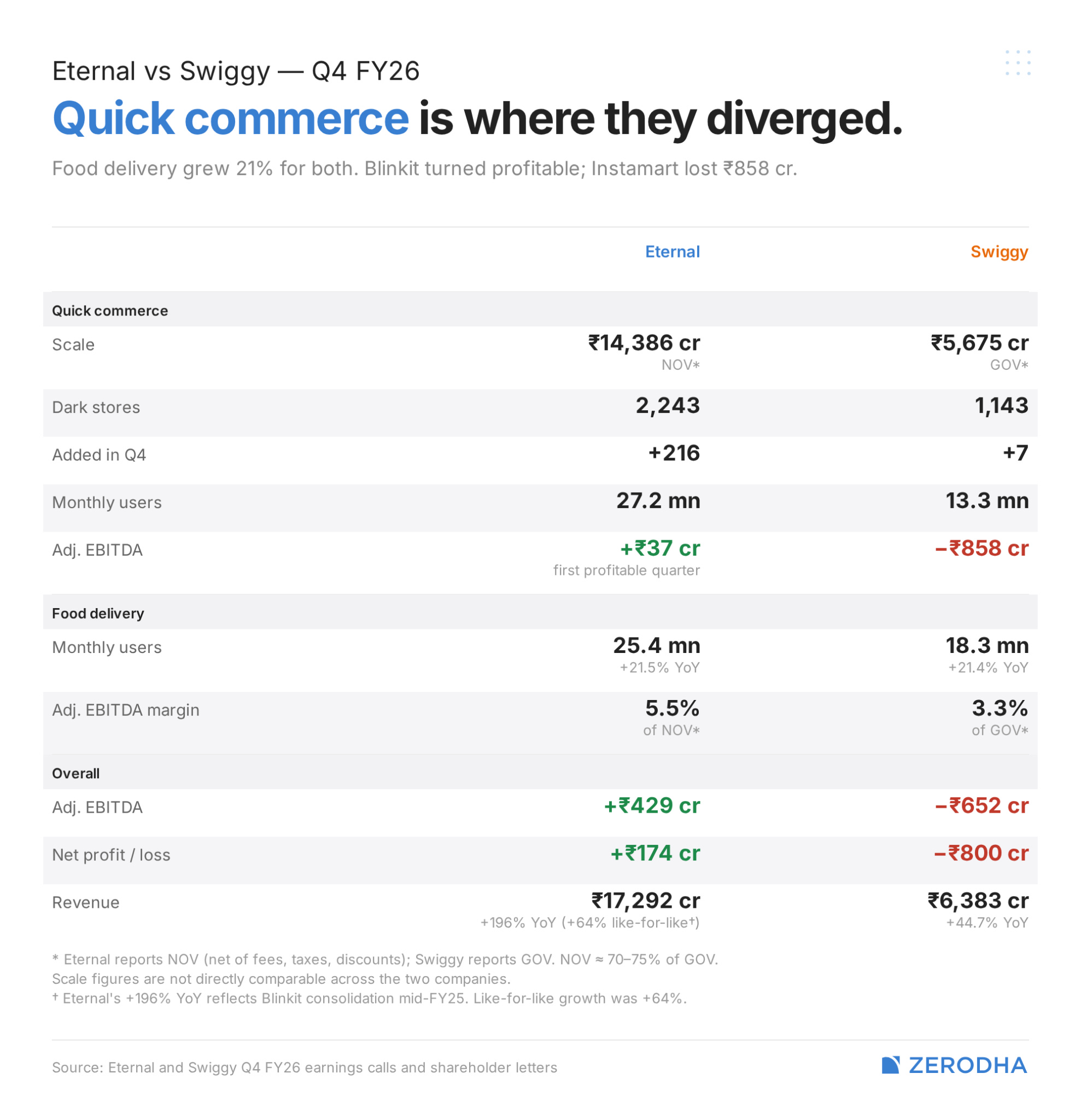

Eternal just crossed a milestone. For the first time since its acquisition, its quick commerce arm, Blinkit, had more monthly transacting users than Zomato. Last quarter, 2.72 crore different users used Blinkit every month, against Zomato’s 2.54 crore.

Meanwhile, over at arch-rival Swiggy, the same quarter showed the opposite tilt. Its food delivery arm posted its strongest growth in nearly four years, while quick commerce slowed. In fact, its dark store network grew by just seven stores — against Blinkit’s 216.

India’s two listed giants in hyperlocal commerce, it appears, are beginning to move in opposite directions. And yet, interestingly, both posted what amounted to one of their best quarters in years. What we’re seeing, perhaps, are the first signs of an industry filled with hyper-growth start-ups finally settling into a shape.

Where things stand

Both companies posted rather strong numbers last quarter.

Eternal’s numbers, in fact, look exaggeratedly good. It reported a revenue of nearly ₹17,300 crore, which was almost 200% higher than its revenues from the same quarter last year. Similarly, its net profit, at ₹174 crore, was nearly four-and-a-half times what it had earned a year ago.

Those incredible numbers, though, come with caveats. That wild revenue jump is largely an accounting artefact. In the first quarter last year, Blinkit went from a “marketplace model” — that is, it sold goods for third parties, and only booked commissions — to an “inventory-led” model, where it owns the stock and books the full value on every sale. Even once you strip that out, though, its like-for-like revenue grew at a still-incredible 64%.

Swiggy had an exceptional quarter too, though not one as stellar as Eternal’s. Its revenue came to ₹6,383 crore, up 45% year-on-year. The company is still making losses, but its net loss for the quarter narrowed substantially — to ₹800 crore, from nearly ₹1,100 crore this time last year.

For both companies, this was a strong end to a year otherwise marked by heavy expenditure. Despite its strong showing in the March quarter, for instance, Eternal’s full-year profit declined by about 30% year-on-year, bearing the weight of heavier depreciation and finance costs. Similarly, across the full year, Swiggy’s losses widened by about a third — given how it spent most of the year carrying out heavy investments in Instamart.

Food delivery: a mature business

Something’s changing with the food delivery business. These arms of both companies no longer behave like explosive, volatile start-ups. Instead, they seem quiet, and perhaps even predictable.

Zomato’s food delivery for the quarter grew 18.8% year-on-year, measured by ‘net order value’ — to a great extent because it had one-fifth more users over last year. This was the company’s third consecutive quarter of acceleration, after its growth bottomed at little over 13% last June. Its margins, meanwhile, held at a healthy 5.5% of its net order value.

At Swiggy, food delivery grew 22.6%, measured by ‘gross order value’ — a slightly different metric from Zomato. That’s the fastest it has grown in 15 straight quarters. Like Zomato, Swiggy too had over one-fifth more users than last year. Meanwhile, its profitability went up to. Its EBITDA margins rose to 3.3% of gross order value — a lifetime high.

Frankly, the two businesses are starting to look rather similar. They’re growing revenues somewhere between the late teens and the early twenties. Both are on-boarding new users at roughly the same pace. Both guide 5–6% EBITDA margins in the medium term. They’re both growing businesses, but they’re no longer start-ups that defined a generation. Instead, it appears, they’re slowly turning into boring cash cows.

If there’s one difference, though, it’s what they’re building around that core business. Over recent quarters, Swiggy has launched a series of specialised propositions inside its food delivery app. Bolt, which offers 10-minute deliveries from restaurants near each customer, now makes up over one-tenth of Swiggy’s food delivery volumes. It has other less known propositions, from 99-Store — for budget-conscious customers — to Food on Train, which gets food to your train journey. Put together, all these initiatives make up a quarter of Swiggy’s food business.

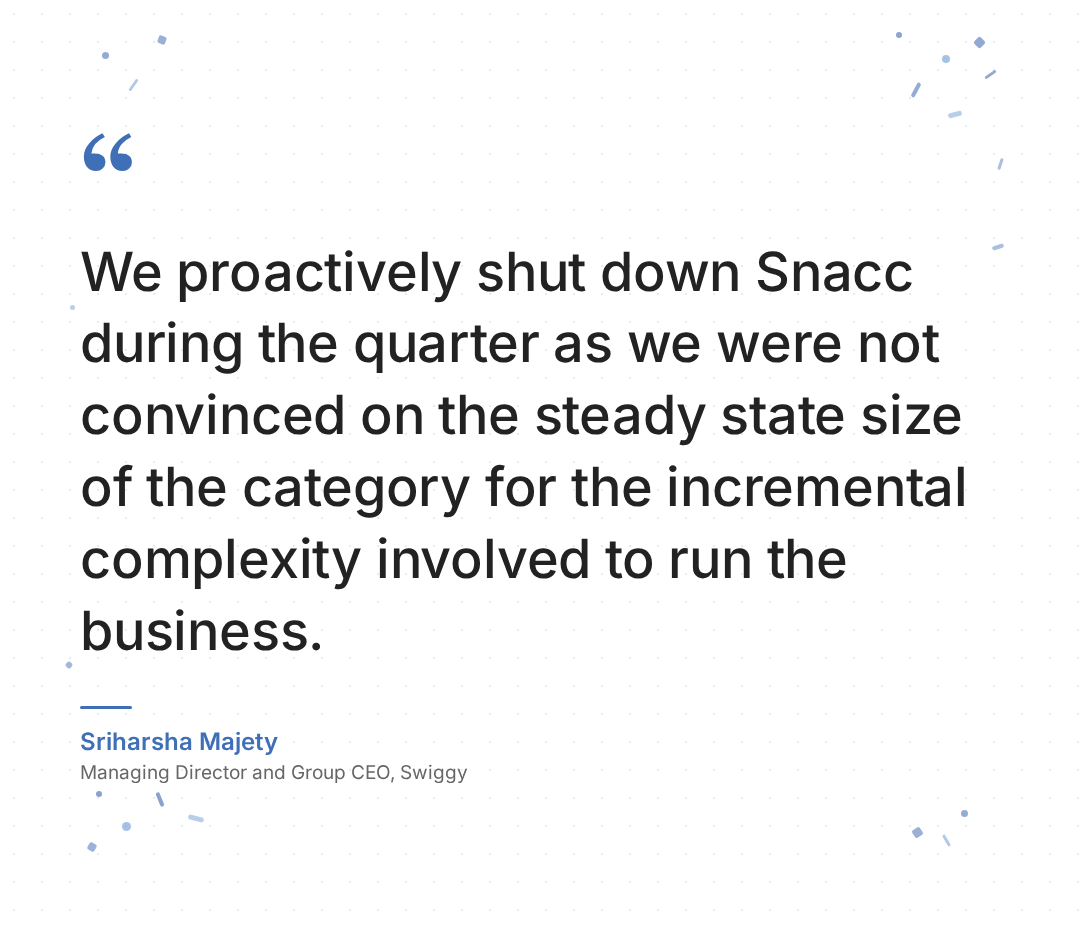

Of course, many of these experiments went nowhere. This quarter, for instance, Swiggy shut down Snacc, its micro-kitchen experiment. The category, according to its management, just didn’t seem big enough for how complex it was to pull off.

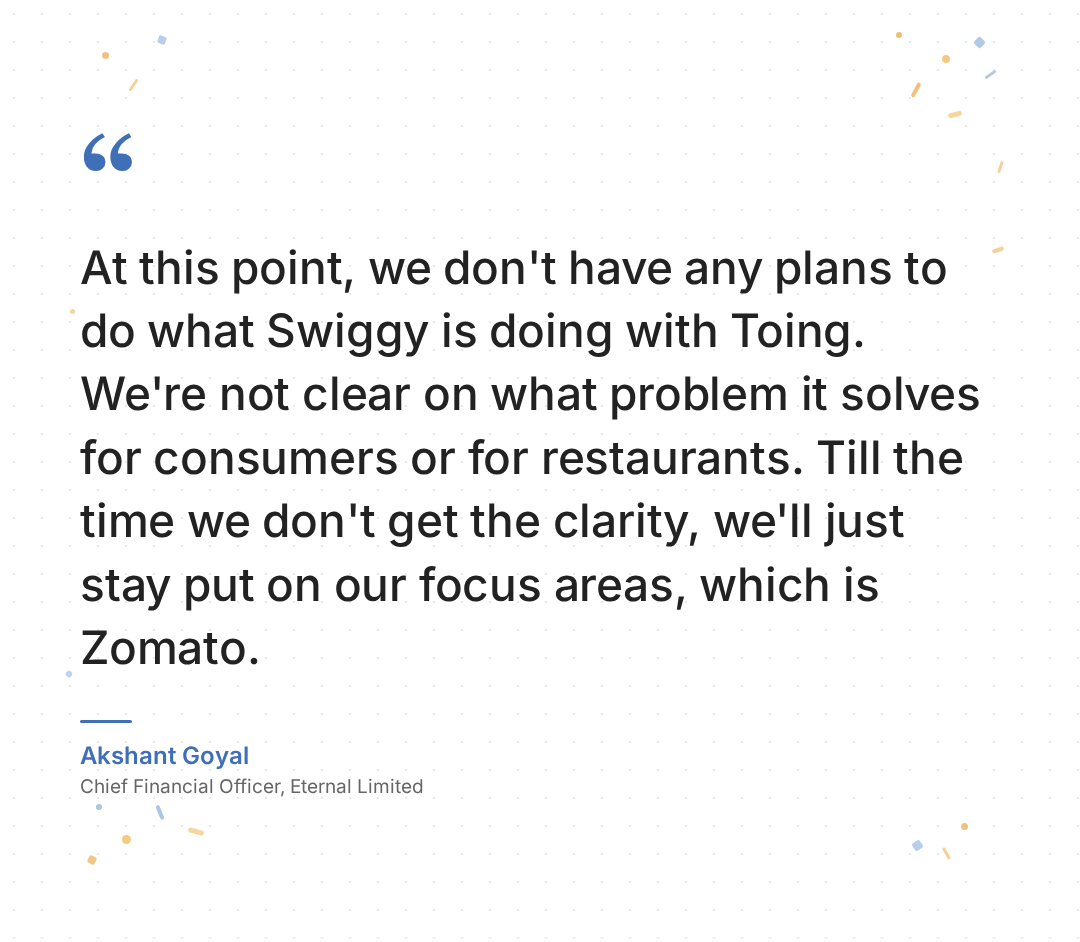

Eternal is more conservative. In fact, it sounds skeptical of the direction Swiggy is taking. When asked whether the company would replicate Swiggy’s ‘Toing’ — a new marketplace for affordable restaurants — CFO Akshant Goyal flatly refused, claiming he simply couldn’t see what problem Toing solved.

This is beginning to look, almost, like a difference of strategy. One company experiments extensively and prunes out whatever isn’t working. The other waits for clarity before making changes. The outcomes seem similar — both run food delivery businesses that grow at similar rates and earn similar margins. The path to getting there, however, looks very different.

Quick commerce, in three lanes

Quick commerce, however, is where the companies diverge.

Both companies rapidly grew their quick commerce offerings. Blinkit’s ‘net order value’ rose by more than 95% year-on-year, last quarter, to roughly ₹14,400 crore. Instamart’s ‘gross order value’ grew rapidly as well, by over 60% — but its total quick commerce business is just one-third that of Blinkit, at under ₹5,700 crore. Blinkit also hit its first profitable quarter, based on its ‘adjusted EBITDA’ — making a small profit of ₹37 crore. Instamart, in the same period, bled ₹858 crore.

Blinkit is growing much faster too. It added 216 net new dark stores this quarter, to an overall tally of 2,243. Instamart has just half as many stores — at 1,143 — and it could only add seven last quarter.

But curiously, each order on Instamart seems to yield much more revenue than Blinkit. Its average order value was ₹700. Blinkit’s was much lower, at ₹525.

These no longer look like the same business.

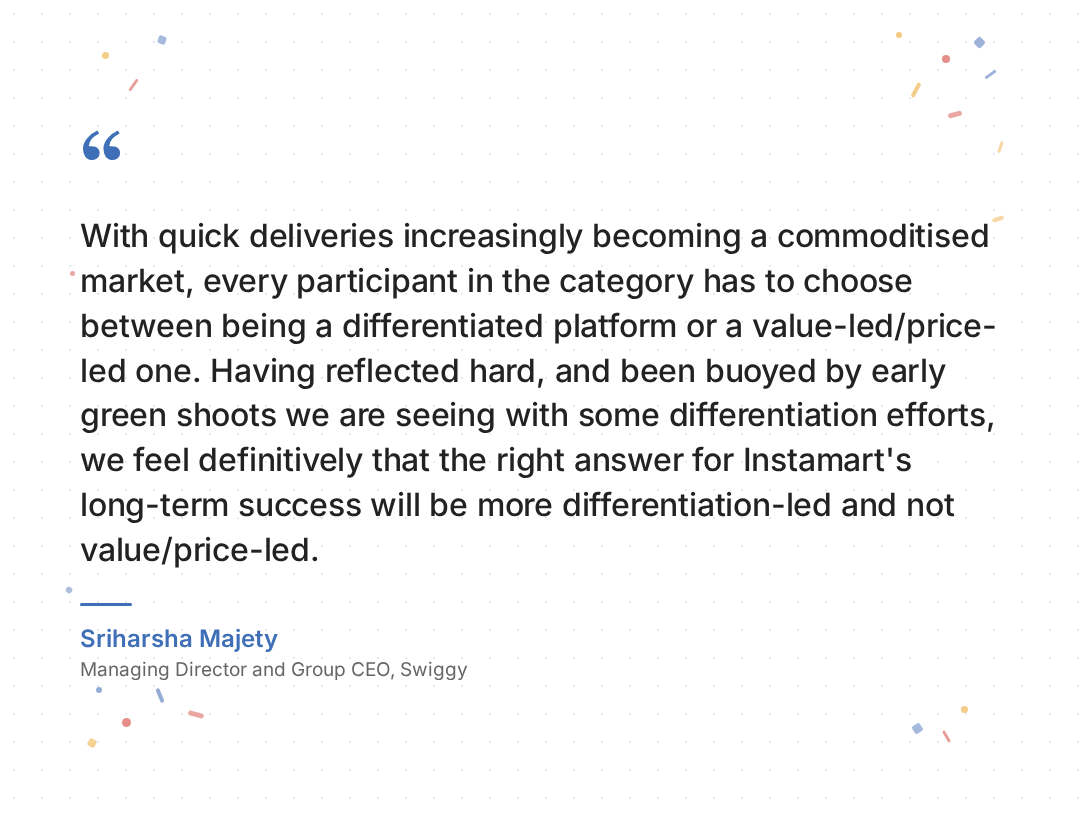

This isn’t entirely by accident. As Swiggy’s CEO, Sriharsha Majety, noted in his shareholder letter, quick delivery has become a commoditised market. Every player now has two choices to get ahead: differentiate, or offer better value. Swiggy decided on differentiation.

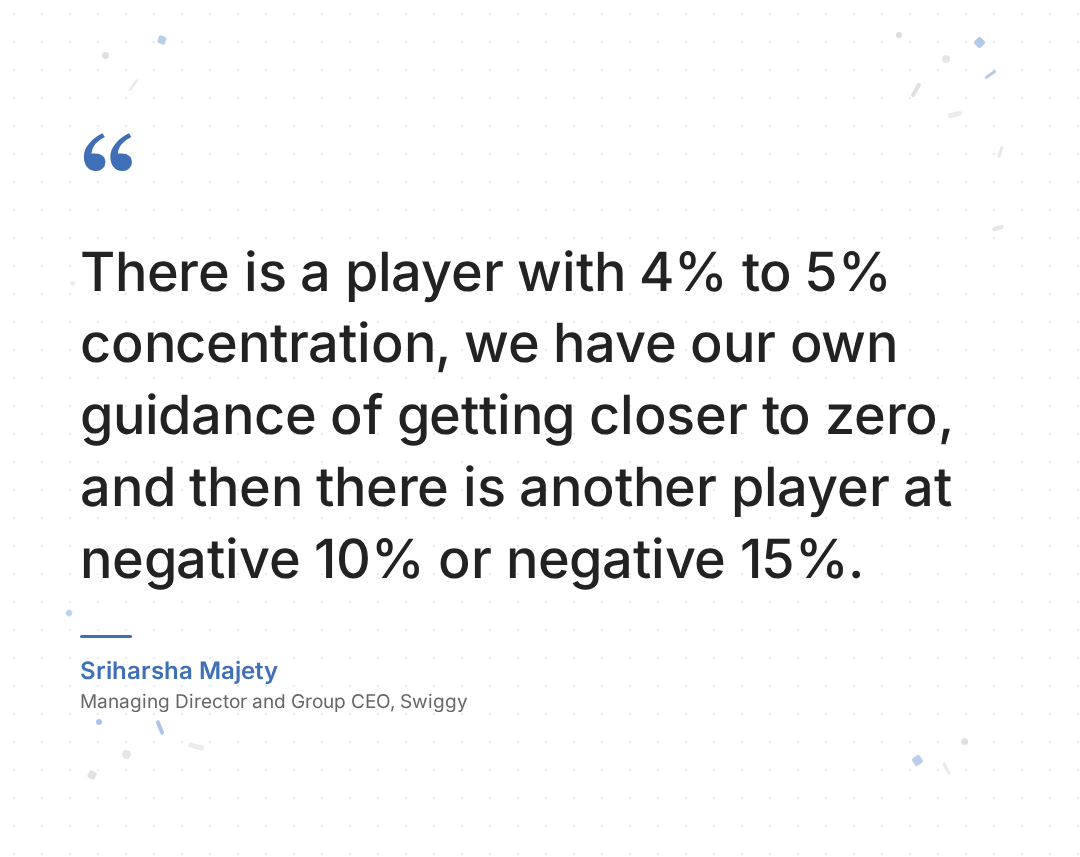

As he put it, India’s three quick commerce giants — Blinkit, Swiggy, and Zepto — are maing three distinct choices. One player — likely Blinkit — is operating at around 4–5% contribution margin. It has arguably become the industry’s incumbent, with both scale and density, and an inventory-led model that lets it manage margins directly. Swiggy’s approaching break-even. A final one — perhaps Zepto — is at roughly negative 10–15%, still pursuing aggressive growth through losses.

Swiggy’s strategy, it appears, is to grow slowly, but move up-market. Consider Noice, its clean-label private brand. Unlike other private label brands, Noice is going premium: high-protein eggs, low-preservative bread, tri-ply cookware. This isn’t for easier profitability — as Sriharsha puts it, Noice is “not a margin-maximising equation”. Its job is to differentiate Instamart, and make it sticky.

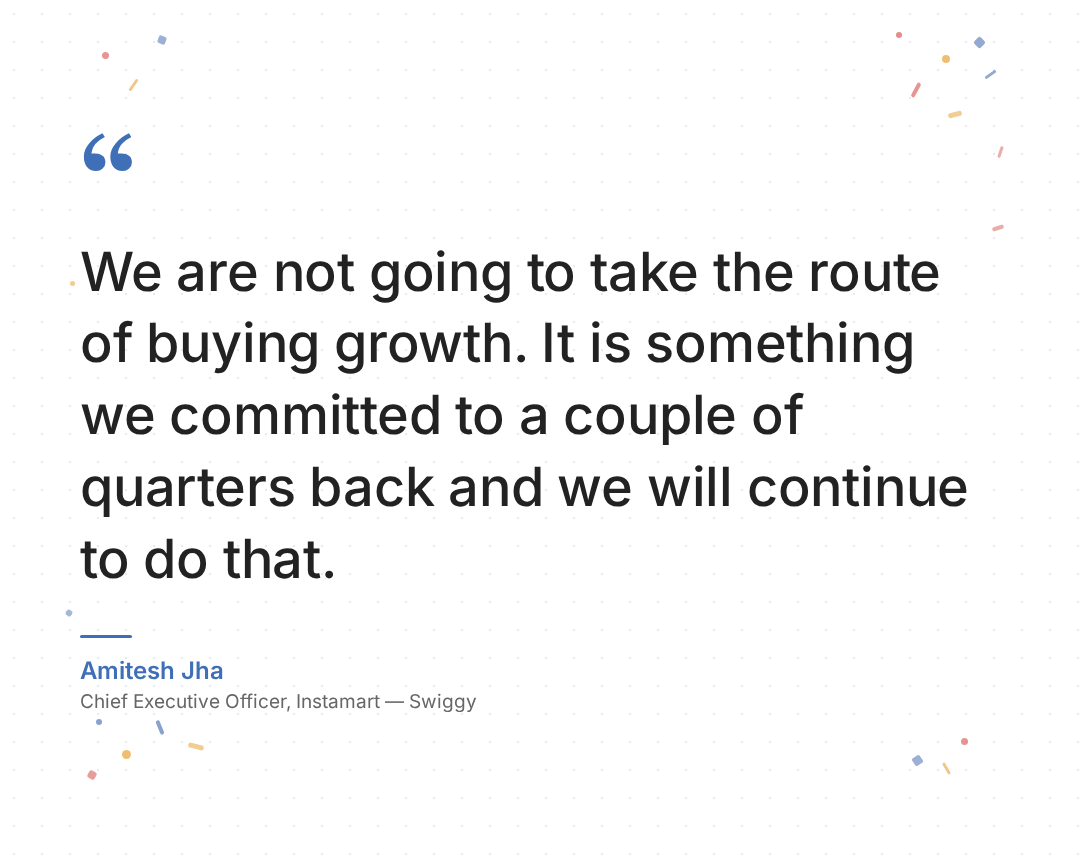

To the company, this marks an attempt at being ‘disciplined’, instead of trying to buy growth.

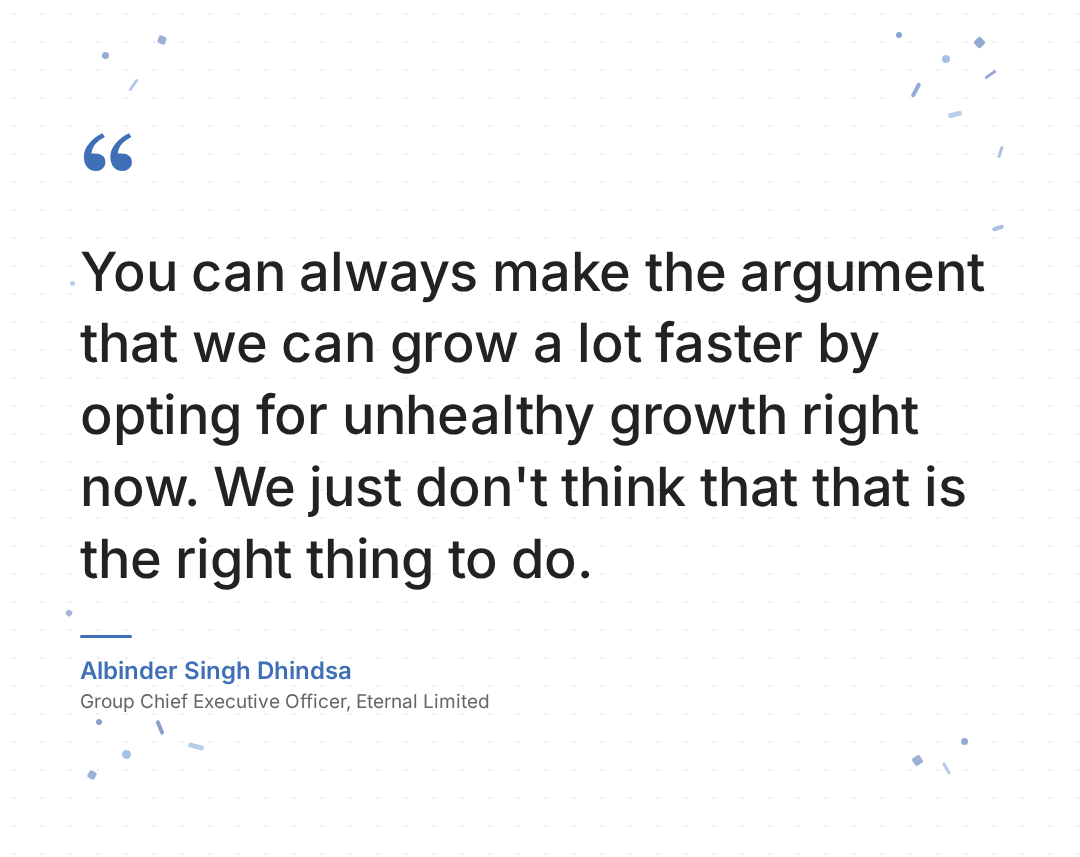

On paper, Eternal’s posture is the same. But what it means by ‘discipline’ is very different. Unlike Swiggy, it’s trying to scale rapidly, but without sacrificing profitability. It believes it can add hundreds of stores and still be conservative. Swiggy’s additions, meanwhile, are in the single digits.

The third lane — that of Zepto — will soon become publicly accountable as well. The company just received in-principle approval to file for an IPO. When it’s finally through, all three of India’s major quick commerce players will have their information out in the public for anyone to see.

What actually pays

There’s another curious development in quick commerce. Companies no longer think they have to stick to deliveries to find profitability. Instead, they’re turning to advertising within their apps — or what the industry calls “retail media”.

Retail media can look like many things: sponsored search results, the brand-specific banners you see on the app, or the little gift boxes you occasionally get with samplers from different companies. It’s a sensible bargain for a brand. If you’re on a quick commerce app, you already want to spend your money. This just nudges you towards a particular brand’s products.

This is why retail media is exploding. India is projected to spend ₹6,000 crore on quick commerce ads this year, a number that’s growing at roughly 22% a year. This has become a massive profit lever for quick commerce firms. Where the economics of delivery, itself, is horrible — with poor margins, and high delivery fees — advertising revenue is practically pure upside.

This is especially lucrative, today, because of artificial intelligence: which allows one to target ads almost perfectly to a consumer. Eternal, for instance, claimed that it simply didn’t know if there was a limit to how much ad revenues would eventually add to its revenues.

Most of that money comes from brands that already list on the platform. That is, when someone advertises through a quick commerce platform, it gets paid twice — first, for the ad, and second, for the delivery.

This adds a new dimension to why premiumisation could be an interesting model to pursue, in this industry. If you can focus exclusively on high value customers, your reach as a delivery platform might suffer, but as an ad platform, you’re actually better off.

Where this leaves things

A year ago, both Swiggy and Eternal looked like mirror images of each other. Both were food delivery giants, burning capital on unending dark store rollouts. Both were extending, in roughly the same way, into adjacent categories.

Now, they look like they’re pulling away from each other.

Eternal’s centre of gravity has moved to quick commerce, where it has more users than for food delivery. It’s investing heavily in this network, opening 216 new stores in a quarter, and that bet seems to have paid off — after all, it just printed its first profit. Swiggy, meanwhile, remains a food delivery company, first and foremost. But it’s making interesting choices with quick commerce, slowing down and betting on differentiation, rather than trying to take Blinkit on by the horns.

Which approach wins the long term? That’s what we’ll be looking at in the quarters to come.

Do India’s midcap IT firms see a gold rush?

Since the second quarter of FY26, we began splitting up our coverage of Indian IT’s quarterly results into the largest companies and the midcap ones. After all, while being in the same industry, the performance of both sets of companies couldn’t be more different, as India’s midcap IT firms were outrunning their larger rivals.

The thesis was that smaller, nimbler companies could use AI to win transformation work that large firms like TCS and Infosys, which have far more organizational drag, couldn’t move quickly enough to capture.

The Q3 FY26 results confirmed it. And so did Q4, where the AI play became more visible. In today’s story, we’ll be looking at three midcap companies: Persistent Systems, Coforge and KPIT Technologies — and what they’re saying about their year.

The numbers

Before we get into the structural forces at play, let’s break down the numbers. Please note that all growth figures are in dollar terms unless specified otherwise.

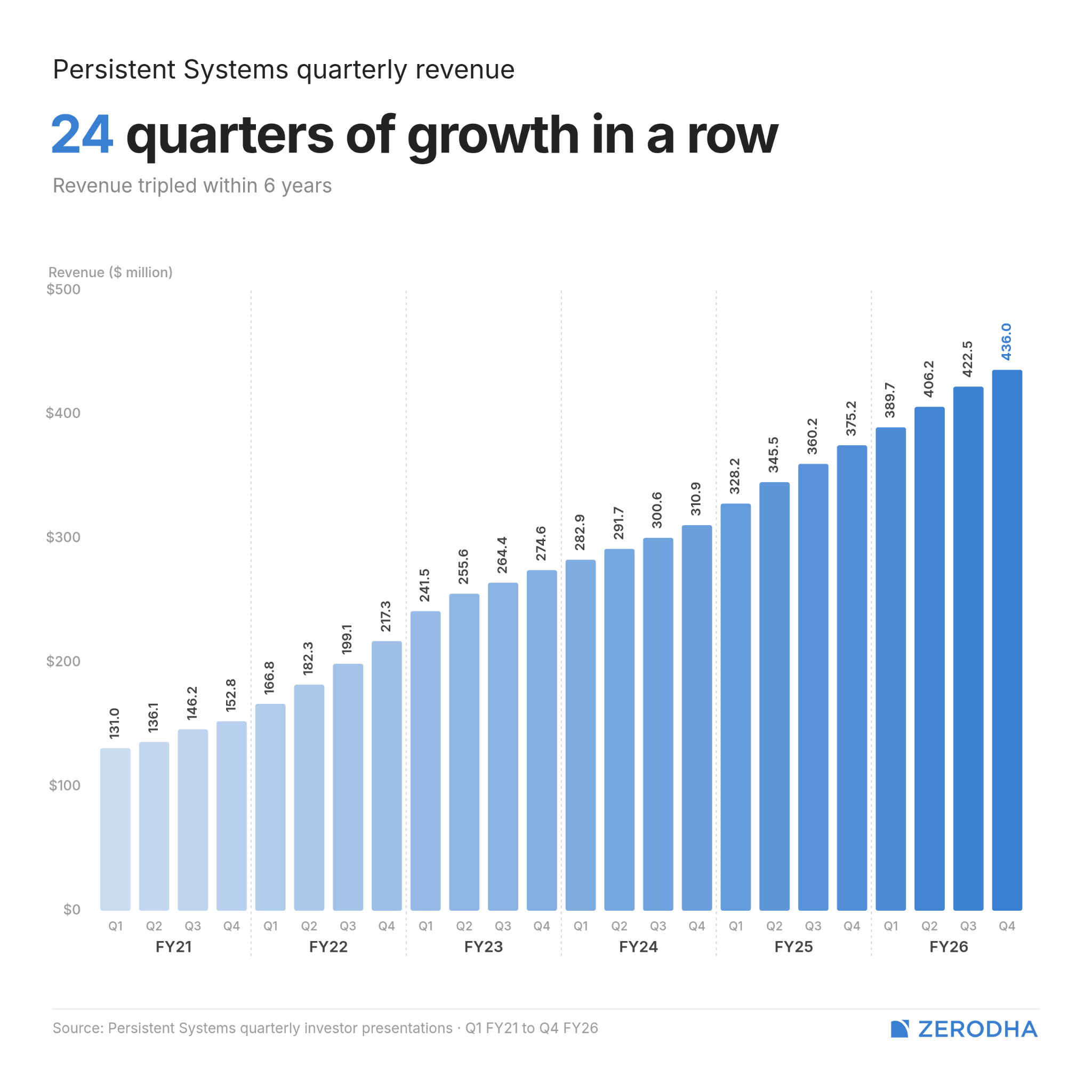

Persistent closed FY26 with $1.65 billion (~₹14,800 crore) in annual revenue, growing 17.4% year-on-year. It delivered $436 million (~₹4,056 crore) in Q4 alone, which was 16% higher than Q4 FY25. This is its 24th consecutive quarter of sequential growth. EBIT margins hit 16.3% in the quarter, while the full-year EBIT settled at 15.6%.

Meanwhile, Coforge’s Q4 revenue came in at $489 million (~₹4,450 crore), up 21% year-on-year. Its total revenue for FY26 was $1.87 billion (~₹16,400 crore), which was 29.2% higher than the previous year. Its EBIT reached 16.6% in Q4 — the highest-ever quarterly margin. Their profit-after-tax this quarter has more than doubled.

KPIT, the automotive-focused IT services firm, reported $185 million (~₹1,711 crore) in Q4 revenue — its best quarter by revenue, up 12% year-on-year. Its EBITDA margins were maintained at 20.6%. However, the full-year picture was softer: total FY26 revenue grew only by 4.8% y-o-y in dollar terms to ~$725 million (~₹6,455 crore). Its net profit also fell by 33%, but not because of operational problems — rather, it was because of currency depreciation and loss of non-core sources of income.

First line of defense

In our recent podcast on Subtext with veteran IT professional Ameya P, we dove deep into why domain specialization is one of the likeliest moats as AI looks to disrupt the industry. He called it the answer to all the ways in which AI looks to flatten the old business model of Indian IT.

This quarter, we could see that exact sentiment made far more explicit by Coforge, which said that they see 6 moats in the AI age. In the order of importance, they are: domain specialization, client relationships, human-AI agent flexibility, agility at scale, a scalable AI platform, and an AI-enabled workforce.

Domain depth is the anchor around which all other moats circle, though. The reasoning is simple: generic AI skills applicable across the board are easily commoditized, but understanding how to use LLMs with enterprise context provides a massive leg-up in driving business outcomes.

For instance, 26% of Persistent’s revenues are made from healthcare. In its earnings call, it discussed how it streamlined early drug discovery for a pharma client. It helped the client streamline data from its siloed datasets, create a knowledge graph out of it, and then trained OpenAI’s GPT models on that structured data.

How does this help? Well, drug discovery is a very uncertain business because human biology is extraordinarily complex. A molecule that appears promising in early research often fails later in clinical trials. Researchers must navigate massive amounts of fragmented data while trying to identify which biological pathways are most likely to lead to successful drugs.

That’s where someone like Persistent comes into the picture. It ensures that the client has a second brain that they can easily tap into data, and can query an LLM on that data to find various possible answers to one question. And with this, Persistent is also building a repeatable solution that they can convert into their own proprietary AI platform.

That’s how, for instance, Persistent has embedded its SASVA platform across the software development lifecycle. Such a platform is often trained on the specific process logic of those industries, and with each client iteration, the product is improved. A generic coding copilot without this context, in comparison, may struggle to do the same.

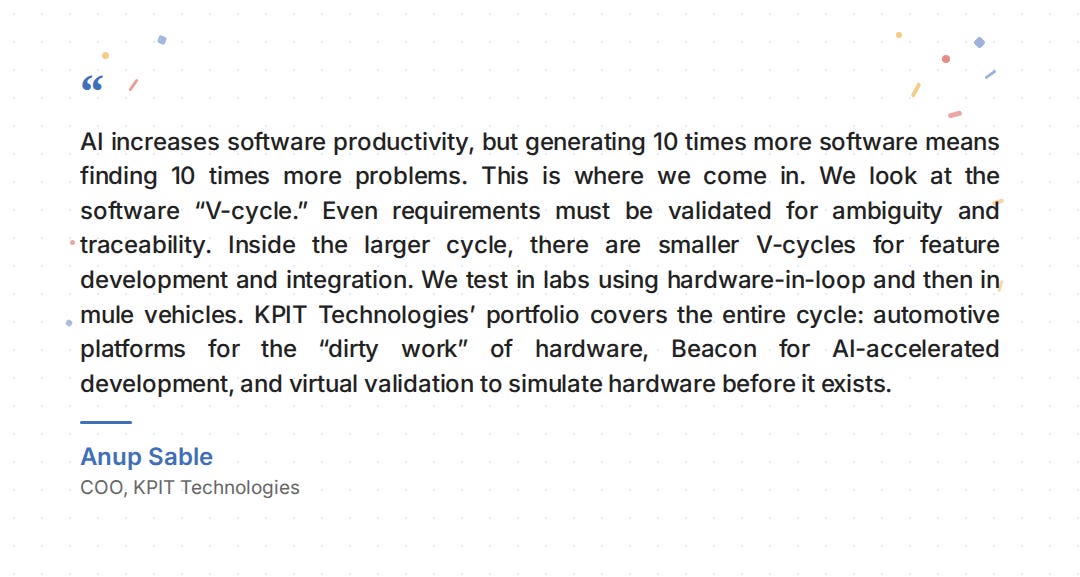

Similarly, KPIT has an IP called Beacon, which acts as an “AI harness”. In their view, while AI dramatically accelerates code generation, producing ten times more software means encountering ten times more integration bottlenecks. Moreover, unlike many of its peers, KPIT’s work focuses on building software solutions for complex hardware, which is a whole other ballgame.

Beacon is designed exactly to resolve defects in complex digital cockpits that a generic model would find much harder to navigate. And as we’d highlighted in our large-cap results story, physical AI is an emerging opportunity that KPIT is well-positioned to make use of.

Coforge, meanwhile, is the industry leader in travel IT services. It has a product called “Decisioning Atlas”, which is a knowledge graph layer that enforces domain-specific reasoning chains. This prevents a generic LLM from hallucinating by providing the rules and constraints within which, say, an airport operator or airline operates.

This proprietary grounding in specific industry workflows is what separates “applied AI” from horizontal AI skills, which commoditize far more quickly. Naturally, designing such applied AI solutions requires strong client relationships and an ability to move fast when things change.

The price of change

We all know by now that AI will render pricing as per headcount and manpower more irrelevant, as clients will demand more transparent, outcome-based pricing. In our coverage of the Q4 results of large-cap Indian IT, we took a look at where companies are in this transition.

Midcap companies, however, are progressing far faster in that aspect.

Take, for instance, KPIT. Over 80% of its new contracts are now fixed-price and outcome-based, with management actively converting the existing book toward a similar structure. In fact, in FY26, 65.4% of KPIT’s total revenue came from fixed-price contracts, up from 57.3% in FY25 — a very meaningful move in a single year.

Meanwhile, Coforge is executing this transition through what they call Mod Squads. The model replaces traditional headcount-based billing with a fixed monthly subscription for pre-built AI agent teams, where clients pay for a result rather than hours. For instance, their insurance underwriting squad has cut underwriting cycles by 50% for one client.

However, the million-dollar question that arises from this is: isn’t AI deflating your business in the short-term?

For one, it shrinks your old revenue. But secondly, with new technology, clients demand lower prices for the same outcome. And third, as companies compete heavily for the same contracts, the prices only go down further, passing productivity benefits back to clients.

Well, if the results of these companies are to be seen, that’s not the belief they hold.

Coforge CEO Sudhir Singh’s position on AI deflation is explicit: while AI-generated code is cheap to build, it is “expensive to own, secure, and maintain“. For players that combine domain depth with technical capability, agentic AI creates a massive recurring managed services layer that didn’t exist before.

Persistent’s CEO, Sandeep Kalra made the same argument from a different angle. He expects his firm to deliver faster outcomes through its proprietary AI platforms. That speed, he believes, will help him retain some margin improvement rather than pricing it away entirely.

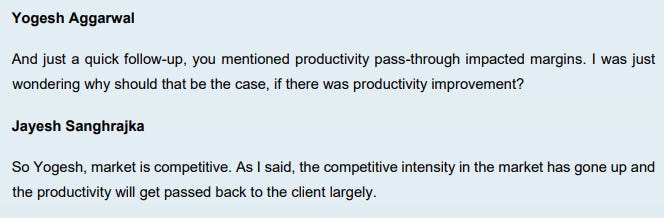

This, perhaps, is why, when analysts pressed Kalra on whether AI productivity gains get passed back to clients, he bluntly said that Persistent will not engage in a “race to the bottom“ by passing 100% of its platform-driven cost savings back to clients.

That’s the opposite of the narrative in large-cap IT: for instance, Infosys’ CFO Jayesh Sanghrajka, did admit that they were pressured to pass on benefits to clients in order to win market share.

There’s another important signal where the shift in economics is visible: in the headcount numbers.

Take Coforge’s example. Between Q4 FY26 and Q4 FY25, its revenue (in rupee terms) grew by 30%, while its employee costs only grew by 20%. Much of the gap between those two lines is likely AI doing work that would previously have required additional hires.

Risky business

Yet, even with strong numbers, the headwinds are real enough that none of these management teams is fully ignoring them. And we highlighted many of these risks in our first primer on the sub-sector.

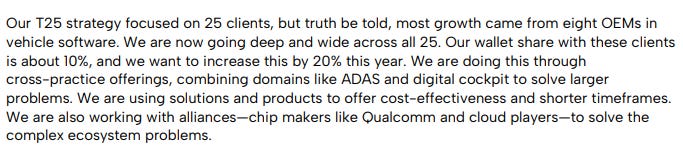

For one, diversification, or the lack of it, remains a structural risk for Persistent and KPIT. Persistent’s top ten clients account for over 42% of its revenue, and nearly 40% of its revenue comes from one category: the high-tech industry.

KPIT even admitted that while their strategy is meant to focus on their top 25 clients, most of their year’s growth was driven by just 8 automakers. In fact, their “strategic clients” drive around 85% of all their revenue.

By virtue of their unique business, KPIT’s situation is perhaps more acute. Two of its largest software-defined vehicle (SDV) programs are winding down by next year. If those programs had continued, KPIT would have seen an additional 4-5% sequential growth per quarter. However, they’re optimistic that they can eventually offset this with new deals.

But, the real issue is broader: across the world, the automotive industry is seeing a downcycle. In particular, European automakers, which make up a large chunk of KPIT’s business, are struggling. This, as we’d covered 2 quarters ago, is what also ailed Tata Elxsi, a more direct peer of KPIT than Coforge or Persistent.

Beyond this, though, geopolitics has created a strange, dark cloud over the heads of the industry as a whole.

For instance, Coforge suffered a loss of ₹140-150 crores on hedges as the rupee depreciated against the dollar. Additionally, due to the Strait of Hormuz crisis spiking oil prices, global airline Spirit Airlines had to wind down operations. This directly hurt Coforge’s margins, but the hit didn’t make a material difference to their otherwise solid quarter.

And since most cars still run on oil, KPIT also finds itself in the crosshairs of this crisis. They haven’t seen higher oil prices affect the spending of their clients yet, but are certainly worried if the situation persists over the next few months. What’s also worth noting is that, by KPIT’s own admission, their growth is not dependent on EVs.

Conclusion

The midcap IT business is riding tailwinds that are far more favorable than their larger peers.

Their strongest defense is their proprietary IP built on domain depth, which they combine with their lack of organizational bloat and ability to move fast.

But here’s the thing: as enterprise clients build more in-house AI capability, and with each new LLM development, clients’ patience for premiums based on “domain expertise“ might actually compress. There is still little visibility on a definitive AI moat. For KPIT in particular, the priority is more immediate, as they also try to navigate headwinds in a sector that’s struggling globally.

Yet largely, their answer to AI deflation has been what any company can and should do in the face of a technology disruption: invest in innovation, then commercialize the innovation fast.

Tidbits

[1] Hyundai India plans ₹7,500-cr capex for FY 2026-27

During its recent earnings call Hyundai Motor India plans to spend ₹7,500 crore in capital expenditure and will roll out a new mid-size SUV, and a localised electric compact SUV this year. Hyundai expects its domestic sales and exports to grow by 8-10% in FY27.

Source: EconomicTimes

[2] Rupee logs sharpest fall in a month as crude oil runs hot over US-Iran stalemate

The Indian rupee endured its sharpest drop in more than a month on Monday to end at it weakest closing level on record as a run-up in crude prices battered the currency after U.S. President Donald Trump rejected Iran’s response to a U.S. peace proposal.

Source: Hindu BusinessLine

[3] Sebi proposes additional measures to strengthen buyback framework

The Securities and Exchange Board of India (Sebi) has proposed additional measures to its earlier proposal of reintroducing open market buybacks through stock exchanges after consultation with the Primary Market Advisory Committee (PMAC).

Source: Business Standard

- This edition of the newsletter was written by Pranav and Manie

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Very timely and insightful analysis especially when there’s likely backlash building up against food delivery apps.

Delivery did not need Silicon Valley “disruption.” Like rideshare apps and taxis, delivery apps leveraged Venture Capital to create a marginally more convenient service where one already existed. In the process, delivery apps shifted consumer behavior and undermined a longstanding and once-sustainable business model.What’s more, delivery apps do not always deliver a better experience.

In his forthcoming book, Against Convenience: Embracing Friction in an Age of Endless Ease, journalist Gabe Bullard argues that delivery apps can claim to make our lives easier, while actually threatening our long-term physical and mental well-being.

“We’re surrounded by tools, gadgets, apps, and schemes that claim to save us from needless effort and undue stress,” he writes in the book’s introduction. “If our so-called conveniences do save time, money, or energy, the savings are short-lived, while the costs linger. These costs are paid in dollars and in the degradation of daily life.”

(source - https://time.com/article/2026/05/08/why-i-quit-food-delivery-apps/ )