A household name in your kitchen is going public

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

MTR takes to the bourses

How does Indian IT grade this quarter?

MTR takes to the bourses

Orkla India is an odd company to assess.

It is a subsidiary of a Norwegian consumer products giant, with a foot in everything from seafood to fabric conditioners. Orkla India, though, runs the most Indian of businesses: selling masalas. And its history, too, is characteristically Indian — touching everything from the rise of Udupi restaurants to the emergency.

Orkla began its life as an off-shoot of Bengaluru’s legendary Mavalli Tiffin Rooms (or MTR) restaurant chain — which recently completed a hundred years.

The restaurant chain is legendary in its own right; it is one of the most prominent bastions of Udupi cuisine in the city. But in the 1970s, a quirk of history forced it to enter the packaged foods business as well.

In 1975, during the emergency, the government imposed the Food Control Act. The law forced a price cap on restaurants. Suddenly, the restaurant could no longer stay profitable while maintaining its standards. And so, briefly, it was shut. To stay afloat, instead, its founding family — the Maiyas — started selling sambar and rasam powders, as well as a variety of instant mixes, from a nearby building.

The emergency would eventually end, and in a few years, the restaurants would be back. But this new business was here to stay. In the 1980s, the two business lines were split between two brothers in the second generation of the Maiya family — with the packaged foods arm going to Dr. Sadananda Maiya and his relatives. It would stay with them till 2007, when it was sold to Norway’s Orkla group for $100 million.

Orkla India is now planning to list its stock. And that gives us a window into a business we hadn’t really thought too hard about before.

A more sophisticated food industry?

Broadly, Orkla operates in two industries: it sells spice powders, and what it calls “convenience foods” — ready-to-eat food, ready-to-cook, frozen food and the like. In both these lines, it’s making the same bet: India’s food market is going to change.

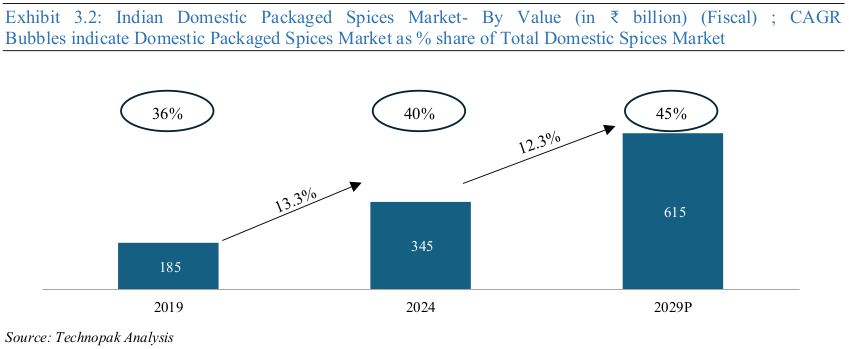

Take spices. Traditionally, people bought loose, unbranded spices from local markets, making the spice trade a heavily local, undifferentiated business. But as India urbanises, and people have more disposable incomes, they’re increasingly buying packaged spices. Orkla expects that, from a market of ₹34,500 crore today — 40% of the total spice market — the packaged spices market will nearly double to ₹61,500 in the next five years, making up 45% of the market.

This opens up new possibilities. For instance, instead of buying individual spices and mixing them at home — a matter of great skill — people are moving to blended spices, like sambar masala or pav bhaji masala, that can make cooking easier and more intuitive. That’s a value-add that local traders might find harder to get right. The market for these, alone, could double over the next five years, from ₹11,500 crore to ₹23,500 crore.

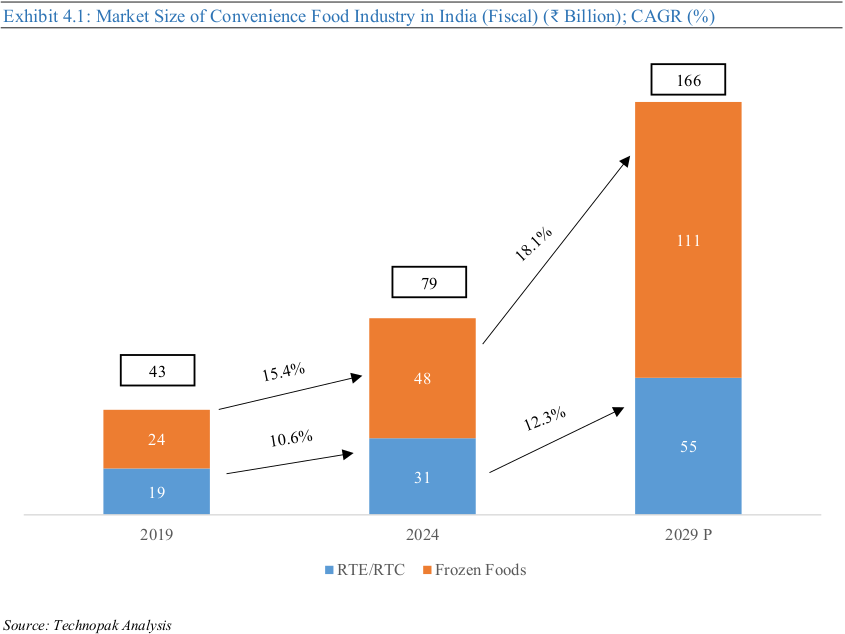

Convenience foods, meanwhile, could see even more dramatic growth, as a simple outcome of changing lifestyles. For now, this is a relatively small market. But across the world, as countries grow richer and more urban — and as women start working — people look for food that’s easy to whip up. India, too, is getting to that point. This could super-charge the segment’s growth. Over the next five years, in fact, Orkla expects the ready-to-eat / cook market to grow by over 12% a year, and the frozen foods market by 18%.

But while the industry may change, what people like to eat remains remarkably consistent. This gives the industry a distinctly regional flavour. Brands cater to distinctly regional preferences. And so, when it comes to a business like spice, India isn’t one market, but a variety of regional markets.

That can turn into a moat, however: even if people migrate away from a region, in their food preferences, people still turn home. Indians in the Gulf, for instance, or Indians from the United States, still buy spices from Indian companies. Last year, India exported ₹2,300 crore of branded, packaged spices to places with a large Indian diaspora. This is a key channel for companies to leverage.

How Orkla runs its business

Understanding Orkla’s culinary universe

Orkla has two marquee brands.

The first is its legacy brand, MTR, which caters to South Indian, and largely vegetarian, food — like sambar powder, or puliogare masala. In 2021, however, the company also acquired the Kerala-based giant, Eastern. Eastern focuses heavily on non-vegetarian food, rounding out Orkla’s portfolio.

Roughly two-thirds of Orkla’s revenue comes from selling spices, both pure and blended. The rest of its business comes from convenience foods.

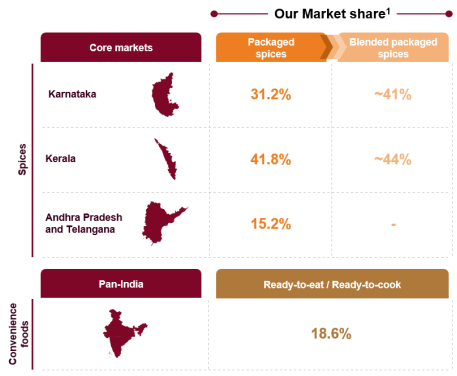

India has many spice brands. Some, like Tata Consumer Products, have a much bigger presence than Orkla. But Orkla has made South India its stronghold. It leads the packaged spices markets of Karnataka and Kerala. In fact, in these two states, it claims to be present in the kitchens of nine of every ten households. It has large presences in Andhra Pradesh and Telangana as well.

The secret behind this dominance is its deep local customisation. Consider the humble sambar. Every South Indian state has its own way of making sambar. Orkla understands this fact, and caters to each state with a different formulation. Its MTR sambar powder caters to customers in Karnataka; its MTR spicy sambar powder works better for Andhra and Telangana; its Assal Kayam Sambar Powder works best for Kerala sambar. That is, the company has turned its unique cultural understanding into a moat.

It’s also a major exporter, with one in every five Rupees in sales coming from abroad. Eastern, in fact, has been India’s most exported spice brand for twenty-four years.

The nuts and bolts

For its spices business, Orkla sources raw materials, turns them into powders, and packages them. It buys raw spices on temporary purchase orders, from the company’s network of 216 suppliers. Some of these links might be slightly fragile. For products like tamarind concentrate or asafoetida, for instance, the company has just a single supplier.

These raw spices go to one of its nine factories, where, these are cleaned up and destoned, and then sorted to ensure that the flavour remains constant. The sorted spices are roasted, powdered, and packaged. That’s what lands up in your kitchen.

This is a uniquely profitable business. Spices, at least in India, aren’t a luxury — they’re used daily, in each of a day’s main meals. And yet, they can command serious margins. Blended spices, in particular, can carry margins as high as 45%-60%.

The company’s convenience foods business is more complex. Here, it isn’t merely processing spices, but cooking entire meals. What it does, specifically, varies widely based on the dish it sells. But typically, these require considerable processing. The most complex, perhaps, are its ready-to-eat dishes, which must be cooked, batch-by-batch, in large industrial kitchens. This same complexity spills into other parts of the chain. Everything from packaging, to quality control, to transportation becomes more complex when you’re dealing with cooked foods.

Eventually, these packs make their way to the market. Most of its products are distributed through “general trade” — a mix of kirana stores, small kiosks, and the like. But increasingly, the company is shifting to newer ways of doing business. E-commerce and quick commerce is quickly becoming an important sales channel for the company. In just the last year, in fact, its sales through digital channels grew by 46.5%.

So far, this resembles any routine manufacturing business. What’s unique about this business, however, is its product development cycle.

There are few products where people are as discerning as they are with food. For both its spice blends and convenience foods, nailing the right taste is critical. That isn’t a simple matter — it requires a deep base of knowledge. Orkla, for instance, runs two ‘Cuisine Centers of Excellence’. The company sends its team of chefs on “culinary travels” to learn about different parts of South India, understand its many cultures, and collect recipes. Through this process, in total, the company has developed a repository of over 4,000 recipes.

The numbers

Orkla’s numbers convey a picture of growing operational discipline.

Over the last year, the company’s unit economics improved visibly. Its raw material costs dropped dramatically, as a percentage of its total income — falling to 47.8% in FY 2025, from 54.9% in FY 2024. And with that, its operating margins expanded from 12.8% to 14.5%. Now, this is partly because the price of spices — the company’s main raw material — deflated over the year. Those costs can rise again.

But there are other indicators of good health. The company has practically no debt on its books — with current borrowings of just ₹2.3 crore. It’s also spitting out cash remarkably quickly, with its working capital days shrinking from 36.3 days in FY 2023 to 21.4 days in FY 2025. These are marks of a quality FMCG business.

Not everything’s positive, however. Despite projecting a rapidly expanding market, the company’s own sales have been stagnant. In the last financial year, its company’s revenues grew by a mere 1.6% year-on-year. The revenues from its spices business actually fell over the year — from ₹1,591 crore to ₹1,571 crore.

To be fair, the company sold more spice by volume over the year — increasing the volume sold by 3.5%. The deflation in the price of spices didn’t just reduce the cost of Orkla’s raw materials — it also brought the company’s own prices down. That’s why the value of its sales looks diminished.

But 3.5% growth is hardly ground-breaking itself. It’s worth wondering if the company has much space left to grow, especially given its focus on a South Indian market that it already dominates.

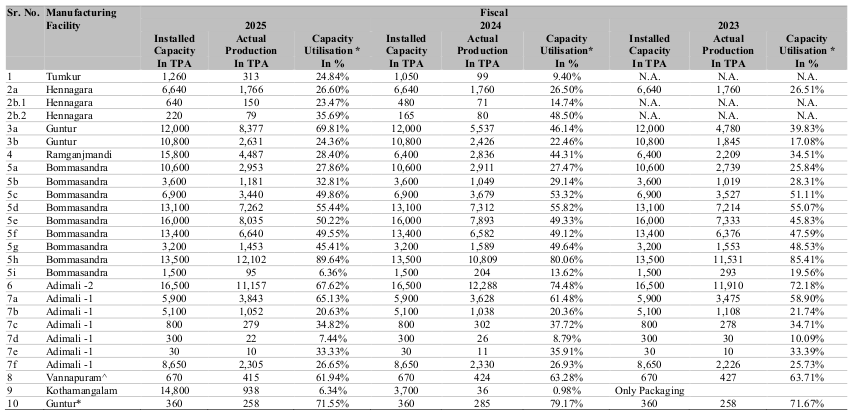

Even more worryingly, the company’s factories aren’t running at full capacity. Its capacity utilisation, in fact, sits at ~46%. And this marks a substantial degree of variation. While some lines have utilisation figures touching 90%, some are running at less than a tenth of their full capacity. Its confectionary unit at Laban, for instance, has consistently seen utilisation figures below 7%.

This could be a troubling sign. It possibly shows that the company hasn’t found the demand it was hoping for while setting up those factories.

The bottom line

In a season marked by big-ticket internet company IPOs, Orkla is an interesting stock market debutant.

The company has a distinctly local story. Instead of spreading itself across the country, it has built itself a regional fortress. Its key moats are intangible — its understanding of South Indian culture, and its encyclopaedic understanding of the tastes that mark this part of the world. But these moats, as its phenomenal margins and cash conversion record show, have helped it set up a formidable business.

But is Orkla a good investment? That’s the grand question. For all its claims, the company’s growth has been flat. There’s a noticeable slack in the company’s factories. In fact, this issue is a pure offer for sale — none of the IPO proceeds will fund any future expansion of the company.

So, where will the company’s next phase of growth come from? If you’re considering an investment, that’s the question you should ask yourself.

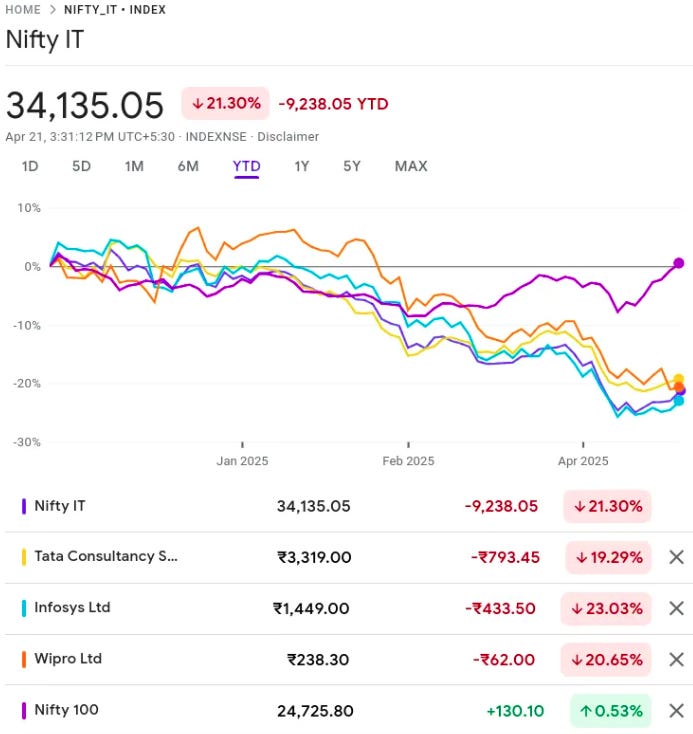

How does Indian IT grade this quarter?

It’s that time of the year again — the latest quarterly results are out for Indian IT companies.

In our last report card, we reported a dismal Q1 FY26 for Indian IT, where the story entailed large-scale firings, delayed wage hikes, and declining revenues. As we’ve highlighted before, Nifty IT has generally not been doing well.

However, the second quarter has been a little bit brighter for the industry, with results across the board being optimistic. The Nifty IT index hit its highest point since July 2024. But it’s what is beneath the results that really interests us. The industry overall has shown decent results, but some companies did much, much better than others.

This piece focuses on the largest IT companies—TCS, Infosys, and HCLTech. But very soon, in another piece, we’ll also cover some mid-cap IT companies that usually fly under the radar, but deserve just as much of your attention.

Let’s get into it.

(Quick note: we say “revenues” for Indian IT, we mean revenues in “constant currency”, i.e. adjusted for exchange rate fluctuations. This is because Indian IT is an export-heavy business that receives most of its payments in dollars.)

A welcome rebound

The last few quarters have been rough for Indian IT.

In Q4 FY25, many companies saw declines in their business in successive quarters — the first time this has happened since FY2021. Analysts have repeatedly reduced their expectations for how Indian IT will do each quarter — and IT firms might still miss those expectations. But this quarter fared much better in comparison.

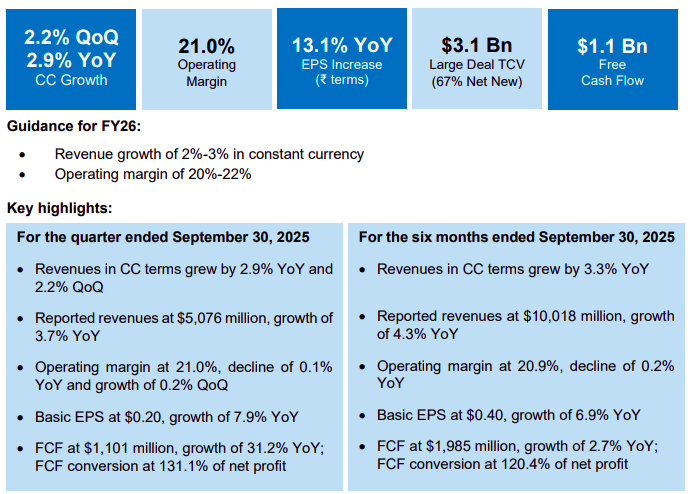

Let’s start with Infosys. Its revenues rose by 2.2% from the previous quarter, recorded at ₹44,490 crore. Operating margins continue to be steady at 21%, while net profit increased by 6.5% from last quarter to ₹7,364 crore.

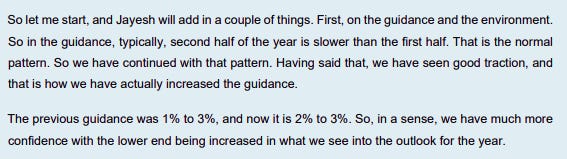

Now, the second half of the year is typically a bit muted for Infosys. But even then, Infosys has raised its expectations for how much their revenue will increase by the end of the year.

Then, there’s TCS, who, this year, had the worst first quarter they’ve had since the pandemic. However, this quarter, they have recorded a measured recovery. Revenue came in at ₹65,799 crore, up 0.8% from last quarter. Net profit reached ₹12,904 crore, a slight increase from ₹12,760 crore last quarter. However, it is worth noting that, compared to the same quarter last year, the company’s revenues continue to be lower. There’s no denying that in the last 12 months, TCS’ business has shrunk overall.

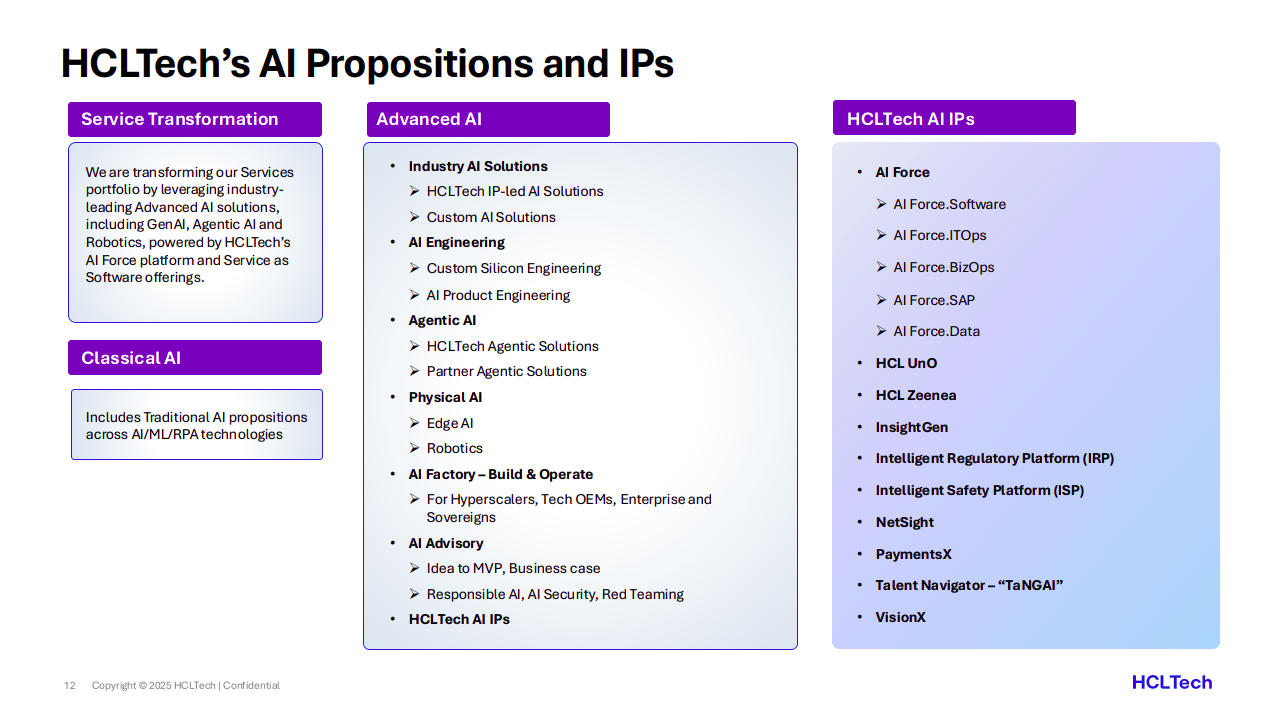

HCLTech recorded a really strong quarter, with revenues up by 5.2% from last quarter to ₹31,942 crore. Net profit stood at ₹4,235 crore, up 10.2% from last quarter while being flat compared to last year. However, this might not even be the highlight of their results. What is most notable is that HCLTech is reporting revenues from AI projects.

And that’s what we’re coming to next.

The first signs of AI adoption?

Every IT company has been talking up AI for the past year. In practice, though, they were stuck at pilot demos with no clear path to revenue. But this quarter, some firms gave us a clearer glimpse of how they’re actually adapting to the age of AI.

There are two ways in which Indian IT companies are approaching AI: one, they’re optimising how they function internally, and two, they’re trying to use it to improve client outcomes externally. Infosys and TCS mostly publicize the former, talking about how AI boosts worker productivity. Infosys credits its internal “Project Maximus“ — an AI-powered initiative — for helping expand margins. TCS launched what it calls the world’s largest internal AI hackathon. These are mostly small efficiencies introduced within the firm that don’t materially impact the revenue and margins.

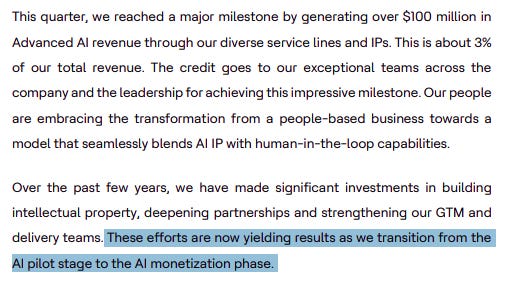

The real prize, however, is to bring in money for AI-enabled services. There, HCLTech has taken the first big step, announcing $100 million (or ~₹882 crore) in “Advanced AI” revenue. Not much, mind you — it makes up less than 3% of their total quarterly revenue — but it’s a start. More than anything, it’s a sign of progress that their AI products are finally beginning to make real money in the outside world.

What does “Advanced AI” mean? Well, HCLTech has built their own customized AI products that they are deploying for their clients. This also means that they’re investing in new assets — representing a slight departure from the asset-light business model that large Indian IT companies are known for.

Of course, these products currently form a small part of their portfolio. Just like their peers, they’re primarily a business that largely relies on putting lots of manpower behind IT maintenance projects. But their AI products mark a pivot, bringing in revenue from deals where AI, and not manpower, is the backbone of their offering.

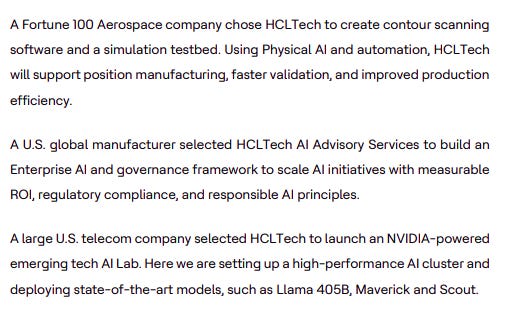

HCL has also pointed to the kinds of deals this entails. These are all interesting deals — from working with a public sector transport authority in Australia, to creating a way to detect boat congestion in real-time, to working with a US aerospace major on software for precision manufacturing.

Not that HCL is the only company with an AI presence. TCS, too, made a blockbuster announcement — it’s investing $6.5 billion to install 1 gigawatt of data center capacity in India. This is a massive departure for TCS’ asset-light model. The company traditionally maintained a return on equity over 50%, but that could change as it funnels billions into new infrastructure.

So, why is TCS doing this? This could be a defensive play. TCS wants to ensure it can offer clients sovereign AI cloud options, defending against AWS and Azure.

But it could also be a bona fide investment. While AI monetization as a whole is still far away, data centers in India have become a huge business in and of itself. If we are in the middle of an AI gold-rush, data centers are the shovel for digging that gold out. And TCS is buying a huge shovel.

The real AI action, though, is happening in midcap IT firms. But we’ll get to that in a different piece.

Hedging against the US

AI isn’t the only change these businesses are contending with. Indian IT is also trying to navigate a tariff and visa war kickstarted by the US.

By all accounts, they’re keeping their heads above water. Recently, we wrote about Indian IT’s dependence on the H1B visa for its offshore-onsite business model, and how the new H1B rules — which increased the visa fee from $5,000 to $100,000 — might impact the industry. We had surmised, then, that the impact of the change may be muted.

Turns out, that is indeed true. Our IT companies have been reducing H1B dependency for years with a variety of strategies, be it shifting their offshore-onsite ratio, increasing local hiring in the US, or even diversifying their business outside the US. All those moves seem to have paid off. The new H1B rules have hardly derailed Q2 performance for any of the bigwigs, with most of their business running on the back of their India-based workforce.

They’re also making active efforts to diversify the business regionally. Europe, in particular (including the UK) has been the brightest spot for many IT companies this quarter. Infosys, for instance, saw their Europe business account for over 30% of all revenue, after years of 5+% annual growth.

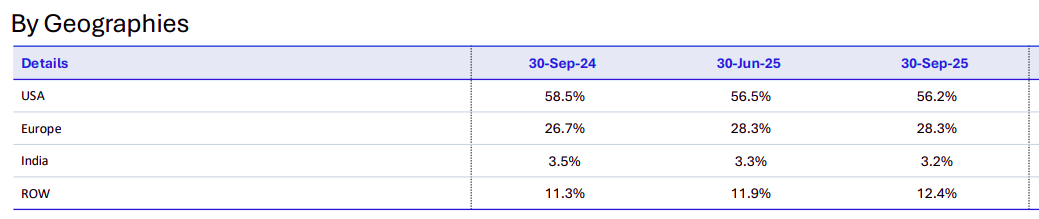

Europe also accounts for ~33% of TCS’ revenues, growing over 5% year-on-year. HCLTech’s Europe business has also jumped from making up 26.7% of the business last year, to 28.3% now.

On the other hand, North American revenues have been flat for many companies — despite making up over most of Indian IT’s business. Infosys saw its North American revenues fall by 1.1% from last year. For HCLTech, the decline was even worse — dropping 2.3% since last year.

Simply put, increasingly, Indian IT is banking on Europe to be a geopolitical hedge against new risks that come from the US. In a world that’s increasingly uncertain, this is a must-have.

Hiring and wage trends

Last quarter would have been terrifying for IT workers. Many companies had delayed wage hikes. Others had announced lay-offs. Amidst all the uncertainty, workers were left holding the short end of the stick.

But Q2 has marked a turnaround. TCS, for instance, has rolled out increments for 80% of its workforce. Despite this hike, its margins expanded, indicating better management of their costs. HCLTech has confirmed that wage revision will take place in the next quarter.

Hiring has shown a comeback. With the exception of TCS, every major firm added employees in Q2. Infosys led with 8,203 net additions—its largest quarterly hiring in over a year. And they will be hiring more.

HCLTech grew its workforce by 3,489 employees as well, while Wipro added 2,260 employees. To a large degree, this is cyclical—freshers who graduate in May-June usually join these companies by September-October.

TCS, however, hasn’t stepped into the job market. In fact, its headcount is down by nearly 20,000 people — or 3% of the workforce. While some of them left voluntarily, most were simply let go. TCS claimed it was clearing redundancies and skill mismatches — which means, possibly, TCS over-hired previously, and are now normalizing.

In fact, companies are getting selective about hiring. None of these companies are mass-hiring; they’re being selective, focusing on their AI, cloud and consulting lines. Where possible, they’re turning to their existing bench capacity to handle excess load. Infosys, for instance, upped utilization from 82% to 85% and is still there. TechCircle quoted an HR executive at a large IT firm, who said:

“Automation and GenAI are changing delivery models….the focus is on reskilling and hiring domain experts rather than scaling volume.”

Conclusion

In summary, the second quarter has marked a steady comeback for our largest IT companies. Both revenues and profits have been up. And we’re finally seeing first signs of the industry finally waking up to the AI opportunity.

However, does this indicate the start of a larger recovery? Indian IT has been stagnating for a few quarters, and some of this newfound growth comes from a lower base. We’ll need to see more before we can confirm that this is a resurgence. The more interesting story, meanwhile, lies in our mid-cap IT companies’ rip-roaring growth this quarter. But that’s for another episode.

Indian IT may not become obsolete in the age of AI. But beneath what seem to be stable results, the industry is certainly in a state of flux.

Tidbits:

Amazon plans to cut up to 30,000 corporate jobs, nearly 10% of its 350,000 corporate workforce, to reduce costs from pandemic overhiring and leverage AI-driven productivity gains.

Source: ReutersA New Zealand insurer, Maritime Mutual, facilitated billions in sanctioned Iranian and Russian oil shipments by providing crucial insurance to shadow fleet tankers, helping transport $18.2 billion of Iranian oil and $16.7 billion of Russian energy products.

Source: ReutersAxis Bank is selling its ₹511-crore debt exposure to bankrupt Lavasa Corp at a reserve price of ₹80 crore as lenders seek exits from the seven-year insolvency case hampered by ongoing litigation.

Source: ET

- This edition of the newsletter was written by Pranav and Manie

We’re now on Reddit!

We love engaging with the perspectives of readers like you. So we asked ourselves - why not make a proper free-for-all forum where people can engage with us and each other? And what’s a better, nerdier place to do that than Reddit?

So, do join us on the subreddit, chat all things markets and finance, tell us what you like about our content and where we can improve! Here’s the link — alternatively, you can search r/marketsbyzerodha on Reddit.

See you there!

Check out “Who Said What? “

Every Saturday, we pick the most interesting and juiciest comments from business leaders, fund managers, and the like, and contextualise things around them.

Introducing In The Money by Zerodha

This newsletter and YouTube channel aren’t about hot tips or chasing the next big trade. It’s about understanding the markets, what’s happening, why it’s happening, and how to sidestep the mistakes that derail most traders. Clear explanations, practical insights, and a simple goal: to help you navigate the markets smarter.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Great article....