A Dhan Dhana Dhan IPO for Jio

Plus: is India ready for the Super El Nino?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Brad Setser on the dollar and the world’s trade imbalance

The role of the dollar, and its influence on global trade, is a complicated story that has constantly changed over time. To make sense of all this, we spoke to Brad Setser, Most of Twitter knows Brad is one of the sharpest voices on all things balance-of-payments. He is a senior fellow at the Council on Foreign Relations. He also served at the US Treasury and the National Economic Council.

We recorded this conversation while the Iran war was unfolding and oil markets were watching the Strait of Hormuz, and not long after Trump and Xi had met in Beijing to negotiate a trade deal. We used the moment to ask him about the things he thinks about most: why the dollar is really strong, what an AI bust would do to it, how the manufacturing surpluses of China, Korea, and Taiwan quietly finance the American deficit, and what China would have to do to rebalance.

Watch the full podcast episode below, where Brad breaks down the sources of dollar demand and the future of global trade imbalances

You can also listen to the full conversation on Spotify and Apple Podcasts. The full transcript of the podcast is below if you prefer to read.

In today’s edition of The Daily Brief:

A Dhan Dhana Dhan IPO for Jio

Is India ready for the Super El Niño?

A Dhan Dhana Dhan IPO for Jio

If there was one thing that the Indian capital markets were waiting for with bated breath, it is the obviously bumper listing of Jio. They just filed their IPO papers with a fresh issue, meaning Jio is raising money for itself and not existing shareholders selling out.

As we covered just last week, NSE filed their papers too. Combined, the estimated issue sizes of both companies put together could be around ₹65,000 crore. These numbers wouldn’t have made sense a decade ago. It is impressive that our capital markets have become deep enough to absorb issue sizes like this.

Jio is essentially the reason why you are watching us today on YouTube, reading us on Substack or listening to us on an audio platform. It is the reason why a lot of companies, occupations, and internet economies exist today, not only in India but outside it. The momentous decision by Reliance to enter the market in 2016 with virtually-free data and talktime opened the floodgates for the Indian digital economy.

You probably know the rest of the story.

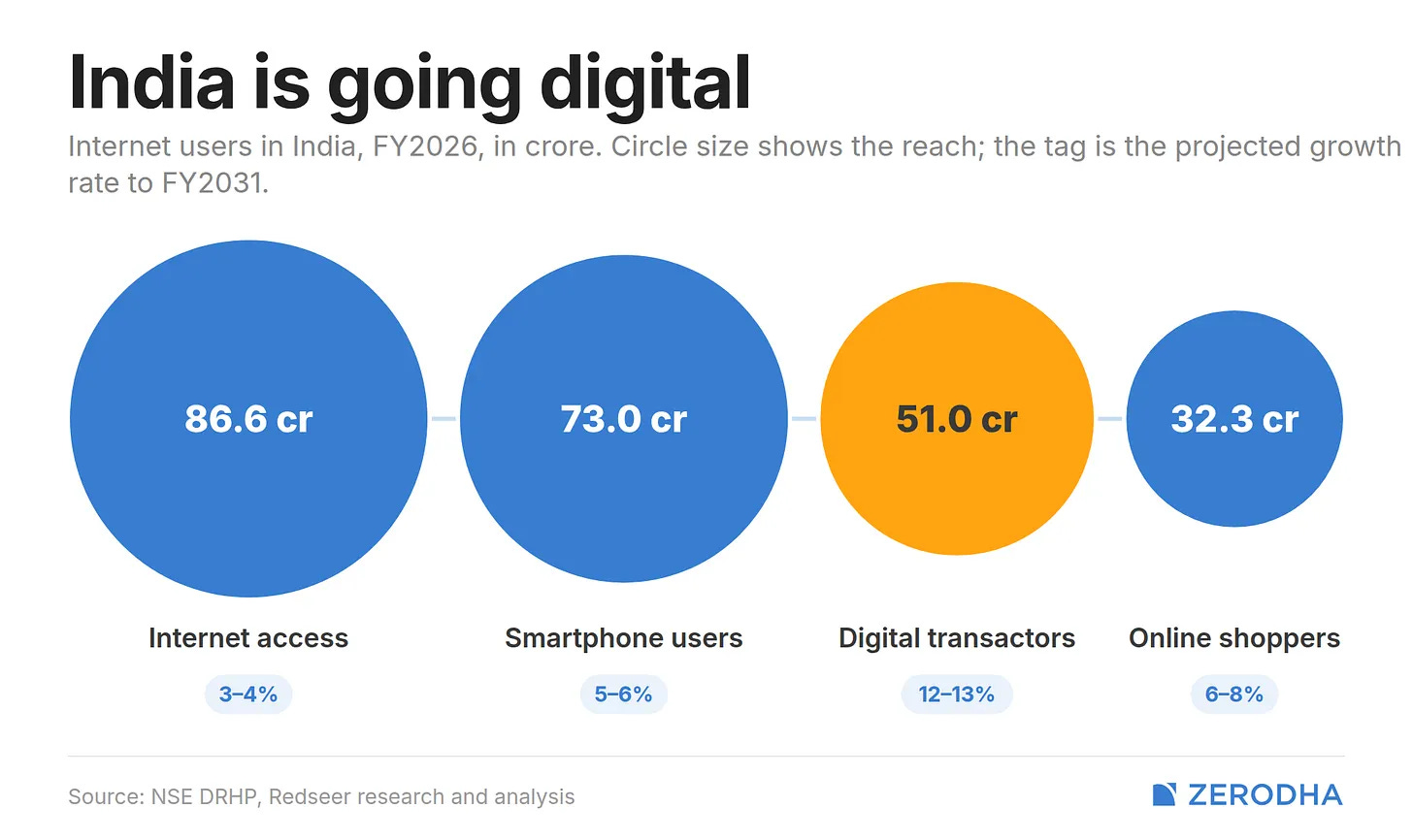

Before Jio, 1GB of data cost around ₹225. Today, it costs about ₹10. UPI, which was launched the same year as Jio, went from near zero to processing 228 billion transactions in 2025. India went from roughly 3 crore demat accounts to over 20 crore, the number of online shoppers has tripled, and data consumption per person went from less than 0.2 GB a month to over 42 GB.

Whenever we used to look at the results of a behemoth like Reliance, it was hard to see what was happening at an individual business level. Each division of the conglomerate is its own labyrinth. But this listing means we will get a proper view into India’s biggest telecom company for the first time. The same will be true for Reliance Retail when it eventually goes public.

With that, let’s dive into the prospectus of India’s largest telecom player.

The money rings

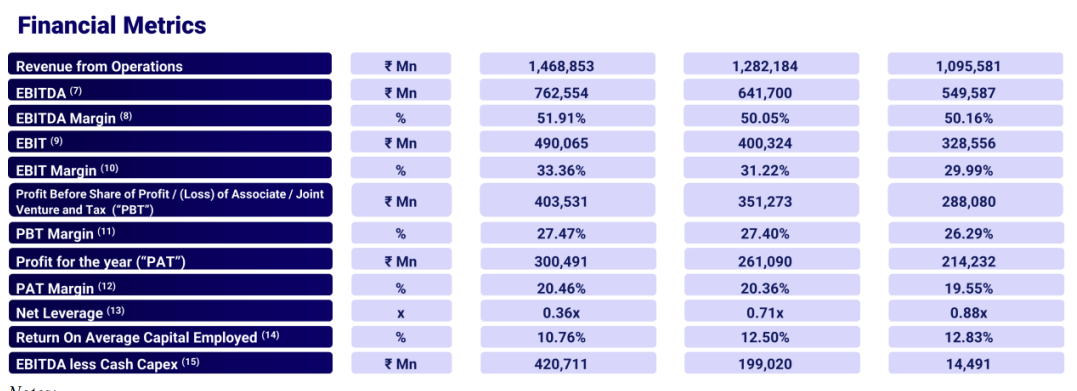

In FY26, Jio Platforms earned ₹1.46 lakh crore in revenue. This is mostly from one thing: mobile broadband subscriptions. Customers buy prepaid or postpaid plans, those plans give them data, and Jio charges for them. That is the core of the business.

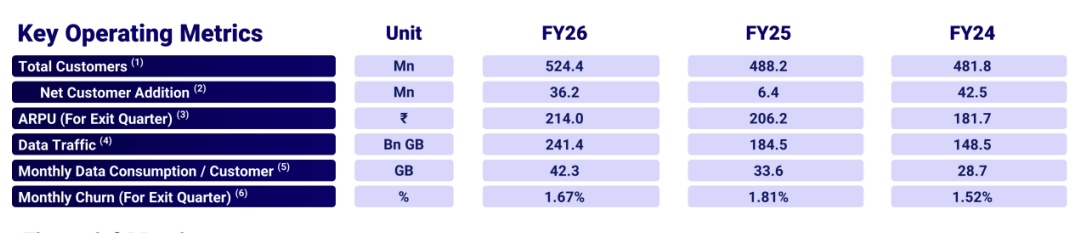

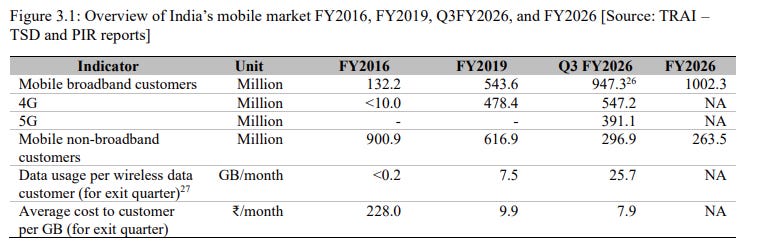

As of March 2026, Jio serves about 52 crore mobile customers, or around 40% of the Indian mobile market. In comparison, Airtel has about 37 crore mobile subscribers and Vodafone Idea has about 19 crore. The network carries about 60% of all wireless data traffic in India and the average data consumption per Jio customer is 42 GB per month.

India has about 126 crore total mobile subscribers today. Of these, about 26 crore are still on 2G networks; they are mostly customers of Vodafone Idea and BSNL who have not yet upgraded their phones to 4G. These are Jio’s most obvious growth pool. Every one of those customers who buys a 4G phone is a potential Jio subscriber.

The ARPU game

Now, the key metric for any telecom is average revenue per user or ARPU, which means how much the company earns per customer per month. Jio’s ARPU is ₹214 per month. For comparison, Airtel’s is ₹257.

Despite having fewer subscribers, Airtel extracts more revenue and profit per customer. This is because Airtel has deliberately focused on premium customers, postpaid users in cities, and enterprise accounts. Jio has a larger but more mass-market base. Both strategies have worked. Two companies, remarkably similar in size, but built on very different customer mixes.

That being said, Jio’s ARPU has also been steadily growing, from ₹181 in FY24 to ₹214 now. In July 2024, Jio raised its tariffs by 10-25% across different plan tiers, and Airtel followed immediately. Remember, this is an industry with effectively three players. And one of those three, Vodafone Idea, has mostly been financially distressed. So, the pricing power of the remaining two is high, and customers do not really have many options here. Such is true for the telecom industries of most countries.

What makes ARPU growth particularly powerful for Jio is that the incremental revenue flows almost entirely to the bottom line. The network is already built, the spectrum is already paid for, and the towers are up. When each of Jio’s 52 crore customers pays ₹10 more per month, that is roughly ₹6,000 crore extra revenue a year with almost no additional staff or infrastructure cost attached to it.

Additional revenue lines

Beyond mobile, Jio also earns from its home broadband business, which can be divided into two parts. One is JioFiber, which connects homes with optical fibre. The second is JioAirFiber, which does the same wirelessly using 5G spectrum, essentially replacing the need to dig up roads and lay cables into every home. As of March 2026, Jio has 2.71 crore home broadband customers and a 42.6% market share in fixed broadband in India.

Enterprise services, offering cloud connectivity and private 5G networks to businesses and factories, is a third revenue stream. These businesses are growing but tiny relative to mobile.

The financial picture

Now, how do the numbers look for Jio?

Well, Jio made a whopping ₹1.46 lakh crore in revenue, with the profit being about ₹30,000 crore. These are strong numbers by any measure, and perhaps unsurprising. But the more important number to note here is free cashflow.

See, building India’s 5G network cost a lot. In FY24, Jio spent around ₹53,000 crore on capital expenditure, which included the purchase of spectrum, installing equipment on towers across the country, laying fibre, building data centres. That left them with not a lot of cash in comparison to their revenues: just ₹1,500 crore (which, well, is still a wild number in absolute terms).

But by FY26, that had fallen to ₹34,000 crore as more of the network got built. Simultaneously, the cash flows improved manifold to ₹42,000 crore. Now that the hole is dug, it’s time to fill it up.

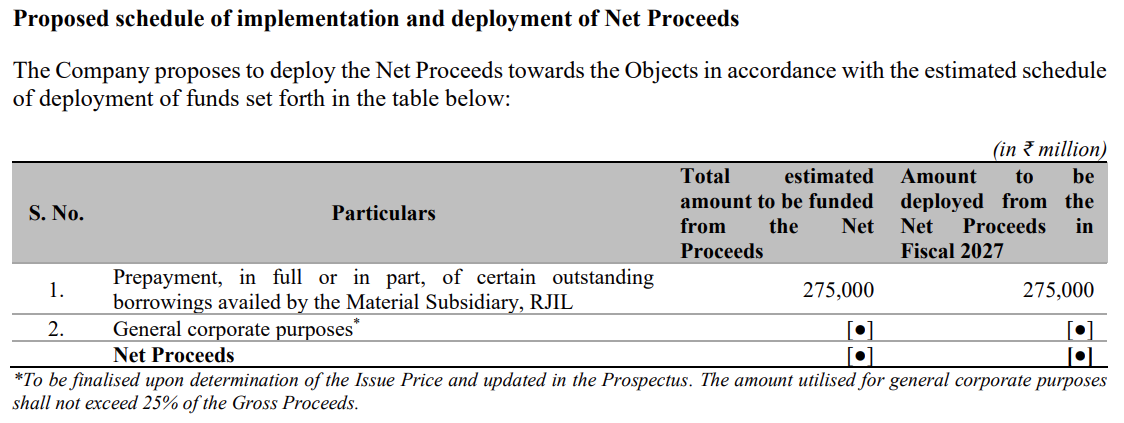

What’s also worth noting is that the biggest chunk of this IPO — ₹27,500 crore — will be used to clean up debt.

Jio borrowed heavily to fund their capex, including in foreign currencies. Borrowing in dollars is cheaper, but there is a catch: if the rupee weakens, the loan becomes more expensive to repay. After paying off the foreign loans, Jio will still have some debt on the books, but it also has over ₹43,000 crore sitting in cash and investments — enough to cover what remains. On a net basis, it will owe almost nothing. A company that just spent over ₹1 lakh crore building a network comes out the other side essentially debt-free.

What this listing actually means

The IPO will make Jio independently trackable for the first time. Today, Jio’s numbers get reported inside Reliance’s quarterly results, but with limited detail and surrounded by oil, retail, media, and financial services. A listed Jio will have to report in full every quarter, which means investors and analysts will be watching ARPU growth, the pace at which 2G customers migrate, how fast capex continues to fall, and whether digital services revenue starts appearing in a meaningful way.

The listing also sets a standalone market valuation for Jio for the first time. The company that built the internet infrastructure of modern India is about to find out what the market thinks it is worth. For the hundreds of crores of Indians who have been paying Jio a small amount every month for years, that is a number worth watching.

Is India ready for the Super El Niño?

Exactly three months ago, on March 23, we covered what a Super El Niño could mean for India.

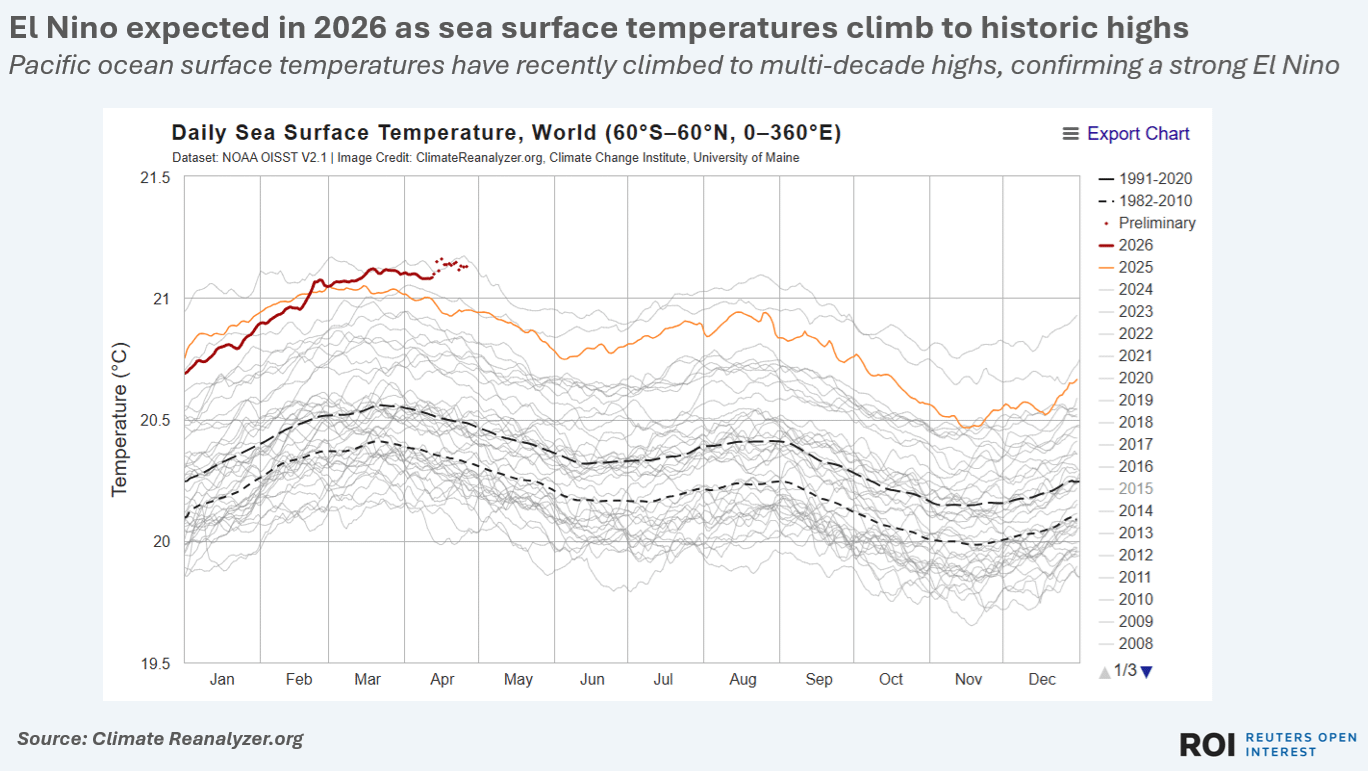

At the time, it was still a forecast. But since then, the forecast has become absolute fact. NOAA confirmed the onset of El Niño on June 11. Sea surface temperatures in the Pacific are on track to cross 2°C above normal by October. That’s borderline Super El Niño territory, rivalling the occurrences of 1998 and 2016.

In India, the IMD downgraded its monsoon forecast twice, and pegged the probability of a deficient season at 35% — more than double the historical base rate. The monsoon made landfall in Kerala three days late on June 4, pushed through the south and east, and then stalled. As of June 17, cumulative rainfall is 38% below normal. Twenty-two of India’s 36 meteorological subdivisions are deficient. Central India — the country’s agricultural heartland — is 62% below where it should be.

And the impact of this has already begun showing up.

On the farms, kharif sowing as of June 12 is down about 4% year-on-year. Pulse sowing has cratered by 43%, cotton by 28%. India’s 166 reservoirs currently hold about 55 billion cubic metres — roughly 30% of their total live storage — which is lower than last year. Perhaps, the most alarming of these stats is in Mumbai, which, right now, only has enough water to meet the city’s needs for 40 days.

On the grid, power demand hit a record 270.8 GW in May — four consecutive days of all-time highs as heatwaves baked northern and central India. Consumer food inflation hit 4.8% in May, the highest in 16 months. The RBI has already raised its inflation projection to 5.1% and cut its GDP growth forecast by 0.3 percentage points to 6.6%.

The question, then, is whether India has enough defences to weather this storm — or rather, the literal lack of it.

The struggles of India’s grid

Let’s start with the energy grid.

Now, power generation isn’t the government’s primary worry. India’s installed power capacity has doubled over the past decade to 520 GW. Coal plants, running at around a plant load factor of 70%, have headroom to ramp up further. At peak demand, this system seemed to hold.

Interestingly, solar alone contributed nearly 22% of output. That is, by any metric, an impressive statistic, and more importantly, a much-needed defense as coal plants may strain. Off-grid installations could also help remove pressure on the national grid. As we noted in the previous story, paradoxically, by suppressing the clouds needed for rains, the El Nino might ensure more time for the Sun, and therefore solar power.

Yet, solar’s usage is still limited because of the lack of battery storage to make use of at night time. India will need an estimated 1.38 lakh circuit kilometres of additional transmission lines to support the integration of renewables properly. In 2025 alone, the grid curtailed an estimated 2.3 TWh of solar power because infrastructure couldn’t safely absorb it — clean energy produced but wasted.

The real anxiety, however, is not really power generation, but power transmission, a topic that we’ve spent quite some time covering on The Daily Brief.

See, El Niño-driven heatwaves don’t hit the country uniformly. Demand surges are regional and sharp: a state boiling at 45°C pulls far more power than the grid planned to route there. Overloaded transformers, stressed feeders, and local distribution networks designed for a different era become the chokepoints.

For instance, during May’s record demand, infrequent blackouts were reported in Delhi and Chennai because the last mile of the grid couldn’t carry it. In fact, in the last few weeks, Delhi saw a series of fires that were attributed partly to the poor state of Delhi’s grid.

Stopping the flow

The most underrated piece of what happens to India’s energy grid is the one that’s most directly affected by it — hydropower.

Hydropower accounts for about 10% of India’s total power generation, and India’s hydro capacity currently stands at over 51 GW. But what makes hydro disproportionately important is its flexibility. Unlike solar, which fades at sunset, or thermal plants that take time to ramp up, hydropower can be turned on and off at will. It’s the grid’s stabiliser, keeping the lights steady when other sources fluctuate.

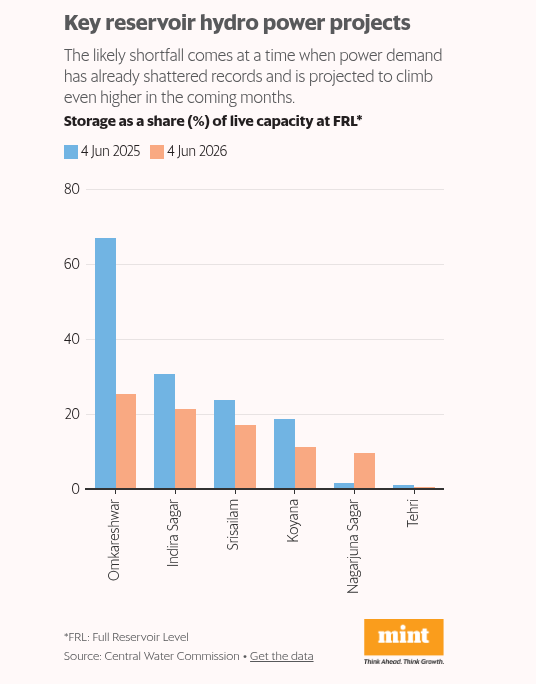

El Niño attacks this directly. Less monsoon rainfall means lower reservoir levels, which means less water flowing through turbines, and hence, less generation. In 2023-24, an El Nino year, hydropower generation fell by 16%. As per Mint, this year, with reservoirs already below last year’s levels and the monsoon stalling, estimates suggest generation could drop about 10%. Of 20 reservoirs linked to hydro-electric projects, water levels in half are at or below last year’s levels.

The impact isn’t uniform, either. Hydro projects in the Himalayas, which are built on snow-fed rivers, are somewhat insulated; they may even benefit from higher snowmelt this summer. But reservoir-based projects in central India are the most exposed. They fill during the monsoon and power the grid through the year, but without the rains, a shortfall will bite hard.

The result is a double bind. When the monsoon weakens, farmers pump more groundwater to irrigate their crops, which raises electricity demand for agricultural pumping. At the same time, the hydro supply that normally helps meet that demand is declining. The grid has to serve rising demand while facing shrinking hydro contributions. Then, coal-fired thermal plants, which are running at high load factors already, have to pick up the slack. That only increases our dependency on coal.

The buffers get bigger than ever

Now, what about agriculture?

For food, India’s defences against a weak monsoon are, on paper, more substantial than they’ve ever been. Wheat stocks as of June 1 stand at 53 million tons — nearly double the official target and the highest level since 2021. Rice stocks 68 million tons against a norm of 13.5 million tonnes. These are record levels for the public distribution system, but that’s what you need to absorb a significant production shortfall without triggering a supply panic.

This is already getting complemented by the trade policy toolkit.

For instance, in May, sugar exports were outright banned until September this year. As we’ve covered previously, ethanol, which is made out of sugarcane, uses a lot of groundwater. With an active industrial policy for fuel blending, India will look to fulfil domestic demand for ethanol first.

Additionally, India has used a rice export ban as recently as 2022, lifting it only in late 2024-early 2025. That is also a quick tool readily available to use on short notice. Meanwhile, ethanol is also made out of foodgrains, and India has diverted rice and maize before towards ethanol production. That lever will now likely become limited to prioritize food security.

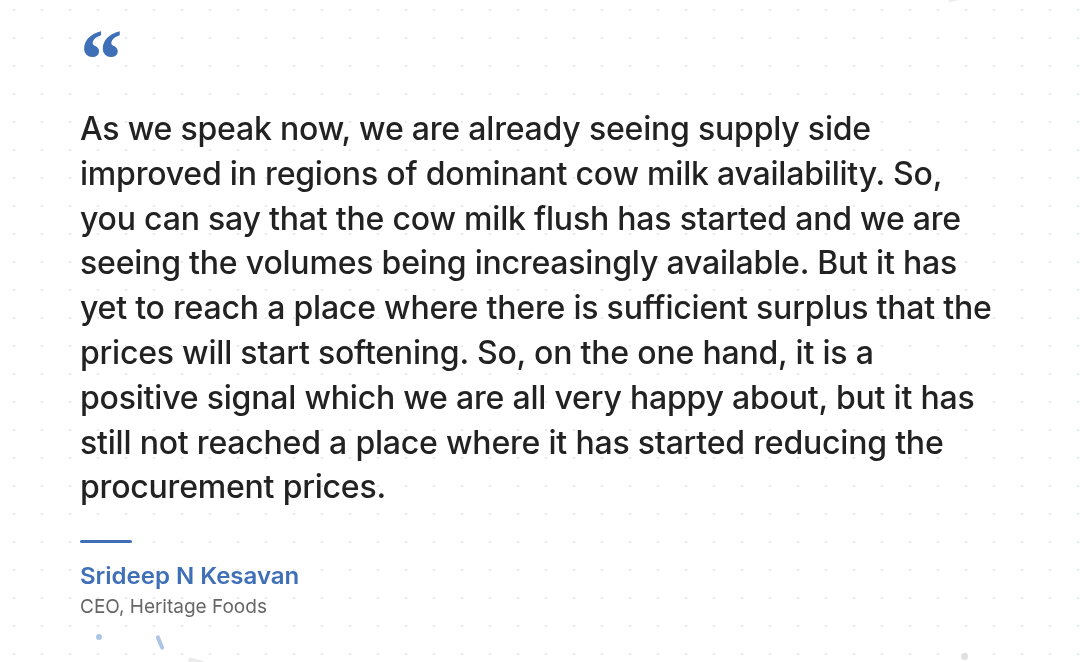

The dairy sector, whose results we covered recently, adds another layer of pressure. Heat stress is already weighing on milk yields, and a weak monsoon threatens fodder availability — the raw material that keeps India’s dairy supply chain running.

The sector has been going through a raw milk shortage for much of the past year, well before El Nino. That hasn’t eased up at all. Yet, some companies, like Dodla Dairy, achieved record sales figures in the quarter. However, that was partly due to stocking up well in advance. And partly, the companies have been seeing some bright spots in India in terms of rainfall.

Irrigation

Now, what has increased our resilience is expanding smarter irrigation systems.

India’s irrigated area has risen from 49% to 56% of total sown land over the past decade. India’s irrigation story has largely been one of moving away from leaning on canal-based systems in the 1950s to a tubewell-heavy system today. The former is mostly useful in times of heavy rainfall, while the latter makes use of groundwater — extremely helpful when the rains fall short.

Ideally, this means that, even in times of drought-like conditions, there should be enough backup of water to handle the needs of the sowing season.

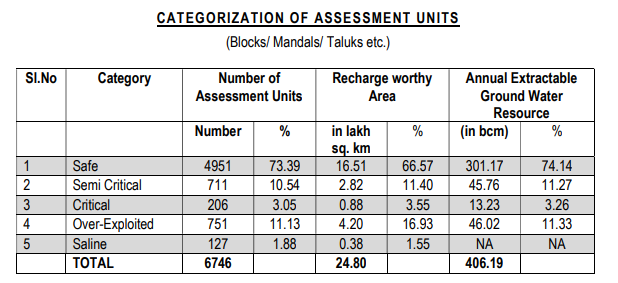

But, this makes us more dependent on groundwater, whose extraction is intense in India. We are the largest user of this resource in the world. Nationally, we use 60% of our annually replenishable groundwater. What’s more, in a cruel paradox, 61% of groundwater recharge still comes from rainfall, which means a weak monsoon undermines the very backup system farmers depend on.

There is also significant variation in how states extract groundwater. For instance, Punjab, Delhi and Haryana extract over 100% of their groundwater, basically taking in more than what the ground can hold. As of 2024, 11% of India’s groundwater blocks were classified by the state as “over-exploited”. Now, that’s still down from 17% in 2017, but it does leave certain states far more vulnerable than others.

Interstate variation

Groundwater extraction is only one of the ways in which the water management systems of various states differ.

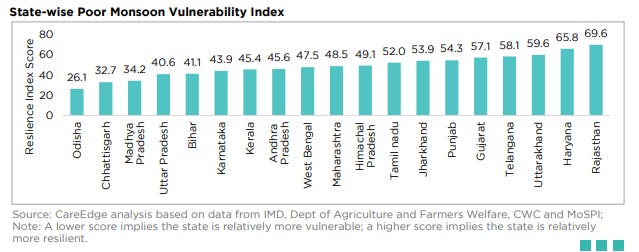

As per CareEdge, the most vulnerable states — Odisha, Chhattisgarh, Madhya Pradesh, Uttar Pradesh, Bihar — are the ones with low irrigation coverage, high crop dependence, and limited diversification. Rajasthan, counterintuitively, ranks among the most resilient, because it has minimal reliance on water-intensive crops and a small agricultural share in its overall economy. Punjab, despite strong irrigation and high reservoir levels, ranks lower than you’d expect, because it remains heavily dependent on water-intensive rice and sugarcane.

On the ground, the Agriculture Ministry has flagged 197 districts as most vulnerable and ordered state governments to overhaul their contingency plans, many of which hadn’t been updated in a decade. Drought-resistant seed stockpiles have been pre-positioned in high-risk areas, and Crop Weather Watch Groups have been formed to monitor conditions weekly.

Whither the rain gods?

The buffers are among the highest they’ve ever been. The policy toolkit has also been prepared. But are they enough?

Kharif sowing as of mid-June has declined from last year. The crops most exposed are overwhelmingly rainfed: about 90% of the area under pulses and oilseeds depends directly on monsoon rainfall.

There is enough reservoir capacity for now. But it is depleting faster than it should be this early in the season. That matters not just for kharif crops but for the rabi season that follows: if reservoirs don’t fill adequately during the monsoon, winter crops like wheat and mustard face irrigation shortfalls months from now.

The last Super El Niño in 2015-16 brought India’s worst drought in decades, causing widespread crop failure and farmer suicides. It also marked the start of one of the worst prolonged drought periods for most of South India, and naturally, climate change was the amplifying effect here.

This time, we have climate change and oil prices which are elevated due to the West Asia crisis. Fertiliser supply chains were already under stress from the Strait of Hormuz disruption before El Niño even arrived.

Whether the defences hold depends primarily on what happens in July and August. If history is any indication, the most effective resolution to this is timely rains.

Tidbits

[1] BHEL, Coal India to invest ₹25,000 crore in Odisha coal gasification project

BHEL and Coal India will jointly invest ₹25,000 crore in a coal gasification project in Odisha. The project aims to convert coal into feedstock for fertilisers and chemicals, create jobs, and reduce India’s dependence on imports in key industrial sectors.

Source: The Economic Times

[2] Sun Pharma to acquire Innovcare Lifesciences for $28.7 million

Sun Pharmaceutical Industries will acquire 100% of Innovcare Lifesciences in a deal valued at about ₹271 crore ($28.7 million). The acquisition is part of Sun Pharma’s efforts to strengthen its portfolio and expand its presence in the pharmaceutical market.

Source: Reuters

[3] Voltas crosses 1 million AC sales in record time during FY27

Voltas sold over 1 million air conditioners within the first three months of FY27, the fastest it has reached the milestone. The company attributed the achievement to strong consumer demand, a wider distribution network, and growing interest in its AI-enabled product range.

Source: Business Standard

- This edition of the newsletter was written by Krishna and Manie.

Over 2 crore Indians invest with Zerodha. Open a free demat account in minutes and invest in stocks, mutual funds, ETFs, and bonds at 0 brokerage. No hidden charges, no gimmicks. Plus, get free access to research tools like Tijori, Sensibull and more.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re a small team. We come across interesting data all the time, but rarely have the bandwidth to do anything with it.

Last week, when we were researching NSE’s IPO, we found ourselves sitting on a goldmine of charts and data points on how Indian capital markets have evolved. That’s when we thought: why not finally try something we’d been putting off for a while?

Points & Figures was originally a section within The Chatter, our newsletter on earnings calls. We always wanted to give it its own home. Tools like Claude have made it possible for a team our size to actually pull it off, without cutting corners on the research.

The first edition looks at the evolution of Indian capital markets, through data we pulled from NSE’s IPO papers.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉