A deep dive into the textile industry

And how will we find jobs for the next 100 crore workers?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

A deep dive into the textile industry

Can we find jobs for the next billion workers?

A deep dive into the textile industry

Pull out a cotton t-shirt from your almirah, and look at the tiny tag stitched inside the collar. Chances are, it probably says “Made in Bangladesh” or “Made in Vietnam”. The chances that it will say “Made in India” are much lower.

This should be strange. We have more land under cotton than any country on earth, more spindles running than almost any country on earth, and more textile workers than most countries have citizens.

Our textile industry is enormous in scale. The textile and apparel industry is India’s second-largest employer after agriculture. 45 million people work in it directly, and many millions more depend on it for their livelihoods — especially in small towns across Gujarat, Tamil Nadu, Uttar Pradesh, and West Bengal, where formal industrial work is otherwise hard to find. The sector brings in about $37 billion in export earnings every year. When it slows down, the effects show up in the larger economy.

And yet, it doesn’t make the T-shirts in your almirah.

How value gets made

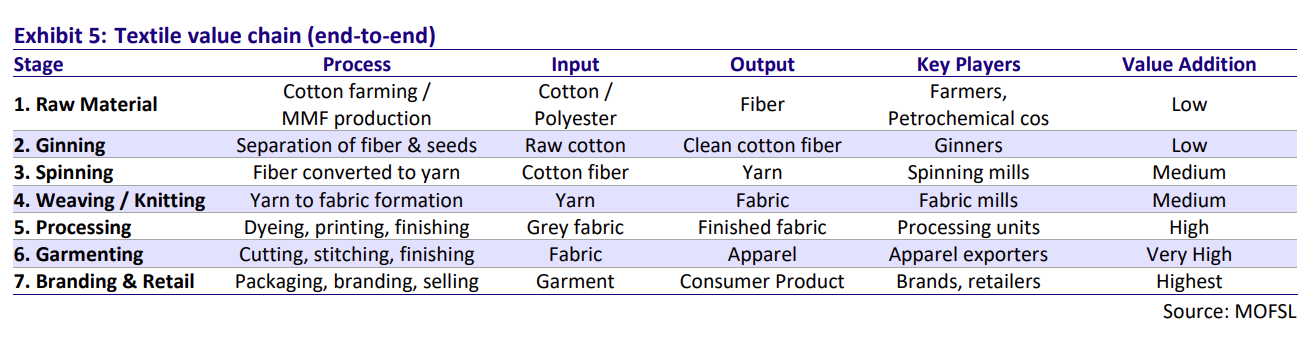

To understand why we’re missing from the world’s closets, it helps to understand the chain that connects a cotton field to a finished t-shirt.

This is a value chain that flows through five stages.

It all begins with raw fiber — either cotton from a farm or synthetics from a chemical plant. This fibre goes first to a spinning mill, where it is cleaned, combed, and twisted into yarn. That yarn is then sent to a weaving unit, where it becomes cloth. At this point, the cloth is coloured a neutral beige. Before it becomes something you’d like to wear, it must go to a dyeing and processing unit, where it is bleached, washed, and colored. Finally, that coloured cloth reaches a garmenting unit, where workers cut and stitch it into clothing.

You can watch this video to understand where cotton fabric comes from.

How Cotton Is Grown and Harvested | Where Cotton Fabric Comes From

At each of these stages, it picks up value.

A kilo of raw cotton is worth about ₹170. Over the course of its journey, it turns into 2 to 3 finished garments, worth ₹800-1,000. That is a 5 to 6x multiplication.

Most of that appreciation, however, happens at the very last stage: garmenting. This is also where most human labour comes in. Until this point, things are largely mechanised, with spinning mills and weaving units doing most of the work. Garmenting, however, is almost entirely manual — hundreds of workers at sewing machines, assembling each piece by hand. The economics here are driven by labor cost and skill, not machinery.

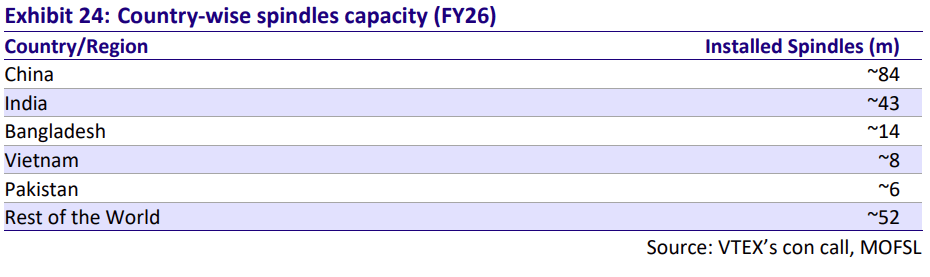

And that’s where our issue lies. India is genuinely strong at the earlier stages. We run more than 43 million active spindles and are the world’s second-largest spinning hub. But we are weak at garmenting. Only, that’s where the most money is made, and where most jobs are created.

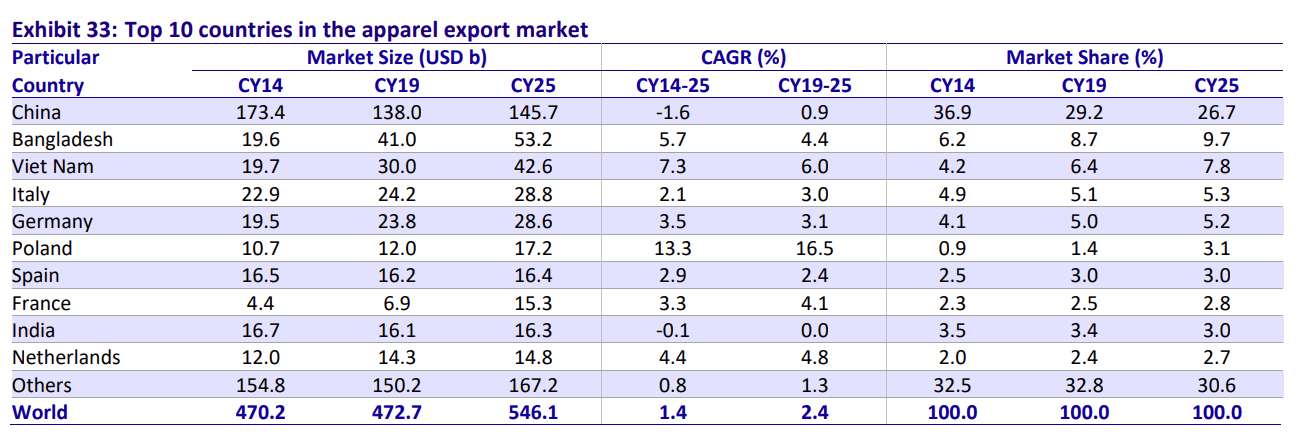

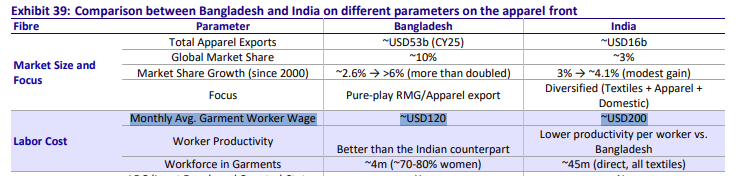

We have been stuck here. India’s share of global apparel exports has barely moved for nearly 20 years. Over the same period, Bangladesh went from 2.2% to nearly 10%. Vietnam went from 1% to nearly 8%. Both were behind us in 2000.

Why are we so stuck? This is the outcome of two factors: one, the fiber we chose to build our industry around, and two, specific policy decisions that kept our factories small.

Cotton vs. synthetics

The clothing world runs on two types of fiber: Cotton, and Man-made fibres (or MMF).

Cotton comes from farms. Its supply moves with weather, harvests, and pest cycles. Man-made fibers, like polyester, nylon or viscose, come from chemical plants. These run at a predictable cost year-round.

Over the last 20 years, fast fashion, activewear, and athleisure drove a massive global shift toward synthetic cloth. Globally, 70% of all fiber consumed for any purpose today is man-made. Even when it comes to apparel specifically, cotton and synthetics are at a roughly equal footing.

India, meanwhile, has stuck steadfastly to cotton. 60% of the yarn we make is cotton. This has made us the world’s largest cotton yarn exporter, but we’re nowhere close in the global man-made fiber trade.

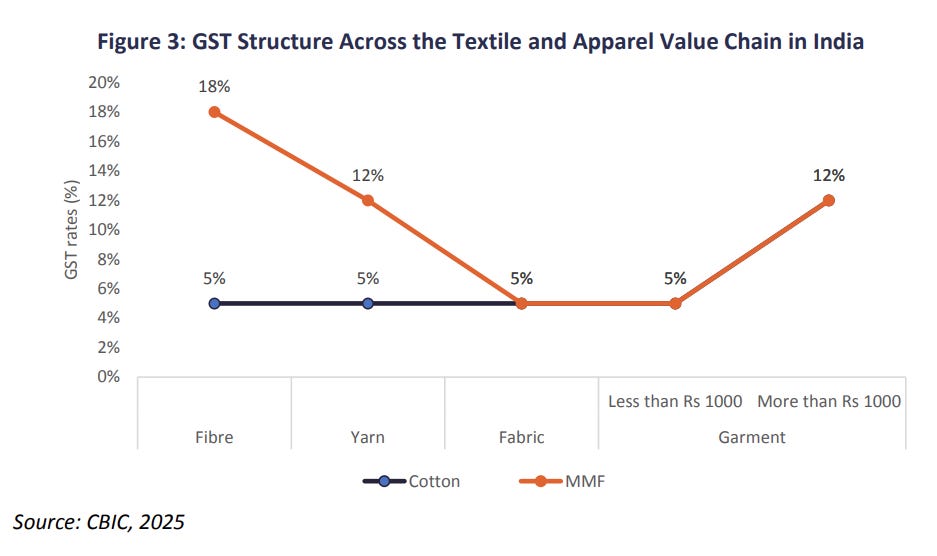

This is reinforced by a structural tax problem for anyone working with synthetic fiber. MMF fibre is taxed at 18%, and yarn at 12%. The fabric woven from it, meanwhile, is taxed at only 5%. If you want to try your hand at making synthetic yarn or fabric, you must pay the higher rate upfront and wait months for a refund, locking crores of working capital in the system. This is a constant drag for anyone in the value chain.

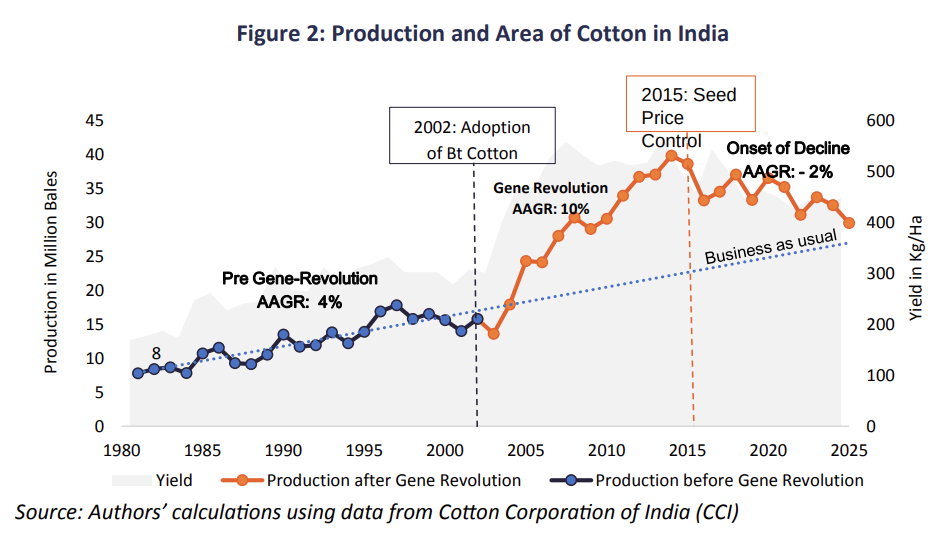

Our cotton comes with its own problems. India has the largest cotton-growing area in the world, but our yields run at roughly half the global average. For a brief period of a dozen years, our yields were improving massively. But in 2015, the government capped what biotech companies could charge for their seeds. This killed any incentive for them to develop better varieties for India.

Our progress stalled. Production levels fell as pests adapted to existing strains. Domestic cotton prices now swing 18-22% in a single year, causing immense volatility for spinning mills and weavers downstream.

How we kept ourselves small

In fact, government policy makes many appearances in this story.

Until the year 2000, the Indian government reserved the entire garmenting sector for small-scale industries. This was well-meaning, of course; the government wanted to protect artisans. The practical effect, however, was that nobody could build a large garment factory in India for decades. China and Vietnam, meanwhile, spent the 1990s building massive, integrated hubs where spinning, weaving, and stitching happened under one roof at enormous scale. By the time India deregulated, they had already built deep relationships with every major global brand, while our textile industry remained artisanal.

Even after deregulation, however, our labor laws penalized growth. Under our labour laws, once a factory crossed 100 workers, one could only fire them with government permission. Reducing headcount during a downturn became nearly impossible. Instead, factory owners chose to stay small by design.

Today, over 80% of Indian apparel factories are MSMEs, scattered across fragmented clusters. They’re unable to take on the large, complex orders that global brands need. Cotton grown in Gujarat, may be spun in Tamil Nadu, and woven in Maharashtra — all connected through a broken logistical system. Each handoff across that geography adds cost and time. As a result, Indian manufacturers are slower and more expensive than their main competitors. For a brand managing tight inventory cycles, this lack of speed is fatal.

Meanwhile, countries like Bangladesh began to undercut us on labour costs. Our garment workers earn about $200 a month on average. In Bangladesh, they earn about $120. That 67% wage premium is a consistent drag for the volume-driven orders that fast fashion brands place.

What is changing

For most of the last 20 years, the conditions for India to break into global apparel trade simply weren’t there. China dominated the industry, beating us on size and organisation. Bangladesh beat us on costs. We were crushed in between.

That might now be shifting, however.

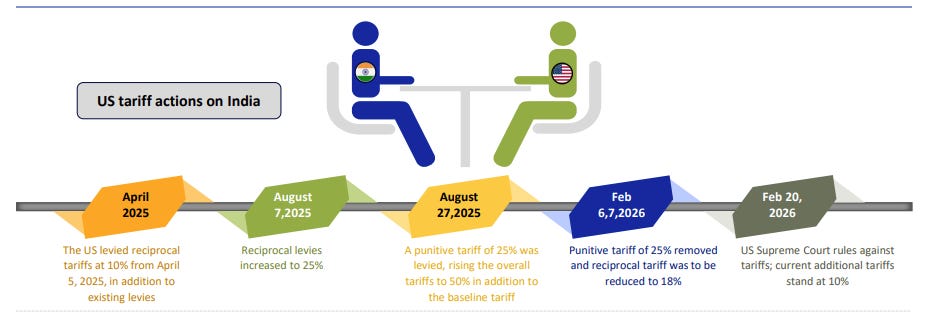

China’s making a slow retreat from the global apparel trade. About 80% of China’s domestic cotton comes from the Xinjiang region, and in 2021, the US passed a law effectively barring imports of goods made with Xinjiang cotton, citing forced labor concerns.

This made global brands deeply cautious about Chinese supply chains, both on tariff grounds, and on compliance and reputational ones. China’s share of global apparel exports has fallen from around 37% a decade ago to about 27% today. Brands are actively looking elsewhere.

Bangladesh had been the biggest beneficiary of that shift. Lately, however, it is under pressure from multiple directions. A political crisis in 2024 forced a violent change in government, making buyers nervous about having too much sourcing concentrated in one country. Meanwhile, its energy situation has worsened. The country depends heavily on imported LNG, the cost of which has spiked. Grid failures are limiting factory hours. Their government recently imposed duties on synthetic fiber imports to protect local chemical producers, raising yarn costs for their own manufacturers at exactly the moment they needed to shift to synthetics.

To add to its misery, Bangladesh’s trade access will also narrow from 2029. The EU currently gives zero import tariffs to countries classified as “Least Developed Countries” (LDC) under a scheme called Everything But Arms. This is essentially a gift to the world’s poorest nations to help their exports compete. Bangladesh qualifies as an LDC, which is why its garments walk into European stores paying nothing, while Indian garments face a 9 to 12% tariff.

But its success has made Bangladesh wealthy enough that the UN wants it to graduate out of LDC status. For now, it has a 3-year extension that’ll go on till November 2029. After that, however, it will lose its zero-tariff benefit unless it can qualify for a separate EU scheme called GSP+, which offers partial duty-free access to developing countries that meet certain labor rights and governance conditions. Nobody knows yet whether Bangladesh will qualify.

India, meanwhile, is negotiating a full free trade agreement with the EU. If that deal closes around the same time, Indian garments could enter the EU at zero tariff for the first time, just as Bangladesh is losing its own preferential access.

In the US, India faced tariffs on textile exports as high as 50% at the peak in mid-2025. While we can say nothing about the United States with certainty these days, for now, the tariff rate is set at 10%.

And the government, meanwhile, is actively pushing export competitiveness. There are now 7 PM-MITRA textile parks in development, with a budget of Rs. 4,445 crore, which are designed to co-locate spinning, weaving, dyeing, and garmenting under one roof. If this works out, it could bring the fragmentation problem to a close, and slash the lead time gap that has held us back.

The part that’s harder to answer

There’s a lot of detail we are yet to explore in India’s second largest industry. Gaining market share isn’t easy even now; and our success is conditioned on many variables falling into place.

Right now, there are hundreds of power loom owners, in small towns like Bhiwandi. Many have been running the same machine for years, braving tumultuous changes to their yarn costs, because they lack the ability to retool for synthetics. The new industrial parks could take years to come up. In the meanwhile, can they begin a turn of India’s fortunes, beating out international competition and bagging contracts?

A lot of the future direction of the industry hinges on questions like this.

Can we find jobs for the next billion workers?

There’s a puzzle in the field of development economics: through the 2010s, the average developing economy grew more than 3% faster than the average rich one. And yet, across the decade, their employment levels grew barely 0.2% faster. For all that extra growth, the jobs dividend was a mere rounding error.

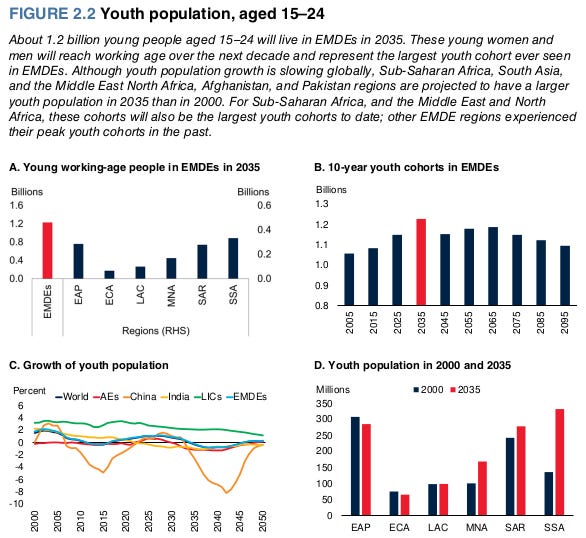

The World Bank has just published a 252 page-long report, called The Global Jobs Challenge, trying to explain why. It grapples with a sobering challenge: roughly 1.2 billion young people reaching working age in emerging and developing economies by 2035. This will be the largest youth cohort in history. How will we find jobs for them all? The report tries to wrestle with this challenge, looking at why growth doesn’t automatically create jobs, and where new jobs could actually come from.

This report may be interesting for the world, but nowhere is it as salient as it is for us, here in India. We have the largest jobs challenge in the world, in absolute numbers. That makes this a report we should take notice of.

Conceptualising the challenge

Here’s the basic problem.

Across the world, in the next decade, about 1.2 billion young people shall enter their working years. Of course, many others will retire, but even accounting for that, the world’s workforce will expand by 450 million. Compared to those that came before, these new workers will also be unusually educated — in fact, they’ll be the best-educated generation the developing world has ever produced.

This won’t happen everywhere at once. India shall see the largest problem in terms of size, with the world’s largest youth population. But the epicenter of this surge will shift from the Indian subcontinent to sub-Saharan Africa, which is increasing faster in percentage terms. Roughly three-quarters of the world’s new working-age workers, until 2050, shall come from that region. More than a fifth of them will live in fragile or conflict-affected states.

Do we have a way of employing them productively, or is the world staring at a potential lost generation?

Structurally, the world economy is slower than before. The world’s growth potential, according to the World Bank, runs a third below where it was in the 2000s. We’re already seeing the impact of it. In 1991, of every 100 working age adults, 69% were actually employed. By 2019, that number had fallen to 64. It is

This makes our problem particularly frustrating: a particularly capable generation of workers is entering a global economy that has become substantially worse at accommodating them.

When growth doesn’t convert to jobs

The Bank carves out a group of twelve “high-jobs-need” economies, where the problem is particularly acute. India is one of them, alongside others from our region, like Bangladesh and Pakistan.

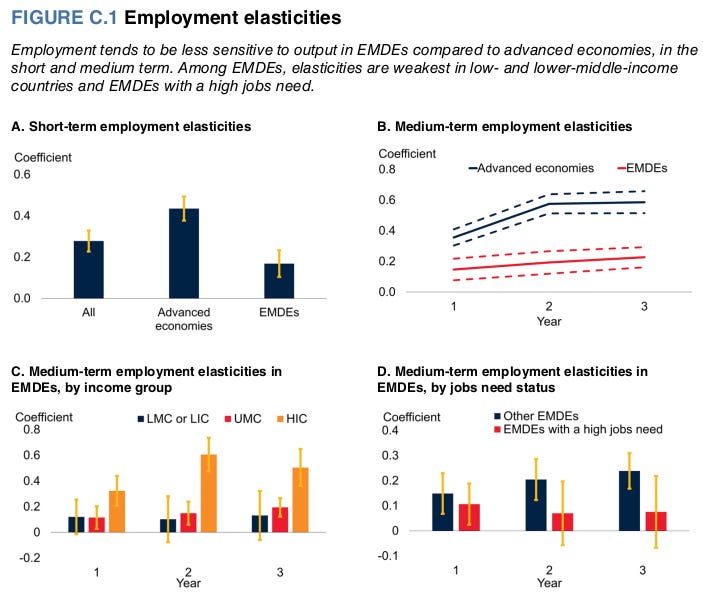

What options do these countries have? One would assume the answer lay somewhere in pursuing prosperity. But there’s a weird statistical problem here; in rich countries, an extra percent of GDP growth brings ~0.6% more employment growth. For the average developing economy, that drops to 0.23%. For these twelve counties, it is just 0.08%. The correlation was so small that you can’t even trust the number. It could be random noise.

To be fair, these countries are adding some jobs in absolute terms. Some of their numbers simply seem off because of how fast these countries’ populations have exploded in recent years. To paraphrase the Red Queen, these countries have to run as fast as they can just to stay in place.

But fundamentally, for countries like ours, growth — while important — isn’t a reliable job-creation strategy.

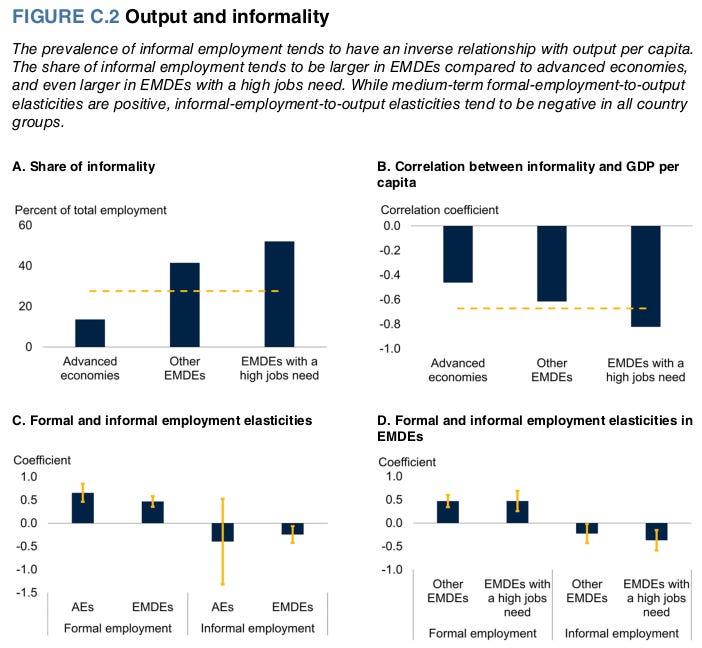

Why is this relationship so weak? The answer is informality. The informal sector in developing economies acts, in practice, as an unemployment insurance system. When growth slows in countries like ours, people absorb the shock by working outside the formal economy: they might help out at a family plot, lend their labour to a construction site, or run a roadside pakoda stall. When growth picks up, some of those people get pulled back into wage work. In much of the developing world, in fact, even when someone is classified as “employed”, they may actually secure wage work for only 20-50% of their days.

That is, where wage employment follows growth positively, informal self-employment runs opposite to it.

Unlike developing countries, which have formal unemployment support programs, in the developing world, many workers sit in an informal buffer instead. In the Indian sub-continent, for instance, nearly 90% of workers are informal. This buffer absorbs shocks in both directions. It can keep employment figures looking stable even while livelihoods remain fragile. At the same time, growth doesn’t create more employment; it just shuffles people out of the informal sector and into the formal one.

This doesn’t mean growth is unimportant. But the quality of growth matters. Good growth happens when it comes from better productivity. When you sort countries by how much they improved their productivity, those in the top quartile by productivity growth saw extreme poverty levels fall by 1% every year between 1981 and 2015. On the other hand, a country can also grow mathematically because more people are entering its workforce. Countries that took this path, however, actually saw their poverty levels increase.

Unfortunately, the path to the best sort of growth — one that raises productivity — increasingly appears to be closing.

Manufacturing is the best sector for turning growth into jobs. It creates well-paying employment at a significantly higher rate than any other sector of the economy. But it is harder to become a manufacturing giant than it was a generation ago — countries like China still dominate industries across levels of complexity, while trade restrictions have more than tripled since before the pandemic. Pollution-heavy industries — often the first rung on the ladder — are harder to set up in an era marked by climate change. Elsewhere, workers must contend with AI eating into routine tasks.

What, then, should a country pursue?

What does work

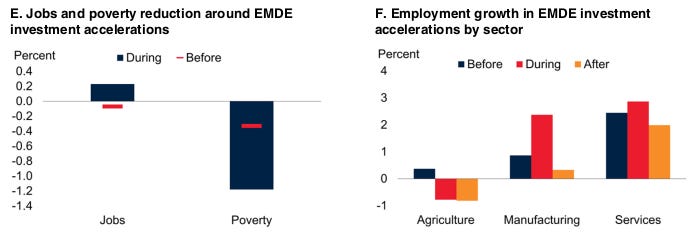

While there isn’t a clear link between GDP growth and jobs, however, there is a strong link between investment growth and jobs. When countries see investment booms, they also experience a major uptick in their levels of employment growth.

The report studies five countries with sustained employment booms — Australia, Chile, Colombia, Korea, and Singapore. All of them had a common signature: they saw a sustained period when investments grew by 9.5% a year, nearly four times the norm. With it came an employment growth of 3.4%. Some of them began their investment cycles from modest income levels, riding these waves to reach prosperity.

Attracting investment, in other words, is a key ingredient in job creation. But investment doesn’t come from nowhere. It chases places with foundational infrastructure, a business-friendly environment, and low barriers to moving private capital. Only, bringing this together, as India’s currently learning the hard way, is harder said than done.

The report identifies five sectors as most likely to absorb workers at scale — infrastructure and energy, agribusiness, tourism, health, and value-added manufacturing.

How are India’s prospects

No country faces this problem at the scale that India does.

In 2035, we shall have the world’s largest youth cohort: with 238 million people aged 15 to 24. This cohort shall be 40% larger than the only country with a population of rival size — China. We’ll add an extra 132 million working-age people by 2050. All of these people will need jobs.

How many jobs, exactly? It isn’t entirely clear. One prominent study estimates that India needs between 60 million and 148 million new jobs by 2030. That is a 2.5x range. This wide dispersion exists because it isn’t clear how many women we can even hope shall enter the workforce. If India’s female participation stays roughly where it is, you get the “easier” target of 60 million. If India manages to bring women into paid work at scale, we shall need roughly 148 million new jobs.

In other words, our gender issues add a substantial amount of confusion to our job requirements.

To be fair, some recent data shows more women entering the workforce. The Periodic Labour Force Survey puts female LFPR at over 40% in recent rounds, up from about 23 percent in 2017-18. But those numbers are complicated. These new jobs are overwhelmingly in unproductive quarters: coming from rural self-employment and agriculture. These look like jobs, but they’re the sort of informal work that become part of the employment buffer without improving people’s lives substantially.

This is characteristic of a larger problem with India’s economy: so often, people participate in the labour force without real demand for their labour. They’re counted as being employed, but are, in reality, badly underemployed. Meanwhile, we’re struggling to create high quality jobs.

This is why chasing jobs alone isn’t enough. India’s larger challenge is to ramp up investment, and create productive jobs. That has proven challenging. On one hand, India has a reasonable degree of public investment. Public capital expenditure has risen more than fourfold since FY18, to over ₹11 lakh crore budgeted for FY26. Gross fixed capital formation, accordingly, has held at around 30% of GDP for three straight years.

Unfortunately, private corporate investment has not followed at the same pace, while household-sector capital formation appears to have weakened. While the government is working on infrastructure, for it to turn into jobs, we need broad private investment.

But things aren’t hopeless. We’re one of only two large developing economies — alongside China — where per-capita incomes actually grew closer to those of rich countries between 2019 and 2025.

In fact, we’ve already seen the sort of investment acceleration the report talks about. The report cites India’s 1990s liberalisation as an example of just that. As we cut tariffs, shut state monopolies in steel and telecom, and let the rupee float, we saw a massive influx of investment through the later half of the decade. That is what we need to replicate.

We won’t have that opportunity forever, though. As we’ve written before, our demographic window is closing. The size of our youth cohort is already falling. This opportunity won’t stay open forever.

The investment test

As the foreword to the report says, “A jobs crisis is not pre-ordained. Population […] sets the stage, but policy writes the script.”

This report spells that script out for us. Private capital has been reluctant to reach large parts of the developing world over the last couple of decades. This is a trend we need to invert. Every rupee we can get in investment translates into greater productive capacity for Indian workers. And if Indian workers can do more with their time, that improves the lot of everyone else.

There’s a lot of discussion on whether India’s growth is “jobless”. That isn’t the most important question in this debate, however. A better question is whether India’s public investment surge can precipitate a broader investment-and-reform cycle. That is what all of the report’s success cases have managed.

It is what turns a construction boom into a jobs boom.

Tidbits

[1] RBI proposes wider money market access for NBFCs and companies

The RBI has proposed allowing NBFCs to borrow and lend in the term money market, while companies would be allowed to participate as lenders. The move aims to deepen India’s short-term funding markets and improve access to liquidity beyond banks.

Source: ETBFSI (The Economic Times)

[2] Climate risks could threaten $55 billion of India’s green energy projects

A Zurich Insurance study estimates that nearly 90% of India’s planned renewable energy pipeline faces high climate risks from floods, hailstorms, wildfires and other extreme weather by 2030. Investing about $4.6 billion in resilience measures could nearly halve the projected damage.

Source: Bloomberg

[3] India may clear first major Chinese-linked auto investment in years

India is likely to approve a $370 million investment by Horse Powertrain, a Renault-Geely joint venture, marking one of the first major Chinese-linked manufacturing investments since foreign investment rules were relaxed earlier this year. The company plans to build hybrid powertrains and engines at Renault’s Chennai plant.

Source: The Economic Times (Bloomberg)

- This edition of the newsletter was written by Krishna & Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how large language model usage changed over the past eighteen months, through the public usage data of one busy AI marketplace.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉