2020: A space odyssey

Or, how India launched its private space age

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Space I: Birthing a future

The complications in India’s digitization story

Space I: Birthing a future

On Sunday, a 190-kilogram satellite, Mission Drishti, separated from a SpaceX Falcon 9, fired its thrusters, and settled into orbit around 500 kilometres above the earth. There, it began covering almost 8 kilometres every second — fast enough to circle the entire planet every 1.5 hours.

Mission Drishti was built in Bengaluru by GalaxEye, a five-year-old startup founded by IIT Madras alumni. It carries what the company calls an “OptoSAR” payload: that is, it has two sensors — one that takes images, and another that senses the earth through radar — letting it see through cloud cover and at night. An onboard AI processor will analyse some of its recordings in space, before the data even reaches the ground.

It is the largest satellite ever built by an Indian private firm.

Amidst all the politics and war and ugliness, there’s a stream of headlines that feel like they’ve arrived from the future. A week before Mission Drishti went up, Skyroot Aerospace flagged off its Vikram-1 rocket from Hyderabad to the launchpad at Sriharikota for what is expected, this June, to be India’s first attempt at a privately-built orbital launch. On Monday, Bengaluru’s Pixxel announced a tie-up with AI startup Sarvam to launch data centres into space.

None of this could have happened five years ago. The law, back then, simply didn’t permit a private Indian company to own and operate a satellite of its own.

How, then, did any of this come about? How did the law fall in place? When did the numbers start making sense? And, most importantly, can these futuristic firms become viable businesses?

That’s what we’re going to explore in this two-parter. Today, we’re looking at how space, as an opportunity, opened up to Indian business. In the sequel, we’ll look at the economics of this nascent industry.

Selling from space

Space, they say, is the final frontier. Out there is the entire cosmos; trillions of galaxies, each carrying hundreds of billions of stars, yet more planets, and other incredible formations that defy imagination. It is so incredibly vast that one cannot help but feel insignificant.

Turn that gaze inwards, though, and space is also a vantage point.

From 500 kilometres above the earth, in a single glance, you can see a sixth of the earth. You can see how our planet curves. Physics itself pulls you so fast that you glide past entire countries in seconds. To see the earth from up there, as astronaut after astronaut has written, is a humbling experience.

That vantage point also creates an economic proposition.

There are three things being in orbit gives us. One, it allows us to observe millions of square kilometers of the earth at once. Two, it allows us to do so repeatedly, letting us see how a region shifts and evolves over time. And three, it allows infinite scale: once we’ve put an asset out there, the incremental cost of observing more of the earth is practically zero.

Together, these create a single capability: space gives us a cheap, quick way of seeing what is happening on the ground. You can see a flood building up before the first drop of rain, or crop stress well before the harvest. You can tell where a ship is in the ocean, or where you can find minerals in the ground. Doing so from the earth would be slower and more expensive.

Consider India’s flagship crop insurance scheme, Pradhan Mantri Fasal Bima Yojana. The scheme ran into a fundamental challenge — if you’re trying to insure a farmer’s crops, you need to quantify how much they lost, and there’s no easy way of doing so. At first, the government tried something odious. It would carry out manual harvests at randomly selected plots, and then guess at what average yields for the area looked like.

Since 2023, though, the scheme has started relying on satellite data, along with machine learning, to create gram panchayat-level estimates of yields. This is both faster and more accurate, and reduces uncertainty for both the insurer and the farmer.

In a sense, the space industry is really a data industry, built on the back of infrastructure that moves through the nothingness above the sky at eight kilometers a second. What data it can transmit depends on what you can haul up there. Sometimes, it’s basic — television signals, calls, and so on. Sometimes, it’s specific, advanced information that entities like governments or insurance companies will pay enormous sums for.

This wasn’t always possible, though.

Space: An industry built for nationalisation?

Until recently, almost no country in the world ran space as a private business.

This was rooted, in part, in international law. The Outer Space Treaty makes states internationally responsible for all national activities in space, including by private firms. If countries were on the hook for whatever people did in space, most sensible countries would keep private entities under a leash.

More importantly, the numbers simply didn’t make sense. Space was too expensive, and the returns too uncertain. One needed to invest tremendous resources in launch vehicles, satellites, tracking and control infrastructure, and more. The hundreds of crores that would take could be wiped out in minutes. Failures were frequent, and catastrophic. This wasn’t the sort of risk private balance sheets were built for.

Finally, there were concerns of security. Launch vehicles and intercontinental ballistic missiles share the same technology. As do high-resolution imaging satellites and military reconnaissance satellites. These were closely guarded secrets which governments were reluctant to give away.

From the 1980s, though, the United States catalysed a shift that brought in private enterprise.

Until then, space was considered an integrated stack. A single entity like NASA would handle everything — building the satellite, putting it in orbit, operating it, receiving its data, turning that data into intelligence, and so on. The government would contract some tasks out to private industry, but in principle, it designed and funded missions end-to-end.

Starting with the Commercial Space Launch Act of 1984, though, it began unbundling parts of this stack for private entities to take over. The US government began stepping back, turning itself into a permitting agency that looked over missions that were designed and funded privately. It also began building a market: turning itself into an anchor customer for a new wave of private businesses.

Once this nascent market took hold, it started finding ways of turning space into a product.

Consider satellites. These were once bespoke products that would be designed from scratch before each launch. The late 1990s, however, ushered in the “CubeSat Revolution”, which made real the idea that you could have a standard configuration — say, a cube with each side 10 cm long — in which anyone could build satellites. This created predictability, and that predictability opened up a market. If you knew what size each satellite would be, you could create “CubeSat buses” that could take dozens of these into space at once, cutting costs down for everyone.

You could also build entire businesses around standard, off-the-shelf components, like solar panels, radios, batteries, propulsion modules, and more.

Once a market took root, it started creating its own momentum.

By the late 2010s, there was a private entity at every step of the space business. If you wanted to send something to orbit, you no longer needed to be a space agency. You could simply buy a spacecraft from a company like NanoAvionics, send it up on the next SpaceX rocket, communicate with it through AWS Ground Station, and so on.

India is now beginning a journey to something similar.

India’s great switch

Until recently, private entities participated in India’s space activity as contractors and customers. Companies like HAL, L&T and Godrej Aerospace built a business out of fabricating components for ISRO’s rockets and satellites. Meanwhile, ISRO had its own roster of private clients. In 1992, it set up Antrix Corporation, a wholly-owned commercial subsidiary, to deal with external customers to the Indian space programme.

But in all this, ISRO sat squarely in the centre. If you were a private entity with space-faring ambitions, the government was simultaneously your regulator, operator, and commercial counterparty. This occasionally led to disaster when those roles collided against each other.

The reforms

In 2020, however, the government made three major moves to structurally change India’s space sector.

One, it set up a new body — the Indian National Space Promotion and Authorisation Centre (or ‘IN-SPACe’) — to serve as an autonomous authoriser, promoter and supervisor of non-governmental space activity. The logic for this came from the Outer Space Treaty, which requires governments to authorise and supervise private space activity. Until IN-SPACe, we had no such body. Once it was in place, we had a framework under which private end-to-end space activity became legally possible.

Two, it tasked the PSU, NewSpace India Limited (or ‘NSIL’) to act as the primary commercial arm connecting India’s space program to industry. Until then, India’s space market was supply-driven: ISRO built space assets, and private entities could ask to access them. NSIL replaced this with a demand-driven model, where it would aggregate demand from the industry, and then connect it with capabilities developed inside ISRO. It was, in essence, asked to “productise” ISROs systems and abilities.

Meanwhile, ISRO was turned into a pure-play space research and development entity, that would push against the frontier: exploring advanced technologies, and sending out space exploration missions — including manned ones.

Basically, India’s space-stack was being unbundled.

The launch

In the years that followed, India would add more pieces to its space framework. By 2023, a new space policy had been locked in. The next year, in 2024, IN-SPACe would make the policy concrete with more detailed guidelines. 2024 would also see us liberalise our foreign investment laws, allowing as much as 100% foreign investment in large parts of the industry.

This policy push brought large parts of space within the reach of private industry. Private entities can now own and operate satellites. They can manufacture and operate the launch vehicles, and build the launch infrastructure to send them up. They can take up satellite spots in the sky, book frequencies to connect back to the earth, and disseminate remote sensing data. None of this was possible before.

In just a few short years, you can see the green shoots of a new industry. Early on, between November 2022 and December 2024, IN-SPACe issued 38 authorisations to 23 different private entities. But as the new regulatory regime fell into place, interest exploded. By March 2025, it had received over 658 applications for various space-related business ventures. It was also commercialising ISRO’s technologies heavily, having entered over a 100 technology transfer agreements by September last year.

This is the wave that startups like Galaxeye and Skyroot belong to.

The way ahead

We’re at the cusp of a genuine, functioning space industry. But there’s still some way to go.

For one, at the moment, there’s no parliamentary law that brings this all together. A Space Activities Bill has made its way to the Parliament repeatedly since 2017, but so far, it has gotten nowhere. A new draft is reportedly winding its way around the government once more, but it’ll probably be some time before the law is passed. There are other regulatory problems the industry will have to work through — including a possible turf war for satellite communications.

But there’s a more fundamental question ahead: one of profitability

This is a business with brutal economics, and the commercial logic is yet to fall in place. There is a generation of entrepreneurship ahead before the industry actually cements its position. A project like Mission Drishti is a remarkable achievement, and is probably a sign of incredible things to come. But it isn’t yet a business.

If there’s one thing that makes us hopeful, though, it is that as we saw in the US, markets can create their own momentum. That, we will dig into in the next part.

The complications in India’s digitization story

Consider what it costs a small manufacturer in India to get a construction permit for their factory.

Before 2015, this typically meant visits to multiple government offices in sequence, physical documents submitted to separate departments, inspector visits on their own timetable, and an informal layer of discretion that determined how long any of it actually took. For a large company, this is much easier to deal with. But for a five-person workshop, it can be the owner’s entire week, or more.

This is the productivity tax that rarely makes it into economic models. A new IMF working paper, published this month, tries to measure it.

The paper finds that when Indian states digitized their administrative processes in the mid-2010s, the productivity of India’s smaller enterprises actually went up. It is certainly a meaningful finding.

But this is also a story with a complicated second act. The same small businesses the reforms were designed to help went on to face a chaotic digital transition, which included a cash crunch due to demonetization. Additionally, the formal credit system never quite caught up with their needs.

The IMF paper’s finding and its complications, taken together, are a reasonably complete picture of how difficult India’s digitalization story has actually been for our MSMEs.

Small reforms, big bang

It’s well known that India’s MSMEs are one of the economy’s more peculiar features — enormous in aggregate, nearly invisible in formal statistics. They employ around 32 crore workers, contribute ~35% of manufacturing output, and account for nearly 49% of the country’s exports.

Yet, according to the MSME Census, many of them are not registered under the Companies Act. They are proprietor-run workshops, family partnerships, and informal units which are legally unincorporated. They often operate largely outside the formal financial system, and are heavily dependent on the owner’s time for anything administrative.

This is what makes compliance costs structurally different for them. When a large firm files its returns or renews its environmental clearance, it has staff. When a small manufacturer does it, that task competes directly with production.

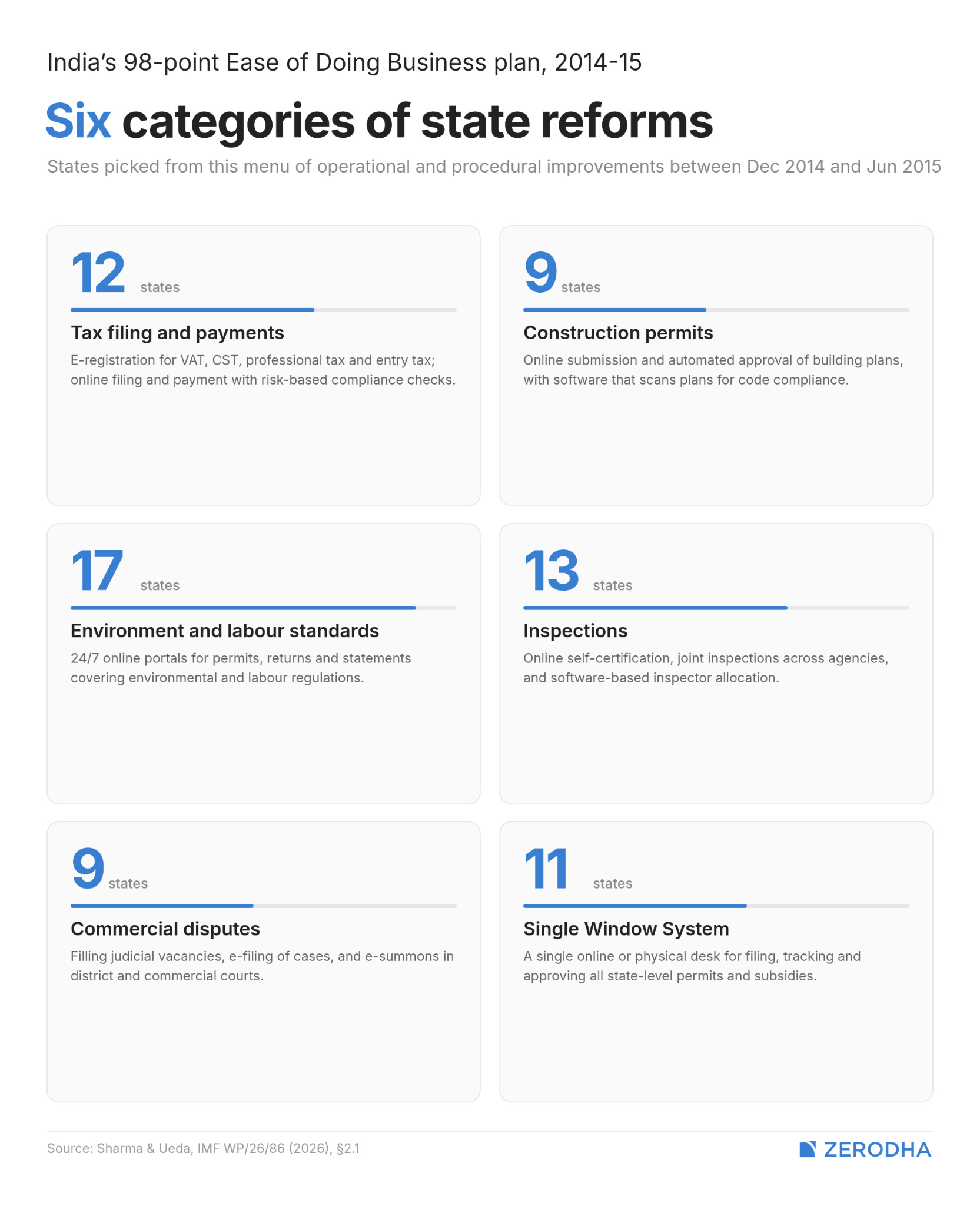

However, in the mid-2010s, the paper notes that different states undertook varying degrees of reform in public administration. The most notable of them was in December 2014, when state chief secretaries finalized a 98-point action plan on ease of doing business. The paper divides all these reforms into 6 categories, which include: tax filing and payments, construction permits, environment and labour regulations, inspections, commercial disputes, and single-window clearance systems.

Different states implemented different numbers of reforms. Critically, the states that did more reforms weren’t systematically richer or faster-growing before the reforms began. The variation in reform depth appears to have been driven by administrative capacity and political prioritization, rather than pre-existing economic advantage.

The paper uses National Sample Survey data on unincorporated enterprises — roughly 3.3 lakh firms in 2010-11 and 2.85 lakh firms in 2015-16 — matched on size, age, location, and industry across states with different reform profiles.

What the data shows

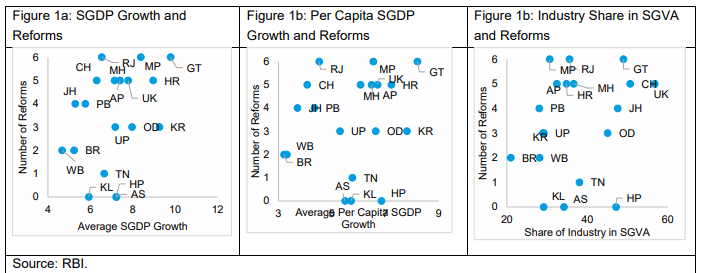

The core finding was that firms in states that implemented more of the reforms saw larger productivity gains than comparable firms in states that reformed less. Gujarat, Madhya Pradesh, and Rajasthan — which were also furthest ahead on the 2014 reforms — outperformed nearly every state they were paired against.

Each additional reform category a state adopted added to firm productivity, though with diminishing returns. While the 2014 reforms were the major inflection point, the results made it clear that cumulative reforms over time helped.

While the headline finding is useful, the dispersion result is more consequential.

Before the reforms, there was wide variation in how efficient similar firms were — even within the same industry in the same state. In high-reform states, that gap narrowed significantly by 2015-16. The authors trace this primarily to capital being allocated more evenly across firms after the reform.

How so? See, in the pre-reform environment, when approvals for permits were incredibly difficult to get, you only had so many choices. You would try to get inspections expedited through personal connections, or even informal payments. The firms that benefited from this weren’t necessarily the most productive. While digital systems may not have fully removed this problem, they’re more likely to process applications without room for personal discretion.

The logic extends to the kind of small administrative interventions that rarely get credit for doing much — we covered many such recent reforms in a past story.

For instance, the Investor Education and Protection Fund Authority (IEPFA), which is the government body that administers unclaimed dividends and shares, digitized its claims process. It didn’t change anything fundamental about financial markets, but simply removed a step that previously required navigating a tiresome, bureaucratic process. This small change significantly improved their approval rate from 850 monthly applications to 9,100.

Multiplied across six categories of administrative reform and tens of millions of firm-level interactions, that equalization effect is what the IMF paper is actually measuring.

What the paper can’t tell you

However, the IMF paper’s findings come with some very important caveats, and even counter-arguments.

A short, narrowly-scoped window

For one, the paper’s scope is only limited to digitization in bureaucracy, and not in the day-to-day operations of an actual company. This problem also applies to its data, which only runs from 2010 to mid-2016.

This makes it hard to ignore the fact that the paper predates what is perhaps the biggest digital shock to India’s economy: demonetization. Overnight, it invalidated over 80% of the currency in an economy that ran almost entirely on cash.

A paper by ex-IMF chief Gita Gopinath, Gabriel Chodorow-Reich et al. found that the cash shock caused by demonetization immediately contracted output, employment, and bank credit in the most exposed districts. The firms hit hardest were precisely the unregistered, cash-dependent microenterprises the IMF paper had been tracking.

In fact, in a past Daily Brief story, we covered a different paper by economist Yutong Chen, which looked at how digitization set back small manufacturing firms, whilst bolstering service sector firms, which were more digital-ready.

The IMF paper is a study of deliberate, process-by-process administrative reform, where the government digitized its own side of specific bureaucratic interactions. Demonetization was its opposite: a sudden, economy-wide mandate imposed on private actors without warning. Both can be filed under India’s digitalization story. But they have little in common as policy instruments, and their effects on small businesses point in divergent directions.

Is paperwork actually the binding constraint?

Secondly, the reforms the paper measures are administrative. They reduce compliance cost and friction. But they don’t directly address what most analyses of MSME underperformance identify as the larger bottleneck: access to capital.

Even after a small manufacturer sorts its permits and clearances out, it still needs credit to scale. If a bank won’t lend because the firm lacks collateral, formal income documentation, or even a credit history, the administrative improvements will be limited in their reach. We’ve covered this problem all too often on The Daily Brief.

India’s MSME credit gap runs into the hundreds of thousands of crores. Fixing the permit portal and fixing the credit system are both necessary. But progress on administrative ease doesn’t necessarily translate into progress on financing access. To be sure, the IMF paper doesn’t make any such far-fetched claim, either. But it’s an important gap to highlight.

The DPI-GDP disconnect

The third counter-argument takes a stab at the idea that digitization was undoubtedly a force for good for India’s economic growth.

A 2025 discussion paper by CSEP attempted a broader assessment of India’s digital public infrastructure (DPI) and found ambiguous results. What they found was that states that adopted digital infrastructure more aggressively didn’t consistently show proportionally better economic outcomes. The relationship didn’t hold cleanly.

Now, the two studies are measuring different things, across different time periods, using different methodologies. But it does suggest that the link between government digitalization and economic growth is not as clean as one might think. The natural experiment that gives the IMF paper its credibility also means it captures the reforms in isolation from everything else happening simultaneously — like credit cycles, state-level capacity, or the demonetization shock.

What comes next

India’s digitization push has never moved in a straight line.

On one hand, you have the 98-point action, which was certainly a much needed reform. It made a remarkable difference to the productivity of the firms that needed bureaucratic relief the most. Meanwhile, it also reduced the distortions that allowed connections to substitute for efficiency.

But the paper also captures a narrow window.

India’s digitization efforts are much broader than just improving bureaucratic efficiency. They affected almost every crevice of the Indian economy. And while the bureaucratic efficiency has been welcome, some of the broader pushes — like demonetization — may have slowed the economy down.

What India’s smallest businesses need now is less about fixing the government’s interface with them, and more about what that government makes available on the other side of the window.

Tidbits:

The National Company Law Appellate Tribunal dismissed Vedanta’s challenge to Adani Enterprises’ Rs 14,535 crore winning bid for debt-ridden Jaiprakash Associates, rejecting Vedanta’s claim its bid was Rs 3,400 crore higher, stating Committee of Creditors’ decision based on commercial wisdom including upfront cash and feasibility was valid.

Source: The HinduIndia allowed traders to export 5 million tonnes of wheat after lifting the 2022 ban, with ITC shipping first 22,000 tonnes to UAE at $275/tonne FOB, but Indian wheat remains $20/tonne costlier than Australian and Black Sea supplies, limiting demand to buyers needing prompt 30-45 day deliveries.

Source: ReutersThe Indian government will not compensate state-run fuel retailers for losses from selling transport fuels below market prices, as a petroleum ministry official confirmed. This is despite companies raising prices for industrial customers, foreign carrier jet fuel and bulk diesel buyers (10% of sales), while keeping retail prices unchanged to protect consumers.

Source: ET

- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Pranay Kotasthane on Navigating the New Uncertain World

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Pranay Kotasthane, one of the sharpest minds we read to understand India and its place in the world. We’ve often featured his insights on this newsletter. This time around, we got him on for a long conversation — one that spans a wide breadth of topics: the world India now has to play in, why the panic around critical minerals is overdone, what’s actually holding back manufacturing, what an India-shaped opening in AI might look like, why Bengaluru feels as stuck as it does, and more. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

India's Space odyssey does feel like we're finally heading towards a sci-fi future! I covered similar topics in my ISRO deep dive, including how indigenous satellites are helping save lives and livelihoods, here: https://www.read.rohitnalluri.com/p/from-saving-lives-to-building-space?r=5h5o0&utm_campaign=post&utm_medium=web

I'd definitely appreciate a read!