No Buyers for Maruti, No Limits for Zuckerberg, No Path for Growth | Who said what? #20

Hello, Welcome to the 20th episode of Who said what? Thanks for tuning in every week.

I’m Krishna and this is the show where I dive into interesting comments by notable figures from across the world—whether it’s finance or the broader business world—and dig into the stories behind them.

Today I have 4 four very interesting comments from RC Bhargava, Mark Zuckerberg and a few others.

Nobody is buying entry level cars

Imagine you run a car company. For decades, you’ve been growing steadily, expanding your reach, and building a reputation as the country’s largest carmaker. But over the past few years, something strange has been happening. The segment that once made up nearly 40% of your sales—the small, affordable cars—has started shrinking. Not just slowing down, but actually declining.

What do you do?

If you’re RC Bhargava, the Chairman of Maruti Suzuki, you call it like it is. In his latest remarks, he pointed to a hard economic truth that few in the industry openly admit: most Indians simply can’t afford to buy a car anymore.

That’s a bold thing to say, especially from someone like him.

Here’s how he broke it down:

That’s two-thirds of all Indian households earning less than around 5lakh annually. And it gets more stark.

In other words, just 12% of Indian households earn enough to even think about buying a car that costs ₹10 lakh or more. And that price tag, Bhargava says, is what it now takes to own a typical car in India—thanks to rising input costs, stricter safety and emissions regulations, and taxes.

“Car buying in India is largely restricted to this 12% of households.”

Which leads to the real punchline:

This is the crisis at the heart of India’s auto industry. It’s not that demand has disappeared because people don’t want cars. It’s that the majority of Indian households have been priced out of the market.

And yet, it wasn’t always like this. For years, small, affordable cars like the Alto or WagonR were the engines of growth. But as regulations tightened—with mandatory airbags, ABS, stricter crash tests, and cleaner emission standards—the cost of compliance has quietly pushed up the price of entry-level cars by ₹80,000 to ₹90,000 per vehicle.

And, Mr. Bhargava didn’t mince words:

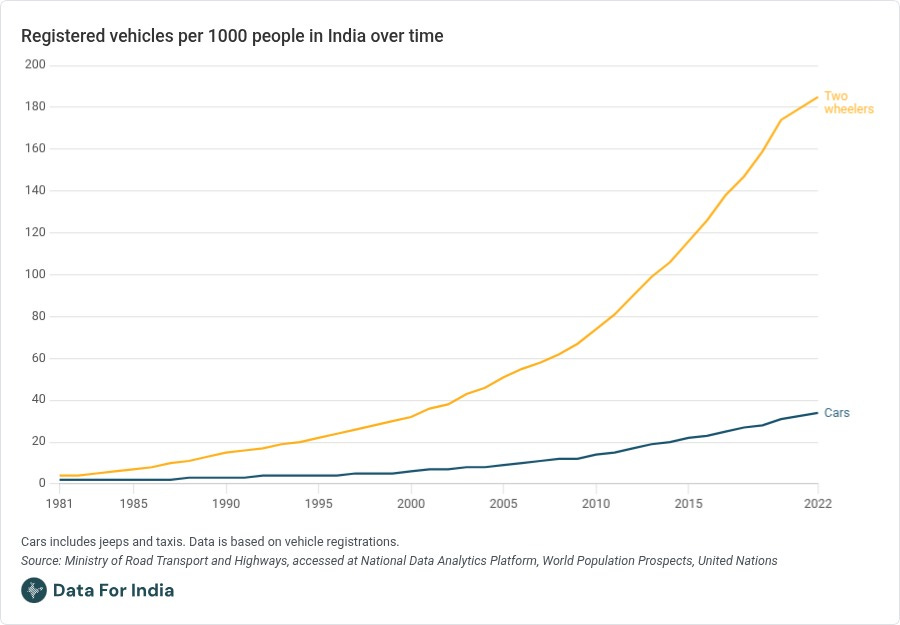

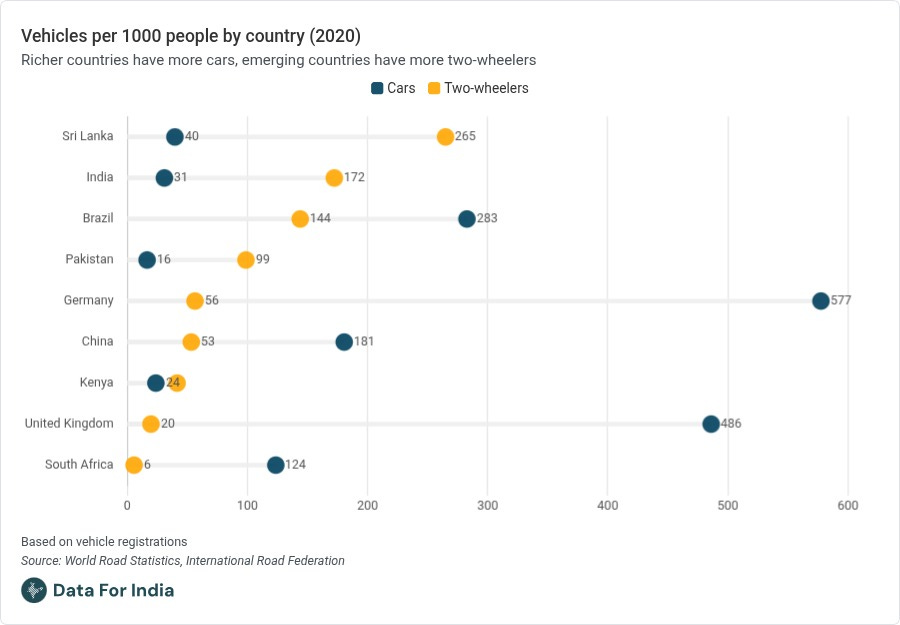

It’s not just incomes that are holding back demand. India remains one of the most underpenetrated car markets in the world. Right now, India has about 34 cars per 1,000 people. ‘

For comparison, Indonesia has 90. China has nearly 250. The US? Over 800. Even with such low penetration, Bhargava warns that growth has stalled because the addressable market is simply too small under current pricing.

He worries that policymakers and industry watchers have misunderstood what’s happening. Some say Indians are shifting from small cars to bigger, pricier SUVs because they aspire for better status and features. RC Bhargava flatly rejects that:

And if small cars are unaffordable, upgrading from a two-wheeler to a car becomes a distant dream. Today, India sells nearly 20 million two-wheelers every year—because, for the vast majority of Indians, a motorcycle is the only affordable personal vehicle.

So what’s the solution? Bhargava looks to Japan for inspiration. He points to their kei cars—tiny, ultra-affordable cars with lower taxes, fewer regulations, and targeted incentives that helped millions of Japanese households upgrade from scooters to cars.

India, he says, needs a similar rethink. Right now, cars are taxed at 28% GST plus cess, making even the cheapest cars out of reach for most buyers. Lowering taxes and relaxing some regulations for truly affordable entry-level cars could be the only way to unlock mass demand again.

Because if nothing changes, the future of the Indian car market may not be millions of first-time buyers moving up from two-wheelers—but rather a stagnant, slow-growing market catering only to the country’s wealthiest 12%.

“Unless somebody can find to bring the cost of the EV down by half or less… affordability.”

“Today nobody can develop at that cost, not even the Chinese.”

For Bhargava, the message is clear: without a car that the average Indian can afford, growth will stay stuck.

Mark Zuckerberg’s beautiful, dystopian fantasy

Especially if you’ve not been paying attention, Meta seems like the biggest AI laggard. Its models garner nowhere near the hype that new labs like OpenAI and Anthropic regularly see. Even its big tech competitors, like Grok or Gemini, have much more mindshare. DeepSeek’s excellent open weight models have blunted Meta’s open sourcing edge as well.

But the AI race isn’t anywhere near being over. And Meta’s pulling out the big guns, bringing everything it has learnt over this years, for this new project. Or at least that’s the signal we’re seeing in a recent interview that Mark Zuckerberg gave to Dwarkesh Patel.

For one, Meta’s next bet is to create an AI that knows you intimately. It’s doing so using a “personalisation loop”. As Zuck told Dwarkesh:

“I think this is going to be a really big year for all of this, especially once you get the personalization loop going, which we’re just starting to build in now really, from both the context that all the algorithms have about what you’re interested in — feed, your profile information, your social graph information — but also what you're interacting with the AI about. That’s going to be the next thing that's super exciting. I'm really big on that.”

Look, if you’re a regular user of AI, you’ve probably already been creeped out a couple of times by what all it knows about you. And if that hasn’t yet happened to you, just open your most used AI app, and ask it to give an honest, unfiltered opinion of you without sugarcoating things. Yeah, it knows things.

Zuckerburg wants to dial this up to 11. Meta already has years’ worth of data on you, from all your Facebook and Instagram activity. He’s going to teach all that to AI as well. You know how Reels have that scary ability of giving you junk that’s tailored exactly to the person you are, keeping you watching for hours at an end? Well, the AI you talk to might soon have that uncanny understanding of you as well.

But that’s not all. There’s another ingredient to this: he wants to change how people interact with AI apps from the current chatbot-centric way of doing things, to something much more conversational. From his conversation with Dwarkesh, once again:

“Being able to mix [Meta’s new voice model] in with the right personalization is going to lead toward a product experience where, if you fast-forward a few years, I think we're just going to be talking to AI throughout the day about different things we're wondering about.

You'll have your phone. You'll talk to it while browsing your feed apps. It'll give you context about different stuff. It'll answer your questions. It'll help you as you're interacting with people in messaging apps. Eventually, I think we'll walk through our daily lives and have glasses or other kinds of AI devices and just seamlessly interact with it all day long.

That’s the north star. Whatever the benchmarks are that lead toward people feeling like the quality is where they want to interact with it, that's what will ultimately matter the most to us.”

Now, we’ve already seen other labs focus on having AI models talk. That’s not an innovation by itself.

What caught our attention, though, was the overall vision: of you constantly in touch with your voice-based AI companion all day long — a little like Ironman and JARVIS. For that to happen, it’s not enough that your AI app is intelligent, or capable. It needs to also be sticky.

That’s what stands out to us. Meta’s focus, with AI, is no longer just on making it more intelligent. Zuckerburg wants to break away from the current AI benchmarks, where they test if models can solve a set of increasingly difficult problems. If you’ve ever wondered why people keeping talking about things like how well models can solve PhD-level maths questions, it’s because of these benchmarks.

“You also mentioned the whole Chatbot Arena thing, which I think is interesting and points to the challenge around how you do benchmarking. How do you know what models are good for which things?

One of the things we've generally tried to do over the last year is anchor more of our models in our Meta AI product north star use cases. The issue with open source benchmarks, and any given thing like the LM Arena stuff, is that they’re often skewed toward a very specific set of uses cases, which are often not actually what any normal person does in your product.

The portfolio of things they’re trying to measure is often different from what people care about in any given product. Because of that, we’ve found that trying to optimize too much for that kind of stuff has led us astray. ”

Instead, Meta wants to crack some way of pushing people to constantly go back to their AI app. And it has a track record of doing so. You know how you seem to open Instagram without thinking, whenever you’re idle, because it’s just so addictive? Well, that’s the kind of thing Zuckerberg wants to bring to AI.

And they might just have cracked the form factor that allows this, with the Meta glasses.

“I think that's part of the reason why the Ray-Ban Meta product has done so well. It's great for listening to music, taking phone calls, taking photos and videos. The AI is there when you want it. But when you don't, it's just a good-looking pair of glasses that people like. It gets out of the way well.

I would guess that's going to be a very important design principle for the augmented reality future. The main thing that I see here is this. It's kind of crazy that, for how important the digital world is in all of our lives, the only way we access it is through these physical, digital screens. You have your phone, your computer. You can put a big TV on your wall. It's this huge physical thing.

It just seems like we're at the point with technology where the physical and digital world should really be fully blended. That's what holographic overlays allow you to do.”

That’s right — Meta’s old “Metaverse” dreams aren’t over. They’ve evolved into a pair of AR-enabled glasses that will eliminate the need for specific computer devices. And because of that, they might be something that you’re constantly in touch with, as though they’re simply another layer to your physical world.

Bring this all together and you see Zuckerberg’s grand vision. A new device that’s always on your eyes, an AI who you’re constantly talking to, which knows you inside out, and is fitted with algorithms that marry your AI with the addictiveness of Instagram.

I’m not sure if the future makes me excited or uncomfortable.

To bring this whole vision to fruition, Meta plans to move to AI agents that will code the next generation of AI. And no, I don’t mean AI models helping human developers code, the way so many do today. I mean agents that basically act as complete, virtual software engineers.

“We're trying to build a coding agent and an AI research agent that advances Llama research specifically. And it's fully plugged into our toolchain and all that.

That's important and is going to end up being an important part of how this stuff gets done. I would guess that sometime in the next 12 to 18 months, we'll reach the point where most of the code that's going toward these efforts is written by AI.

And I don't mean autocomplete. Today you have good autocomplete. You start writing something and it can complete a section of code. I'm talking more like: you give it a goal, it can run tests, it can improve things, it can find issues, it writes higher quality code than the average very good person on the team already.”

On one hand, this probably means we’re soon approaching a point where AI development will suddenly take off at a level we can’t imagine, with physical infrastructure being the only limiting factor for how fast we can go. On the other hand, every dystopian AI sci-fi story begins with AI learning to train AI. So there’s that.

Gita Gopinath and Raghuram Rajan on central bankers

A big part of our job—by that I mean the people running this channel—is to stay in touch with the news all the time. But I’ll be honest: this whole saga around tariffs is something I’ve been actively trying to avoid. One day they decide something, the next day everything changes, and this has happened so many times now that I just tapped out of it.

But here’s the thing—even if me or anyone else has tuned out of the daily back-and-forth, the impact of all this is very real. This constant flip-flopping has created this whole mood of uncertainty hanging over the global economy. Even the IMF, in their latest World Economic Outlook report, basically admitted it. I’d written about this earlier inThe Daily Brief. In fact, things are so uncertain right now that the IMF had to switch how they make predictions. Normally, they use something called a baseline forecast—basically their best estimate of how the world will look next year. But this time they couldn’t even do that. Instead, they had to use what they called a reference scenario. Which is really just freezing their model and saying: “Okay, let’s assume the world looks like this—these tariffs, these interest rates, this level of chaos—and we’ll base our numbers on that.” It’s like admitting: “We don’t know what’s going to happen, so let’s just freeze the madness here and work with it.”

Now, why am I telling you all this? Recently, the IMF released a video where Gita Gopinath, the IMF’s Deputy Managing Director, and Raghuram Rajan, the former RBI Governor, were talking about how emerging countries like India have actually handled these tough times pretty well.

Here’s what Gita Gopinath said:

But then she explains why they were able to stay strong. She says:

Now, she’s saying that countries like India, built strong systems for keeping inflation under control. They had clear targets for inflation, they didn’t panic and change their approach every time something went wrong globally. They stayed the course. And because of that, they earned something super valuable in central banking: credibility.

But here’s where it gets tricky.

She points out that staying credible in today’s world is way harder than it used to be. The answer is again—unpredictability. And when everything’s changing all the time, it becomes really hard for central banks to communicate clearly. And the tough part, she says is, if you explain too much, people might get confused or think you’re flip-flopping. But if you explain too little, people might think you’re hiding something or that you don’t have a grip on things.

And that’s when she turns to Raghuram Rajan and basically asks him:

He says:

Yeah, I didn’t understand this other, I took help of ChatGPT.

He’s saying that it doesn’t matter if the law says the central bank is “independent.” If people, politicians, or society stop trusting the central bank, no piece of paper is going to save it. Independence isn’t something you automatically get because it’s written in law—it’s something you earn by convincing people that you’re doing something important, that you’re holding things together.

And he explains it even more:

Basically: a central bank’s independence depends on the people who believe in it. It could be investors who care about low inflation. It could be regular people who just don’t want prices to spiral out of control. If those people believe the central bank is protecting them, they’ll stand up for its independence.

Then he talks about communication:

Here he’s saying: a central bank can’t just talk to economists. It needs to talk to regular people. It needs to explain: “Look, we’re not randomly changing interest rates. We’re doing this to keep inflation under control, so your savings don’t lose value, so food prices don’t go crazy, so the economy stays steady.” You have to help people understand why your work matters to them personally.

But then he gives this really honest warning:

Then Rajan talks about something really relatable for anyone in India: the dollar-rupee rate. He says that in India, everyone—from politicians to middle-class families—watches the dollar-rupee exchange rate not anything else.

Parents sending their kids to study in the US, businesses importing or exporting goods—they all care about how many rupees it takes to buy one dollar. If the rupee falls fast, people start to panic. Parliament asks questions. It becomes political.

So what does the Reserve Bank of India do? Rajan explains that they don’t try to fix the exchange rate at a specific number. They don’t say, “₹80 per dollar and that’s it.” That would be risky. Instead, they focus on smoothing out the big swings. If the rupee’s falling too fast, they slow it down. If it’s rising too fast, they slow that too. The goal isn’t to defend a number—it’s to prevent chaos.

Finally, Rajan warns about something central banks in richer countries like the US have done: buying government bonds or other assets to stabilize markets. He says: sure, it can work for a while. But one day, the central bank will have to sell those assets. And when that happens, it could cause prices to crash. And that creates new problems.

In the end, both Gita and Rajan are basically saying: in today’s world—where everything’s unpredictable, policies keep changing, markets are jittery—central banks in emerging markets have to be really, really careful. They need to stay independent, communicate clearly, manage inflation, keep markets calm, and use their tools wisely.

The End of Manufacturing-Led Growth?

India’s Finance Secretary, Ajay Seth, in a recent interview at the Hudson Institute spoke about India’s goal of becoming a developed country by 2047. He made some striking claims about manufacturing and development—claims that challenge a lot of what we’ve been taught about how nations grow rich.

These comments jumped out at me because they go directly against the playbook that transformed Japan, South Korea, and more recently China from poor to prosperous. And they tie into an even bigger argument from economist Richard Baldwin, who believes the old path to development is closing for newcomers.

Seth’s Challenge to Export-Led Growth

He was clear: manufacturing is still critical for India’s future. With 55% of Indians living in rural areas and 40% relying on agriculture (which only makes up 17% of GDP), he called moving people into non-farm work “an absolute imperative.”

But here’s where it gets really interesting. Seth explicitly rejected the traditional export-led model. He said:

“The economic model of growing by exporting with or without significant domestic consumption is no longer valid in the 21st century.”

Instead, he pitched a more balanced approach:

“Make for India, make for the world.”

Why? His argument is that a country of 1.4 billion people can’t depend on imports alone. And beyond that, relying too heavily on exports while keeping domestic consumption low just creates global trade imbalances. As he put it:

“Any economy trying to export its way while keeping domestic consumption low creates imbalances for the global economy.”

The Golden Path That May Be Closing

To really understand why Seth’s comments matter, you have to look back at how other countries got rich.

Japan was the first to show what manufacturing-led growth could do after World War II. They started with textiles, moved into steel and shipbuilding in the 1960s, then into cars and electronics in the 1970s, and later into semiconductors and robotics in the 1980s. This steady climb up the value chain delivered 10% growth a year for decades.

South Korea copied that model almost step for step. Starting in 1962, they launched five-year plans, picked big family-run conglomerates (the chaebols), gave them cheap credit and protection—but insisted they export. The payoff was huge: per capita income jumped from $103 in 1962 to $5,438 by 1989.

China got a later start but scaled even faster. They kicked off Special Economic Zones in places like Shenzhen in 1979, offering tax breaks and infrastructure to lure in export-focused manufacturers. The results were staggering: nearly 10% growth a year for 40 years, 800 million people pulled out of poverty, and China becoming “the world’s factory,” now making nearly 30% of all global manufacturing output.

Each of these countries followed the same formula: use cheap labor to build export industries, then slowly move up the ladder into higher-value products.

Baldwin’s Warning: The Ladder Is Being Pulled Up

But Richard Baldwin, an economist who’s been studying this for years, thinks that ladder is getting harder to climb. His research shows that from 2008 to 2020, 60% of lower-middle-income countries—and a whopping 85% of other developing economies—didn’t follow this manufacturing-export path. In fact, many were moving in the opposite direction.

Why? Baldwin points to three big shifts.

First, automation. As he explains:

“Digitech automates labour out of manufacturing” and “international cost differences shrink.”

Translation? Robots don’t care if labor is cheap. Automation makes wages less of a deciding factor.

Second, China’s dominance. Baldwin says China has become “t” with an output bigger than the next nine countries combined. China overtook the U.S. in manufacturing share back in the late 2000s—and has since doubled it. There’s just not much room left for new players.

Third, the rise of digital services. Baldwin predicts that “intermediate services trade will grow much faster than goods trade for the foreseeable future.” In other words, services—not factory goods—are going to drive global trade growth.

The Service Alternative

Baldwin thinks the future is about “service-export-led growth.” Instead of copying China’s Shenzhen, he imagines developing countries building the next Bangalore: development hubs powered by skilled workers and digital tools, not assembly lines.

And interestingly, Seth’s vision for India seems to echo this shift. While he still sees a role for manufacturing, he’s betting big on services too. A prime example? India’s three-layer Digital Public Infrastructure.

The first layer is Aadhaar, India’s national ID system, which processes 90 million authentications every day. The second is UPI, India’s instant payment system, which handles 550 million transactions worth $9 billion daily. And the third layer is a consent system to protect data privacy.

This digital backbone has transformed India’s economy without relying on traditional manufacturing. As Seth pointed out:

“One in every two adult Indians does a transaction in a day.”

Thanks to UPI, transaction costs are just 0.05%—compared to 1.8% for credit cards. That’s a huge gain in efficiency.

Democracy’s New Advantage

There’s another fascinating piece to Seth’s argument: he insists democracy is essential for development.

“Coming from a country with 1.4 billion people, being a beneficiary of a democracy, I don’t see any other viable means of governance.”

This flips another piece of conventional wisdom. The old manufacturing model often worked best under authoritarian regimes that could suppress consumption to boost exports. Democracies, by contrast, had to balance citizen demands with economic goals.

But a services-led model needs things like reliable electricity, internet access, and educated workers—investments that often happen faster in responsive democracies where voters can pressure leaders for better services. As Seth put it:

“It is incentives which work with the people,” not top-down commands.

The Stakes Are High

Seth believes India can keep growing at 7% a year over the next decade. If the global environment is favorable, maybe even 7.5%; if not, maybe 6.5–7%. But hitting those numbers means India has to deepen its domestic growth drivers and boost productivity.

If Baldwin’s right that “manufacturing export-led growth is dead or dying,” then developing countries face a sobering truth: the escalator that lifted billions out of poverty is slowing down—just as more people are trying to get on.

This debate between Seth and Baldwin isn’t just academic. It’s about whether the global economy still offers a clear, reliable path from poverty to prosperity for the billions who haven’t made that journey yet.

🧑🏻💻Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

Please let me know what you think of this edition.

Great stuff as always! Interesting, insightful and unique!

Man, fantastic article... seriously makes one think... thanks much for putting out info/thoughts like these.