WTO just sent a Warning!

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

An era of shrinking trade?

Jerome Powell sees storm clouds gathering

Indians and the global gold rush

An era of shrinking trade?

We’ve spent the last few weeks screaming hoarse about how the Trump tariffs will upend international trade. Of course, you should always take forecasts with a pinch of salt, especially when there are so many things up in the air — and when there’s an event that shakes up the entirety of global trade, everything is up in the air. But everything we’re looking at seems to indicate that, at least in the near future, things could get bleak.

Case in point: the World Trade Organization just released their April 2025 outlook. The picture they're painting isn't pretty. They're forecasting a contraction in global merchandise trade. In fact, their latest estimates see them backtracking from estimates they made just a few months ago, at the start of this year. Back then, they were mildly optimistic about the fate of global trade. But we’re in a new paradigm now, and all the old assumptions have fallen apart.

As they openly admit, these latest estimates are just their best guesses. Even they don’t quite know where things are headed, even though they’re literally the global authorities on world trade. They tell you to take their forecasts with a pinch of salt.

But if you’re looking for a way of thinking about what could happen amidst all this uncertainty, this is as good a place to look as any. Let's dive in.

A time of historic uncertainty

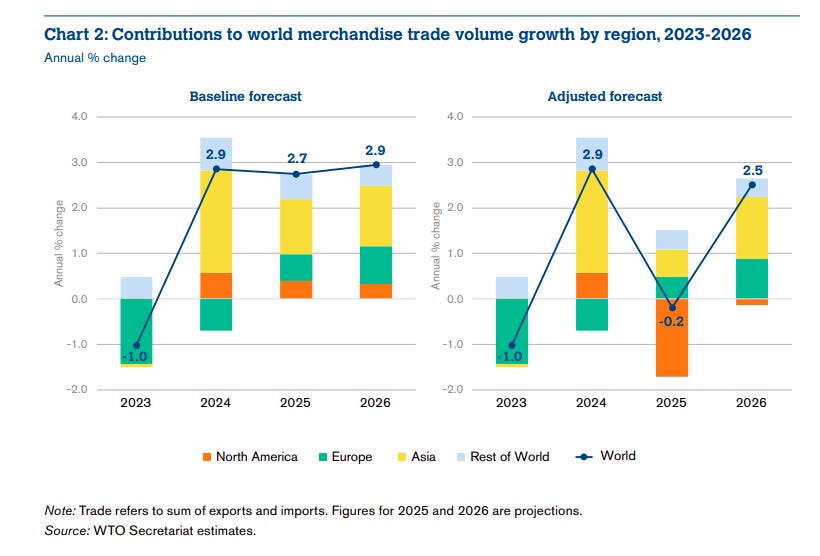

When this year began, the WTO thought global trade would grow by close to 3% in both 2025 and 2026. Back then, they assumed that trade would proceed as usual — with fluctuations in demand and supply, and perhaps the odd political disruption, but nothing out of the ordinary.

That might have been the case, except that they couldn’t have predicted the sledgehammer that was Trump’s trade policy. In a few short months, global trade has been hit by intense headwinds — baseline tariffs, country-specific tariffs, auto tariffs, steel tariffs, and frictions of every other sort.

Suddenly, the global trade picture looks very different. The world’s largest importer has been yanked out of the global economy by force. And that has pushed the WTO to recalibrate all its assumptions. It now expects global merchandise trade to actually shrink by 0.2% in 2025. All their hopes of growth have evaporated.

This whole situation, the WTO says, is simply unprecedented in recent history. Their economists are currently working without a playbook, because there’s never been a comparable policy shift in the modern era of global trade. This is a little like trying to forecast the weather during the middle of the biggest hurricane ever recorded. A big chunk of their report is just them talking about how they’re trying to make sense of the uncertainty — by modelling something called ‘trade policy uncertainty’. More on that in a bit.

Oh, and things could be even more negative. Trump’s liberation day “reciprocal tariffs” have been paused for now, and people are hoping they don’t come back. But that’s not the sort of thing you can bank on — not with his track record. If those come back into effect, as originally planned, we could see global trade decline by as much as 1.5% this year.

In just a few months, we've gone from expecting a healthy growth in trade to projecting the kind of disaster we last saw during the global financial crisis.

Regional breakdown

Of course, this pain isn't being felt evenly around the world.

As you’d expect, North America is taking the biggest hit. After all, the U.S. is at the center of these trade tensions, so North American trade flows will obviously take the biggest beating. The region is expected to subtract 1.7 percentage points from global trade growth this year. That's enough all by itself to pull the global figure into negative territory. A lot of this is concentrated in the United States — U.S. exports are projected to fall by a staggering 12.6% this year, while imports could drop by 9.6%.

Things look better elsewhere. The WTO believes that Asia will still contribute positively to global trade growth, though much less than it previously expected. The WTO previously thought it would add 1.2% to global trade growth. Now, they're looking at just 0.6% growth. Once again, the trade war is a big culprit here. China's exports to the U.S. are expected to collapse by 77%. That's not a typo — one of the world’s biggest trade partnerships, one worth more than half a trillion dollars annually, might soon be up in flames. China, meanwhile, is expected to redirect more exports to other regions.

Europe is holding relatively steady, contributing about 0.5 percentage points to global growth — instead of the 0.6 points originally forecast. Thankfully for them, most of their trade happens within the EU — which means they're somewhat insulated from the worst of Trumpian trade policy.

Other regions — Africa, the Middle East, and South and Central America — might still contribute positively to trade growth. After all, a lot of their exports, like energy products, will always remain in demand.

But for some countries, there’s a surprising upside here — one that even caught the WTO by surprise. Some of the world's poorest nations might actually benefit from these tariff increases, at least in the short term. Least Developed Countries are now projected to see export growth of 4.8% this year, up from the 3.5% forecast from a couple of months ago.

Why? Well, the answer to that question is also why international trade is so hard to control in the first place.

Trade diversion

Trying to move international trade around is like squeezing a balloon in the hope that it becomes smaller. It doesn’t work as you’d like. Press on one side, and the air just moves elsewhere.

As Trump’s tariffs squeeze international trade, a lot of that trade will simply shift around. In fact, we're already seeing big shifts in who's buying from whom. For instance, as per the WTO, as Chinese exports to the United States contract, a lot of those goods will move to regions outside North America. The latter could rise by 4-9%, in fact.

This will create both winners and losers. As China is cut out of the US market, countries with similar export profiles — like Cambodia, Bangladesh, or Lesotho — might see sudden windfalls as U.S. importers look for alternative suppliers. This is why so many Least Developed Countries might see a sharp rise in their export growth.

But all those Chinese goods will go somewhere too. There are growing concerns that those goods will flood markets all over the world, killing off local producers in those markets. Those countries may then attempt their own protective measures, potentially spreading trade restrictions even further.

What about services?

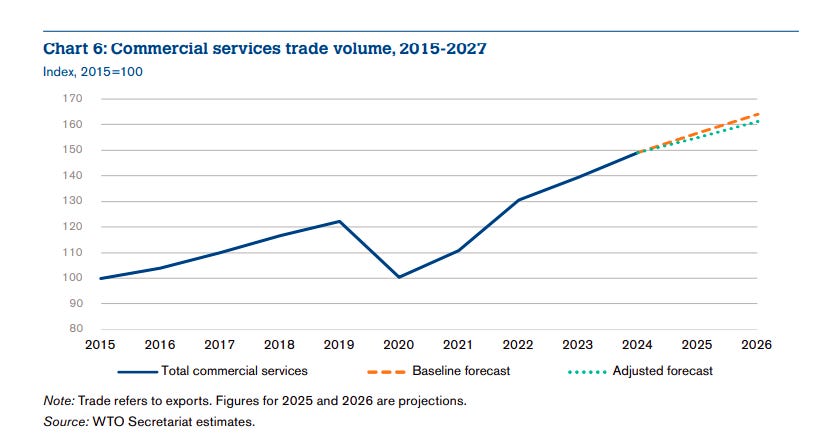

But all those tariffs are all just on goods. What happens to services — things like travel, IT, or financial services?

The WTO finds that even though services aren't directly subject to tariffs, they're not immune to the fallout. It expects global services trade to grow by 4% this year, down from the 5.1% they projected in their baseline scenario.

Why the slowdown? There are several reasons:

First, some services, like transport or logistics, are directly linked to goods trade. Ship fewer goods around the world, and you’ll see less demand for freight shipping, port services, and logistics. The WTO is now forecasting transport services growth of just 0.5% this year, down from 2.9%.

Second, all this trade uncertainty could make consumers cautious with their discretionary spending in general. They might travel a lot less, for one. International travel, in particular, is highly sensitive to economic uncertainty. The WTO has reduced its growth forecast for travel services to 2.6%, down from 4.2%.

Third, there are many intermediate services that support goods trade — like engineering, R&D, or professional services. They’ll face reduced demand as tensions rise.

Interestingly, the WTO believes that digital services — things like streaming, online education, and software — will hold up relatively well, with projected growth of 5.6%. Digital services, it seems, are more resilient than physical ones.

How do we deal with all the uncertainty?

A huge part of the WTO’s report is simply around how nobody knows how things will pan out. In economist-speak, this is called ‘trade policy uncertainty’, or TPU.

If you’re running a business that depends on global trade, your biggest headache isn’t a tariff alone. It’s that you have no idea what the rules might be next month. If the world’s trade outlook has shifted so completely in the last three months, what else might we see? Imagine you’re planning to build a factory for exports. Would you still go ahead, when business conditions might look entirely different by the time you inaugurate it? In times like this, businesses tread cautiously. They might delay investments, put expansion plans on hold, and avoid entering new markets.

According to the WTO, one-sixth of its projected trade contraction comes from this uncertainty alone — and not from the tariffs themselves. What’s more — 40% of the negative effect that global GDP will see over this episode will come from tariffs alone.

Right now, people are uncertain about trade with the United States. But as countries adjust and react to Trump’s tariffs, that could spark another wave of uncertainty. This could lead to contagion — as an American problem quickly becomes a global problem. As per the WTO, if the uncertainty goes beyond the U.S. and affects global trade, global merchandise exports could crash by a full 4.3 percentage points, pushing the entire world’s GDP down by 1%.

The end of the global economy

All of this leads to perhaps the most concerning long-term trend: the fragmentation of global trade.

The promise of international trade was that as more people conduct more business across borders, very different countries might come a lot closer to each other. We saw that play out for a couple of decades. But it’s beginning to unwind. The WTO is seeing clear evidence that, increasingly, trade flows are being shaped by geopolitical alignments rather than purely economic factors.

Since the war in Ukraine began, trade between blocs of countries with similar political views has grown 4% faster than trade between blocs. The same pattern is also visible in foreign direct investment, especially in strategic sectors like semiconductors, green energy, or critical minerals.

At this rate, we might see the global economy split into two major geoeconomic blocs. This, combined with more trade policy uncertainty and non-tariff barriers, could reduce global GDP by almost 7% by 2040. The poorest economies would suffer the most from this growing cleavage, with losses exceeding 9%.

That's the real danger here. We’re not just seeing a temporary dip in trade growth, but a fundamental reorganization of the global economic architecture. The unprecedented prosperity for the past several decades might disappear with it.

Where does this leave us?

The once-stable rules-based trading system is facing its greatest test in generations. What started as bilateral tensions between the world's two largest economies threatens to transform into a broader reconfiguration of global trade.

The immediate outlook isn't great. In the short term, both merchandise and services trade might take a hit. Even keeping the tariffs aside, the sheer uncertainty of this moment will weigh on investment and trade decisions. One hopes that, over the longer term, cooler heads prevail, and we see a gradual de-escalation of trade tensions.

Otherwise, we might continue down the path of fragmentation, with the global economy falling apart, giving way to small economic blocs.

Jerome Powell sees storm clouds gathering

It’s not just the WTO that’s anxious about the current moment in our economic history.

Jerome Powell, the Federal Reserve Chairman, made some revealing remarks at the Economic Club of Chicago yesterday. He painted a candid picture of an economy at a crossroads, facing new challenges from trade policy, immigration changes, and fiscal uncertainty.

Powell, of course, is one of the most important economic officials in America, and has held that post through one of the most challenging times in its recent history. His words carry a lot of weight. So, while we recommend you watch the entire discussion, we’re going to do a quick recap of everything he said.

The state of the American economy

At this moment, the American economy looks alright. Powell described the U.S. economy as being in a "solid position". Last year, the economy grew at a respectable 2.4%.

America’s unemployment rate is hovering only slightly above 4% – close to what economists consider full employment. Job growth has slowed down from last year. But right now, the slower labor force growth is being counter-balanced by fewer layoffs, and so, the unemployment rate has remained fairly stable. There are still more job openings than job seekers. And wage growth, while slow, is still outpacing inflation.

Inflation, while above the Fed's 2% target, has been coming down. Things have "significantly eased" from the pandemic highs of mid-2022, without the painful rise in unemployment that often accompanies efforts to tame inflation. March data shows total PCE prices rising 2.3% over the last year, while core inflation increased by 2.6%.

That sounds alright, doesn’t it? You might even feel hopeful, looking at the data.

But there are risks to the American economy, and they’re growing darker. Recent data, Powell noted, suggests that America’s economic growth has slowed in the first quarter of 2025. The biggest problem, perhaps, is what Powell called a "sharp decline in sentiment" among both households and businesses — largely due to uncertainty around trade policies. Outside forecasters are revising their projections downward, though they still think the American economy will grow this year.

In short, while America is still in decent shape, storm clouds are gathering.

The Trump effect

So what's really driving market anxiety? Powell directly addressed the elephant in the room: the new administration's policy changes. He pointed to four areas where the Trump administration is implementing "substantial policy changes", which are making people jittery: trade, immigration, fiscal policy, and regulation.

Powell didn't mince words on tariffs. He stated that "the level of tariff increases announced so far is significantly larger than anticipated," adding that "the same is likely to be true of the economic effects, which will include higher inflation and slower growth."

Sounds fairly tame? Here’s the thing: administrative officials don’t usually comment on policy at all. This is a rare moment of candor from a Fed chair about administration policy.

Powell also pointed to how inflation expectations have gone up a fair bit, all because of the tariffs. This may not just be a temporary rise, he warned, but potentially a period of persistent price pressures. Ultimately, this will depend on three things: how big the effects of the tariffs themselves are, how much of that shows up in prices, and how people’s longer-term expectations move with them.

Powell elaborated on this point later, speaking to Raghuram Rajan — comparing the situation to the pandemic-era semiconductor shortages, which caused prolonged, multi-year inflation in the auto sector. Those disruptions could "take some years" to resolve. And that means inflation carries on for years, long after the shock of the tariffs subsides.

The Fed's dual-mandate dilemma

That brings us to a critical dilemma facing the Fed. See, the Federal Reserve has two big goals — maximum employment and price stability. And it may soon find itself in a "challenging scenario," where those two goals are straining against each other.

Here's the problem: tariffs might push inflation higher, while simultaneously slowing economic growth and raising unemployment. At that point, the Fed faces a tough choice. If it hikes rates to control inflation, that could make the economy even tighter, and further harm employment. On the other hand, if it cuts rates to support jobs, that might fuel even more inflation.

This is a tough spot to be in. Powell noted that most of the time, weak economies have low inflation, while strong economies have higher inflation. This allows a central bank to push in the opposite direction, rebalancing the economy. The current situation, on the other hand, could push both unemployment and inflation higher simultaneously.

As Powell put it, "Our tool only does one of those two things at the same time," making this a "difficult place for central banks to be in."

The Fed's reaction function

So what does this mean for US interest rates? Powell carefully avoided making any commitments, but his remarks offer some important clues.

For now, Powell stated that the Fed is "well positioned to wait for greater clarity before considering any adjustments to our policy stance." In other words, the fact that the American economy is relatively stable means that, right now, he has some breathing room — and he’s going to use it to wait.

Trump isn’t a fan.

To Powell, the Fed's primary obligation is to keep longer-term inflation expectations well-anchored — that is, to ensure that people don’t start believing that prices will keep rising rapidly for the foreseeable future — and to prevent a one-time price increase from becoming "an ongoing inflation problem."

Reading between the lines, it seems the Fed is unlikely to cut rates anytime soon despite slowing growth, as the inflation risks from tariffs loom large. At the same time, Powell didn't signal any imminent rate hikes either. He’s going to dig in and adopt a wait-and-watch approach as the administration's policies unfold.

This comes in stark contrast to market expectations from just a few months ago, when many were anticipating multiple rate cuts in 2025. This is a distinct change in outlook, and Powell acknowledged this shift, noting that we've moved from what looked like a potential "soft landing" scenario to one where JP Morgan is now estimating a 60% chance of recession this year.

U.S. debt and deficits

Powell didn't shy away from addressing America's debt problem. He stated plainly that "U.S. federal debt is on an unsustainable path," although he clarified that it's "not at an unsustainable level" just yet.

Powell offered a candid assessment of where the fiscal problems lie. The largest and fastest-growing portions of federal spending, he pointed, are Medicare, Medicaid, Social Security, and now interest payments.

The political focus of programs like DOGE, on the other hand, is on discretionary spending. To Powell, that doesn’t make much sense — it represents a small and already declining percentage of federal spending. Cutting that spending doesn’t really count as a serious attempt to solve the problem.

He emphasized that actually addressing such fiscal challenges requires bipartisan cooperation — something that’s currently in short supply.

Structural uncertainty and long-term challenges

Rajan asked Powell about what he called "structural uncertainty" – not just policy uncertainty but questions about fundamental changes in America's economic philosophy. What followed was one of the most insightful exchanges of the session.

Powell acknowledged the profound level of uncertainty. He noted that businesses and households are reporting "incredibly high uncertainty" in surveys. Fed research shows that such uncertainty leads businesses and households to "step back from decisions," he pointed.

The potential long-term implications of this uncertainty are striking. People would pull back from investing in such an environment. They would demand higher expected rates of return to give their money away. Fundamentally, the United States would become an economy with more structural risk, making the country less attractive to investors.

This gets to the heart of concerns about America's economic trajectory and global competitiveness. While Powell was careful to say "we don't know that at this point," his willingness to even address this possibility reflects the gravity of the current situation. If long-term expectations change, that would change the calculus of every business in America.

He also offered insights on immigration policy — noting that the sharp decline in immigration has coincided with falling demand for workers, which is why unemployment has remained stable at the moment. Both the demand and supply for workers has fallen together, making things look more stable than they are. The long-term implications of reduced immigration, though, could be significant.

Powell also had interesting takes on topics that are immediately relevant to investors. For instance, Rajan asked Powell directly about the so-called "Fed put" — the market belief that the Federal Reserve will intervene if stock markets plummet. Powell firmly rejected this notion. While markets are experiencing volatility, he said, they remain "orderly and functioning" given the circumstances.

The current drop in American markets, in other words, isn’t an episode of paranoia. It’s how markets are supposed to behave. And if there’s nothing fundamentally wrong with the markets, there’s nothing for the Fed to do.

Banking and financial system resilience

In such trying times, how is America’s financial system keeping? There are some fears, in particular, that too many real estate loans, or unsustainable private credit, could spark the next big financial crisis.

When Rajan asked about the resilience of financial institutions, however, Powell expressed confidence in the banking system, describing it as "well capitalized with liquidity and quite resilient."

He acknowledged that some medium and small-sized banks have "elevated concentrations of commercial real estate," but noted that regulators have been working on this issue for a while. The largest banks generally don't have high concentrations in this sector, making it a manageable challenge.

On the rapidly growing private credit sector, Powell made an important distinction: much of it has been funded with "a private equity-like structure" where investors are purposely committed for long periods. And that means they’re immune to bank runs. However, he cautioned that this sector "has not really been through a significant credit event". Basically, the whole system is still untested. We don’t know how it’ll behave if a crisis does hit.

Final thoughts

On the surface, Jerome Powell seemed measured as ever, when he delivered his remarks in Chicago. But look closely and they’re a revealing assessment about the economic challenges ahead. He has signalled genuine concern about the impact of recent policy changes. The message is clear: Prepare for heightened volatility and uncertainty in the months ahead. Right now, markets are left to navigate what Powell described as "historically unique developments with great uncertainty."

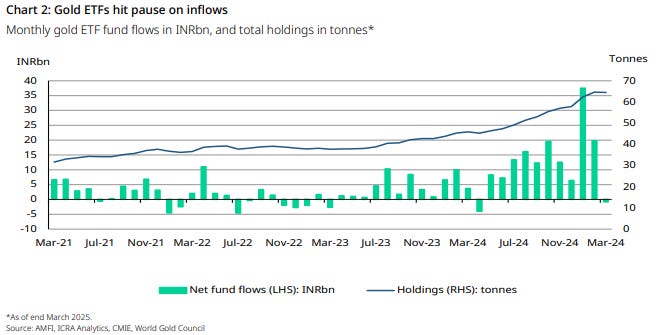

Indians and the global gold rush

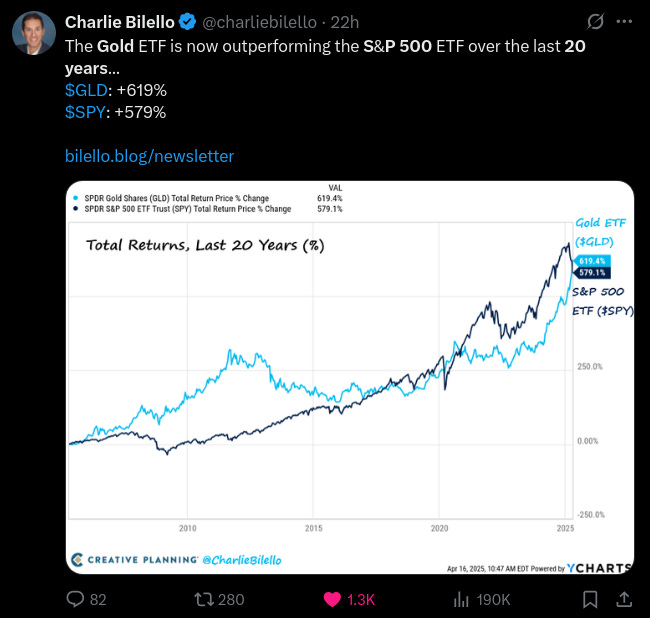

With all this uncertainty around, there’s an interesting side-plot: the gold markets are going wild. As people lose trust in the Dollar, Gold has become the safe haven that investors everywhere are turning to. International gold prices recently smashed through the $3,350 per ounce barrier (that’s Rs. 9,000 per gram) — an all-time high. In fact, with the recent rally, gold has now delivered better returns than the S&P 500 over the last twenty years — and that’s after staying flat for almost a decade in between.

In India too, domestic gold prices have mirrored the global trend, rising 23% this year to reach ₹93,217 per 10 grams. But this isn’t just an asset class for us. India is one of the world’s biggest consumers of gold. So, as the world gloms on to gold, what are Indians doing?

Here are a few quick pointers, from a recent World Gold Council report:

The sky-high prices of gold means that gold jewellery has suddenly become a lot less affordable. People are spending a lot less on jewellery now — purchasing it strictly when necessary, like for weddings. Discretionary purchases have fallen. In response to the soaring prices, Indians are also exchanging jewellery instead of buying it outright. In fact, 40-45% of Indians’ gold purchases, right now, involve exchanges of some sort.

Investors, interestingly, aren’t quite as hot on gold. In a sharp divergence from the rest of the world, Indians are actually selling off their gold ETFs. Indian gold ETFs small net outflows in March. It looks like Indians are booking their profits as the rest of the world cowers under Trumpian uncertainty.

The RBI has a similar story. It was, for a long time, one of the world’s biggest buyers of gold. Over the last year, gold’s share in our forex reserves had jumped up by 4%. As prices have risen, though, the RBI has moderated its gold buying pace. After pausing purchases completely in February, it added just 0.6 tonnes in March — compared to its previous average of 6.6 tonnes per month.

Tidbits

Smartphones Top India’s Export Chart with $18.31 Billion in Shipments

Source: Business Standard

Smartphones have become India’s top export commodity for the first time in any financial year, clocking $18.31 billion in shipments during April 2024 to January 2025 (10MFY25), according to the Department of Commerce. This marks a 54.7% rise from $11.83 billion in the same period last year, overtaking exports of automotive diesel fuel which stood at $16.04 billion. A key contributor was Apple, whose iPhone shipments from India to the US surged by 208% year-on-year in January 2025 alone, reaching $1.63 billion. Cumulatively, smartphone exports to the US touched $6.6 billion in 10MFY25, up 64% from the previous year. The sector’s rise comes after its 23rd rank in FY19 and 4th in FY24. Preliminary estimates suggest FY25 smartphone exports could reach ₹2 lakh crore, with iPhones accounting for nearly ₹1.5 lakh cr. of that. The shift is linked to Apple’s production move to India post-2021 and participation in the PLI scheme, which has also generated 1.3 million jobs, according to industry sources.

NTPC Steps In to Buy 15 GW of Unsold Renewable Power

Source: Business Standard

NTPC Ltd has announced its decision to purchase 15 GW of renewable energy that was left unsold from tenders it issued in the last two years. Acting as a Renewable Energy Implementation Agency (REIA), NTPC had floated tenders for 25 GW, of which 60% remains without buyers due to states refusing to sign Power Purchase Agreements (PPAs). This issue extends across the sector, with a total of 40 GW of RE capacity from agencies like SECI, NHPC, and SJVN also lacking Power Sale Agreements (PSAs). Both NTPC and SECI each account for 12 GW of this pending capacity, while NHPC and SJVN account for 8 GW each. NTPC plans to procure the unsold power at ₹2.8 per unit, foregoing the usual trading margin of ₹0.07 per unit. The utility is expected to sell the power through merchant markets, to commercial and industrial users, or as part of dispatchable energy solutions backed by storage.

Wheat and Rice Stocks Surge Above Targets, Easing Supply Concerns

Source: Reuters

India’s wheat stocks in government warehouses rose 57% year-on-year to 11.8 million metric tons as of April 1, 2025, reaching a three-year high and comfortably surpassing the government's buffer target of 7.46 million tons. The rise comes at the start of the new crop year and provides relief amid past concerns over domestic supply and price spikes. The Food Corporation of India (FCI), which missed its wheat procurement target last year by collecting only 26.6 million tons against a target of 30–32 million tons, now aims to procure 31 million tons in 2025. Meanwhile, rice reserves, including unmilled paddy, have hit a record 63.09 million tons, well above the buffer norm of 13.6 million tons. This significant surplus in both wheat and rice stocks offers the government more flexibility to manage supply and prices in the coming months.

- This edition of the newsletter was written by Bhuvan

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Informative.