Why the Paint Industry is under stress

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

The paints sector: Vibrant splashes amongst fading hues

Why Indians are hesitating to consume

The paints sector: Vibrant splashes amongst fading hues

When do most of us decide to paint our homes?

In happy times, right? Festivals? To welcome the monsoon, perhaps? Basically, whenever we feel optimistic or want a fresh start. If life isn’t going as well as you hoped, and you’re trying to prioritise expenses, painting your house will probably be the first expense you cut out. In that way, paint demand can be a quirky barometer of consumer confidence.

In the fourth quarter of FY2025, India’s paint companies found that many consumers were putting off that splash of color. This was a profoundly interesting quarter: demand patterns shifted, a new heavyweight made its presence felt, profit margins didn’t behave as expected, and companies doubled down on new trends.

Let’s break it down in plain English to see what’s going on beneath that drying coat of paint.

Demand is dwindling

In Q4 FY25, paint demand was a tale of two worlds – urban and rural. Urban demand was weak, continuing the slowdown we had seen in previous quarters. Big-city consumers were hesitant to spend on redoing their walls, perhaps postponing those non-essential paint jobs.

Asian Paints actually called the recent demand environment “the worst in two decades”.

Rural and small-town India provided a silver lining. Paintmakers noticed a volume pickup in tier-2, tier-3 towns and the countryside. Rural consumers, for a long time, had struggled with a cash crunch, and had cut back on discretionary spends. This quarter, however, marked a slow return. A good harvest or optimism about the upcoming monsoon might have helped folks in villages to consider painting their homes again.

Even so, rural demand wasn’t enough to compensate for the urban lull. And so, overall demand for the industry to remain weak.

This story also played out in how consumers saw premium and budget paints.

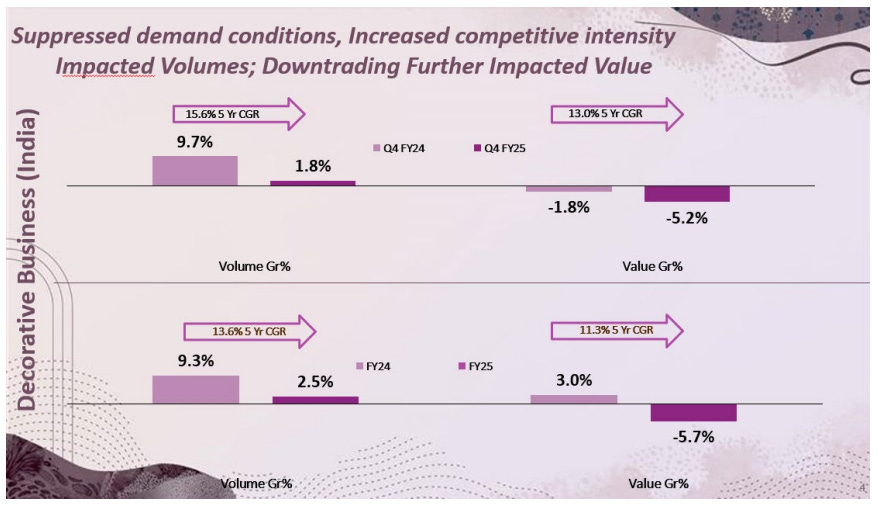

Paint companies have been pushing premium products for a while — like washable emulsions with silky finish, or weatherproof exteriors that last longer. For some players, this quarter, that bet worked out. For instance, Berger Paints reported steady momentum in its premium emulsion category and focused on high-margin luxury paints and waterproofing solutions to drive growth. Others, however, saw the opposite. Many consumers across India were feeling the pinch of high prices and downgraded to cheaper paints or local brands. Asian Paints observed that sluggish retail demand was partly because customers gravitated toward more affordable local brands amid rising competition. In simple terms, some people said, “Why buy the expensive brand when a cheaper paint will do the job?” This downtrading hurt the sales of premium paints for the market leader.

Despite these challenges, paint companies did manage to sell more liters of paint in many cases. Only, the money they earned from those sales didn’t rise as much. They sold more paint, but at lower prices. Why would that happen? Because companies offered price cuts and discounts to attract price-conscious buyers and to fend off new competition. Asian Paints is a prime example: it saw a modest 1.8% rise in volumes in its crucial decorative segment, but its sales revenue actually fell by about 4%, because it slashed prices by more than 5%.

That story isn’t universal. Berger Paints, for instance, managed a healthier balance – it clocked around ~7% volume growth and a 4.4% increase in value, indicating it didn’t have to sacrifice pricing much to drive sales.

But all in all, while organized decorative paint volumes were flat-to-slightly up, value growth was muted or even negative in this quarter.

The Competition Heats Up

Last quarter, we had tracked one of the biggest shake-ups the paints sector had ever seen: Grasim Industries (part of the Aditya Birla Group) launched its paints brand Birla Opus, and then steam-rolled through the sector.

Until then, the market had been dominated by legacy players who had long histories — Asian Paints, Berger, Kansai Nerolac, Akzo Nobel, etc. But Birla has deep pockets, and was up for the challenge. Grasim announced its foray in early 2024. In the space of just a year, in Q4 FY25, Birla Opus has already ramped up massively. They’ve set up five new plants across India, making them the second-largest decorative paint player by capacity. They built all this capacity at lightning speed — a bold move in an industry where individual factories are set up over many years.

Capacity is one thing. What about selling the paint?

Birla Opus hit the market running. In the March quarter, Grasim claimed that Birla Opus had already grabbed a “high single-digit” percentage of the decorative paints market share in revenue terms.

That’s huge for a newcomer. How did they achieve this? That is a long answer, that we answered in this video.

Asian Paints, the industry leader, was forced to react. It offered some price cuts in late 2024, when input costs fell, partly to stay competitive when Grasim/Opus arrived on the scene. Those price cuts, as we saw, dented its revenues in Q4. But there’s a limit to how far it’ll go. Asian Paints’ management has made it clear that they won’t engage in a prolonged price war, and will instead focus on improving its value proposition.

We highlighted this in our new newsletter called The Chatter. Check it out if you like interesting business tidbits you won’t pick up from the news.

Of course, Birla Opus isn’t just eating into Asian Paints’ market share. Other established players like Berger and Kansai Nerolac have also been responding to this threat.

Berger Paints, which is the second-largest traditional player, actually had a decent Q4. It even gained market share in decorative paints.

How? Berger’s strategy, amid the heightened competition, has been to focus on premium products and efficiency — it’s essentially trying to command a premium rather than entering a discount race. Their MD suggested that Birla Opus is following a strategy of “purchasing market share” through high spending, and questioned its sustainability.

Meanwhile, there’s another competitor that’s eyeing the paints business. JSW Paints — part of another conglomerate with big ambitions — has been expanding its footprint too. Although it’s still a small player, it’s trying to make much deeper forays. There’s even talk that JSW Paints might acquire Akzo Nobel India, which makes Dulux paints, to instantly enlarge its foothold on the industry.

All this means the big paint companies can no longer coast comfortably. Big competitors are marching into the scene, and they have to fight for every gallon of market share.

The Margin Story

With such high competition and all the demand flux, how did the profits and margins fare in Q4 FY25?

On the positive side, raw material costs have eased compared to the inflationary period a year or two ago. Key inputs — like crude oil derivatives, which are used as solvents, etc., and titanium dioxide, the pigment that gives paint its opacity, saw prices soften in recent months.

However, that didn’t automatically translate into booming profits for everyone. Why? Because with so much competition all around, companies had to give up some of those gains in other expenses, while they passed the rest on to consumers.

Take Asian Paints as a case in point. While its material costs were lower, it also spent more on advertising, dealer commissions, and promotions to hold its market share. All these moves ate into the bottom line. As a result, Asian Paints’ consolidated net profit fell sharply by 45% year-on-year, to about ₹692 crore in Q4. This number was a big miss relative to expectations

Do note, though, that this decrease includes a one-time loss from the sale of its Indonesian unit, which also dragged profits down.

A core issue was pricing: as mentioned earlier, Asian Paints undertook price cuts that pressured its sales value. It couldn’t hold on to the profits from all the raw material deflation. The competition essentially forced a trade-off: it had to sacrifice some margin to protect volumes. Although the management doesn’t seem keen to cut prices further, at least this quarter, the damage was done. Revenue fell and margins shrank.

Interestingly, the falling Rupee played a role as well. While the cost of inputs was benign, the Rupee exchange rate was not. This made imported chemicals pricier, eating into the benefit of global price drops.

On the flip side, not everyone had a bleak profit story.

Berger Paints actually saw its net profit jump 18% YoY in Q4, thanks to strong volumes and cost controls. It managed to keep growth on track without eroding its margins — a notable feat in this environment.

In summary, raw material relief was counter-balanced by intense competition, forex volatility and higher marketing spends. As the dust settled on Q4, companies found that simply having cheaper raw materials isn’t enough; you have to hold your price or differentiate your product to actually see the profit boost.

Conclusion

Q4 FY25, in short, was an interesting one for the Indian paints sector.

Demand was mixed. It was lackluster in cities, but flirted with a rebound in the villages. Competition turned fierce with a new giant at the gates. Margins were a tug-of-war between cheaper materials and pricier marketing battles. And through it all, companies kept an eye on the future with premium products, services, and innovations to entice consumers.

As we head into FY26, the industry is cautiously optimistic. Management commentary across the board suggests hope for a demand recovery, aided by factors like government infrastructure spending and a forecast of a good monsoon.

Whether that comes or not, the takeaway from Q4 FY25 is clear: even a seemingly staid, boring industry like paints, sometimes, can be in for a wild ride.

Why Indians are hesitating to consume

India’s Private Final Consumption Expenditure (PFCE) makes up roughly ~60% of our GDP. But unfortunately, this figure isn’t growing nearly as fast as we’d like.

Let’s de-jargonise that, so that you really get what we’re talking about.

Of every ten rupees that flows through our economy, six are spent by ordinary people like you and me — on everything from groceries, to getting a haircut, to buying a new mobile phone. Economists call this “consumption,” and it makes up the backbone of our economy. If consumption fails, the “India growth story” starts falling apart as well.

There’s a chance that’s precisely what we’re seeing right now.

For a couple of years after the pandemic, Indians were quickly increasing how much they consumed. Between FY 2021 and 2022, our consumption grew by 11.7%. The next year, we added another 6.8% to our consumption figures. This was a tremendous tailwind for our economy — and it showed up in our excellent GDP growth numbers. In retrospect, though, that was an aberration — a little data kink that merely spoke to how our economy behaved at the end of a once-in-a-century wave of disease. That momentum, sadly, wasn’t meant to last.

FY 2024 knocked the wind out of our sails. India’s consumption growth fell to 5.6% — well below our long-term average. That, in itself, isn’t worrying. One swallow doesn’t make a summer. What’s worrying, though, is that our consumption had started faltering before the pandemic. What if our economy is hitting structural limits, and was already struggling before the pandemic? What if the pandemic sent all our statistics askew, hiding deep problems in plain sight?

Now, we aren’t economists. We could be wrong about all of this. But we’ve been trying to wrap our heads around some recent research on this — including a new note by Motilal Oswal and a paper by CSEP.

Here’s everything we could understand.

A return to the pre-pandemic trend?

In the years before the pandemic, India’s economy was in a worrying spot.

For a three year period between 2017 and 2020, our economy was in a phase of sharp deceleration. Consumption growth — which averaged a robust 7.9% between FY 2015 and 2017, had fallen to 5.7%. Our economy came under severe stress, ending in a terrible crisis in our financial sector. By FY 2020, our GDP growth had slowed to its lowest level in over a decade — 3.9%.

And then came COVID-19.

For one year, our economy went into free fall. People were forced to sit home, and it wasn’t always clear that the world would return to normal. People clamped down. Many deferred making any major purchases.

But slowly, we began to realise that the disease was temporary, and that we had the tools to get over this challenge. Normalcy was just around the corner. That terrible anxiety of the first COVID year waned, and by the time FY 2022 was reaching its close, our economy was roaring back into shape. That year, our GDP growth rate touched an all-time high of 9.7% — if only because the base year was so terrible — and it remained elevated for a couple of years.

But this obscured one thing. Our consumption never returned to the pre-pandemic trend:

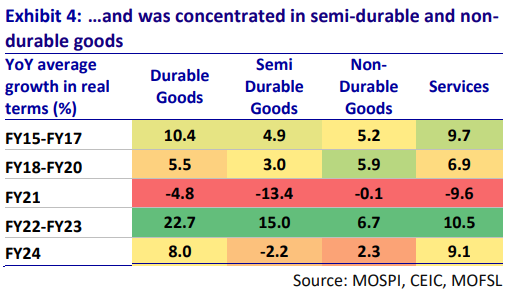

There are two categories where this swing has been particularly notable: durable and semi-durable goods. These are, simply put, goods that last a while. Durable goods — automobiles, furniture, electronics, and other such stuff — typically stays around for at least three years. Semi-durable goods — like clothes or footwear — have a slightly shorter life.

When the pandemic hit, people held off on these longer-term expenses. When it ended, they returned with a vengeance. For two years, people seemed to go on a revenge buying spree, with sharp upticks in both categories. People’s consumption of durable goods went up 22.7% over FY 2022 and 2023. They lapped up semi-durable goods too, with consumption growing at 15% a year.

And then, both fell off a cliff. In FY 2024, durable goods consumption grew by a much slower 8%. Consumption of semi-durable goods actually fell by 2.2%. The momentum had broken.

To be fair, things were slightly better last year. We don’t have data for all of FY 2025, but at least for the first half of the year, consumption went up by 6.7%. But once you dig into that figure, our problems are far from over. This isn’t just a quirk of numbers either; India’s FMCG giants, too, have been complaining about how our sluggish consumption making it harder to sell. As the engine of our economy, frankly, consumption is sputtering.

What gives?

Stalling wage growth

The first and most important reason for this decline is painfully simple: people just aren’t earning enough.

For all the talk of India’s booming economy, data suggests that most people’s paycheques haven’t actually grown fast enough to keep up. Unfortunately, India doesn’t release any country-wide wage growth statistics, so a lot of this is guesswork. We could be entirely wrong here. But incidental data, at least, gives one reason for concern.

In recent years, for instance, our per-capita GDP growth has averaged at around 3.55% annually, compared to the ~6% we regularly saw over most of the last decade. Before the pandemic hit, the growth in Indians’ disposable incomes were falling steadily — from 13.5% in FY 2013 to 7.7% in FY 2020. And that seems to have returned. All through FY 2024, as per the government’s Periodic Labour Force Survey, wage growth in urban India kept declining — especially for ‘non-salaried workers,’ who work informal jobs in sectors like construction.

Why is this relevant? Well, there’s something called the “permanent income hypothesis” that Milton Friedman proposed back in 1957. Basically, how much people consume today depends on what they think they’ll earn tomorrow. People match their spending to what they expect to earn over the long term. Temporary setbacks don’t rattle people. Permanent setbacks, however, push people to slash what they’re willing to spend.

Falling consumption, then, is not just a sign that people have less money with them today. It’s a sign of hopelessness over the long term.

That’s really the dangerous thing. Indians’ optimism in our economy has been fairly low for a long while. The RBI regularly carries out a survey to measure consumer confidence, and from what it has found, that has been fairly subdued for many years. Midway through May 2019, consumer confidence in our economy began dropping, and then fell off a cliff during the COVID-19 pandemic. While it has recovered considerably since, it hasn’t broken above 100 — which is the line that separates optimism from pessimism. Indians, in other words, haven’t truly been happy with how things are for half a decade.

Inflation is hollowing everything out

Our problem isn’t one of low wage growth alone. It’s that our recent run-in with high inflation has eaten away at anything extra that people have earned.

This was a particularly bad problem to have if you’re poor. See, poor households spend a large chunk of their paycheck arranging for food. And that’s where much of the inflation of recent years has been concentrated. In FY22, food made up 27% of overall inflation. By FY24, it was over 55%. In the first half of FY25, it was a staggering 67%.

For India’s poorest households, this turned inflation into a nightmare. To them, inflation felt far worse than the headline figure of 5 or 6% that official data pointed to. In FY24, for example, the bottom 20% of rural and urban India faced inflation rates that were 0.5 to 1.2 percentage points higher than the richest 20%.

Here’s one example. We separately calculate the inflation rate for rural labourers, based on the sorts of things they might buy. Between 2022 and 2024, the consumer price index for rural labourers (CPI-RL) rose at an average rate of 7%. That’s more than double the 3.4% average from FY16 to FY19. But here’s the real punch in the gut: nominal rural wages over the same period barely kept pace, growing at just 6.5%.

What this means is simple: inflation ate away at almost every additional rupee earned. Real rural wages — wages adjusted for inflation — barely budged at all. Across FY22 to FY24, they averaged a meagre 0.1% annual growth. To put that in perspective, between FY14 and FY19, real rural wages grew at a healthier 2.3% per year.

That stagnation in rural wages is a major reason why consumption of everyday goods has stayed so weak. After all, if your wages aren’t rising, and inflation is eating away at whatever little gains you have, you’re forced to cut back.

Debt burdens are rising

But here’s a question: if Indians’ incomes haven’t been increasing too quickly, and any increase we’ve seen has become the victim of inflation, how did consumption go up so quickly after the pandemic?

Much of that spending, it seems, was on credit, driven by people borrowing more.

India’s household debt has been climbing steadily. Back in FY15, household debt was about 31% of our GDP. By FY23, it had jumped to nearly 40%. By the first half of FY25, it had crossed 43%. This growth in borrowing has been far sharper than the growth in people’s borrowing. All this extra debt, in itself, has slashed Indians’ disposable incomes.

What’s worse: the nature of this debt has changed. Earlier, most household debt was for buying homes. But now, a big chunk of it — over 32% — is from personal loans: money borrowed to fund consumption, for things like appliances, weddings, or even just day-to-day expenses. Back in FY 2016 and 2017, this used to be at a much lower 21.4%.

For a short while, this borrowing binge may have boosted consumption. When consumption spending went up by an annual 9.6% between FY 2022 and 2023, household debt shot up much faster — by as much as 17.5% in FY 2023. This was like a sugar rush for the economy. Over time, a crash was due. When people’s debt burdens mount, that spooks them out, and makes them much less likely to spend.

Things will be worse if they’re caught up in a debt trap. Household debt has grown to 43.5% of our GDP — a scarily high number. The Reserve Bank has warned that 40% of borrowers have more than one loan. Overdues are rising, especially for smaller loans below ₹50,000. The last time consumption collapsed, it was preceded by a debt crisis, which nearly took India’s non-banking financial sector with it. This debt burden could turn into a serious problem once again.

How do we get out of this situation?

In the short term, some of the forces that pushed consumption down in FY24 have started to ease.

For instance, we saw a good monsoon last year. With that, we had a good kharif crop, which has helped boost rural incomes. The ‘’gross value added” by our agricultural sector will likely be as high as 3.8% in FY 2025, well above last year’s 1.4%. The government has also increased its spending on rural employment schemes like NREGA and rural roads by 20% in this year’s budget. And that could make a serious change: according to CRISIL, in the last 14 years, private consumption and government spending have usually gone hand-in-hand.

With better monsoons, inflation has also stabilised to its lowest level in years. This has given RBi the confidence to bring down interest rates, which might bring some relief to borrowers.

All these tailwinds could give consumption a bit of a short-term lift.

But none of these fixes are permanent. Another bad monsoon could bring us here again. Sadly, many of our problems are structural. Ultimately, our only way out is to create new, long-term sources of wealth and employment, and thus give Indians more confidence in their future.

Until that happens, our consumption story will remain a little fragile, hostage to monsoons and government purses. After all, the question isn’t just whether people have money to spend today — it’s whether they believe they’ll have it tomorrow. It is that belief that India must work to create.

Tidbits

India Surpasses Japan to Become World’s Fourth-Largest Economy: NITI Aayog

Source: Business Standard

India has overtaken Japan to become the fourth-largest economy globally, according to NITI Aayog CEO BVR Subrahmanyam. The IMF’s April 2025 World Economic Outlook projects India’s GDP for FY26 at $4.187 trillion, marginally ahead of Japan’s $4.186 trillion for the calendar year 2025. For FY2026–27, India’s GDP is expected to rise to $4.601 trillion, while Japan’s is projected at $4.373 trillion. India’s GDP for FY25 has been revised upwards to ₹331 trillion from the earlier estimate of ₹324 trillion. However, GDP growth is expected to decelerate to 6.5% in FY25, down from 9.2% in the previous fiscal year. Subrahmanyam also stated that India is on track to surpass Germany in the next two and a half to three years to become the third-largest economy.

India’s Auto Duty Concession to UK Tied to Engine Size and Price, Phased Over 10–15 Years

Source: Economic Times

India’s import duty concessions for the automobile sector under the proposed Free Trade Agreement with the UK will be implemented gradually over a 10 to 15-year period. According to a senior official, the offer is structured with specific relaxations linked to engine capacity and vehicle prices. The concessions are not uniform but designed with segmented conditions to limit market disruption. The agreement includes safeguards aimed at protecting India’s domestic auto industry, which is considered a sensitive sector. These measures reflect a calibrated approach to market access while maintaining regulatory control. The auto duty relaxation is part of broader FTA negotiations intended to boost trade without compromising key domestic interests.

Ashok Leyland Reports 5.7% Revenue Growth in Q4; Faces Cost and Demand Pressures Ahead

Source: Business Standards

Ashok Leyland reported a 5.7% year-on-year rise in standalone revenue for Q4 FY25, reaching ₹11,857 crore, supported by 5% volume growth. EBIRDA growth was 12%, aided by softer raw material costs. EBITDA margin expanded by 90 basis points year-on-year to 15%, while net profit rose 30% due to stable depreciation costs. The company ended FY25 with a cash balance of ₹4,000 crore and no net debt, even after incurring capital expenditure of nearly ₹950 crore. However, April volumes, including exports, declined by 6% year-on-year. The imposition of a safeguard duty on steel for 200 days starting April is expected to impact input costs over the next two quarters. Analysts note that these developments could weigh on near-term performance despite strong fundamentals.

- This edition of the newsletter was written by Kashish and Pranav.

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Introducing “What the hell is happening?”

In an era where everything seems to be breaking simultaneously—geopolitics, economics, climate systems, social norms—this new tried to make sense of the present.

"What the hell is happening?" is deliberately messy, more permanent draft than polished product. Each edition examines the collision of mega-trends shaping our world: from the stupidity of trade wars and the weaponization of interdependence, to great power competition and planetary-scale challenges we're barely equipped to comprehend.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉