Why Indian conglomerates are chasing fast fashion

It’s because they can

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Why Indian conglomerates are chasing fast fashion

The IMF has a grim outlook for the world

Why Indian conglomerates are chasing fast fashion

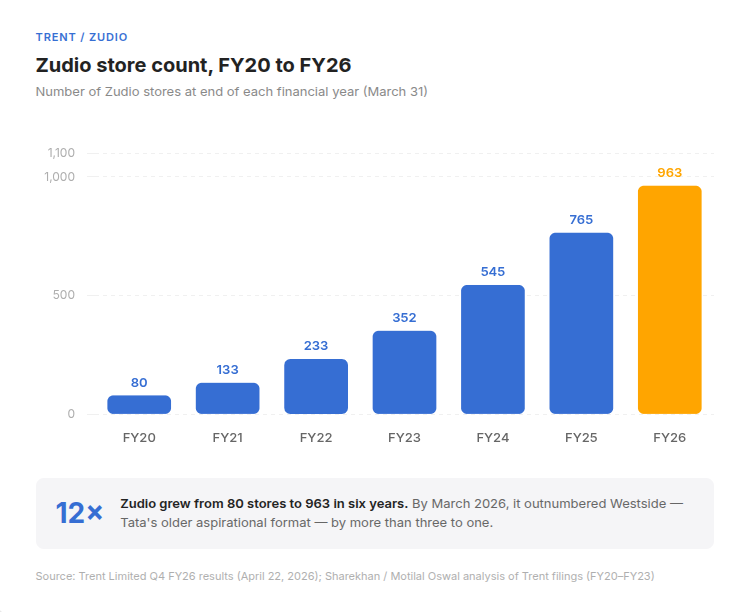

Trent, the Tata Group’s retail arm, published its full-year results last week. By March 31, 2026, it was running 963 Zudio stores across India. Zudio, if you haven’t been, sells T-shirts for ₹399, jeans for under ₹600 with 47 new cities entered in the last quarter alone and 80% of new stores in Tier II and Tier III cities.

Tata is not alone here. Reliance launched Yousta, where all products are priced below ₹999 and most below ₹499. ABFRL, the Aditya Birla fashion arm, launched OWND! in September 2025, starting at ₹399, targeting Gen Z, with 10,000 styles, and in April 2026 hired a new CEO for it, Marco Agnolin, who previously ran Bershka and Diesel.

So three of India’s largest conglomerates, companies whose combined reach spans oil refineries, steel mills, telecom networks and cement plants, are in an active competition over the cheapest part of the wardrobe.

The obvious answer is that young Indians want affordable clothes and the market is large. True, but that explains why the segment exists, not why the Tatas and the Ambanis are the ones winning it. There are plenty of younger, nimbler, more fashion-native companies that spotted the same demand.

But fewer than 10% of the 700-plus D2C fashion brands operating in India have grown beyond ₹50 crore in revenue. Most of them have not scaled. And the reason behind this might have nothing to do with fashion or taste.

Why cheap fashion is harder to run than expensive fashion

Fashion is structurally different from most consumer goods in one way that matters enormously at low price points.

A shampoo company has a product. The formulation changes once a decade. You forecast demand, manufacture, ship. If you over-produce, you discount. Nothing expires.

This whole equation gets exponentially hard for a fashion retailer . Each permutation and combination of size, colour, design, and trend is a new distinct item that can succeed or fail on its own terms.

A store like Zudio might carry thousands of distinct items at any point. Every single one carries its own demand risk. A style can miss. A colour can arrive out of season. The size ratio can be wrong, too many smalls, not enough mediums. And unlike shampoo, a fashion item has an expiry date that has nothing to do with chemistry. Last quarter’s trending cargo pant is this quarter’s markdown problem.

At ₹2,999 per piece, you can survive your own mistakes. Mark something down 30% and the store recovers something. The margin provides a buffer. At ₹499, that buffer does not exist. A slow-moving ₹499 item cannot be meaningfully discounted. It is effectively a write-off. So the only way value fashion works is if you are right, which style, which colour, which size, which city, how many units, most of the time, and you turn inventory fast enough to catch errors before they compound across a thousand stores.

Trent’s own FY26 results statement says their “disciplines around inventory provisioning“ was the business’s operational drivers. The company also announced a ₹2,500 crore rights issue, part of which is earmarked specifically for expanding and automating supply chain and warehousing.

The supply chain India built was built for someone else

India is one of the world’s largest garment producers. The clusters in Tiruppur, Surat, Ludhiana and Bengaluru supply H&M, Gap and Marks & Spencer. The industry is enormous, mature and efficient. It is also almost entirely calibrated for the wrong customer.

India’s garment manufacturing base was built around western fashion buyers: bulk orders, four-to-six month planning horizons, standardised international sizing, Free On Board export contracts. That supply chain runs on lead times of 75 to 90 days from order to finished goods, fabric procurement, sample approval, bulk production, finishing, quality checks, documentation. The system is efficient for a customer who plans seasons far in advance and orders in large volumes.

But domestic fast fashion— the kind Zudio, Yousta, and OWND want to operate— needs the exact opposite.

Reliance’s FY25 annual report says its apparel business runs a design-to-shelf cycle of 30 days. To go from a sketch to a Yousta store shelf in 30 days, you cannot wait for fabric to be ordered after a design is confirmed. For that Relaince needs raw materials pre-positioned at vendors before the production decision is made, and manufacturers who can run small batches and pivot to a new style within days.

A garment factory running on 90-day export cycles has its entire operation organised around that rhythm: fabric procurement schedules, workforce planning, production line sequencing, quality check processes. Restructuring for 30-day domestic cycles means changing all of that, different raw material buffers, different production sequencing, different everything. A factory makes that investment only when a retailer can guarantee enough consistent purchase orders to recover the cost of retooling.

That operating model, 30 days, small batches, Indian sizing, high style rotation, is not what Indian garment factories are used to doing. Which means that when Zudio or Yousta want to restock a trending item in week three, they are calling a factory that was built for a completely different customer, and asking it to work differently that fits their model. And the factory would only comply if they would get enough volumes and business from them.

Volume as the only moat that matters

Trent with 963 stores and ₹20,000 crore in annual revenue can make that promise. Reliance Retail, with 19,340 stores and 349 million registered customers, can make that promise. A brand doing ₹50 crore in annual revenue cannot.

This is the moat that the category conversation consistently misses. The competitive advantage in value fashion at scale is purchase order volume required to get a manufacturer to change how it works, and then sustain that relationship at the speed the business model needs.

The private label structure of these businesses ties this together. Zudio, Yousta and OWND! are all entirely private label, every item designed, sourced and sold by the retailer, with no external brand names. At sub-₹500 pricing, there is simply no margin to pay a third party for their name. So the retailer absorbs every function, designer, buyer, production manager, quality controller, that traditional fashion distributes across a supply chain.

That means the business is not just the retail store, but ownership of the complete supply chain. Which is why Reliance describes its fashion operations as “yarn-to-wardrobe”, vertically integrated from fabric sourcing through design, production and distribution.

When ABFRL needed someone to run OWND!, it did not hire from Indian retail or Indian fashion. It hired Marco Agnolin, the man who previously ran Bershka, Inditex’s youth fast fashion format with 854 stores across 68 markets, and before that Diesel. He is someone who has spent his career operating this machine at scale across dozens of countries.

The business that looks like fashion but works like industry

Tata, Reliance and Birla are not in value fashion because they have better taste than smaller competitors. They are in it because value fashion at national scale is an industrial supply chain problem, and industrial supply chain problems are precisely what these companies can solve with their scale and their deep pockets.

A Bain & Company study found that fewer than 10% of the 700-plus D2C fashion brands operating in India have scaled beyond ₹50 crore in revenue. Most fashion-native brands hit a wall, not because their product was wrong, but because they could not build the supply chain infrastructure that national scale requires.

Which is exactly why the people who built India’s steel plants, oil refineries, and telecom networks are the ones running it.

The IMF has a grim outlook for the world

Every April, the IMF releases its World Economic Outlook (WEO), which is basically an official report card on the global economy. The headline report is usually split up into 3 or 4 chapters, and the first chapter simply provides economic growth forecasts.

This year’s edition does the same for sure, but there is one major difference compared to past reports. You see, most of the report is about war, whose incidence has risen pretty sharply compared to 4 decades ago.

The WEO is not really a document known for dramatic language. But when the IMF bases most of its flagship publication on the impact of armed conflict, there couldn’t be a bigger sign of how tense the times are currently. Between an oil crisis of magnitudes not seen in at least 5 decades, and geopolitical tensions that underscore that crisis — and other things beyond that — the world has its hands full.

Two of the three chapters in this year’s WEO are entirely about the military turn in global politics. Chapter 2 studies what rearming costs an economy, and Chapter 3 studies what actual war costs. Together, they form something like an escalating argument — spending, fighting, recovering — with each stage more economically damaging and harder to reverse than the one before.

The findings in the first chapter will be obvious to anyone with even the smallest hint of the state of the world today, so we won’t spend time going into those. Let’s dive into what chapters 2 and 3 of the WEO say.

The price of rearming

Start with where most countries currently are: spending more on defence without yet fighting a war.

The numbers are striking. Over the past five years, roughly half of all countries worldwide have raised their military budgets. As of 2024, nearly 40% of countries were spending more than 2% of GDP on defence — up from 27% in 2018. In June 2025, NATO members committed to raising defence and security spending to 5% of GDP by 2035, more than double the previous target. Arms sales by the world’s largest 100 defence firms have, in real terms, doubled over two decades.

The intuitive assumption is that defence investments are as stimulative as any other. Governments spend money, factories hum, workers get hired, and there’s economic growth. This is partly true, but the picture is messier. That’s because, well, defence spending doesn’t work like other forms of government expenditure.

When a government builds a road or hires more teachers, the spending diffuses broadly through various stakeholders: like construction workers, local businesses, households, etc. But defence spending is too concentrated in a narrow set of industries to do that: think aerospace, specialised materials, and transport equipment.

So, a military buildup functions less like a general demand stimulus and more like a targeted shock to a specific set of sectors. Workers and capital have to shift toward defence industries from wherever they currently sit, and that reallocation is slow, expensive, and often disruptive to the sectors losing resources.

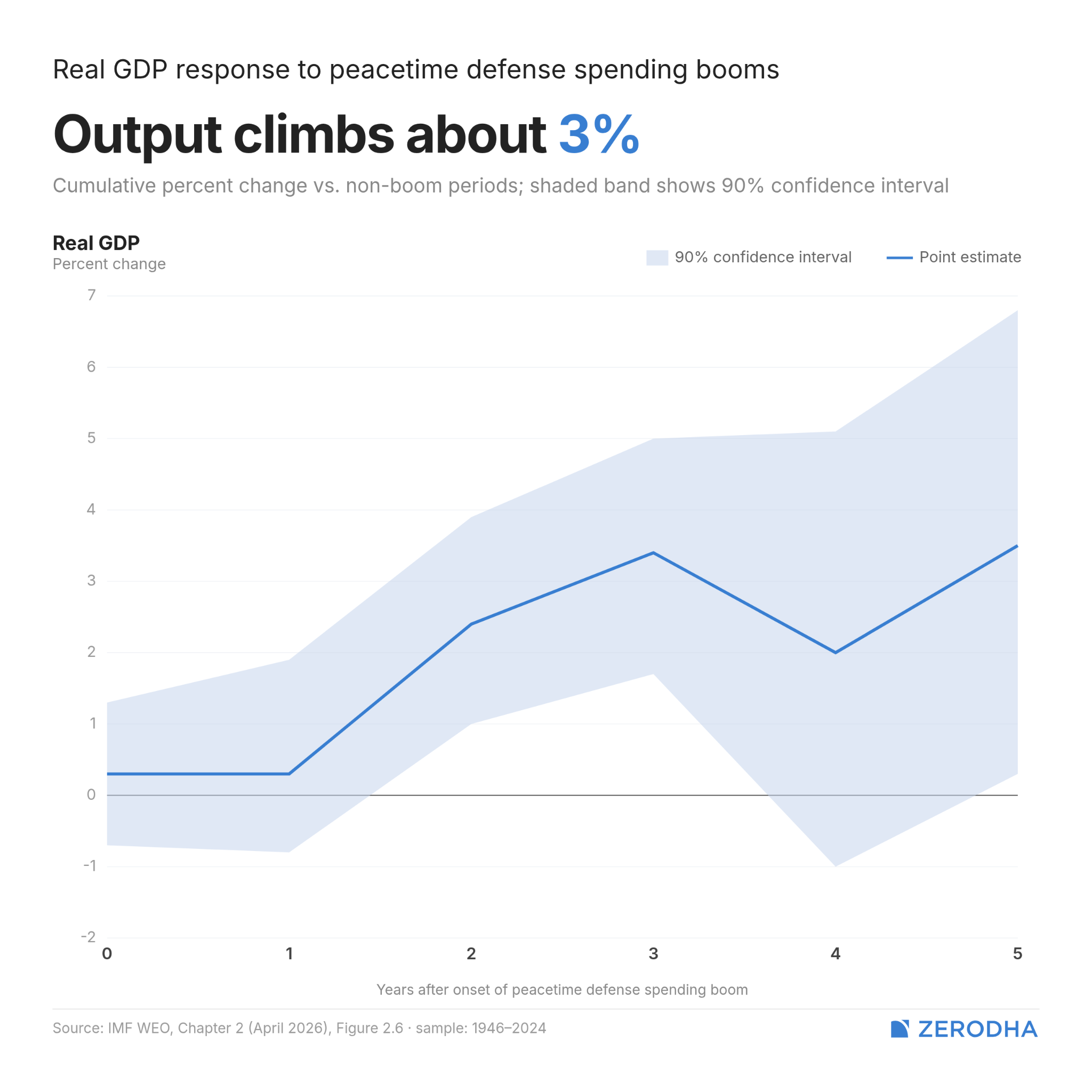

The short-term effect might still be positive, though. The IMF finds that in peacetime, defence booms raise GDP by ~3% more than it would otherwise have been, while inflation rises briefly and then fades. Over longer horizons, if the spending is directed toward R&D, genuine productivity gains can follow; the internet, GPS, and much of modern semiconductor technology trace their origins to military R&D.

But there are two substantial forces working against this.

Import leakage

The first is the import leakage problem. Most countries don’t make most of what they buy. Nearly 80% of the military equipment purchased by European Union member countries is imported. The United States alone accounts for nearly half of all revenue among the world’s top 100 arms firms.

So when, say, Poland buys fighter jets from the US or artillery systems from South Korea — which it has been doing at an extraordinary pace — the demand stimulus flows primarily to foreign producers. Poland bears the full fiscal cost of the purchase; the economic benefit lands elsewhere.

Fiscal burden

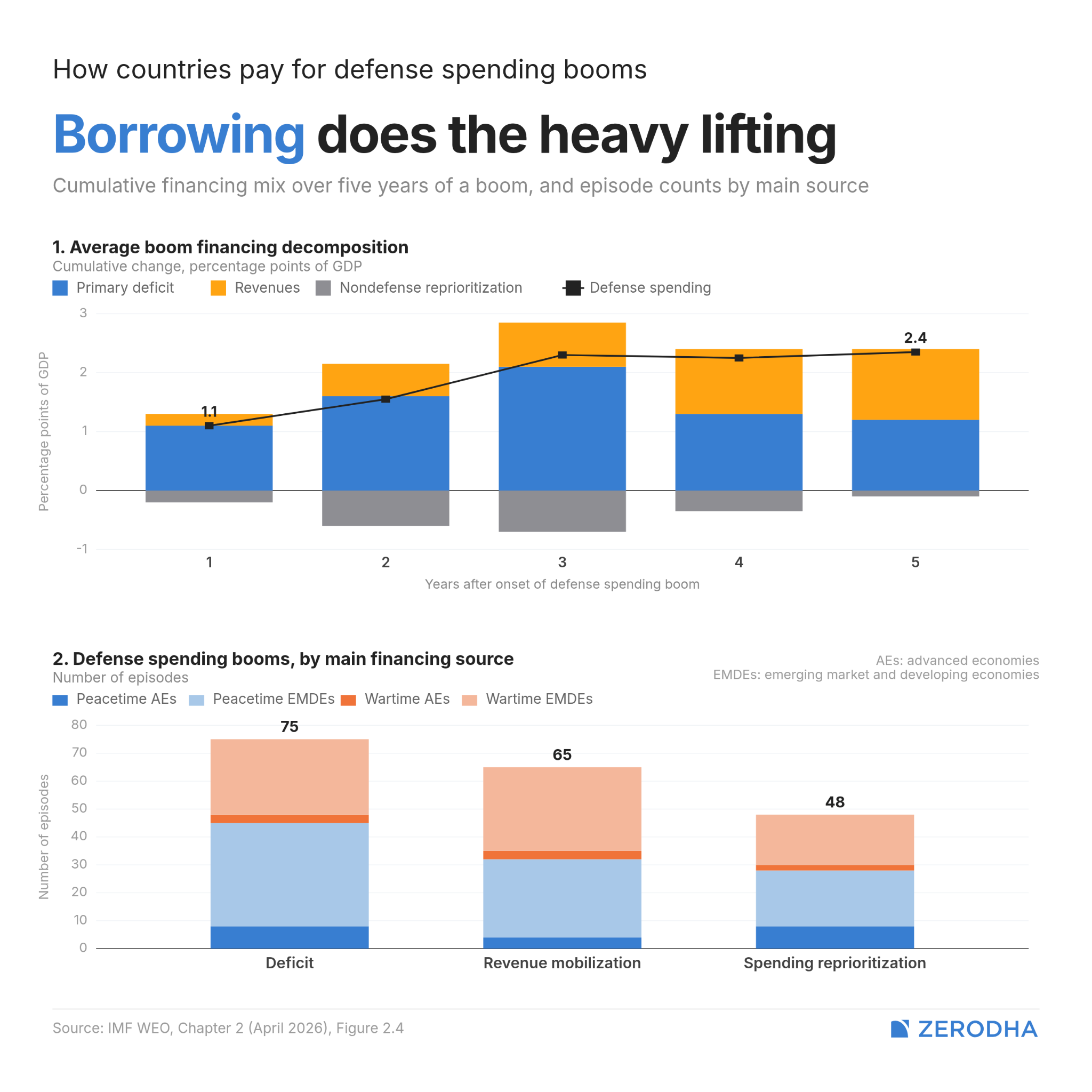

The second is what happens to the government’s finances. A typical boom widens the fiscal deficit by about 2.6% of GDP and raises public debt by roughly 7% within three years. About two-thirds of defence buildups are financed by borrowing. When higher public debt tightens financial conditions — as it often does — firms outside the defence sector find credit more expensive, and private investment gets crowded out.

The IMF’s firm-level data shows this directly: during booms associated with rising public debt, firms become measurably more financially constrained and pull back on investment. The defence sector gains, but much of the rest of the economy loses.

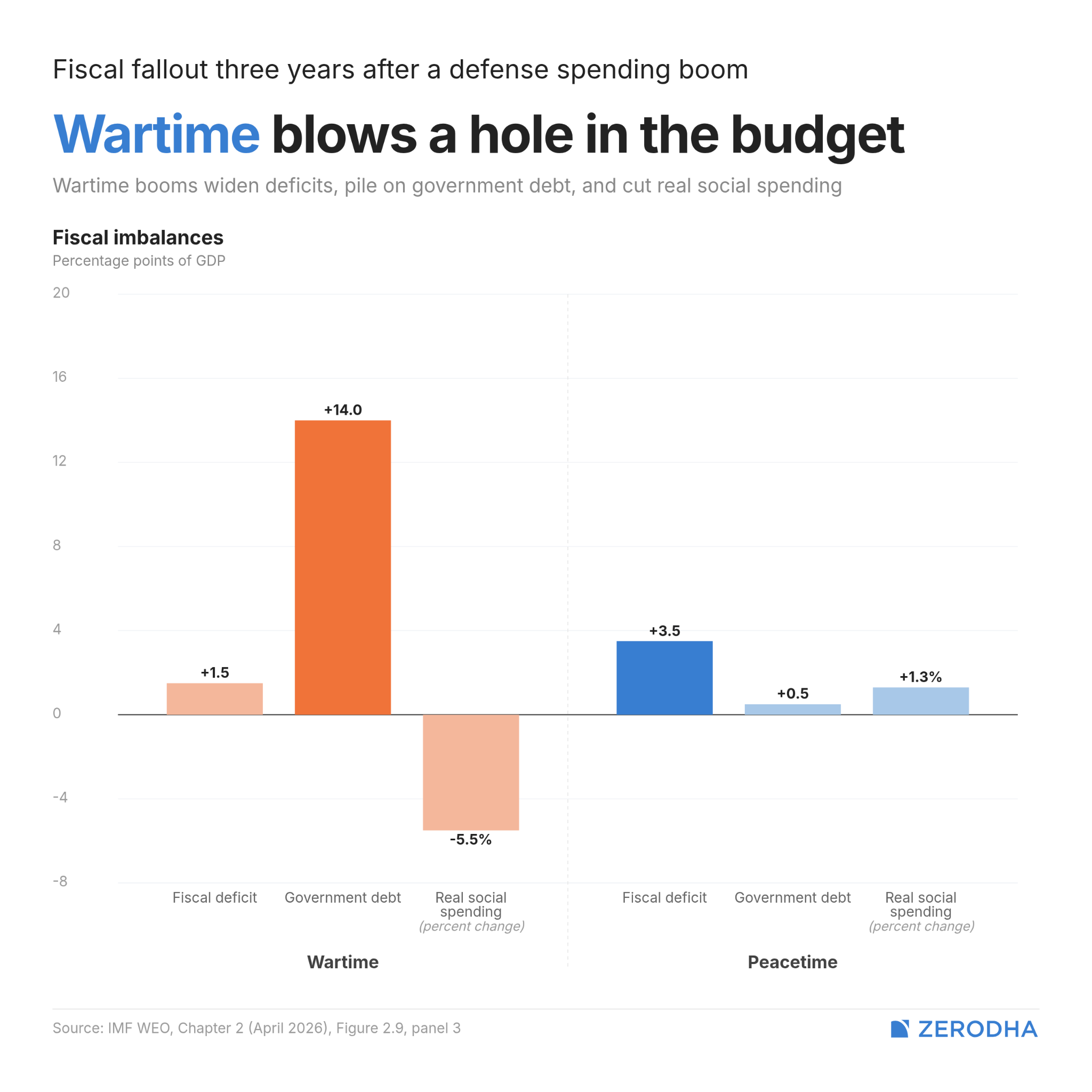

When the financing comes from cutting other spending rather than borrowing, the tradeoff is even starker. Health, education, and social protection fall by about 1% of GDP within three years. In wartime booms, social spending falls in real terms regardless of how the military expansion is financed. And public debt jumps by about 14% of GDP, nearly double the peacetime cost.

What actual conflict does

If rearming is expensive, war makes no economic sense. That’s what the IMF’s third chapter devotes itself to. And the answer goes beyond the destruction of physical and human capital, or what the reallocation of the productive capacity that survives towards military uses does.

For one, private investment collapses almost immediately in conflict-site economies. Even if a factory is standing and functional, its owner stops expanding it because they can’t be sure their assets, their workforce, or the government itself will exist in the same form next year. Uncertainty is one of the most powerful forces in wartime economics, and crucially, it operates independently of physical destruction. You don’t need your city to be bombed for investment to stop. The expectation of instability is enough.

Then, the fiscal situation deteriorates. Military outlays surge, but at the same time, the government’s ability to collect taxes weakens as economic activity contracts, administrative capacity erodes, and more of the economy moves into informality. Total government consumption can look stable on paper, but what that usually means is that defence is quietly crowding out everything else.

The external sector breaks down in an asymmetric way. Exports fall harder than imports. War damages the domestic production base, disrupts trade routes, and causes importing countries to shift their sourcing away, sometimes permanently. Foreign investment pulls back sharply, too. The government is left with a shrinking set of external financing options: diaspora remittances, foreign aid, and very little else.

All of this eventually hits the currency, as foreign exchange reserves drain down. Governments with flexible exchange rates see their currencies depreciate, while those with fixed rates face pressure to devalue. Either way, depreciation feeds back into inflation, which is already running hot from the supply disruption. Governments usually respond by imposing capital controls, restricting how much money can leave the country.

For the average conflict-site economy, the IMF estimates that output falls ~3% immediately at the start of a conflict, and reaches cumulative losses of around 7% over five years. These losses are larger and more persistent than those from banking crises, currency crises, sovereign debt defaults, or major natural disasters.

The losses don’t stop when the fighting does, either. Output deficits persist even a decade after conflict begins. Capital stock is about 4% lower five years in. And, of course, the harms go beyond macroeconomic scars. Individual health data from 41 countries shows lasting damage to cognitive ability, physical health, and mental wellbeing in people who lived through war.

Countries not involved in the fighting are not immune either. Neighbouring economies and major trading partners of conflict-site countries see output fall by around 1% in the first two years, as trade routes disrupt and regional uncertainty suppresses investment. These effects eventually fade, but they fall on countries that had no say in starting the fight.

Recovery is harder, and highly conditional

Once a war ends, the natural assumption is that rebuilding begins. Investment floods back, reconstruction creates a boom, and within a decade or so the country recovers. But as per the IMF’s data, that’s almost too fantastical a story.

To begin with, peace itself frequently doesn’t hold. In about 40% of post-WWII postconflict episodes, countries relapsed into conflict within five years of the fighting ending. In those cases, the economy didn’t even have a base to rebuild on because the conflict resumed before any new foundation could be laid.

When peace does hold, recovery takes place, but modestly. Output begins to rise, reaching about 3.9% above end-of-conflict levels five years later. The problem is that this starts from a substantially lower base. A country that lost 7% of output during the conflict and then recovers 4% of that loss is still far below where it would have been without a war.

Most of the recovery that does exist is almost entirely driven by labour. After all, workers come back from displacement, soldiers return to civilian life, and refugees trickle home, so labour supply recovers relatively quickly. But capital barely comes back, and neither does productivity. Investors remain cautious about committing money to a country where peace feels uncertain.

So, firms do something rational but economically limiting: they substitute toward labour and away from capital. Hiring workers is cheaper and more reversible than building factories. The result is an economy with more people working but no more efficient — the same tools, the same infrastructure, just more hands. This is why post-conflict recoveries can look statistically reasonable while feeling hollow on the ground.

But some countries have broken this pattern, and the IMF looks closely at how.

Rwanda is the extreme case. The 1994 genocide caused GDP to fall 42%, while inflation also reached 42%. Within a decade, though, growth had recovered to 6–9% annually and inflation was back at 2%. The recovery was built on several things happening at once: donor-financed imports that immediately suppressed inflation by relieving shortages, comprehensive debt restructuring, a rebuilt national revenue authority, radical anti-corruption reform, and so on. Bosnia, Cambodia, and Côte d’Ivoire show similar patterns at different scales.

Conclusion

The IMF is not in the business of predicting which wars come next. But it is in the business of reading macroeconomic signals — and the signal embedded in this edition of the WEO is unusually direct. The world is producing more conflict, not less. The number of active wars is at its highest since 1945. And the economic costs are being distributed globally, even to countries that aren’t fighting.

The countries most exposed to conflict are also, almost by definition, the least equipped to implement the policies that make recovery possible. The conflict trap the IMF documents — where fragile peace collapses back into war before any stabilisation can take hold — is not a failure of knowledge. The policy toolkit is reasonably well understood. It is a failure of institutional capacity, political will, and the near-impossibility of making good long-run decisions in the middle of a crisis.

That gap, between what works and what countries can actually deliver, is what makes war so economically catastrophic. And so hard to come back from.

Tidbits

Hindustan Zinc posts record profit, announces 550% dividend

Hindustan Zinc reported a 67.6% YoY jump in Q4 profit to ₹5,033 crore and 49% revenue growth, driven by higher metal prices and strong production. The company also announced a ₹11 per share interim dividend (550%), marking a record performance across key metrics.

Source: ET Now

India–New Zealand FTA to be signed, aims to boost trade

India and New Zealand will sign a Free Trade Agreement on April 27, aiming to double trade to $5 billion in five years. The deal will offer tariff-free access for Indian goods and open opportunities across sectors like textiles, pharma, and services.

Source: Economic Times

Bharti in talks to sell majority stake in insurance business

Bharti Group is in talks to sell up to 85% stake in its life insurance unit to Prudential Plc for about ₹7,000–8,000 crore. The deal would mark Bharti’s exit from life insurance, while helping Prudential expand in India’s growing market.

Source: Economic Times

- This edition of the newsletter was written by Aakanksha and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

How can Indian IT flip the AI script ft. Ameya P

The age of AI agents has, so far, been a thorn on Indian IT’s side, at least as far as valuations are concerned. Its business model is getting stale each passing day - that’s understood. There might be a possibility that Indian IT might just adapt to the new paradigm. But what does adaptation for Indian IT look like? What are the forms of inertia they will have to overcome to successfully change themselves? And even if they do adapt, will they be able to defend their new business?

To unpack all this, we spoke to Ameya P, a veteran in the global IT industry, and a prolific technology investor well-known for his investing takes on X. It’s an incredibly nuanced conversation from an expert who understands the nitty-gritties of what each AI development brings forth for this industry.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉