Why China Won’t Let India Rise?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Is China really suppressing India’s rise?

What the UNCTAD says about global trade

Is China really suppressing India’s rise?

If you’ve been following us for a while, you know we’re obsessed with China. So when, a few days ago, the American economics blogger Noah Smith wrote about how China was “trying to kneecap Indian manufacturing”, we figured we just had to bring this discussion to you.

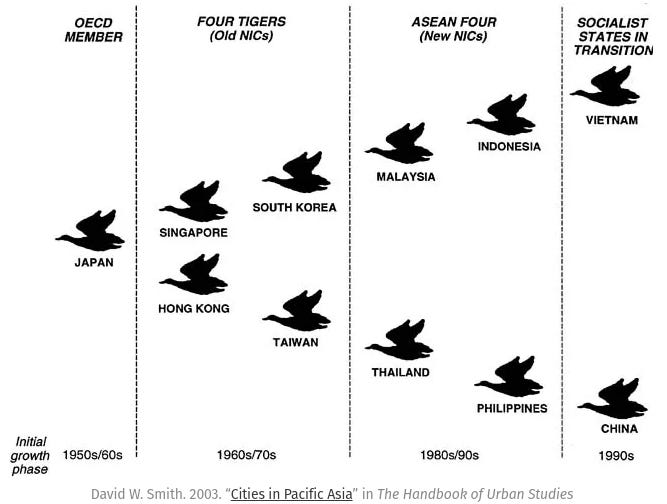

The basic argument is that most countries invest abroad as they climb up the economic ladder. As countries become rich, costs rise, and their enterprises look abroad to other countries where they can diversify. Those countries, in turn, see their own periods of growth and foreign investment. This almost resembles flying geese:

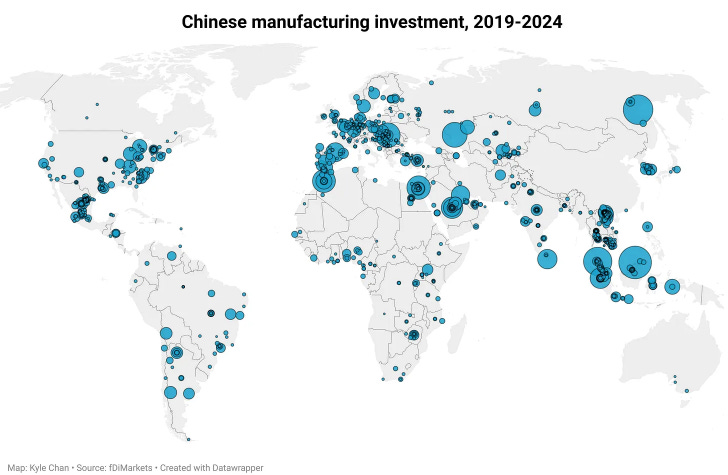

After many such waves, it is now China’s turn to invest abroad. And China has been doing so, all across the world:

Only, there’s an explicitly geopolitical facet to their investments — they seem to be pursuing some sort of “industrial diplomacy”. That is bad news for India. China sees us as both a geopolitical rival and a potential economic threat. This is why, the argument goes, China is blocking both investments and technologies from coming into India.

Until last year, we were in a much better position. We got a lot of support from the United States, which gave us the hope that we could counter-balance a China that was throwing its weight around. But America has now abruptly changed its economic trajectory. Without its support, the stakes for us are suddenly a lot higher.

That’s why we’re curious about where India-China relations currently stand. Do things still look bad? Are we openly antagonistic? Are we specifically being targeted as rivals to China? Now, we’re no experts on the topic. Geo-economics is a complex, multi-faceted chess game, and we’re not even close to seeing the entire board. But this is our best sense of how things look.

India-China relations: A brief history

A decade ago, Chinese firms were deeply interested in entering India. Chinese firms were steadily increasing their presence in India. India’s major industrial hubs were seeing ever-increasing Chinese investments. For instance, major Chinese mobile phone manufacturers — like Oppo, Vivo, and Xiaomi — had opened up major operations in India.

India was a fantastic investment destination for Chinese firms. We were, like China, a large, populous country with a deep domestic market. China was also just a few decades ahead of us in its industrial development journey, and many things it manufactured seemed perfectly suited for an economy like India — both to build and to sell.

But things took a sharp turn for the worse in 2020, as relations between the two countries soured. In April 2020, India changed its investment norms to block investments from China. Following a government notification, innocuously called “Press Note 3 of 2020,” any investments from India’s neighboring countries now required government approval. In theory, this was meant to stop foreign countries from buying up Indian companies for cheap during our COVID-era economic distress. In effect, though, it became a tool against China. We’ll come to this shortly.

Tensions soon became far worse, after the Galwan Valley clash in June 2020. In response, India banned hundreds of Chinese mobile apps on grounds of national security and cut many Chinese firms out from doing business in India — particularly from government procurements. Indian tax authorities, too, began arresting Chinese executives who worked in India.

Relations between the two countries have been icy ever since. While the total trade between the two increased through this period, India was making active efforts to move away from China. Many of our Production-Linked Incentive schemes were built around reducing our dependence on China and presenting ourselves as a global alternative. And last year, the United States replaced China as India’s largest trade partner.

China’s shifting investment strategies

Fast-forward to today. A lot has been written about the West’s attempts to embrace a “China+1” strategy, and “friend-shoring” or “near-shoring” their imports away from Chinese firms.

Zoom in, though, and this picture is rather complex. For instance, a lot of the money to make this strategy work was supplied by China itself. Chinese firms have spent the last five years “internationalizing” themselves. They have invested heavily in “connector countries” — countries which straddle the divide between the Chinese and Western blocs, and whom Western countries would therefore be more willing to accept imports from.

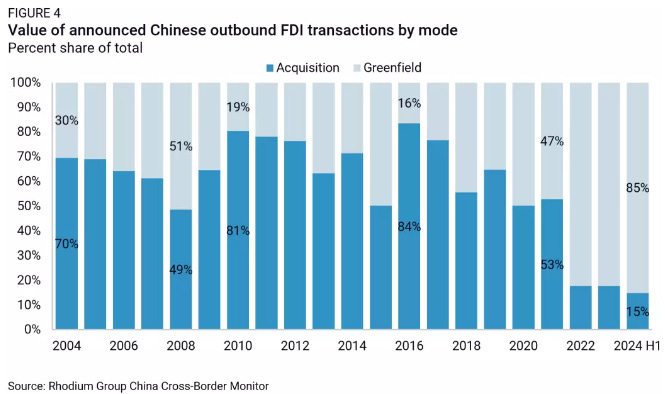

And so, even as the world was trying to cut back on trading ties with China, the countries that came to replace it — such as Mexico, Thailand, and Vietnam — saw a rapid surge in Chinese FDI. Notably, these investments were increasingly in ‘greenfield’ projects. Where previously, China would just focus on buying up old factories to acquire footholds in other countries, it was now building new units from scratch. By doing so, it was actively bringing capital into other economies, and creating thousands of jobs.

Notably, however, its diversification hasn’t purely been economic. Instead, a lot of its proposals have apparently gone to countries that seem ‘friendly’ to China. Take Europe for example. Last year, the EU voted for new tariffs on Chinese cars. In retaliation, China asked its EV companies to pause their investment plans in countries that voted in favour of the tariff. Meanwhile, countries like Spain and Hungary — which China sees as friendly to it — benefited from investments.

Some commentators have argued that India has seen the worst end of Chinese investment policy. This is, arguably, why India hasn’t really benefited from the China+1 move, despite trying to play itself up as a natural replacement for the country. But does this narrative really hold water?

Is China throttling Indian investments?

A key narrative, amidst this global shift, is that China is directing its firms not to invest in India. While China was never a major source of FDI into India — at least compared to countries like the United States or Japan — their investments are even lower now. Since 2020, in fact, we’ve only seen a faint trickle of investments from the country. In 2023, for instance, we barely received US$ 42 million from China.

But is this entirely the Chinese government’s doing? There are some reports, for instance, that the Chinese Ministry of Commerce strongly told their car makers to avoid investing in India.

But that case is over-blown. A major reason China doesn’t invest in India is that we weren’t keen on taking Chinese investments in the first place. Remember Press Note 3? In theory, we brought in the notification after the People’s Bank of China bought over 1% of HDFC Bank for cheap when the market crashed after the COVID-19 pandemic. We wanted to protect ourselves from other countries, who were trying to take advantage of us during a crisis.

But the notification operated much more widely. In essence, with the notification, every single Chinese investment proposal was to be screened by the government. And the government wasn’t generous. In 2023, for instance, a total of three applications for investment were approved — even as dozens were rejected. The rate of approval has improved slightly since. But even so, it isn’t particularly great. By April 2024, India had received 526 FDI proposals from China. 124 of those were accepted, while 201 were rejected. The rest were left in limbo.

Major Chinese companies came at the wrong end of this notification. For instance, in 2023, the Chinese EV giant BYD made a proposal to invest $1 billion into an EV factory in India. The proposal was rejected. The company has now taken an import-only strategy in India and has refused to open a local unit. Meanwhile, elsewhere, BYD has been creating tens of thousands of jobs.

Now, China hasn’t been particularly fair to India either. For instance, it banned India from accessing critical minerals like Germanium and Gallium — which are critical for chip manufacturing. Similarly, it refused to give customs clearances to German tunnel boring machines, that were made in China and were being exported to India. This stalled our construction of roads, metros, and railway tunnels.

Most recently, this January, China tried to sabotage India’s success in making iPhones. Getting those factories in was a major coup for India’s PLI policies, and China — who saw it as a conspiracy between the United States and Taiwan — wasn’t happy. It stopped Chinese engineers from moving to India and blocked critical equipment from reaching Indian iPhone factories. As a result, Foxconn, which owned those factories, had to scramble to relocate resources from Taiwan to India.

These aren’t isolated incidents. China routinely creates havoc for Indian industries by blocking their access to Chinese workers, inputs, or know-how. In all, though, this doesn’t resemble a concerted attempt to block India’s rise. The reality, instead, is a little more nuanced.

An alternate explanation

Back in 2020, China was openly belligerent towards India. India had to respond in whatever ways it could — and Chinese companies were its biggest target.

This was also a time when China took a deeply confrontational stance with the rest of the world. At the same time, China was becoming more expensive to manufacture goods in as well. This created an opportunity for India. The world over, countries started diversifying their supply chains. This looked like a golden opportunity for India to finally see a manufacturing boom — after all, much like China, India had a large market and cheap labour. It seemed like the only country that could really replace China as the factory of the world.

Only, the boom never really came. Despite a few high-profile successes, manufacturing has never become a significant part of our economy. This is partly because India has a restrictive policy environment, which makes it hard to set up large-scale manufacturing. But there’s another reason for this.

There was perhaps only one country in the world that could really create a manufacturing boom for India — and that was, sadly, China. It was they who had the technology to set up cutting-edge factories needed to practically make anything at all, and it was their people who knew how to run them. Where we succeeded, such as with manufacturing iPhones, it was because Chinese workers came to India and showed us what to do. But elsewhere, we missed out to countries like Vietnam and Mexico, which received billions in Chinese investment.

Of course, this isn’t to say that we took the wrong call by standing up to China. Back then, we had to do whatever we could to retaliate against an aggressive neighbour. But such decisions have trade-offs, and a big trade-off was how we lost the opportunity to bring in more manufacturing to India.

A potential thaw?

Over the last year, even while India-China tensions have flared up occasionally, it looks like there’s a new attempt to mend ties.

It began with last year’s economic survey — which argued that if India wanted to benefit from the China+1 strategy, it could not look past China. Instead, it had to get Chinese firms to invest in India.

Meanwhile, there were cautious attempts by both sides to cool the temperature on India-China relations. For much of last year, India had softened its rhetoric on China, reflecting a growing recognition that India needs Chinese technology and capital. In October last year, Prime Minister Modi and President Xi had their first formal meeting in five years.

Recently, Prime Minister Modi commented on how India and China were trying to restore their relationship from before 2020. In response, the Chinese Foreign Ministry praised his statements, stating that “an elephant-dragon ballet” was the only choice ahead for the two countries.

A couple of years ago, there was a consensus across the board: that India and China were locked in an existential contest. Back then, India and the United States seemed like natural allies, who were both committed to fighting a common adversary. In all honesty, that might still hold true. But after a long time, we at least see the possibility of a new narrative.

We’re keenly watching whatever happens next.

What the UNCTAD says about global trade

UNCTAD has just come out with a new report — its ‘Global Trade Update (March 2025)’ — which spells out how global trade looks at the moment.

At first glance, the report looks like any other technical report, packed with statistics and projections. But scratch beneath the surface, and it’s clear that more than just a trade update, this is a warning. The era of global cooperation and economic expansion is over. Tariffs, as we’ve often mentioned in this newsletter, are no longer a relic from the past. They’re back with a vengeance, and this report highlights just that. Trade is now explicitly being reshaped by politics, protectionism, and the increasing intervention of governments.

Here’s the big picture from the report: global trade remains resilient, but uncertainty looms. In 2024, trade hit a record $33 trillion. This record high was largely driven by a 9% annual increase in services trade, while goods trade saw a more modest increase of 2 percent. But early signs in 2025 indicate that this expansion may slow down. More importantly, beyond the sheer amount of trade, we’re now asking new questions: who is trading with whom, under what conditions, and for what strategic purpose?

Tariffs Are Back—And They’re Not Just About Economics Anymore

The UNCTAD report places a heavy emphasis on the return of tariffs as a major force in global trade policy. For decades, tariff rates declined as globalization expanded. But that trend has reversed. Countries are no longer simply using tariffs for economic protection over key industries — they are wielding them as political weapons. This is exactly what we have conveyed in our previous editions: that tariffs have become more of a political tool than an economic one.

The U.S.–China trade war, once thought to be an anomaly, has set a precedent: tariffs are now being used to shape global power dynamics.

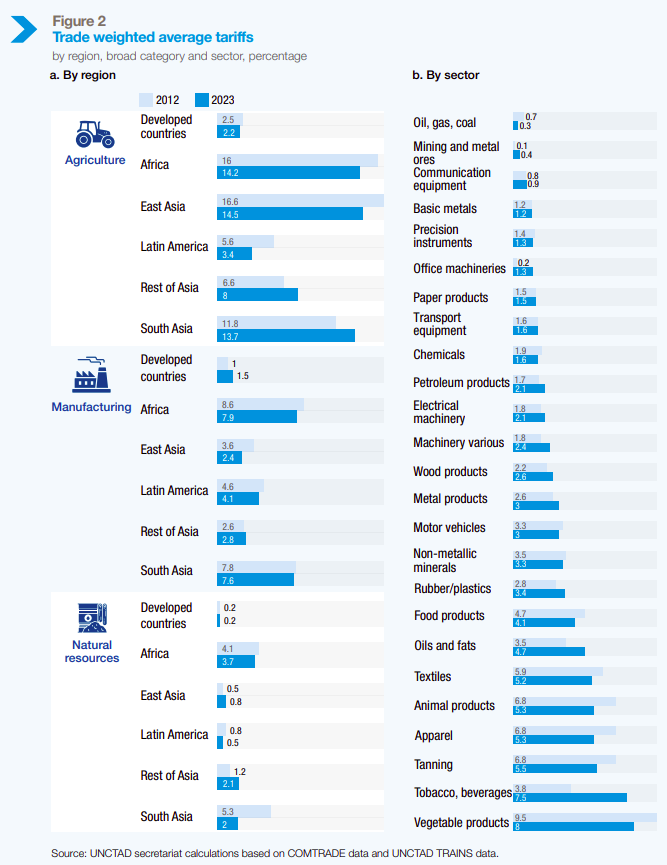

Developed countries, despite their historical advocacy for free trade, continue to impose trade barriers and high tariffs on key manufactured goods, while keeping tariffs on raw materials low. In fact, manufacturing goods have recently seen some of the highest escalations in tariffs.

This ensures that wealthier nations retain their dominance in high-value industries, while developing economies remain locked in the lower end of the global value chain as suppliers of raw materials.

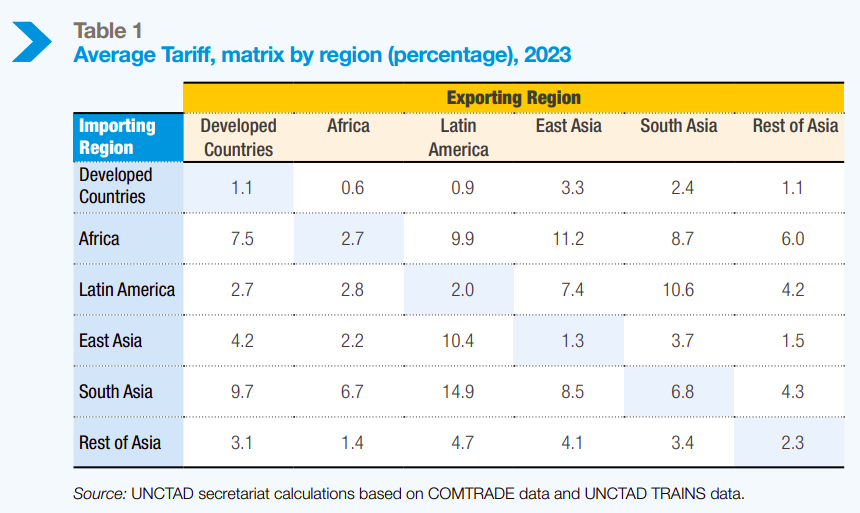

Agriculture also has high tariffs. Developing nations, today, face tariffs as high as 20%, despite Most-Favored-Nation (MFN) rules.

Importantly, the tariffs on processed goods are higher than those on raw agricultural commodities. As a result, developing economies might struggle to move beyond basic agricultural exports to processed, value-added food industries—precisely because tariffs keep their finished products out of Western markets.

South Asia is an interesting case. It’s widely known that we have some of the highest tariff rates for imports. At the same time, our goods also face some of the highest tariffs across the world for our exports.

Supply Chains Are Splintering, But China Remains Central

A central theme of the report is that global supply chains are being reconfigured — but not as quickly or as drastically as some policymakers had hoped. While there has been a push for “friend-shoring” (trading within political alliances) and “nearshoring” (moving production closer to home markets), China remains the dominant force in global trade.

While India, Vietnam, and Mexico have benefited from trade shifting away from China, no country has truly replaced China’s scale, efficiency, and infrastructure.

The U.S., under both Biden and Trump before him, pursued a strategy of economic decoupling from China, attempting to curb Beijing’s influence over global supply chains. This policy began with Trump’s aggressive tariff measures in his first term, and under Biden, evolved into a more sophisticated industrial policy — including restrictions on Chinese technology, sanctions on AI development, and efforts to create alternative supply chains for semiconductors and critical minerals.

Despite this, the UNCTAD report suggests that the idea of fully decoupling from China remains unrealistic. Even as supply chains shift, China continues to expand its trade surplus, and its economy remains deeply integrated with both developed and developing markets. India, despite its aspirations to be an alternative to China, still runs a significant trade deficit with its neighbor (-$103 billion), underscoring the difficulty of reducing dependency on Chinese goods.

The U.S.–China Trade War Isn’t Going Anywhere

The U.S.–China trade war, which has been simmering for nearly a decade, is poised to escalate further in 2025. According to UNCTAD, new tariffs and retaliatory measures are likely, particularly in strategic sectors like semiconductors, clean energy, and AI technologies.

Of course, this has been the case for many years now. But the key concern is that this is no longer just a U.S.–China issue. Instead, we might see spillover effects. Other major economies, including the EU and Japan, are now aligning with Washington to restrict China’s influence in high-tech sectors. The result is a fragmented global trading system where countries are being forced to pick sides.

China’s 2025 Economic Stimulus: Will It Boost Global Trade?

One of the most significant forward-looking elements in the report is China’s plan to stimulate its economy in 2025, with a GDP growth target of around 5%. The success or failure of this stimulus will have ripple effects across the global economy. If China boosts infrastructure spending, it could drive up demand for commodities like steel, copper, and energy, benefiting major exporters like Australia, Brazil, and parts of Africa. On the other hand, if the stimulus fails to reignite growth, it could signal a prolonged period of economic stagnation for China, dragging down global trade in the process.

What Comes Next? The Future of Global Trade in 2025 and Beyond

The overarching takeaway from the UNCTAD report is that trade is no longer just about economics—it’s about geopolitics, industrial policy, and national security. The era of unfettered globalization is over, and 2025 will be defined by a more fragmented, more volatile trading system.

Countries are increasingly looking inward, prioritizing domestic industries over global integration. Supply chains will continue to shift, but China’s dominance will not disappear overnight. Meanwhile, trade imbalances will persist, shaping policy decisions in the U.S., China, India, and beyond. Industrial policy and government intervention will determine which industries thrive and which struggle.

Ultimately, 2025 will not be a return to “normal” trade patterns. Instead, the shifts are solidifying. The global economy is moving into a new phase where trade policy is as much about power as it is about profit. The question is no longer whether the world will embrace free trade again, but rather how governments will use trade to shape their own national interests.

For businesses, investors, and policymakers, the message from UNCTAD is clear: prepare for turbulence, because global trade is now a battleground.

Tidbits

Blackstone has made a non-binding $1.2 billion offer to acquire AkzoNobel India’s decorative paints business, including the transfer of intellectual property. AkzoNobel NV, which holds 74.76% in its Indian subsidiary, is considering selling its powder coating operations and International Research Center.

India’s crude oil imports fell 10.6% year-on-year to $10.34 billion in December 2024 from $11.57 billion in December 2023, as shipments from key suppliers Russia, Saudi Arabia, and Kuwait declined. Imports from Russia dropped 18.48% YoY to $3.19 billion, with volumes down 12.3%, marking the first decline in four months. Saudi imports fell 43.1%, while Kuwait’s shipments decreased 38%, with volumes declining 36.4% and 33.6%, respectively. The overall import value was also down 16.5% month-on-month from $12.4 billion in November 2024.

India’s Production Linked Incentive (PLI) scheme for bulk drugs has led to the commissioning of 34 projects, enabling the production of 25 key Active Pharmaceutical Ingredients (APIs). The scheme has attracted ₹4,200 crore in investments, generating ₹1,500 crore in sales, including ₹400 crore in exports. Bulk drug and intermediate exports stood at $3,520 million between April- December FY25, marginally exceeding imports at $3,504 million. In FY24, exports were $4,787 million, while imports were $4,556 million.

- This edition of the newsletter was written by Krishna and Pranav

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

dont talk nonsense, have you seen indian authorities tax hostility on china, the govt should have kissed their feet because without chinese 4g phones there digital india dreams was a fantasy. the govt has effectively seized all the chinese companies under fake cases and forced even to transfer equipments .

why because apple has come into the picture and the chinese are not required.

if i rob you blind will you trust me .