Why Bank Stocks Are Suddenly Booming

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

RBI makes it easy for banks

Diamonds in the rough

India’s Tax on Steel is here

RBI makes it easy for banks

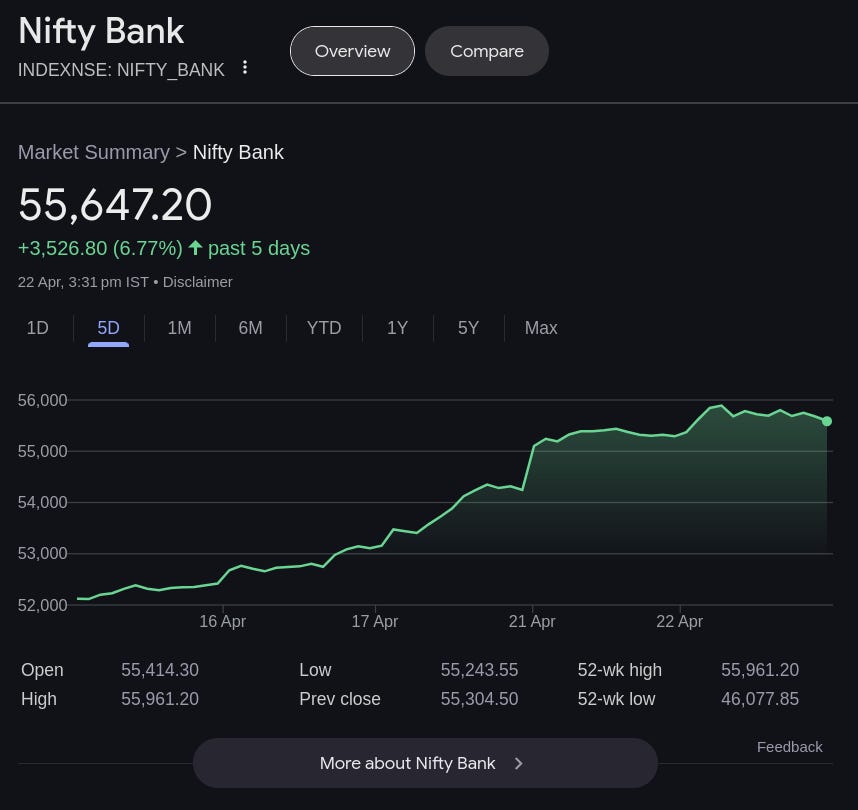

The RBI recently came out with a notice finalizing new rules about how banks manage their Liquidity Coverage Ratio (LCR) and it has had banking investors really happy. These final norms turned out to be far more benign for banks than the July 2024 draft, prompting relief in the banking sector. Bank stocks rallied on the news, as the Bank Nifty index hit record all time highs on April 22, 2025, driven by the “softer-than-expected” rules, as per Business Standard.

But what’s this new notice about, how is it related to the July 2024 draft and how did it all start with the fall of Silicon Valley Bank halfway across the world? There are a lot of questions and context needed to uncover this. So let’s take it from the top, shall we?

Where did it all start?

The collapse of Silicon Valley Bank (SVB) in March 2023 highlighted how rapidly deposits can flee a bank in the age of digital banking. SVB experienced a massive, technology-fueled bank run as depositors moved funds out via online channels, underscoring new liquidity risks for banks. Global regulators took note, and the Reserve Bank of India (RBI) began examining whether its liquidity coverage ratio (LCR) assumptions were adequate in this new context.

The LCR is an international standard requiring banks to hold enough High-Quality Liquid Assets (HQLA) (cash, central bank reserves, government bonds, etc.) to cover expected cash outflows in a 30-day stress scenario. This number must mandatorily be above 100%.

On July 25, 2024, RBI released a draft circular which outlined several significant changes intended to enhance banks’ liquidity resilience in the face of tech-driven withdrawal risks, like the SVB crisis.

The key proposals in the draft were:

Higher Run-off for Digital Deposits: Run-off refers to the portion of a bank’s liabilities that are expected to be withdrawn or leave the bank in a stress scenario. So if let’s say a bank has retail deposits of, say, ₹1,000 crores, and a run-off rate of 5%, then it means that it is assumed that ₹50 crores of that deposit might be withdrawn in the next 30 days under stress scenario. This might not actually happen, but the numbers provide for the worst case scenario.

Banks would have to assume an additional 5% “run-off” on retail deposits accessible via internet or mobile banking (IMB). In other words, any retail or small-business deposit with digital banking access would be treated as less sticky: “stable” deposits’ assumed 30-day outflow rate would double from 5% to 10%, and “less stable” deposits from 10% to 15%. So basically, now banks would need to keep more high quality liquid assets, against the same amount of deposits, meaning less money left to lend outside, hurting profitability.Haircuts on Government Securities in HQLA: So for every deposit the bank had, some money had to be set aside in this high quality liquid assets. But, even top-quality liquid assets like central government bonds would no longer count at full value. The draft proposed valuing G-sec holdings at no more than current market price, minus a haircut, basically reflecting their true value. This change aimed to account for potential price volatility in even safe assets – a lesson from SVB where rising rates eroded bond values.

Including Pledged Fixed Deposits as Outflows: Currently, non-callable FDs (which cannot be prematurely withdrawn by customers) were excluded from LCR outflow calculations, because technically they can’t be withdrawn, therefore had 0% run-off. The draft insisted that if such an FD is pledged against a credit facility, it should be treated as callable – meaning the bank must assume it could be drawn down if the borrower defaults or needs to liquidate the collateral. In effect, loans against FDs would no longer let the underlying deposit stay invisibly “locked” for LCR purposes; the pledged deposit would count as a potential cash outflow.

The draft was slated to take effect from April 1, 2025, giving banks only about 8 months to prepare. These draft norms were viewed as strict and potentially onerous. Analysts estimated the proposals would significantly reduce reported LCRs across the sector – by 11–18% on average, per an IIFL analysis. Some banks’ LCRs could have fallen below the 100% regulatory minimum under the draft.

Banks would have needed to add a large volume of HQLAs (mostly government bonds) to meet the new requirements by April 2025. Market estimates at the time suggested an additional ₹2–4 trillion of government bond demand would be created – hence bond yields actually dipped in anticipation of banks buying more G-secs (India’s 10-year yield hit a 2-year low when the draft was unveiled, reflecting this expected demand).

But the banks did not take it well.

Banks Were Unhappy

The Indian Banks’ Association (IBA) sought to water down and delay the rules. Specifically, banks argued that a 5% additional run-off was too high, urging a reduction to about 2–3% instead. On the implementation timeline, banks requested more time beyond April 2025, given the systems changes and incremental HQLA buildup required.

There was apprehension that forcing banks to hold substantially more HQLA would “squeeze credit” to the real economy. Funds tied up in government bonds or cash reserves are not available for lending.

So, the RBI listened. By November 2024, there were indications that RBI was reconsidering – especially after the government’s formal request. The guiding principle became finding a “balance between credit needs of the economy and the health of the banking sector”, ensuring liquidity resilience without unduly choking lending.

Final (& Lenient) LCR Guidelines Came

After evaluating the feedback, RBI issued the final LCR guidelines on April 21, 2025 and it caught everyone by surprise, positively. Here is what changed:

Reduced Run-off Add-on for Digital Deposits: The additional outflow assumption for digitally accessible deposits was cut in half. Banks must now apply only a +2.5% run-off factor (not 5%) on deposits with internet/mobile banking access

This meant, the stable retail/small biz deposits with digital access will carry a 7.5% run-off (vs 5% currently), while the less-stable retail/small biz digital deposits will have a 12.5% run-off (vs 10% currently)

Compared to the draft, which had 10%/15%, this is a significant easing. About ~85% of banks’ deposits are estimated to be in the “digitally enabled” category, so this change substantially reduced the burden relative to the draft.

New Lower Run-off for Non-financial Wholesale Deposits: The final guidelines introduced an entirely new concession that was absent in the draft. Unsecured wholesale funding from non-financial legal entities (i.e. corporates, trusts, partnerships, associations, etc. that are not financial-sector entities) will now attract only a 40% run-off rate, instead of 100%.

In other words, a chunk of what was previously treated as potentially “flighty” wholesale deposits will be considered more stable.

Additionally, the proposal in the draft about treatment of pledged non-callable deposits and haircuts on government securities in HQLA, holds.

But, one of the biggest reliefs: banks were given an extra year to comply. The final guidelines will take effect from April 1, 2026, instead of April 2025 as originally proposed. This generous transition period ensures banks can adjust gradually – whether by accumulating a bit more HQLA or tweaking their deposit base – without scrambling.

What does it mean for the Banks?

The central bank’s impact study on December 2024 data showed that, had the final norms been in place, the aggregate banking system LCR would rise ~6% (vs. current rules) and “every bank would meet the minimum LCR of 100%”. By contrast, the draft norms would have lowered the LCR system and put some banks under 100%. In short, the final package turned what banks feared as a potential constraint into a net positive.

Essentially, the reduction in outflows from the wholesale deposit rule more than compensates for the increased outflows from digital deposits for most banks, therefore the estimated 6% rise in LCR.

An additional outcome of higher LCRs is that banks will have excess HQLA they can redeploy. This creates an opportunity to use liquidity more efficiently.

ICRA’s estimate was an additional ₹2.7–3 lakh crore could become available as lendable resources for the banking system. Morgan Stanley likewise projected an additional loan growth of 1–2% due to these LCR changes.

By freeing some liquidity to move from low-yield assets (like cash or 3-5% yielding T-bills) into higher-yield uses (like loans ~8-10%), banks stand to earn more. The impact on net interest margin (NIM) and profitability is positive, though modest in percentage terms.

CLSA estimated that sector-wise NIM could improve by ~3 bps (0.03%) due to this redeployment. IIFL’s more detailed modeling, assuming banks maintain around 120% LCR buffers, suggested individual banks’ NIMs could expand by anywhere from 1 to 18 bps.

Conclusion

What began as a post-SVB tightening exercise ended as a balanced recalibration of liquidity rules. The chain of events – from the alarm bells of SVB’s digital bank run, to RBI’s heavy-handed draft in July 2024 aimed at preempting such risks, through months of industry feedback and government concern about credit – culminated in April 2025 with final LCR guidelines that thread the needle.

We find it very reassuring, that the RBI paid heed to the feedback from the industry, and came up with the final rules, that not only set a proactive tone of preventing anything like the SVB happening in India, but at the same time not doing anything that hampers the credit growth too much.

Diamonds in the rough

India’s polished‑diamond exports have dropped to ₹ 1.10 lakh crore, their lowest level in twenty years. That headline number hurts on its own—but the real sting is what it means for India’s broader trade and for Surat, the city that turns dull rock into sparkle. Gems and jewellery still bring in about 7 % of all merchandise exports; diamonds contributing to roughly 50% of that number according to last fiscal year’s number.

When diamond earnings tumble, India’s trade balance and a million pay‑cheques tumble with them.

How a rough rock ends up in Surat

Before we talk about falling exports, let me set up some quick context. You see, a diamond starts life 150 kilometres underground, where heat and pressure turn carbon into crystal. Millions of years later a volcanic blast called a kimberlite eruption drags those crystals toward the earth’s surface. Miners in Botswana, Russia or Canada scoop up the volcanic rubble, crush it, and pull out cloudy stones called “roughs.”

Those roughs fly to trading rooms in Antwerp or Dubai, where dealers argue over colour, clarity and carat. Almost every parcel then heads for Surat. Why? Because no other place has the sheer muscle that Surat does: more than five thousand polishing units and about 8-10 lakh workers who turn dull pebbles into sparkling gems more cheaply, and often more neatly, than anyone else.

Every 9 out of 10 diamonds we get to see in the plush stores in the big cities all over the world is cut and polished in India’s Surat. Diamond money fuels bus routes, street‑food stalls and entire blocks of laser‑machine factories. We couldn’t verify this claim but a bunch of articles say that diamonds are generally considered to be around 80-90% of Surat's industrial output.

From boom times to a bust

Back in 2021‑22 the diamond trade was booming. India sold polished stones worth ₹ 2.92 lakh crore (US $40 billion)—its best year ever.

In a normal year Surat’s maths is simple:

buy roughly ₹ 90,000 crore of rough diamonds,

polish them,

sell the finished stones for about ₹ 1.5 lakh crore,

and keep the ₹ 60,000 crore difference to pay workers, electricity bills, bank loans and profit.

Last year that “difference” melted to only ₹ 21,000 crore. Why?

Finished‑stone prices tumbled. A price guide called RapNet—think of it as the “sensex” for one‑carat diamonds—dropped 20 % in 2023 and another 14 % in 2024.

Rough‑diamond prices also slid—down about a third from their 2022 peak— but not enough to protect margins.

Because money was tight, many workshops never reopened after the 2024 Diwali break. The Gujarat Diamond Workers’ Union says about 2,000 small factories (roughly 40 % of the cluster) are still shut. Those that did reopen halved working hours. Wages that once touched ₹40–50 thousand a month have fallen to ₹15–18 thousand. Union leaders link this sudden income crash to around 70 worker suicides in the past seventeen months.

Shocks that landed together

1. Sanctions shut the “Russian shortcut.”

Until last year a Surat workshop could buy rough stones from Russia, cut them in India, stamp them “Indian origin,” and sell them to American or European jewellers with no problem. That door is now bolted.

1 Jan 2024 — Phase 1: The G7 banned any rough or polished diamond that ships directly from Russia.

1 Mar 2024 — Phase 2: The ban widened to diamonds originally mined in Russia, even if they were later cut and polished in a third country like India.

Trace‑or‑trash rule: Every diamond headed to a G7 buyer must now stop at a verification hub in Antwerp and prove its exact mine of origin. No papers, no entry.

Because the United States and Europe together buy about 70 % of the world’s diamond jewellery, Indian cutters know they will struggle to sell any gem that started life in a Russian mine. So demand for Russian rough has collapsed— even though India itself never banned it.

Add weak global demand and a mountain of unsold stock, and importers have little reason to bring in more rough of any kind. According to our understanding and research this is one of the reasons why India’s rough‑diamond imports fell 24 % last year: not because customs blocked them, but because exporting the finished stones now looks risky and often unprofitable.

2. Soft U.S. and Chinese demand—and the LGD effect.

America buys over 30 % of India’s diamond jewellery. Inflation thinned wallets, weddings were scaled back, and one in five U.S. engagement rings now sports a lab‑grown diamond (LGD) that looks identical but costs 60‑80 % less. Surat polishes these synthetics, yet last year’s LGD exports—about ₹ 10,700 crore—replace only a tiny % of the revenue lost on naturals. In China, a stubborn property slump pushed shoppers toward gold and away from gems, wiping out India’s second growth engine.

3. Tariff shock.

On 28 March Washington warned that a 27 % duty on Indian diamonds could start on 9 April. U.S. wholesalers sprinted to import before the tax date, giving March exports a cosmetic one‑percent bump. When the duty was paused for 90 days, buyers froze. Factories that had emptied shelves for the rush suddenly had no April orders.

4. The inventory mountain.

With demand weak and LGD prices sliding, polished stones piled up. The Global Trade Research Initiative (GTRI) says there’s a major buildup of unsold diamond inventory in India, with the gap between net rough diamond imports and net polished diamond exports widening from $1.6 billion in FY22 to $4.4 billion in FY24

It is established industry practice for diamond traders to use inventory as collateral for bank loans. However, banks are now much more cautious, especially after high-profile defaults and frauds. Lenders have increased collateral requirements and are wary of accepting diamond stock as security due to its illiquidity and valuation risk

Why the slowdown matters far beyond Surat

Jobs and local economies.

Cutting and polishing keeps about 10 lakh Indians directly employed and another 20 lakh busy in side businesses—people who drive trucks, sell tea and snacks near the factories, repair laser machines, ship parcels or insure them. When two lakh cutting seats sit empty, whole neighbourhoods lose rent, bus fares and grocery sales.

Foreign‑exchange cushion shrinking.

Gems‑and‑jewellery exports still brought in ₹2.37 lakh crore last year, but that’s down from almost ₹3 lakh crore two years ago. A drop in diamond earnings widens India’s current‑account gap—money the country then has to borrow in dollars or cover with costlier oil and electronics imports. A thinner forex cushion can pressure the rupee when global energy prices spike.

India’s Tax on Steel is here

India just slapped a temporary 12% tax on certain imported steel products for about 200 days to protect local steel companies. These companies have been struggling to compete with ultra-cheap foreign steel, primarily from China, South Korea and Japan.

But why now? Has it happened before? Who else will be impacted? Let’s break it down.

What Exactly Happened?

We have to rewind a bit to understand the background.

Over the past two years, India – despite being the world’s second-largest steel producer – has been importing more steel than it exports. In the fiscal year 2024-25, India’s finished steel imports hit 9.5 million tonnes, a nine-year high. In contrast, India’s steel exports have slumped. So, the balance tipped: more foreign steel coming in, less Indian steel going out.

How did this happen? In one word - "dumping" - when a country floods another market with products priced so low that local producers simply can't compete.

Countries like China make more steel than it needs domestically. When their economy slows down, instead of cutting production, they often ship excess steel overseas at rock-bottom prices.

Chinese mills were offering steel at around $460–480 per tonne, and even after adding the usual customs duty and freight costs, the total landed price in India came to about $530–$535 per tonne, which translates to about ₹44,000–45,000. In comparison, the same kind of steel made in India was selling for around ₹51,000–52,000 per tonne in March and early April 2025. That meant Chinese steel was cheaper, a big saving for manufacturers who use steel as a raw material.

But that price advantage was exactly what made Indian steelmakers worried. They were being undercut so badly that some had to slash prices or reduce production.

Where is this steel coming from?

Primarily from our three Asian neighbors, China, South Korea, and Japan, which accounted for nearly 80% of Indian steel imports. China was the top steel exporter to India and was only recently replaced by South Korea.

And this problem did not look like it was stopping. In fact, it looked like more countries were rushing in.

In 2023-24, Vietnam sent nearly 1 million tonnes of steel to India, a huge leap from virtually nothing before, and became the fourth-largest supplier of steel to India. And Vietnam, like South Korea and Japan, benefits from a free trade agreement, meaning its steel entered India without any import duties.

China doesn’t have a free trade agreement with India. However, Chinese steel was often so cheap that even after paying India’s basic import duty of around 7.5% it could still compete and undercut Indian steel.

Major Indian steel producers like JSW Steel, Tata Steel, and the government-run SAIL have been calling for protection for years now. Indian steelmakers saw the writing on the wall – a lot more cheap steel was on the way.

Why Right Now?

The timing wasn't random. Let’s get into what’s been brewing under the surface:

The Directorate General of Trade Remedies started a formal investigation in December 2024 into whether action was justified. By March 2025, the DGTR was convinced that there was a “sudden and sharp” rise in imports that could cause serious injury to Indian manufacturers. That phrasing is important because, under WTO rules, that’s the test for applying a safeguard measure. Officials then recommended imposing a 12% safeguard tariff, essentially giving the green light.

In early 2025, trade tensions between the U.S. and China flared up again. The U.S. had maintained its 25% steel tariff, and there were fresh moves in Washington to tighten screws on Chinese goods. That raised fears that even more Chinese steel might get redirected toward India.

Global Context and Comparative Measures

India's move also aligns with global trends where countries are taking steps to protect their steel industries from cheap imports.

Since 2018, when the US imposed 25% tariffs on foreign steel during the US-China trade dispute, there's been a domino effect. Countries globally launched 129 trade measures against steel imports between 2019 and 2023, according to the Indian Steel Association. Malaysia imposed anti-dumping duties ranging from 2.52% to 36.80% on certain steel products from China, India, Japan, and South Korea in January 2025 for 120 days.

Without a tax, India risked becoming the "dumping ground" for steel that couldn't go elsewhere.

Not All Steel Is Affected

Interestingly, India isn't blocking all steel imports. The duty is targeting only specific products and sources:

Specialty steels are exempt: Electrical steel for transformers, tinplate for packaging, stainless steel, and several other specialized products won't face the extra duty. Why exempt these? The main reason is that many of these either are not made in sufficient quantities in India or are very high-end niche products. Similarly, stainless steel wasn’t part of the sudden import surge that’s hurting carbon steel producers, and hence is exempted.

Premium-priced imports are safe: The safeguard duty comes with a price threshold. If the imported steel is above a certain price, it won’t be taxed the extra 12%. If hot-rolled steel costs more than $675 per ton or color-coated steel exceeds $964 per ton, no extra duty applies. This targets only the suspiciously cheap imports.

India's Steel Trade History

This isn't India's first attempt to protect its steel industry. From 2015 to 2017, India imposed a series of safeguard duties and minimum import prices on steel products when facing a similar situation. Back then, cheap Chinese steel was also the primary concern, with imports surging nearly 71% in 2014-15.

India has historically shifted between protectionist and more liberal trade policies for steel, depending on market conditions.

Conclusion

For India, steel is not just another commodity; it’s the backbone of infrastructure and manufacturing. Ensuring the industry’s health is almost a strategic need. It is also one of the remaining economies with a growing need for steel. Global steel dynamics are shifting fast, and India doesn’t want to be left absorbing everyone else’s oversupply. For now, this gives domestic producers a fighting chance to stabilize and stay competitive.

Yet, India also champions itself as a supporter of free trade on the international stage – so it has to justify that this safeguard is a legal, necessary remedy to a specific problem, not a slide into protectionism.

What happens after 200 days? The DGTR will conclude its investigation and decide if a longer-term measure is needed. By then, the landscape might have changed – maybe global prices will rise making dumping less attractive, or maybe India’s demand will have grown further. Only time will tell.

Tidbits

Samsung and LG Challenge India’s ₹22/kg E-Waste Recycling Mandate in Court

Source: Business Standard

South Korean electronics giants Samsung and LG have moved the Delhi High Court against India’s revised e-waste pricing policy, which mandates a floor price of ₹22 per kilogram for recycling. The companies argue that this rate is 5 times higher than existing market prices, significantly raising their compliance costs. The move comes as part of a broader government effort to formalize the e-waste sector, which saw only 43% of its waste recycled in 2023. At least 80% of e-waste is currently processed by informal players. Other major firms like Daikin, Havells, and Voltas have also filed similar petitions, citing financial strain and poor implementation. LG has criticized the policy for penalizing producers instead of addressing gaps in enforcement, while Samsung claims the revised pricing will impact operational viability. The legal dispute highlights the growing tension between environmental regulation and business sustainability in India’s consumer electronics market.

Core Sector Growth Inches Up to 3.8% in March, FY25 Closes at 5-Year Low

Source: Business Standard

India’s core sector output rose by 3.8% in March 2025, up slightly from 3.4% in February, according to data released by the Ministry of Commerce and Industry. The uptick was driven by strong performance in cement (11.6%), steel (7.1%), and electricity (6.2%). However, key sectors like natural gas (–12.7%) and crude oil (–1.9%) remained in contraction, with refinery products posting a marginal 0.2% growth. For the full fiscal year FY25, core sector growth came in at 4.4%, marking its slowest pace in five years. This compares with 7.6% in FY24, 7.8% in FY23, and 10.4% in FY22. The Index of Core Industries accounts for 40.27% of the Index of Industrial Production (IIP). Core sectors like coal also showed weak momentum at 1.6%. Analysts attributed electricity growth to rising temperatures, while oil and gas remained subdued due to import substitution and lower prices.

RIL Buys Up to ₹10,000 Cr in G-Secs Amid Falling Bond Yields

Source: Business Standard

Reliance Industries Ltd. (RIL) has purchased government securities worth an estimated ₹7,000 to ₹10,000 crore from the secondary market during the second week of April, following the Reserve Bank of India’s Monetary Policy Committee decision to cut the repo rate by 25 basis points on April 9 and shift its stance to “accommodative.” The purchases were made on and around the policy day, with private banks also participating actively. Market participants expect the yield on the 10-year benchmark government bond to fall further to 6.25 percent. The RBI has injected ₹3.3 lakh crore through open market operations and ₹2.2 lakh crore via long-term variable rate repo auctions, with net banking system liquidity in surplus by ₹1 lakh crore. The move by RIL aligns with expectations of continued softening in yields and deeper rate cuts in the coming months.

- This edition of the newsletter was written by Kashish, Krishna and Prerana.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉