Who said what about the Dollar Supremacy, Structural Uncertainty, India’s Investment Thesis, and Global Trade Politics?

Hello, I’m Kashish Kapoor and welcome to Who said what?—the show where we dive into interesting comments from notable figures across the world, whether in finance or the broader business world, and explore the stories behind them.

I’m filling in for Krishna this week yet again, and no, he’s not been fired, yet. I’m just filling his shoes until he’s back.

For today, I’ll go over the comments from Dario Perkins, Raghuram Rajan, Jerome Powell, Goldman Sachs & Manish Chokhani.

Let’s get started.

Dario Perkins on dollar supremacy

Today, we're exploring fascinating perspectives on the US dollar's future. Even though the dollar is the currency of the United States, what happens to it determines the fate of emerging market countries like India. So whether you want to or not, you have to pay attention to the future of the dollar.

Let's start with an interesting tweet from Dario Perkins, Managing Director of Global Macro at TS Lombard.

Perkins also added in a follow-up tweet:

Let's break down what's happening here and put it in the broader context of some fascinating developments in the global economy.

The Dollar Drama of 2025

So what exactly is Perkins responding to? Well, if you've been following the news, you'll know that we're witnessing what some are calling the beginning of a "dollar crisis." Since mid-January, the dollar has fallen more than 9% against major currencies, with about 40% of that decline happening just since April 1st. This comes after the massive tariffs that Trump has imposed on pretty much the entire world that have been paused.

As the Financial Times puts it in their recent article, investors and analysts around the world are now confronting two critical questions:

First, how far can the dollar's recent decline go? With foreigners owning $19 trillion of US equities, $7 trillion of US Treasuries, and $5 trillion of US corporate bonds, even a small shift away from these positions could put sustained pressure on the dollar's value.

Second, and perhaps more profound: Could these outflows eventually erode the dollar's unique role in the global economy and financial system?

And, why does this matter? Because for decades, the dollar has been the foundation of global finance – the safe haven where investors go when things get rough. It's the currency that dominates international trade, the benchmark for global commodities, and the anchor for the world's financial system.

But now? That certainty is being tested.

The Trump Effect

The catalyst appears to be the policies of President Trump's second term. The Economist magazine just published a stark warning titled "How a dollar crisis would unfold," arguing that Trump's massive tariff increases have created economic uncertainty, disrupted supply chains, and boosted inflation.

Add to this America's already challenging fiscal position – net debts at about 100% of GDP and a budget deficit of 7% – and then pile on congressional plans that could add $5.8 trillion in deficits over the next decade. Put simply, investors are starting to worry about America's economic credibility.

The Economist writes, and I quote

"The shocking thing is that a full-blown bond-market crisis is also easy to imagine."

The Plaza Accord Reference

This brings us to an interesting historical parallel. Back in 1985, the major economies signed what was called the "Plaza Accord," where countries agreed to intervene in currency markets to depreciate the dollar against the Japanese yen and German Deutsche mark. The result? The dollar fell 40-50% against those currencies.

Fast forward to today, and there's been talk of a possible "Mar-a-Lago Accord" – named after Trump's Florida residence. As Ila Patnaik and Ajay Shah explain in their recent article, Stephen Miran, who now chairs Trump's Council of Economic Advisors, has been floating ideas about restructuring the global trading system. The core idea is similar to the Plaza Accord – coordinate internationally to bring about a significant dollar devaluation, possibly around 20%.

But here's where Dario Perkins' tweet becomes really insightful: he's drawing a clear distinction between two different phenomena.

What Perkins is actually saying

Perkins is making a nuanced point that many commentators are missing. He's saying:

Yes, global investors are diversifying outside the US in 2025 – that's happening and it's causing the dollar to weaken.

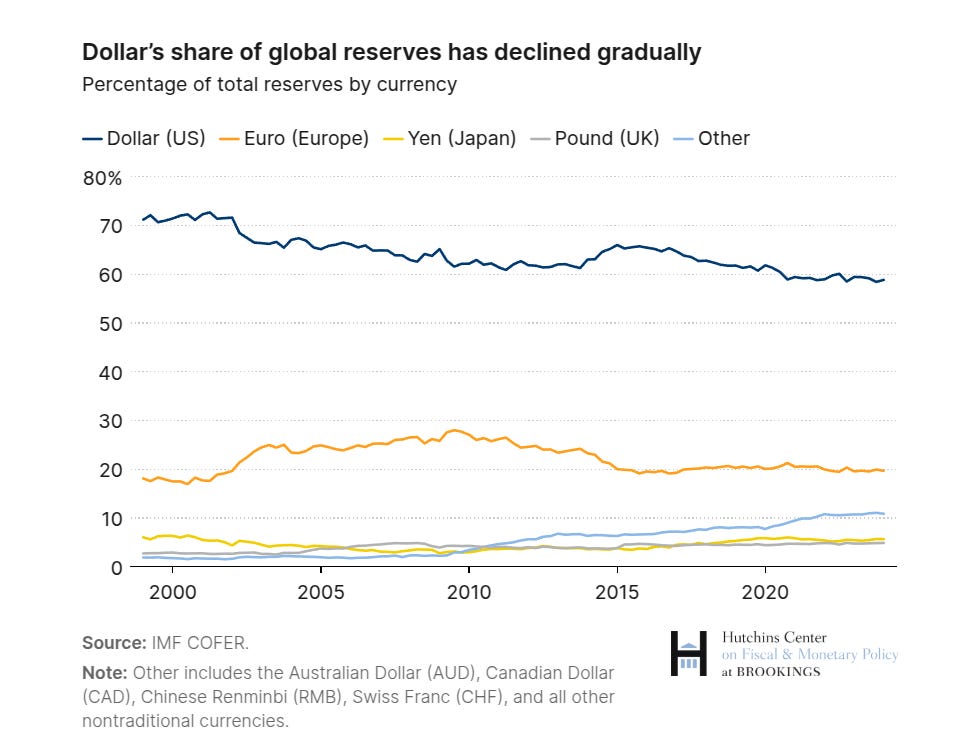

But no, this doesn't mean the dollar is about to lose its status as the world's reserve currency.

Why? Because of what economists call "network effects." The dollar isn't just valuable because the US is powerful – it's valuable because everyone else uses it. It's like how Facebook became dominant not because it was necessarily the best social network, but because everyone was on it. The more people who use the dollar for international trade, the more valuable and essential it becomes.

Why The Dollar is Different

As Patnaik and Shah point out in their article, any attempted Mar-a-Lago Accord today would face major challenges:

First, unlike in 1985, China would need to be a key player, and they're dealing with their own economic problems.

Second, currency markets today are vastly deeper and more liquid than they were in 1985, making central bank intervention less effective.

Third, central banks globally now operate under inflation targeting frameworks that limit their ability to manipulate currencies.

And fourth, there's a question of whether there's even political will in the US for a policy that would reduce Americans' purchasing power by making imports more expensive.

The Contradiction

In his follow-up tweet, Perkins highlights an astonishing narrative whiplash: "How did we go from 'US exceptionalism' to 'is the US uninvestable?' in three months?"

This captures something important. The speed of the shift in market sentiment suggests something other than fundamental economic forces at work. As one commenter replied to Perkins, "People go 'long hysteria' quickly."

Impact on Emerging Markets

Now, let's talk about why this matters beyond Wall Street and Washington. The dollar's status directly affects countries like India and other emerging markets in profound ways.

When the dollar strengthens, emerging market debt denominated in dollars becomes more expensive to service. When it weakens rapidly, it can cause inflation through higher import costs. Dollar volatility can trigger capital flight from emerging markets as global investors retreat to safety.

As former Citicorp boss Walter Wriston once observed

"Capital goes where it is welcome and stays where it is well treated."

For emerging markets, the movement of dollar-denominated capital can mean the difference between growth and crisis.

Conclusion

So where does this leave us? The dollar is certainly facing challenges, and we're seeing capital flows shift in response to policy uncertainty. But a full collapse of the dollar's reserve status? That's a much higher bar to clear.

Remember what The Economist notes – there's simply no viable alternative. The euro lacks sufficient safe assets, Switzerland is safe but too small, Japan has its own debt problems, and cryptocurrencies lack state backing.

As Patnaik and Shah conclude, a Mar-a-Lago Summit might make for "a useful propaganda device" for Trump, but it's unlikely to fundamentally reshape the global financial system. What we should really be watching is how far the dollar retreats from its safe haven role as measured by the USD/EUR rate and long-term bond yields.

In finance, sometimes the most valuable insight is recognizing the difference between a genuine structural shift and a temporary market reaction. And that's exactly what Dario Perkins' tweet helps us do.

Powell and Rajan on Economic Uncertainty

Next, we're diving into a fascinating exchange between Federal Reserve Chair Jerome Powell and former Reserve Bank of India Governor Raghuram Rajan at the Economic Club of Chicago.

Their conversation happened against the backdrop of major policy shifts from the Trump administration, particularly around trade and tariffs, which has created waves of uncertainty in the markets.

Rajan on Structural Uncertainty

Let's start with this question from Raghuram Rajan about something he calls "structural uncertainty":

This is a fascinating question that gets at something much deeper than typical economic uncertainty. Let me break down what Rajan is really asking here.

Normally, businesses face what economists call "policy uncertainty" - like wondering if interest rates might go up or down, or if a tax credit might expire. But what Rajan is pointing to is something much more fundamental - a wholesale shift in America's economic approach.

He's suggesting that businesses aren't just uncertain about specific policies, but about the entire rules of the game. Will the U.S. remain committed to free trade? Will global supply chains continue to make sense? Will America's role in the global economy fundamentally change?

And Rajan makes a crucial point about investment: Even after tariffs stabilize, companies might still hesitate to build new facilities because they can't be sure if the policies will stick around beyond this administration.

Powell’s Response

Then came Powell’s response and it is revealing. He acknowledges the extraordinary level of uncertainty businesses are facing, citing feedback from CEOs who say they've never experienced anything like this in decades-long careers.

What's particularly notable is that Powell doesn't dismiss these concerns. Instead, he essentially confirms that this level of uncertainty - if it persists - would fundamentally change how businesses operate in America.

He says, and I think this is key:

"If the United States were to become a jurisdiction where risks are just structurally higher going forward, that would make us less attractive as a jurisdiction."

That's central banker speak for: "This could seriously damage America's position as a premier destination for investment."

U.S. Debt Sustainability

Now let's look at our second soundbite, where Powell addresses the question of U.S. debt sustainability:

This is classic Powell - honest but measured. He's making a crucial distinction between the current level of debt and its trajectory.

When Powell says the debt is "not at an unsustainable level," he's saying America isn't facing an immediate debt crisis. The U.S. can still borrow at reasonable rates, and there's no risk of default.

But by saying it's on an "unsustainable path," he's warning that we can't continue indefinitely with the current pattern of spending and revenue.

The Deeper Context

What makes Powell's comments particularly significant is that they come at a time when the U.S. is running historically large deficits during a period of full employment. Typically, countries run deficits during recessions and try to balance budgets during good economic times.

Powell points to where the real fiscal challenges lie - entitlement programs like Medicare, Medicaid, and Social Security, plus growing interest payments. He notes that these are the parts of the budget that are growing fastest, yet they're hardly addressed in political debates.

Instead, as Powell points out, "100% of the conversation" focuses on discretionary spending, which is already declining as a percentage of federal spending.

And Powell makes a crucial point about political reality: These entitlement issues "can only be touched on a bipartisan basis" - meaning neither party can solve this alone.

Connecting the Dots

These two soundbites actually connect in a fascinating way. The structural uncertainty Rajan asks about could potentially worsen America's fiscal situation. If businesses invest less due to uncertainty, economic growth could slow, making the debt burden relatively larger.

At the same time, uncertainty about America's fiscal path could itself become a source of "structural uncertainty" for businesses trying to plan for the future.

Powell's comments reveal a Fed chair navigating incredibly complex waters. He's signaling that the Fed is likely to face a challenging scenario where both unemployment and inflation rise - a situation that makes monetary policy particularly difficult since the traditional response to one problem makes the other worse.

So what's Powell's strategy? Essentially, wait and see. As he put it in his opening remarks:

"For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance."

Goldman Sachs on India as a Standalone Allocation

Now, we're diving into a fascinating investment perspective from Goldman Sachs Asset Management. Earlier this month, they published a report titled "India: Structural Strength and the Case for a Standalone Allocation." Let's dig into what they're saying and why it matters, especially as global investors navigate this period of dollar volatility we've been discussing in previous episodes.

The Goldman Thesis

Goldman's core argument is straightforward but powerful: India deserves to be treated as its own distinct investment allocation, separate from the broader "emerging markets" bucket most investors use.

"We believe India's equity market presents a compelling case for standalone asset allocation given its high growth and strong earnings potential, and subsequently, higher equity returns. India also has a large and diverse equity universe, and low correlations to other markets, heightening the appeal of a dedicated India equity allocation."

This isn't just another bullish call on India – it's a structural recommendation about how portfolios should be constructed. But what caught my attention the most is that the timing is particularly interesting.

Why Now?

Goldman is making this case after what they describe as a "correction" in Indian equities since September 2024. Despite this pullback, they're arguing that India's fundamentals remain strong, with projected earnings growth of 14% for 2025 and 15% for 2026.

In their view, this correction creates "an attractive entry point into one of the fastest growing major economies of the world."

But why exactly do they believe India deserves special treatment compared to other emerging markets?

Goldman points to several structural factors that make India unique:

First, the growth story. Now we know that this is as cliche as it gets, but, India is projected to deliver 6-7% real GDP growth over the next few years – remarkable for an economy of its size. For context, that's roughly three times the growth rate expected in most developed economies.

Second, demographics. India has the world's largest population and one of its youngest, with a median age of about 28 years – a full decade younger than the US.

Third, market dynamics. India's stock market has delivered annualized returns of 16.7% over the last five years, compared to just 8.8% for the broader MSCI Emerging Markets Index.

Fourth, diversification benefits. The Indian market has shown low correlation to both developed and other emerging markets, making it particularly valuable for portfolio construction.

And finally, market depth. With over 2,500 companies listed on the National Stock Exchange and around 5,000 on the Bombay Stock Exchange, India offers the breadth and sector diversity typically found only in developed markets.

Connecting to the Dollar Story

Now, let's connect this to our recent discussions about the dollar's volatility and potential decline. Goldman doesn't explicitly reference the dollar's troubles in their India thesis, but the timing is no coincidence.

As we've explored with Dario Perkins' tweets and The Economist's analysis, there's growing concern about the dollar's trajectory in 2025. As global investors look for alternatives, India's combination of growth, scale, and relative insulation from global trade disruptions makes it an attractive destination for capital.

Goldman specifically notes that

"… resilient external balances and low exposure to the US by way of goods exports and geopolitical neutrality may provide India with a strong economic moat against global tariff uncertainty."

In other words, India might be one of the best positioned major economies to weather the storm if the dollar situation deteriorates further.

But, there are Risks

Goldman doesn't ignore the challenges, though. They note that India isn't immune to geopolitical conflicts and their ripple effects. Prolonged tensions could impact commodity prices and disrupt trade. They also acknowledge that weather shocks could disrupt agricultural supply chains and spark food price inflation.

But the key point here is resilience. India's economy is primarily domestically driven, which provides a buffer against external shocks that few other large economies enjoy.

What this means for investors?

So what should investors take away from Goldman's perspective?

First, the traditional approach of lumping India in with broader emerging markets may no longer make sense. India's weight in the MSCI Emerging Markets Index has more than doubled from 7% a decade ago to around 17% today – and Goldman expects that share to grow.

Second, Goldman is suggesting that the optimal approach is active management focused on bottom-up stock selection, especially given the opportunities across the market cap spectrum. They highlight that small and mid-cap stocks have outpaced large caps over the past five years, offering "strong alpha potential for disciplined, on-the-ground investment teams."

Third, they point to the strength of domestic capital flows. Monthly inflows through systematic investment plans (SIPs) – India's version of automatic investment plans – now top $3 billion monthly. This growing domestic investor base provides a cushion during periods of foreign investor outflows.

Conclusion

So where does this leave us? Goldman's case for India as a standalone allocation isn't just about chasing high returns in an emerging market. It's about recognizing structural shifts in the global economy and adapting investment approaches accordingly.

As they put it:

"While India's economy and equity market has faced a soft patch recently, we believe it's important to put cyclical speedbumps and structural tailwinds into context."

In many ways, this parallels what Dario Perkins was saying about the dollar – distinguishing between cyclical shifts and structural changes is crucial for navigating today's complex investment landscape.

For investors concerned about dollar volatility and looking for growth opportunities with some insulation from US economic troubles, Goldman's India thesis offers a compelling alternative. Whether you agree with their specific allocation recommendation or not, their analysis highlights how the tectonic plates of global finance are shifting beneath our feet.

Manish Chokhani on India being kept out of global supply chains

Finally, we're diving into a fascinating debate sparked by a comment from Manish Chokhani, Director at Enam Holdings, during his recent interview with CNBC TV18. The statement that's got everyone talking?

"India was kept out of the global supply chain for decades. This Trump-led global reset may finally bring us in."

This claim has kicked off quite a discussion, with some prominent voices strongly disagreeing. Let's dig into the perspectives and see what's really going on here.

Chokhani’s Perspective

During his interview on CNBC's "Market Masters," Chokhani painted a picture of India being deliberately sidelined in the global economic chess game. He argued that India was "completely sidelined" on the global chess board - not in the UN Security Council, not allowed to properly integrate into the WTO, and even seeing countries around us like Bangladesh and Pakistan sometimes performing better in sectors like textiles.

According to Chokhani, the rules of the game were "laid out in a manner to keep India held back." He sees the current Trump-led trade reordering as a potential opportunity for India to finally become integrated into global supply chains, especially as the US seeks alternatives to China.

Chokhani pointed to encouraging signs, noting that US Commerce Secretary Bela Beset has mentioned India among the first four countries (along with UK, Japan, and Korea) the US wants to sign trade deals with. He described this potential realignment as possibly "the most bullish thing" for India's economic future.

In Chokhani's view, being part of these global supply chains is crucial for India to break through its manufacturing ceiling of 14-15% of GDP (versus its aspiration of 24%) and to create the kind of catalyst that helped countries like China and Southeast Asian nations develop their economies through export-led growth.

The Counter Perspective

But not everyone agrees with this assessment. Amit Kumar Gupta (@amitgupta0310) offered a direct rebuttal on social media:

"India was not kept out of any global supply chain. India joined WTO in 1995 much before China. We choose to concentrate on services business, primarily IT services over manufacturing."

Gupta further pointed out that even recent efforts haven't yielded the desired results:

"Even now, post Covid when the focus has shifted slightly to manufacturing by the incumbent government...except semiconductors/i-phone assembly, none of the PLI schemes have borne fruits. This is despite corporate tax cuts in 2019. Private capex is lying shattered on the ground and there are huge ifs and buts how it will actually unfold over next decade."

This represents a fundamentally different view - that India wasn't excluded but rather made its own strategic choices to focus on services rather than manufacturing. In this perspective, the current challenges aren't about breaking into supply chains but about addressing internal issues that have limited private investment in manufacturing.

Other Expert Views

The experts on the CNBC panel also raised some important points about India's approach to global trade. They discussed India's non-tariff barriers and relatively high tariff regime, which have often been criticized by trading partners.

One of the panelists pointed to the stark economic reality: the US is an $80,000 per capita economy while India is at about $3,000 per capita. This massive gap limits how much American goods could realistically enter and compete in the Indian market, regardless of tariff levels.

There was also discussion about India's hesitancy to join regional trade agreements like RCEP, with Chokhani defending this decision by suggesting that joining would have primarily benefited imports from the east into India, without necessarily helping Indian exports to the west.

The Bigger Picture

What's particularly interesting in this debate is how it reflects two competing narratives about India's economic journey:

The "external barriers" narrative: India was deliberately kept out of global supply chains by a system designed to benefit certain countries at the expense of others.

The "internal choices" narrative: India made strategic decisions to focus on services, and current manufacturing challenges stem from domestic policy issues rather than external exclusion.

Looking at neighboring countries provides some interesting context. Vietnam, with a GDP per capita around $4,000, has become a manufacturing powerhouse, attracting significant investment from companies looking to diversify beyond China. Bangladesh, with a GDP per capita of only about $2,500, has built a massive garment industry that outperforms India's in many markets.

Then there's the case of Mexico, which leveraged its proximity to the US and NAFTA (now USMCA) to build integrated supply chains with its northern neighbor, becoming a major manufacturing hub.

The Question For You

So here's what I want to ask you, our viewers: What do you think? Has India been systematically held back from global supply chains as Chokhani suggests? Or did India simply make different strategic choices than countries like Vietnam, Mexico, or even Bangladesh?

Did these other countries do something fundamentally different to attract global manufacturing that created millions of jobs? Or is Chokhani right that the current trade realignment represents a unique historical opportunity that wasn't available before?

Let me know your thoughts in the comments. And if you've worked in manufacturing, trade policy, or related fields, I'd be especially interested in hearing your perspective based on your experience.

That's it for today's "Who Said What." Remember to like and share, and let me know in the comments which economic debates you'd like me to break down next time. See you soon!

The daily brief is nice. Our substack is nicer, for hardcore investor types.