Hey everyone, welcome to another episode of Who Said What! This is the show where we take interesting comments, headlines, and quotes that caught our attention and dig into the stories behind them. You know how every week, there’s a bunch of headlines that grab everyone’s attention, and there’s so much hype around them? Well, in all that chaos, the nuance—the real story—often gets lost. So that’s the idea: to break things down.

Today, we have six very interesting comments from last week.

We have entered a bear market

Ishmohit from SOIC, who’s one of the sane voices in the investing space, recently shared his thoughts on how to invest in a bear market.

The market has been on shaky ground lately, with Indian indices down about 13% from recent peaks. While that’s not quite the classic definition of a bear market—usually a 20% drop from the top—it’s still painful.

More importantly, many smaller stocks are already feeling a deeper pinch. According to Ishmohit, roughly 60% of small- and mid-cap stocks have fallen by over 30%, indicating we might be past a mere pullback.

Adding weight to this view is a technical indicator called “VStop,” which has turned negative on both weekly and monthly charts for the first time since the 2020 COVID crash. You don’t need to be an expert on technicals to sense the implication: The market could be entering a sustained downtrend instead of a momentary dip.

Price Correction vs. Time Correction

Ishmohit breaks down weak markets into two distinct phases.

Price Correction This is the quick, sharp drop—like the 13% fall in the major indices or the more dramatic 30% plunge in many smaller stocks. It tends to happen suddenly and can be shocking, but at least it’s over relatively fast.

Time Correction Once prices have tumbled, the market may stop crashing yet fail to stage a meaningful recovery. This sideways drift can last for 6–12 months, leaving investors frustrated and fatigued. For those who started investing after 2020—when markets rebounded almost in a straight line—this can feel especially draining.

Three Ways to Handle a Bear Market

1. Short-Term Traders

If you’re the type who trades frequently, Ishmohit advises holding more cash. Short-term rallies in a bear market can be traps—temporary bounces that lure buyers before prices slide again. Staying liquid can help you avoid getting caught at these false peaks.

2. Medium-Term Investors (1–2 years)

If you typically hold stocks for a year or two, consider buying in small increments during dips rather than putting all your money in at once. This way, if the market drops further, you still have cash left to deploy at even lower levels. Also, take a hard look at your existing stocks. If you’re stuck with “broken” names that have weak fundamentals—those that soared when optimism was high but don’t actually earn much—consider switching to sturdier picks. It might hurt to sell at a loss, but doing so could spare you from a worse loss later.

3. Long-Term Investors (3+ years)

For investors with a multi-year horizon, a bear market can be an opportunity. Think of it as downtime to “repair your nets”—meaning you focus on studying companies, refining your watchlist, and being patient. There’s no rush to invest everything immediately; instead, wait for quality businesses to become reasonably priced. Bear markets don’t last forever, and when they do turn, being positioned in solid stocks can be very rewarding.

Beware Overpriced Stocks

While frothy valuations (80–100 times earnings) were commonplace in the euphoric phases of 2020 and 2021, they can be dangerous now. As the market mood shifts, investors question whether such high valuations are justified. This skepticism often results in harsher price drops for stocks that were banking on “perfect” future growth.

Old Winners Might Not Lead Again

Even if the market eventually recovers, the stars of the last bull run—like certain chemical, pharma, or tech stocks—may not be the leaders next time. Market leadership rotates, so it’s worth keeping an open mind and not clinging to yesterday’s success stories.

Ishmohit’s central message is that the market’s tone has changed. While we may not see a dramatic, continued crash, the shift to a “time correction” could seriously test investors’ patience.

Warren Buffett on holding cash

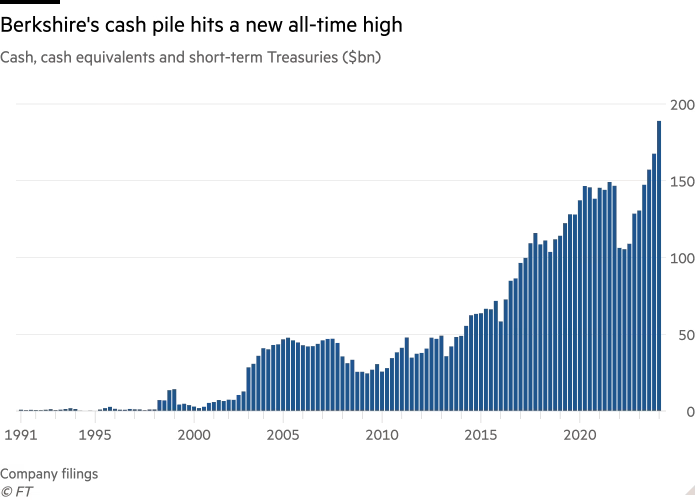

Warren Buffett’s latest annual letter touched on several fascinating—and in some ways provocative—points about Berkshire Hathaway, its approach to capital, and its role as a major taxpayer and investor in the U.S. economy. Though Buffett’s prose is typically straightforward, there’s a lot behind those lines that deserve deeper exploration.

One of the most striking pieces of information comes from his discussion of Berkshire’s tax payments.

This single sentence reveals how large Berkshire’s contribution to federal corporate tax revenue has become. Essentially, one company—that too a conglomerate of many businesses—accounts for a significant share of all U.S. corporate taxes. The deeper reason behind this outsized figure is Berkshire’s strategy of continually reinvesting its profits. Instead of sending most earnings back to shareholders through dividends, Berkshire channels that cash into existing subsidiaries or new acquisitions, aiming for growth that eventually boosts taxable income. Over time, those reinvestments become larger engines of profit and, in turn, higher tax obligations.

At its heart, this is a reminder that no matter how profitable a company might look in numerical terms, those figures will mean little if the buying power of the dollar collapses. Inflation erodes the real value of money; if the government spends or prints recklessly, businesses and citizens can lose wealth without a single transaction taking place, simply because each dollar purchases less. Buffett’s concern is that without careful management of national finances and monetary policy, the United States could find itself in a situation where the currency’s value is undercut, jeopardizing the stable economic environment on which Berkshire—and, indeed, most companies—depend.

Put another way, it might seem that Berkshire is just sitting on enormous piles of money, but that’s not where most of its value lies. The bulk of Berkshire’s assets are in businesses—whether wholly owned, such as its insurance or railroad operations, or in the form of large stakes in publicly traded giants. Around $272 billion remains invested in equities, and there is an undisclosed amount in subsidiaries not listed on the stock exchange

The cash, much of which is parked in short-term Treasury bills, is strategically held for flexibility. Buffett has often compared cash to oxygen: you hardly notice it when you have plenty, but if you’re running low, you might face a crisis. This approach allows Berkshire to act quickly when the market takes a downturn or a great business comes up for sale.

Having significant cash available at the right moment gives Berkshire a competitive edge, but it doesn’t mean the firm has lost faith in owning productive assets; it just means it’s prepared for unforeseen opportunities.

Here, he expresses gratitude for the conditions that have enabled Berkshire’s success—principally a strong legal and financial framework that fosters long-term investment and innovation. At the same time, he offers a clear warning that failing to safeguard the dollar’s value would undermine the prosperity that companies like Berkshire have enjoyed. From Buffett’s perspective, America’s capitalist system, despite its flaws, offers remarkable opportunities, but it is not immune to the risk of fiscal mismanagement.

If inflation surges or public debt becomes unsustainable, those opportunities can shrink dramatically.

All of these observations fit together in a broader narrative about responsibility—both corporate and governmental. Berkshire pays large sums in taxes because it continues to reinvest and grow, thereby generating ever-increasing taxable income. The government, in turn, collects those taxes and has a duty to manage them wisely.

That management includes exercising caution with spending and monetary policy so the purchasing power of the dollar remains stable. For those new to markets, Buffett’s letter is a reminder that healthy economic systems depend on cooperation between the private sector’s growth-focused ambitions and the public sector’s stewardship of the currency and broader fiscal environment. Only when both sides play their part—businesses reinvesting and governments acting prudently—can long-term prosperity be sustained for everyone involved

China vs the world

Noah Smith, who’s well-known economics commentator, recently published a piece titled “Manufacturing is a War Now,” which argues that manufacturing capability has become a central pillar of geopolitical power. Specifically, he warns that China has achieved dominance in many sectors—from batteries to drones—and that this edge isn’t just an economic advantage; it could also become a military advantage.

Let’s start with the main point of Smith’s argument: China’s manufacturing supremacy didn’t happen by accident. According to Smith, this is the result of decades of strategic industrial policy dating back to the early 2000s. Beijing identified electric vehicles (EVs) and battery technology as national priorities as far back as its 2001 Five Year Plan. Fast forward to today, and China now leads in the production of batteries, drones, electronics, and a wide range of other sectors that have obvious military implications.

He notes that manufacturing capability directly translates into military capability. He highlights the war in Ukraine as an example: stockpiles were quickly depleted, and the fight turned into a race to produce more munitions and equipment faster. When it comes to large-scale or prolonged conflicts, the country that can build more weapons and supplies at the fastest rate usually has the upper hand.

The Disturbing Data

What makes Smith’s piece especially troubling is the data he lays out:

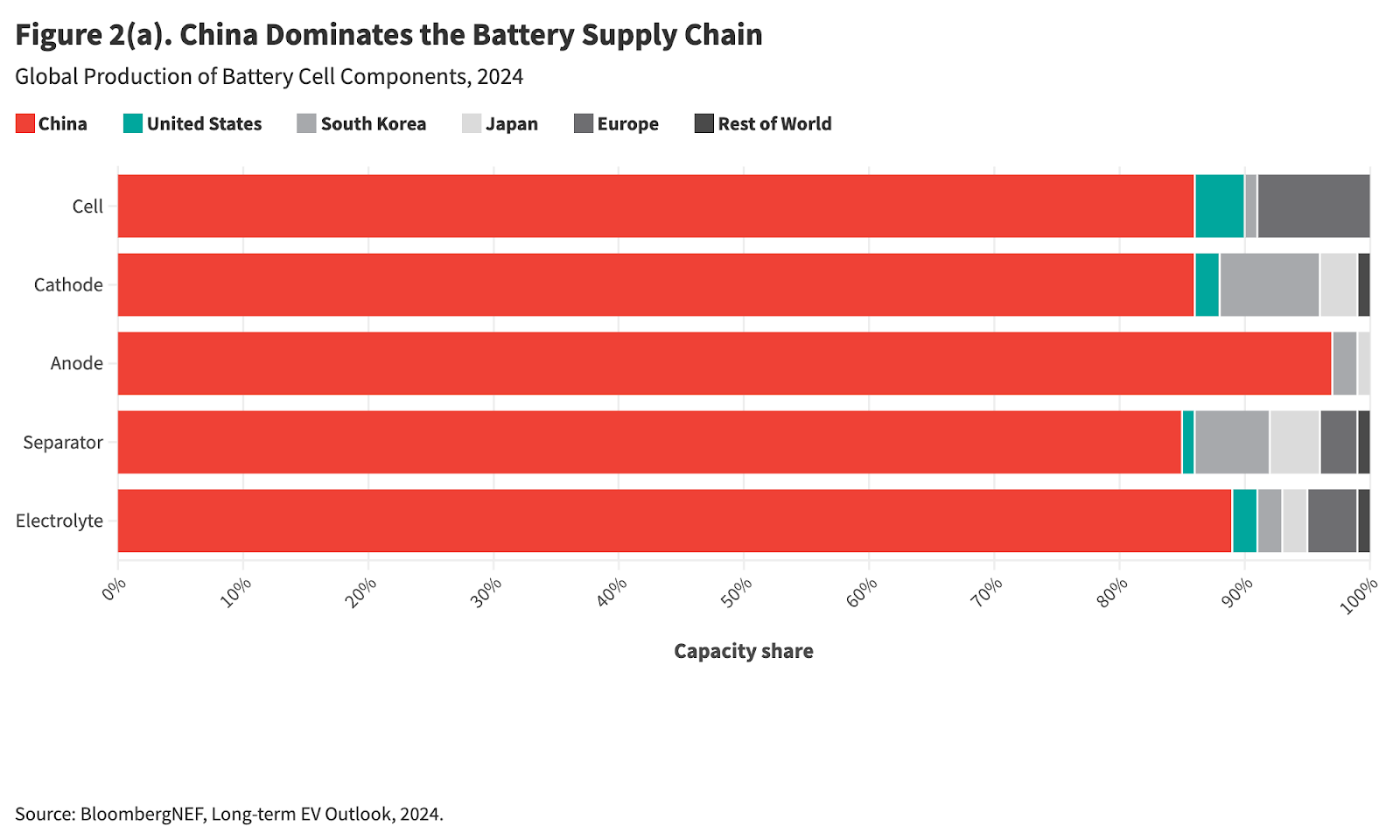

70-90% of global production across multiple battery supply chain stages is now in China’s hands.

According to UNIDO data, China might reach 45% of global manufacturing by 2030. That level of dominance has only been matched twice: once by Britain at the dawn of the Industrial Revolution, and once by the United States after World War II.

Smith’s essay pairs perfectly with a Carnegie paper that narrows its focus on the battery race. While it confirms that China dominates current lithium-ion battery technology at every step—from mineral extraction to final assembly—the Carnegie authors also say there’s still hope for the United States.

Their argument?

The U.S. can leapfrog by going all-in on next-generation solid-state batteries with lithium-metal anodes. These batteries promise dramatic improvements in safety, energy density, and charging speed and could power everything from thousand-mile-range EVs to advanced military technologies (think uncrewed submarines).

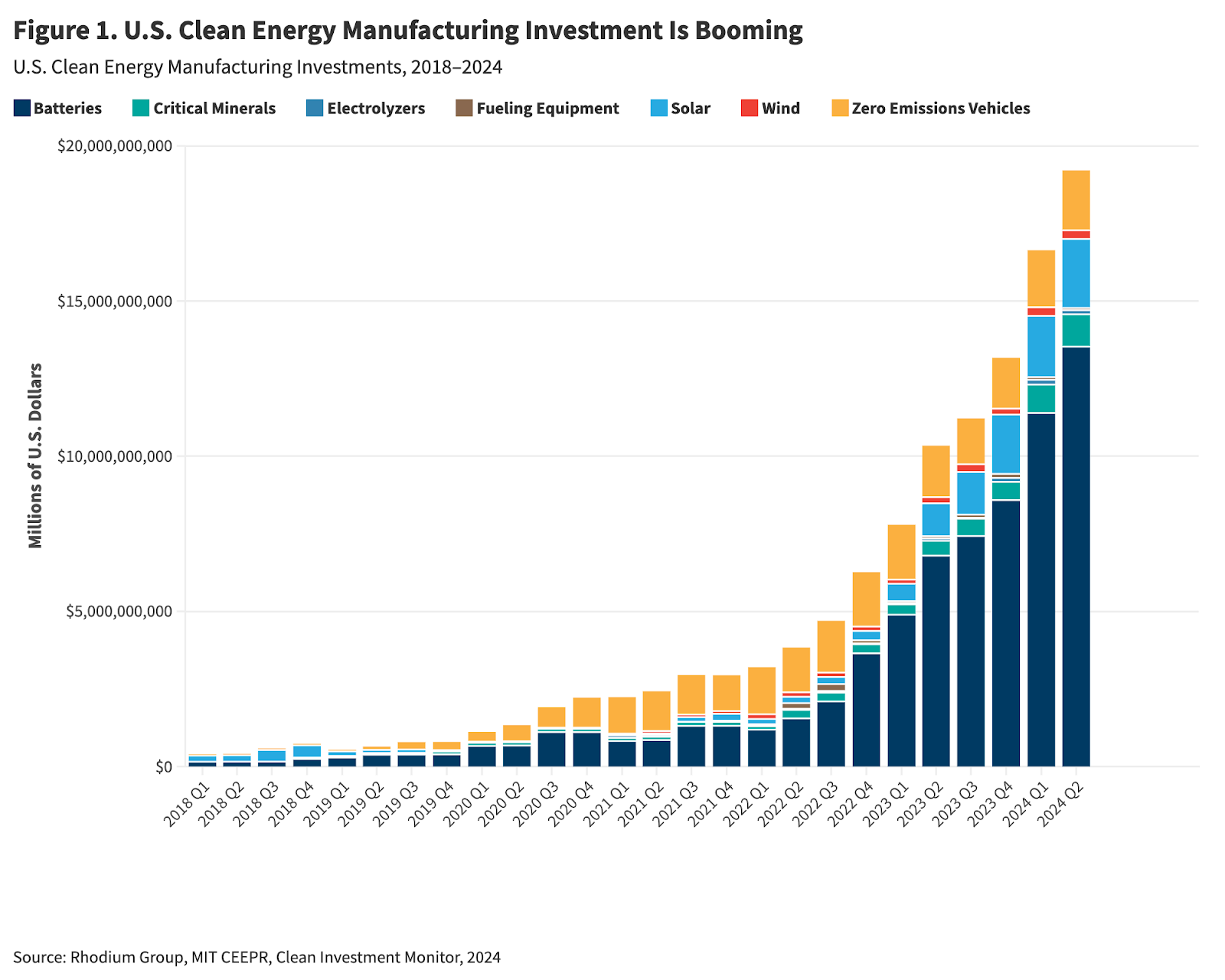

However, the authors warn that right now, the U.S. is investing almost entirely in current-generation lithium-ion tech—over 90% of a recent $40.9 billion manufacturing investment is going to tech we’re already behind on.

To change course, they suggest:

Boosting R&D funding, noting that China has taken the lead in battery research publications.

Introducing targeted financial incentives to encourage scaling up these next-gen batteries.

Creating protected initial markets through government procurement—so that new U.S. companies can build momentum without being crushed by cheaper Chinese manufacturing.

Enemy or Rival?

One aspect of Smith’s piece that makes me uneasy is the way he frames China as an “enemy” rather than a “rival.” This is where Harvard political scientist Graham Allison comes in. Allison wrote about the “Thucydides Trap,” referring to the historical pattern where a rising power threatens to displace an established one—and in many cases, that leads to war. Out of 16 such power transitions over the past 500 years, 12 ended in conflict.

Examples include the tension between Britain and Germany before World War I, where economic and naval competition escalated into open warfare, and the ancient Greek rivalry between Athens and Sparta (the original scenario Thucydides wrote about). Peaceful transitions—like when the U.S. replaced Britain as the leading power in the early 20th century—usually happened between nations sharing closer cultural and political ties.

The Risk of Escalation

So, while Smith’s military metaphors (“manufacturing doesn’t just support war—in a very real way, it’s a war in and of itself”) underline the urgency, they might also push us toward a dangerous mindset. If both sides feel they’re in an unavoidable conflict, it could become a self-fulfilling prophecy. Competition is clearly real, and China’s industrial policy does aim at dominance, but how we define that competition—enemy versus rival—matters.

Let me know your thoughts: Is China inevitably an “enemy” in the manufacturing race, or is there still room for peaceful competition?

China does something and the world pays

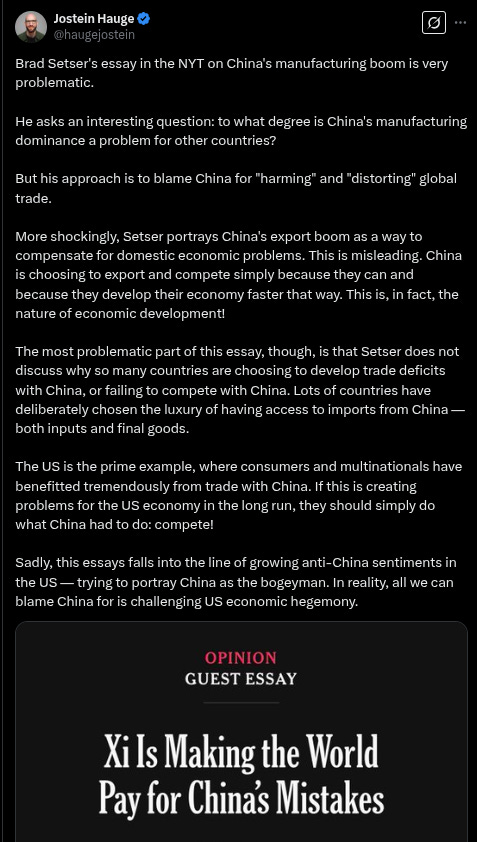

Brad Setser, a senior fellow at the Council on Foreign Relations, is one of the go-to people to learn about what’s happening with China. His recent New York Times op-ed,"Xi Is Making the World Pay for China's Mistakes" sparked an interesting debate about China's manufacturing dominance and trade imbalances.

This also connects nicely with points raised by Noah Smith about manufacturing competition that we just spoke about.

Brad makes a striking claim: China has fundamentally distorted global trade through policies that create a heavily one-sided relationship. He backs this up with eye-opening data:

Over the past six years, China’s manufactured exports have grown more than 10 times faster than its imports.

China now dominates global production across multiple sectors:

Has the capacity to produce two-thirds of the world’s cars.

And controlling solar cell and battery production.

He argues that this dominance isn’t accidental. After the 2008 financial crisis, instead of boosting consumer spending, China funneled savings into infrastructure and property, leading to a massive real estate bubble. Then, when Xi Jinping cracked down on the housing sector in 2020, China compensated by ramping up its manufacturing capacity and exports. In Setser’s words, that’s “making the world pay for China’s mistakes”—essentially exporting the consequences of its own economic mismanagement.

His main objection? Labeling China as “harming” global trade might be off the mark. Jostein sees China’s export strategy as a standard path to development—one that many successful economies have taken throughout history.

Hauge also points out that countries like the U.S. chose to run trade deficits with China. It’s not as though this was forced upon them; American consumers and multinationals, in many ways, benefited from cheaper goods and expanded supply chains. So, Hauge’s message to the U.S.? If you don’t like these deficits, then simply compete rather than casting China as a villain.

Setser’s Macroeconomic Response

Brad responded to this. He highlighted several macroeconomic points that support his argument:

China’s 45% savings rate is extremely high compared to other countries.

Such high savings can fuel either domestic bubbles (like China’s property market) or global imbalances in trade.

One country’s surplus necessitates another country’s deficit—not everyone can compete if someone else is controlling such a huge slice of the pie.

Some Asian economies (e.g., Taiwan) have remained competitive by intervening in currency markets and limiting social spending, but that only shifts the problem somewhere else.

The U.S. has accommodated China’s surplus through fiscal deficits, but that comes at a cost for the U.S. economy.

China’s growing surplus is crowding out other economies, so it’s not just a matter of the U.S. refusing to “keep up.”

Hauge did acknowledge some of these macro points, but he continued to emphasize that China’s economic development is largely a success story—one that benefits many countries. He wondered if Setser’s real issue is wanting to preserve U.S. dominance rather than moving toward a world with shared power and prosperity.

Why This Debate Matters

So why is this important? Well, it ties into Noah Smith’s commentary on manufacturing competition—where he argues we should see industrial competition almost like warfare—and also links to the Carnegie report that highlights the strategic importance of battery technology. All three sources are wrestling with the same broad concern: China’s rapid expansion in manufacturing could pose both economic and security challenges for other nations.

But they don’t all point the finger in the same direction or suggest the same fixes:

Noah Smith talks about using industrial policy and creating common markets to counter China’s rise.

The Carnegie report suggests focusing on next-generation technology—like advanced batteries—to leapfrog and stay ahead.

Meanwhile, Setser and Hauge are debating the structure of the global trading system, questioning whether China’s approach is an unfair distortion or just a classic development strategy.

The Bigger Picture

In the end, their disagreement reflects two competing views on international economics:

View One: China’s state-led industrial policy distorts fair market competition, and the global trading system should step in.

View Two: China is simply following a well-worn path that many successful economies have used, and it’s challenging the assumption that Western economic power should remain unchallenged.

Do not catch the falling knife

Vinay Paharia, the CIO of PGIM mutual fund, posted something very interesting on his LinkedIn, talking about something that affects almost every investor—behavioral biases.

Vinay has drawn attention to an eye-opening pattern among retail investors. He found that over a ten-year period, individual investors more than doubled their stake in the worst 25% of companies—going from a 9% share to almost 20%. In stark contrast, their holdings in the best 25% of companies stayed flat at around 12–13%.

Now, here’s the kicker: those “best” companies generated an average return of 34% over the same decade, while the “worst” companies actually lost money, averaging a -4% return. So the very stocks retail investors kept buying more of did significantly worse over time, and the ones they barely touched went on to do remarkably well.

Vinay points out that multiple classic behavioral biases could be causing this:

Anchoring Bias – Investors like you and me often fixate on a stock’s previous high or their initial purchase price. When the price drops, they treat it as a bargain, regardless of whether the fundamentals support that notion.

Value Illusion – This is basically “catching a falling knife.” Investors see a steep price drop and mistake that drop for actual value, even if nothing else justifies it.

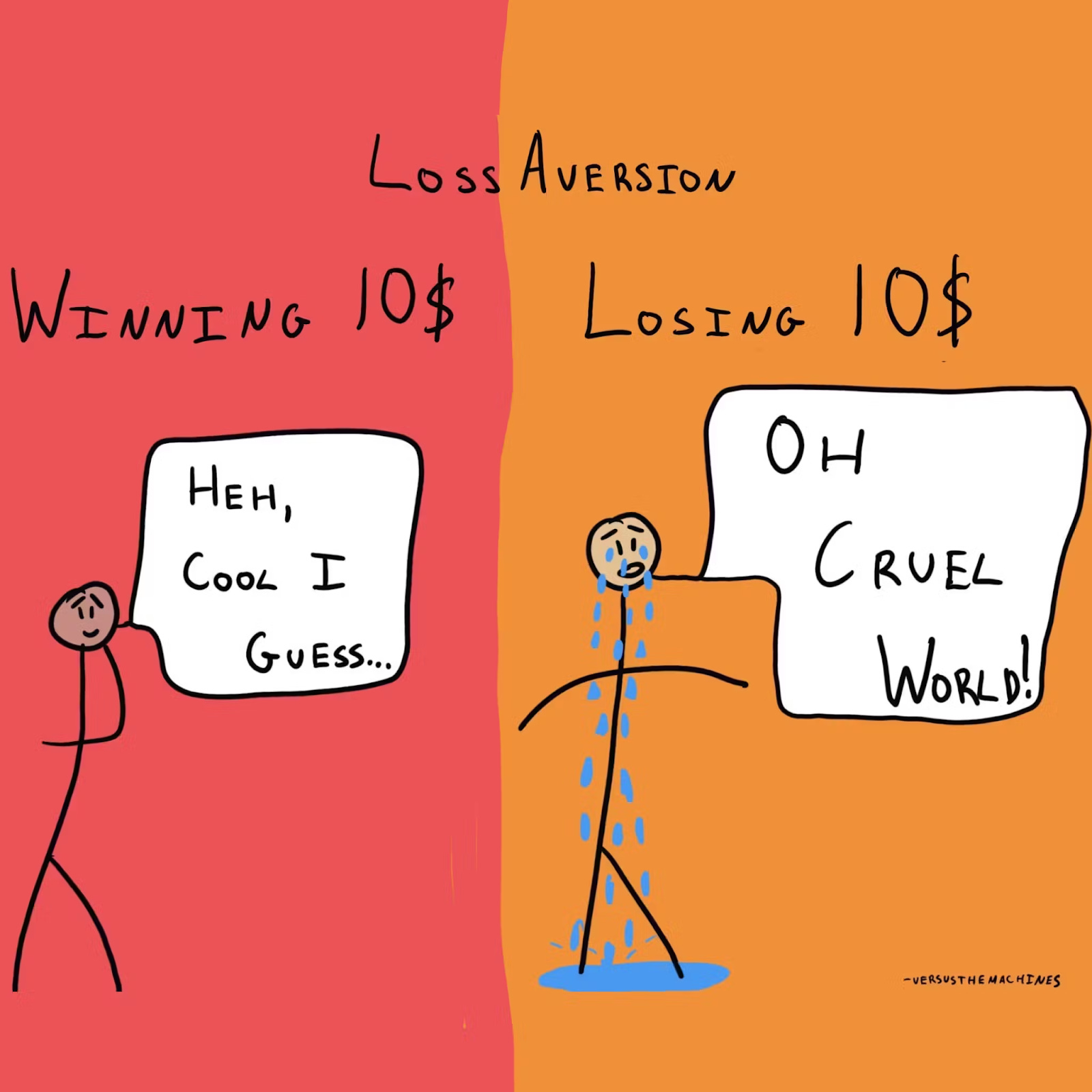

Loss Aversion – From Kahneman and Tversky’s prospect theory: We all hate losses more than we like gains of the same amount. It makes people cling to losing stocks longer to avoid “locking in” a loss.

Recency Bias – Placing too much weight on recent price movements and expecting them to reverse quickly, even if the broader trend or fundamentals suggest otherwise.

Confirmation Bias – People hunt for evidence that supports the belief that a fallen stock is bound to bounce back, ignoring any signs that it might not.

All these biases combine into a dangerous feedback loop. Retail investors see a stock tank, consider it “cheap,” buy more, and stay stuck in underperforming companies. Meanwhile, they miss out on the winners because they’re too anchored to the old price references to build up bigger positions there.

Vinay’s warning is crystal clear: Beware of the Anchoring Bias. Do not catch the falling knife. And he’s not just offering anecdotal advice—his insights are backed by extensive academic research. Studies by Barber and Odean and their work on the “disposition effect,” plus research specific to the Indian market, all show that retail investors often make decisions based on these reference points instead of genuine fundamental value.

So, that’s the story. Even though the idea of “buying low” is attractive, it can turn into a painful trap when we let our biases, rather than solid research and fundamentals, guide our decisions.

OpenAI's GPT-4.5 Launch Intensifies Global Chip Battle

Now, we will take a close look at a big moment in artificial intelligence: the launch of OpenAI’s new GPT-4.5. But before that, here is some quick context.

A Computing Crisis

Let’s start with NVIDIA CEO Jensen Huang, who recently issued a strong warning about AI’s insatiable appetite for computing power. In a recent interview, he noted:

“The amount of computation necessary to do that reasoning process is a hundred times more than what we used to do.”

He’s talking about how modern AI models effectively “think to themselves” before giving you an answer, and this has led to a massive spike in the need for computational resources. That warning seems spot-on because just now, OpenAI launched GPT-4.5, confirming that AI’s computing requirements are truly exploding.

Sam Altman Confirms the Strain

OpenAI’s CEO, Sam Altman, made a candid admission on February 28 when announcing GPT-4.5:

“Bad news: it is a giant, expensive model. We really wanted to launch it to plus and pro at the same time, but we’ve been growing a lot and are out of GPUs. We will add tens of thousands of GPUs next week and roll it out to the plus tier then.”

So right away, we see how these skyrocketing demands for computing power have real-world impacts: even OpenAI doesn’t have enough GPUs right now to roll out GPT-4.5 to everyone at once.

OpenAI’s official announcement for GPT-4.5 also points out this is no minor upgrade. It’s a huge leap in “unsupervised learning,” making it much more compute-intensive than previous models:

“GPT-4.5 is a very large and compute-intensive model, making it more expensive than and not a replacement for GPT-4. We are still unsure if we’ll continue offering it long-term through our API due to its resource demands.”

This admission raises a big question for the entire AI field: How do you handle a technology so powerful—and so expensive—that it strains even the largest tech infrastructures?

Collision with Export Restrictions

Just as these new AI models are demanding more computing firepower than ever, we’re also seeing new export controls that could limit chip availability. Enter Brad Smith, Microsoft’s President. He warns that Biden administration export restrictions on AI chips might end up hurting American technological leadership more than helping it.

These restrictions are undermining one of the essential requirements needed for a business to succeed—namely, confidence by our customers that they will be able to buy from us the AI computing capacity that they will need in the future.

Smith worries that if U.S. companies can’t freely supply allies with advanced chips, those nations might turn to Chinese chipmakers—an outcome he calls “a gift to China’s rapidly expanding AI sector.”

Cascading Implications

So, if Altman and Huang are both right about AI demanding ever more computation, there are several big consequences on the horizon:

Energy Consumption Challenges: If AI computing demands keep skyrocketing, who has enough power to run all these machines? It could create a competitive advantage for countries with robust and affordable energy grids.

Supply Chain Pressures: Building data centers isn’t just about chips. Brad Smith points out that it also means manufacturing advanced electrical generators—sometimes in places like Lafayette, Indiana—and shipping them to Poland or other locations worldwide.

GPU Shortages: Sam Altman’s admission that OpenAI is literally “out of GPUs” underscores the crunch. As more companies roll out advanced AI models, everyone will be scrambling for limited hardware.

Policy Implications

With national security concerns on one side and the race to build cutting-edge AI on the other, policymakers are stuck in a tricky balancing act. Smith proposes a middle-ground approach: keep strict standards on what types of chips can be exported (so they don’t fall into unfriendly hands), but remove quantity limits that hamper economic growth and worldwide AI development.

The key takeaway is this: Advanced AI models like GPT-4.5 demand so much computing power that restricting chip exports could slow AI progress everywhere outside the countries that manufacture the most sophisticated chips. That includes some of America’s closest allies—places the U.S. normally wants to collaborate with on technology.

It's a new side project we started, and it's starting to become fascinating in a weird and wonderful way. We write about whatever fascinates us on a given day that doesn't make it into the Daily Brief.

So far, we've written about a whole range of odd, weird, and fascinating topics, ranging from India's state capacity, bathroom singing, protein, Russian Gulags, and economic development to whether AI will kill us all. Please do check it out; you'll find some of the most oddly fascinating rabbit holes to go down.

Please let us know what you think of this episode 🙂

Excellent curation and articulation of the prevailing topics. However, it would be even more valuable to explore related subjects for each, providing detailed explanations in sections to ensure a broader and deeper understanding.

Great article! Long but insightful. Keep writing.

Excellent curation and articulation of the prevailing topics. However, it would be even more valuable to explore related subjects for each, providing detailed explanations in sections to ensure a broader and deeper understanding.